nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

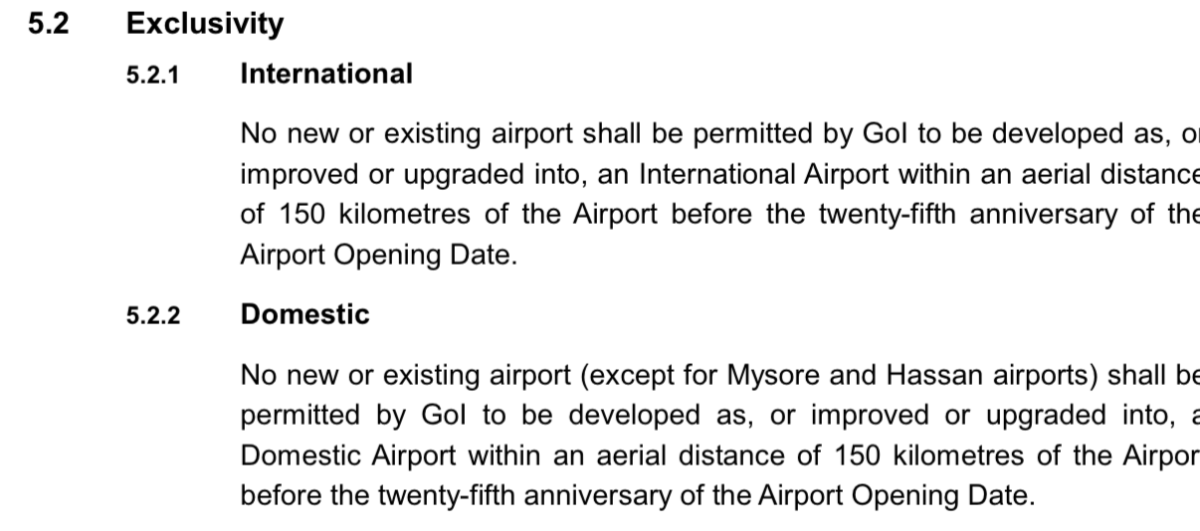

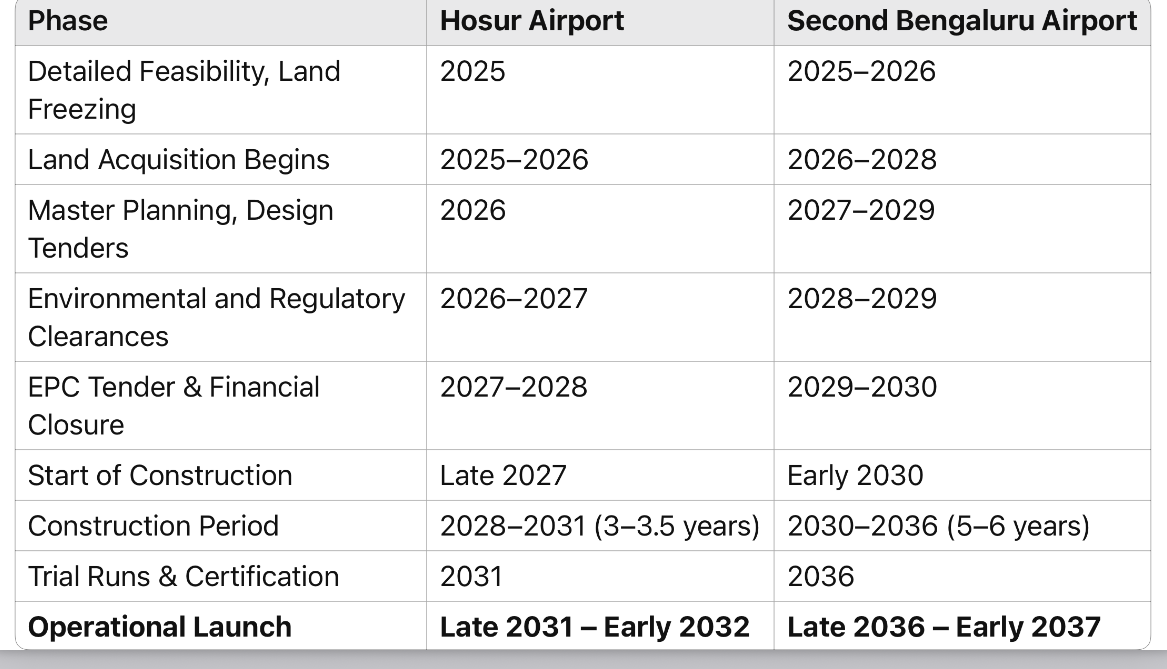

I tend to agree, at least in the medium term (20 years). Referring back to the exclusivity clause it depends on your definition of development but it’s hard to see a work around that doesn’t involve BIAL. https://www.civilaviation.gov.in/sites/default/files/2023-02/moca_000743.pdf Typically development would extend to: -Land Acquisition -Planning and Approvals -Zone changes etc Some possible timing to bring on either option (Hosur or 2nd Bangalore airport) Perhaps throw Chennai into the mix “They (the Chief Minister and Watsa’s delegation) discussed various potential investment opportunities in Tamil Nadu, including Chennai and Hosur Airports. As the majority owners of the world-class airport in Bengaluru, they are keen to leverage their expertise to develop such facilities in Tamil Nadu also,” Thiaga Rajan said” https://www.deccanherald.com/amp/story/india/tamil-nadu/fairfax-ceo-meets-tamil-nadu-cm-stalin-discusses-chennai-and-hosur-airports-3516836

-

It’s an interesting development. I don’t have any more insight into this than you. Just trying to demonstrate pros-cons. Thinking about the recent article it does allay some fears about the sunset. My concern is that their leverage is reduced with the second Bangalore airport and the time it takes to come on line in terms of the exclusivity. I can see Hosur working even if it is a bargaining chip. Potentially I can actually see Kepegowda plus two 30m passenger airports. BIAL’s position is strengthened if they get to participate in both, with Hosur first.

