Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Alright, how's this for some bush league idiocy? A couple days before the take private announcement I notice Fairfax trading at $500 per share. At the time I have about 2% of my portfolio in Atco, so I says to myself, self, you'll probably be able to sleep a bit better at night riding Fairfax from $500 to $1000 over the next few years than riding Atco from $11 to $25. And, you'll have one less security to keep track of. With that logic in tow I promptly sold out of my Atco stake - which I'd held for a long time - for around $11 and turned around to buy Fairfax at $500, only to learn that my brokerage no longer allows OTC trades! A couple days later the take private deal is announced, and by the time I had transferred cash to my other brokerage Fairfax was already up 7%! As the saying goes, a fool and his money are soon parted.

-

FYI - Vanguard no longer permits buying FRFHF, because it’s OTC.

-

They're for employee comp plans. I believe when they first appeared Prem said they were mostly for managers and would be earned over a long period of time. I'm assuming the vesting schedule extends beyond the more traditional 4 or 5 years, but I don't know the specific terms. Maybe 10% will vest annually, I don't know.

-

@Viking as always, THANKS for the fantastic analysis. One thing you may want to add into the spreadsheet is an assumption that the diluted share count will continue increasing by 200,000 to 250,000 shares annually (until prevailing trends change). 15%+ yoy growth of diluted share count is a bit disappointing, and certainly offsets a sizable portion of the benefits of the buybacks. Diluted shares: 2016: 0 2017: 689,571 +689,571 2018: 890,985 +201,414 2019: 1,159,352 +268,367 2020: 1,273,250 +113,898 2021: 1,503,931 +230,681

