Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Parsad , great point. Volatility freaks out lots of Fairfax shareholders - but extreme volatility over the past 5 years is when Fairfax made their best investments. It’s very counterintuitive. In 2024 with volatility low in financial markets, Fairfax has resorted to hitting solid singles. Still gets the baserunners around the bases and across home plate. Still scores lots of runs.

-

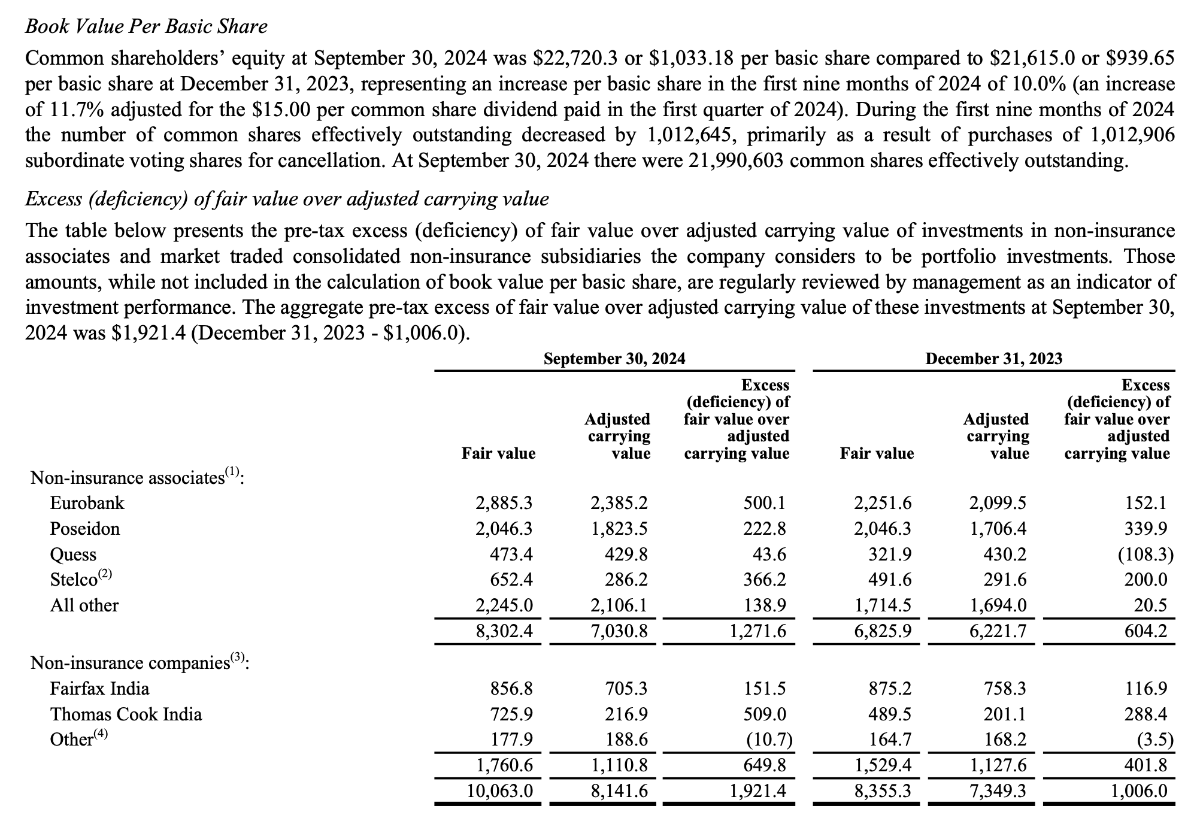

So 9 months into 2024, Fairfax has: 1.) Increased book value per share from $940 to $1,033, an increase of $93. 2.) Paid a dividend of $15/share. 3.) For non-insurance associate and consolidated holdings, increased excess of FV over CV from $1 billion to $1.9 billion, an increase of $900 million (pre-tax). This is significant value that has been created that is not captured in book value. Also, the 'fair value for some of these holdings looks stupidly low (meaning book value is even more understated). Their stake in Fairfax India has a fair value of $857 million? It should be much more than this (driven by BIAL). The fair value for Poseidon, at $2 billion, has not changed in 2024. Sokol at Fairfax's AGM in April said the cost to build new containerships had increased 30%. Atlas is just taking delivery of the last of its newbuilds as part of its massive expansion strategy executed over the past 3 years - the value of which has just increased by around 30%. Yet the 'fair value' on Fairfax's balance sheet has not changed? There are more good examples. 4.) Effective shares outstanding have been reduced by 1 million = 4.3%. Much lower share count boosts investment per share, float per share and earnings per share. Bottom line 2024 is shaping up to be another very good year for Fairfax and its shareholders. Fairfax has not done anything flashy. Just lots of solid execution. Boring. Kind of like watching paint dry. Expect more of the same in the coming years. (PS: That is what a compounding machine looks like.) ----------

-

Another strategic shift Fairfax appears to be making is to build out the size of the non-insurance operating companies bucket. In 2022 they took out Recipe. They just added Sleep Country. And in Q4, with the takeout of Peak Achievement (Bauer) they will add one more. This could take pre-tax earnings for non-insurance operating companies from $150 million to perhaps $300 or $350 million per year - which now makes it a meaningful number. This income stream is different from the other 4 incomes streams Fairfax has: - It is not correlated with the insurance business/cycle - so provides important diversification to earnings. This benefits the income statement. - It also provides an important source of liquidity for the company - they are owned/controlled assets that could be sold if needed. This benefits the balance sheet. It will be interesting to see if Fairfax continues to grow the non-insurance consolidated companies bucket in the coming years.