-

Are these actual questions or are you just trolling?

-

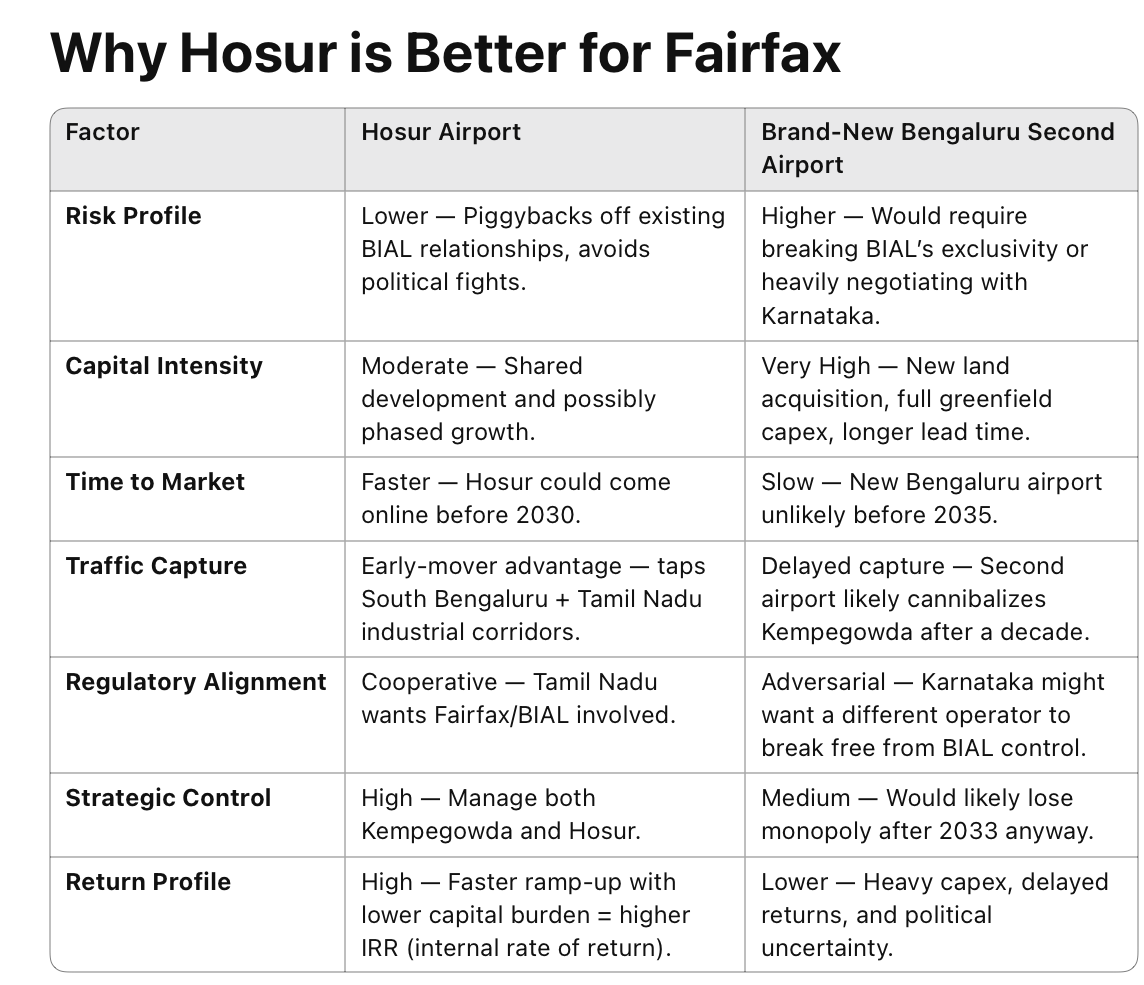

https://www.moneycontrol.com/news/india/tamil-nadu-cm-meets-fairfax-bial-officials-as-hosur-airport-plan-gathers-pace-13007659.html Interesting development, if Hosur is given the greenlight under BIAL management does this preclude the second airport in Bangalore? Hosur might be a better bet for Fairfax than a brand new airport that falls outside the exclusivity agreement

-

I think you will find even quality insurance companies are running 100%+ CRs in India: Top-tier private insurers (ICICI Lombard, HDFC ERGO, TATA AIG) target and get close to 100%-103% combined ratios. Mid-tier growth-focused players (Go Digit, SBI General, Bajaj Allianz) run moderate underwriting losses (105%-110%), but acceptable for their growth phase. Public sector insurers (New India, United India) routinely run very high losses (~120%+), but they survive due to government support and investment income. Here’s why: Price wars: Intense competition, especially in motor and retail health insurance, forces companies to underprice premiums to gain market share. Mandatory loss-making products: Insurers must sell motor third-party insurance at regulated prices that often don’t cover claims. Fast claims inflation: Healthcare and repair costs rise faster than premium adjustments. Younger industry: With only ~20-25 years of history, the private insurance sector in India is still maturing, leading to more pricing errors. Public sector drag: State-owned insurers routinely underprice risks for social obligations, distorting competitive pricing. Investment income cover: Historically, high bond returns allowed insurers to tolerate underwriting losses, masking the real problem. Regulatory price caps: Insurers can’t freely raise prices to match rising claims, especially in health insurance.

