Leaderboard

Popular Content

Showing content with the highest reputation since 05/07/2023 in all areas

-

This is one of my favorite things to rant about so let me apologize in advance. This isn't a comment about Brett Horn in particular - I don't know him, and maybe he's great. But what I strongly recommend is to look to the broker analysts as a gauge of popular sentiment (if even that) or to understand how brokers drum up business. Nothing more. It is not a coincidence that companies reliant on capital raising tend to get the widest coverage and the best ratings. But since the ostensible separation of research from investment banking (and the removal of skin in the game - analysts ability to actually buy stocks in their coverage universe - in the name of removing conflicts of interest), the job is basically a glorified sales job for trading volumes. And many of them, if they do get a real nugget of information or have an actual insight, share it behind closed doors with whichever client trades the most through their bank. In other words... I wouldn't think that hard about it. The analyst incentive is to not stand out in a bad way and keep making ~$1-2mm/year to keep their kids in fancy schools. Even if one is actually bearish, he/she almost certainly won't stick his/her neck out and risk embarrassment and losing that cushy gig. Sorry, I've done that job as a bright eyed and bushy tailed junior analyst and unfortunately saw how the sausage is made, so maybe I'm too cynical now. Maybe the general takeaway is to keep your expectations low and allow yourself be pleasantly surprised, but the clear and simple fact is that @Viking and others with real insight and skin in the game do a 10x better job than any broker analyst. Maybe this wasn't the case in Lee Cooperman's days at GS (though it was probably even sketchier then) but it is now. At the bare minimum, the pay and prestige aren't what they used to be. The real talent is elsewhere. Expect the sell side estimates to keep climbing higher as Fairfax executes.2 points

-

Depends on how short, but in general are a better inflation hedge than most other assets. The best immediate inflation hedge is oil. But oil is also exposed to idiosyncratic risks like cratering demand if the economy is also weakening (and politics!). So a basket that is heavily skewed to oil, some to gold, and some short-term fixed income should be a reasonably good hedge against inflation. Oil is immune to interest rates, but not immune to the economy. Gold/short term bonds are largely immune to the economy, but not real rates. As a basket, they should diversify the idiosyncratic risks of real rates, nominal rates, and the economy while hedging inflation. Future implications of deficit spending? More volatile inflation going forward.1 point

-

https://east72.com.au/wp-content/uploads/2024/04/E72DT-Quarterly-Report-March-2024.pdf

1 point

1 point -

Updated April 8, 2024: Chapter 1 (overview of Fairfax) and Chapter 4 (float) have been updated. Updated versions of both the PDF file and Excel workbook are attached below. For members who enjoy reading my posts on Fairfax I have attached at the bottom of this post two documents: 1.) Fairfax - Hiding in Plain Sight: PDF file contains about 80 of my best posts on Fairfax, organized into 16 chapters (now +350 pages long). 2.) Excel workbook: companion document to the PDF file, contains 11 worksheets (see below for details). Sanjeev, thanks for everything you do running this board. For all the members on this investing forum, ‘thank you’ for breaking bread on a daily basis and sharing your thoughts on investing and life. Over the years, it has been a life changing experience for me and my family. What is contained in this document is the collective wisdom of this group. Let’s hope i have captured it reasonably well. I always appreciate getting some feedback… maybe one or two things you like and one or two things you don’t. What is missing? Thank you. A message from the legal department: Both documents are incomplete and contain errors. What is contained in the attached documents is not intended to be investing/financial advice. Its purpose is to educate and entertain. Have a great 2024! Viking ----------- The Excel file contains 11 worksheets: 1.) FFH-23: lists and tracks many of Fairfax's equity holdings in real time 2.) Size: ranking of Fairfax's equity holdings by size 3.) Moves: detailed compilation of many on Fairfax's transitions going back to 2010 - organized by year 4.) 23 Earn Est: detailed 2023 earnings estimate 5.) Premiums: the build for 'underwriting profit' 6.) Interest: the build for 'interest and dividend income' 7.) Associates: the build for 'share of profit of associates' 8.) Investments: the build for return on the total investment portfolio 9.) Shares: reviews 'effective shares outstanding' 10.) Float: the build for float 11.) 13yr View: A 13 year view of many key metrics for Fairfax 12.) Effects of discounting and risk adjustment - IFRS 17: quarterly summary of build Fairfax Apr 8 2024.pdf Fairfax Apr 8 2024.xlsx1 point

-

@Luca I like all three investments. See below for comments. 1.) BDT has been an outstanding long term investment for Fairfax. “We continue to invest with Byron Trott through various BDT Capital Funds. Since 2009, we have invested $978 million, have received $979 million in distributions and still have investments with a year-end market value of $683 million. Byron and his team have generated fantastic long-term returns for Fairfax, and we very much look forward to our continued partnership.” 2.) ShawKwei looks like it has been a solid long term performer. The fact Fairfax is adding new capital suggests they like the prospects. “Since 2008 we have invested with founder Kyle Shaw and his private equity firm ShawKwei & Partners. ShawKwei takes significant stakes in middle-market industrial, manufacturing and service companies across Asia, partnering with management to improve their businesses. We have invested $536 million in two funds (with a commitment to invest an additional $64 million), have received cash distributions of $217 million and have a remaining value of $504 million at year-end. The returns to date are primarily from our investment in the 2010 vintage fund, which, though decreasing 8.8% in value in 2023, has generated a 12% compound annual return since 2010. The 2017 vintage fund, which has drawn about 84% of committed capital to date, increased 23.1% in value in 2023 but has a compound annual return of 3.5% since inception. We expect Kyle to make higher returns on monetization of his major assets.” 2.) Grivalia Properties gets an incomplete from me today. It is a bet on the jockey play. George Chryssikos has had the Midas touch for Fairfax in Greece - making them +$1 billion so far. I am inclined to give Fairfax the benefit of the doubt on this one - my guess is it works out ok. We should know much more in 2024 as more resorts come on line. “Grivalia Hospitality, under George Chryssikos, had a strong year of execution as two assets, including its largest, opened for business. The One & Only resort in Athens is a flagship in ultra-luxury hospitality and we are the proud owners. If you haven’t booked your summer vacation yet – you know what to do! 2024 will see one additional asset come into operation – which will take the operating portfolio to five. These include Amanzoe in Porto Heli, ON Residence in Thessaloniki, Avant Mar in Paros, One & Only and 91 Athens Riviera in Athens. Focus now turns to operational and service excellence for these resorts with Greece forecast to receive a record number of tourists in 2024. George has another five high end hotels in development over the next few years. George has an outstanding track record in real estate and as I said last year, he has already made us $1 billion! We expect George to repeat that accomplishment with Grivalia Hospitality over time! At year end we carried Grivalia at €513 million for our 85% stake.”1 point