-

Looks like another solid quarter to me. A question for board members: are the gains from the Stelco sale and the take out of Peak Achievement (Bauer) not yet realized? I.E. they will be realized when Fairfax reports Q4 earnings? “On July 15, 2024 Cleveland-Cliffs Inc. ("Cliffs") entered into a definitive agreement with Stelco to acquire all outstanding common shares of Stelco for consideration of Cdn$70.00 per share (consisting of Cdn$60.00 cash and Cdn$10.00 in Cliffs common stock), which received shareholder approval on September 16, 2024. Subsequent to September 30, 2024, Stelco received final regulatory approvals and expects the transaction to close on November 1, 2024. Accordingly, on July 15, 2024 the company measured its investment in Stelco as held for sale and ceased applying the equity method of accounting. The company's current estimated pre-tax gain on sale of its holdings of approximately 13 million Stelco common shares is approximately Cdn$495 ($366), calculated as the excess of consideration of approximately Cdn$881 ($652 or $50 per common share) over the carrying value of the investment in associate at September 30, 2024 of approximately Cdn$387 ($286.2).” “September 30, 2024 it was announced the company will, through its insurance and reinsurance subsidiaries, increase its investment in Peak Achievement Athletics Inc. ("Peak Achievement") to a controlling interest by acquiring the 42.6% equity interest owned by Sagard Holdings Inc. The company currently applies the equity method of accounting to its investment in Peak Achievement and expects to consolidate Peak Achievement in its Non-insurance companies reporting segment upon closing, which is anticipated to occur in the fourth quarter of 2024, subject to customary closing conditions. Peak Achievement is engaged in the design, manufacture and distribution of performance sports equipment and related apparel and accessories for ice hockey, roller hockey, and lacrosse, under brands such as Bauer Hockey, Cascade Lacrosse and Maverik Lacrosse.”

-

@whatstheofficerproblem, thanks for the kind words. Happy to hear you found the PDF useful

-

@SafetyinNumbers, thanks for posting. Earnings expectations look like a pretty low bar to me (putting it mildly). It basically says one of two things (or some combination of the two): 1.) Fairfax is massively over-earning today. 2.) When it comes to the near record earnings that Fairfax is delivering, when it comes to capital allocation, the management team will destroy capital moving forward. Really? I love that set up. Looks like we are at the ‘climbing the wall of worry phase’… Definitely no where near the ‘euphoric, blow off top’ stage.

-

@ourkid8, I will admit i do not fully understand the situation in the middle east all that well. i try and understand the big picture. This helps me process the specific events that are happening. Can you explain to me where Hamas and Hezbollah fit in to what is happening? I think it is true that Hamas has as part of its charter the destruction of Israel (and killing Israeli’s will get you to into heaven etc). I think Hezbollah is largely the same. Hamas is the government body of Gaza and Hezbollah is firmly in control of the government in Lebanon (at least it was). To come into power, both Hamas and Hezbollah killed off all those who stood in their way. My understanding is neither Hamas nor Hezbollah accept Israel's right to exist. As a result, they have no desire to peacefully co-exist with Israel. When i hear people talk about Palestinians and they do not state their position on Hamas and Hezbollah i am not able to process or understand what they are saying. It is not possible to separate the people from government in power.