-

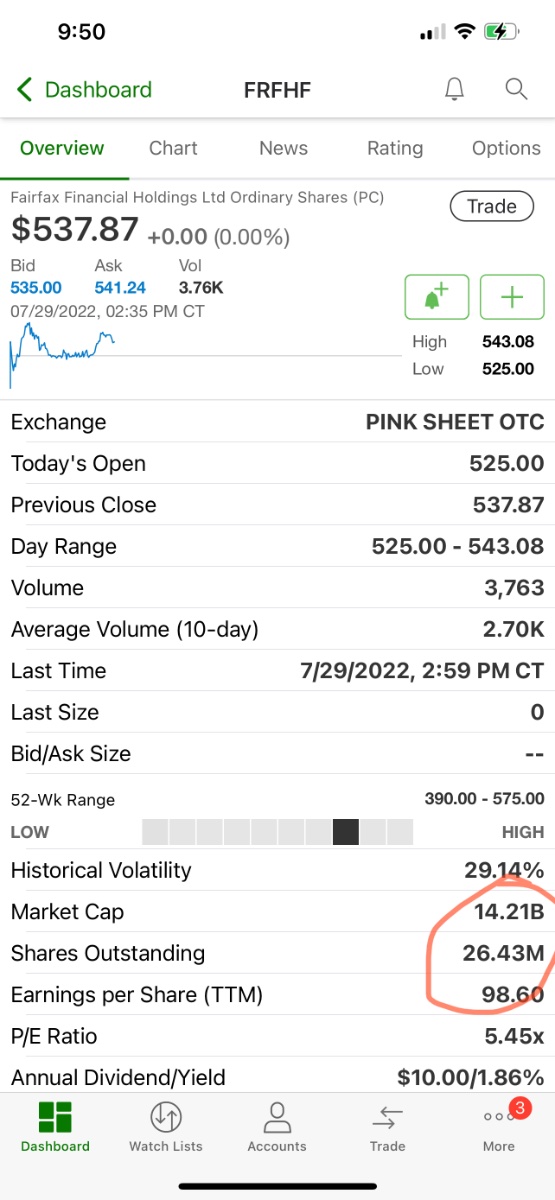

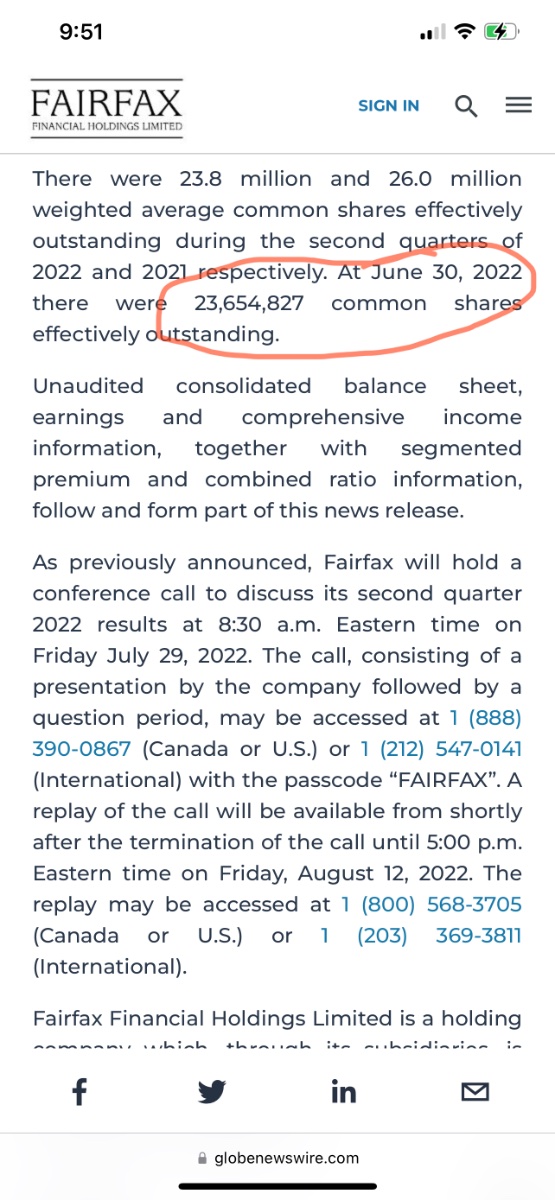

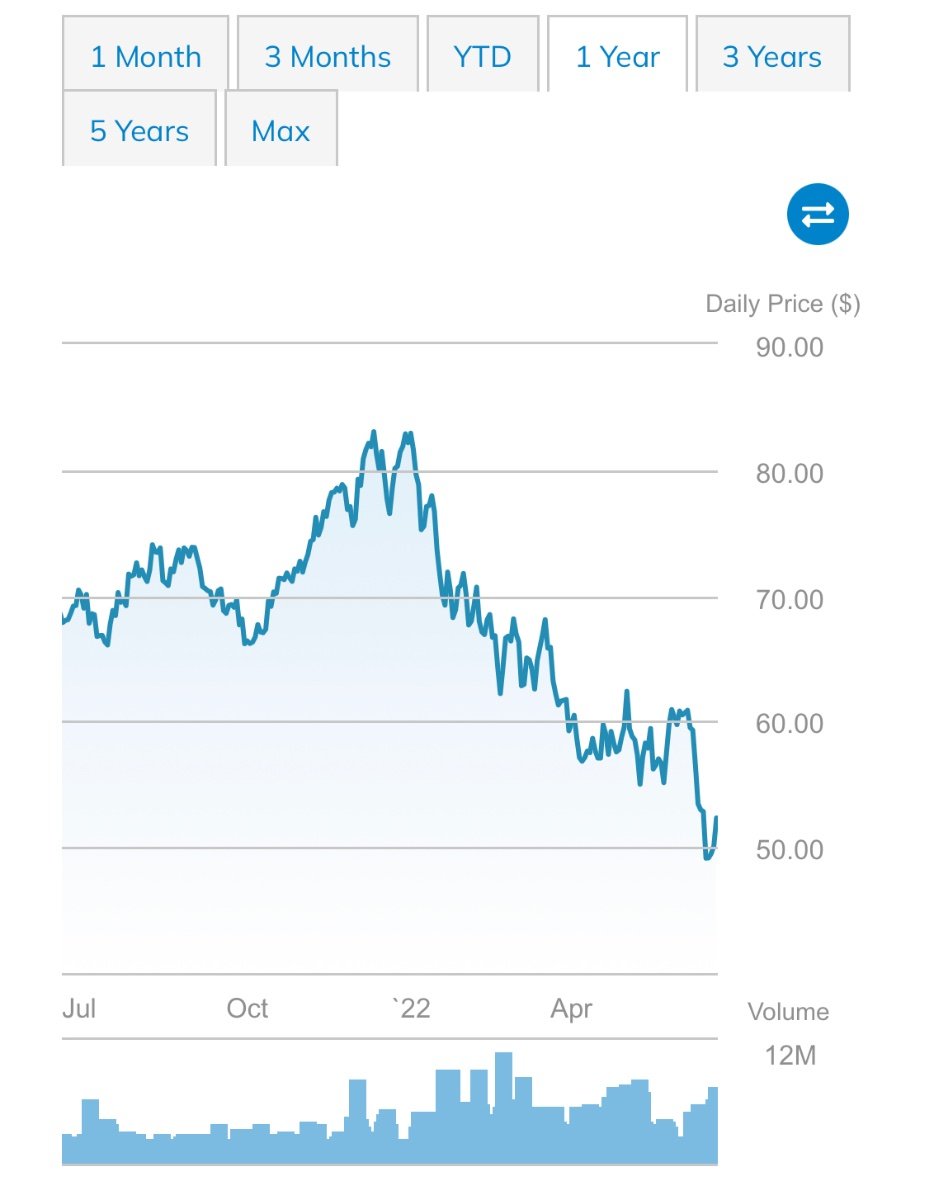

Dammit I’m officially irked. Yahoo shows FRFHF’s market cap at $13.57 billion, implying somewhere around 25 million shares outstanding. TD Ameritrade has the market cap at $14.21 billion and 26 million shares outstanding. Fairfax, obviously the official source, tells us there are 23,654,827 shares outstanding. If we multiply 23,654,827 actual shares by the actual share price of $537.87 we get an ACTUAL market cap of $12.7 billion! TD Ameritrade is overstating the value by more than 10%. This means Mr. Market technically believes that one of the best positioned insurers on the planet for this environment, which is earning roughly $2.5 Billion of operating income AND that will have $2 Billion worth of fresh free cash available as dry powder within the next six months (during a Hard Market) is Only worth $12.7 Billion! That’s downright crazy.