-

I think Fairfax will take FIH private. If they took their performance fee in shares, FIH would have to issue those shares increasing the float. FFH took cash to buy shares in the open market and reduce the available share count...I suspect they will continue to take cash going forward. At some point, they will offer to take FIH completely private. FFH is generally happier when they own the whole pizza, rather than a few slices. In the meantime, they will bring in outside investors including some of their friends to fund the purchase of IDBI. Let's see where this $1B goes that they just raised. I suspect they will inject it into FIH, increasing their percent ownership dramatically! Fairfax will be one of the largest foreign institutional investors in India in 20 years...outside of nation-state owned entities. Full disclosure: I own zero FIH. I just let FFH handle the investments in India. I don't have the time, expertise or access they do to know the Indian market nearly as well as they do. Cheers!1 point

-

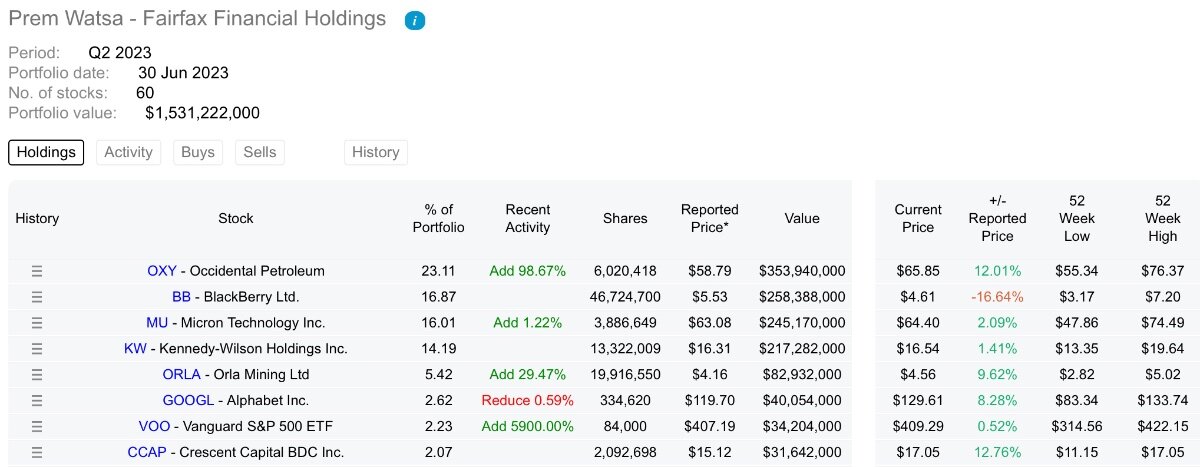

Clearly Berkshire was sold to generate funds to buy Occidental

1 point

-

Plus: "When you put all of that together, we look at that operating income of $4 billion as a pretty conservative number."1 point

-

I'm surprised that CIBC, in their note on the MW report, didn't mention that MW chose only FFH's closely-held investments where fair value exceeds carrying value. What about those that trade publicly whose fair value exceed carrying value... like FIH? Taking my estimate for YE BVPS and adding to it the difference between fair value and carrying value for ALL closely-held investments and incorporating an appropriate haircut for taxes on the difference, FFH's FMBVPS ($987) is more like 8% higher than reported BVPS ($914). The IFRS change argument is ridiculous as all insurers are faced with the same set of accounting rules. It may work better for long tail liabilities than short in a rising interest rate period, but FFH didn't make up the rule to suit its balance sheet and it will suffer relatively if rates decline. What kind of market responds positively to this standard of analysis? How is Brett Horn still employed? So many questions.1 point

-

Yea I totally respect someone like Steve Eisman and the way he goes about it, but these bullshit artists who basically do nothing but take positions and then rant and rave on social media and TV....total scumbags.1 point

-

Thank you. Ditto this.1 point

-

Your mortgage is fixed for 30 years in the U.S. generally. The bank isn't going to come in and sell your house from underneath you if the price falls but you can still pay your mortgage payment. Cheers!1 point

-

National Bank mentioned a few of the driving factors for stock price increase this year. It looks like analyst are starting to catch on to what has already been mentioned here. https://www.theglobeandmail.com/investing/markets/inside-the-market/article-fridays-analyst-upgrades-and-downgrades-for-jan-26/1 point

-

I can't speak for others but based on the 2024 portfolio thread, JOE is still one of the most commonly held / heavily weighted positions. Kuppy recently commented on valuation on his Twitter (this is his largest position), reiterating that there is still a significant discount to NAV despite the run-up in price.

