Thrifty3000

-

Posts

683 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Yes! The asset price will correlate with intrinsic value long term. Multiple expansion is not guaranteed, but it’s a nice bonus that’s likely to happen.

-

I’m not suggesting this is a deal breaker concern. And, I don’t know whether FFH is handling it differently than other insurers. But, back in 2015 FFH had reserved $896 million for asbestos. In my mind that suggests FFH expected to eventually pay $896 million. However, since 2015 they’ve actually paid something like $1.2 BILLION and they are still showing reserves of over $800 million. If FFH has historically not discounted their reserves then it seems pretty clear to me they are intentionally under-reserving. Let’s say in 2020 they had reported more realistic asbestos reserves - of maybe $1.5 or $2 billion - wouldn’t this have put even more pressure on their credit line covenants? I’m trusting how they are handling asbestos reserves is above board with regulators, but there appears to be a strong incentive to under-reserve here, so I’ve flagged this as an area that I need to look into more.

-

Ha, what happens when the population of potential buyers of an asset consists only of value investors that will never pay full price?

-

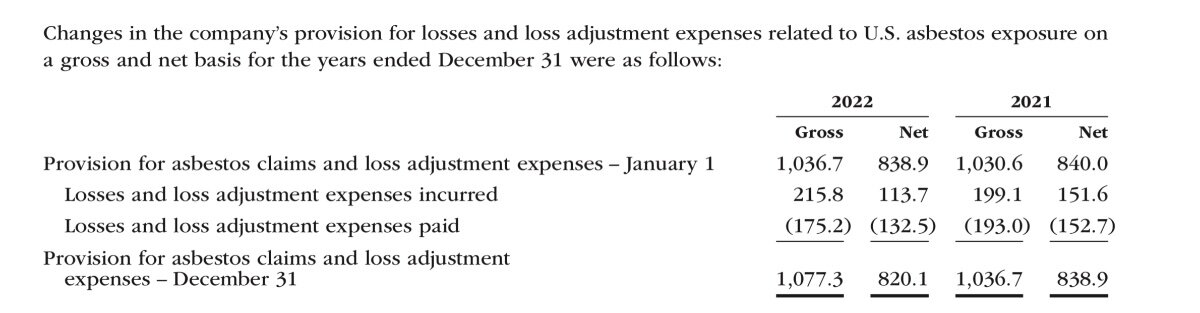

Something concerning related to this that I flagged in the annual report… Asbestos provisions and amount paid: 2021 provision: $840 million 2021 paid: $150 million 2022 provision: $839 million (really?) 2022 paid: $132 million 2023 provision: $820 million!! Anyone else see a problematic pattern there?!

-

Great news. My understanding is if a reinsurer fails to pay claims then the primary insurer is still on the hook for the liabilities. (That’s why insurers disclose gross premiums and net premiums.) Therefore the reinsured premiums involve a certain amount of credit/counterparty risk (which should correlate with the reinsurer’s credit ratings). That’s why higher credit ratings are an important competitive advantage for reinsurers. I’m sure the A+ rating increase will drive additional pricing power.

-

When Buffett has been asked in the past why he didn’t foresee some market top or bottom he has responded that if he had any such crystal ball he wouldn’t be investing in equities, because he would be able to make a whole lot more money trading derivatives.

-

For something like 90% of the last quarter century rates were lower than what they locked in. In that context I think what they did is pretty extraordinary. Knowing they don’t have an interest rate crystal ball it feels like it would be irresponsible and overly conservative to wait for rates to hit the 99th percentile before making a move.

-

Looking at the interest rate sensitivity table from the Q1 report it looks to me like bonds will take a roughly $500 million hit. A 100 basis point interest rate increase would be a $700 million hit. I’m assuming rates increased roughly 70 basis points during the quarter. Also, last year FFH had interest rate hedges that would have reduced the impact of rising rates. It appears they did not hold anymore of these hedges as of the end of Q1.

-

FWIW here is how FFH models/considers aggregate catastrophe risk (from the annual report): "Currently the company’s objective is to limit its company-wide catastrophe loss exposure such that one year’s aggregate pre-tax net catastrophe losses would not exceed one year’s normalized net earnings before income taxes. The company takes a long term view and generally considers a 15% return on common shareholders’ equity, adjusted to a pre-tax basis, to be representative of one year’s normalized net earnings. The modeled probability of aggregate catastrophe losses in any one year exceeding this amount is generally more than once in every 250 years."

-

Here is a list of the top University Hospitals. Of course you have Hopkins and Mayo, which have been mentioned several times, but don't overlook the world-renowned healthcare providers in places like Tennessee, Alabama and North Carolina. It's usually pretty easy to navigate their websites to read about the doctors within each specialty and learn what their areas of focus/research are.

-

To answer your question about getting an appointment... If calling to schedule an appointment doesn't work: Ask the scheduler (or call the receptionist at the office) and ask who that doctor recommends seeing. Email the doctor (you can get anyone's email). In your email mention the person who connected you to them, describe any specifics of your case, ask if they can work you in, and if they can't work you in ask who they would recommend seeing if they were in your situation.

-

I think when the life of a loved one is at stake it's appropriate to be shameless in seeking the care they need. If you consider your entire network you're probably only 2 or 3 degrees away from a leading specialist. Somewhere in your network of family, friends, coworkers, neighbors, religious group, former classmates, civic organizations, kids' sports teams, social media, CoBF, etc there is someone who will gladly introduce you to someone that will gladly help you solve your problem. You just gotta be shameless and tenacious. I learned the lesson from my dad when he was faced with my mom's first bout of cancer. After her doctor estimated a 20% chance of survival, my dad shamelessly leveraged his network to find a new doctor. He ultimately called the CEOs and Presidents of the largest hospital, health system, med school and health insurance provider in our state to ask for referrals. With their help they found a new doctor. 30 years later, much to my wife's dismay, my mom is still alive and kicking. Haha.

