Thrifty3000

-

Posts

637 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Trading Fairfax Financial (FRFHF) on Vanguard

Thrifty3000 replied to JGBRK's topic in Fairfax Financial

Well, good luck with that. Vanguard treated me like garbage when I asked to speak to a manager about FFH. And, I wasn’t rude or anything. I was just shocked when I said I would likely transfer my existing FFH shares (not a small number) to another brokerage that trades FFH, and the kid basically just says, “so, is there anything else I can do for you?” (I’m sure Bogle flipped in his grave.) In contrast, Ameritrade treats me like royalty and I have less than 15% of my portfolio with them. (Though that’s changing every time I pick up more FFH.) I say hold your Vanguard ETFs and Mutual funds in a Vanguard account, so you don’t get charged extortionist transaction fees. But, move everything else to a brokerage that actually cares about keeping your business. #cancelVanguard haha -

Trading Fairfax Financial (FRFHF) on Vanguard

Thrifty3000 replied to JGBRK's topic in Fairfax Financial

Hear, hear! -

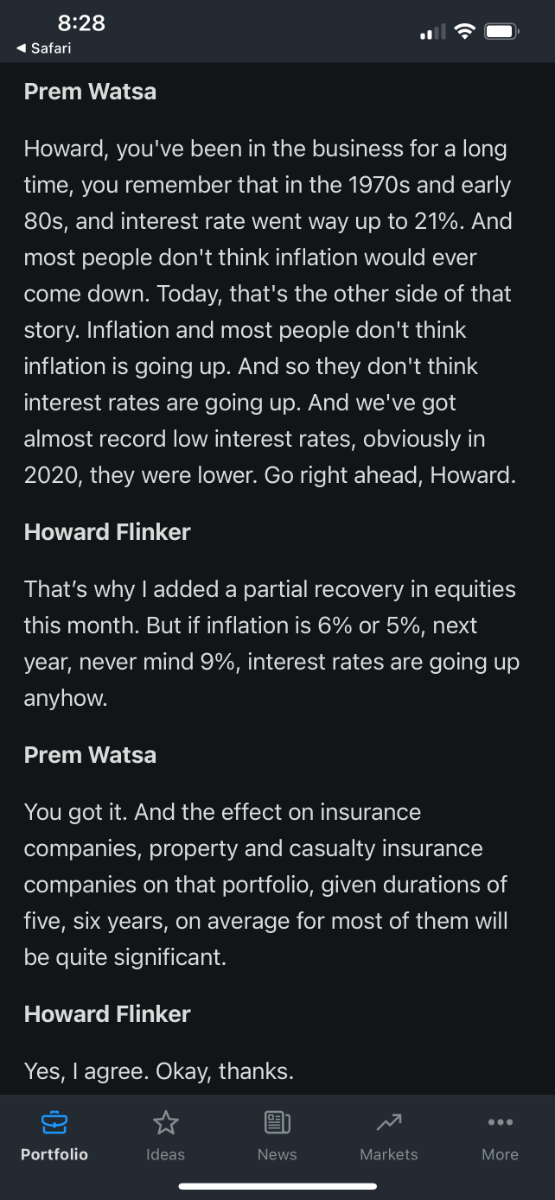

@Viking all this interest rate and inflation talk begs the question, have you factored in higher interest expense for FFH into your model going forward? Curious what interest expense per share is today and what it could look like when FFH's debt rolls over. (Actually, I think you've mentioned you assume combined ratio and interest rates will correlate in a way that allows overall earnings to remain reasonably protected.)

