glider3834

-

Posts

1,019 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Riverstone Europe/Barbados sale proceeds went to Holdco, Fairfax did have option to repurchase their equity positions (in Riverstone Europe) which I think they would do through their subs not the Holdco & they would need around $1,2 bil & they look to have the cash in their insurance subs to do it . I don't think there was an option for Fairfax to buyback their European run-off business - they have kept the US run-off business which I think was a strategic move.

-

Yep Prem has promised us lumpy returns! - most European banks, including Eurobank, are really taking it on the chin recently due to Ukraine conflict/risk around Russia exposures - I believe Greek banks have limited direct exposure to Russia but now there is economic uncertainty around impact (higher energy costs etc) on Greece - but on the flipside Eurobank looks cheaper now at just 60% of TBV- an opportunity for Fairfax to raise its stake a bit more?? Also I think given Fairfax's current share price, another opportunity is there now for them to buyback their stock - NCIB or maybe another SIB perhaps?

-

+1 Still digesting - just flagging this one which I haven't seen before (or maybe I missed it) it looks like an Asia focused version of BDT 'Since 2008 we have been investing with founder Kyle Shaw and his private equity firm ShawKwei & Partners, which takes significant stakes in middle-market industrial, manufacturing and service companies across Asia, partnering with management to help improve their businesses. We have invested $398 million in two funds (with a commitment to invest an additional $202 million), received cash distributions of $198 million and have a remaining value of $374 million at year-end. The returns to date are primarily from our investment in the 2010 vintage fund, which increased 46% in value in 2021 and has produced a compound annual return of approximately 16% since 2010. The 2017 vintage fund has drawn about 50% of committed capital to date, with a much-improved outlook for new deals, including its recent acquisition of CR Asia Group.' Also I got my estimate of closing market value of Exco Resources wrong - Fairfax have marked it up by only 12% to $267 mil from $238 mil. I thought it would be marked up higher - Chou Funds increased their stake by higher percentage - different valuation method perhaps or maybe Chou Funds have increased their shares held/cost base which they didn't break out in quarterly reports? Anyway positive that Exco increased their total proved reserves by 85% in 2021.

-

I think Prem & Fairfax did a big energy deal, I would bet that its more than likely going to happen through David Sokol/Atlas with Fairfax chipping in capital if needed. If they do a banking deal in Europe, its probably going to happen via Eurobank - here is a recent one in Dec-21 https://www.eurobank.gr/en/group/grafeio-tupou/etairiki-anakoinosi-28-12-21 Also it was interesting that Fairfax sold two of their direct owned IIFL India holdings and bought shares in Fairfax India - I think this was in part an opportunistic move as Fairfax India shares are cheap but also IMHO because unless its a future insurance deal then most of their future India deals (with exception of Quess or Thomas Cook sector related deals) I suspect will happen via Fairfax India

-

so I think Fairfax's thinking on Farmers Edge is that crop insurance is being increasing digitalised so data now (like in most industries) is critical to underwriting. However, whether they should have invested so heavily in a pre-profit, insurtech start up is the question. Crop insurance is Hudson insurance (Odyssey) largest business & they are recently partnering with Farmers Edge https://odysseygroup.com/news/unique-digital-infrastructure-creates-new-connectivity-in-crop-insurance/ They haven't executed & missing your forecasts post IPO is something you just don't do. My impression from last CC is they have enough cash now to get to break even - lets hope so!

-

viking yes I think this echoes Prem's comments in the 2020 AR 'As you know, we are building Fairfax for the next 100 years (long after I am gone, I think!!). Recently, I came across two books on long lived companies: ‘‘The Living Company, Habits for Survival in a Turbulent Business Environment’’ by Arie de Geus, and ‘‘Lessons from Century Club Companies, Managing for Long Term Success’’ by Vicki Tenhaken. They both make the point that companies that have survived for over 100 years have four characteristics: 1. They are sensitive to the business environment, so that they always provide outstanding customer service. 2. They have a strong culture - a strong sense of identity that encompasses not only the employees but also the community and everyone they deal with. Managers are chosen from the inside and considered stewards of the enterprise. 3. They are decentralized, refraining from centralized control. 4. They are conservatively financed, recognizing the advantage of having spare cash in the kitty. Fairfax has many of these characteristics and we continue to build our company for the future.'

