nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

@Viking impressive work. Its always difficult coming up with a single number for a company with so many moving parts. I like the way you haven’t “counted any chickens before they have hatched”. Some back of the envelope bracketing around your base case • Low Case (20%}: ~$126 (big cat year, equity decline) • Base Case (in line with yours): ~$176 • High Case (20%): ~$245 (bond rally, TRS, 10-15% equities, large one-off gain) The range illustrates just how much torque is now embedded in Fairfax’s earnings power, especially if markets cooperate or if we see continued strength in underwriting. If there’s one area where I think you may be on the conservative side, it’s net gains on investments. With Fairfax’s equities off to a solid start in 2025, and the potential for a drop in yields, there’s a real chance that line comes in materially higher than your $1.1B estimate—particularly if the FFH TRS continues to do its thing. But as always, better to err on the cautious side than bake in too much optimism. I think there’s a high probability we see Fairfax crack $200/share EPS at least once over the next 3 years. A bear market could obviously delay that, but would also likely set the stage for some truly impressive earnings if spreads blow out and they rotate into theopportunity. Still feels a bit surreal that we’re even contemplating earnings at these levels and that the floor might now be north of $100/share.

-

Syndicate -> Algo Platform ->Underwriting-as-a-Service (UAAS). It’s a beautiful thing. The investment banks will be falling over themselves to lead the IPO

-

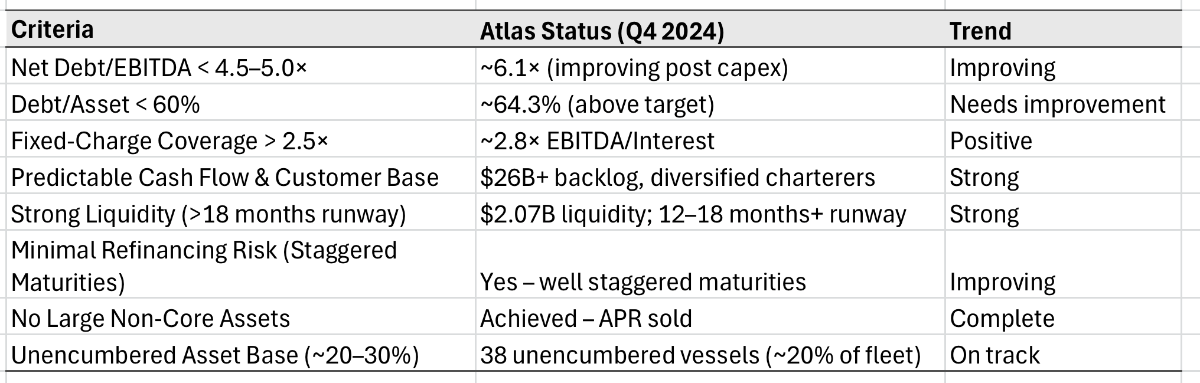

Achieving investment grade for Atlas will be an important development especially if we are H4L. Not 100% sure of the criteria but it may look something like this: Likely a ‘26 or ‘27 development but Atlas is still on a credible path.

-

Hopefully nothing in it but I felt like we never got a decent explanation for the departure of Graham Talbot. You get used to such longevity of tenure for Fairfax in general that it probably stands out more than it should.

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Galloway does a reasonable job of keeping his personality in check and letting Dr Fiona Hill provide some excellent insights…at least for me. (Transcript attached) Bio Dr. Fiona Hill has established herself as one of the world’s foremost experts on Russia and European geopolitics, with a remarkable journey from working-class origins in Northeast England to advising U.S. presidents and leading major academic institutions. Podcast Summary • The conflict is evolving from a bilateral issue to a global power realignment, with Russia, China, Iran, and North Korea forming a bloc against Western democracies • Modern great power politics is bypassing international institutions and sovereign rights, resembling 18th-century diplomacy where powerful nations carve up regions • Economic leverage matters more than military size - Europe has the economic power to stand against Russia without US support if they find the political will • Nuclear powers breaking security guarantees (as with Ukraine giving up nuclear weapons) risks global nuclear proliferation as nations conclude only nuclear weapons ensure safety • Trump and Putin approach negotiation with fundamentally different understandings - Trump seeks deals for business and nuclear reduction, while Putin seeks strategic dominance • The world is becoming increasingly multipolar, with "swing states" like India, Saudi Arabia, and Brazil gaining influence by refusing to commit to either major power bloc 20 MARCH • EP 341 • 1 HR 7 MIN..pdf -

