nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

https://www.moneycontrol.com/budget/india-s-insurance-market-poised-to-grow-the-fastest-in-g20-economic-survey-article-12925602.html “The Swiss Re Institute, as quoted in the survey, has forecast 11.1 percent growth for India's insurance sector from 2024 to 2028, attributing this to an expanding middle class, technological advancements, and supportive regulatory frameworks.”

-

https://stories.jobaaj.com/news-updates/india/budget-2025-from-74-to-100-fdi-in-insurance This has been doing the rounds for a while. Seems as though it has been confirmed

-

I wasn't sure if there was going to be a 2025 thread but it seems we are using this one again. I appreciate others posting their positions, so here are my two main accounts. Personal Account Retirement Account The main changes are the build in the Nintendo position throughout 2024 and the rotation of Mkl into Fairfax during one of the sell offs during year. I'm also gradually getting over my aversion to owning Fairfax subs. https://thecobf.com/forum/topic/20512-share-your-portfolio-2024/page/2/

-

Do you enjoy the process or just the proceeds?

nwoodman replied to Milu's topic in General Discussion

+1, hard to see value in the US markets in aggregate. I would take a stock picking even if it risked underperforming rather than passively invest in what I consider a fine example of irrational exuberance. In terms of the question posed, I lean more toward the process. The proceeds have given me many more choices, but the things I enjoy don't cost that much. It's more intellectual scorekeeping than anything else, plus I genuinely enjoy learning and thinking about businesses that aren't my chosen profession. Charlie's latticework of mental models always resonated. “To the man with only a hammer, every problem looks like a nail.” “If you get into the mental habit of relating what you’re reading to the basic structure of the underlying ideas being demonstrated, you gradually accumulate some wisdom.” The wisdom part has not been fully cemented, but the journey has been fascinating. -

Great interview. Natalia Strafti is a class act, quick bio: 2000: Began her career at EFG Eurobank as Investment Analyst, later becoming Deputy Head of Advisory and Asset Management. 2008-2014: Head of Investments and Asset Management, managing 1.5B+ in real estate investments, including green-certified office redevelopments. 2014-2021: Chief Operating Officer (COO) of Grivalia Properties REIC, leading operations and sustainability initiatives, and driving successful share capital increases and IPO efforts. 2021: Appointed Deputy CEO of Grivalia Hospitality, overseeing acquisitions, development, and luxury hospitality projects. 2025: Promoted to CEO of Grivalia Hospitality, focusing on innovation, sustainability, and expanding in the ultra-luxury sector. Intuitively a rise to CEO after 25 years with the same company just seems so much more culturally valuable than an outside appointment. Very consistent with Fairfax’s approach and their value of tenure.

-

Nice numbers from Digit https://www.business-standard.com/markets/news/go-digit-general-insurance-shares-rally-9-after-strong-q3-details-here-125012300348_1.html https://www.ndtvprofit.com/markets/go-digit-general-insurance-share-price-jumps-as-q3-profit-nearly-triples Market loving it after the recent Indian sell off

-

@Viking, when this came up a while back there was a view that they were over the reported 33.29%. That div calculation suggests the same

-

Looking at this more closely, I don't think the sale gives them the ability to mark to market because of the rules around equity method accounting: "To capture the excess of fair value on their balance sheet, Fairfax would need to: 1. Reclassify the Eurobank stake as a financial asset (FVTPL or FVOCI). 2. Lose significant influence over Eurobank (e.g., reduce stake or governance involvement). 3. Take an impairment reversal under IFRS if applicable. Absent these changes, the excess fair value can only be disclosed but not formally reflected in the balance sheet under the equity method." However, the gain on sale of the 80m shares does flow through the P&L. Roughly (2.4-0.92)*80m/0.96=123.3 m =123.3/22=5.6 per share

-

That sounds more like they are taking money off the table to me than compliance. The upside is that that it will free up Eurobank to repurchase shares. Definitely closer to FV than it was but still cheap. Should give Fairfax around 80mx€2.40/.96=$USD200m pre-tax Edit: it gives them a mark too https://www.eurobankholdings.gr/en/investor-relations/shareholders/shareholding-structure

-

@Jay Rent thanks for the above info , greatly appreciated

-

Thanks, the Kungsleden is on my list too in particular the Abisko–Nikkaluokta . This hike is in Tasmania, the Island state at the bottom of Australia. It is only 67km but hiking in SW Tasmania is usually measured in days/hrs. It is some tough country!