-

Super interesting to read the comments on Fairfax on the board today. They get to lots of important questions for an investor: - Valuation? - Prospects? - Concentration / portfolio weightings? Of course, there are two more important inputs: - How is a person is wired? - What is there life situation? And i would add one more input: - What are the alternatives? What each of us does will depend on how we answer each of the questions above. i think the key to valuing Fairfax is getting a good handle on: 1.) What is underlying book value today? - Reported book value + excess of FV to CV + hidden value - As more assets get taken private (a clear trend in recent years) the ‘hidden value’ bucket will continue to grow and more quickly. Fairfax will find a way to surface this value over time. - ‘Hidden value’ examples: BIAL is probable the best. Grivalia Hospitality. Peak Achievements (this will likely be surfaced with the take private deal). There are more (i.e. what is Recipe worth today?). 2.) What is the ‘normalized’ earnings power of the company today? - What number should get plugged in for realized/unrealized investment gains? - What is the ‘normalized’ ROE today? 3.) How much will earnings grow over the next 3 to 5 years (from normalized level)? - This will be driven primarily by the capital allocation decisions made by the management team today and in the coming years. Their track record the past 6 years has been stellar (Does this matter?). - It looks to me like Mr Market expects little to no earnings growth from the company over the next 3 to 5 years. - Of course, earnings per share is what matters. (Mr Market appears focussed on earnings.) 4.) How should the company be valued today? - What price to (true) book value multiple is appropriate? Two other inputs for me are the following: 1.) Share buybacks: Is the company buying back shares? If so, how much? - Fairfax has been very aggressive with buybacks in 2024. Does this continue? - Fairfax is on pace to reduce effective shares outstanding by around 5% in 2024. All things being equal, this by itself will drive per share growth of 5% in 2025. What matters are investments per share, float per share and earnings per share. Materially lowering the share count matters. A lot. 2.) FFH - TRS position: Is the company continuing to hold this position? The truth is Fairfax has seen such a significant transformation in its earnings power over the past 3 years we are still learning what the answers are to the questions i posed above.

-

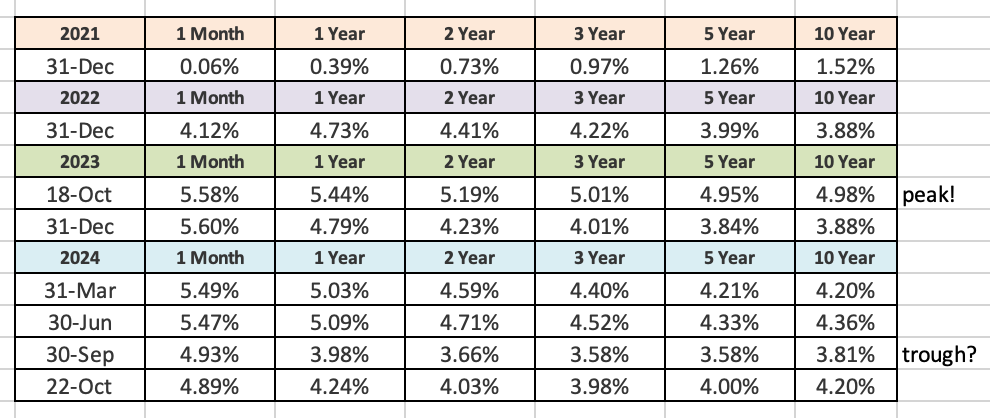

Below are a few of the things i will be watching for when Fairfax reports Q3 earnings. The order of items reflects my level of interest - not how important they are to Fairfax and its performance over the long term. Anything missing from my list? 1.) Impact of substantial decline in interest rates in Q3 When Fairfax reports Q3 results the 800lb gorilla will likely be the impact of the big decline in interest rates that we saw in Q3. Rates were down significantly across the curve. This will have two big impacts of Fairfax: Change in value of the fixed income portfolio - resulting in a big unrealized gain. Impacts of IFRS accounting - resulting in a big loss. My guess is the two impacts will net into a nice unrealized gain for Fairfax. How big? No idea. What do other board members think? Of interest, so far in Q4 we have seen bond yields spike higher. Should this hold, this will reverse some of the net effect that happens in Q3. Fairfax also tends to be pretty active in how they manage their fixed income portfolio (from an historical perspective). It will be interesting to see if they are able to find a way to take advantage of the extreme volatility we have seen in the bond market over the past 3 months. 2.) Capital allocation Update on effective shares outstanding Under 22 million? any commentary? Still view shares as being significantly undervalued? (Are they still holding FFH-TRS position?) Asset sale / purchase: any commentary? Purchase of Sleep Country. What will it deliver pre-tax to non-insurance consolidated bucket? Sale of Stelco. Pre-tax investment gain = $397 million, expect Q4 close? 3.) Insurance What is growth in net premiums written? What is CR? What is level of catastrophe losses? In line with expectations? What is level of reserve releases? Commentary on hard market? 4.) Interest and dividend income Is it still growing? Flat? Declining? Interest and dividend income was $590 million in Q1 and $614 million in Q2. Is Fairfax’s investment in Kennedy Wilson’s debt platform continuing to increase in size? 5.) What is share of profit of associates? Eurobank? Chug, chug, chug? Poseidon? Are we seeing green shoots? 6.) Equities What are investment gains from equities? The equities I track suggests mark to market gains from equities will be solid in the quarter. For Associate holdings, what is the excess of market value to carrying value? This is value that is not being captured by book value. 7.) What is book value per share? At June 30, 2024, BVPS = $979.65 8.) Miscellaneous topics Some notes from 1H 2024 results: Tax rate looks elevated. Q3? Amount of earnings accruing to non-controlling interests looks elevated. Q3 Currency has been a headwind to BV in 1H. Tailwind in Q3? Life-ins/runoff costs look elevated. Does trend continue in Q3? Due to new issuance, the interest cost has popped higher. What is the new run rate?