1 point

-

If I were you, I'd upvote this post.1 point

-

@Luca, In my opinion the option : "Unopinionated" is missing. Happy New Year to you.1 point

-

I think the risk for markets is that the S&P 500 is already trading at 20x forward earnings. The long bond is already below 4%. The S&P 500 is already at levels last achieved when the Fed Funds rate was close to zero, the Fed was printing money like crazy, the US government was doling out handouts to all and sundry, and the US economy was enjoying one of the strongest economic recoveries in the post WW2 period. And to the extent interest rates go lower it will be because growth is slowing down considerably and most Wall Street forecasts are pencilling in 10%+ EPS growth for the S&P 500 in 2024 and a lot faster growth for Mag7 and the like. Also the Fed seem to make it up as they go along. While I wouldn't discount a political motivation for promising rate cuts in an election year especially with a lot of government debt requiring refinancing, they will look very stupid if inflation increases in 2024 and they try to go ahead with rate cuts.1 point

-

I guess it may be time for another flush: I do not think the Saudi's will play this over again like in 2015, as it cost them dearly.1 point

-

1 point

-

I think the Shiller PE is the best, but still imperfect way to look at the market price to value. Lets ignore how top heavy the S&P 500 has gotten and how Shiller doesn't account for tax or interest rates and assume you could use it as a market timing tool. If you did, you'd have to be out of the market for years on end, even decades, all the while missing growth in S&P earnings until you get back in. I don't see any mechanical rule that is possible to follow from it. For example, if you get out at a 30 PE and back in at a 20 PE, it would have gotten you out in 1929 just before the peak but put you in again in 1930 to ride it down to a 70% loss in 1931. Or out in April, 1997 (800) and not back in until Oct 2008 at 1000. That looks great until you realize that adjusting your basis for dividends lowers it to $570 and increases your returns to 5% annualized. So if you had the incredible self-will made of pure steel making decisions emotionlessly on positive expectation mathematics that is necessary in order to be able to sit out the market for 11 and a half years you would have, roughly broken even holding bonds instead of the market? In reality if you are going to actively invest, measures of how cheap or expensive the market is shouldn't matter at all. You either find attractively priced opportunities, or you build up cash and keep looking in different places. If the S&P 500 is overvalued, that doesn't mean mid-caps or small caps are, and if they are all generally overvalued that doesn't mean there aren't still a few great opportunities in all of them. Buffett clearly described the internet bubble as it was happening, but he didn't sell his stocks. No one did.1 point

-

These days I give a decent amount of credit to Prem for his capital allocation decisions and opportunities. Buying back stock like Singleton of Teledyne, at book value or below, is something that few other CEOs are willing or able to do in a rational, shareholder friendly fashion. He also has the ability to buy back portions of associates that he has sold off to OMERS to raise the capital needed for previous buybacks (10% of Odyssey). The longer term focus on shareholder value, and maintaining franchise value of the insurance subs by not laying off staff in times of crisis (COVID) is also a differentiator from competitors. I used to work for a competitor that wasn’t able to maintain capital levels sufficient to support the writings of premium levels when they rose from the inflation shock of the last few years, and their capital levels dropped because they were reaching for yield on their bond portfolio. I got laid off recently as the staff cuts began, in an effort to return to profitability so that capital levels could be rebuilt. (I am able to view the early retirement with equanimity because I have over 70% of my retirement assets in Berkshire and Fairfax.) The less experienced staff that has been retained will be cheaper, but most of the value I added over the years was in using my experience to help the company avoid self inflicted wounds through poor business decisions. Fairfax’s insurers will have a continuing and expanding advantage over the company I used to work for because they have a solid balance sheet, and a growing insurance business, which gives them the best of both worlds — experienced staff and opportunities for professional growth for the newer employees that are added each year. Don’t underestimate the value of the corporate culture that has been created at Fairfax. That can be part of a company’s enduring moat just as much as more easily understood business model advantages can be….1 point

-

@vinod1 with earnings growth of 5% are you not essentially saying Fairfax’s capital allocation will be poor moving forward? Part of the reason I am so optimistic on Fairfax today is: 1.) the cash flows are front loaded. We know with a fairly high confidence level that they are going to deliver record operating earnings 2023-2025. Buffett teaches us when valuing a company the TIMING of future cash flows is exceptionally important (the sooner the better - the higher the valuation a company should get). 2.) the opportunity set to deploy capital is very good today and i suspect is about to get even better: and Fairfax has +$3.5 billion that will be re-invested each year moving forward in a very good investment environment. Bond yields are at 15 year highs. Small cap stocks are trading at bear market lows. If we get a recession all equities will go on sale (and already cheap equities will get stupid cheap). When it comes to capital allocation today, Fairfax is like a major league hitter getting lobbed softballs. As a result, I will be surprised if earnings growth is 5% per year moving forward. You also bring up ‘one time’ losses. Fairfax’s results will be volatile. Especially if we get a recession (no idea if this happens). My view is volatility is a good thing for Fairfax - smoothing results out over a couple of years. The TRS-FFH purchase in late 2020/early 2021 is a great example. They masterfully took advantage of extreme volatility in Fairfax shares - extreme pessimism. Another great example was selling corporate bonds and shifting to government bonds and shortening duration to 1.2 years in late 2021. They sold at the top of the fixed income bubble. The extension of their fixed income portfolio to 3.1 years in October looks exceptionally well timed. Selling Resolute at the top of the lumber cycle? Brilliant. Selling pet insurance for $1.4 billion…. Nuts. Lots of these decisions are $1 billion decisions… they are ‘needle movers’ for Fairfax and its shareholders. Fairfax investors fear volatility. I think they might have it backwards. Especially given how Fairfax is positioned today (strong balance sheet and record operating earnings). Investors in Fairfax should be praying for volatility. With both insurance and financial markets. Thriving in volatile markets - this looks to me like it is likely a significant competitive advantage for Fairfax today compared to peers.1 point