-

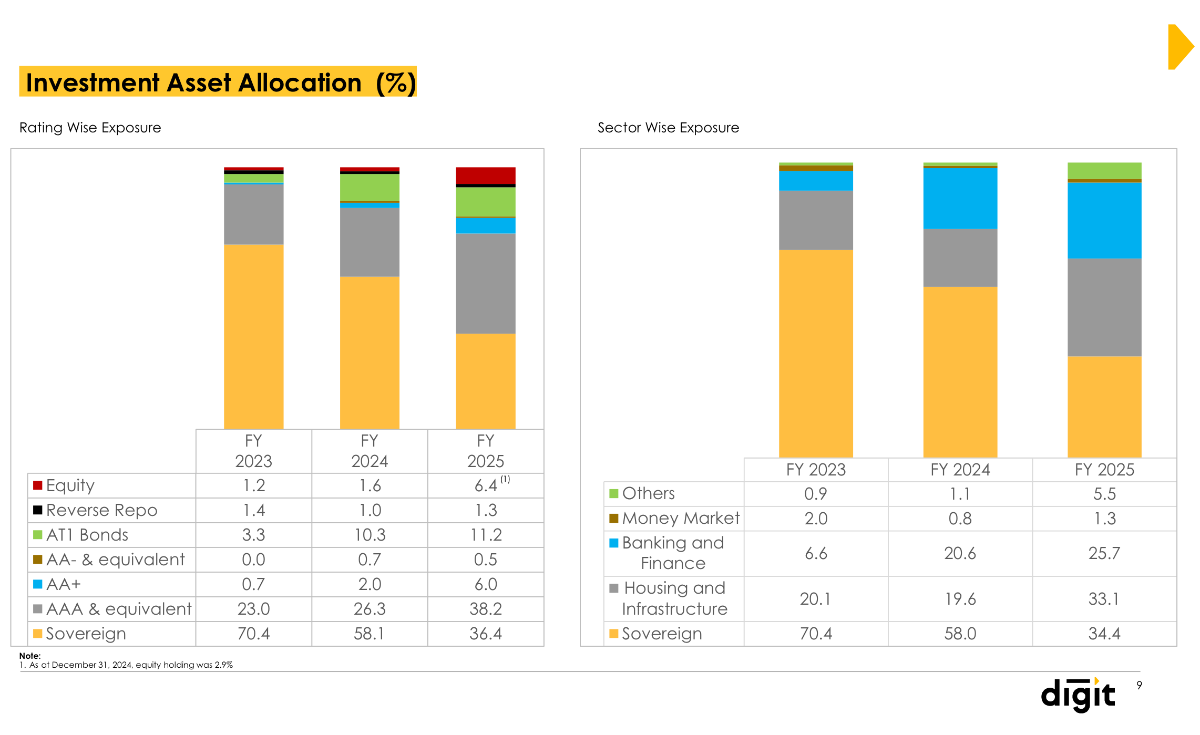

MS review of the Q4 results (attached). Some additional points: 1/n Accounting Method Impact: The report explains the impact of the new 1/n method of accounting for long-term policies, which affected GWP growth (reported 10.3% vs. 13.5% excluding 1/n impact) Unlike some competitors, Go Digit fully accounted for commissions on deferred premium, ensuring PAT remained unchanged despite the accounting change Expense Management Progress: EOM (Expenses of Management) ratio improved to 33.4% under the old method, a reduction of ~3 percentage points vs. FY2024 The company is on track to achieve its EOM regulatory targets in FY2026, which is significant as many industry players have struggled with this compliance Normalized Loss Ratio Guidance: Management provided specific guidance for "normalized" loss ratios of approximately 70%, with flexibility of 2 percentage points due to mix changes and catastrophic events This suggests they see current elevated loss ratios as temporary and expect improvement Investment Portfolio Strategy: Beyond just increasing equity allocation to 10%, the report shows Go Digit has been adjusting its fixed income portfolio mix There's been a substantial reduction in sovereign debt (36.4% vs. 58.1% in FY2024) and increases in AAA & equivalent bonds (38.2% vs. 26.3%) AT1 bonds exposure increased to 11.2% from 10.3% in FY2024 Commercial Lines Opportunity: The report highlights "others" segment (commercial lines) forming 16% of GWP and growing 31% YoY This is identified as a key growth driver, suggesting a strategic shift toward higher-margin commercial business EPS Trajectory Expectations: Morgan Stanley projects significant EPS growth: ₹4.42 in FY2025e → ₹6.29 in FY2026e → ₹8.07 in FY2027e This represents 42% CAGR over two years, which is substantial but still wouldn't justify the current P/E of 65.1x FY2025e earnings without sustained growth beyond this period Competitive Intensity Outlook: Morgan Stanley notes management expects competitive intensity to abate in retail lines as regulators focus on EOM compliance In health insurance, they've observed pricing improvements in smaller renewals post April 1, 2025, suggesting market rationalization may be beginning Changing Reinsurance Dynamics: The report mentions "higher reinsurance capacity" as a potential driver for growth in commercial lines This suggests improved availability of reinsurance support, which had been constrained in previous years. What is the 1/n Method? The "1/n method" refers to a specific accounting approach for recognizing premium revenue from long-term insurance policies that was implemented by the Indian insurance regulator (IRDAI) effective October 1, 2024. Under the 1/n method: 1. Premium Recognition: For multi-year policies (particularly long-term motor insurance policies), premium is recognized evenly over the policy term instead of all upfront. 2. Mathematical Calculation: If a policy is for 'n' years, only 1/n of the premium is recognized as Gross Written Premium (GWP) in each year of the policy term. 3. Accounting Treatment: The remaining premium moves to "Unexpired Premium Reserve" instead of being counted in the current period's GWP. How the "1/n" Accounting Change Affects Go Digit Insurance What Is 1/n? When selling multi-year insurance policies, Digit now must spread premium recognition evenly across years instead of counting it all upfront. Five Key Impacts on Digit 1. Makes Growth Look Slower: Reported growth: 10.3% (with 1/n) vs. 13.5% (without 1/n) For a growth-focused company like Digit, this affects market perception 2. Makes Underwriting Look Worse: - Combined ratio appears higher (111.3% vs. 109.7%) -Creates false impression of deteriorating performance 3. Creates Comparison Problems: -Different companies handle this change differently -Digit records all commission expenses upfront while others might defer them Makes competitor comparisons misleading 4. Affects Regulatory Targets: - Impacts ability to meet IRDAI's asset requirements - Digit already needed special permission (forbearance) for previous targets 5. Complicates Investor Communication: -Management now reports two sets of numbers -Requires more explanation to show true business performance Bottom Line This accounting change distorts Digit's financial metrics without changing the actual business performance. Their profit remains the same, but reported premiums and ratios look different. Management emphasizes focusing on true economic performance rather than accounting metrics during this transition. GODIGIT_20250428_2250.pdf

