Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Is there a value rotation going on today?

Thrifty3000 replied to BG2008's topic in General Discussion

I have a friend whose mom has boxes of Beanie Babies sitting in an attic that originally cost something like $16,000. Every time I see her mom I have the smart assed thought to ask how many divvies those babies paid out last quarter. I refrain. -

Added JD yesterday to round out my China basket. The basket is about 4% of my portfolio.

-

Is there a value rotation going on today?

Thrifty3000 replied to BG2008's topic in General Discussion

Don’t forget the impending crypto bust that will happen as soon as the greatest greater fool has placed their bet - and the crypto cult finally figures out how to discount all future cryptocurrency dividends to the present. -

Bought a basket of beat up AF Chinese stocks over the last few days. Around 1% position each. Will check back on how they’re doing in 5 or 10 years: BABA PDD TCEHY

-

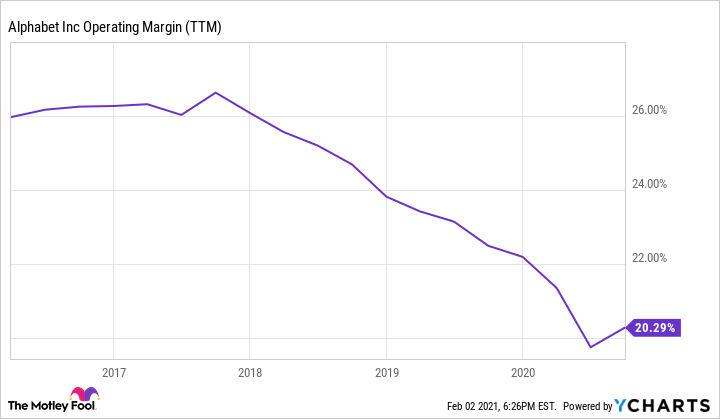

Here are some charts of Google’s margins. If Google’s price had dropped 50% in the last year I bet we’d be hearing a lot more about Google’s margins declining to zero.

-

Munger in 2019:

-

Thanks @ValueMaven! Yes, that’s what I’m talking about. I know bonds are a minuscule percentage of the portfolio today, but there was a time back when interest rates were a real thing - pre-2010 - when bonds regularly amounted to over 10% of the portfolio. And, yes, Buffett has been able to work some magic with special bond situations over the years. So, it occurred to me that if the whole interest rate concept ever becomes a thing again that we don’t really know who will be qualified to take the reins. Oh well.

-

Ok, this topic has been viewed nearly 300 times and no one has answered! No worries. How important could the bond portfolio be anyway? (Sarcasm alert)

-

I haven't looked into this in a while. Who is handling the day to day bond portfolio management for Berkshire Hathaway? Has there been any discussion of whether Todd and Ted will have any say in bond portfolio allocation post-Buffett? (I know Ted made a lot of money buying distressed debt pre-Berkshire.)

-

My bankers are amazing. I’m having them draw something up by COB. (Totally joking. I don’t have bankers. Haha.) My comment about selling puts was just some good-natured ribbing from one investor nerd to another - an attempt to goad mcliu into digging deeper on a contrarian thesis. Gosh knows this board could use some serious contrarian argument to combat the optimistic groupthink (count myself among the guilty optimists). But, at this point we have to dig deeper than superficial statements about the last decade’s performance. To improve our financial models I think we need to delve deeper into things like: - Prem’s succession plan - mid-cycle (post hard market) insurance earnings potential - reasonable/deserved conglomerate discount - reasonable/deserved discount for Watsa ownership structure Those are the kinds of factors that can materially impact future valuation. (And they make it hard for me to assign a value greater than 1x book until resolved or better understood.) The missteps and corrections made over the last decade have been pretty thoroughly debated in this and the other FFH threads.

-

If you keep that up you’re going to convince me to start selling puts.

-

I think normalized $60 per share earnings is reasonable. I also think $1000 per share valuation in the next 3 to 5 years is a decent bet.

-

Based on recent commentary on the Stelco board it sounds like we can conservatively pencil in, say, $.80 of look through EPS for Stelco. So, I’m updating the running list. Below are the estimated look through earnings per FFH share for 12 of the common stock positions (representing a bit over half the common stock carrying value): FFH Look Through Atlas: $7 per FFH share Eurobank: $6 Resolute: $2.4 Fairfax India ???: $2 BDT (Byron Trott): $1.5 CIB: $1.5 Kennedy Wilson: $1 EXCO: $1 Recipe: $1 Stelco: $.70 Quess: $.50 Blackberry: $0 Total: $24.60 USD

-

Man, I hope it does languish at $450. And, I hope FFH buys back 2 million shares a year at that price for the next 12 years. And, after that I hope they start paying out a $450 per share annual dividend on the last remaining 1 million shares (in perpetuity). Haha.

-

I agree. No way that deal is interest free. I’m hoping it’s more in the 5% or 6% range though.

-

Would be nice to know what kind of annual interest payment is attached to that Odyssey deal. if there’s no interest then this increases look through earnings per remaining FFH share by $4 or so dollars. (A very good outcome. Spending $40 per share to pick up a growing $4 per share.) If the interest rate is in the 10% range then look through only increases by maybe $1 per share. (A good outcome if non-Odyssey earnings grow a lot faster than Odyssey’s earnings.)

-

Ok, here’s what we have so far on rough look through earnings for 11 of the common stock positions (representing a bit over half the common stock carrying value): FFH Look Through Atlas: $7 per FFH share Eurobank: $6 Resolute: $2.4 Fairfax India ???: $2 BDT (Byron Trott): $1.5 CIB: $1.5 Kennedy Wilson: $1 EXCO: $1 Recipe: $1 Quess: $.50 Blackberry: $0 Total: $23.90 USD

-

Is that in USD? So, shall we say Resolute = $2.40 USD (look through earnings per FFH share)? That’s a pretty solid number.