-

1 point

-

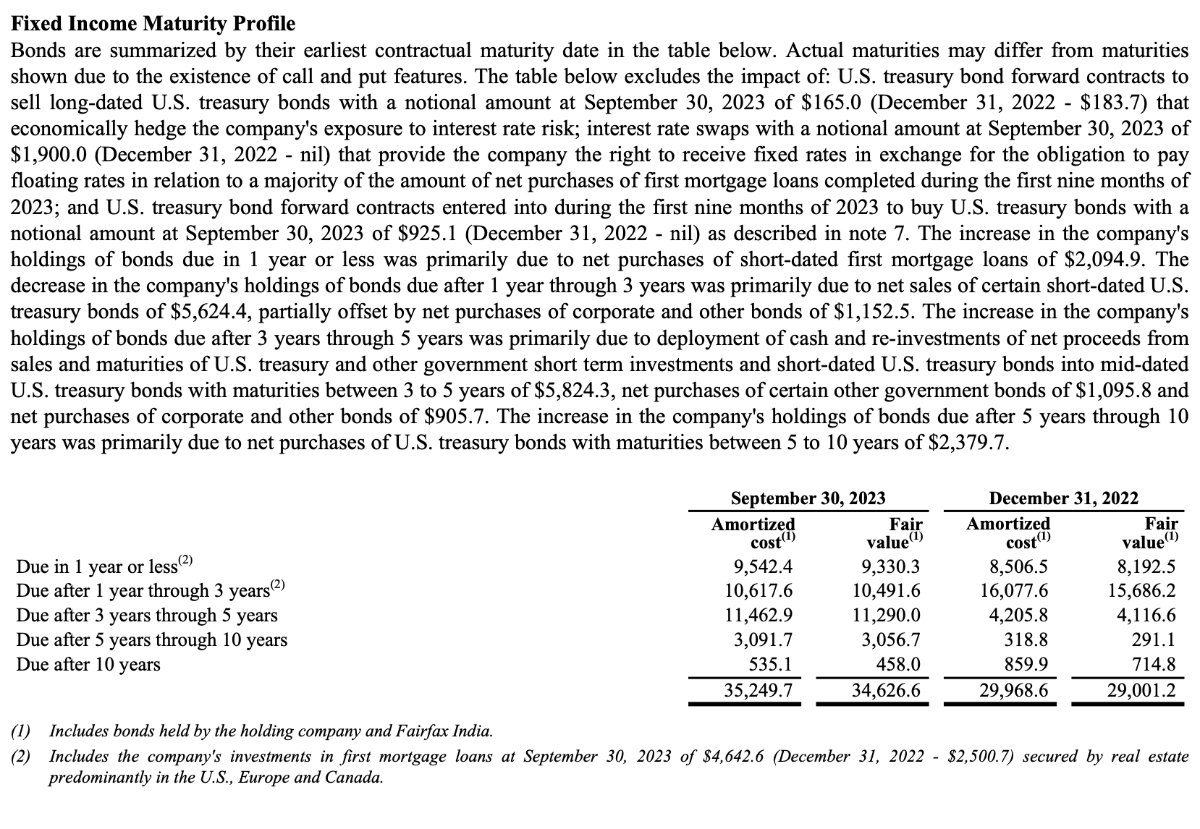

https://www.globenewswire.com/news-release/2023/11/02/2772905/0/en/Fairfax-Financial-Holdings-Limited-Financial-Results-for-the-Third-Quarter.html "Book value per basic share at September 30, 2023 was $876.55" "We achieved an underwriting profit of $291.6 million on an undiscounted basis and a consolidated combined ratio of 95.0% for the quarter, reflecting significantly lower catastrophe losses and excellent current accident year underwriting margins. Gross premiums written grew by 5.0% and net premiums written grew by 4.8%, primarily reflecting new business and continued incremental rate increases in certain lines of business." "At September 30, 2023 the company's insurance and reinsurance companies held portfolio investments of $56.8 billion (excluding Fairfax India's portfolio of $2.0 billion), of which $6.4 billion was in cash and short term investments representing 11.2% of those portfolio investments. During the first nine months of 2023 the company used cash and net proceeds from sales and maturities of U.S. treasury and other government short term investments and short-dated U.S. treasuries to purchase $5.8 billion of U.S. treasuries with maturities between 3 to 5 years and $2.4 billion of U.S. treasuries with maturities between 5 to 7 years, and to make net purchases of $2.1 billion of short-dated first mortgage loans and $1.6 billion of corporate and other bonds with maturities primarily between 2 to 5 years. These actions should result in continued higher levels of interest income for approximately the next 4 years." "At September 30, 2023 there were 23,115,838 common shares effectively outstanding." FFH_-_2023_Q3_Interim_Report_.pdf FFH_-_2023_Q3_MD&A_section.pdf1 point

-

Prem and Patrick Byrne never complained about short-selling. They only complained about naked short-selling and coordinated attacks through certain analysts, media and hedge funds, who specifically created downward spiral attacks because they artificially increased the number of shares available as the DTC wasn't properly enforcing fail to delivers. I don't think any critic ever had an issue with short-selling itself...which is part of creating an efficient market. Cheers!1 point

-

Thanks, Viking! With so much moving parts and different earning streams, FFH is one of the companies, which earnings is extremely hard to model (and maybe it is a plus and an opportunity vs analysts/market), but I think you did an incredible job doing this.1 point

-

@MMM20 - Slow clap for you funniest guy on the board1 point

-

Thank you, @Luca, Yes, I practice gallows humor [German : Galgen witz, Danish : Galgenhumor] to mentally cope with and to mentally survive the madness thats going on here in Europe. It is for sure needed. I have started to follow Sahra Wagenknecht, based on the content of your last post. My spoken German is a bit rusty, but I have no problem taking care of dailyday activity by speaking German, while in Germany, while I have absolutely no problem with understading all shades and nuances of the German language spoken or written. [Insufficient active vocabulary, because of lack of practice]. I also feel like a touchy bitch when our North American friends here on CoBF talks about money and starts blending US South border security into this European warfare matter. It concerns preventive measures in relation to 1st or 2nd order effects in relation to other and European NATO member states in case the situation escalates further. If our common North American CoBF members cannot or will not understand this, then I am not able to explain it. Just to try to trigger some kind of embarrassment into our fellow North American CoBF members with such stance, I will try to dig up some factual data about how Denmark has behaved in relation to Ukrainian refugees coming to Denmark since the war in Ukraine started. @Luca, Nassim Taleb would express it as "You simply don't have the same skin in the game as your North American friends on CoBF." -Period. - - - o 0 o - - - Edit : Bloomberg [September 26th 2023] : Erdogan Says Turkish Approval of Sweden NATO Bid Hinges on F-16s. Just Recep Tayyip Erdogan oportunistic modus operandi.1 point

