Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

YASSS!! Now we’re talkin!

-

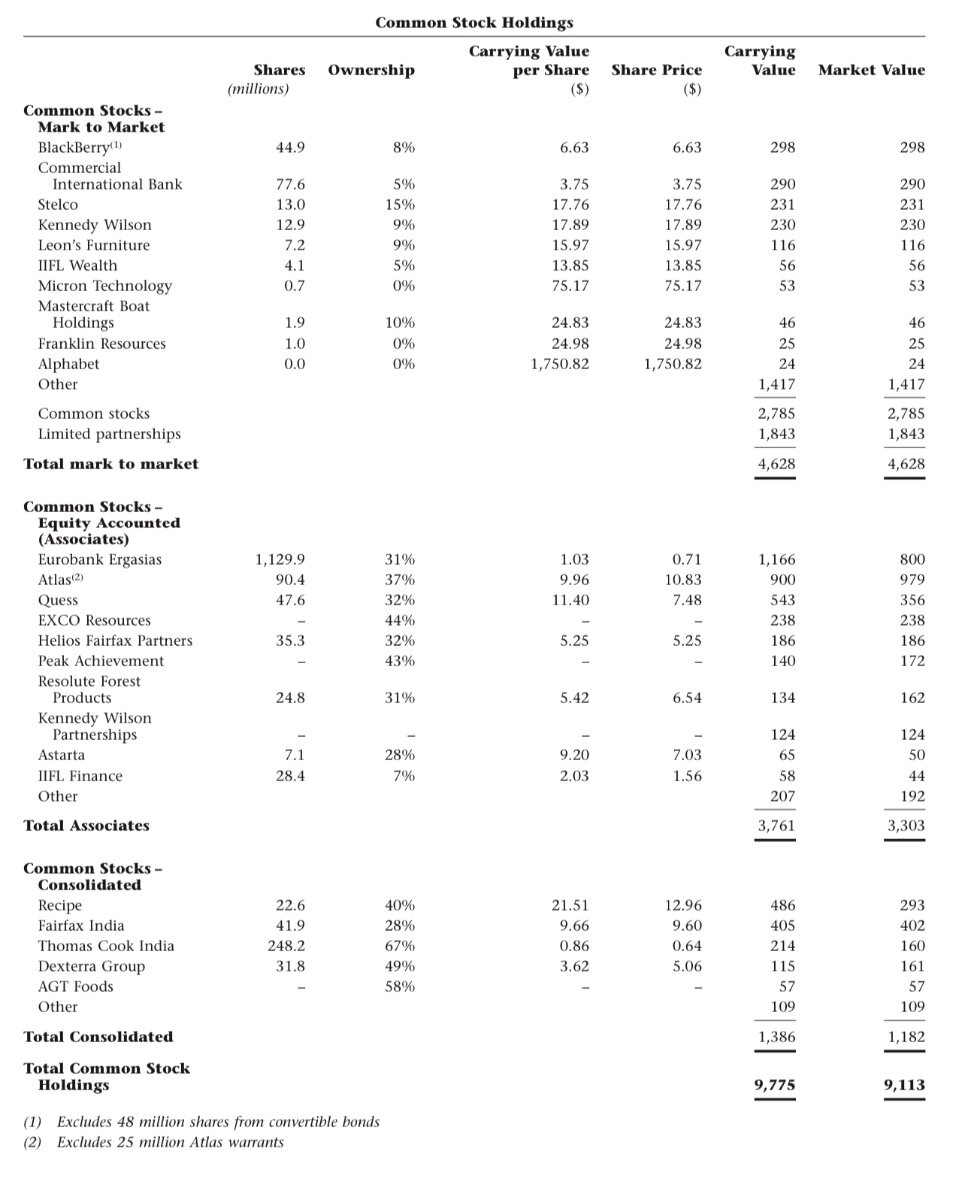

The dividend interest from bonds is baked into the $30 of after tax insurance earnings (which I discounted in attempt to strip out the dividends from the common stock holdings). It would probably be more useful if I separated insurance operating earnings from the dividends, but Viking has already done that in a couple of his recent posts forecasting 2022 insurance and dividend income. I believe his posts had something like $31 per share from insurance and $19 per share from dividends. But, I believe those estimates were pre-tax and I believe his dividend estimate included common stock dividends, which need to be removed if using the common stock look through earnings. So I felt like $30 per share was a reasonably conservative estimate of those two sources, but I'm open to suggestions.