-

Tidy set of results from Digit. https://www.godigit.com/content/dam/godigit/general/investor-relations/financial-information/financial-results-q4-fy2024-25.pdf CC Slide deck https://www.godigit.com/content/dam/godigit/general/investor-relations/stock-exchange-disclosures/investor-presentation-for-q4-fy-2024-25.pdf CC: https://www.godigit.com/content/dam/godigit/general/investor-relations/investor-call-recordings/investor-call-recording-q4-fy-2024-25.mp3 Go Digit General Insurance Reports Exceptional Financial Performance in FY2025 Go Digit General Insurance Limited has announced its audited financial results for the quarter and year ended March 31, 2025, showcasing remarkable growth across key metrics. The company's performance demonstrates strong business momentum, improved profitability, and enhanced financial stability. Financial Highlights Year-over-Year Performance (FY2025 vs FY2024) Go Digit has delivered outstanding financial results for FY2025, with profit after tax surging by 133.9% year-over-year to ₹42,494 lakhs from ₹18,168 lakhs in the previous fiscal year. This significant profit growth substantially outpaced the 14.1% increase in gross premium written, which rose to ₹10,282.24 lakhs from ₹9,011.06 lakhs in FY2024. The company's earnings per share more than doubled to ₹4.65 from ₹2.08 in the previous year, representing a 123.6% increase. This remarkable EPS growth reflects the company's success in translating premium growth into enhanced shareholder value. Income from investments showed strong performance, increasing by 26.2% to ₹1,10,910 lakhs, contributing significantly to the overall profitability. Quarterly Performance (Q4 FY2025) The fourth quarter results were equally impressive, with profit after tax growing by 119.5% compared to Q4 FY2024, reaching ₹11,561 lakhs. While this represents a slight decrease of 2.8% quarter-on-quarter from Q3 FY2025, the substantial year-over-year growth demonstrates the company's strong trajectory. Gross premium written in Q4 FY2025 reached ₹2,572.98 lakhs, up 10.2% from Q4 FY2024, though it decreased by 3.8% from the previous quarter. This seasonal fluctuation is consistent with industry patterns, as noted in the company's financial statements. Segment Performance Go Digit has achieved growth across all major business segments, with particularly strong performance in certain areas: Marine Insurance The Marine segment emerged as the fastest-growing business line, with net premium earned increasing by an extraordinary 107.2% year-over-year to ₹978 lakhs. Q4 performance was even more impressive, with 279.8% YoY growth and 379.8% QoQ growth, highlighting the company's expanding market share in this segment. Fire Insurance The Fire segment demonstrated robust growth, with net premium earned rising by 35.8% year-over-year to ₹11,926 lakhs. The quarterly performance showed 65.0% YoY growth and 57.1% QoQ growth, indicating strong momentum in this business line. Crop Insurance Crop insurance showed significant growth with a 21.5% year-over-year increase to ₹65,727 lakhs. The Q4 performance was particularly strong with 46.9% YoY growth and an impressive 61.6% QoQ increase, demonstrating the company's growing presence in agricultural insurance. Health Insurance The Health Group Corporate segment, a major contributor to revenue, grew by 16.4% year-over-year to ₹1,32,208 lakhs. The Health Retail segment also performed well with a 13.3% increase to ₹6,682 lakhs. Motor Insurance Motor, the company's largest segment by revenue, delivered steady growth of 9.1% year-over-year to ₹5,42,405 lakhs. While Q4 showed a slight 0.9% QoQ decline, the 4.8% YoY growth for the quarter indicates stable performance in this competitive segment. Key Insurance Metrics and Financial Strength Insurance-Specific Performance Indicators Go Digit demonstrated meaningful improvements in several critical insurance metrics: Solvency Ratio: Significantly strengthened to 2.74 from 1.61, well above the regulatory requirement, indicating robust capital adequacy and enhanced ability to absorb unexpected losses. Combined Ratio: Slightly improved to 104.5% from 104.8%, showing disciplined underwriting despite aggressive growth. While still above 100% (indicating underwriting losses before investment income), the trend is positive. Incurred Claim Ratio: Increased marginally to 73.9% from 72.7%, reflecting slightly higher claims relative to earned premiums. This warrants monitoring but remains within acceptable industry parameters. Expenses of Management Ratio: Improved to 39.0% from 41.3%, demonstrating better operational efficiency and cost control. Net Retention Ratio: Decreased to 80.1% from 85.8%, indicating the company is ceding more risk to reinsurers, potentially as a prudent risk management strategy during rapid growth. Return on Equity: Maintained at approximately 7.2%, showing consistent shareholder returns despite significant capital expansion. Earning per share (Basic): More than doubled to ₹4.65 from ₹2.08, reinforcing the company's ability to translate premium growth into shareholder value. Persistency Ratios: While not explicitly disclosed, the strong premium growth suggests healthy policy renewal rate These metrics collectively paint a picture of a company balancing growth with prudent risk management. The improved solvency and expense ratios are particularly noteworthy, as they suggest the company is strengthening its financial foundation while scaling operations. I had the opportunity to touch base with Kamesh at the AGM. He seemed upbeat on the Indian economy exiting its slow patch. He indicated they have some new products that they were excited about e.g. cattle insurance. Also reiterated that it is proving harder to outgrow the pie but remained bullish longer term on the ability of the overall insurance pie to grow. CC Notes 1. Growth Outlook: - Expect industry growth of 3-4% next year - Potential growth in commercial lines (fire, marine, liability) - Motor segment growth to be monitored month-by-month - Potential increase in third-party premium rates -Fire could be the next segment to move to 5% market share - Kamesh mentioned that when looking at Gross Written Premium (GWP), Go Digit expects to grow 1.7-1.8 times faster than the industry's growth rate. 2. Health Insurance: - Competitive market in April, but early signs of improvement - Loss ratios remain competitive across different health segments - Comfortable with current competitive intensity 3. Underwriting and Profitability: - Focused on improving combined ratio - Small improvements can significantly boost profits due to high leverage - Not dependent on capital gains - Expect improvements from rate increases and renewal book maturity 4. Expense Management: - Reduced expense ratio by 2.9% in FY25 - Expect IRDAI to take steps to reduce commissions - Shifting towards lower commission, higher-quality business 5. Investment Strategy: - Increased equity allocation from 2.9% to 6.4% - Targeting 10% equity allocation - Investment yield at 7.2% without capital gains