-

Was peace possible if NATO agreed to stop its expansion?1 point

-

https://foreignpolicy.com/2023/09/22/ukraine-war-ethics-morality-murky/1 point

-

I coulden't have phrased it better than @no_free_lunch above. Also : Wikipedia : Ukraine - Declaration of Independence. Please also here note which countries were among the first three contries to recognize this on December 2nd 1991 : Poland, Canada and ? ... Russia!.1 point

-

@UK, @no_free_lunch, there has not been a poll done in at least a year of US citizens asking whether or not they would be willing to pay $100 per person per year to support the war in Ukraine. You may think $25bn per annum is a small price to pay, but US citizens think otherwise. Also, nobody is talking about handing the region over to Russia. However, it is NOT the job of US taxpayers to support Ukraine. It is the job of Ukrainians. Yes, we are obligated to defend Poland and the Baltics due to treaty obligations. Meanwhile, let's not forget, Ukraine has never existed as a country. Western Ukraine was part of Austro-Hungarian empire for centuries, and eastern Ukraine was called Little Russia for centuries, and part of Russian empire, and was Russian speaking. Hell, Kiev was called the mother of Russian cities.1 point

-

Luca, I definitely agree with you on contrarian situation here and big excitement on a micro level/valuations, especially on Prosus/Tencent. But it seems to me that all political/geopolitical/macro situation just continues to go to the wrong direction. And in order to succeed just beeing contrarian is not enought. But I hope things still could change and you will also be right in the end.1 point

-

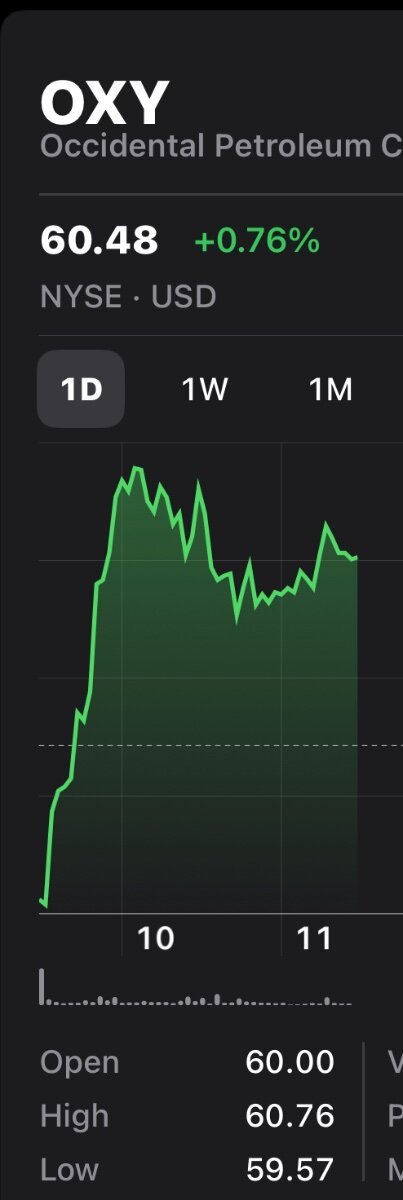

That’s a big weighting to OXY. Don’t disapprove, as I was kind of kicking myself I didn’t buy some in the mid 50’s. However, I do prefer these type of positions in my long term compounders. The index position is a head scratcher at these levels though. It’s funny, a lot of people have bagged Gaynor at MKL for his myriad of holdings and argued why not just have an ETF position. FFH seem to think so. All appears more rump, less tail albeit with a slight inflationary bias and in the case of OXY leveraging the implied BRK put.

1 point

-

Never attribute to malice that which can be adequately explained by stupidity. Hanlon’s razor.1 point

-

I begged @Dinar to talk me off the ledge regarding Nintendo. The next day I found this in a used book I bought on Amazon: I'm fine.

1 point

-

“Janet Yellen concerned about Chinas new export controls”….. Think Janet is equally “concerned” about any of the US policy directed towards China or Russia? Even Canadian tariffs? Nah bro. https://www.cnbc.com/2023/07/07/yellen-says-shes-concerned-about-chinas-new-export-controls.html1 point