-

I’m with you there. I read Hoisington religiously (after popping a few Prozacs haha). For years Hoisington has laid out the case for the forces and trends that will continue pushing long term interest rates lower. Too much debt, too much debt, too much debt. And, they have not faltered on that thesis. They have, however, called out the one scenario they watch for that would have them unload all their long term treasuries in a heartbeat. That is, in short, if congress passes a law legalizing banana republic style money printing. Recently, however, their letters have discussed the near-term implications of the extraordinary fiscal/monetary response to the pandemic. Their position is if the government doesn’t intervene further then we’re looking at a painful recession that has already started. But, if we have a painful recession and the government follows the same playbook used during the GFC and the pandemic, then we’re looking at more near-term inflation and volatility. Hoisington doesn’t have any reason to believe the government will exercise restraint. So, Hoisington is calling for ever more extreme cycles of volatility until the government and the Fed get back on the rails of the original Fed mandate. And, they’re calling for increased risk of banana republic style inflation. Hoisington has the luxury of not having to do anything about near term volatility, as long as their investors trust them. They can hold long term treasuries through the short term cycles, and benefit from the long term deflationary trends. Prem doesn’t have the luxury of ignoring short term volatility, because it can disrupt insurance underwriting capabilities - as is being seen throughout the insurance industry this year. In short, I think Prem and Hoisington can maintain the same long term outlook, but have to position their portfolios differently to navigate near-term volatility and risk. Here is Hoisington’s conclusion from their most recent letter… “Monetary considerations coupled with these real side indicators point to recession and a reduction in inflation and long-term Treasury bond yields. If the Fed stays within the scope of the Federal Reserve Acts, they will have difficulty in containing the recession and fostering a recovery. But that situation puts us on alert to the possibility that the Fed returns to a Pandemic type of response that generated an inflation rate far above their target, as the experience of the past two years has so painfully taught. The economy might recover temporarily, but the expansion would be interrupted by another cost-of-living crisis and the Fed would not achieve either of its mandates for employment or inflation.”

-

This is from the earnings call in July. Prem may expect long term deflation, but it sounds to me like near term inflation risk is top of mind these days…

-

Yeah, I think we have to rule out seeing FFH reach for yield on the bond front. Prem believes strongly in regression to the historical mean when it comes to interest rates. So, I expect we won’t see them make any aggressive moves unless they find some yields that are at least a standard deviation above historical norms. Prem has mentioned a number of times how scary it was in the 80’s to invest in bonds thinking you were getting a great rate (at 7%, 8%, 10%, etc) only to watch yields continue climbing above 15% with seemingly no end in sight. He doesn’t want to be in that situation.

-

Yes, FRFHF. I don't appear to have the ability to trade FFH.TO in my account.

-

Vanguard allows US clients with personal accounts to continue owning it, they just won't allow you to buy more going forward. It's a recent policy that wasn't in place when I bought the bulk of my shares in 2020. I'm sure Vanguard still holds FFH in its international ETFs. And, it may still execute over the counter trades for professional clients. I assume they stopped allowing OTC trades after they went to a zero commission model. I noticed my other brokerage, which has a mostly zero commission model, does actually charge several dollars per OTC trade.

-

@Viking I agree with your reasons for it being undervalued. A couple other factors... 1) I've also always assumed there would be a permanent, deserved, discount because of the dual share class structure giving control to the Watsa gene pool. I'm not sure how to quantify it, and I'm sure there will be times when Mr. Market overlooks the risk, but it's a relevant factor nonetheless. Probably not a bad idea to knock 10% to 20% off of a DCF or sum of the parts valuation to factor it in. (Some children of billionaires do a perfectly fine job selecting good operators to run the family business. Other children of billionaires go bat$hit crazy.) 2) This is actually more of a question. Will there be a liquidity/visibility discount for not being listed on the NYSE anymore? I'm curious if that takes it off the radar of a lot of algorithmic traders and ETFs. Furthermore, I know firsthand Vanguard won't even let US clients purchase Fairfax. That has to sting a bit. It seems we're left with the handful of value investors that do their own independent research and thinking to support the value of Fairfax; many of whom were burned holding Fairfax over the last decade. ^ that's why I think we may need a couple years of solid book value growth before Fairfax starts showing up on stock screens and garnering attention from more big money managers. In the meantime I hope the price stays crazy discounted while FFH buys back hand over fist.