Atlas/Poseidon Q4 is out. Another CFO departs. https://www.sec.gov/Archives/edgar/data/1794846/000162828025013894/sc-6kq42024.htm Key Highlights from Q4 2024.pdf

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Just watched Adolescence on Netflix. A remarkable achievement and a cut above the usual Netflix fare (98%RT). I am a big fan of Stephen Graham Co-creator and plays Jamie’s father. “This is England” is one of my faves. One Shot “The most talked-about aspect of “Adolescence” is its remarkable filming technique. Each hour-long episode was captured in a single, uninterrupted take – an extraordinary technical and artistic achievement. Director Philip Barantini, known for this signature style, explained: “Basically that means we press record on the camera, and we don’t press stop until the very end of the hour”. Subject Matter ”Beyond its technical achievements, “Adolescence” offers a profound examination of contemporary issues affecting young people. The series was conceived by Stephen Graham in response to a disturbing increase in violent knife crimes in Britain, including the murders of Ava White and Elianne Andam. Graham and Thorne wanted to explore the motivations behind extreme acts of violence against girls by young boys. The narrative particularly focuses on how online culture influences teenagers and the challenges parents face in understanding their children’s digital lives. Jack Thorne stated on BBC Radio 4 that they aimed to “look in the eye of male rage” and examine the influence of public figures like Andrew Tate on young boys. The series presents a nuanced exploration of how online radicalization can affect vulnerable young minds. As one reviewer noted, the show “articulates insights that surpass most recent portrayals of modern identity—highlighting how our offline experiences intertwine with our online personas, complicating the understanding of individual motivations and behaviors”. I think this is type of drama and societal statement the English do so well. It’s compelling, understated and reinforces what we know as parents, guardians, role models, we are ground zero but the predatory bastards don’t make it easy. Will be interested in what others think. -

It means nothing (too short a time frame), but this must be the best YTD portfolio alpha Fairfax has achieved in quite a while. Weighting is everything but the graph below gives a win/loss flavour in a soft market. SPY -3.2%and NASDAQ -6.2% (17/3/25)

-

It was certainly telegraphed via his letter but good to see it actually happen

-

TOKYO, March 17 (Reuters) - Warren Buffett's Berkshire Hathaway raised its holdings in five Japanese trading houses, regulatory filings showed on Monday, in the U.S. conglomerate's latest investments in Japan's top commodity firms that began nearly five years ago. https://www.reuters.com/markets/wealth/berkshire-raises-stakes-japanese-trading-houses-filings-show-2025-03-17/

-

It was the Pahar Trust https://www.pahar-trust.org/our-history

-

Speculation that final bids for IDBI will be in by June. https://www.financialexpress.com/business/banking-finance-financial-bids-for-idbi-bank-by-june-3775882/

-

You guys have a slightly unhealthy obsession with this analyst. Vacuous analysis attached Morningstar FRFHF Investment Report.pdf Fairfax Is Enjoying a Favorable Moment Morningstar.pdf

-

Yep long term its a high probability play structural tailwinds (demographics, digitalization, industrial expansion) should offset cyclical headwinds (monetary policy, global trade, geopolitical risks). It might play out something like this: Short Term (1-2 Years)→ Cautious Optimism (Recovery underway but external risks remain) Medium-Term (2-5 Years)→ Growth Acceleration (Domestic consumption + industrialization take hold) Long-Term (5-15 Years)→ Potential Superpower (If reforms, manufacturing, and global positioning succeed) Its a large part of my Fairfax thesis and I look forward to cringing as they are referred to as “the Berkshire of India” one day