-

Another one I wrestled with is Byron Trott's contribution. He has contributed an average of something close to $2 per share annually going back to 2009. I'm not sure if that can be baked into the go forward earnings or not. Byron still manages a FFH portfolio that was worth over $600 million at year end 2020. So, maybe $1 to $2 per share of look through going forward is reasonable.

-

I didn't include it because Resolute happens to be pretty far down the list in terms of carrying value. I'll be happy to edit my post and add Resolute's or any others' look through earnings that anyone wants to toss out. I do prefer normal or mid-cycle earnings for cyclical investments. Do you have any sense of what Resolute's "normal," mid-cycle, earnings might look like? (I know the TTM earnings have been pretty nuts.)

-

Aight, continuing down my FFH per share look through earnings line of thinking, I came up with rough look through earnings per FFH share estimates for FFH's 9 largest common stock positions (which constituted roughly half the 2020 YE carrying value of FFH's common stock portfolio). I quickly dug up comments on earnings - or free cash flow - from various sources (including this message board), and I divided by 26 million shares (because I'm optimistic on repurchases). Because it's really quick and dirty estimation, if I had a reasonable estimate of 2022 earnings I'd use that (thanks @Viking), if I only had Prem's comments on 2020 results I'd try to pin down the 2019 results and make a judgment call. On EXCO and Recipe I started with 2020 free cash flow and simply assumed 2022 would be 1 or 2 times better than their Armageddon performance (why I'll never be an accountant). And, for Fairfax India I just had to go with a crazy conservative number, because I've never been disciplined enough to pin look through earnings on that one down (believe me, I've tried). So, I'm basically throwing this out there in hopes someone far more disciplined than me will be frustrated by my inaccuracy and offer a more precise estimation (in other words I'm trying to provoke somebody else to do the hard work, which makes me just a slightly more sophisticated troll than Liberty is on the Altius board. Haha, love you buddy - you know it's true). I'll spare you my per-holding logic and just get to the point, here goes: (look through USD per FFH share - assuming 26 million shares. To add margin of safety I usually round down to the nearest $.50.) Atlas: $7 per FFH share Eurobank: $6 Fairfax India (???): $2 CIB 290: $1.5 Kennedy Wilson: $1 per EXCO: $1 Recipe: $1 Quess $.50 per Blackberry: $0 Total: $20 per share So, in addition to the $20 above, if we conservatively assume the after tax 2022 insurance earnings per share (without double counting dividend interest from the companies above) is $30 per share (see @Viking's recent analysis) then the look through earnings power from insurance and the 9 holdings above is approximately $50 per FFH share. Now, the 9 holdings above account for only half of FFH's common stock carrying value. The big question is what is the rest of the portfolio capable of earning on a per share basis. And, this is where I have a bit of a thesis... If the rest of FFH's assets (including the other half of the common stock portfolio) can earn as much as the 9 holdings above, then you are looking at total look through earnings per share in the neighborhood of $70 per FFH share. If you can assume Prem is a reasonably disciplined value investor determined to earn a 15% return over time then if you divide the estimated $70 look through EPS by the $450 share price you get a year 1 look through earnings return of 15.5% - thus exceeding the investment hurdle rate. In sum, a meaningful billion dollar buyback is looking like a gift from the investment gods, and Mr. Market is dumber than a brick on this one. EDITS: The Following Estimates Added After The Original Post BDT (Byron Trott): $1.5 Resolute: $2.4

-

So that’s another $6 of look through earnings per FFH share. Add that to expected earnings for the insurance ops and ATCO and FFH shares are beyond crazy-stupid-cheap (not to mention the earnings power of all the other assets). Hmm, could that be why FFH is trying to buy a huge chunk of shares back?

-

@Viking Do you know if anyone has been crazy enough to attempt a “normalized” look through earnings per FFH share forecast on the non-insurance investments? I mean, FFH’s portion of ATCO’s expected 2024 earnings alone is pretty interesting. If you add just that one to your insurance ops’ per share contribution then the current share price starts looking pretty nuts.