-

When it was $265 I was forecasting Fairfax earning $28 per share annually with earnings growth modestly outpacing inflation. That was based largely on their earnings of the prior 5 years and their share dilution trends. I invested a lot around $250 per share because I thought there was a decent chance Prem wouldn't repeat past sins, earnings would outpace expectations, and the share price could double within 5 years. Boy, were my earnings and share dilution projections off. I'm now more in the same camp as Viking as far as future expectations. So, I think FFH has hit its stride, and it will be a lot of fun to hold for the next few years. I also think $500 per share today represents about the same discount to my future expectations as $250 did when I first backed up the truck.

-

To further expound, BRK will probably be a ready buyer of ATCO for $10+ billion in a few years.

-

It just hit me what the next few chess plays might look like once Sokol is drawn even deeper into the FFH sphere after the Atco deal. First, Sokol gets a board seat at Fairfax, and it comes with some kind of rich, share-based, incentive to be more involved with operations and deal-making than just being a board member (but, it won't come with a formal operational title). Second, within 5 years we'll start seeing some sweetheart deals involving both BRK and FFH, because at that point Greg Abel will be rewarding his old buddy D. Sokol for sourcing the much-needed ideas.

-

Alright, how's this for some bush league idiocy? A couple days before the take private announcement I notice Fairfax trading at $500 per share. At the time I have about 2% of my portfolio in Atco, so I says to myself, self, you'll probably be able to sleep a bit better at night riding Fairfax from $500 to $1000 over the next few years than riding Atco from $11 to $25. And, you'll have one less security to keep track of. With that logic in tow I promptly sold out of my Atco stake - which I'd held for a long time - for around $11 and turned around to buy Fairfax at $500, only to learn that my brokerage no longer allows OTC trades! A couple days later the take private deal is announced, and by the time I had transferred cash to my other brokerage Fairfax was already up 7%! As the saying goes, a fool and his money are soon parted.

-

FYI - Vanguard no longer permits buying FRFHF, because it’s OTC.

-

They're for employee comp plans. I believe when they first appeared Prem said they were mostly for managers and would be earned over a long period of time. I'm assuming the vesting schedule extends beyond the more traditional 4 or 5 years, but I don't know the specific terms. Maybe 10% will vest annually, I don't know.

-

@Viking as always, THANKS for the fantastic analysis. One thing you may want to add into the spreadsheet is an assumption that the diluted share count will continue increasing by 200,000 to 250,000 shares annually (until prevailing trends change). 15%+ yoy growth of diluted share count is a bit disappointing, and certainly offsets a sizable portion of the benefits of the buybacks. Diluted shares: 2016: 0 2017: 689,571 +689,571 2018: 890,985 +201,414 2019: 1,159,352 +268,367 2020: 1,273,250 +113,898 2021: 1,503,931 +230,681

