nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

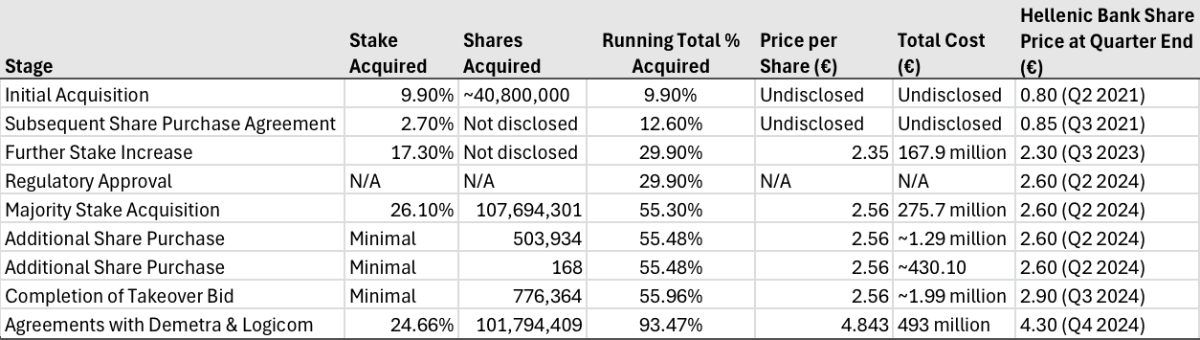

I am sure that it is not lost on anyone, but I did find it interesting that the way the deal is structured via installments it is actually cheaper than the 10% they bought from Siemens last year for $250m last year, even if it is notionally $5m more • June 2023: Acquired an additional 3% equity interest for $75 million. • December 2023: Acquired an additional 7% equity interest for $175 million. Use a discount rate of your choice, but I get $238m in January 2025 dollars at r=10%

-

I much prefer the modern Fairfax approach. A weekend spent reviewing the short thesis, a sensible rebuttal, the courtesy of a question at the CC, then on with business. That Munger quote on wrestling pigs springs to mind.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Was waiting for an update on this. Hopefully you enjoyed it. I will never forget seeing this for the first time and then pressing replay countless times Was almost a techno Viking moment, but maybe because of the cameos -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

That was great. We had the good fortune to attend our local SO as they performed Beethoven’s 9th over the weekend. Every time I hear it is a constant reminder that there is not a wasted note, and one of the finest pieces of music of all time. Conductor Jaime Martin Soloist Lauren Fagan soprano Margaret Plummer mezzo-soprano Stuart Skelton tenor Sam Dale Johnson bass MSO Chorus Warren Trevelyan-Jones chorus Stuart Skelton was a standout

-

Quite possibly, these guys have more under utilised IQ points than I have in aggregate. Some thoughts nonetheless: 1. 2x's interest coverage may be the lower bound for covenants. 3x's give them a shot at IG. I think they don't have a choice at the moment given higher for longer 2. This play is a small but important part the overall Fairfax portfolio. If rates rise then Atlas sucks but Fairfax rolls at higher yield. Rates fall then Atlas becomes very profitable. 3. Good chance that there will be an embedded buyout clause in the novations. 4. These guys are clever, hopefully Brian Bradstreet is in someway involved on the debt side and advising as part of the broader portfolio 5. The only head scratcher is why are paying divs at this stage in their growth A rough cut on sensitivity: CURRENT POSITION (Q3 2024): Interest Expense: $174.6M quarterly ($698.4M annualized) Operating Earnings: $334.6M quarterly ($1,338.4M annualized) Current Interest Coverage: 2.3x Total Borrowings: $10.39B Average Interest Rate: 6.66% RATE SENSITIVITY: Interest Rate Changes (Annual Impact): +100bps: Additional Interest: +$103.9M New Interest Coverage: 1.96x Coverage Decline: -14.8% +50bps: Additional Interest: +$52M New Interest Coverage: 2.12x Coverage Decline: -7.8% -50bps: Interest Savings: -$52M New Interest Coverage: 2.48x Coverage Improvement: +7.8% -100bps: Interest Savings: -$103.9M New Interest Coverage: 2.69x Coverage Improvement: +17% FAIRFAX PERSPECTIVE: At higher rates: Atlas interest burden increases Fairfax investment portfolio yields improve Net positive for Fairfax despite Atlas stress At lower rates: Atlas profitability improves significantly Each 100bps = ~$104M annual impact Could accelerate path to investment grade Edit: In terms of divs, Fairfax may also see this as the return of capital phase as opposed to return on capital. Just spit balling.