-

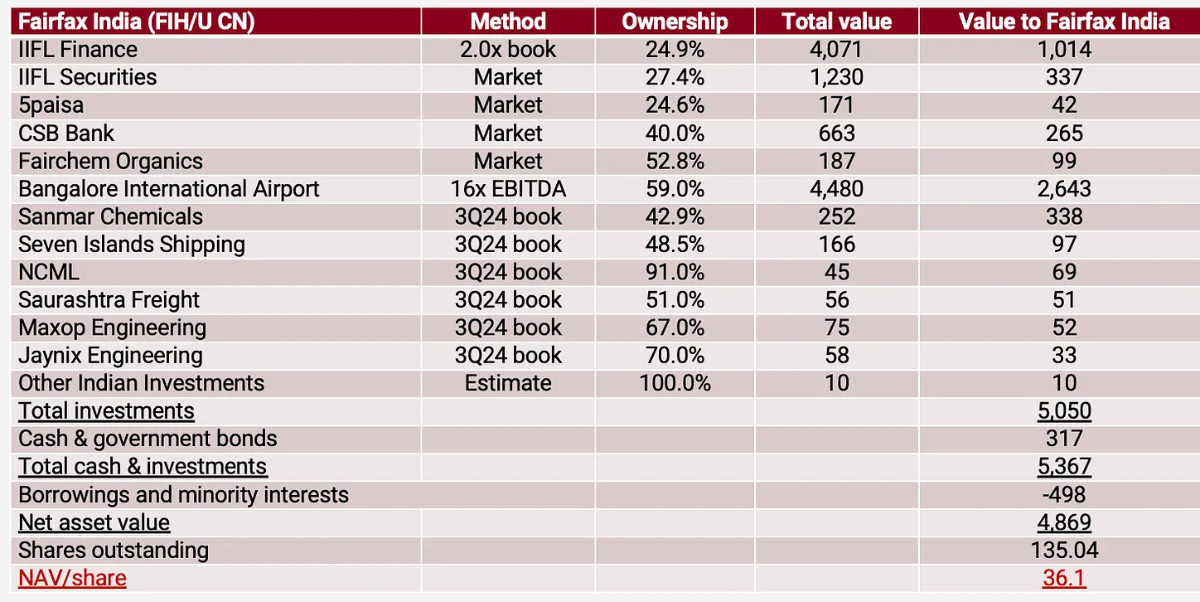

Based on sum of the parts Asian Century Stocks arrives at a NAV of $36 but conservatively ascribes no value to the future purchase from Siemens or the land development. https://www.asiancenturystocks.com/p/fairfax-india-fihu-cn-2024-update A +50% holding company discount seems very cheap. As the article goes on to say if they get the airport IPO happening by September ‘25 then the gap should close. I recently bought a few as the discount to IV just seems too large to ignore.

-

Yep, never say never. It’s been on a bit of a tear, after a break-even quarter and the Cylance sale for ~$160m plus shares in Arctic Wolf. After adjustments this gives them $80m now and $40m in a years time. The fact that they paid $1.4 bn in cash (ouch) in 2018 is history. I am sure we have all written off the BlackBerry investment so it’s like an option on IoT and Secure Comms at this stage. Hopefully WSB boys get behind it again https://www.blackberry.com/us/en/company/newsroom/press-releases/2024/arctic-wolf-and-blackberry-announce-acquisition-agreement-for-cylance

-

I don’t think any of us does. I think we are back in Bradstreet’s sweet spot I.e normal rates vs abnormally low. Also the hubris/sugar hits of the wins from the GFC and Bank of Ireland are just distant echoes. Eurobank has worked but no Midas touch. Shorts done, replaced by considered stock picking. Last time, I mention it, I promise, but a very different President in Peter Clarke. I think Prem has his A-Team for the next 10-15 years. Let’s see how Ben Watsa does at Fairfax India, but so far I don’t see any red flags there. If this transition works out it will truly cement Prem as one of the greats. Edit: I threw a few more on the pile over the last couple of weeks and as recently as last night. Still my highest conviction idea other than Nintendo.

-

No one?

-

That looks awesome, count me in. Merry Christmas all.

-

I hope they don’t raise it for another 10 years. I understand the background to paying a dividend in the first place (management compensation/cashflow) and hopefully $15/share suffices. Fairfax hardly seems short on ideas for capital allocation so retaining earnings surely is the best course of action. Selfishly, for me the tax implications of recycling the dividend back into Fairfax shares are horrible.

-

Purely a curiosity, but as we close out the year it’s interesting that the FRFH (USD) share price is +/- the same as a Class A but with 40 years difference to the month. One hell of a compounding curve over a 40 year time horizon. Magnificent! EDIT: Those minor perturbations between the voting vs weighing machine no doubt were hotly debated and in the end, corrected, but also resulted in large wealth transfers. Also you needed to survive the 50% draw downs.

