Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

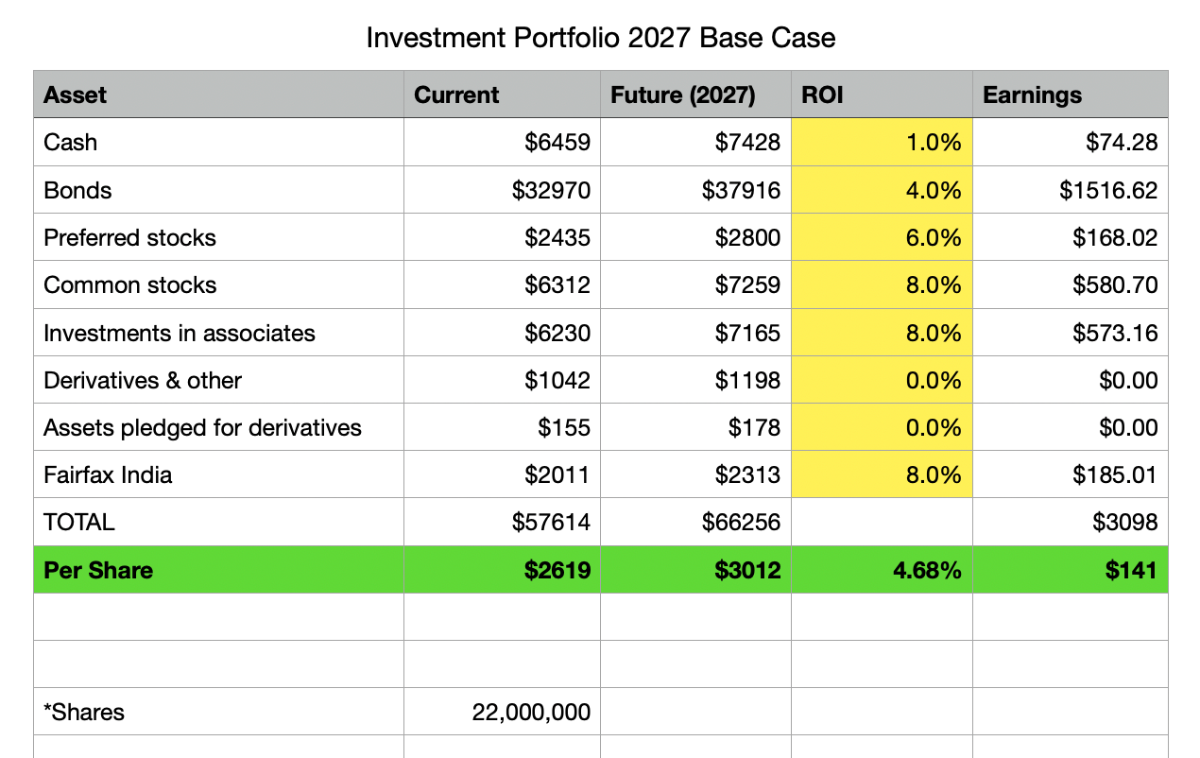

Now, if we fast forward to 2027, and project a scenario where the hard market has cooled and short term interest rates have moderated, we could easily be looking at something more like this (I simply increased each asset class by a total of 15% to account for 3 years of conservative growth, and I reduced the share count a bit)... 4 years from now, after the cliff of locked in near term interest rates has past us by, the portfolio will still be able to produce $140+ per share without needing to do anything spectacular from an investment standpoint! You can add, say, $10 to $50 per share for insurance underwriting profits and we really are looking at the normalized 20% returns @Viking has been proclaiming. And, again, the all star investment team barely has to show up to work to produce the kinds of returns I'm forecasting. These estimates are probably too conservative.