-

A Tradewinds article (attached), reporting on Q3, indicates that the five vessels sold to ONE were then leased directly to OOCL, difficult to determine if this falls within the ONESEA JV. It makes you wonder whether Atlas has maxed the balance sheet, especially with the other novations. Time will tell. “Key Financial Metrics: Revenue: Up 34.7% to $601.4M ("Revenue was up at $601.4m, versus $446.6m") Net Profit: Down to $130.6M ("net profit in the third quarter was $130.6m, down from $142.9m") Interest Costs: Up 86.5% ("financial costs rose, notably interest to $174.6m from $93.6m") Strategic Moves: August Vessel Transaction Ordered 6 x 13,000 TEU vessels "Five of these contracts were novated to ONE in September 2024" Subsequently chartered by ONE to OOCL on 15-year terms June Newbuild Program "Four of these contracts were immediately novated to a customer" "13 of these contracts were thereafter novated to certain nominees and upon delivery, these 13 newbuilds will be chartered by the Company from such nominees under bareboat charters" Operational Execution: "During the first nine months of the year, it took delivery of 23 newbuildings at a cost of $2.4bn" "As at 30 September, Seaspan had 36 vessels under construction, down from 40 at the end of 2023" Strategic Implications: Moving from pure ownership model to mixed approach Financial pressure driving innovative structures Maintaining operational presence while reducing capital intensity Strategic relationship with ONE evolving (27.8% ownership) ONESEA JV represents new direction in service provision Conclusion: Seaspan are adapting to financial constraints while trying to maintain their market position, but the loss of the OOCL charter opportunity (through ONE) suggests they would prefer direct ownership when possible. This looks more like strategic adaptation to circumstances than a deliberate shift away from the ownership model.” Seaspan sells five boxship newbuilding contracts to ONE as profit falls TradeWinds.pdf

-

Estimating Seaspan’s % of the global fleet. For the want of a better number I always figured 10% might be a material threshold CURRENT POSITION (Q3 2024): - Seaspan: 1,874,000 TEU - Global Fleet: 27.5M TEU - Current Market Share: 6.81% FUTURE POSITION (Est. 2026-2027): Seaspan Growth: - Current: 1,874,000 TEU - Newbuilds (36 vessels): ~450,000 TEU - Future Seaspan Total: ~2,324,000 TEU Global Fleet Growth Projection: - Current: 27.5M TEU - Industry orderbook: ~7.2M TEU (through 2026) - Estimated scrapping: ~1.5M TEU - Projected 2026 Global Fleet: ~33.2M TEU Future Market Share Calculation: 2,324,000 TEU / 33,200,000 TEU = 7.0% Key Context: - Seaspan's growth is secured through firm orders - Global fleet growth includes confirmed orderbook - Position as largest independent owner will be maintained - Share calculation considers both newbuild deliveries and vessel retirements - Excludes any potential M&A activity or additional orders Key Benefits at 10%: Shipyard Pricing: Better newbuild pricing and priority slots Financing: Improved terms and broader funding options Operating Costs: Enhanced economies of scale Charter Markets: Greater influence on charter rates Industry Influence: Stronger voice in regulatory and industry matters

-

Indeed I did, thanks

-

This filing from 2021 (which may well be out of date) shows the reconciliation. It differentiates Fairfax Finacial’s position in Eurobank when including the Hellenic Financial Stability Fund (33%) and excluding HFSF (34.7%). https://www.eurobankholdings.gr/en/grafeio-tupou/etairiki-anakoinosi-20-07-21?utm_source=chatgpt.com “The HFSF holds shares in Greek banks as part of its mandate to stabilize the financial sector following the Greek financial crisis. However, it does not operate as a typical shareholder: • Voting Rights: The HFSF often holds restricted or limited voting rights. In some cases, it abstains from regular shareholder votes unless explicitly required to act in its supervisory role. • Non-Commercial Ownership: Unlike private shareholders (e.g., Fairfax), the HFSF’s primary goal is to ensure financial stability rather than profit or exert influence for strategic or operational decisions.”