-

Normally don’t get too excited by these renders but these guys do seem to deliver. I remember thinking the same thing about T2 and what they delivered, IMHO, was better than the initial pitch deck. This looks pretty swish.

-

This scene from Succession always struck a chord. Agree with the posters above, work is super important. However, having the choice on what to work is the real gift. I get a kick out of community service ( Scouts, SAR etc) but I know it’s not everyone’s bag.

-

Looks like she “put in the work” as well.

-

Just returned from the Western Arthurs Traverse in Southwest Tasmania—what an ass kicker! It’s easily the toughest hike I’ve ever done. The Western Arthurs is widely regarded as one of Australia’s hardest treks, and now I understand why. Located in the Roaring Forties, the range is the first to bear the brunt of weather systems rolling in from the Southern Ocean. Combine that with relentless mud, countless pack hauls, and a travel pace of less than 1 km/h through some of the most rugged terrain imaginable, and you’ve got a hike that earns its reputation. Fortunately, I’ve spent years training the kids to help carry their old man through bucket-list adventures like this one! https://www.alltrails.com/explore/trail/australia/tasmania/western-arthurs-traverse?mobileMap=false&ref=sidebar-static-map

-

Agree, decent amount of work for Siemens in just connecting the airport by rail, let alone everything else that is going on https://press.siemens.com/in/en/pressrelease/siemens-consortium-partners-bengaluru-metro-rail-corporation-limited-rail

-

It is the price discovery aspect of the exchange that is the interesting factor here. Unless I am way off, I think FIH got a bargain.

-

A brief primer on SPV, I believe there is a bit of a refocus by the parent but I don’t follow them closely. Background ‘Siemens Project Ventures GmbH (SPV), as part of Siemens Financial Services, operates within a defined strategic framework set by Siemens AG. Its primary role is to invest in infrastructure and energy projects that align with the parent company’s long-term objectives. However, certain trends and strategic decisions within Siemens AG may have influenced SPV’s recent actions: 1. Strategic Realignment at Siemens AG • Siemens AG has been undergoing significant restructuring in recent years, emphasizing its core competencies in digital industries, smart infrastructure, and mobility. • Non-core assets, particularly those tied to infrastructure projects without a direct link to Siemens’ strategic technology focus, have been earmarked for divestment. This includes stakes held by SPV, such as in Bangalore International Airport Limited (BIAL). • Divestment of such assets allows Siemens AG to redirect capital toward higher-priority growth areas like industrial automation, electrification, and digital services. 2. Global Financial and Market Pressures • Siemens AG and its subsidiaries, including SPV, have been affected by: • Global supply chain disruptions, especially in energy and infrastructure sectors. • Geopolitical tensions, which have created uncertainties in some of Siemens’ markets, prompting a tighter focus on financial discipline. • Divesting assets like BIAL helps ensure financial stability while enabling investments in transformative areas. 3. Specific Challenges in India • Complex Regulatory Environment: The infrastructure sector in India often involves regulatory complexities and long gestation periods for returns on investment. This might have made the BIAL stake less attractive compared to Siemens’ other global projects. • Shift in Focus: Siemens AG has been prioritizing digital and energy-efficient solutions in India, areas where it sees significant growth potential. Selling the airport stake aligns with this localized strategy. 4. Siemens Energy Spin-Off • The spin-off of Siemens Energy in 2020 had ripple effects across Siemens AG’s operations, requiring divestments to strengthen financial positioning for Siemens Energy and other business units. • Siemens Project Ventures may be under indirect pressure to liquidate legacy or non-strategic investments, like the BIAL stake, to align with the group’s new focus areas. 5. Efficient Capital Allocation • Siemens AG’s capital allocation strategy emphasizes higher returns on investments. Infrastructure investments like BIAL often have a lower ROI compared to high-growth areas such as renewable energy technologies, industrial IoT, or smart grids. • SPV’s sale of its BIAL stake could reflect this shift, allowing Siemens to consolidate resources for sectors where it holds a competitive advantage. Summary While there is no direct evidence of undue pressure from Siemens AG on SPV, the broader strategic realignment at Siemens, coupled with financial discipline, likely influenced SPV’s decision to divest its stake in BIAL. This move aligns with Siemens AG’s efforts to streamline operations, optimize its portfolio, and focus on technology-driven growth areas. For SPV, the sale is part of its ongoing mission to adapt its portfolio to the evolving priorities of its parent company.”