-

@TB As a general rule, i try and keep politics out of my investing framework, especially for those investments i view as medium to long term holdings. I am following what is going on. As with all my investments, I will follow the facts and fundamentals and make adjustments as needed. It is the same approach I am taking with the US election. PS: I do not own any Fairfax India today (it is on my watchlist).

-

Do you plan to continue holding Berkshire once Buffett is gone?

Viking replied to Milu's topic in Berkshire Hathaway

This is a very interesting topic for me. Specifically the ‘sitting on a big capital gains’ angle. Given Fairfax’s run the past 4 years, my guess is many investors are sitting on significant capital gains in taxable accounts. Most of our assets were in tax deferred accounts. That changed when we sold our house in 2021 - now a growing portion are in taxable accounts. My strategy with Fairfax over the past 4 years has been to be pretty aggressive with realizing part of the growing capital gain each year. This works for me because: 1.) Both me and my spouse are ‘retired.’ So we decide which bucket to pull our income from each year (non-registered, LIF, RRSP, TFSA). Tax considerations play an important role in determining how much we pull from each bucket. - In Canada today, capital gains are taxed at a pretty low level. 50% of capital gains are free. We are only taxed on 50% of the gain. I am not sure this will stay this way. 2.) I may want to use the funds sitting in my taxable accounts in the coming years to make a real estate purchase. Nothing imminent. As a result, i do not like the idea of sitting on a big (and growing) tax liability indefinitely. This leads me to prioritize selling some Fairfax in our taxable accounts each year and paying tax. 3.) Selling Fairfax in my taxable account does not impact the number of shares of Fairfax i hold. This is because i have the ability to purchase an equal number of shares in my tax deferred accounts (TFSA, LIF and/or LIF). - When selling Fairfax in my taxable accounts I have been able to do it when Fairfax has hit new all time highs. Each time I have actually been able to re-buy the Fairfax shares in the same account, usually within a month or two later, at a slightly lower price. I have done this because i do want my best ideas in my taxable account (#2 priority after TFSA). 4.) I greatly value simplicity. All things being equal, i don’t want to be sitting on a big tax liability with a big part of my non-registered accounts. I am ok paying a little tax now to lessen an issue - and give me more flexibility in the future. Anyways, everyone’s situation is different. Now that my non-registered accounts are growing in size, i am having to learn some new things - like how to think about and manage a big (and growing) tax liability. Bottom line, this is a great problem to have. But it certainly does have a lot of layers to it. The key has been to have a multi-year plan - and then to opportunistically execute the plan. And each year i modify the plan as needed (based on our evolving situation, new information and as my knowledge improves). -

Fairfax is earning about $600 million in interest income/dividends each quarter. The Stelco sale is expected to close in Q4. Their insurance subs have started dividending significant amounts to Fairfax. My guess is catastrophes like Milton will be a short term headwind to earnings (Q4) and a medium term tailwind to earnings (extend the hard market in reinsurance another year or two). Fairfax has been cutting back on its catastrophe exposure in recent years. One of the worst thing that could happen to Fairfax is a soft market. No hurricane losses over a couple of years would likely bring one on.

-

I agree. I also think the transition at Markel from being Markel (family) run to the current management structure also explains a big part of the underperformance in recent years (when compared to Fairfax). Prem is still firmly in charge at Fairfax and has been instrumental in the renaissance the company has experienced over the past 6 years. I am less impressed by Gaynor the longer he is at the helm of Markel (and I find Gaynor's constant and over-the-top marketing to be more than a little nauseating - actually a little insulting). Succession planning is so important (and unknowable). PS: At Fairfax's AGM this year, I also found Prem's comments about long term shareholders to be a little off-putting. (My view is a rational investor SHOULD have sold Fairfax when management lost their way with investments. To pretend otherwise is an insult to their intelligence.)

-

@nwoodman I was lucky to get a copy of the book at this years AGM (at the silent auction/dinner the night before the AGM). The book does an outstanding job of walking the reader through Fairfax's first 25 years of existence. I understand Fairfax pretty well. This book added much more depth to my knowledge. Lots of great information on the key people at Fairfax (some of whom are still there), including where they got their start/training. It really is a crazy (amazing) story. It is unfortunate there is not a digital copy available for people to read/easily access. I really liked learning about the importance of Markel to Fairfax's start and first few years. It is interesting to compare the two companies today. Fairfax not only caught Markel, but has blown right by them in terms of all key metrics. Most importantly, Fairfax looks much better positioned than Markel today (people, structure, execution, results, prospects).

-

+1

-

It is not surprising to see global wealth continue to motor higher. Looking at Canada, my guess is the increase in 'wealth' over the past 20 years has likely been epic. 1.) We have had a housing bubble. Most households in Canada own (not rent) so the housing boom has created an enormous amount of wealth for an enormous number of people. 2.) At the same time, stock markets have also performed exceptionally well. Lots of Canadians have also seen a significant increase in the value of their financial assets. 3.) Canada also has a national pension plan (CPP) that has significantly increased in value. Another wealth driver for Canadians. Bottom line, a very large number of Canadians have seen their wealth increase materially over the past 20 years. This will have important positive impacts on the economy moving forward - that I don't think are fully understood today. And the wealth transfer that will be happening over the next 10 to 20 years will be epic. This will also have important impacts on the economy.