-

MS released a note fessing up to missing the double tightening (fiscal and monetary). They see light at the end of tunnel, government capex (note attached). Government capex can kick start economic activity but you need a confident private sector to follow. To that end the current Tariff craziness is a stick in the spokes IMHO. It’s a balance between growing domestic consumption and the potential for a reduction in manufacturing investment by MNC’s. MS are pretty confident that a trade deal gets done, again I am not so sure but I hope so. Summary 1. India’s Growth Slowdown and Recovery • The slowdown was unexpected and attributed to double tightening of fiscal and monetary policy, even though macro stability indicators weren’t alarming. • Government spending contracted due to elections but is now recovering, especially capital expenditure. • Monetary policy was tightened via policy rates, liquidity conditions, and regulatory measures but is now easing. 2. Drivers of India’s Recovery • Government capex growth: The central government has increased capital expenditure. • Triple monetary policy easing: Policy rates, liquidity injection, and regulatory easing. • Lower food inflation: Boosting real household incomes and supporting consumption. • Services exports growth: India’s services exports have nearly doubled since 2020, helping sustain economic momentum. 3. Broader Consumption Recovery • Tax cuts for lower-income households to support urban consumption. • Lower inflation improving real incomes. • Job creation rebounding, supported by strong services exports. • NBFC regulatory easing to enhance credit flow. 4. Capital Expenditure (Capex) Outlook • Government capex is rising, with a focus on state government investments. • Private capex is lagging, affected by global uncertainty and weak goods exports. 5. Trade and Tariff Risks • India has low goods exports to GDP, making it less exposed to a global trade slowdown. • However, India faces direct tariff risks, especially on pharmaceutical exports to the U.S.. • A U.S.-India trade deal is expected by late 2025, but in the meantime, tariff uncertainties may impact investment sentiment. Conclusion India’s recovery is driven by domestic demand, strong services exports, and government policy support. Despite trade risks, India is less reliant on goods exports than other Asian economies, making it a potential outperformer in the region. ASIA_20250310_1915.pdf

-

Nice, if you aren’t climbing then the further from the maddening crowds of the EBC trek the better. Larkya La Pass looks amazing The Nepalese are some of the most wonderful people you will meet too. They are nice for the most part in Kathmandu but do get exponentially more friendly the further from Kathmandu you get. I had the good fortune as part of some charity work a few years back to visit villages that were accessible only by walking. Quite a profound experience, the people I met made me really question Western values and what it means to be happy. I hope you have a similar experience.

-

@DooDiligence Both of my treks - EBC/Island Peak (18 Pax)and Mera Peak (12 Pax) - we were running with reasonably large groups so organised everything before hand and were able to negotiate discounts accordingly. Even though we felt we had done our DD we still ran into issues though. On the Island Peak trip our porters just never showed up after we arrived in Lukla, our guides hired Yaks so no harm no foul. For Mera, our lead guide actually got lost with two of our party. It turns out the owner of the guiding company had done the Mera Peak trek previously just not actually our guide. Alltrails came in handy . The gear (microspikes etc) that they supplied was very ordinary in both cases. Depending on what you doing, anything mission critical such as spikes, down jacket, gloves mittens you want to BYO in my opinion. I was happy with the crampons and mountaineering boots for Mera but Island Peak was a bit of a shitshow in terms of mountaineering gear.. It really must be emphasised that the notion that Nepal has “trekking peaks” is a bit of a misnomer. Anything above 6000m can turn very ugly very fast and you need good mountaineering clothing especially boots. All the guiding companies will tell you about their success rates but in reality only about 30% actually bag the trekking peaks. For us it was 7/18 for Island Peak and 3/12 for Mera Peak. You might be able to wing it and find a guide in Kathmandu but for me having an idea of cost and itinerary before hand helped me a lot. In both cases our guiding company provided good support before we even arrived in Nepal and that was worth it alone. Haven’t been to Bhutan but it sounds interesting

-

Yes, $25m seems likely to be a regulatory minimum to play. I would imagine this scales quite quickly. All in all a very exciting development, they now have the holy trinity of insurance. I am sure this process must have felt like pulling teeth at times, it took 7 years but they got it done. I would go so far as to say the liberalisation of the indian insurance industry is in no small part because of Kamesh and Fairfax. Their success with Go Digit General Insurance likely strengthened their credibility with regulators when pursuing additional licenses. The fact that this approval came during the final board meeting chaired by IRDAI Chairman Debasish Panda suggests it may have been viewed as a capstone achievement of the regulatory regime’s liberalization efforts. A pleasure to watch