-

Excellent, some upgrades were on my personal catalyst list. Probably saves them 30-40bps on future borrowings. Fitch Upgrade – April 2025 IDR: A- (from BBB+), Outlook: Stable Why the Upgrade? Strong underwriting: 92.7% combined ratio (7 years profitable) Large holding company cash: $2.3B High net income: $3.9B in 2024 Solid capital: Prism score “Strong” Improved fixed-charge coverage: 10.6x Current FLR (Financial Leverage Ratio) 30.3% consolidated 25.9% excluding non-recourse debt Future Upgrade Triggers Combined ratio in low 90s FLR ≤ 25% (or ≤ 21% ex-non-recourse) Prism score: Very Strong Continued reserve releases Downgrade Triggers Combined ratio ≥ 95% FLR ≥ 32% (or ≥ 28% ex-non-recourse) Holding company cash < $1B Reserve hits or major leveraged acquisitions

-

Made my morning

-

Some notes from the meeting: 1. Strategic Clarity & Investment Focus Helios Fairfax Partners has sharpened its investment focus around four core themes aligned with Africa’s long-term growth: “There’s essentially two mega trends that are most relevant to investing in Africa now and far into the future. One is demographics and urbanization, and the other is technology.” HFP’s investment strategy emphasizes: • Consumer Non-Discretionary • Digital Infrastructure • Financial Services & Fintech • Tech-Enabled Business Services These sectors are selected for their secular growth and resilience, forming the backbone of both the co-investment and seeding efforts. 2. Legacy Asset Transition – Nearly Complete A major strategic shift has been the wind-down of legacy assets from the pre-Helios era: “You fast forward to 2024, that 100% [legacy portfolio] is now 8%… and the remaining 92% is represented by Helios-managed investments.” • ~$280M in legacy assets (2020) reduced to ~$22M by 2024. • “We’ve retained or recovered at least 90% of the value of that legacy portfolio.” This capital was redeployed into high-conviction, growth-aligned investments. 3. High-Conviction Co-Investments & Venture Bets HFP has demonstrated disciplined deployment into high-growth opportunities: Co-Investments: • Tron (medical distribution in Morocco) • Helios Towers • M2P (banking SaaS for India, Africa, MENA) “Our co-investments, taken as a whole, were up 17% year on year… up about 50% since inception – that’s the 1.5x you see.” Venture & Seeded Investments: • Galatea Bio (genetic data for drug discovery) • Moment (African payment aggregation) • SeamlessHR (enterprise SaaS for HR) “The digital ventures portfolio was up 10%, and our sports & entertainment investments were up 18%.” These investments outperformed both local and global benchmarks: • Co-investments beat MSCI Africa by 14 pts, S&P 500 by 4 pts. • Seeded investments beat MSCI Africa by 10 pts . “It’s clear we are generating quite material alpha, which is obviously the point.” 4. Fee and Carry Income – A Key Weakness, but Improving The transition to a multi-strategy platform has temporarily weighed on earnings: “In 2024, we received no TopCo distributions into HFP… the residual revenue effect of our below-target 2020 fundraising.” “So, the present is not great, but the outlook… is generally positive in this regard.” Current fundraising momentum is encouraging: • Private Equity Fund V: Near first close toward $750M • Climate Fund: $200M raised, targeting $400M • Sports & Entertainment: $50M of $75M secured “The funds that really make the biggest difference from a fee standpoint are going quite well.” 5. Market Discount – A Story of Complexity, Not Fundamentals Despite improving fundamentals, the stock trades at a deep discount: “As of March 31… the shares are at a minimum, 60 to 70% of the value.” “The share price is close to an all-time low… I think it’s probably close to the largest [discount] that it’s been.” Management attributes the discount to structural opacity: “It feels… quite difficult for people to connect all of the dots amidst all of the noise that’s been going on.” 6. 2024 Financial Performance – Transition Pain Reflected in Numbers • NAV dropped from $500M to $423M, down 12% YoY. • Driven by: • $55M drop in carried interest valuation • $22M in startup/transitional costs • Missed 15% compounding target, but underlying investments performed well . “We’re not there yet… but we believe the groundwork has been laid.” 7. Organizational Stability and CFO Transition New leadership is in place to streamline financial reporting and operations: “We appointed an interim CFO… Mike Corporal… 25 years in senior finance roles including CFO at Franklin Templeton.” A simplification plan is underway to make reporting and valuation clearer to investors. Investor Outlook The core investment strategy is showing strong early results. The transition from legacy holdings is nearly complete, co-investments are compounding at ~19% IRR, and seeded investments are performing well. Fundraising is improving, and organizational streamlining is in progress. The primary challenge remains narrative clarity and income visibility. If the team delivers on simplification and sustained fee income, the discount could narrow materially.