-

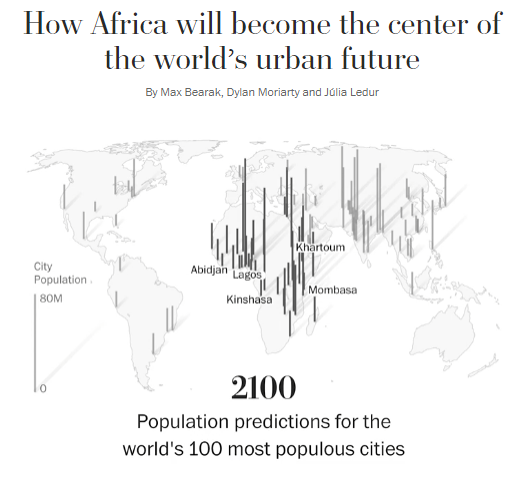

The next 80 years look pretty bright for Fairfax Africa and India. This graphic was in today's Washington Post...

-

Aww shucks. #Blushing Thanks for the shout-out @Viking! Given the continued progress on the non-insurance capital allocation strategy, the thesis on FFH still seems like a no brainer: a) FFH generates and allocates hundreds of millions of dollars of free cash annually, among b) a portfolio of insurance businesses capable of generating solid long term returns on capital c) a stable of non-insurance capital allocators that can earn double digit returns in their sleep - Burton, Sokol, Trott, etc. d) stock repurchases at a steep discount to intrinsic value ^ In a yield starved world full of greedy capitalists, can you guess which of those conditions I'm betting will no longer exist a few years from now? Haha.

-

@Viking and @Parsad how are you factoring in share count/dilution going forward? From 2009 to 2019 dilution was a pretty serious tax on EPS. Are those days behind us? I get they may have changed course on that recently, and some of the dilution may have been one time stock awards to incentivize long term managers. But, I dug up some of my notes from last year on this and the trend isn't in our favor: Annualized Share Growth Rate Approx 4% Diluted Share Count: 2009: 18,397,898 2010: 20,534,572 2011: 20,405,427 2012: 20,566,866 2013: 20,360,251 2014: 21,598,139 2015: 22,564,816 2016: 23,017,184 2017: 26,100,817 2018: 28,396,881 2019: 28,060,536 Share Based Awards 2009: 96,765 2010: 98,226 2011: - 2012: 240,178 2013: - 2014: 411,814 2015: 494,874 2016: - 2017: 689,571 2018: 890,985 2019: 1,159,352

-

Yeah, but who in the year 2000 DIDN’T see Amazon worth a few trillion by 2021?! Probably the same idiots that don’t know that in the year 2041 Amazon will be bought in bankruptcy court by HP-Neuralink! $hit I may have said too much.

-

Market Disconnect is One of the Craziest I've Seen in 23 Years!

Thrifty3000 replied to Parsad's topic in Fairfax Financial

Parsad! Shhhhh, you're spoiling the fun! Buy 'em back, Prem! -

It sounds 100% consistent with the strategy they've been executing over the last decade - establishing a diversified "portfolio" of capital allocators, each having demonstrated potential to outperform at multi-billion dollar scale (Fairfax India, Fairfax Africa, David Sokol, Byron Trott, Wade Burton, etc, etc). Out of a dozen or so allocators some will fail to impress. But, that doesn't matter. Fairfax only needs three or four to become true rock stars, and Fairfax will be able to shovel loads of free cash into the rock stars' piles for decades. The lackluster performers will fade out. It's the same strategy they implemented to build a handful of outstanding insurance companies. Consolidating capital and authority among a handful of the most talented insurance managers they could find. Now they're doing it with their portfolio of non-insurance capital allocators. I think it's brilliant. Definitely fun to watch. And, I think so few people get it. Imagine if you're Prem. Hmm... Do I give my next free dollar to a great insurance company in a hard market, or do I give it to Wade Burton, Byron Trott, David Sokol, and so on? Which proven opportunity to compound our investment at a high rate do we pick? What an incredible situation to be in! It's different than Berkshire's strategy, where Buffett was the primary capital allocator for most of the company's existence. Berkshire will soon be handing the capital allocation reigns to a portfolio of TWO capital allocators - Todd and Ted - of whom only one has shown an ability to outperform. This idea of nurturing a larger portfolio of capital allocators has been in the works for years at Fairfax. A beautiful example of ultra long term strategic thinking, IMHO.

