nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

A good take by Henry McVey (attached) in his latest Flash Macro. The regional breakdown is worth a read but nothing startling “Rates: We expect 10-year rates to rally, but probably not trade sustainably below 4% once investors recognize that inflation could move up closer to 4% plus from 3%. Powell had said that tariff-driven inflation is ‘transitory,’ but the level of these tariffs will put pressure on that statement. Said differently:even as growth weakens, the Fed will need to follow a measured approach to easing. From a currency standpoint, we expect the USD will likely stay weaker, Euro and JPY stay stronger, and we are watching countries like China and Vietnam. All else being equal, we see a closer proximity between the U.S. and the rest of the world, whichcould also affect flow of funds. Equities: As of this writing, the S&P 500 is down 12% from its 2/19 peak, and down 4.8% vs. the 4/2 close. For now, we would not rush to buy the dip. While the market was discounting 15% or so tariffs, it was not discounting 25-30%. Keep in mind that during the last bout of tariff-driven macro anxiety in 2018 (which ultimately proved benign), markets fell 20% peak-to-trough. Also, as we show in Exhibit 3, the market has not fully yet discounted recession risk. Similar to our message in 2020, we think allocators of capital should be prepared with shopping lists in anticipation of opportunities, particularly if hard-landing type conditions occur. Given the amount of money on the sidelines, we think credit will likely bend, not break. On the equity side, would expect more volatility, potentially presenting an opportunity to lean in, especially if a recession scenario gets fully priced in.” 2025-april-tariffs-flash-macro.pdf

-

Patrick Boyle’s take https://youtu.be/IpKe_HbVG64?si=Ew53lVVEfrkvjdK1

-

Couldn’t resist, not perfect, but I really liked your analogy

-

Scroll up, but in a nutshell it is a deficit proxy.

-

An antipodean perspective, in recognition of the arts.

-

We were discussing this very point in the link below over dinner. It is a kick in the guts for some on the list that just seems so disproportionate due to the methodology. The potential for unintended consequences just seems disproportionate to any gains. https://www.bloomberg.com/news/articles/2025-04-03/trump-tariffs-are-disaster-for-the-world-s-poorest-countries Summary points: Poorest countries are hit hardest: Cambodia (49%), Laos (48%), Lesotho (50%), and Bangladesh (37%) — despite many having previously enjoyed duty-free access under LDC or AGOA programs. Soft power is sacrificed: The U.S. is pulling aid and slapping tariffs — opening the door for China to fill the void in regions like Southeast Asia and sub-Saharan Africa. Punishment without cause: Many of these countries export labor-intensive goods (e.g., garments) and don’t have the capacity to buy much from the U.S. — yet they are treated like bad actors due to a one-size-fits-all formula.

-

The methodology for “the chart” is now being widely reported https://www.bloomberg.com/news/articles/2025-04-03/trump-s-reciprocal-tariff-formula-is-all-about-trade-deficits The framing in the table below was helpful for me. The discussion above even more so. Slow burn or crisis? Personally I think while futures are voting for crisis, slow burn is the likely outcome. While stupid policy, it is never as bad as all the hand wringing makes out. It’s the end of US exceptionalism but that was a bit overdone as a thesis.

-

Fair point, I don’t follow CVS so those notes were more about my lack of familiarity and a first cut on what the catalysts were over the last 6 months. Agree $70 appears to be consensus. More broadly it was also an observation on how their equity capital allocation is functioning. For me this is kind of the last shoe to drop. Insurance-tick, bonds-tick, equities-tick. Going one step further, equity allocation is also about an opportunity set that is in their wheelhouse. So in an overvalued market, the fact that they are finding ideas that are paying up so quickly is very heartening.

-

@Viking thanks as always. While minor in comparison to Orla, in terms of timing, that CVS purchase was stellar. Turns out CVS was one of the top, if not the top performer in the S&P500 for the quarter. I think it’s also notable what they sold in Q4 as well. Even the “but they bought BlackBerry” crowd would have to confess the Q1 results were a lesson in “seeking alpha”. Some notes on CVS: • Leadership Transformation: New CEO David Joyner (appointed October 2024) implemented effective turnaround strategies focusing on operational improvements • Exceptional Earnings Performance: Q4 2024 results substantially exceeded analyst expectations with EPS beating forecasts by 34% • Medicare Advantage Optimization: Strategic benefit adjustments and improved star ratings enhanced profitability in the health insurance segment • Digital Innovation: Launch of redesigned AI-powered app serving 60 million digital customers improved customer experience • Cost Rationalization: Closure of underperforming retail locations and implementation of efficiency measures strengthened margins • Analyst Confidence: Multiple Wall Street upgrades with 18 of 21 analysts giving buy ratings and significant price target increases • Reduced Short Interest: Declining short positions signaled growing investor confidence in the company’s recovery • Favorable Sector Dynamics: Healthcare emerged as 2025’s strongest performing sector, providing additional tailwinds for CVS