-

This was my (dodgy) transcript from that section ————————- ‘We very close partners with the state government, and therefore the state government trusts us and involves in all these involves us in all these discussions. So like you might be pointed out, there are exclusivity at that stage. What one must remember is that all the peak hours, and it's really 1585 and 15 million. That growth is coming from filling up the values, right? And the city is already choking at that point of time, because there's need for further capacity, and that capacity is going to come only. So we're aiding the government here. We were involved in the selection of those three sites. We recommended our favorite our part of those three sites, because we believe that that was the best process for the central government, as was going to happen at all points of time in this discussion, what we were trying to do is protect our interests at no point, because our interest.” Future Airports: "We're trying to hire the best possible candidates... We need several more, especially in the ambition of operating more airports, and the opinion for privatization, acquire more airports, several more CEOs and senior leaders in those positions." Government Privatization Signals: Gopal noted: "The government has been talking about many privatizations, infrastructure assets, more airports... 12 or 13 airports are likely to come up now, so we are migrating." "Last time they were advertising their airports, we also participated, but we participated with discipline. We were outdid by more than substantially." ————————— Consistent with your summary they are very much involved in this process. I came away with a good vibe. Prior to today my concern was that given the long lead time on construction a competitor could cut ground prior to the expiration and started operating after expiration. Much less concerned now, especially after the manning comments. It also reinforced the competitive advantage Fairfax has when it comes to developing the talent

-

Awesome. Anything stand out compared to what we have discussed here? Any thoughts on the “interesting time” in which live? I.e. tariffs, $<60 oil etc

-

Just a quick follow up. MS ran a sensitivity study on the implied pricing at ~€2.05 ——————— Cost of Risk is a key profitability metric for banks. It measures how much the bank sets aside for potential loan losses, expressed as a percentage of total loans. Formula: CoR = Loan loss provisions / Total loans It reflects credit quality. A higher CoR means the bank expects more loans to go bad, so it sets aside more in provisions. A lower CoR signals stronger asset quality and fewer expected defaults. —————— 1. Base Case (Morgan Stanley’s Official Valuation) Fair value: €3.18 Implied upside: ~55% • Loan growth (2025–27): ~7% CAGR • Fee & commission growth: +7% • Net interest margin: ~2.4% • Cost of risk (CoR): ~0.5% • Return on equity (ROE 2027): 14.6% • Valuation multiple: 1.23x P/BV on 2027e book • Dividend payout: ≥50% Morgan Stanley’s view: Solid balance sheet, decent growth, improving returns. They expect normalization—not acceleration—and still see strong returns and capital return to shareholders. 2. Stress Case (What the Market May Be Pricing In) Fair value: ~€2.07 Implied ROE: ~10.1% Stock price: matches this scenario • Loan growth (2026–27): ~4–5% • Fee growth: ~4% • NIM: 2.25%-2.3% (implied) • CoR: Raised to 0.9% • Rate sensitivity: ECB rates cut by 50bps • EPS hit: -30% by 2027 vs base • ROE (2027): Falls to 10.1% • Valuation multiple: 0.73x P/BV on 2027e Book • Dividend payout: Still assumed ≥50% Morgan Stanley’s view: This is a conservative macro view—slower growth, higher risk, and softer margins. But crucially, this already appears priced in at a €2.05 share price. It comes down to how hard we think Europe slows, however there seems a decent margin of safety IMHO EEMEA_20250408_1454.pdf BANKS_20250407_0330.pdf

-

Looks like they are going to blow this up good and proper. That Tropic Thunder line springs to mind

-

Take it that is EGFEY? To add to your points the margin ratios I am offered are crap too, no doubt due to liquidity and market cap. Unfortunately I can’t buy it directly on the Greek exchange thru my fleecer of choice.

-

+1, the policy is ham fisted but those delivering the messaging have been disastrous. It is incompetence beyond belief. To go one step further it is also the bond market that is the adult in the room (it was always thus).

-

I think you are being a bit kind in terms of “resident expert” but I agree it’s cheap. Hopefully we may learn a bit more about how they are seeing things later this week if they have some representation at Fairfax’s AGM. I still think they are worth between €3.5-4 and the MS analyst who I think is one of the better ones out there has her target at €3.18. Attached is her latest weekly comps, it’s looking like an outlier at these levels and was around the price I bought it a few months back. I think the future still looks very bright. EEMEA_20250407_0857.pdf

-

Stuff it, its a shitshow but this did give me a chuckle

-

I am not saying it is great policy its just coming from the author it seemed semi rational. I came at this from a perspective it was completely nuts and have been working up from that point. I can see a scenario if there was some clever considered participants it could be accomplished but this is a matter of expediency. Hence the markets shitting dual bricks of economic knock ons and governance. Its worth ranking against the alternatives and its obvious its a timeframe decision:

-

True, the notion of “fair trade” flips the entire post-WTO framework on its head. The problem is, enforcing “fairness” in this model requires leverage, and that increasingly looks like extortion and coercion. The irony is, the U.S. helped build the post-WWII system precisely to avoid this kind of transactional coercion. WTO rules, MFN status, binding arbitration — all of it was designed to prevent the strongest country from throwing its weight around unilaterally. It’s been fraying for a while though and the ‘China shock’ has put it into overdrive. I always figured that demographics would take care of China.

-

I have been reading Miran’s “user guide” on the flight to Toronto. The thesis is actually quite sound but with the caveat that it requires incredibly careful execution, diplomatic finesse, and institutional coordination — all of which are in short supply under a populist, confrontational presidency. Even if he is not the most characteristic guy, I think Miran does a much better job of explaining than Trump but more importantly Lutnick. Final Evaluation: Miran’s User’s Guide rationally supports a coherent post-globalization strategy in theory – combining tariffs and currency policy to force fairer burden-sharing – and it provides a toolkit to do so. The Trump administration is embracing the toolkit (especially tariffs) but runs the risk of misapplying it by neglecting the careful balancing acts emphasized in the paper. The plan can succeed only if pursued as an integrated, flexible strategy rather than a one-dimensional trade war. Both proponents and critics can find ammunition in this analysis: Pro-Strategy Argument: The current global trade arrangement unfairly disadvantages the U.S.; this plan offers a way to correct course, restore industrial competitiveness, and make allies and rivals alike contribute their fair share. It uses leverage the U.S. uniquely has and can do so without domestic harm if executed wisely (as 2018–19 showed). Overvaluation and imbalances are unsustainable; better to address them on U.S. terms now than face uncontrolled crises later. Against-Strategy Argument: The plan gambles with the global economic order. It could provoke retaliation, drive away allies, and destabilize financial markets. Legal unilateralism might isolate the U.S. and weaken the very system that underpins its financial power. The assumptions of smooth currency offset and limited retaliation may not hold at larger scales, risking inflation or recession at home. There are also moral and geopolitical costs to aggressive tariffs on poor nations and coercive tactics on allies, potentially ceding leadership to others in the long run. His own words: ”There is a path by which the Trump Administration can reconfigure the global trading and financial systems to America's benefit, but it is narrow, and will require careful planning, precise execution, and attention to steps to minimize adverse consequences.” It’s not the only way to achieve rebalancing but it is credible.