-

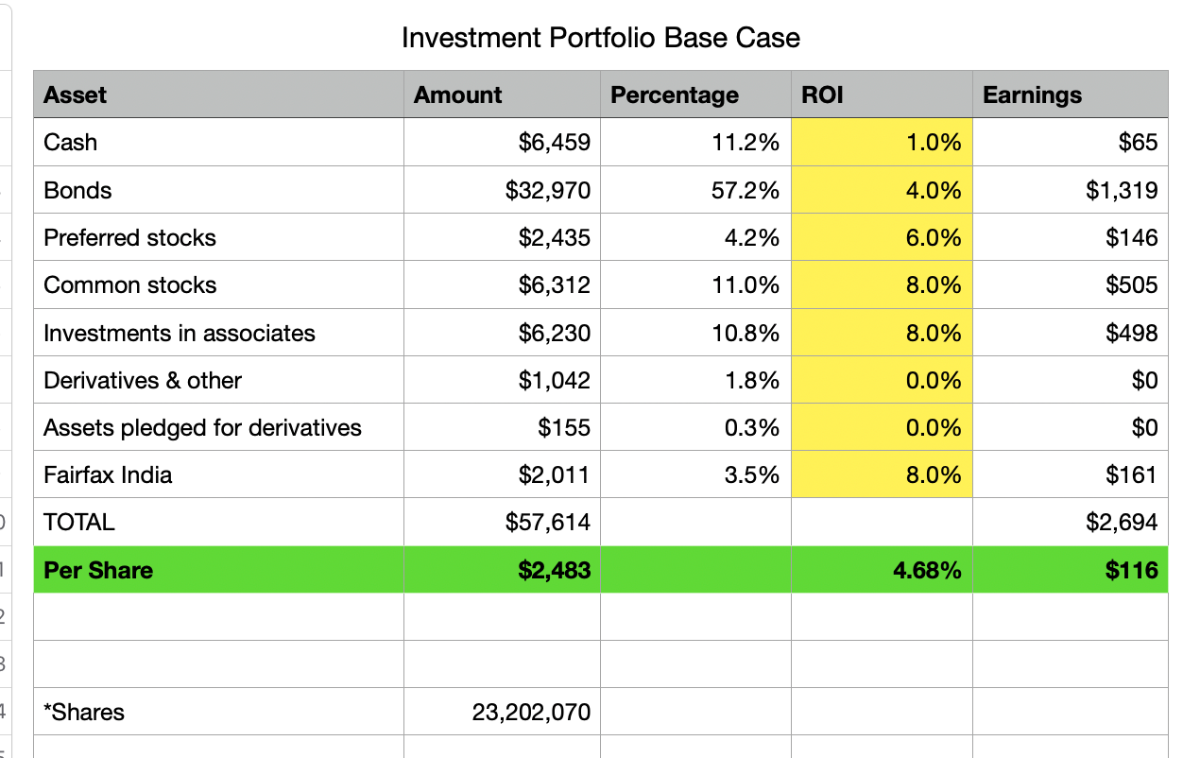

By gum, I think I'm starting to see eye to eye with @Viking on this argument that FFH is selling for around 5X normal earnings - and not 5X temporary hard-market-induced inflated earnings! Here is what the current investment portfolio would look like with very conservative ROI estimates for each asset class (ie. 1% ROI on cash instead of today's 5%). Notice that even with conservative ROI estimates the contribution per share would be $116.