-

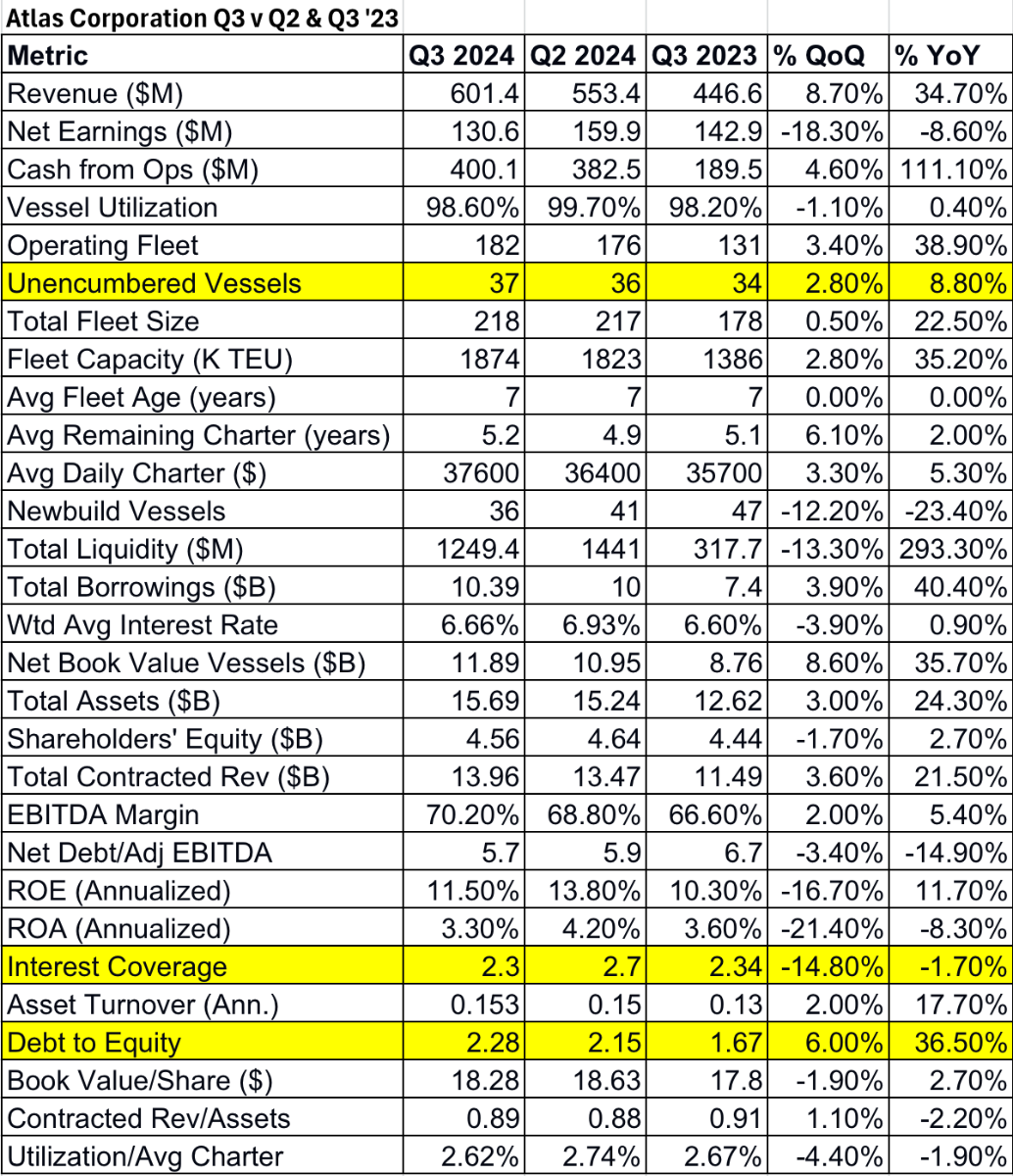

Atlas has reported https://www.sec.gov/edgar/browse/?CIK=0001794846 Quick Summary Financial Performance: Revenue Q3 2024: $601.4M (up 34.7% from Q3 2023) Year-to-date: $1,676.5M (up 35.4% from 2023) Growth primarily driven by delivery of 41 newbuild vessels since September 2023 Operating Results Operating earnings: $334.6M in Q3 2024 (up from $218.5M) Net earnings: $130.6M in Q3 2024 (down from $142.9M) Operating expenses increased to $107.6M (up 15.9%) Vessel utilization improved to 98.6% Cash Flow & Liquidity Operating cash flow: $400.1M in Q3 (up from $189.5M) Total liquidity: $1.25B Cash: $549.4M Undrawn credit: $700.0M Total borrowings: $10.39B Weighted average interest rate: 6.66% Fleet Operations: Current Fleet 182 operating vessels Total capacity: 1,873,880 TEU Average vessel age: 7 years Fleet utilization: 98.6% Vessel Development 36 vessels under construction 6 newbuilds delivered in Q3 3 additional deliveries in October/November New orders for six 13,000 TEU and six 13,600 TEU vessels Strategic Developments: Formed ONESEA Solutions joint venture with ONE Entered sale-leaseback financing for multiple vessels Significant vessel order activity with both owned and novated contracts Dividends: Q3 dividends: $52.0M (down from $208.0M in Q3 2023) Year-to-date dividends: $156.0M (down from $274.0M) Balance Sheet Position: Total assets: $15.69B (up from $13.07B end of 2023) Shareholders' equity: $4.56B Total borrowings-to-asset ratio: 66.2% Future Outlook: Strong contracted revenue stream with $23.5B in gross contracted cash flows Continued fleet expansion through newbuild program Focus on maintaining high utilization rates and operational efficiency Strategic emphasis on long-term contracted cash flows and fleet modernization Ongoing capital investment in fleet maintenance and expansion

-

