nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Hopefully it plays out something like this: “1. PVC Price Recovery and Demand Growth (Mid-to-Late 2025 Onward) • The PVC market is showing early signs of stabilization, with prices bottoming out in late 2023. • Industry experts predict higher global PVC demand in late 2025 and 2026, driven by a rebound in construction and infrastructure spending, particularly in India and Southeast Asia. • India’s PVC consumption is expected to grow at 8% CAGR, creating a structural demand tailwind for Sanmar’s Chemplast Sanmar unit. • Timing: Expect a gradual price recovery from mid-2025, with stronger margins by 2026. 2. Anti-Dumping Measures in India to Support Domestic Pricing (Q2 2025 Onward) • The Indian government is advancing anti-dumping duties on paste PVC and suspension PVC imports, particularly from China, South Korea, and the EU. • If finalized, these duties would reduce import pressure and improve pricing power for domestic producers like Chemplast Sanmar. • The PVC Quality Control Order (QCO), set to take effect by June 2025, will further limit low-quality imports, benefiting domestic manufacturers. • Timing: Once anti-dumping measures are officially imposed (likely Q2-Q3 2025), expect price support and margin recovery for Sanmar. 3. Full Utilization of Expanded Capacity and Operational Efficiency Gains (Q3 2025 Onward) • Sanmar has completed major capacity expansions (e.g., 41,000 TPA specialty PVC addition and full ramp-up of TCI Sanmar’s 400,000 TPA Egypt plant). • Efficiency improvements and higher utilization at TCI Sanmar (Egypt) should significantly boost profitability once PVC prices stabilize. • Timing: Efficiency-driven profitability improvement from Q3 2025, with full impact in 2026. 4. Diversification into Higher-Margin Specialty Chemicals (Late 2025–2026) • Sanmar is expanding its Custom Manufactured Chemicals Division (CMCD) to cater to high-value agrochemical and pharma markets. • Five new contracts signed for specialty chemical intermediates, with a second-phase expansion of the new plant planned in 2025. • This shifts revenue mix away from commodity PVC toward less cyclical, higher-margin products. • Timing: Specialty chemicals’ revenue contribution will increase meaningfully from late 2025. 5. Stronger Financial Position and Lower Debt Burden (Q4 2025 Onward) • After the 2021 IPO and debt repayments, Sanmar significantly reduced its financial leverage, lowering interest costs. • Fairfax India remains a long-term supportive investor, providing stability. • Recent cost control measures and cash preservation efforts position the company for profitability in the next market upturn. • Timing: Lower financial costs and improved cash flows from Q4 2025, supporting sustained profitability. Expected Timing for Sanmar’s Return to Profitability • Short-Term (H1 2025): Limited profitability improvement, awaiting pricing recovery and regulatory actions. • Mid-Term (H2 2025): Anti-dumping duties, demand recovery, and full plant utilization start boosting margins. • Long-Term (2026): Stronger profitability driven by higher PVC prices, specialty chemicals growth, and cost efficiencies.” We shall see. Fairfax seems happy to wait it out, so that’s good enough for me.

-

Love your work. Didn’t realise or had forgotten that there was a sunrise on that deal. I always figured that they would buy this in first. That color explains it.

-

Don’t disagree but the thesis is the airport. Sanmar is going to be a drag for the next year but should start working from 2026 onwards.