-

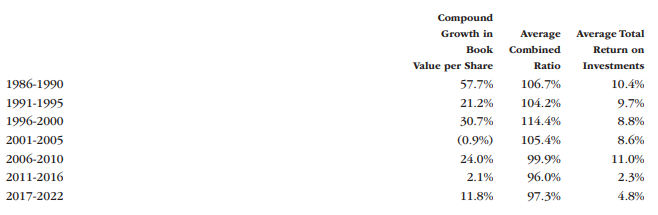

When thinking about FFH's longer term EPS potential I have to frame it more like... Over the next 10 years will average annual EPS exceed: $100 USD (almost certainly) $150 USD (likely) $200 USD (possibly) I think we can safely assume the "normalized" earning power of the business is currently in the neighborhood of $100 to $150 per share. Working for us we have roughly: $2,500 of Investments Per Share $1,000 of Insurance Premiums Per Share Slap a reasonable ROI on those investments, a reasonable CR on those premiums, and assume a reasonable growth rate over time, and FFH easily earns an average of $150+ annually per share over the next decade. Now, what can we expect over the next decade for earnings and growth? Well, Prem gave us his version of guidance on each of these things in his annual letter. He provided charts of FFH's key historical trends, explained that profitable growth has always been in FFH's DNA, and argued we should expect profitable growth going forward. In the 2 charts attached and in his accompanying commentary Prem essentially laid out the most important guiderails for investor assumptions: ROI on the investment portfolio will likely fall somewhere between 2.3% and 11%, and Prem believes the miserable days of 2.3% ROI are well behind us. Combined ratios will likely fall between 96% and 114%, and Prem believes the last 17 years of sub-100% CRs are more indicative of likely future performance. Revenue will grow, as it has in every 10 year period since 1985, almost certainly by no less than 50% and very likely by more than 100%. (I will be surprised if premiums aren't at least $50 billion a decade from now.) Reasonable Assumptions? After reviewing the historical charts and reading the annual report would it be unreasonable to assume normalized: 5% ROI on Investment Portfolio = $125 per share 97.5% Combined Ratio = $25 per share 7% annual growth $150 USD of normalized annual per share earning power growing to $300 USD per share by 2033. I don't think it's that hard to make the case that those assumptions are too conservative, and I think @Viking and Prem are doing a good job of making that case.

-

^ Yup

-

If there’s a major crisis they can suspend dividend payments which would alleviate pressure.

-

I don’t think they would have to liquidate investments at sub cos and take a tax hit. They have hundreds of millions worth of bonds rolling over every month. They can simply not reinvest the bond proceeds and dividend that cash.

-

I thought they had over a billion at the holdco. But, in addition to that keep in mind: FFH has a $2 billion undrawn revolver. FFH has lots of operating income flowing in every month. The subs operate autonomously and should only need holdco money in an emergency. The subs appear to have plenty of dividend capacity right now (it's in the annual report).

-

What are you listening to ? (Music thread)

Thrifty3000 replied to Spekulatius's topic in General Discussion

^ if you want to hear what god sounds like on the guitar fast forward to the 3 minute mark. -

Regarding Digit, according to this footnote on page 69 of the annual report it sounds to me like Digit is stuck in the regulatory mud… Digit Insurance and the company applied to the Insurance Regulatory and Development Authority of India ("IRDAI") for approval to convert the company's holdings in compulsory convertible preferred shares issued by Digit ("Digit CCPS") into equity shares of Digit. The IRDAI subsequently communicated that the application could not be considered in its current form as conversion of the Digit CCS would result in Digit (currently classified as an "Indian promoter" of Digit Insurance) becoming a subsidiary of the company, which was, at such time, prohibited under the then prevailing Indian insurance regulations. Since then, the IRDAI has enacted new regulations that have introduced a definition of a "Foreign Promoter", which would permit an Indian insurance company (like Digit Insurance) to be a subsidiary of a "Foreign Promoter". However, Digit does not currently qualify as a "Foreign Promoter" under these new regulations. Digit, Digit Insurance and the company intend to continue to explore all avenues under applicable law to achieve the company's majority ownership of Digit through conversion of the company's Digit CCPS.

-

Aha, here is the exact statement from the annual report. He didn't specify that $1,375 was the buyback bogey. Today's statement that $1,375 is the bogey is new, important, news... "Over our 37 years, excluding dividends, we have compounded book value by 17.8% annually and our stock price has compounded by 16.1% annually. Over these 37 years, there are only 55 companies of the 6,000 companies listed in 1985 on the U.S. exchanges (NYSE, NASDAQ and American) – i.e., only 1% – that have had an annual return above 15%. For our stock price to match our book value’s compound rate of 17.8%, our stock price in Canadian dollars should be $1,375. And our intrinsic value exceeds book value, a principal reason being that our insurance companies generate huge amounts of float at no cost. This is the reason we continue to buy back our shares as we continue to think they are very cheap."

-

Is Warren Buffett or Charlie Munger Smarter?