-

Share price close to US$467 BVPS US$630 at 31 Dec-21 Will have a loss on equity positions since 31 Dec (hard to quantify $s still waiting for AR 2022), but I think this can also be offset by Q1 net operating income & Digit revaluation still to come. So I would estimate P/BV in 0.74 to 0.76 range - so still looks cheap IMHO

-

viking I think its worth isolating the 'float per common share' - to back out the float % that belongs to minority interests in the insurance subs (eg Brit, Allied) Then we can compare float per share with other insurers that have 100% owned insurer subs. I think Fairfax reports total float & float per share for ease of reporting and because they are consolidating those subs where they have control and/or majority ownership.

-

Just following on from interesting discussion on Fairfax's capital allocation/equity investment strategy and whether they have pivoted in any way. I think they have pivoted around focusing more on internal rather than external opportunities which also provides lower risk IMHO. I think if we were looking for a common thread - Fairfax has been very focused on their existing holdings/subs - no major new acquisitions from 13Fs in last year or so - but more focus on optimising/maximising value from existing investments both in insurance and non-insurance . To use a cricket analogy - not trying to swing for the fence (hit a 6) on every ball, but just take lots of easier 1s & 2s. Their largest cash outlays have been on their own undervalued stock - equity swaps & $1 bil share repurchase. A lower risk approach. They won't short any more - again a lower risk approach. So I don't think Fairfax are changing the types of equity investments they are making or we might expect them to make in the future & which has driven most of their book value growth per share over time - they are value investors - but if they are going to make new acquisitions, they appear to be looking to internal opportunities (existing positions/investees) first - Kennedy Wilson investment recently is a good recent example or recent purchase of Fairfax India shares. And also on the insurance side, the focus is on growing premium organically - again lower risk. FFH have also been increasing in FFH ownership (incl Riverstone) in non-insurance investees (post buybacks) Fairfax India 41.8% (current) , 34.5% (Dec-20) Eurobank 32.2% (Sep-21) , 30.5% (Dec-20) Stelco 17.8% (Feb-22) , 15% (Dec-20) Worth noting too Resolute has new share repurchase plan up to 10 mil shares, which could increase FFH's ownership from 38.6% to 43.4% approx. And there is another Sunday ramble from me Looking forward to Prem's shareholder letter next week too!

-

lets hope not! Actually Fairfax added to their Eurobank stake in Q3 & took it to around 32% - Eurobank sold off pretty hard today, along with other financial stocks in Europe & globally, but I think eventually things will settle down

-

Yes fair enough - I probably should have said Speculative tech valuation bubble - i was thinking more about his Dec-20 interview where he pointed to valuations of ZM, SPOT, PTON

-

Yes makes complete sense - KW have a great track record Fairfax could become a liquidity provider this year & if this volatility keeps up it could offer some big opportunities for them in fixed income/equity side - they couldn't be in a better position honestly with just over 50% of their portfolio in cash/ST investments - Prem has finally been proved dead correct with this tech correction finally coming to play - I just wish they had reduced their BB holding which has sold off YTD ( that is my only criticism) although that looks to be offset from their gains on Eurobank - otherwise the rest of their portfolio positioning looks ok

-

Looks like a good move - 13 mil warrants provide potential upside

-

There has been some volatility in Quess shares due to recent change in CEO but i think this article addresses issues - business strategy unchanged and outlook sounds positive as covid reopening should drive more staffing demand/outsourcing https://www.moneycontrol.com/news/business/we-selected-the-best-man-for-the-job-ive-never-felt-more-comfortable-with-the-business-as-it-is-today-quess-corp-chairman-ajit-isaac-8123061.html