-

@mananainvesting, I can't actually answer that question. My answer would be gibberish. Because it would lack important context about my personal situation (my specific reasons for selling). With Fairfax I have a large core position. I then flex this core position up and down. Sometimes by quite a bit. What I do with the flex part of my portfolio primarily depends on what Mr. Market does. But even the sizing of my core position can fluctuate up and down. Again, depending on the facts and fundamentals at Fairfax. And what is going on in the general market (what do other opportunities look like). And what is going on in my head. And taxes are becoming an important factor for part of my Fairfax position (a very good problem). A couple of new wrinkles for me this year are retirement and estate planning considerations. I will be 60 next year so these two topics have been becoming more important to me (I am at the learnings stage). On the retirement angle, I am beginning to think I probably should have 2 or 3 years of living expenses socked away in a cash type account (thanks to comments from others of this board recently). This is not a big deal, but it likely means I will reduce the weightings of all of my individual holdings. On the estate planning angle, if I am ever hit by a bus my family needs to know what to do with all of the different investment portfolios (we are all hit by the Father Time bus eventually). A year ago I started to shift part of our portfolios into broad based ETF/index funds (mostly XIC.TO and VOO). A year later, I love how I feel about it - so much so that I have shifted more into ETF/index funds. This is providing my family with a clear roadmap of what to do the day I am no longer around (or able) to manage our investments. In recent years, taxes have also become an important factor for me. I may sell a chunk of Fairfax in a non-registered account to lock in a large gain for tax purposes. I also have some philosophical things rattling around in my head. I like reading Morgan Housel's stuff. His view is at my age I should be focussed on 'preservation of capital' not maximizing 'return on capital.' Buffett (or Munger) have said a similar thing: 'why would you risk what you need for what you don't need'. Does it make sense for me to have a concentrated position in a stock given my current situation (I have enough)? I also change my mind a lot. At the margin. I like to try things. And then wait and see how I feel afterwards. Was it a good decision? or not? My price target might change next week (it might go up and it might go down). Anyways, this post is probably reading like the writing of a complete nut job. All I can say is it has worked for me for 25 years

-

Over the past 4 years, we have been learning a few things that we did not know about Fairfax: 1.) Their business model is unique in P/C insurance and very powerful when management is executing well. 2.) Their management team is very good. And they have been executing exceptionally well for the past 6 or 7 years. 3.) Their P/C insurance operations are very good. Much better than most people think. 4.) After 6 years of hard work, they have largely fixed the problems that existed in their equity portfolio. A headwind has flipped and become a tailwind. 5.) Record earnings (continuously, over many years) + excellent capital allocation (like Fairfax has been doing) + compounding = significant increase in intrinsic value. The question that i have not seen answered anywhere (in any great detail) is just what is this company actually worth today? The problem is most answers to this question lean heavily on past results. To get a proper answer, the answer needs to be focussed primarily on the future. IMHO, record earnings, excellent capital allocation and compounding provide the best clues. (If intrinsic value compounds at mid-teens average per year over the next couple years, how likely is it that EPS will decline over that same time horizon?) Most analysts are raising their P/BV multiple in lock step with the stock price moving higher. So they don’t look stupid. Well, everyone except Morningstar, that is (and there are no words to describe their Fairfax ‘analysis’ - it is borderline criminal it is so bad).

-

A question for board members. When Fairfax takes Peak Achievement private (expected in Q4) will they mark up their 43% stake to reflect the purchase price? If so, this should drive a meaningful realized investment gain in Q4. Fairfax's carrying value for its 43% position in Peak Achievement is $129 million. At June 30, it had a fair value of $226 million. The sale price for 100% of Peak has not been disclosed. Some reports suggested Peak was being shopped for $800 million. A post on Twitter suggests the final sale price (likely including debt) values the company at $1 billion. ----------- Fairfax is 'sitting' on about $2 billion in unrealized investment gains today. This figure has been growing rapidly over the past 4 years. As Fairfax harvests this value in the coming years it will be incremental to analysts EPS earnings forecasts. How Fairfax harvest this value will vary. Sometimes it will be an outright sale like Stelco. Other times it will be change in their ownership stake, like Peak Achievement (if I am understanding things correctly).

-

@dartmonkey, when putting together my summary of Fairfax's equity holdings: 1.) I start with the summary Fairfax provides in their annual report each year. This provides a great deal of information (all the different buckets and sub-buckets). 2.) Then layer in holdings that we know about but that Fairfax did not have in the annual report (these amounts will be subtracted from the sub totals so they do not get counted twice). 3.) Then incorporate new news each quarter: 13F, Fairfax announcements etc. When each annual report comes out I start at the beginning again. ---------- As you rightfully note, there are holdings worth billions in value that we know little about (what the holdings are and how they are doing over the year). --------- As a result, my estimate (tracking spreadsheet) is usually light when it comes to estimating actual reported gains and losses from investments.