-

Thanks for this, EXCO continues to be a bit of black box to me. Looks like it is heading in the right direction

-

Thanks, fingers crossed they did. Given the volatility and uncertainty it’s a good time for patient long term capital to be consolidating these types of assets. I liked his analogy too: “WEF is acquiring oil sands properties at a time when foreign energy companies continue to exit the region and smaller private players are selling rather than trying to raise the money needed to build a producing property. The dominant oil sands companies, including Canadian Natural Resources Ltd. , Cenovus and Suncor, are also bulking up. “If we were real estate investors, we would be the folks who buy one house in a great neighbourhood full of elderly homeowners, then keep buying great houses as they come to market,” said Mr. Waterous, managing partner and chief executive officer at WEF, in an interview.” Energy investor Waterous closes $1.4-billion oil and gas fund - The Globe and Ma.pdf

-

Indeed, they had this to say in their recent 20F “Following its investigation of the maritime, logistics and shipbuilding industry in China, the U.S. Trade Representative has proposed charging service fees under Section 301 of the U.S. Trade Act of 1974 for docking of vessels made in China and vessels owned by companies that operate vessels made in China or are manufacturing newbuild vessels in China, if such fees are implemented, the resulting service fee regime could have an effect on our financial condition and result of operations. On March 12, 2024, certain parties filed a petition under Section 301 of the U.S. Trade Act of 1974 (“Section 301”) regarding the acts, policies, and practices of China to dominate the maritime, logistics, and shipbuilding sector. On April 17, 2024, after the U.S. Trade Representative (“USTR”) initiated an investigation of China’s targeting the maritime, logistics, and shipbuilding sectors for dominance. Following the investigation, on January 23, 2025, the USTR reported its determination that China’s targeting of the maritime, logistics, and shipbuilding sectors for dominance is unreasonable and burdens and restricts U.S. commerce and thus is actionable. On February 21, 2025, the USTR issued a notice of proposed action under Section 301, which provides, among other things, for significant service fees for Chinese-built vessels and for companies that operate Chinese-built vessels or have contracted to build vessels in China. The proposed action is subject to a period of public comment and public hearings before it is implemented. It is unclear from the USTR’s February 21, 2025 notice how the proposed service fees will be levied and which party involved in the operation of a Chinese-built vessel will be required to pay the fees. We are closely monitoring the proposed action and assessing its potential impact on the Company in light of the fact that 88 of our time-chartered vessels were built in China and that we have orders for 36 vessels from Chinese manufacturers.” Some further notes: ”Seaspan may face significant challenges with the proposed Trump administration taxes on Chinese-built ships. The plan to impose fees of up to $1.5 million per U.S. port call for Chinese-built vessels could make U.S. port calls too expensive for some operators, potentially leading to rerouting of cargo through Canada or Mexico. Seaspan, which has ordered ships from Chinese shipyards like Hudong-Zhonghua, is closely monitoring these developments. The increased costs could impact Seaspan’s operational efficiency and profitability, as they might need to adjust their shipping routes or absorb the additional fees.” “The exact percentage of the global fleet that is Chinese-made is not specified in a single figure across all types of ships. However, Chinese shipyards have a significant presence in various sectors: -Cargo Ships: Chinese yards account for 47% of cargo ships above 10,000 DWT. -Tankers: They make up 24% of the global tanker fleet. -Container Ships: Chinese-built vessels comprise a substantial portion, with companies like MSC having 24% of their fleet as Chinese-made, and Maersk having 20%. -Bulk Carriers: Chinese vessels account for 75% of the bulk carrier fleet” https://www.reuters.com/markets/trumps-fees-chinese-ships-will-hurt-us-companies-maritime-executives-tell-2025-03-24/?utm_source=perplexity

-

Great post! It got me thinking more about Prem's aspirations for the 100-year company. Your post was timely, as I had meant to collate some upper-level thoughts for a family member to this end anyway. Notes attached Fairfax Financial- Building a 100-Year Company?.pdf

-

Yep, that wasn’t on my bingo card for 2025. These guys have more angles than a protractor.