-

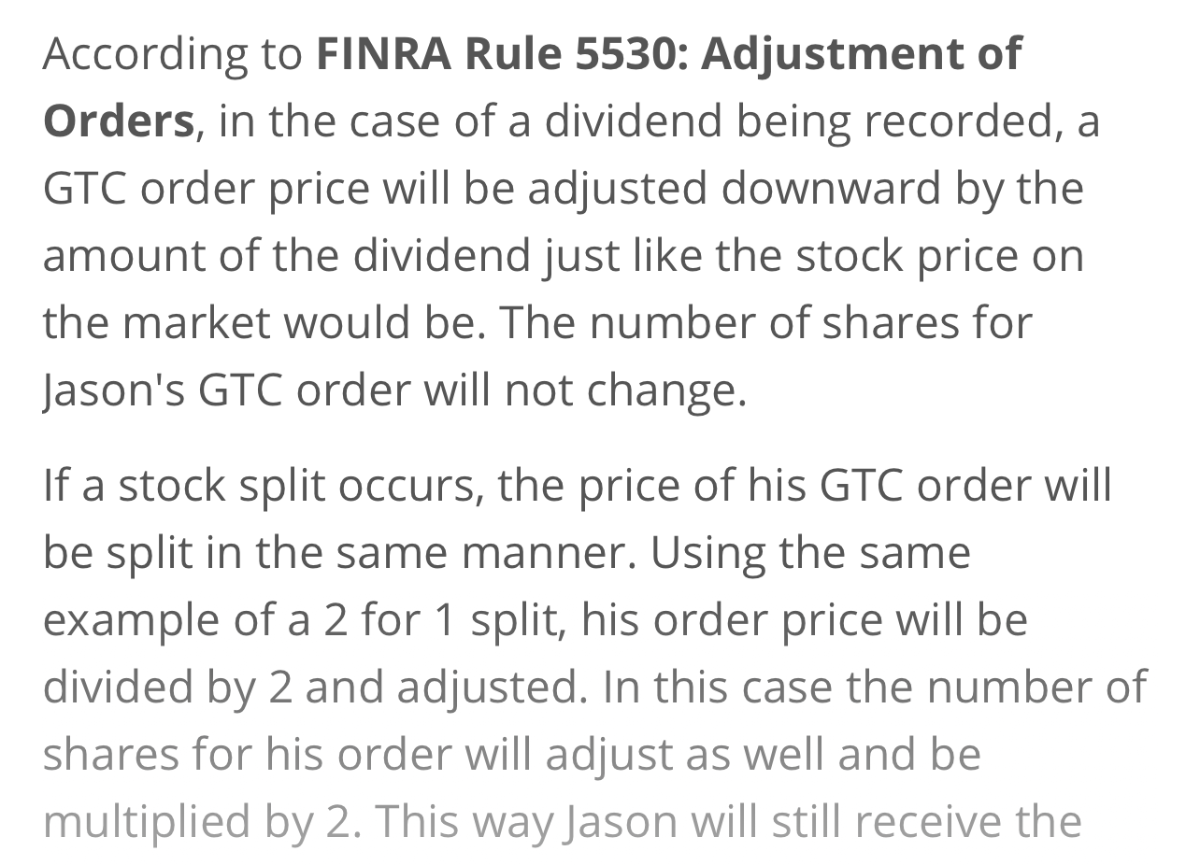

ok, just to continue this riveting conversation with myself I’ve found FINRA Rule 5530, which addresses the rules for adjusting orders in the event of a dividend or stock split. I haven’t been able to find specific guidance on how to handle changes to the number of outstanding shares, but logically exchanges should treat it the same as a stock split, which supports the idea that when the exchanges factor in the new share count we should see a solid bump in Fairfax’s share price.

-

I have some questions about how stock exchanges and Mr Market handle sizable share count changes: The timing and method of updating the number of shares outstanding is an area of stock exchange operations that I don’t fully understand. I assume when the share count is changed that the exchange simply takes the closing market cap and divides it by the new share count for the next day’s opening. (And open bids/asks are automatically adjusted as well.) ^ Question 1) is that how exchanges handle share count changes - closing market cap divided by new share count? For FFH I notice TD Ameritrade is showing a market cap of $14.21 billion and a shares outstanding count of 26.43 million. And a share price of $537. According the the latest quarterly report, as of June 30 the share count was materially lower than 26.43 million at 23,654,827. If you divide the current market cap of $14.21 billion by the new share count we see a share price materially higher than $537 at roughly $600. Question 2) When will the exchanges update the share count to reflect reality? Question 3) Should we expect a significant adjustment upward to the share price to around $600 when the share count is changed? Or is Mr Market already anticipating and pricing in the share count change in a way that we should expect something like a quick sell off and a market cap reduction after the adjustment? Altius recently experienced the reverse of this when it’s share count was significantly increased after Fairfax exercised its options. On the day of the share count adjustment the stock price immediately dropped around 10%. So it appeared Mr Market had not anticipated the share count change. That’s why I’m curious if we can expect a large share price increase for FFH soon when the shares outstanding count is reduced.)

-

Amen!