-

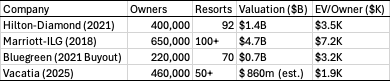

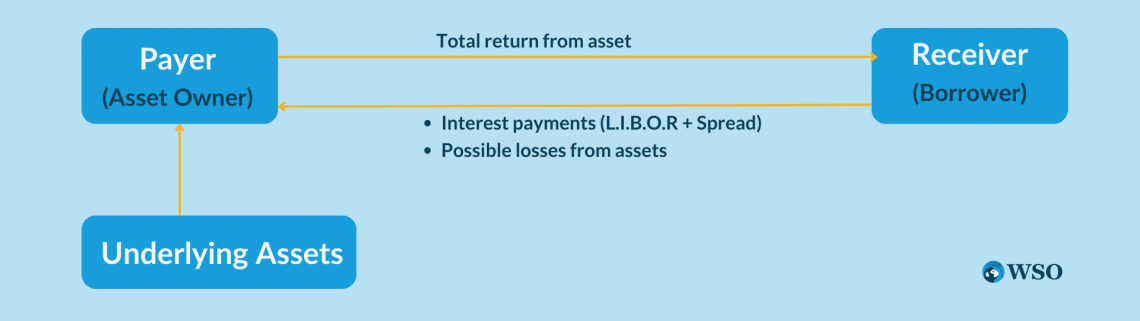

I've attached some notes on Vacatia. I sound like a broken record, but I love these structured deals. I doubt its lost on anyone here but this is such a sweet spot for Fairfax. There seems to be no shortage of deals to be done. Hopefully we hear some more color from the Fairfax team in a few hours time. Caroline Shin Bio: Caroline Shin is a seasoned tech entrepreneur and hospitality executive best known for co-founding Vacatia, a platform modernizing timeshare management. Key highlights of her career: • Built and sold Hotwire: As a founding team member, she helped scale the travel site before its $685 million sale to InterActiveCorp in 2003. • Led Starwood Hotels’ CRM strategy: Boosted market share by 20–40% for top properties through data-driven pricing and loyalty programs. • Founded Vacatia (2015): Created a tech platform serving 750+ resorts, helping owners rent/sell timeshares and manage operations digitally. • Launched Vacatia Partner Services (2023): Expanded into hands-on resort management, now overseeing 4,750+ units across the U.S.. • Co-founded Store Vantage: A SaaS tool optimizing staffing and customer relationships for small businesses. Trained as a nuclear engineer at MIT, she applies analytical rigor to solving hospitality challenges. Outside Vacatia, she runs a pet grooming business and advocates for Korean American community initiatives. Edit: Updated following Q4 24 CC, very good of Wade to break it out *Note: actual interest on the $170M warehouse will vary with SOFR. At a 5% base rate, SOFR+4% = 9% (≈$15.3M/year). If rates decline, interest expense will fall (and vice versa). The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate that reflects the cost of borrowing cash overnight using U.S. Treasury securities as collateral. It is widely used in financial markets as a replacement for LIBOR (London Interbank Offered Rate) for pricing loan bonds and derivatives. Weighted Average Yield: Fairfax's weighted average cash yield is robust based on the structured notes alone (excluding equity). On $810M of combined loan investment, the annual interest of ~$87M equates to roughly a 10.7% blended yield. Including the floating portion at current rates, the overall yield is in the low double-digits, which is very attractive for a secured, asset-backed investment. This reflects the risk profile (timeshare assets are somewhat niche and less liquid), but Fairfax negotiated rich terms. Company Comps Vacatia and Blizzard Vacatia: Company Analysis V3.pdf

-

Good pick up. We have a much better idea now

-

The way I see it, it doesn’t make much different to IV but does derisk the share price or potential for larger than market type movements. I did wonder last year whether some of those corrections may have been exaggerated due to the perceived TRS implications.

-

Personally I am very happy that they have started retiring the TRS. If they can close out roughly 10%/quarter it would be a thing of beauty. It was an asymmetric but highly leveraged bet that has worked out well. In a 50% draw down Fairfax stock would not be immune and there would be a beta amplification because of them. I think any indication of IV that it signals needs to considered together with liquidity and risk/reward considerations.

-

we probably need to pin this, but the bank (counterparty) is price agnostic, Fairfax is renting their balance sheet and taking the directional risk.