-

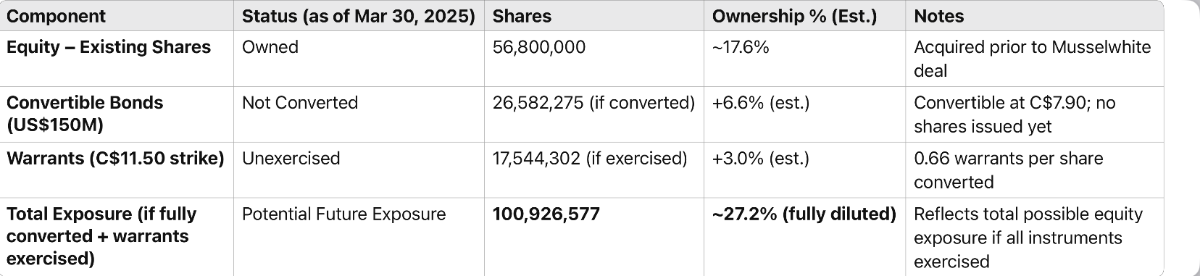

Something like this if fully converted?

-

Maybe a little OT but I found this article mildly interesting in the context of distressed credit. Overall spreads are still pretty skinny but the opportunities are growing in niche areas. From Bloomberg(and attached): Khosla Sees One of Best Opportunities in a Decade “Victor Khosla, the founder of Strategic Value Partners LLC, is looking to hire amid one of the most promising environments for opportunistic credit investors in the last 10 years. “For investors like SVP, if you take out the first six months of Covid, there’s never been such a rich vein of opportunities over the last decade in an economy that’s not in a recession,” Khosla said in an interview.” “Khosla’s Angle: He’s not talking about the broad market. He’s talking about: • Distressed opportunities (e.g. German corporate bonds, office real estate, chemicals) • Off-market or highly negotiated deals (e.g. buying a London office at 60% off) • Private credit and bespoke financing (especially in illiquid European markets)” While pockets of distressed debt signal underlying vulnerabilities, credit spreads typically don’t widen systemically until markets lose confidence that the stress can be contained. For Fairfax, it’s still early days—but it’s encouraging to see the opportunity set beginning to expand Khosla Sees One of Best Opportunities in a Decade- Credit Weekly - Bloomberg.pdf

-

What was the venture on your own?

-

Thanks, the first thing that comes to my mind is “fortune favours the prepared mind’. Secondly and most importantly is not getting shaken out is the real test. Those positions have lead to some serious “alpha”. I dare say that even if you stumbled upon some of them, seeing what worked, framed other investments. It goes to the heart of Mungers views on patience and quality.

-

Thanks, that is a whole lot of history and whole lot of business cycles. It gels with something I have been thinking about lot about lately…patience is very much an edge. Many pay lip service but few can do it. If I could ask a follow up, is the fat tail of compounders in your portfolio a function of attrition from a more diversified portfolio perhaps influenced by tax or a deliberate policy of concentration from the outset ? I only ask because I have ended up over 20 years with a fairly concentrated portfolio partly due to tax but also my own biases. When I started out I could never fathom owning say 80% in Berkshire but I kind of get it now if you have confidence of an OK return and there is a large capital gain tax liability.

-

Cool, any high conviction positions?

-

No view on the next acquisition but I would be delighted with a script based offer on something sensible at these levels. It may stop me looking at historical P/B charts.

-

Without knowing the coupon, it is hard to say. Typically, the coupon might be 2-4% less than straight debt. As you say, this might bring the coupon in line with the div. From Metlen's perspective, the interest rather than dividend is tax deductible, so there is that. I don't know their credit situation and whether they are close to covenants (job for another day). If Fairfax is earning 3-4% interest income and has the option, it would be a good deal. Whether it is a sweetheart deal, time will tell. If they can grow as they have in recent times, even a zero coupon might work

-

Not that I could find; I was interested in this as well. Sent a request to IR, but not holding my breath. The original press release is pretty light on https://www.metlengroup.com/news/ase-announcements/corporate-actions/fairfax-increases-again-its-stake-in-metlen/