-

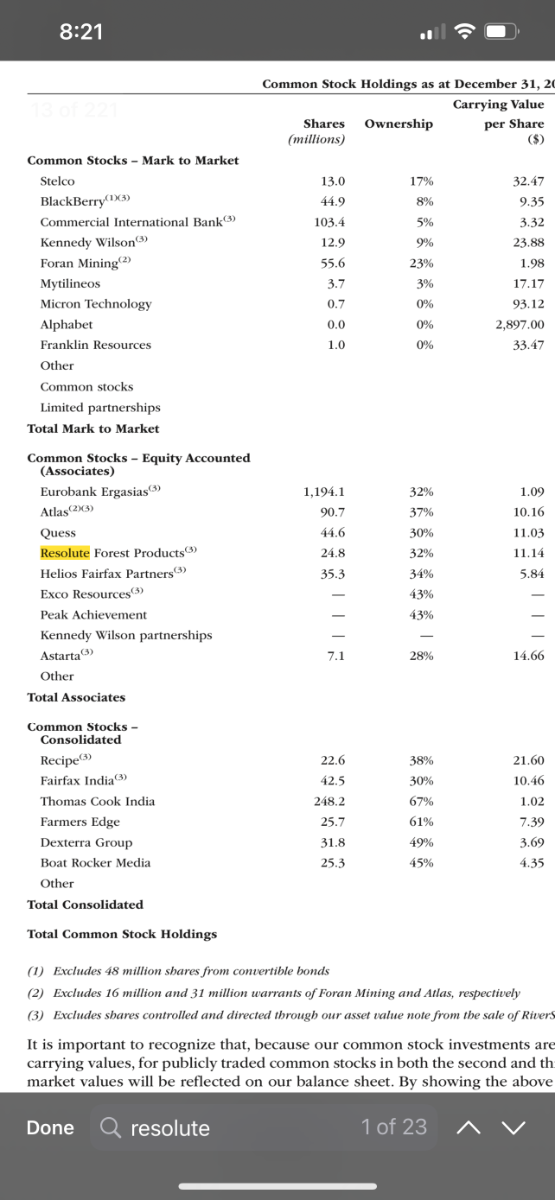

There it is. Thanks, @glider3834 Also, in the 2019 report Prem said they had net investment of $745 million in Resolute.

-

Note (3) in the annual report says: Excludes shares controlled and directed through our asset value note from the sale of RiverStone Barbados

-

Well, according to the annual report FFH owned 32% of the common as of the end of last year.

-

^ I believe FFH owns around 44%

-

I have a hall pass.

-

Yes! I thought about mentioning that in one of my rants. It’s not going to be easy to contend with.

-

The home builders have already been whacked. Down 40%. That’s a strong leading indicator of recession.

-

That’s good insight. That tells me two things. First, Sokol still endorses Abel even when he has little to gain. (Sokol is one of only a handful of people in the world who has really had to consider what would be required to run BRK post Buffett.) Sokol could have just as easily told your friend that he doesn’t envy anyone having to take on BRK post Buffett. Second, Sokol saying it will be worth buying BRK on the death dip assuming Abel will be in the captain’s seat is another implicit Abel endorsement. If Abel follows Sokol’s ruthless management by objectives approach, Ajit keeps the insurers humming, and if Todd and Ted ably source and evaluate deals, we may be able to replicate much of the Buffett brain.

-

I doubt it will drop below 1.2 or 1.0 times BV. Todd and Ted will be buying back shares like crazy.