-

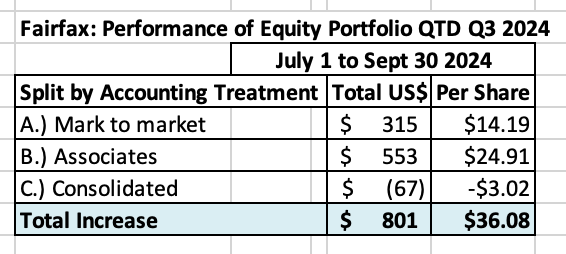

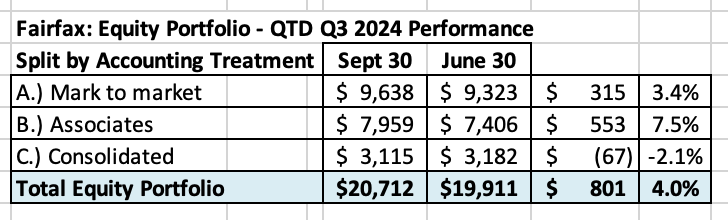

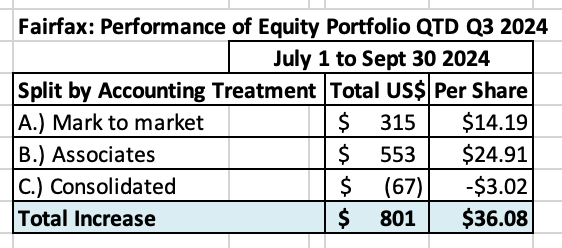

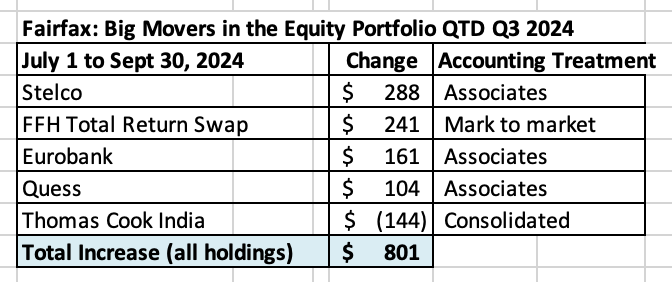

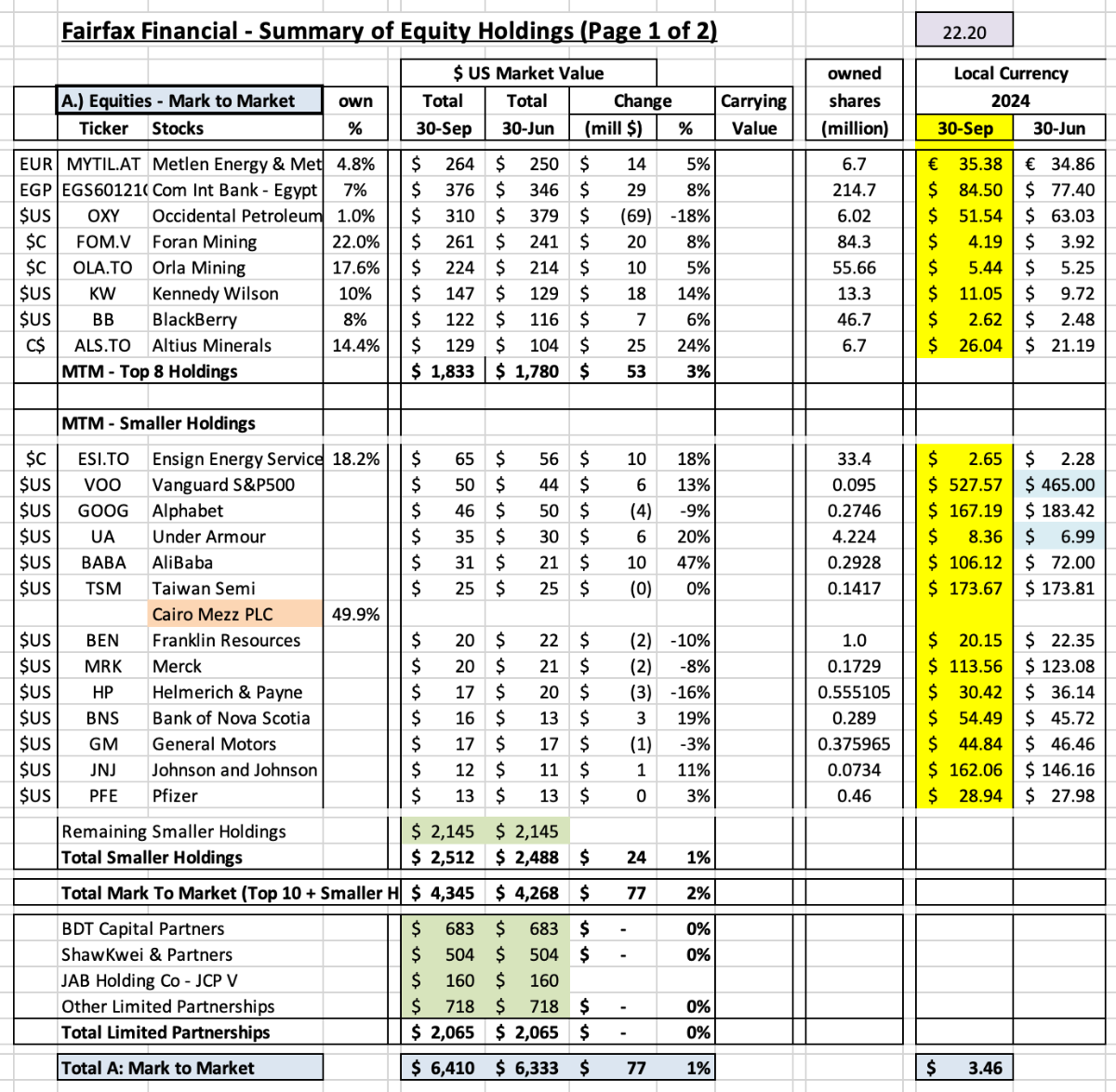

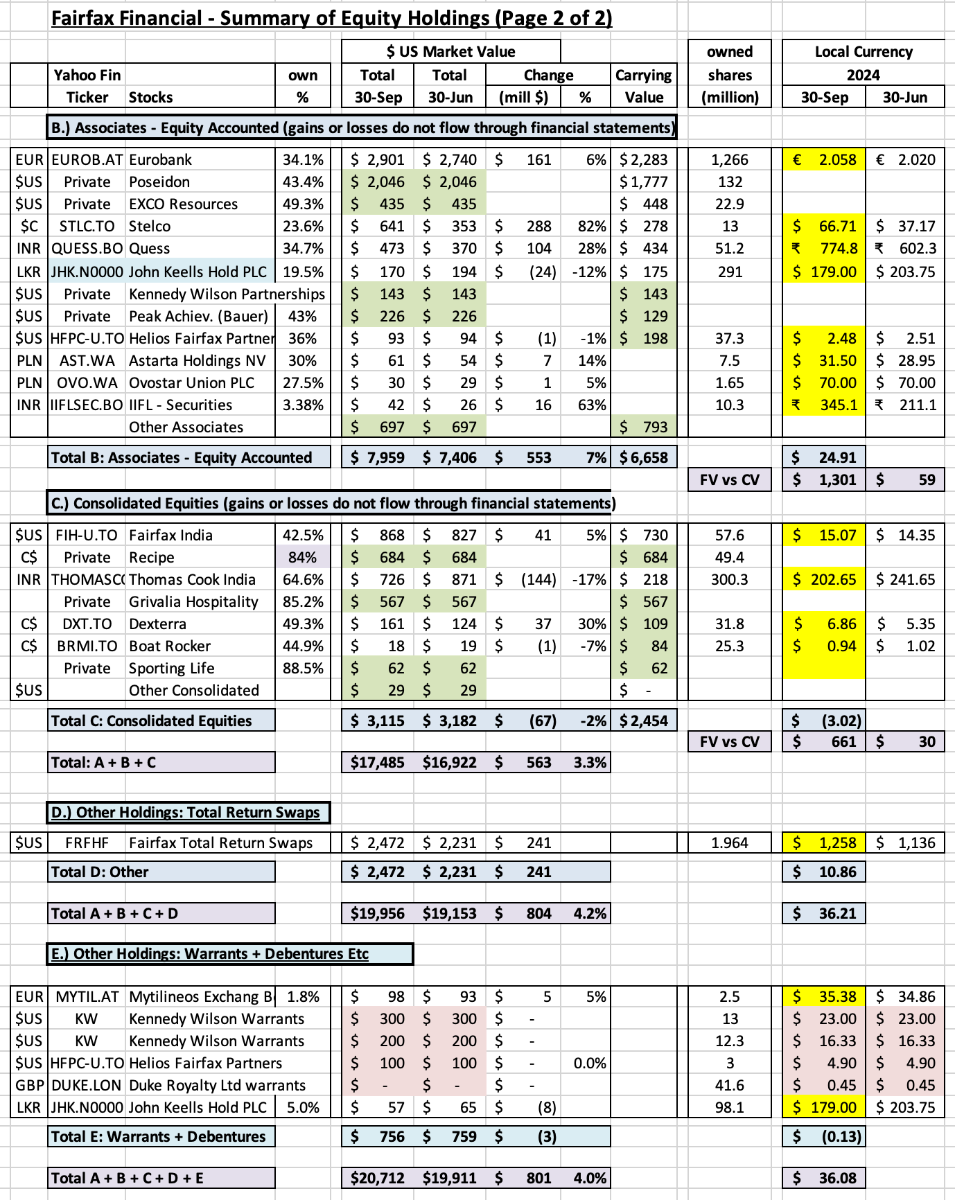

Estimate of change in value of Fairfax’s equity portfolio in Q3 - 2024 Fairfax’s equity portfolio (that I track) increased in value in Q3, 2024 by about $800 million (pre-tax) or 4.0%, which is a solid result. It had a total value of about $20.7 billion at September 30, 2024. After being a headwind in 1H 2024 (on US$ strength), currency flipped to being a tailwind in Q3 (on US$ weakness). Notes: I include the FFH-TRS position in the mark to market bucket and at its notional value. I also include warrants and debentures that Fairfax holds in the mark to market bucket. My tracker portfolio is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). My equities tracker does not include the change in value of Digit, Fairfax's P/C insurance company in India that is now publicly traded. The total value of Digit increased about $400 million in Q3. This amount needs to be adjusted to reflect Fairfax's ownership stake. Split of total holdings by accounting treatment About 47% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 53% are Associates and Consolidated holdings. The Sleep Country and Peak Achievement (Bauer) acquisitions (which are expected to close in Q4) will significantly increase the consolidated bucket of holdings. Over the past couple of years, the share of the mark to market holdings has been shrinking. This means Fairfax's quarterly reported results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of about $800 million = $36/share (pre-tax) The mark to market change is an increase of about $315 million = $14/share. This does not include the gain on the sale of Stelco when it closes (expected in Q4). The change in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports each quarter. What were the big movers in the equity portfolio Q1-YTD? Stelco is up $288 million. Fairfax is expected to book an estimated pre-tax gain of $390 million on the sale of its 13 million shares in Stelco. The sale is expected to close in Q4 2024. The FFH-TRS is up $241 million and is now Fairfax’s second largest holding at $2.5 billion. Eurobank is up $161 million. Currency has been a tailwind in Q3 (strong Euro). Quess continues its big move higher, and is up another $104 million. Market value of $473 million now exceeds carrying value of $434 million. Thomas Cook India, down $144 million, gave back some of its recent gains. Market value of $726 million significantly exceeds carrying value of $218 million. Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $2.0 billion pre-tax ($89/share). The 'excess' of FV to CV has been materially increasing in recent years. This is a good example of how book value at Fairfax is understated. Excess of FV over CV: Associates: $1.3 billion = $59/share Consolidated: $661 million = $30/share Equity Tracker Spreadsheet explained We have separated holdings by accounting treatment: Mark to market Associates – equity accounted Consolidated Other Holdings – total return swaps and warrants and debentures The value of each holding is calculated by multiplying the share price by the number of shares. All holdings are tracked in US$, so non-US holdings have their values adjusted for currency. This spreadsheet contains errors. It is updated as new and better information becomes available. Fairfax Oct 1 2024.xlsx

-

Did the conflict in the middle east not just get kicked up another notch? It looks like Israel has decided the Hezbollah threat in Lebanon needs to be addressed. Are we learning the emperor has no clothes (Iran and its proxies / those who want Israel to disappear)? Or is this simply the ‘calm’ before the storm? It is interesting that financial markets appear to be ignoring the wars in middle east.