-

https://www.ekathimerini.com/economy/1265036/fairfax-invests-further-into-metlen-group/ Fairfax Financial, one of the holding companies with the greatest exposure in Greece in recent years, is increasing its stake in leading Greek group Metlen Energy & Metals, investing a further 110 million euros, the Athens-listed company announced on Monday. In a statement, Metlen said it has reached an agreement with Canada-based Fairfax to enter a €110 million exchangeable bond, through which Fairfax will have an option to acquire 2.75 million Metlen treasury shares within two years at a price of €40 per share, representing 1.92% of the Greek group’s share capital. It added that following that acquisition, Fairfax’s total stake in Metlen will increase to 8.35%. Some additional notes: Strategic Implications This transaction aligns with Metlen’s broader strategy to fund its “Big 3” transformation program, which includes expanding into critical raw materials (e.g., bauxite, gallium) and renewable energy infrastructure. The capital infusion arrives as Metlen prepares for its London Stock Exchange listing and potential inclusion in the FTSE 25 Index, enhancing its global visibility and access to institutional investors. Historical Investment Timeline Fairfax’s relationship with Metlen (formerly Mytilineos) dates to 2012, when it first acquired shares. Subsequent milestones include: • 2022: A €50 million equity purchase and €50 million exchangeable bond at €20 per share, raising Fairfax’s stake to 4.68%. • February 2025: Exercise of prior exchangeable bonds increased Fairfax’s stake to 6.43%. • March 2025: The latest €110 million bond extends this partnership, reflecting 13 years of collaborative growth. Capital Markets Day and LSE Listing Metlen has scheduled a Capital Markets Day on April 28, 2025, at the London Stock Exchange, where it will detail its €295.5 million investment in raw material production and renewable energy projects. The Fairfax deal strengthens Metlen’s balance sheet ahead of this event, providing liquidity to advance its 530 MW Australian solar portfolio and 71.5 MW Italian solar projects. Financial Performance and Shareholder Returns • 2024 Results: Metlen reported €1,080 million EBITDA (+7% YoY) and proposed a €1.50 per share dividend. • Debt Management: Adjusted net debt stood at €1,776 million (Net Debt/EBITDA: 1.7x), manageable despite aggressive CAPEX. Valuation/Prospects • Valuation Upside: The €40 conversion price implies a 12.5x P/E multiple on 2024 earnings, below peers in the European energy sector. • FTSE 25 Prospects: Metlen’s London listing could attract $500 million–$1 billion in passive fund inflows, given FTSE 25 inclusion criteria. Edit: Attached some MS coverage of the deal METLEN_20250324_1310.pdf

-

MS have released their India Economics – Macro Indicators (24-mar-25) worth a flip thru prior to the FIH AGM Summary: 1. Growth Outlook – Gradual Recovery • High-frequency indicators (GST collections, power demand, credit growth) show marginal improvement. • Air passenger traffic and consumer sentiment are holding up, though auto sales declined. • GDP for March quarter is tracking at ~6.7% YoY, with FY2025 expected at 6.3%, and 6.5% for FY2026–27. 2. Inflation – Softer CPI, Stable Core • Headline CPI fell to 3.6% YoY in Feb 2025 from 4.3% in Jan. • Core CPI (ex-food/fuel) rose to 4.0% YoY. • Inflation risks include weather events (monsoon) and commodity prices. 3. External Sector – Strengthening Services Offset Weak Goods Trade • Services exports surged: +23.6% YoY in Feb. • Goods exports declined: –10.9% YoY. • Goods trade deficit narrowed to $14.1bn, lowest since Sep 2021. • Net services balance hit an all-time high of 5.7% of GDP (annualized). 4. Policy and Liquidity – Easing Stance • RBI cut rates by 25 bps in Feb; Morgan Stanley expects two more 25 bps cuts (April and June), bringing terminal rate to 5.75%. • Liquidity is still in deficit but is expected to improve after FY-end. 5. Fiscal Performance – In Line with Targets • FYTD fiscal deficit is ~4.4% of GDP, aligning with revised FY25 target of 4.8%. • Spending remains skewed towards capital expenditure. 6. Employment – Mixed Signs • Naukri Job Index improving modestly. • EPFO payroll additions stable. • Rural wages steady at ~6% YoY. • NREGA demand for jobs has softened from FY2024 levels. 7. Investment Indicators – Uneven • Private projects have picked up slightly, public ones are stable. • Capacity utilization is above long-term average (71.9%). • Real estate: New sales and launches are rising. 8. FX and Trade • India’s FX reserves are healthy at ~$654bn, with ~11 months of import cover. • CAD expected to remain around 1% of GDP. • REER (Real Effective Exchange Rate) is below long-term mean, offering export competitiveness. Looks like the economy has bottomed out after the mid 24 trough. Air Travel and Air Cargo still looking strong INDIA_20250324_0020.pdf