-

Thank you for sharing this. I just read it. I'm still processing it. I think the comments about Abel's work ethic from Ron Olson probably added the most color to my perception. (Sokol said the same about Abel's work ethic, and I know Sokol is a Killer with a capital K, but Sokol Always has an agenda. So I take his input on this with a grain of salt.) My gut is when it comes to Abel we're looking at an affable fella who appears to be a top 1 percentile operator. In terms of likability, work ethic and competence I'm sure he compares favorably to most Fortune 500 CEOs. And, that in itself ain't a small deal. But! Here's what's strange. Buffett is a god - Full Stop. He is capitalism's-da Vinci-meets-Michaelangelo-meets-Mozart-genius-Freak-Of-Buffett damned-Nature). Is it too much to ask for his successor to at least be a demi-god? The mark of a great individual is an organization that fails in their absence. The mark of a great leader is an organization that is stronger 5 years after their gone. Do I think Berkshire will be stronger after 5 years with Abel at the helm? Meh, maybe, but almost certainly thanks to momentum, and not because of Abel. What does being a god look like? In the height of the tech bubble Buffett acquired one of the world's largest and most respected reinsurers (Gen Re), and its massive bond portfolio, using extremely overvalued shares of Berkshire Hathaway as the currency. It was one of the most ingenious business deals of all time. As part of the acquisition, Buffett bagged a gigantic portfolio of bonds for 50 cents on the dollar right before a) the financial world crumbled b) equity prices tumbled back to Earth c) demand for safe haven bonds skyrocketed Not long after the acquisition he recognized Gen Re had a large cache of financial weapons of mass destruction in the form of derivatives, and he forced Gen Re to unwind all of them - no matter what it took. He made that call well in advance of the Great Financial Crisis - starring, you guessed it, financial weapons of mass destruction! Furthermore, Buffett, drawing from his nearly Unmatched encyclo-fu@king-pedic memory recognized Gen Re's numbers were starting to lag the industry and Buffett fired the CEO - mind you, of one of the most respected insurers on the planet! (Buffett has historically been pretty ruthless about obvious underperformance. See Todd Combs being sent in to rescue Geico.) ^That is how a god manages a conglomerate worth hundreds of billions of dollars. It IS absolutely as befuddling and miraculous as rocket surgery. I don't know Abel personally. I have nothing against the guy. But, I'm still pretty certain he ain't a god. I'm not yet convinced he's even a demi-god. And, so, similar to @Parsad's BRK reservations, I believe BRK will outperform the S&P 500 as long as WEB is lucidly in the captain's seat. I'm not anywhere close to convinced it's "humanly" possible for BRK to outperform the S&P 500 for the next 3 or 4 decades. And, certainly not with Abel running the show. Is it possible to find someone better than Abel? God only knows.

-

Serious question. Is Greg Abel legit? And, if so, why do you believe he is? I can’t name anything outstanding he has done. Do we know for sure he isn’t just a “company guy” that has ridden the coattails of D Sokol - and the Midamerican management team Sokol put in place?

-

I Need a Laugh. Tell me a Joke. Keep em PC.

Thrifty3000 replied to doughishere's topic in General Discussion

Great news! My doc says I’m not a hypochondriac. I just think I’m a hypochondriac. -

^ with that said, I'm only about 10% cash right now. So, I'm not freaking out. Just enjoying the ride.

-

We're about six months into this decline. 2000 Tech Bubble: - It took TWO abysmal YEARS to slowly griiiiind down to a bottom. Then took about FIVE MORE years to revisit the tech bubble peak for about a split second. 2007 Housing Bubble: - It also took nearly TWO abysmal YEARS to slowly griiiind down to a bottom. Then took about FOUR MORE years to revisit and sustain the housing bubble peak. (During those bubbles the Fed had loads of fire power and readily jumped in to help.) 2021 Everything Bubble: (This time around the Fed has already accepted defeat on staving off recession. The Fed's out of ammo and believes its only option is to pick the economy's poison; either high inflation or high rates.) - After only six months, has the market fully baked in the implications? Or will it take TWO YEARS of declining purchasing power, bankruptcies and a sidelined Fed for Mr. Market to root his way to a bottom? It sure feels like we're still a bit ahead of our skis.

-

wow I didn’t even open the press release email when I got it because I assumed it was noise. Seems like a nice time to have an extra bil lying around. Bravo, FFH.

-

isnt there some risk of bonds being paid back at par while insurance claim costs increase with inflation?

-