-

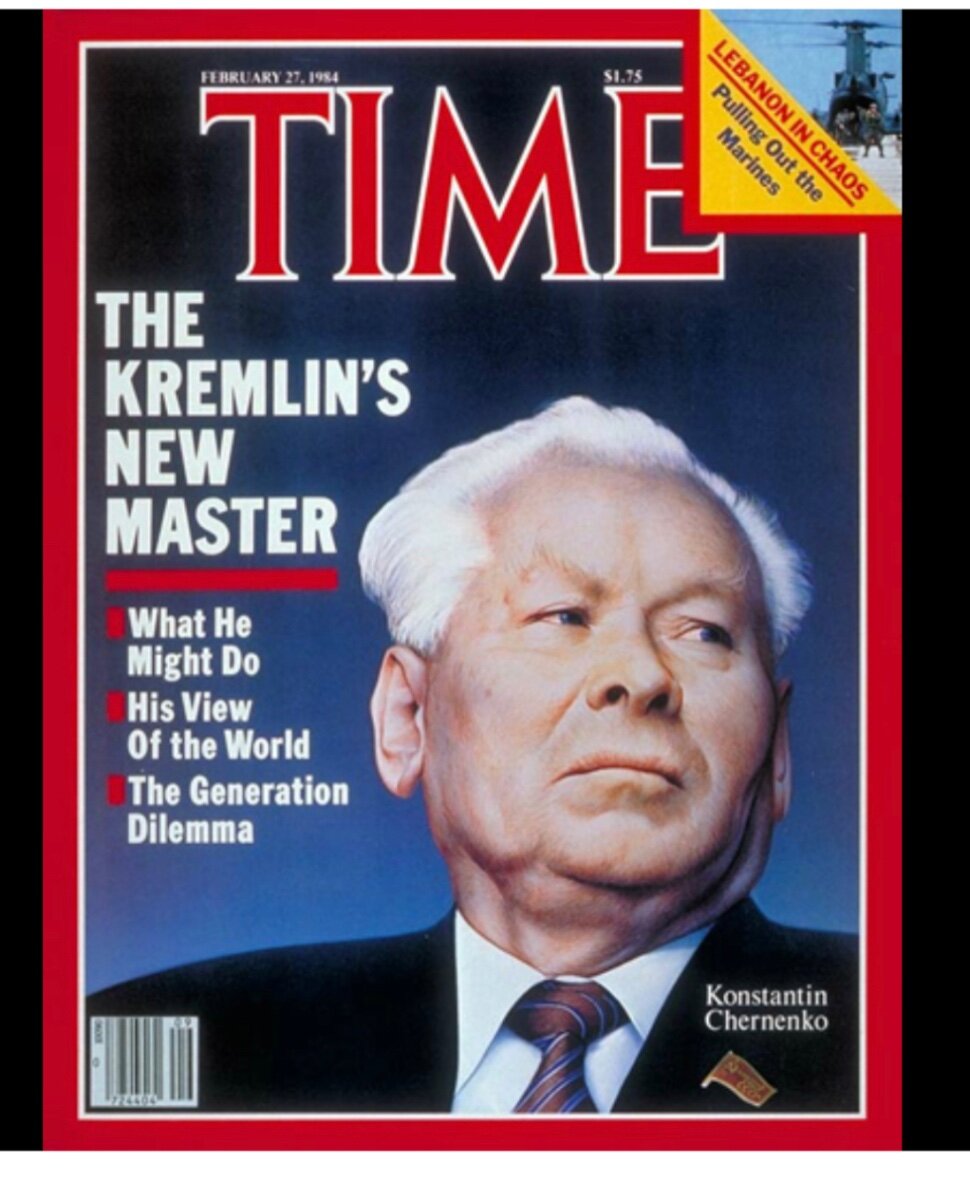

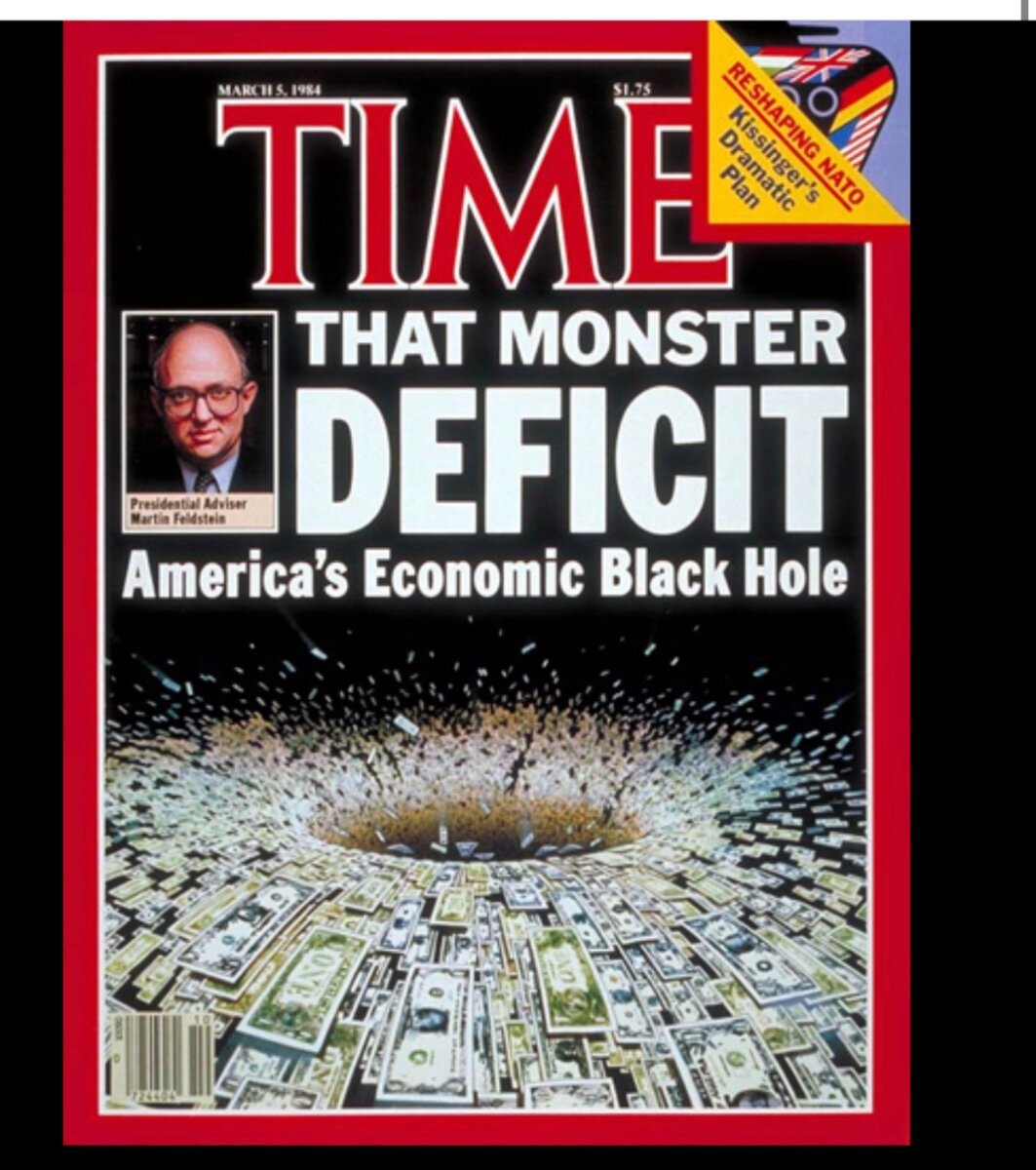

A lot changed in the past several decades, yet much remains the same: concerns about the economy and the geopolitics Time magazine cover page in Feb 1984 and March 1984; doom and gloom couple of years later Chernenko died making way for Gorbachev and the economy did just fine