Very happy to be wrong as I think Eurobank would be wise to repurchase shares here. Not to mention the conflict of capital return decisions that may be at odds with the other 67% of shareholders Edit: fixed typo

-

In terms of Eurobank buybacks, Fairfax currently sits at 32.93% from YE 23 annual report. As far as I can tell, 33% is a key threshold (Article 24 of Greek Banking Law 4261/2014, aligned with CRD IV and enforced by the Bank of Greece). "Crossing the 33% threshold means Fairfax would have “significant influence” over Eurobank under regulatory definitions. This can result in additional scrutiny and obligations, including: • Regulatory Approval: • Fairfax would need to apply to the Bank of Greece to increase its stake beyond 33%. • The approval process would involve assessing Fairfax’s financial health, governance practices, and the impact of its increased influence on Eurobank’s operations. • Suitability Review: • Fairfax’s ability to contribute to the stability of Eurobank would be evaluated. • Regulators might scrutinize Fairfax’s other investments, its financial strength, and its strategic intentions for Eurobank. • Increased Oversight: • Greater regulatory oversight may apply to Fairfax, especially if it is perceived as the controlling shareholder. This could involve regular disclosures and accountability for Eurobank’s governance and strategic decisions." 1. Fairfax could always sell into the buyback, but would they want to? 2. They could always seek approval to cross over the threshold, but if they felt that way, I think they would have pushed for it when this was a true 25c dollar. This may change Some notes attached. It's still a good story for Fairfax, even if proves to be a stream of divs Edit: It looks like they are already at 33.29% as of Q3 24 https://www.eurobankholdings.gr/en/investor-relations/shareholders/shareholding-structure#:~:text=The percentages of Eurobank Holdings' voting rights,Group Companies (CGC)*** * Helikon Investments Limited**** Threshold notes.pdf