-

True story I like to share with people who have a specific life threatening issue - like cancer. My mom had breast cancer in the 90s and then got a lymphoma about 10 years ago. Her (insert expletive) doctor, of course, referred her to a general oncologist within his own medical group. Going to a general oncologist sounded like a death sentence to me, so I emailed a radiologist I knew that worked at a local, reputable, teaching hospital. I told her the situation and asked for her recommendation. She then recommended a colleague that was one of the LEADING SPECIALISTS in the world on how to treat lymphomas in women who had already received chemo for breast cancer! When we went to meet with that doctor they told us two things: - there is not a cure for my mother’s cancer. - but, he would collaborate on her case with other world-renowned specialists at MD Anderson, Emory, Hopkins, Mayo, etc to devise a treatment plan. Fast forward through a few months of treatment and she was completely cured!! Long story short, if you have a specific medical issue: - do whatever it takes to find THE specialist and travel to meet with them! (I’m a big fan of teaching hospitals.) - make sure they collaborate with other leading specialists at other reputable hospitals.

-

Just watched it! Such a good documentary. Thanks for suggesting. I should preface that I’m one of the MOST gullible people I’ve ever met, BUT I’m SO EFFING convinced this stuff is legit! I think the alien case is a lot like the COVID lab-origin case. There is so much undisputed, consistent, and highly credible evidence from such a wide array of sources out there (including photo and video evidence in the case of UFOs), that the burden of proof has been shifted from proving it right to proving it wrong! Luckily we have decades (and maybe centuries) of evidence that these visitors are friendly observers rather than threats. Humans are merely creatures wandering around the “Earth zoo”. FWIW I’m basing my entire thesis on about 10 hours of super-entertaining documentaries and Joe Rogan podcasts! Haha.

-

Hahaha! 9.6kbaud modem. I’m having flashbacks to my Napster days.

-

Looks like this one was also made by the James Fox fella I mentioned above. Will check it out. Here’s the trailer for his new documentary about the Brazil incident…

-

If you really want to go down the hole with this stuff I recommend these two conversations. Joe Rogan interview with Bob Lazar: The one with Bob Lazar is interesting because he made claims over 30 years ago that couldn’t be proven or verified at the time. And over the years more and more of his claims have been validated. For example he claimed having access to technology that used Element 115, which wasn’t even on the periodic table back then, and couldn’t be proven to exist until recently with the construction of large hadron colliders. Joe Rogan interview with James Fox: The one with James Fox is interesting because he recounts multiple examples of the most credible events - events where there are a variety of mutual witnesses and significant evidence. He recently made a documentary about what he thinks is probably the most significant event to date. It happened in Brazil in the 90s and was witnessed by civilians of all ages, police, doctors, military, politicians etc.

-

Maaaan, don’t you know you can create a gravity distortion engine by converting element 115 to dark matter, concentrating the resulting antigravity field in the direction you want to travel, and move friction-free through space?! Haha. I learned that from a Joe Rogan podcast with Bob Lazar.

-

Wow! Duh, I don't know where my head is today. Thanks for clarifying! So, it's really just a simple calculation of expected growth vs. the TRS interest expense. I trust Hamblin Watsa to handle that one. It will still be an interesting signal whenever they decide to exit the TRS, but that's true of any share related transaction. (I added a correction to my post.)

-

Seems to me we're getting closer to the point where it makes sense to cash in the TRS gains and focus on buying back the $1 billion Odyssey position from OMERS. Not sure if we ever nailed down the interest rate FFH is paying OMERS for that deal, but it sounded like an $80 or $90 million annual interest expense. Given FFH's expected earnings power it sounds to me like a risk-weighted break even point might be in the neighborhood of $800 to $1,000 USD per FFH share. (Of course this depends on the TRS interest rate and, more importantly, on how FFH sees its growth prospects. The more growth expected the higher they'll let the TRS run.) In fact, I think the point at which they cash out the TRS will be a pretty strong signal for how FFH sees its growth prospects. If they were to cash out the TRS now I'd think it's a signal they expect normal earnings to remain flat beyond the 3 year horizon. However, if the shares run up to $1,000 USD and they still hold the TRS then that seems like pretty strong conviction favoring growth. ^ PS. "cash in the TRS gains" is the wrong terminology. I should have said "exit the TRS position". TRS gains have already been booked.

-

To Prem’s credit he did repeatedly lay out their thesis for their caution and short positions (see every Hoisington quarterly letter ever written for a technical explanation of Prem’s thesis). He also qualifies EVERY decision with a statement along the lines of “this bet may or may not work, but we expect it to work.” He knows every capital allocation decision is nothing more than a bet where he expects the odds to be in his favor. That’s capital allocation for you. Any investor had every right to disagree with Prem. However, I don’t recall much public dispute with Prem’s logic given the extreme debt to gdp ratios globally, and the deflationary experiences of post-great-depression USA and post-early-90s-Japan. Prem just happened to pick a fight with maybe the most extreme financial experiment in the history of human civilization - a global central bank ZIRP bandwagon! (See every Grant’s Interest Rate Observer during that period.) Prem has a billion dollar brain and a multi-decade track record. His net worth will be higher a decade from now than it is today. He’s wired for that. A snowball, if you will. He ain’t dumb.

-

+1

-

^ the people have spoken

-

Assuming they sell treasuries yielding 4% to pay for this I estimate it will add around $4 of after tax EPS for FFH shares. Not bad.

-

I’m all for giving zoom a try. Will be fun. Thanks