1 point

-

Who needs to boycott Bud Light when you have great vodka? My guy came through with some goods for Americas birthday. No Gold unfortunately.

1 point

-

Prigozhin, whose Wagner troops have pulled back from Bakhmut, also attacked Russia’s current war efforts in the face of Ukraine’s counteroffensive. Directly contradicting Putin’s claims that Moscow has fended off Kyiv’s counterattack, Prigozhin also accused the Russian military leadership of lying to the public about the scale of its losses and setbacks in Ukraine. “The Russian army is retreating in all directions and shedding a lot of blood … What they tell us is the deepest deception.” https://www.theguardian.com/world/2023/jun/23/wagner-chief-accuses-russias-military-of-attack-and-says-evil-leadership-must-be-stopped1 point

-

FIH is a beach ball under water that’s slowly being filled with air, eventually it will “pop” up. When that happens who knows? The BIAL is a direct beneficiary of India’s growth. Indigo airlines of India ordered 500 airplanes. https://www.reuters.com/business/aerospace-defense/airbus-wins-historic-500-plane-indigo-order-2023-06-19/1 point

-

I wish! No, 54 in July and look like a grown up Charlie Brown. Good grief! But my niece and nephew keep me young. Nothing like trying to keep up with a 5 year old and 8 year old! And I also follow Buffett's adage and eat like them. That being said, there's only so much chicken fingers I can eat unlike them! Cheers!1 point

-

The incredibly high living standard the US enjoys today is largely the result of the global world order it imposed/built/lead after world war II (with, of course, lots of help along the way from other nations). This positioning allows US companies dominate the world (economically) - China and Russia exempted (perhaps India too). If the US retreats, the void will simply be filled by China/Russia/totalitarian regimes. Shrinking your empire is never a good choice - it is usually catastrophic. That is, after all, what the Soviet Union did in 1991. Reversing a bad decision is pretty much impossible (Putin is learning that lesson today).1 point

-

I don't see why Xi has to figure out how the US does things in order to lead his country. Even so, I doubt Xi is dumb or otherwise incapable of understanding any complex topic, including "how the free markets operate".1 point

-

Some interesting comments from Powell's presser. Of course he is data dependent so if inflation falls off a cliff and we fall into recession this may all change. But certainly indicates rates will stay higher for longer. I wonder that once markets start to believe this they might assign lower PE multiples to stocks. “It will be appropriate to cut rates at such time as inflation is coming down really significantly. And we’re talking about a couple of years out.“ "I think, as anyone can see, not a single person on the committee wrote down a rate cut this year -- nor do I think it is at all likely to be appropriate if you think about it." "Inflation has not really moved down. It has not reacted much to our existing rate hikes. We’re going to have to keep at it.” "There's just not a lot of progress in core inflation." "We want to see it moving down decisively." "Risks for inflation are still to the upside."1 point

-

Plugging my nose and adding to csu1 point

-

+1! You can add a couple more: 03. Chairman & CEO has never sold a share = Exceptional. 04. Chairman & CEO donates a shitload of money, but never uses his name or his family's name = Exceptional. Cheers!1 point

-

I think it's reasonable to model a normalized EPS of $100 USD going forward, which is clearly not priced into the shares. Where I get stuck is on growth rate and where normalized EPS will land in year 4 and beyond ( @Viking focuses on 2 to 3 years out, but I happen to enjoy wasting brain cells on rough 5 and 10 year forecasts). Let's oversimplify and say after tax EPS breaks down neatly into 3 factors: $40 per share of insurance underwriting earnings at a combined ratio of 95 $40 per share of interest income at an average yield of 3.5% $20 per share of non-insurance/interest earnings growing 10% annually Total Baseline EPS: $100 ^ Notice $80 of earnings is tied to two CRITICAL variables entirely out of FFH's control; the insurance cycle and interest rates. Now let's setup a conservative scenario for EPS in year 4. First, for simplicity's sake, let's assume that in years 1 through 3 a total of $300 per share was reinvested and results in additional earnings of $30 per share in year 4 (we'll call this 'earnings on reinvested cash'. Then, let's assume we're in a soft, mid-cycle, insurance rate environment, and that short term interest rates have declined to a level more in line with long term GDP growth potential. Year 4 EPS Scenario: $30 per share of insurance underwriting earnings assuming modest premium volume growth and a CR of 98 $20 per share of interest income at an average yield of 1.5% $60 per share of non-insurance/interest earnings (including $30 EPS from cash reinvested in yrs 1-3) Total Year 4 EPS: $110 ^ Under that highly conservative, highly oversimplified, set of assumptions I can see a scenario where earnings remain relatively flat for at least the next 4 years. From years 4 to 10 let's assume EPS grows 10% annually. That gives us the following EPS projections for years 5 and 10: Year 5 EPS: $121 Year 10 EPS: $195 If we slap a 15x multiple on those conservative estimates we're looking at: Year 5 Share Price: $1,815 Year 10 Share Price: $2,925 If you buy at $700 per share you're looking at a decent shot at a 15% return over the next 10 years. Not too shabby.1 point