-

Kamlesh Goyal, Prem Watsa-backed Value Attics Reinsurance gets Irdai nod “There was a longstanding need to have private reinsurance players in India, and becoming India's first private reinsurer marks a significant milestone for us. With this, the Digit group of companies (general insurance, life insurance, and reinsurance) will strive to become a one-stop solution for all insurance needs, allowing us to provide full-spectrum risk coverage,” said Kamesh Goyal, Value Attics Reinsurance. This was a long time coming but perserverence has paid off. Congrats to Kamesh & Co Some further background The timing of this approval is particularly noteworthy as it occurred during the last board meeting chaired by IRDAI Chairman Debasish Panda, who completed his three-year tenure at the regulatory body on the day the approval was announced. During his chairmanship, Panda had consistently advocated for increased foreign direct investment in the insurance sector, including a call for 100% FDI to achieve the ambitious goal of “insurance for all” by 2047. This vision reflects a recognition that India’s insurance penetration, which stands at merely 4.2% according to the Economic Survey 2021, requires significant capital infusion and market dynamism to reach its full potential. The approval of Valueattics Re can thus be seen as a parting achievement that aligns with Panda’s broader vision for the sector’s development. The entry of Valueattics Reinsurance into India’s reinsurance market is expected to have profound implications for the competitive landscape, particularly for the state-backed GIC Re, which has long maintained its dominant position as India’s primary reinsurer. GIC Re has operated with significant advantages, including the first right of refusal for reinsurance business from Indian insurers and mandatory cession requirements, which have helped it maintain a 60% market share in India’s reinsurance market as of FY17, up from 45% in FY16 and 43% in FY15. However, these regulatory advantages have gradually diminished, with mandatory cession requirements declining from 15% in FY13 to 5% more recently, reflecting the regulator’s incremental efforts to create a more level playing field. With Valueattics Re entering the market with strong financial backing from established players in the insurance ecosystem, GIC Re will face unprecedented domestic competition. This competitive pressure is likely to drive GIC Re to innovate, refine its pricing strategies, and enhance its service offerings to maintain its market position. The combined ratio performance of GIC Re, which has historically hovered around or slightly above 100% (100.16% in FY17, 107.03% in FY16, and 108.86% in FY15), may come under additional scrutiny as private competition introduces more efficient operations and potentially more aggressive pricing strategies. This dynamic could ultimately benefit insurance companies and policyholders through improved service quality and potentially more competitive reinsurance terms. Beyond the bilateral competition between GIC Re and Valueattics Re, the market currently includes thirteen foreign reinsurance branches established by global reinsurance companies. These international players, including Munich Re, Swiss Re, and Lloyd’s of London, bring substantial global expertise and capital resources to the Indian market. The IRDAI has been actively recalibrating the regulatory framework governing these entities, as evidenced by the Draft Amendment proposed to come into force on April 1, 2023, which aimed to harmonize provisions applicable to Indian Insurers, Indian Re-insurers, Foreign Re-insurance Branches, and Lloyd’s India. A notable provision required every India-based Foreign Re-insurer, including Lloyd’s, to maintain a minimum retention within India of 50% of Indian Reinsurance business underwritten, with allowances for retrocession to International Financial Service Centre Insurance Offices.

-

Its my understanding that they have 5 years but you are correct in that it would eventually need to be voted on: The continuing preservation of the 41.8% voting power of the multiple voting shares is subject to a majority of the minority shareholder ratification vote (i) at the annual meeting of shareholders following the period ending December 31, 2020 and any one or more consecutive five-year periods thereafter during which the number of our outstanding shares (multiple voting shares plus subordinate voting shares) has increased by at least 25%, or following any calendar year more than five years after the last ratification vote (or after August 31, 2015) if the number of our outstanding shares (multiple voting shares plus subordinate voting shares) has increased by at least 50% since the last ratification vote (or after August 31, 2015); (ii) if we intend to issue more than 50% of our outstanding shares in a single transaction; and (iii) within five years after V. Prem Watsa is, for whatever reason, neither our Chairman nor our CEO. At August 31, 2015, the number of our outstanding shares (multiple voting shares plus subordinate voting shares) was 23,583,605. https://www.fairfax.ca/wp-content/uploads/2025/03/FFH-Notice-and-Circular-March-7-2025-2.pdf