Thrifty3000 replied to nickenumbers's topic in Berkshire Hathaway

Alice Schroeder has the IQ test results of Warren Buffett and his sisters. She will not make them public while they are still living. I think it’s safe to assume Buffett’s and Munger’s IQs are at least 150. The big difference between the two men’s intellect, expertise and business skill is less a function of IQ and very much a result of FOCUS. Buffett is an investment encyclopedia. I think it’s safe to say his focus and detailed memory of all things relevant to compounding capital is probably unmatched. Munger was interested in being wealthy, but never as obsessed with business as Buffett. Munger is interested in broadly understanding how things work, the people who shaped the world, and in leading tangible projects that have tangible results - like designing his sailboat and designing/funding college dorms. One thing that is especially rare and impressive, that we can all witness, is their recall of specific details from distant memories when responding to UNIQUE questions during annual meetings. I’m not talking about the questions they get asked every year. I’m talking about the one offs where they will recount specific names, examples, and details of relatively inconsequential events that happened decades in the past. Even more impressive are the events that didn’t involve them, but were simply stories or news events they learned about second hand. There’s no doubt their minds are especially powerful. (I think Munger was more impressive than ever this year given his age.) In summary and in summation: When a Harvard Business School interviewer once asked a young prospect named Jeffrey Skilling how smart he is, the answer given was “I’m fu@king smart.” Warren Buffett and Charlie Munger are both fu@king smart! Haha -

Their stated goal is to compound book value by 15%. It sounds like they assume the stock price will sustain at least 1.2x book over the long term. So buying back at below 1.2x book will benefit shareholders (relative to book value). I don’t think they are committing to 18% long term per share growth. However, 18% can be achieved if they allocate capital exceptionally well, which can include buying back shares at a discount to intrinsic value. Currently the share price is 20% below their buyback threshold, however, they are choosing to invest in growth rather than buy back shares. That indicates they believe they can deploy capital at returns of at least 15%, which is a great sign. Fairfax is in the ultimate investor catbird seat and we’re enjoying the ride. (This is easily the most exciting ride of my 2 decade investment career. I’ve never had this much conviction in a long term opportunity.)

-

I think it’s essentially following Berkshire’s buyback rule of thumb of paying up to 1.2x book value.

-

Prem said something important on the conference call that I hadn’t heard before… He told us Fairfax is willing to buy back shares while the price is below $1375 CAD. ($1029 USD) He said that number would preserve the historical relationship between price to book value per share that has compounded at over 18% long term.

-

FWIW I believe the $33 per share is pre tax.

-

It sounds to me like you work for one of the agencies trying to keep aliens under wraps, further validating their existence.

-

Exactly. It’s pure entertainment

-

I’m the type who will be skeptical of UFOs until I’m personally beamed into a flying saucer and probed by aliens. With that said, in the words of our ol’ buddy Chuck Munger, it feels like there’s a bit of simple pain avoiding denial going on in this thread. Even though none of us have seen credible evidence of aliens, I do think there is credible evidence that: - there has been a strong stigma against reporting UAP in the United States. - there appears to be a concerning amount of tax money being spent outside the reach of congress - presumably under the guise of top secret alien-related initiatives. Two of our congressmen strongly expressed concerns with this during last week’s hearing, and one went so far as to threaten the Holman rule if he continues to get run around from defense officials. (This is actually where I think the recent crackdown could provide the best drama. I put low odds on proving aliens exist, and very high odds on learning that some crooked government insiders/contractors found a clever way to pocket billions of dollars of defense department budget with practically no accountability.) - despite what several posters claim there does appear to be a number of reasonably credible sources with loads of reasonably credible evidence worthy of further investigation. Examples: 1) If you haven’t watched the recent congressional testimony of three reasonably credible witnesses check it out. I think they presented their cases well. 2) South American cultures do not have the same alien stigma that North Americans have. Their governments have been open about having military groups dedicated to UFO investigation/intelligence for years. They have made cases public and released videos, etc. 3) Following the US’s opening up about UAP in 2017 other governments that had long vehemently denied UFOs started changing their stories. Japan was probably the most notable. 3) While we are all fanatical about analyzing investments, there are a large number of fanatics that enjoy spending their time searching for aliens. One such person I’ve recently learned about is a retired ER doctor that claims to have encountered a UAP over 3 decades ago outside Boon North Carolina. He started a foundation and devoted the last 33 years to building a network of over 700 whistleblowers and witnesses, and a trove of over 7 terabytes of documentation/evidence. He has been consulting congress and intelligence agencies and has recently turned over all of his data. He is currently trying to make it public. (Don’t get me wrong, plenty of the stuff this guy says sounds completely crackpot to me, but a couple of his most crackpot theories were echoed by others in last week’s congressional hearing.) Long story short, congress needs to figure out if some crooks in the defense department should face the firing squad, and also, it’s probably too early to write off hundreds of witnesses and whistleblowers that have risked their lives, careers and reputations to call attention to concerns the world is just now starting to take seriously.