-

While I usually deplore SBC, in the case of Fairfax it was one of the aspects of the comps package that really got me across the line a couple of years back when I was on the fence about purchasing more. It got me thinking about the longevity of their employees and sharing in the upside as well as downside. Perhaps I needed a little convincing back then that it wasn’t some black box scam run by charlatans, the kind of company Muddy Water SHOULD have targeted.

-

That's cool. How they unwound was a key question for me. Looks like we may be getting an answer there

-

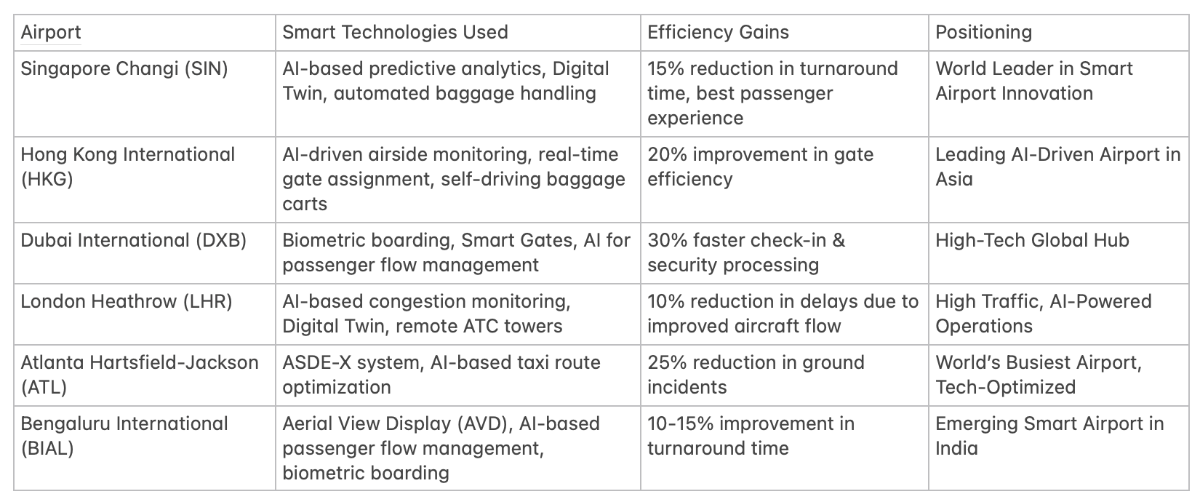

A few articles floating around about the introduction of Aerial View Display (AVD) at KIA. Some notes attached (geeking out) https://www.indianeagle.com/traveldiary/bengaluru-international-airport-aerial-view/ This is far more than just some CCTVs strung around the place. The productivity and safety gains make it a no-brainer, but from my reading, the primary headache is dealing with an individual airport's legacy IT backbone. While there are plans, only 5% of airports globally have made the leap. The fact that BIAL has completed a successful implementation shows class on many levels. I like this asset more and more and you can't help but think it can only further their case for the second airport. From the notes AVD Primer - BIAL.pdf

-

2002 in a former investco, then 2011 in personal accounts. First company I really had confidence in buying on the way up. Prior to a large position in BRK,it was mainly industrial cigar buts, and prior to the cigar buts I really had NFI. The evolution in thinking, to buy what you know and take advantage of periods of undervaluation and be wary but not afraid of concentration, was among the best lessons I have learnt. Thanks W & C.

-

I wonder if it is also a cleaner arrangement to be out of BIAL if they intend to bid on the 2nd airport.