-

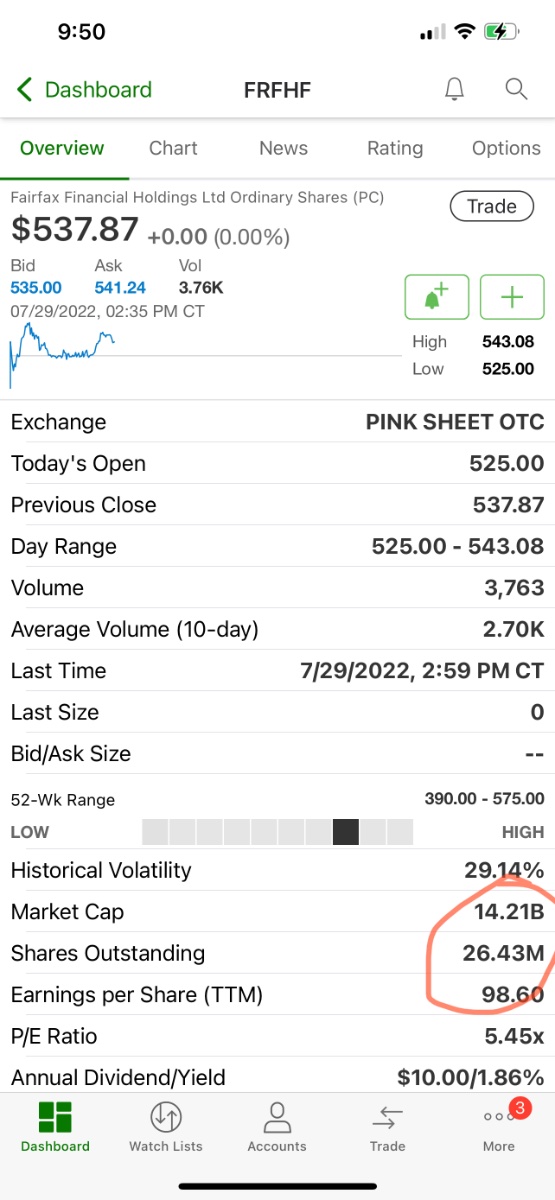

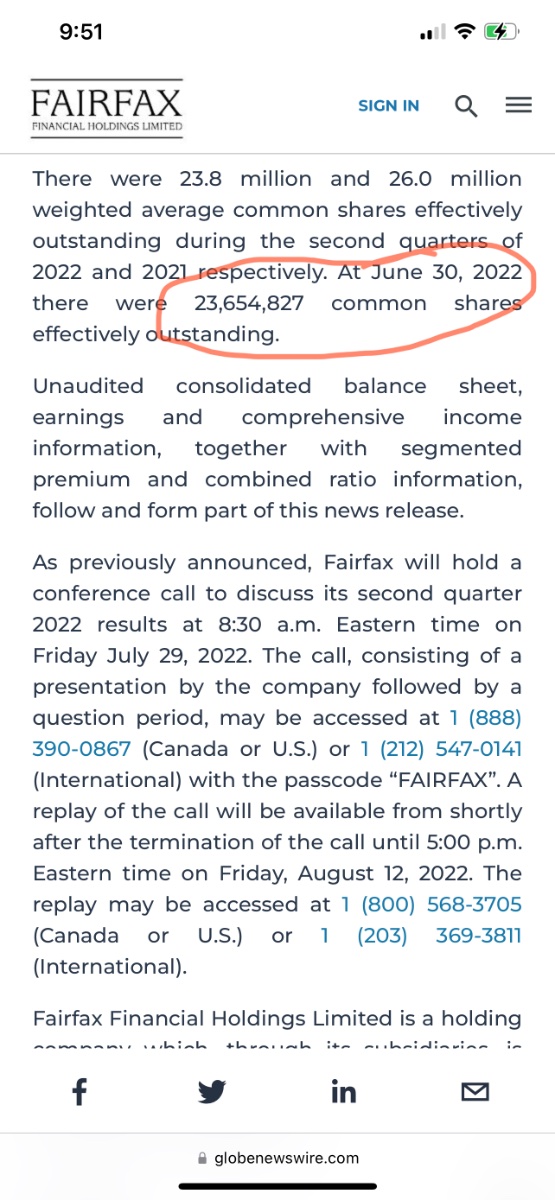

Dammit I’m officially irked. Yahoo shows FRFHF’s market cap at $13.57 billion, implying somewhere around 25 million shares outstanding. TD Ameritrade has the market cap at $14.21 billion and 26 million shares outstanding. Fairfax, obviously the official source, tells us there are 23,654,827 shares outstanding. If we multiply 23,654,827 actual shares by the actual share price of $537.87 we get an ACTUAL market cap of $12.7 billion! TD Ameritrade is overstating the value by more than 10%. This means Mr. Market technically believes that one of the best positioned insurers on the planet for this environment, which is earning roughly $2.5 Billion of operating income AND that will have $2 Billion worth of fresh free cash available as dry powder within the next six months (during a Hard Market) is Only worth $12.7 Billion! That’s downright crazy.

