nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Way beyond my pay grade but this run, while reminiscent of 2007, lacks some of the more obvious macro markers. I do appreciate your thoughtfulness.

-

Probably best not be a knob about it and just enjoy the fact that he got to see it. Just saying.

-

It probably means nothing to him, but I am glad we are both alive to see it.

-

Ouch, it’s been a busy season in Canada. Do you think they were swimming a bit naked? “Reinsurance recoveries include the full utilization of the $25 million available under the company's catastrophe aggregate treaty.” https://www.newswire.ca/news-releases/definity-releases-estimate-of-financial-impact-from-catastrophe-losses-806928340.html Cat Agg Treaty: 1. Threshold or Attachment Point: The treaty specifies an aggregate amount of losses that the insurer must incur before the reinsurance coverage kicks in. This is often referred to as the “attachment point.” 2. Coverage Limit: The treaty also defines a maximum amount that the reinsurer will pay once the attachment point is reached. This limit caps the reinsurer’s liability under the agreement. 3. Period of Coverage: The coverage typically applies to losses occurring within a defined period, usually one year.

-

The sub positions are an interesting thought exercise. My take is that it creates some clever optionality and a sign that Fairfax is not short on ideas. It creates a reasonably clear pathway to decent returns if they are light on for ideas in the future or there is a significant changing of the guard. I guess the other side of the argument is the tipping point of running a highly leveraged book. I will never become complacent about their debt levels but I do give them the benefit of the doubt in terms of how they manage the risk and wherever possible make it non-recourse and bump it into “equity”.

-

AerCap springs to mind. Maybe GATX. However there is an operational/service aspect that is unique to Seaspan (crew, maintenance, compliance etc). I always figured between capital allocation and the ops side of the business it was a good fit for Sokol.

-

MS released their Indian Macro Indicators Chartbook Key points: 1. GDP growth remains resilient, with GDP growth of 7.8% year-over-year in Q1 FY2025 (April-June 2024). The report forecasts GDP growth of 6.8% for FY2025 and 6.5% for FY2026. 2. Inflation has moderated, with headline CPI inflation at 3.5% year-over-year in July 2024, a 5-year low. Core inflation edged up slightly to 3.4%. 3. The trade deficit widened to $23.5 billion in July 2024. The current account deficit is expected to remain benign at around 1% of GDP in FY2025. 4. Domestic demand indicators show some softening but remain generally positive. Manufacturing and services PMIs remain in expansion territory. 5. The fiscal deficit has narrowed to 4.4% of GDP on a 12-month trailing basis as of June 2024. 6. Monetary policy remains steady, with the repo rate unchanged at 6.5%. The report expects rates to remain on hold through FY2025-26. 7. Key risks stem from external factors, but the overall outlook remains constructive on India's economic growth prospects. INDIA_20240821_2300.pdf

-

Fair point, I was just interested in @Blake Hampton’s perspective. I tend to focus more at the company level but trying to redevelop some larger market valuation guardrails. It strikes me there are some positive feedback loops that could come unstuck but this is more about managing my own margin levels than slaying “bubble dragons”. Aggregate margin levels and market valuations indicate to me that this is not the time to be balls to wall, so other thoughts on what might be driving extended valuations are worth noting.

-

Thanks, I was aware of the effect on Berkshire’s reporting but hadn’t considered it in the broader market context. The positive feedback loop you alluded to is worth some further research.

-

I don’t disagree. Could you please expand a little on your first point about cap gains? A link would do.

-

Thank-you, this struck a chord.

-

+2, the model requires superior investment acumen and a willingness to potentially suffer a “conglomerate discount” A game that only aligns with longer term thinking (nuts on the line helps too). A motherhood statement but Berkshire is primarily an investment company/capital allocation machine that uses float as part of their funding. As it turns out they have been pretty damn good at insurance but I think this is partly a reflection of temperament (again thinking long term). Fairfax only has to do 1/10th as well as Berkshire and the answer should be quite pleasing. A high probability IMHO.

