MMM20

-

Posts

3,438 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

I believe they’re opportunistic with even the shares purchased for comp so it has some lumpiness

-

Thrilled they're smashing the buyback button. It's the best when you're convinced a stock is trading at a third or maybe half of (a growing) intrinsic value and mgmt makes it easy to sit on your ass. Back to the beach...

-

Honestly I was only half joking about the KW land redevelopment or Recipe synergies. Is there anything unique about this one? Are Canadians really loyal to it? Scratching my head down here in the US as I’ve read for years about how volumes are struggling and even Napa and Sonoma wineries are closing left and right. And if Prem thinks it’s cyclical, why not buy STZ, TAP, BUD, DEO?

-

>20x FCF for wine? Isn't that a struggling industry with typical multiples in the mid single digits? What's Prem's angle here? Working with KW to redevelop the land? Synergies with Recipe?

-

Your point is a valid one (and of course we should all learn from Munger) but I think it’s also worth mentioning that many folks just went off the cliff paying up to 40-50x (I'm not sure that's what Charlie had it mind) doing exactly that and now find themselves down 60%+ (and of course declaring many of these still great companies broken). We know there is a price too high for even the best business and these style boxes come in and out of favor and always go too far. I’m waiting for someone to ask why Fairfax isn’t also participating in this GOOGL fundraise…

-

Are you you weren’t misinterpreting “there is no good reason” as “there is a good reason but I don’t know it”…? Seems like that might be the crux of the consternation.

-

Can you walk us through this?

-

Absolutely hilarious take. Prosus trades at a discount to the Tencent stake alone. Exor is almost there with Ferrari. These are two of the best businesses in the world. You’re getting everything else for free or better. Time is our friend in those situations. No need for the discounts to close. Are we in a similar spot with Bangalore airport yet…?

-

Board is testy today. That does it, I'm buying another share.

-

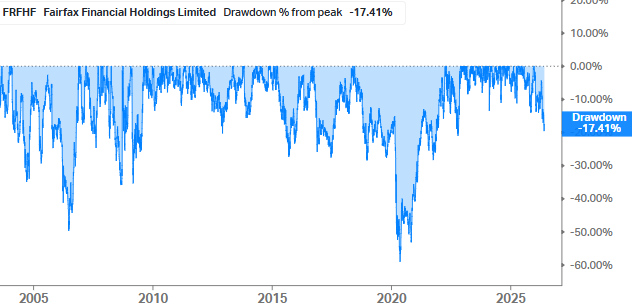

I can only speak for myself, but I wanted to push back on the whole discussion about family conversations, the possibility of some extended weakness (of course it could happen), and so on, b/c this current drawdown is par for the course, every year or two on average, and shouldn't really change anyone's thinking about anything...

-

I personally get concerned when everything I own is working at the same time. If you have a sufficiently diversified portfolio, you should expect things to work at different times. The experienced investors here with big positions presumably know this and have the conviction, temperament, and structure to see it through.

-

I don’t mean this disrespectfully, but bearprowler’s question is exactly the sort of thing we would expect to see at local bottoms. Another Dutch auction buyback incoming?

-

Prosus CEO has seen the light and cut way back on the Tencent sales FWIW. They wrote about that shift a quarter or two ago... selling Delivery hero, Meituan, other non core stuff. Still bought back $100mm last week, and we still get more Tencent per Prosus share. But it’s far from perfect and I’ll flip to Tencent if it trades at a premium.

-

Welcome to the pain train, Prem. Yes, Ferrari is a beast and might be the best business in the world. Yes, we are effectively buying it for low teens P/E with the NAV discount at Exor these days. But no, we cheap value guys will never make money in it. The market gods have spoken.

-

The key thing has been the cheap mid 2010s insurance acquisitions. Skeptics tend to want to exclude those from their analysis of capital allocation performance. A lot of money has been made taking a holistic view and noticing how those great acquisitions (and great management of them) totally transformed the structural earnings power of the company. Guess what, most good investors’ returns follow a power law type distribution with a few outsized winners driving the bus. In this case, it’s mostly those acquisitions. IMHO the poor framing and analysis even shows up here in how “stock positions” is separate from the general conversation. Probably the biggest single variant perception has been to fading those who insist on analyzing the various buckets in isolation. It’s a smarter-sounding version of the same mistake made by the people who fixate on particular investments like BB, which plenty of guys told me 5 years ago was disqualifying and made FFH uninvestable. Unless the stock basically doubles overnight I’ll keep betting that those people are wrong.

-

Do you count buying insurance companies on the cheap as part of their investing track record or not?

-

Fine, name your favorite Canadian entrepreneur then. Maybe he’s not quite the Canadian bill gates. I hope you get my point. It’s not like I said Ryan Reynolds or Gretzky. My point is that they could probably do well to do more to upgrade the board these days at this scale and as they transition to the next generation of leadership.

-

Maybe it’s worth revisiting the conversation about whether it’s time for Fairfax to upgrade its governance including the board. I don’t mean to single out Lauren Templeton, but can’t we go get some more truly independent and high level business people at this point in FFH’s development? I would think some of these folks own the stock already, and for Canadians it would be as prestigious as BRK’s board. Like why not go get Tobi Lutke or someone at that level?

-

Value it on normalized investment returns and combined ratio and with this amount of the best kind of leverage, a big structural advantage that somehow remains overlooked, it's easy to see how the long term CAGR could easily continue to be in the ~20% range, especially if Mr Market ever slides them into the "great capital allocator" / "compounder bro" bucket at some point in the future. We're talking about a ~10% earnings yield, almost all of which is distributable for buybacks at a discount. And those earnings should grow at double digit rates for a long time. How many opportunities like that exist in "big cap, outstanding track record, long runway" land nowadays? Sure, odds are the various drivers will have a down period at the same time at some point, but maybe our only edge as non-pod investors is the ability and duration to focus on the structural advantages because we can accept and live with that cyclicality and volatility - and maybe even take advantage of it because we don’t have risk managers or LPs looking over our shoulders every month (or day). Of course, that doesn’t mean there aren’t better ideas out there! I think I've got a few too!

-

I think it was cheap then and even cheaper now, a coiled spring. I’m adding for the first time in a few years. The business owner mindset + staying patient and willing to accept a dead year or three might be our only structural edge in the pod shop era. They don’t have the duration. Over/under for the price 5 years from now is US$5000.

-

Who is Prem's abominable no man? Who's his most trusted advisor? Who pushes him toward quality? I'd argue it takes 3-6 people to perform the function of one Munger. Peter Clarke? Brian Bradstreet? Wade Burton? Jennifer Allen?

-

One of the many reasons your posts are valuable. Thanks for sharing.

-

I own some GPN+FOUR, but nowadays I’m wondering: would buying this entire group actually be the best move? Should we channel Buffett in South Korea or Japan?

-

This is why it’s been easy to just hold the damn stock!

-

FOUR - We got a runner - by Short & Squeeze Corner.pdf