-

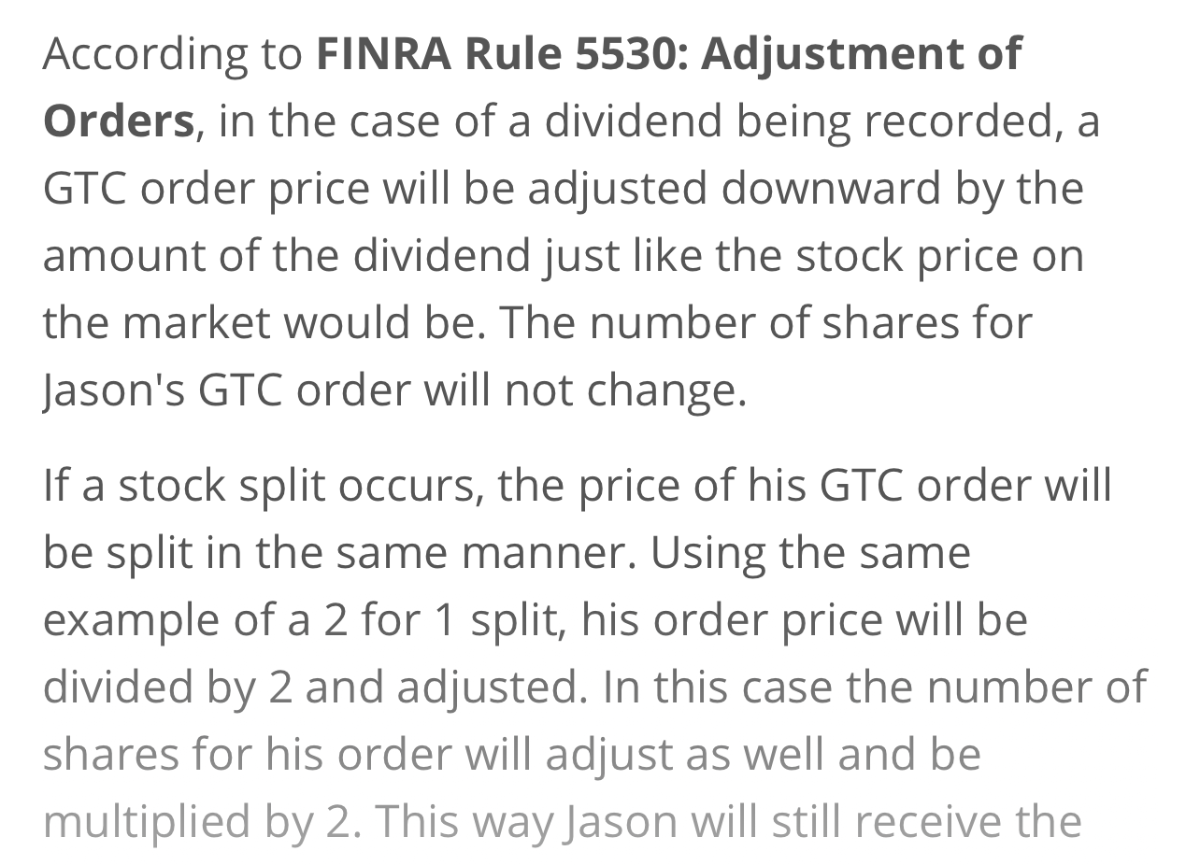

ok, just to continue this riveting conversation with myself I’ve found FINRA Rule 5530, which addresses the rules for adjusting orders in the event of a dividend or stock split. I haven’t been able to find specific guidance on how to handle changes to the number of outstanding shares, but logically exchanges should treat it the same as a stock split, which supports the idea that when the exchanges factor in the new share count we should see a solid bump in Fairfax’s share price.