-

@viking, as we know it is a cyclical mean reverting commodity business so what really matters is underwriting discipline. I am not seeing anything that suggests they are being anything other than disciplined. Timely that Morgan Stanley released a recent industry status report summarised as follows: 1. Market Conditions: - The report indicates diverging trends between life and P&C insurers. - P&C insurers are generally in a stronger position currently, but facing some headwinds. 2. Social Inflation: - This is a major concern for commercial carriers, putting pressure on margins and potentially leading to higher combined ratios. - The long-term impact of social inflation may be underappreciated by the market. 3. Personal Lines: - Personal lines carriers like Progressive and Allstate are seeing improving results, particularly in auto insurance as pricing stabilizes. 4. Reinsurance: - Reinsurers had mixed results - ahead on earnings but below expectations on premium growth. - Pricing remains firm, but growth is moderating, which could be an early sign of softening. 5. Commercial Lines: - Facing challenges due to social inflation and potential reserve inadequacies. - Pricing remained stable to positive overall in Q2 2024, but there are some marginal declines sequentially from the previous quarter. 6. Potential for Softening: - While not explicitly forecasting a broad market softening, the report provides some indicators that could point in that direction: a) Moderating growth in reinsurance b) Sequential declines in commercial pricing c) Stabilizing personal lines pricing - However, the report also notes that different segments of the market are in different stages of their cycles. Perhaps I could have made it clearer in my original post, but I agree that their mix of lines and geography helps. Although a CR of a 100 is hardly the end of the world, especially if is a better CR than your peers. Maybe I place too much emphasis on relative performance, but I see this as important over time. Ultimately Fairfax will turn out to be an OK or great investment based on their capital allocation, same as Berkshire. This means “don’t lose capital”. INSURANCE_20240819_0411.pdf

-

I am in the combined ratios revert to 100 camp. However i wouldn’t be surprised if the mix of insurance Fairfax is writing today may favour better CRs than 10 years ago. @glider3834 posted a league table a while back of Specialty underwriters that showed Fairfax had made considerable inroads primarily at the expense of Markel. Then there was that insight that Markel baulked on Allied World. Not saying it will be different this time but I do feel there is perhaps more flexibility across lines and geography than there used to be. This may allow a bit more of a National Indemnity philosophy in terms of underwriting discipline. Thank you again Andy Barnard. Buffett on NICO “Some companies would feel that having [a significantly higher expense ratio] would be intolerable - but what we feel is intolerable is writing bad business… If you get a culture of writing bad business, it’s almost impossible to get rid of. We would rather suffer too much overhead than to teach our employees that, in order to retain their jobs, they needed to write any damn thing that came along, because that’s a very hard habit to get rid of once you’re hooked on it… I think we’re almost the only insurance company in the world - certainly public - that sends the absolutely unequivocal message to the people associated with us that they will never be laid off because of a lack of volume.”