-

Ok, so what number should we plug in for FFH’s look through earnings from Resolute? (Resolute earnings * Fairfax’s ownership percentage) / 25,000,000 shares = ?

-

I completely agree. I’ll definitely break it down per share if I can wrap my mind around it. I know Prem has offered clues for what to expect. For example, I believe he said in a normal market they’ll write premiums of around 1x book value (I think it’s book value). And, in hard markets they’ll ramp volume up to 1.5x book value. So, out of curiosity, I was trying to see what their premium volumes looked like after prior hard markets. Was there an obvious decline in premium volume from 1.5x book back to 1x book? Or did they hold premium volume steady and let book value grow to 1x? I know it’s getting in the weeds. I was just surprised to see a decade of completely flat premium volume, followed by a decade of a 10% CAGR (and 15% annually in the last 5 years). In the big picture we really just need a conservative growth rate estimate on premiums and a mid-cycle CR estimate in order to project normalized per share earnings potential.

-

Yeah, I started to go down that road, but I was actually trying to see if I could get a better sense of what to expect with the insurance ops and earnings after the hard market ends. So I’ll probably be looking at several other things pretty soon.

-

For those who think FFH should be judged on their last decade of performance check out the growth in net premiums written from 2000 to 2009 vs. 2010 to today. What if the lessons they learned from 10 years constructing their insurance capital allocation machine were applied over the last 10 years to non-insurance capital allocation? Step 1) Attract and retain great capital allocators over the course of several years. Step 2) Shovel free cash in the direction of the best performers.

-

So I was talking to a friend a couple days ago who is a major Boglehead-Vanguard-fanboy. He says Vanguard just shared the highlights of its upcoming annual global outlook report (my friend swears it’s a must read). Apparently Vanguard is warning that the current consensus expectation of the fed’s neutral interest rate staying in the 1.5% range over the next few years is too low. Vanguard research suggests rates will more likely land in the 2.5% range - to stave off inflation, etc. “Market expectations for a terminal rate around 1.5% are more than a percentage point higher than the Fed's current federal funds rate target of 0% to 0.25%. But they're below the Fed's 2.5% neutral-rate estimate and Vanguard's 2% to 3% neutral-rate estimate.“ I take interest rate projections with a grain of salt, but I’m assuming higher than expected rates will likely be mitigated by FFH on the whole via higher bond portfolio earnings, while knocking fifty to a hundred million of annual earnings off of Atco’s projections (I believe Atco was assuming 1.7% rates in their projected earnings).

-

I guess I didn’t make clear enough that I was just throwing out $30 as a random number for Digit and Ki - just to help make the point of how I think about wild cards. I probably should have said $X. Lesson learned. Haha. TBH, I haven’t gone through the trouble of putting an actual number on Digit or Ki yet (I just remember getting excited when learning about them during the annual meeting - and realizing they could be game changers). I owned a token amount of FFH for over a decade and watched closely as they fought to put together a solid non-insurance investment strategy. (I’ve written pretty extensively about their non-insurance strategy in the past). I loaded up on FFH during the Covid scare while FFH was in the mid 300’s. My original thesis didn’t factor wild card assets or hard markets in at all. Those are just icing on the cake as far as I’m concerned. I originally invested based on lower earnings and growth expectations than I have now (I also expected fairly heavy stock issuance/dilution to continue - which I don’t anymore). If FFH’s stock price ran up to maybe $1,400 per share in pretty short order (which ain’t happening, btw), that’s probably about the time I’d start taking a real hard look at the wild cards and assets like the Kennedy Wilson real estate, etc to see whether the stock was getting too far ahead of itself. Otherwise, as long as it’s priced somewhere south of $1400 per share, and it’s looking like earnings will average somewhere between $60 and $100 per share over the next 5 years, then I’m plenty happy to collect a nice div, defer taxes and hang on while book value and earnings grow. As always, I’ll expect the stock price to eventually catch up. I’m perfectly happy to ride this thing out long term - as long as shorts remain off the table and the business keeps developing the way it has been in recent years.

-

Great question. I definitely factor low earnings, high-growth, high-potential, assets like Digit and Ki into the valuation. I just look at those after I’ve nailed down all the predictable earnings streams. So, with FFH I start by estimating there’s $70 or so of predictable/knowable/quality look through earnings power in their portfolio. AND, it’s usually a good idea to spend some time looking at the sources of those earnings and make judgment calls about growth rates and ability to reinvest at decent returns. Is that $70 growing, stagnant or shrinking? After that I’ll look at the wild card assets like Digit and Ki. For those I have to rely on recent arms length transactions, management communications and expert analysis to gauge what the asset is worth and could be worth in the future. If I feel the valuations are purely speculative then I may choose to ignore them. If I feel there’s real and growing value, but no earnings yet, I’ll probably come up with a pretty heavily discounted per-share value. Just making up a number for Digit and Ki, let’s say I think they’re worth $30 per share. With an estimate of the predictable per-share earnings power, and a rough idea of the present value per-share of the non-earning growth assets, I feel pretty good about being able to look at the share price and decide whether a stock is a bargain or not. For example, if FFH is selling for $450 per share, and for that $450 you’re able to buy $30 worth of wild card high growth assets and $70 of real, relatively predictable, annual, growing, diversified, look through earnings it’s pretty easy to see that Mr. Market isn’t serving up all that many other opportunities like that these days. (And, as we value investors know, when you see opportunity you gotta be ready to act in a big way. Elephant guns.)