-

This group (DRASTIC) is to the covid lab leak theory what Wall Street Bets was to the GME thesis: https://www.newsweek.com/exclusive-how-amateur-sleuths-broke-wuhan-lab-story-embarrassed-media-1596958

-

I have a hunch India's current covid wave will play out like prior waves have played out in other countries - like Italy and the US. Now that hospitals are at max capacity and global media has all eyes on India, governments will lock down, people will mask up/distance, and case loads will peak in a couple weeks. It will then take several weeks for cases to decline to the pre-wave level.

-

Bravo, Sanjeev! Thanks for making the effort to upgrade the site. Being a tech entrepreneur myself, I know full well how difficult it can be to migrate from one system to another. I'd be willing to bet you have some entertaining war stories. I once had an executive coach advise me that the best way to derail a prosperous career is to take the lead on an IT project. Haha. I know I've proved him right at least a couple times. I can already see there are some awesome and very valuable new features. I can't wait to dive in further. Many many thanks!

-

No, I think that time for Fairfax was back in 2003. The decision that we are no longer going to buy crappy insurers and turn them around led to the group of quality insurers they have today. The second part of that was making Andy Barnard in charge of all of the insurers. Even with Fairfax's more eclectic style of investing, the real culprit behind their underperformance has been due to betting against and shorting the market after 2009. They took advantage of the 50% correction, but started hedging and that really hurt their performance. Even with minimal exposure to the stock market, they would have done very well just in their bond investments, conglomerate investments and the equities they did invest in...excluding their shorts and market bets which cost them significantly. Maybe the decision to stop shorting is a step in the right direction...simplifying their portfolio decisions. Cheers! Sanj, please stop describing what FFH did as "hedging." More than 100% of FFH's equity portfolio was "hedged." When your hedge-ratio exceeds your exposure to the underlying (ie, more than 100%) that's called speculation. It was one of the investment decisions where the excessive position sizing reflected poor risk management. SJ They were bets on values regressing to the mean. Historically he was able to wait out Mr. Market and take advantage of volatility (see dot com and housing bubbles). Unfortunately, Mr. Market hasn’t cooperated for over a decade and Prem learned his lessons the hard way. Prem is smart. He learned. He’s not just another run of the mill, self-made, Canadian, multi-billionaire from India. And, he has formally, in writing, taken shorting off the table. I don’t think he is addicted to shorting or to shareholder lawsuits. This issue is easy to understand and was even easier to solve. He also knows he doesn’t have to juice earnings with shorts anymore, now that he has more good investment opportunities than he has capital (for the foreseeable future). Now, all he has to do is reward a bunch of all-star insurance and non-insurance managers/investors like David Sokol, Byron Trott, Wade Burton, etc if they can grow capital by more than 15%. If they can do it, they get more capital. If they can’t then they don’t. The real story of the last ten years was not the shorts. It was the global network of non-insurance capital allocators he has been assembling. The next ten years won’t look like the last ten years. And, the stock will trade above BV again soon enough.

-

+1

-

This is what’s going on. I wish I was joking... https://www.reddit.com/r/wallstreetbets/

-

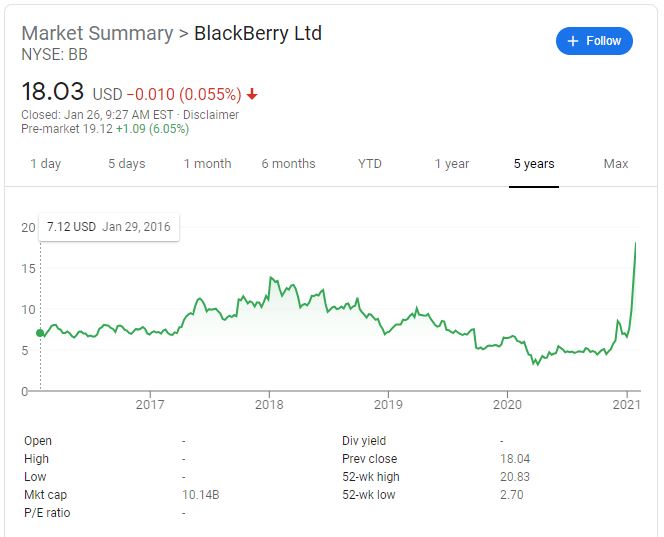

As a board member Prem could also be urging BB to issue tons of shares and build a war chest (like Tesla has done with their WSB-fueled lottery winnings).