-

@Viking like Fairfax, Eurobank still seems incredibly cheap even after a decent revaluation. The best way to own it is via insurance leverage. However, I must confess I broke my own rule of not owning Fairfax positions and picked up some EGFEY last week as a bit of a cashflow non-USD play. Personally think it should be valued closer to €3. Fokion Karavias is a fascinating guy and a top operator. There is something about these chemical engineers that end up in banking/insurance, need to add that to the investment pattern recognition algo Education: • National Technical University of Athens: Earned a degree in Chemical Engineering. • University of Pennsylvania, Philadelphia, USA: Obtained both a Master’s and a Ph.D. in Chemical Engineering. Professional Career: • JPMorgan, New York (1991): Began his banking career in the Market Risk Management Division. • Citibank, Athens (1994): Served as Head of Fixed Income Products and Derivatives in Greece. • Telesis Investment Bank (2000): Held the position of Treasurer. • Eurobank Group (1997–Present): • Joined as Head of Fixed Income and Derivatives Trading. • Progressed through roles including Deputy General Manager and Treasurer (2002–2005), General Manager and Executive Committee Member (2005–2013), and Senior General Manager overseeing Corporate & Investment Banking, Capital Markets & Wealth Management (2014–2015). • Appointed CEO of Eurobank SA and Eurobank Holdings in 2015. Board Memberships and Affiliations: • Hellenic Bank Association (HBA): Vice Chairman of the Board of Directors. • Hellenic Federation of Enterprises (SEV): Member of the General Council. • Greek Tourism Confederation (SETE): Honorary Member of the Board. • Eurobank Private Bank Luxembourg SA: Former Board Member (2012–2022).