-

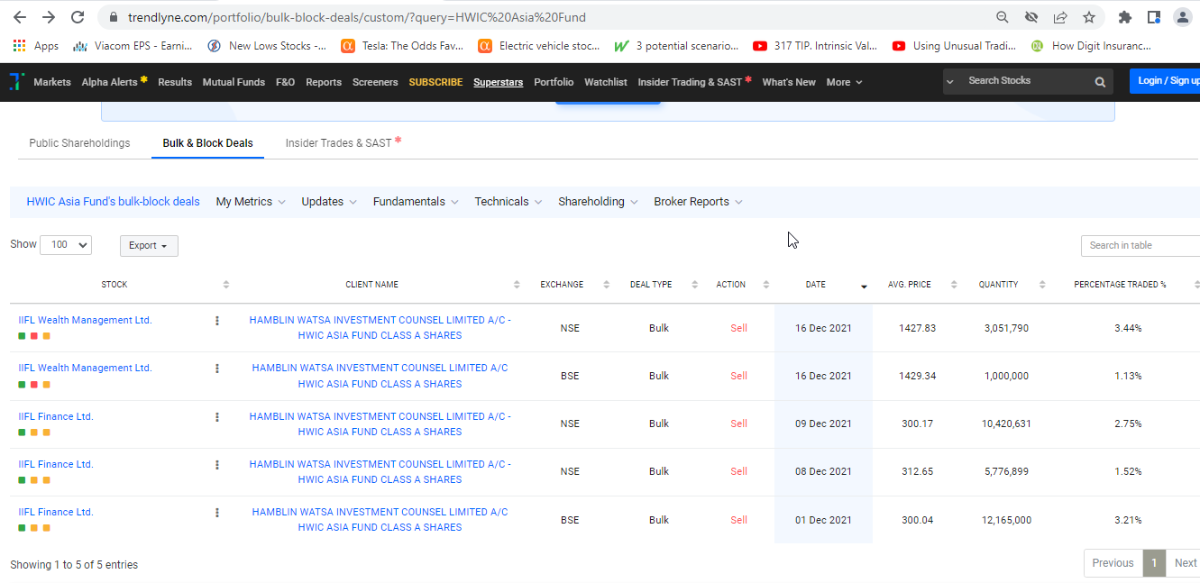

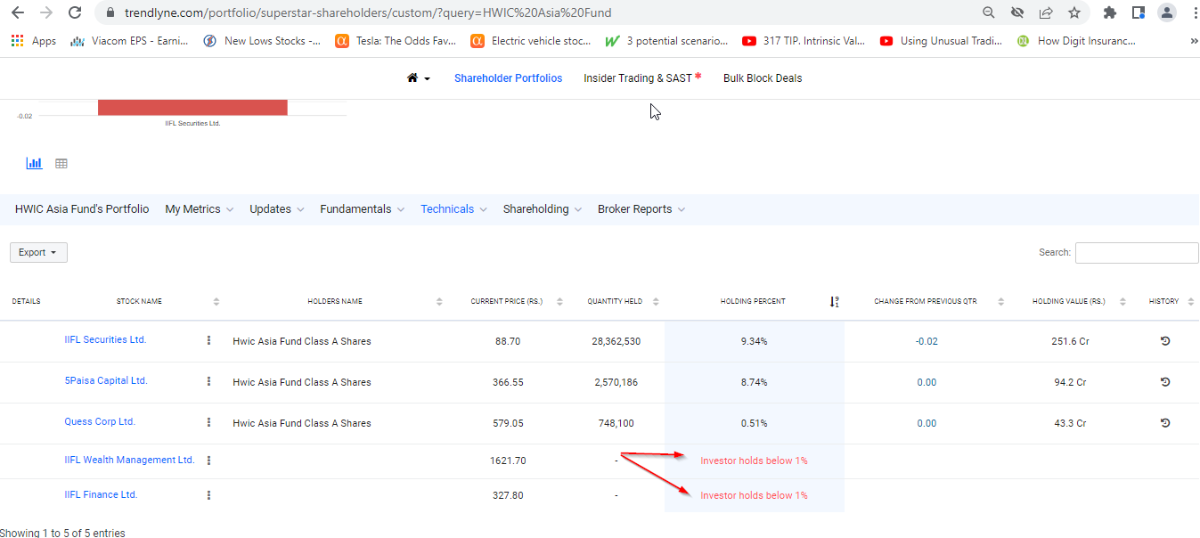

It looks like Fairfax Financial (via HWIC Asia) has reduced its direct holdings in IIFL Wealth as well as IIFL Finance during Q4 (while Fairfax India (via FIH Mauritius) holdings in both companies has not changed in Q4). So possibly they did this to raise cash to buy shares in Fairfax India directly, effectively to take advantage of that big discount to book & buy the underlying holdings (incl IIFL Wealth & IIFL Finance) effectively at a discount. Just a thought ... Now holds less than 1% in each

-

Digit is a high growth digital insurer with a sustainable business model (profitable on IFRS basis in year 3) - I wouldn't put Lemonade or Root in that category IMO - they are are losing bucketloads of money ,operating in very competitive, mature markets & have narrow product offerings. Look with Digit on valuation - gut instinct probably bit lower but not a drawdown of the size you have indicated. We may never find out for certain because Digit have indicated they don't need to raise capital now & also that they are better capitalised than a lot of their insurer competitors (which actually gives them a competitive advantage). Its worth noting too that Digit have increased their market share by around 25% from 1.6% (mar-21) to 2% (Jan-22) of non-life market so the underlying IV has grown since the time of July capital raise to current IMO I think this article probably makes some good points on your question