-

"Dear Prem, Sell BlackBerry. Sighned, - God"

-

It looks like he bought at an average cost of $308 USD roughly or about $420-425 CDN per share. It says he bought in the last few days before the press release...I would imagine it was around the 9th, 10th, 11th and 12th, where the stock was around $425 CDN or less and volumes rose. If he is buying there, then I would imagine he is expecting a return of better than 15% annualized or more over the next few years. Cheers! The question then becomes is Prem expecting a 15% return a good predictor of future 15% returns. ...and one to ask: ''is 15% a realistic expectation?''. I am approaching a decade of holding FFH and I am seriously wondering if this is a realistic target as recent shareholders (10 years or less) are yet to benefit from such appreciation. It sure attracts new ( and naive) investors. I am tired of hearing the 30 years track record and while I focus on the last 10 years, I can only come to the realization that shareholders fell short of expectations. yeah , yeah ... I am still around and will for quite some time, but I needed to vent and share ;) Even during the depths of the hedge fund crisis, when Fairfax stock fell to $53 USD, I don't remember Prem buying shares in such a significant amount. Frankly, I'm shocked that he put $150M of outside capital into Fairfax...that would be a decades worth of dividends for him. And if he didn't borrow the money, I would imagine that's probably half his net worth outside of what is held in Sixty-Two Corporation. Then again, I've got half my net worth outside of Corner Market Capital in Fairfax and Atlas Corp right now, so maybe I shouldn't be surprised...and I'm very comfortable with both and think both have 50-100% upside over the next 2-3 years! Cheers! What is the thesis on ATCO? David Sokol

-

M2 Money supply growing at 28.4%

Thrifty3000 replied to LearningMachine's topic in General Discussion

wabuffo, thank you for a gracious, thoughtful, beautiful explanation. I'd like to first mention that a young guy named Nathan Tankus gained a lot of notoriety over the last year posting blogs explaining complexities of the financial system using the same kind of visual, T table-based, explanations you use. His fan base exploded when Bloomberg featured his blog in a story. You might like his posts: https://nathantankus.substack.com/ Also, just to be sure I'm correctly synthesizing the Hunt/Hoisington position with your explanation above, is it fair to say scenario 2 cannot legally happen independent of a corresponding tax receipt or treasury issuance? In other words, the government cannot legally create new private sector assets without taxing the private sector or increasing public sector debt to pay for those assets? Thus, making the Hunt/Hoisington case that deficit spending is near term inflationary (6 to 18 months) due to temporary supply constraints, but longer term deflationary, because the additional public sector debt decreases prospects for longer term private sector productivity/growth (as the private sector will be on the hook for servicing the additional debt). I believe this has been the ongoing rationale for Hoisington's position in long term treasuries - that the global, central bank-driven, debt explosion of recent years is long term deflationary. However, I believe in a recent newsletter Hoisington warned if the US congress legalizes scenario 2 above without requiring corresponding taxation/debt - aka legalizes true money printing - that all bets are off. Sounded like if that happened Hoisington would unload their long positions overnight, while expecting devastating, Weimar Republic-style, economic consequences (hence, the reason true US government money printing has been illegal thus far). -

+1

-

FFH average EPS: - 2005 to 2009: $33 - 2010 to 2014: $17 - 2015 to 2019: $28 - 15 year average EPS: $26 Still under the same management. Actually generates earnings over time and pays consistent dividends! (Not a money losing unicorn. Not a negative yielding bond.) Was recently selling for less than 10x very long term historical average earnings. Current price is slightly above where the CEO was willing to buy $150 million more. Unfortunately, it feels like bitterness from those who bought into the hype of 2005 to 2009 - paying close to $400 per share - is clouding a lot of judgment about the opportunities/risks presented today. People seem to want to vent frustration, while it seems a perfectly prudent investment is right in front of us. Maybe there should be a “Vent frustration with Prem” thread to provide therapy and isolate emotionally charged frustrations. Maybe a “Show love for Prem” thread too for balance. Haha.