-

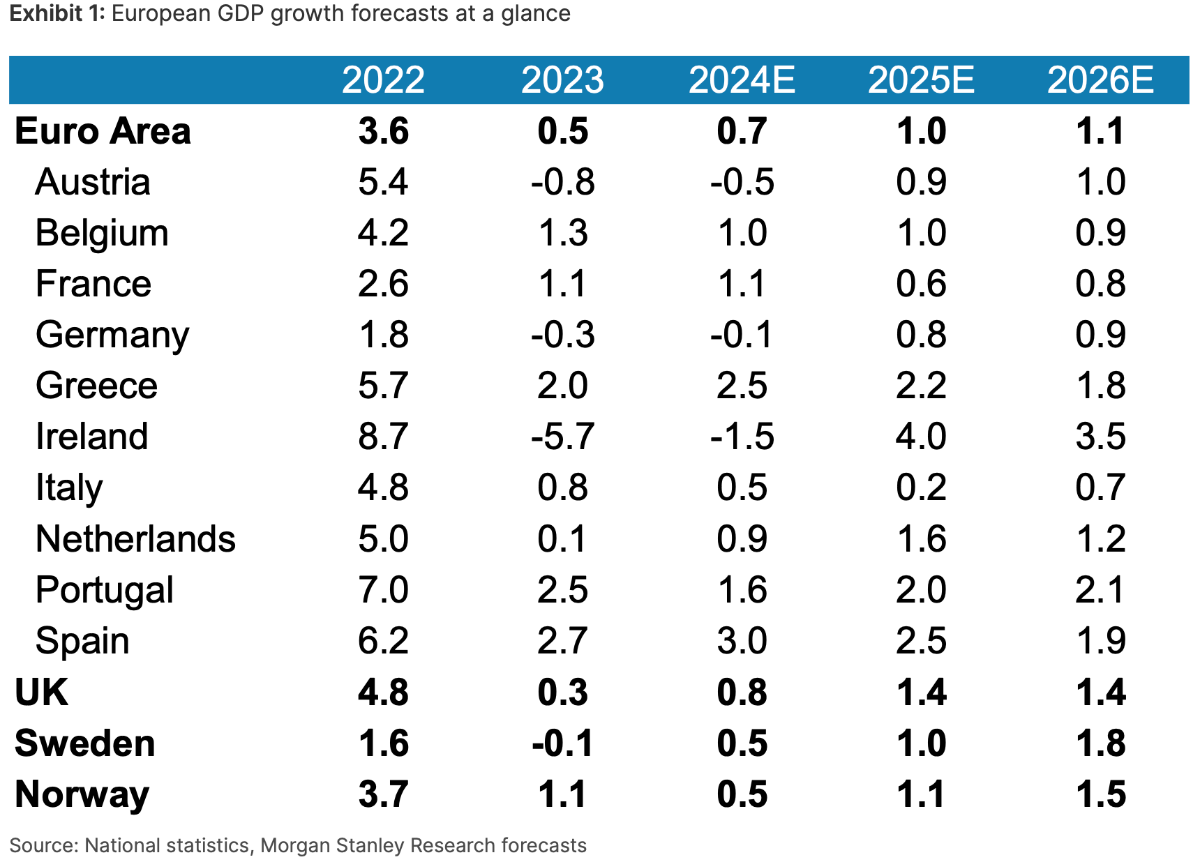

MS released their European outlook for 2025/2026: Overview Summary of the 2025 European Economic Outlook: The Euro area is expected to experience modest growth, stabilizing close to potential levels at 1.0% in 2025 and 1.1% in 2026. Private consumption will strengthen, supported by real income gains and declining household saving rates. Investment is forecasted to rebound as monetary policy eases, but fiscal consolidation and trade tensions will act as drags on growth. Inflation is predicted to fall below the European Central Bank’s (ECB) 2% target, leading to further rate cuts. Risks include potential global downturns, geopolitical tensions, and domestic political uncertainties. Focus on Greece: Growth: • Greece is set to remain a standout performer in the Euro area, with growth projected at 2.2% in 2025 and slightly lower at 2.0% in 2026. • The robust performance will be driven by a combination of: • Strong investment flows from EU recovery funds. • A resilient tourism sector, continuing to bolster economic activity. • Structural reforms and improvements in fiscal management implemented over the past decade. Inflation: • Inflation in Greece will mirror the broader Euro area trend, declining steadily over the forecast period. However, wage growth may remain slightly elevated due to tight labor markets, preventing a more rapid fall in inflation. Trade and Fiscal Policy: • Greece’s economic trajectory is supported by improved trade balances, with strong export performance in services like tourism and shipping. • Fiscal consolidation continues but at a less restrictive pace compared to earlier years, allowing for some domestic stimulus to support growth. Risks: • Greece remains vulnerable to external shocks, such as: • A potential slowdown in global trade or tourism. • Rising geopolitical tensions in the Eastern Mediterranean region. • Domestic challenges include maintaining the momentum of reforms and ensuring the effective deployment of EU recovery funds. Outlook: Greece is expected to remain one of the fastest-growing economies in the Euro area, leveraging its EU recovery fund allocation, improved fiscal health, and strong export sectors. However, external vulnerabilities and the need to sustain structural reforms are critical to maintaining this trajectory. YEARAHEAD_20241117_2200.pdf

-

I know everyone’s mileage differs, but I personally think this is one of the best pieces of advice he has ever given. “I have one further suggestion for all parents, whether they are of modest or staggering wealth. When your children are mature, have them read your will before you sign it. Be sure each child understands both the logic for your decisions and the responsibilities they will encounter upon your death. If any have questions or suggestions, listen carefully and adopt those found sensible. You don't want your children asking "Why?" in respect to testamentary decisions when you are no longer able to respond. Over the years, I have had questions or commentary from all three of my children and have often adopted their suggestions. There is nothing wrong with my having to defend my thoughts. My dad did the same with me. I change my will every couple of years - often only in very minor ways - and keep things simple. Over the years, Charlie and I saw many families driven apart after the posthumous dictates of the will left beneficiaries confused and sometimes angry. Jealousies, along with actual or imagined slights during childhood, became magnified, particularly when sons were favored over daughters, either in monetary ways or by positions of importance. Charlie and I also witnessed a few cases where a wealthy parent's will that was fully discussed before death helped the family become closer. What could be more satisfying?”