-

@John Hjorth your comment gets at political culture. Russia has never had a democratic political culture (they tried for a brief time and not surprisingly it was a catastrophe). Democratic political cultures are not the norm - autocracies are the norm (I am including autocracies masquerading as democracies here). So I am not sure Russia will ever get one.

-

I think that might be the real lesson here. Buying Fairfax India at book value (or at a premium)g it appears there was little margin of safety. The emotional toll has also been significant for some long term holders. The stock today has a margin of safety. Importantly, a new investor also does not carry the emotional baggage of some long term investors. It really is an interesting case-study. Importantly, the most important chapters of the story are still being written (like BIAL) or have yet to be written.

-

@ICUMD At the end of the day we need to be as rational as possible. If your analysis told you it was the time sell and move on then that is the right decision for you. Here is my take on Fairfax India. I think the stock is cheap. I also think there is a good chance that significant ‘hidden’ value will be realized when the BIAL IPO happens. The issue with Fairfax India is when the value will be realized by Fairfax India and Fairfax. Not is the value actually there. As a result, i view Fairfax India not as a speculation but primarily as a timing play. For patient investors, the risk/reward looks pretty attractive. Do I own Fairfax India shares today? No. That is primarily because I am way overweight Fairfax. However, i have owned Fairfax India many times in the past as a short term trade. I usually have kept my position size modest. ————— The key is what is the value of the collection of assets that Fairfax India owns? And what has it done over the past 5 years? I think BIAL is the real deal. Coiled springs usually (eventually) get released.