https://www.insurancebusinessmag.com/us/news/technology/ceo-turns-back-to-private-markets-after-reverse-merger-derailment-324535.aspx “Now that the public markets are depressed, it’s causing valuations in the private market to be a little bit lower, but not quite as extreme, right?” In other words, the private markets continue to have an appetite for private technology investments, though they’re slightly more sober about it. “There’s still a lot of [venture capital] appetite,” Harper said.

-

looking at the 13F - no major changes among Fairfax's largest equity positions in Q4 from what I can see https://www.dataroma.com/m/holdings.php?m=FFH

-

Just on Ukraine - if Russia does invade there is real risk of asset seizures (which happened in Crimea) & this would impact Fairfax but not in a material way from what I can see. I genuinely hope the situation can get resolved peacefully obviously it would be terrible for the Ukrainian people. For Fairfax I see these assets at risk - Astarta - has large Ukrainian agri-industrial business - 28% ownership - Fairfax carrying value $65 mil Fairfax Ukraine - 70% ownership - shareholder equity 2020 $90 mil (GWP $144 mil) In terms of insurance liability exposure I would expect they would have the standard war exclusion clauses so not expecting issues on liability side but more the assets at risk - I don't know what assets Fairfax Ukraine has & whether they can be moved to friendlier territories. I am sure Fairfax has been making contingency plans either way.