-

Some further notes on the proposed sites for the second airport attached. Some thumb-suck estimates on the new build cost too: 30-50m passengers Land $US1.2bn Airport Construction $2.5bn Total ~$3.7bn Perhaps I need to rethink my lower bound $4bn valuation on KIA Bengalarus second airport: Nelamangala and Kanakpura Rd emerge as top choices (Hindustani Times) "To accelerate the project, the state government is considering inviting Bangalore International Airport Limited (BIAL) to spearhead the development, the report added. This move could help navigate the non-compete clause that restricts the construction of another airport until 2033. Officials believe BIAL, which successfully operates KIA, would be well-equipped to take on the new project." Why is Karnataka racing to finalise its 2nd airport site in Bengalaru? A neighbour is in the fight (The Print) But building the second airport also has its challenges. In its concession agreement signed with the Union government on 5 July2004, BIAL ensured that it remains the sole airport in Bengaluru, at least until 2033. “No new or existing airport shall be permitted by GoI to be developed as, or improved or upgraded into, an International Airport within an aerial distance of 150 km of the airport before the 25th anniversary of the Airport Opening Date,” according to the concession agreement. The only concession is for the development of Mysuru and Hassan airport. The new proposal by Karnataka is likely to complicate matters. “We are exploring if we can give the contract to build the airport to BIAL itself. In this way, they can waive off the non-compete clause,” the official cited above said. As of January 2024, Fairfax has invested approximately $7 billion in the country. Watsa stated, “In the next five years, we are looking at doubling that. We got a few projects already that we’re working on.” Indeed! Notes on Proposed Sites for Bengaluru’s Second Airport.pdf

-

That's along the lines of what I was reading. There seems to be a political angle, with various "officials" wanting the second airport in their jurisdiction. There also appears to be a bit of confusion, as the 90 million passengers the officials are getting their knickers in a knot over are slightly less than the 100 million capacity BIAL is currently designing T2 Phase 2 and smaller T1 upgrades to accommodate by 2030. There is always a fair chance that final passenger numbers are much higher than even the 90-100m envisaged, so perhaps there is merit in a second airport. A 2008 concession agreement between Bangalore International Airport Limited (BIAL) and the government prohibits new airports within 150 km of KIA until 2033. So, it is unclear to me if this will be tested. Plans for an airport in Hosur, in Tamil Nadu (40 km from Bengaluru), face legal hurdles due to this clause. The Hosur airport would also be at Karnataka's disadvantage, which is where the upside might be that BIAL gets an inside run on developing a second airport. BIAL have certainly proven their bona fides with T2. Challenges and Next Steps (as far as I can tell) Political Consensus: Ministers lobby for sites in their constituencies (e.g., Nelamangala vs. Kanakapura), but the government insists decisions will prioritize connectivity and economic impact. Land Acquisition: Estimated cost of ₹10,000 crore for 4,400–5,000 acres. Federal Approval: After finalizing the site, Karnataka plans to submit the proposal to the AAI by mid-February 2025. Estimated Timeline: A second airport will take 7-8 years, hence the sudden flurry. If BIAL gets the gig, great; if not, I'm happy to see deliberations drag on in true Indian style.

-

+1, I was just starting to look at them yesterday. The Indian market is a bit frothy so figured they might be a 20-30% overvalued. Based on “bullshit earnings” multiples I got the following: It is quite the range but whichever way you cut it seems undervalued on the FIH books. There has been a bit of chatter about the second airport too, so it will be fascinating to see how that evolves. Either way seems like a good margin of safety and I am sure we are looking forward to seeing what the market comes up with.

-

Good stuff, pass on my congrats to Ryan. It certainly touches on all the relevant points and reinforces the margin of safety even after some impressive gains. A rarity in this market. While $6bn for BIAL would be at the top of my range, $4bn is roughly my lower bound. Hopefully we find out what the market thinks relatively shortly. I also appreciated the %contribution of each sub to the ROA calc, again it just reinforces the low bar required to achieve an ROE of 15% now that they are paid to sit in the safety of treasuries. It also did a nice job highlighting the optionality that Bradstreet’s positioning offers….they will make out like bandits in a credit dislocation. The numbers tell a great story but coupled with the management mix of old wise heads and protégé's it should provide a very long runway indeed. Prem in the role as super coach, is where he adds the most value IMHO.