-

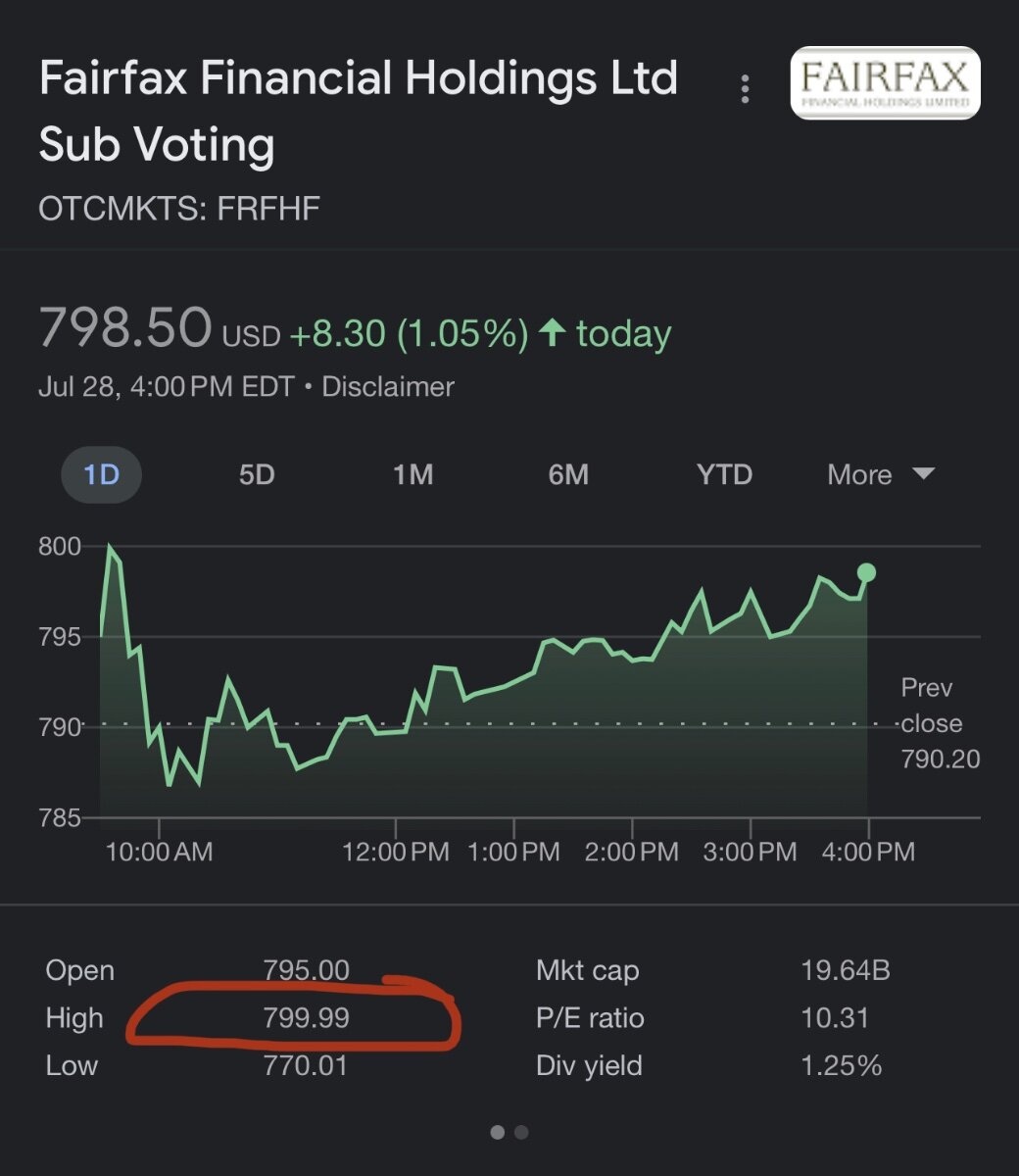

High: $799.99 Up 35% YTD

-

18. Intrinsic Value – Discounted Cash Flow

Thrifty3000 replied to Dave86ch's topic in General Discussion

Buffett does write out relevant information of interest on the cover and in the margins of annual reports. He doesn’t do formal DCF because he already knows the hurdles he needs to hit, so he just has to predict the odds of hitting a given hurdle. For example, to earn a 15% compound return Buffett knows the value of an asset has to double in 5 years and quadruple in 10 years. Buffett just has to decide whether he can reasonably predict the value in 5 or 10 years and then he pulls the trigger if he can buy the asset for half to a fourth of that future value today. He also has a number of tricks up his sleeve that allow him to juice returns. For example: - he knows a 1% price increase can increase profit by 10% (why he likes sticky products). He pushes companies to raise prices after he buys. - he knows Berkshire gets a much better interest rate than the company could get on its own. Recap that debt, reduce the interest expense, and increase profit margin. He also knows he doesn’t need to hit grand slams every time because the insurance float provides a lot of leverage which helps juice the ROE, even when an investment earns sub-par returns. -

Awesome! Thanks. Will definitely check it out.

-

Circling back to forecasting what Fairfax will likely do with those $9.5 billion of profits rolling in over the next 3 years, here are some more specifics in order of predictability. Purchasing GIG: $860 million Common share dividends: $660 million Options to purchase minority stakes and Riverstone portfolio: $2.675 billion (see summary below) Total: $4.195 billion For reference: summary of options to purchase: - Allied: FFH Can buy 17.1% by 9/24. They