-

https://moralfoundations.org/ Jonathan Haidt has some interesting theories and research, covered in brief on that page but in more depth in his book "The Righteous Mind: Why Good People are Divided by Politics and Religion" The gist of it is that evolution baked into us a basic framework of "moral taste buds" -- we can tell when something is fundamentally unfair, or when someone is being disloyal or cheating, etc. Troops of monkeys with an overly vicious alpha will naturally form a coalition to do away with the tyrant. Sic semper tyrannis, since before humans walked the earth. I remember hearing about a study with monkeys where two monkeys are separated but they can see each other, and they each have to do the same task in order to get a reward. The first monkey is given some grapes, a favorite food for them. The second monkey sees this. Then the second monkey is given some cucumber slices instead of grapes for its reward. The second monkey brain must emotionally be screaming "UNFAIR!" because it takes the cucumber slices and throws them in the face of the lab tech. Being able to detect when things seem fair will tend to lead toward survival of the group, so genes which help us detect fair treatment have been kindly baked in through evolution, or they're god-given by his/her magnificent evolutionary process. We've got a lot of pro-social genetic behaviors baked in like that. We experience a thing called "Elevation Emotion" when we witness acts of moral beauty. Just witness this pizza delivery guy who saved a bunch of kids from a burning house and try not to feel elevation emotion. That feeling is baked in to most of us (minus perhaps the psychopaths) But that's just the beginning. Biological evolution gets you to cave man level where life is pretty much like the Hobbes quote "solitary, poor, nasty, brutish, and short." Then comes the cultural dynamics. By the power of language we have shared stories and myths. Using these shared stories, we humans have been improving on our genetic hardware by installing new moral ideas as software "Necktop Apps" (Daniel Dennett's fun term) ... we build agreed sets of guidelines and hard rules for the really important stuff ... but it has morphed over time. We have evidence that very ancient people used to kill children and bury them under the foundation stones of new dwellings. Perhaps their gods told them that it helped ward off evil spirits. Warding of evil spirits was an important concern through the ages. People in England during Shakespeare's time would put three big scratch marks on their fireplace mantles to repel witches who might otherwise descend into the house through the chimney. Even up through the middle 1800s in American folk religious belief, people used "Lamen parchments" with religious power words on them like "Tetragrammaton" and seven pointed stars and funky line drawings, and amulets on necklaces and coin shaped talismans. Why did they stop sacrificing kids? In the Abrahamic tradition it's arguable that they stopped because of the story of Abraham and Isaac and the ancient interpretation which is essentially: "This story proves it's okay to stop killing kids, and kill rams and sheep instead." To our modern minds it is so far out of context that it just looks like Abraham had a psychotic break and turned murderous on his kid. Just because something is "made up" as you say, it doesn't mean it has no power. Money is "made up" and yet Osama Bin Laden, a great hater of all things USA, had suitcases full of dollars. Why? Because if everyone else in the world agrees that you can trade suitcases full of green paper for real physical goods, then it's real. The superpower of humans is our ability to have millions or billions of people share the same ideas and act according to them. Take the story of Job in the Old Testament. I don't think that guy really existed and I don't think god and satan placed bets on how far he could be pushed, etc. But whether or not Job was a real person is like the least interesting question you could ask about the text. The interesting questions are along the lines of, "What were the authors grappling with and how did this story serve their community? What can we learn from the story?" Can anyone name one single way in which the story of Job is _more_ powerful if there is a real human versus an allegory. Our lives are uncertain and temporary. Against this backdrop, the human mind craves certainties. I admit I grew up believing Job was a totally real person, but I find the story so much more interesting when I'm not painted into that corner of believing an all powerful being did a good guy so dirty just because of a bet. There are plenty of hints that Job wasn't real, by the way, which is why I changed my mind. (There are multiple different endings to the story right there in the text of the old testament, for example -- and this is a pretty good indication that some editing was taking place.) One more way to look at it: Aesops Fable of the Tortoise and Hare. Does the power of that fable derive from the fact that a real tortoise one day had a race with a hare and won because he kept at it slow and steady? Nope. But when you're having a hard slog of it one day, you might remember the old story and feel a bit of inspiration to just keep plugging away at your task and eventually complete it. The inspiration came from the story, not from a literal physical race. At least when the atheists think there's a right thing to do they can be expected to give you their rationale. Because they aren't leaning their moral authority against the idea of a god, they basically _have to_ back up their arguments and try to be convincing. On the other hand, I have often experienced an exasperating form of know-it-all-ism where religionists think they get to declare "This is what is right, both for me and for you. Because god." And then they walk off like they think they just dropped the mic. I don't think any human deserves that much unquestioned loyalty. That kind of environment would be an incubator for religious tyrants. When you boil it all down, why would you say our sense of morality needs to be founded on a god, I mean the kind that exists even when nobody believes in him/her? Why does that provide anything better than what we've got which is a set of moral rules that have evolved with our civilizations? If there really does exist an unambiguous Absolute Morality with a real god backing it up, then which god is it and what are the North Star rules? And more to the point, why would those rules be _more_ valid if the god is real?1 point

-

Regardless of what’s going on, haven’t folks realized by now it’s a bad idea in general to make bets against basically everything blowing up? Essentially wagering that the powers that be will just stand by and let it happen? You’re already seeing it in the US….now folks wanna blame and be hostile that the bear trade is losing steam but bottom line is you should know better and when there’s intervention, like there always is, you don’t get to moan and groan about how you got screwed. Even more generally speaking, WTF is it with the bear people? Like there’s a million and one ways you can make easy money being long a whole variety of things. Yet for some reason these folks have this need to stand on a pedestal, screaming for attention, hoping to call a measly 10-25% down move? Which is not only challenging, but also difficult to time. So these experts and fund managers and doomsdayers aren’t even really trying to make money it seems, but simply get attention and walk around for a short while as “the guy who called it”….isn’t that kind of pathetic?1 point