-

correction - its US$160 so would be 30% of current share price

-

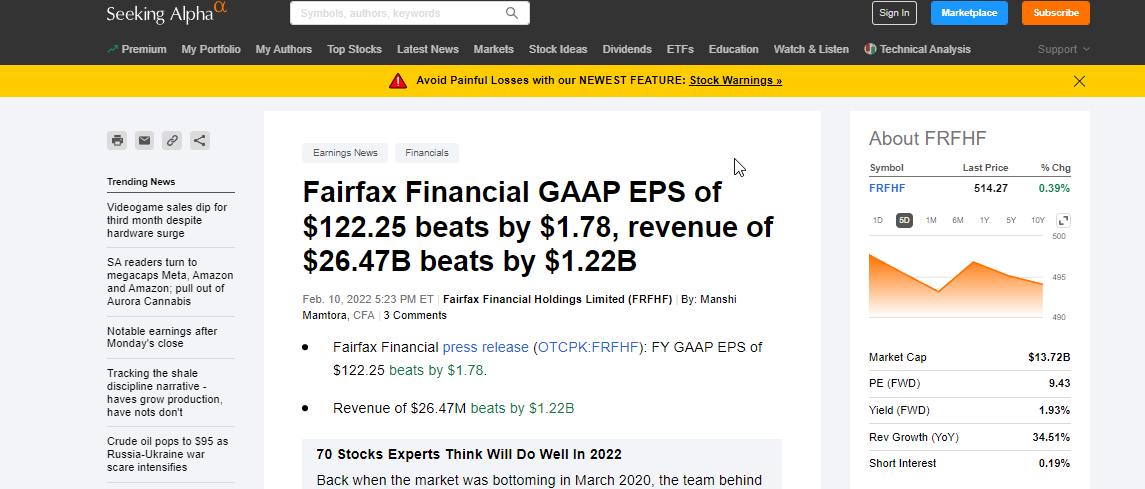

Talking about the narrative on Fairfax changing... WATSA’S STILL GOT IT Prem Watsa’s investing acumen powered Fairfax Financial in its latest quarter. While profit almost doubled in the company’s core property and casualty insurance and reinsurance operations, it was the US$938-million gain on investments that accounted for the lion’s share of earnings in the fourth quarter. For the year, investing gains surged to US$3.45 billion. We’ll keep an ear on what Watsa tells analysts in a conference call this morning. https://www.bnnbloomberg.ca/the-daily-chase-blockade-hammers-auto-sector-prem-watsa-flexes-investing-smarts-1.1721969 Also SA fixed the earnings release revenue number

-

Without looking at their numbers, Kamesh Goyal was interviewed recently & said they became profitable on an IFRS basis by the end of their 3rd year in operation.

-

It starts to get nuts when you start putting valuation on the remaining 90% interest If 10% sale resulted in $429 mil realised capital gain - a sale of remaining 90% (9 x $425 mil) could yield a further realised gain (over book value) of $3.825 bil - divide that by 23.9 mil shares & you get $160 per share which is 25% of Fairfax's market cap that is not reflected in Fairfax's book value. Even if you take a conservative view & dial that number down - or because its OMERS or whatever - it is still going to be significant number & that is just Odyssey - what about the other insurers that Fairfax owns?? If you do a valuation of Fairfax based on float per common share you start to get a snapshot of that value (maybe theres a chart worth doing there Odyssey had 28% NWP growth for 2021 & had 49.8% NWP growth in Q4! Its growing very fast & it has a very long, stable record of underwriting profitability. That really counts too!

-

yes good point SJ - I just wanted to strip it out so we could compare 2021 & 2020 to see any improvement in underlying CR - but to go back to your point which Prem just made on the conference call they believe their reserving is conservative - so their reported combined ratio probably understates how profitable the underwriting actually is & that is likely to manifest itself in fav develop in future years.

-

2020 CR 97.8 exclude catastrophe loss 4.7 (-) exclude covid loss 4.8 (-) add back net fav develop 3.3 (+) Underlying CR (excl catastrophe, excl covid, excl net fav develop) 91.6 2021 CR 95.0 exclude catastrophe loss 7.2 (-) exclude covid loss 0.3 (-) add back net fav develop 2.2 (+) Underlying CR (excl catastrophe, excl covid, excl net fav develop) 89.7 If we try & estimate 2022 CR Lets assume they continue the trend & reduce underlying CR down to 88.0 from 89.7. Lets assume 0.1 CR covid loss (reduced from 0.3 in 2021), 6.5 CR catastrophe loss (at higher end of range from 4.7(2020) to 7.2 (2021)), net fav development 1.0 (reduced from 2.2 in 2021 to 1.0 in 2022) Then you get estimate CR 93.6 for 2022 & would estimate underwriting profit for 2022 = $1.15 billion (est 18 bil net earned premium x (100-93.6)%) so I would agree with you guys @Parsad & @Viking - I think 93-94 range for CR looks about right for 2022

-

'At December 31, 2021 the company's insurance and reinsurance companies held $24.9 billion in cash and short-dated investments representing 50.3% of portfolio investments' I think they might have reduced their fixed income portfolio duration even more in Q4 39% at 31 Dec-20 44% at 30 Sep-21 50% at 31 Dec-21