-

I have some questions about how stock exchanges and Mr Market handle sizable share count changes: The timing and method of updating the number of shares outstanding is an area of stock exchange operations that I don’t fully understand. I assume when the share count is changed that the exchange simply takes the closing market cap and divides it by the new share count for the next day’s opening. (And open bids/asks are automatically adjusted as well.) ^ Question 1) is that how exchanges handle share count changes - closing market cap divided by new share count? For FFH I notice TD Ameritrade is showing a market cap of $14.21 billion and a shares outstanding count of 26.43 million. And a share price of $537. According the the latest quarterly report, as of June 30 the share count was materially lower than 26.43 million at 23,654,827. If you divide the current market cap of $14.21 billion by the new share count we see a share price materially higher than $537 at roughly $600. Question 2) When will the exchanges update the share count to reflect reality? Question 3) Should we expect a significant adjustment upward to the share price to around $600 when the share count is changed? Or is Mr Market already anticipating and pricing in the share count change in a way that we should expect something like a quick sell off and a market cap reduction after the adjustment? Altius recently experienced the reverse of this when it’s share count was significantly increased after Fairfax exercised its options. On the day of the share count adjustment the stock price immediately dropped around 10%. So it appeared Mr Market had not anticipated the share count change. That’s why I’m curious if we can expect a large share price increase for FFH soon when the shares outstanding count is reduced.)

-

Amen!

-

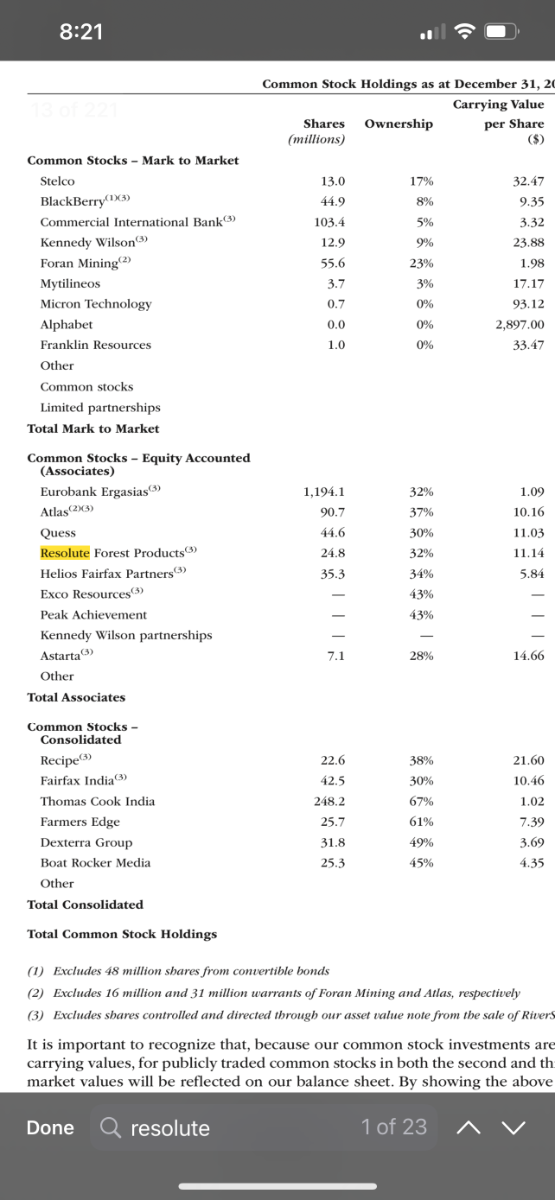

There it is. Thanks, @glider3834 Also, in the 2019 report Prem said they had net investment of $745 million in Resolute.

-

Note (3) in the annual report says: Excludes shares controlled and directed through our asset value note from the sale of RiverStone Barbados

-

Well, according to the annual report FFH owned 32% of the common as of the end of last year.

-

^ I believe FFH owns around 44%

-

I have a hall pass.