-

Some notes on Amy Sherk, Fairfax’s new CFO attached. Another 20+ year appointee, succession planning at its finest. Amy Sherk- The New Chief Financial Officer of Fairfax Financial Holdings….pdf

-

Damn, that voting machine….it get’s me every time. If you are under the age of 25 you get a free pass btw

-

MS with the note and a decent upgraded PT of €3.18 for Eurobank. That sounds more like it Nida. Summary 1. Investment Outlook: Still More to Go • Greek banks remain rate-sensitive but benefit from solid loan growth (+7.5-8%), underpenetrated fee income, and normalized cost of risk (COR). • Valuations are still cheap at 6.5x FY26e P/E, with a 25% upside on average. • Morgan Stanley raises its 2027 rate assumption to 1.5% from 1.0% and lowers the cost of equity (COE) by 100bps, improving the growth outlook. 2. Earnings and Dividend Projections • Net interest margin (NIM) compression due to rate cuts is expected to be fully offset by loan and fee growth. • 50% dividend payouts expected between 2025-2027, returning ~25% of the market cap in dividends. • Greek banks are trading at a discount to European peers, but this gap is expected to narrow due to strong GDP growth (2.2% in 2025 vs 0.8% EU avg). 3. Stock Ratings and Price Targets • Piraeus Bank (BOPr.AT) upgraded to Overweight, Eurobank (EURBr.AT) downgraded to Equal-weight, while Alpha Bank and National Bank of Greece (NBG) remain Overweight. • New price targets: • Piraeus: €6.14 (previously €4.94) • Alpha Bank: €2.64 (previously €2.11) • Eurobank: €3.18 (previously €2.77) • NBG: €10.66 (previously €9.05) 4. Comparative Valuations • Greek banks trade at 0.8x FY26e P/B vs EU banks at 1.1x. • Greek banks’ Return on Tangible Equity (ROTE) is 13%, in line with EU peers in 2025 but slightly lower in 2026 due to lower leverage. 5. Individual Bank Highlights • Alpha Bank (Overweight): Strong balance sheet, lower NPEs, resilient to rate cuts, 6% loan growth CAGR expected. • Eurobank (Equal-weight): Best-in-class returns but risk/reward better at Piraeus and Alpha. • Piraeus Bank (Overweight): Cheapest valuation, NPE ratio below 3%, significant capital return. • NBG (Equal-weight): Capital return story, slower earnings momentum expected. 6. Risks • Macro environment remains fragile, potential shocks could impact recovery. • Absorption of EU recovery funds could be slower than expected. • Higher-than-expected cost of funding could affect profitability. Love their work, sounds like our friends at Morgan Stanley might be leaning in a little more to the great European rotation where you bravely depart P/E 25’s and modest growth and invest at P/E 7 for a 15% grower. Brave stuff indeed. EEMEA_20250307_0401.pdf

-

I think like a lot of us, the on-again off-again tariff spat makes it difficult to call. Without getting into the politics, I think energy/oil is almost too important to receive the full brunt if Tariffs really do go ahead. https://www.canadianenergycentre.ca/explainer-why-canadian-oil-is-so-important-to-the-united-states/#:~:text=“Light” and “heavy”,qualities in between the two When I started assembling the notes SCR was trading in the low 20’s, at that price the risk seemed priced in. The share price has since bounced so a slightly lower margin of safety now. A higher risk in the short to medium term is oil in the 40’s. Longer term that will be a great setup. For a long term holder of assets that sort of volatility is an opportunity for Fairfax not a threat. I think we can all see what they (Fairfax) are assembling and that is a basket of these types of assets. As long as you don’t overpay you do OK over the full cycle. OK => Good, with float leverage.

-

I tend to agree. I wouldn’t see it as a negative though. I think where analysts are missing the mark arises from the unknowable (timing wise) but inevitable rise in yield spreads. Howard Marks touched on this recently and rationalised it but you can guarantee he’s not swinging for the bleachers. https://www.oaktreecapital.com/insights/memo/gimme-credit