-

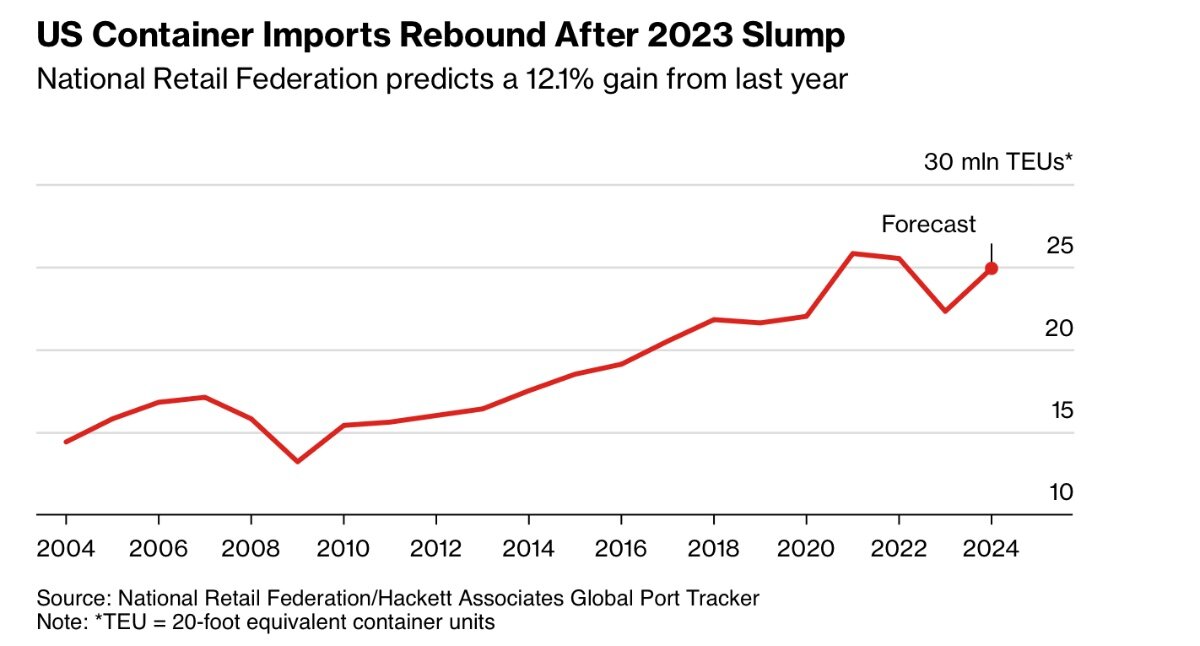

From Bloomberg: Imports Are Surging Again at US Ports, But Without the Logjams “Today, despite worries about a softening economy, the busiest US port complex — Los Angeles and Long Beach, which account for roughly a third of all container imports to the country — is processing import volumes near the highs set during the pandemic. The complex had its third-strongest month ever in July, just shy of an all-time high reached in May 2021. Total US container imports through major ports this year will reach 24.9 million measured in 20-foot equivalent units, close to 2021 and 2022 levels that topped 25 million, according the National Retail Federation.” “In addition to back-to-school demand and preparation for the year-end holiday season that typically sees an uptick in activity this time of year, volumes have also been affected by moves to build up inventories ahead of potential increases in US tariffs on Chinese goods.”

-

True, picking up on @SafetyinNumbers point above, I think that is why we follow their capital allocation so closely. There is a bit of scar tissue that has built up with Fairfax over the years from capital allocation misadventures. I just don’t have those concerns with Berkshire and they make mistakes too. Even when Buffett is doing nothing it feels like optionality. To this end Wade’s recent CC comments resonated when he said he wasn’t finding much value in equities at the moment, I can empathise there. Happy for them to keep the allocation to equities small until there is some really interesting or just take out an entire company e.g. Sleep Country. I have probably touched on this before, but I have often thought that Berkshire has access to more timely information than the Fed. It strikes me that Fairfax is entering a similar position in terms of data from their various subs which are now far and wide. This has to help in general but in terms of managing a bond portfolio surely it must provide some semblance of a competitive advantage. This ‘access to information’ also extends to key relationships and deal flow. For me deal flow is key and I think that is something that has definitely improved in the last 5 years or so. Berkshire doesn’t seem to get the opportunities they did when I first started to follow them 20 years ago. It might be the law of large numbers but I do feel they got crowded out by the Fed during Covid so there is that. The good thing for Fairfax is that a $US1-2bn deal can make a material difference, as long as they are rational.

-

@@Viking Good post and guilty as charged, the P/B heuristic is just so tempting. I think it has caused me to underestimate the true earning potential—and hence value—of both Fairfax and Berkshire over the years. Although P/B of 0.6x’s was a decent marker of a margin of dafety.

-

https://cyprus-mail.com/2024/08/07/eurobank-completes-mandatory-public-offer-for-hellenic-bank-shares/# “Finally, according to the bank’s articles of association, nominations for the position of director can be submitted by shareholders from August 4, 2024, until the close of business (2:30 p.m. Cyprus time) on August 30, 2024.” Still intrigued to learn whether Hellenic’s current concentrated shareholder base is consistent with listing rules. Either way it’s an interesting stalemate in terms of a full takeover. My only concern is the likes of Demetra and ETYK keep agitating for reversal of the merger. A reversal is highly unlikely, so more an irritation.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

That should be a blast, enjoy -

Well played sir. Guess we should be careful of wishful thinking

-

Love the asymmetry. It does make you wonder, if on balance, there might be a few more pleasant surprises for Fairfax shareholders from that era. Not necessary for the thesis but says a lot about management’s staying power IMHO.