-

Eurobank – Plum | Expanding Strategic Partnership “Eurobank expanded its strategic partnership with UK-based Plum Fintech Limited ("Plum") by advancing a second €5 million minority capital investment to Plum, one of Europe's fastest-growing fintechs that has built a "smart money management" app. With its new investment in the company, Eurobank has invested a total of €10 million in Plum and is becoming one of its main financiers. At the same time, Plum has successfully completed its second fundraising round, raising a total of ~€18.4 millionfrom Eurobank and third-party investors.” Some notes attached on Plum Fintech Ltd. Interesting that Plum’s CEO, Victor Trokoudes, is ex Transfer Wise (WISE.L). I hadn’t made the link previously. A recent interview: Plum Fintech.pdf

-

Superb! So played out something like this:

-

Good stuff, lot of value there at the moment if they spin it out

-

They might have lightning in a bottle with Ki . Different insurance type, but Lemonade, an “AI Insuretech” is sitting at a lazy $3.5 bn and hasn’t turned a profit. Hmmm The MS take away from their investor day gives you a flavour of how heady the space is. Meanwhile Ki and for that matter Fairfax just do! LEMONADE_20241120_0501.pdf

-

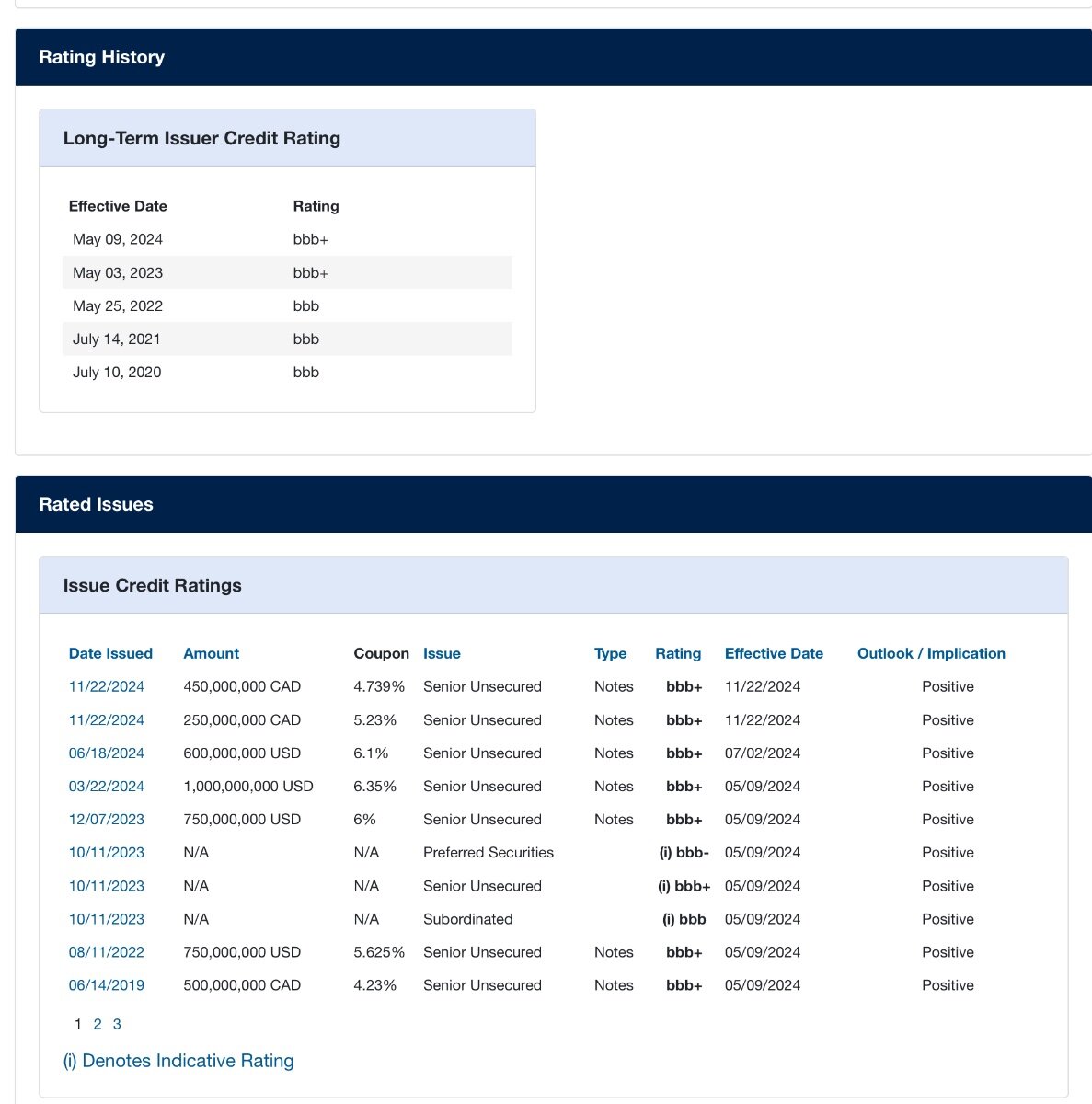

AM BEST has kept their rating at bbb+ and importantly their outlook positive. Will be interesting see if they gain a notch next year (possibly May).

-

Gautam Adani: US summons & a new twist in India intensify billionaire's troubles Article Summary 1. US SEC Summons: Both Gautam Adani and his nephew, Sagar Adani, were summoned by the SEC over bribery and securities fraud charges. They are required to respond within 21 days to avoid default judgments. 2. Indian Legal Challenges: A new application in India’s Supreme Court seeks to incorporate US indictment documents into an ongoing case alleging stock manipulation. The Securities and Exchange Board of India (SEBI) is also probing non-disclosure of these investigations to Indian exchanges. 3. Global Financial Fallout: Several global banks are reconsidering extending credit to the Adani Group. Ratings agencies, including S&P Global and Moody’s, have downgraded the outlook for key Adani Group companies. 4. International Deals Canceled: Kenya terminated two major deals with the Adani Group following the bribery allegations, further impacting the conglomerate’s global operations.

-

(10 year Treasury + ERP) as a discount rate against future cash flows. However, like yourself I am chasing higher returns or greater margin of safety. Don’t want to utter those words but in an age of passive fund flows not sure it is all that helpful anwyway. I like Fairfax because i don’t have to work to hard to arrive at an answer that says low double digit returns are likely even from this point. They have enough opportunities presenting that they aren’t wedded to SPX which is reassuring