bought 12% for $733.5 in 2022. I assume the 17.1% will cost around $1.1 billion. - Odyssey Re: FFH can buy 10% for $900 mil beginning 1/25. - Brit: FFH can buy 13.9% for $375 mil beginning 10/23. - Riverstone: FFH can buy/sell certain securities in the Riverstone portfolio. I’m not clear on all the puts and takes on this one so I’m just earmarking $300 mil for it.

-

Sounds like insurers are taking a beating. I couldn’t believe how much Travelers jacked up my rate this year. 40% increase on a homeowner policy (only increased coverage by 20%). I started to shop it but got distracted with vacation.

-

@Viking Amazing analysis. You’re a saint for doing this. You mentioned your “big ‘miss’ is related to capital allocation”. If we assume they will net $9.5 billion over the next 3 years, then it looks to me like at least half of that is already earmarked for things like: - buying out the minority stakes of some of their existing portfolio companies. - retention/reinvestment by associates. - paying common share dividends. - buying GIG. After paying for the fairly easily predictable items like those above, what do we have left, maybe $3 or $4 billion? If they buy back another 1.5 million shares at an average price of $900 per share, then we’re looking at another $1.35 billion spend. I don’t think there is too much to be concerned about with the uses listed so far. So, I assume that leaves them with maybe a couple billion dollars to play with over the next 3 years for which we can’t easily predict the use. That’s where the fun stuff happens.

-

I agree it’s likely trivial and under control. Here are the annual payments since 2015: 2015: $130 2016: $197 2017: $174 2018: $170 2019: $138 2020: $141 2021: $152 2022: $132 > $1.2 billion paid over 8 years. Would be easy enough to benchmark their numbers against a few other insurers.