-

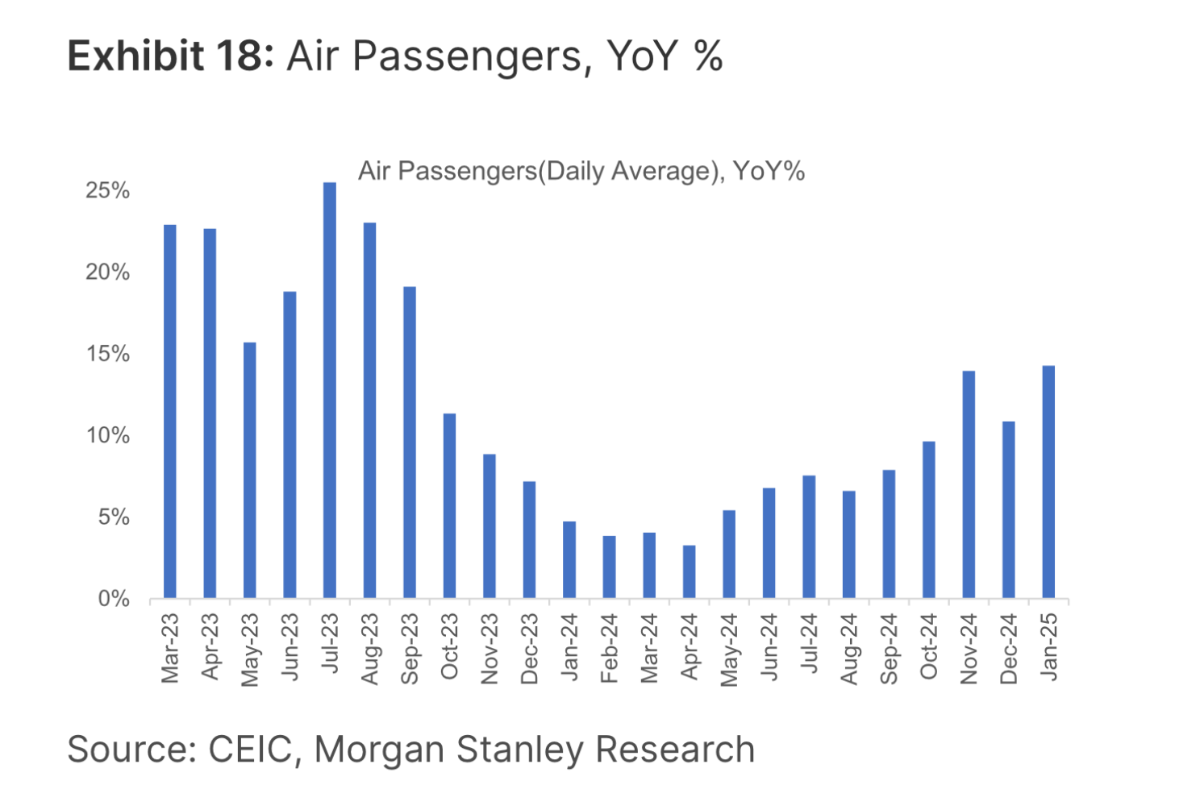

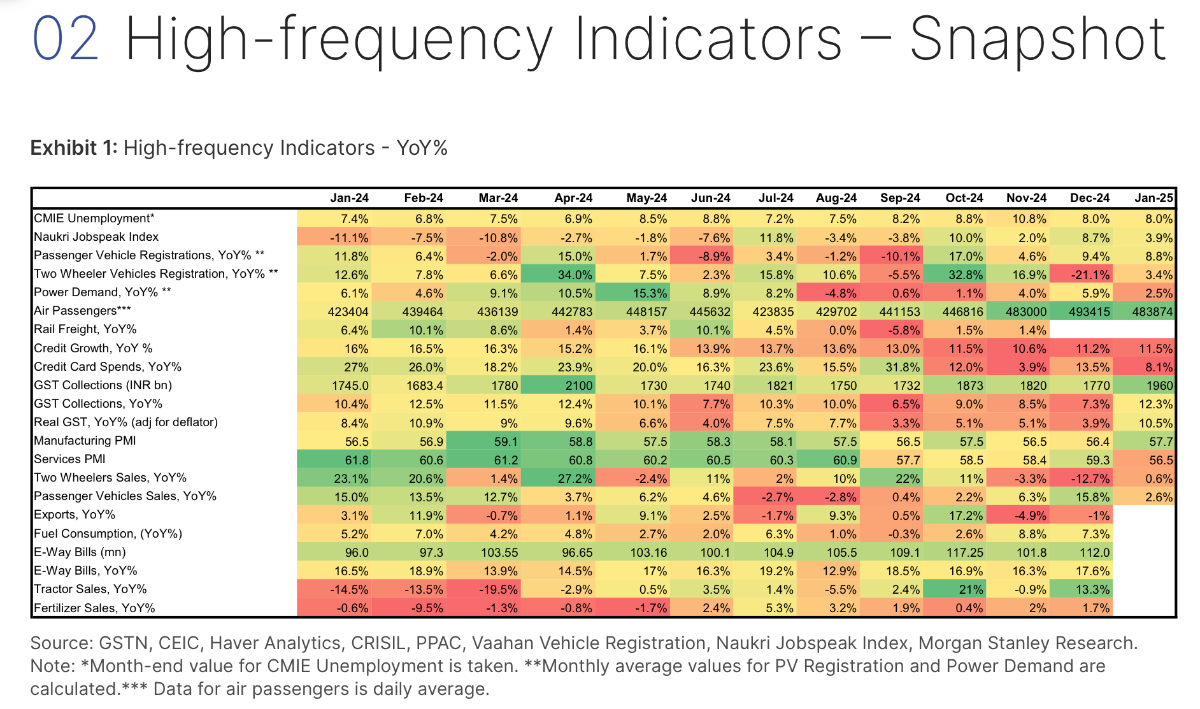

MS recently update their Indian macro chartbook. Healthy YoY Air Passenger growth.

-

I have attached a couple of notes on book + float valuation. It's something I have been pondering lately, and I guess it all comes down to what you can and ultimately do with the float. The prompts were (1) a valuation range of Fairfax based on Book+Float and (2) the circumstances under which you would ascribe 100% valuation to float. It is nothing particularly startling and has been covered before, but it may still be of interest. (It also tested the Deepseek R1 model via Perplexity, which is not bad given my minimal prompting). Fairfax Book + Float.pdf 100% Float Valuation.pdf

-

Good for you. Pics tell the story of money well spent

-

Never count out the vagaries of the market. I also think it is a little dependent on the ramp towards the Anchorage IPO later in the year. “Waiting for Godot” springs to mind. It will be interesting to see if we get any color via the Q4 CC or AGM. “If the IPO does not occur by September 2025, OMERS’ stake in Anchorage will remain fixed at 11.5% under a valuation protection mechanism. This prevents dilution of OMERS’ ownership, even if future valuations increase. Without the IPO, OMERS loses the opportunity to adjust its stake proportionally to Anchorage’s market value post-listing. Valuation Ratchet Clause • If the IPO proceeds but values Anchorage below the $2.6 billion valuation assigned to BIAL in 2021, OMERS is contractually entitled to additional shares to compensate for the lower valuation. • This “ratchet” mechanism ensures OMERS retains its economic interest relative to the agreed 2021 baseline, potentially reducing Fairfax India’s ownership share in Anchorage.”

-

True, I was referring to TSX60 inclusion and thinking that this may be more susceptible to declines in systemic downturns than the composite due to higher institutional flows i.e. Vol amplification.

-

The irony is not being in the index might help. Not to mention that fall in the Loonie and what it means for their large non-Canadian earning streams. But who knows, Mr Market is going to do his thing.