-

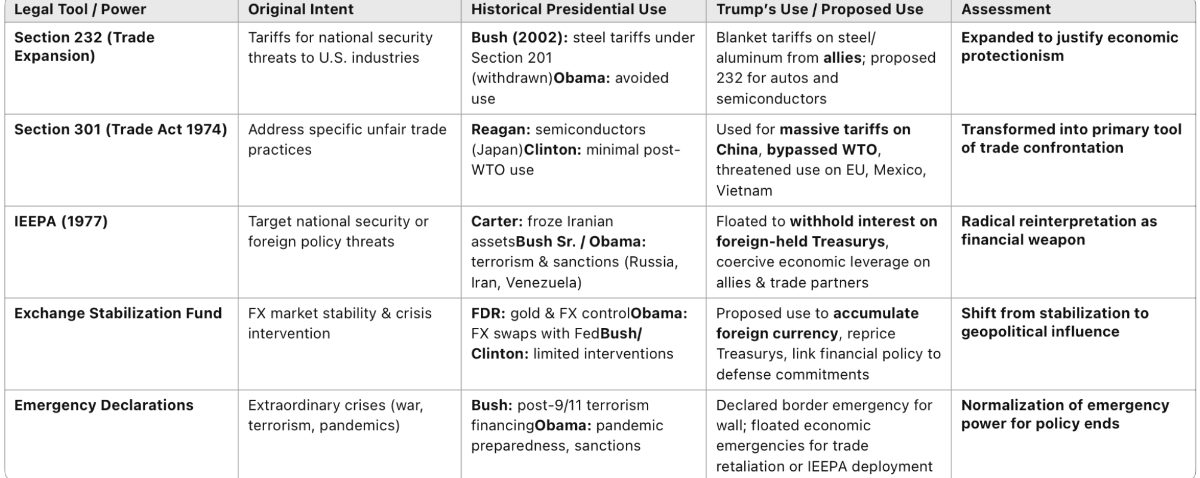

It’s interesting to see how each of the Executive Economic Powers maps against its original intent and how they have been “recast”. Other presidents have used these tools — but typically in response to war, terrorism, or short-term crises. Trump’s innovation is weaponising them as a standing policy framework to reshape the global order.