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Thanks, good stuff indeed. Dubious politics but I like the sound. Definitely some Rammstein overtones -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Caught Pearl Jam earlier this week. Vedder’s vocals are ageless and Mike McCready still goes hard, a very enjoyable night out. The Pixies as a support act was an absolute bonus.

-

All good points and thinking more about it reinforces the difference between good management and great management. as I said in another thread I think the capital return process benefits from management having skin in the game. Some final thoughts: 1. Overpaying Reduces Returns, But Context Matters: I agree that overpaying for buybacks locks in lower-than-optimal returns. However, for high-ROE companies, intrinsic value grows quickly. Even buybacks slightly above intrinsic value can yield acceptable long-term returns if better reinvestment opportunities don’t exist. For instance, a 6.7% buyback yield might seem low compared to a 40% ROE, but it’s still far better than holding cash or pursuing suboptimal acquisitions. 2. Alternative Capital Allocation Options: Your example highlights that high-ROE companies should prioritize reinvesting internally. However, if those opportunities are exhausted, buybacks might still be the best available option—even slightly above intrinsic value—because they are often more tax-efficient than dividends and can still generate competitive returns. 3. Valuation and Fair Value: I completely agree that high growth doesn’t justify buying at any price. It’s critical to estimate fair value based on realistic assumptions about future growth and returns. For high-ROE companies, this fair value may grow rapidly, meaning today’s “above IV” price might actually be reasonable if intrinsic value is compounding quickly. 4. Buybacks in Low-ROE Companies: You’re absolutely right that low-ROE companies with deeply undervalued shares can achieve outsized returns through buybacks. However, for investors with access to a high-ROE company—even buying slightly above IV—the compounding effect of high reinvestment rates can often dominate returns over time. Bringing the conversation back to Fairfax, while the P/IV is closer to 1, its not difficult to make the case that buybacks are still very accretive. What is interesting to ponder is the enduring effect of these buybacks at such a large discount. There is an obvious ROIC benefit but there are also perceptual benefits too. The creativity of the TRS is worthy of an academic paper or two.