-

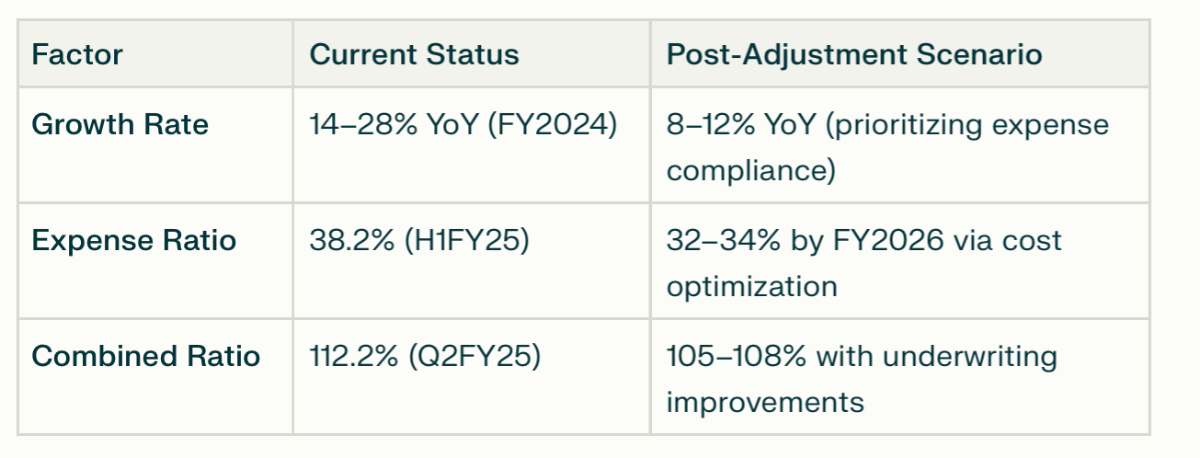

Looks like they have had to pull in their horns a little and perhaps explains the slower growth: https://www.financialexpress.com/money/expense-ratio-has-risen-post-eom-guidelines-go-digit-chairman-3651451/?t&utm_source=perplexity https://www.financialexpress.com/business/banking-finance-go-digit-receives-irdai-show-cause-notice-over-excessive-expenses-3649103/?t&utm_source=perplexity Go Digit’s expense ratio breach is directly tied to its growth strategy, particularly its rapid expansion in retail segments like motor and health insurance, which require significant upfront commissions and marketing costs. While the company has reduced its expense ratio from 41.1% to 38.2% in H1FY25, it remains above IRDAI’s 30% cap, prompting a show-cause notice for exceeding expenses in H1FY24 and H1FY25. Here’s how growth and regulatory compliance intersect: Growth-Driven Expense Pressures 1. Upfront Cost Recognition: • Go Digit’s business model incurs commissions and marketing expenses (₹572 crore in Q2FY25) immediately, while premiums are earned over the policy period. This mismatch inflates short-term expense ratios during growth phases. • Example: Health insurance premiums doubled YoY in FY2024, but associated commissions are expensed upfront, contributing to elevated expense ratios. 2. Retail Segment Focus: • Retail policies (motor: 69% of FY2024 premiums) require higher distribution costs compared to corporate segments. Go Digit’s 61,900+ partners in tier II/III cities drive growth but increase commission payouts. 3. Combined Ratio Impact: • Despite premium growth (14.2% YoY in Q2FY25), the combined ratio worsened to 112.2% due to rising claims (₹851 crore) and expenses. Underwriting losses widened to ₹244.83 crore, reflecting growth-related inefficiencies. Regulatory Response and Strategic Implications 3. IRDAI’s Show-Cause Notice: • The notice highlights non-compliance with the 30% EoM cap for H1FY24 and H1FY25. Go Digit attributes this to delayed regulatory feedback on its forbearance application (filed May 2023), but enforcement pressures are mounting. 2. Growth vs. Compliance Trade-Off: • Short-Term Slowdown Likely: To meet IRDAI’s cap, Go Digit may need to temper growth in high-commission segments (e.g., motor) and renegotiate agent commissions. This aligns with industry trends where insurers are shifting to lower-commission products. • Long-Term Scaling Strategy: The company’s 3-year glide path aims to reduce expenses through tech-driven efficiencies (e.g., AI underwriting) and portfolio diversification into fire/crop insurance (lower claims ratios) Spitballing:

-

MS provides limited coverage (attached). Based on the most recent IRDAI figures growth has slowed but that was off some pretty amazing figures. For non-life they have 2.85% of the market. If the market in aggregate grows double digits then even with no market share growth that should still look good in terms of float in 5-10 years time. No doubt the share price will bounce around but longer term this is a decent portion of the Fairfax thesis for me. Also consider the life insurance division, that is not publicly listed, has 0.28% of First Year Premiums after only getting a license in June 23. First year premiums measures new business but does not account for policy renewals or retention. So a decent but not completely perfect proxy for market share. If both get to around 3% market share towards the end of the decade then it will be quite the story. I think they are targeting closer to 5% market share Thinking more about the changes announced in the Indian Budget this morning: The Indian government’s move to allow 100% FDI in insurance addresses some structural challenges for foreign investors like Fairfax Financial Holdings, but it does not automatically resolve the specific regulatory hurdle Fairfax faces with its CCPS conversion in Go Digit Infoworks (parent company of Go Digit Insurance). Here’s a breakdown: Key Context of Fairfax’s CCPS Issue 1. Regulatory Rejection (2022–2024): • IRDAI blocked Fairfax’s proposal to convert its CCPS in Go Digit Infoworks into equity, as it would make the Indian promoter (Go Digit Infoworks) a subsidiary of Fairfax, violating rules that prohibited foreign-owned subsidiaries from acting as promoters of Indian insurers under the 74% FDI regime . 2. Structural Hurdle: • The rejection centered on the subsidiary rule, not the FDI cap. Even at 74% FDI, Indian promoters could not be subsidiaries of foreign entities. Fairfax’s CCPS conversion would have diluted founder Kamesh Goyal’s stake and shifted control . Impact of 100% FDI on Fairfax’s Case 3. Positive Developments: • Removal of Partner Dependency: 100% FDI eliminates the need for foreign investors to partner with Indian entities, simplifying ownership structures . • Regulatory Review: The government plans to “review and simplify” existing guardrails, potentially addressing restrictions on subsidiary structures. This could create a pathway for Fairfax’s conversion request. 4. Unresolved Challenges: • Subsidiary Rule Ambiguity: The 100% FDI announcement does not explicitly override IRDAI’s prohibition on foreign-owned subsidiaries acting as promoters. Without clarity here, Fairfax’s CCPS conversion remains in limbo . • Conversion Ratio Penalty: Go Digit was fined ₹1 crore in 2024 for failing to disclose changes to CCPS conversion terms, highlighting ongoing regulatory scrutiny of such instruments . Likely Outcomes • Requires Further Regulatory Action: For Fairfax to convert its CCPS, IRDAI may need to explicitly permit foreign-owned subsidiaries as promoters under the revised FDI framework. The Budget 2025’s promise to “simplify guardrails” could enable this, but no formal amendments have been announced yet . • Strategic Alternatives: Fairfax might pursue alternative structures, such as direct equity infusion into Go Digit General Insurance (the listed entity) or renegotiating the CCPS terms under the new FDI regime . Conclusion While 100% FDI removes the ceiling on foreign ownership, Fairfax’s CCPS issue hinges on whether IRDAI revises its subsidiary rule. The policy shift creates a favorable environment, but resolution requires specific regulatory adjustments. For now, Fairfax’s path to majority ownership of Go Digit remains conditional on further reforms. GODIGIT_20250109_1753.pdf