-

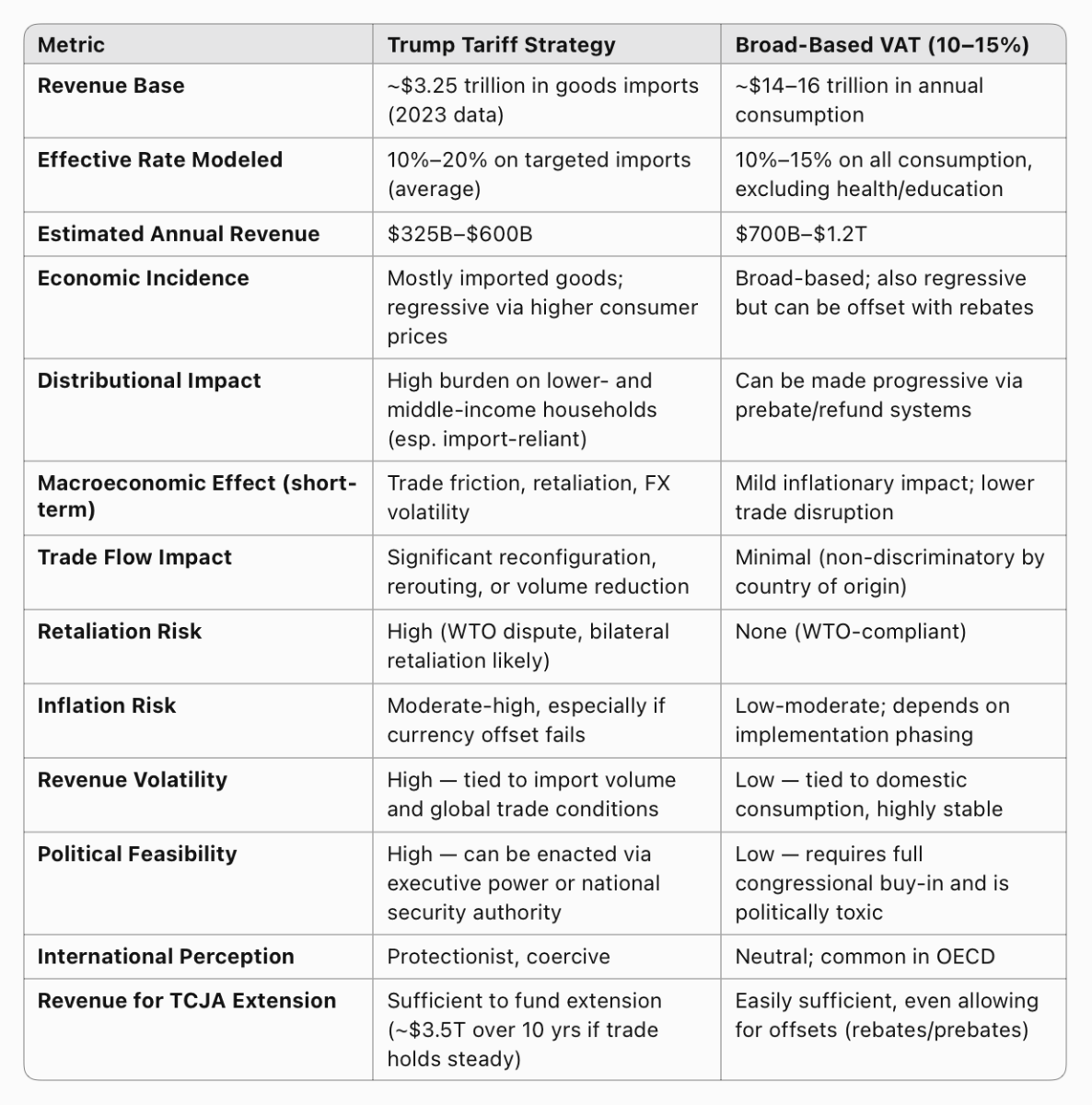

Thinking about these Tariffs as a consumption tax that can be implemented by the executive branch is quite helpful (at least to me). It’s not just about tax of course it is also a reordering of global trade relations, a middle finger to the WTO and a radical expansion of executive authority, all under a veneer of strategic policy. https://www.hudsonbaycapital.com/documents/FG/hudsonbay/research/638199_A_Users_Guide_to_Restructuring_the_Global_Trading_System.pdf • Trump’s tariff model prioritizes unilateralism, geopolitical leverage, and populist framing — but comes with higher risk, volatility, and lower efficiency. • A VAT is economically cleaner, more stable, and widely used globally, but politically infeasible in the U.S. due to its regressive optics and anti-tax sentiment. Take home: If the goal is stable, long-term, deficit-neutral tax cut financing, VAT wins on fiscal grounds. If the goal is populist optics and tactical trade leverage, the Trump tariff doctrine is more aligned — but at substantial macro and global risk.

-

Made my day!

-

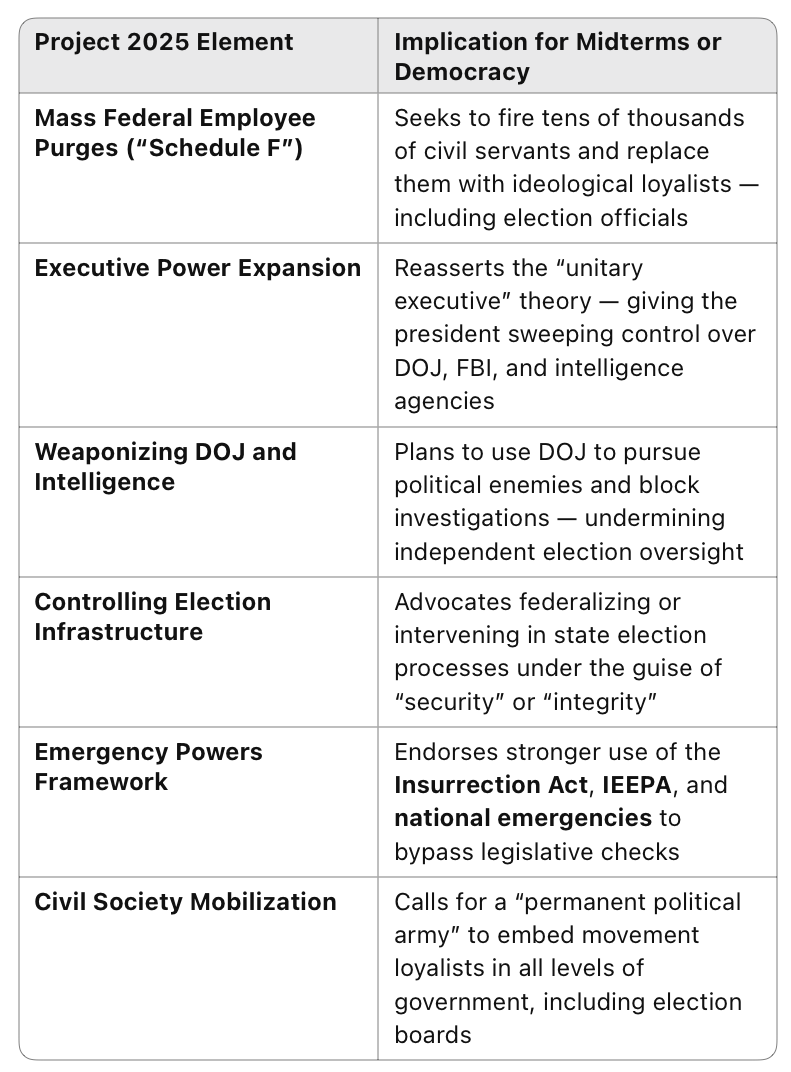

I think this one won’t get up but it sows the seeds, hence an important development. The mid terms will be front of my mind now for many republicans. There was an insightful post above that questioned whether there will be mid terms. Thinking about this some more in a probabilistic fashion: I am sure he will give it a crack though. The Project 2025 framework provides some insight: Why This Matters for the 2026 Midterms Project 2025 doesn’t just plan for presidential transition — it lays groundwork for capturing and consolidating state and federal election machinery, including: Installing Trump-aligned state-level attorneys general and secretaries of state Conditioning federal funding on compliance with federal “election integrity” standards Pre-clearing election plans, especially in urban and Democratic strongholds Building a legal and narrative basis to challenge any loss as illegitimate In other words: Project 2025 is the playbook to make disruption legal — or at least procedurally shielded. If this oversteps the mark in terms of politics, @Parsad feel free to delete. It’s more about trying understand the various mechanisms in a probabilistic fashion than a political commentary. It’s very difficult to even remotely understand the logic. Even the tank the market and roll at lower yields doesn’t pass the scratch and sniff because of the obvious sovereign risk implications. If markets believe the chaos is orchestrated or systemic, not temporary, they’ll demand higher yields later due to: Political risk Policy volatility Inflation uncertainty Governance concerns As much as everyone believes the markets are tanking because of the economic implications, I think it is more about the governance implications. Perhaps it is as simple as a consumption tax that you get to put lipstick on as a nation building initiative then pass that tax cut that was your real MO.