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Great interview and top summary. I have attached a transcript. Building on your summary: 1) That notion of inelasticity can result in fragility in both directions, e.g. China in 2015 -85% 2) His discussion on Alpha was fascinating: “The solution sets that we use in finance, we’re all very good at math, but alpha is actually just the intercept on a linear equation. The behaviour of your portfolio is equal to its beta times the market return plus some idiosyncratic measure we call alpha. Alpha equals mx plus b. If you use a linear solution to a curved surface, over time, mechanically, your alphas get pushed lower. It’s just math, and it’s a function of the fact that we’re really not as good at math as we like to talk about being. We’re just using the wrong metrics.” “The real issue is that we have effectively allowed a system to persist that mechanically inflates valuations, inures us to that process, allows us to create all sorts of narratives around both why it’s happening and what the degree of wealth that is being created is.” 3) On exponentially “If you jump back to that slide that I showed you before, and I want to be very clear, I don’t think that this is ultimately going to happen because the volatility will become so extreme, but if you jump back to slide 11, it shows that exponential curve, that orange line going higher. The easiest way to think about that is as you get to somewhere in the neighborhood of 80% passive, and remember, we’re only about 45% right now, at around 80% passive, the Shiller PE would be somewhere around 400 to 500. But I don’t think that’s going to happen because I think we’re actually approaching the inflection point where the passive has become so large that it creates its own enemy." 4) On bitcoin “Bitcoin doesn’t have that capacity [for innovation]. You can work as hard as you want. It’s under a fixed release schedule. And as a result, there is no reward to human innovation.” A couple of others 5) Regulatory Frameworks Green criticizes the current regulatory environment, pointing out that index providers have been largely exempt from diversification requirements due to effective lobbying. He believes this lack of regulation contributes to the increased risk in markets. “We allowed the markets to become far more risky while pursuing a theoretical ideal of complete markets. Candidly, I think that we’re ultimately going to pay a penalty for it.” 6) On Leverage "So the answer is you invest passively, but that then exacerbates the societal risk that we face when ultimately we try to take that money out… Candidly, if you can, you want to actually leverage that exposure. Doing things like buying call options which historically had delivered significantly negative returns now actually largely offer positive returns because the market has shifted in that drift feature" The key question is how actionable all this is. I think it is just another asymmetry to be aware of in terms of portfolio construction. One thing that is ringing in my ears, though, is how leverage becomes the heart of any alpha in an indexing world. That is where 6 sigma-type events are generated. The Rational Reminder Podcast - Michael Green- Market Efficiency Is Not The Question.pdf -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

A true true great. He must be doing the rounds as he was featured here too. One of the better interviews I have seen recently -

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

All good questions and unfortunately I don’t have an answer. Thanks for laying them out they are definitely thought provoking. A couple of observations 1) I can’t recall any time in the last 10 years when I have encountered so many value investors contemplating indexing 2) Old metrics like debt/gdp are at all time highs but there seems to be complete ambivalence 3)There seems to be a new generation “experimenting with margin” 4)We have our “market darlings” the Mag 7. 5)We have a narrative in AI, that is exciting but is a little hard to pin down in terms of real productivity gains. 5)You have Buffett sitting in cash, and the Fairfax team looking but not finding I am no permabear but the set up sure feels a bit strange to me and maybe we have had the rap over the knuckles we needed last week. I am sure I will get over it, especially if these companies continue to deliver. In that case Indexing has picked the right horses. It was just interesting to learn that my sketchy thoughts weren’t unique and that others had developed the thinking further and applied some actual rigour and data. I will keep an open mind as this is the system in which we are all playing. -

Ah, saw this earlier today but the penny didn’t drop that it was that “Cairo”. Thanks @glider3834 @petec From Perplexity: Cairo Mezz Plc was established in 2020 in Nicosia, Cyprus with the corporate objective to hold the notes issued in the context of the Cairo securitization. The company was formerly known as Mairanus Ltd. and changed its name to Cairo Mezz Plc in September 2020. Cairo Mezz Plc was incorporated in 2020. Its shares were distributed to Eurobank shareholders in 2020, representing a 75% ownership of Eurobank Cairo's securitisation mezzanine tranche. The theoretical value of the distributed shares, based on Deloitte's valuation, was set at EUR 57.5m, EUR 0.0155 per Eurobank share or EUR 0.186 for every 12 shares held. Cairo Mezz Plc was established in Cyprus in 2020 specifically to hold mezzanine and junior notes from the Cairo securitization of Eurobank's non-performing loans. Its shares originated from being distributed to existing Eurobank shareholders in 2020.