Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Munger_Disciple , here is another way to look at tail risk... I live in Vancouver. There is a very good chance that we will get hit with an earthquake at some point in the future - we just don't know when and how big. So knowing this, is it rational for a person to live in Vancouver? Perhaps a better example is hurricane risk in Florida - or in many parts of the US. Lots of really bad hurricanes are coming in the next 50 years. we just don't know exactly where they are going to hit and when. Is the rational solution to move to a different part of the US? Again, the problem I have is I just don't know how to create something actionable from what I think I 'know.' If there is a 1% or even a 2% risk (timing of which is unknown), does that mean the investment should be avoided? Perhaps the answer is that ultimately there are no risk free investments (including Berkshire Hathaway). And perhaps this opens up the element of luck and its influence on investment returns. This is a really interesting topic.

-

@Munger_Disciple , the challenge I have with 'tail risks' like the one scenario you mention above is I have no idea how to model them into my valuation for the company. What you are discussing is not specific to Fairfax - it is a risk to the entire P/C re/insurance industry. TODAY, NO P/C INSURANCE STOCKS HAVE YOUR SCENARIO FACTORED INTO THEIR STOCK PRICE. One of the biggest reasons I like Fairfax so much today is relative valuation - it trades at a much cheaper valuation than all peers. Despite having: 1.) the best 5 year track record (growth in BVPS) 2.) the best management team (in terms of capital allocation) 3.) the best near-term earnings outlook Given the exceptional near-term outlook for the company I am willing to overlook the risk of $600B loss event. It really is an interesting thought exercise - not specific to Fairfax, but all P/C insurance stocks. Does it really mean they are all uninvestable for a rational investor? If so, why is Buffett loading up on Chubb? They would get killed if we had a $600B loss event. Is Buffett not thinking clearly?

-

Lots of interesting posts in this thread. My largest equity buy the past 3 months was; 1.) increased my Fairfax position by 20% at average cost of C$1,485 on Aug 2. Fairfax delivered better than expected results and the stock sold off about 8% over 2 or 3 days. 2.) increased my Fairfax position by another 20% at an average cost of about C$1,445 on Aug 7. When including the gain from the recently announced sale of Stelco and the excess of FV over CV of the equity holdings, Fairfax was trading at close to 1 x BV - crazy cheap. With the spike in Fairfax's share price over the past 2.5 weeks I have sold 75% of the shares I added. The average gain was about 7% - that is what I am targeting with these types of trades so I often sell early. I did something similar when Fairfax sold off aggressively in early Feb (when Muddy Waters published the 'report' of a UFO sighting). I find 'flexing' my position size (up and then back down) in my best ideas can be a good way to get a little extra return out of my best ideas. This strategy works best when a stock is very volatile - and it looks like volatility in Fairfax is picking up a little. This strategy worked very well for me with Fairfax when it traded on the NYSE from 2003 to 2009 (Fairfax delisted from NYSE in 2009). I only 'flex' in my tax free accounts (RRSP, LIF, RESP etc). I will do it very selectively in my TFSA account. So my 7% short term gain in Fairfax has no tax consequences. I keep about 25 to 30% of my portfolio for tactical opportunities like this. My goal with this portion of my portfolio is to simply earn a modest 8 to 10% over a year - no pressure. When not invested it sits is cash and earns 3.5% to 4%. I love having cash on hand when Mr. Market gets irrational, like it did a couple of weeks ago. My experience (over 20 years of investing) is a couple of wonderful opportunities that fall in my circle of competence will present themselves each and every year - I just don't know in advance what they will be. But that's ok with me.

-

I am in the process of getting back up to speed on Poseidon. With profitability at the company spiking (as the new-builds come on line) and interest rates come back down my guess is this investment is poised to outperform (perhaps significantly) in the coming years. This is Fairfax's 3rd largest equity holding (after Eurobank and FFH-TRS) so this would be very good news for Fairfax and its shareholders. I have a question for board members: What type of an investment is Poseidon (well really Seaspan)? What other company is it mostly like? It is in the containership industry. But from a functional perspective, with its contracted/stable long term cash flow business model, is Poseidon (the Seaspan part) in practice more a utility-like business? Is Poseidon (the Seaspan part) kind of like Fairfax's equivalent of Berkshire Hathaway's Mid-American energy? Not an exact match of course. My guess it's not a fluke that Sokol, who was the architect of Mid-American Energy when he has at Berkshire Hathaway, chose Seaspan/Atlas as his next act. Are the two businesses more similar than is generally recognized? Anyways, how do other board members view this investment?

-

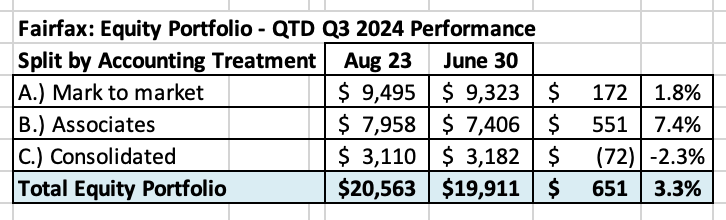

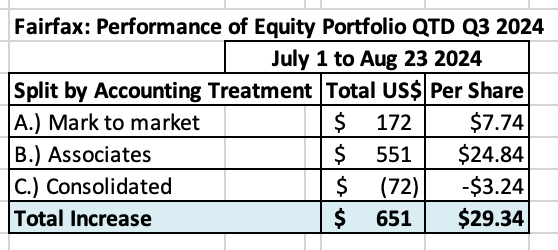

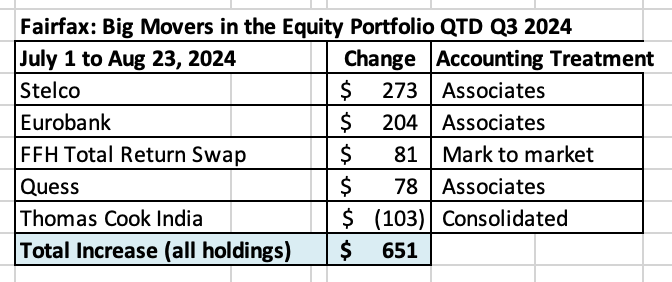

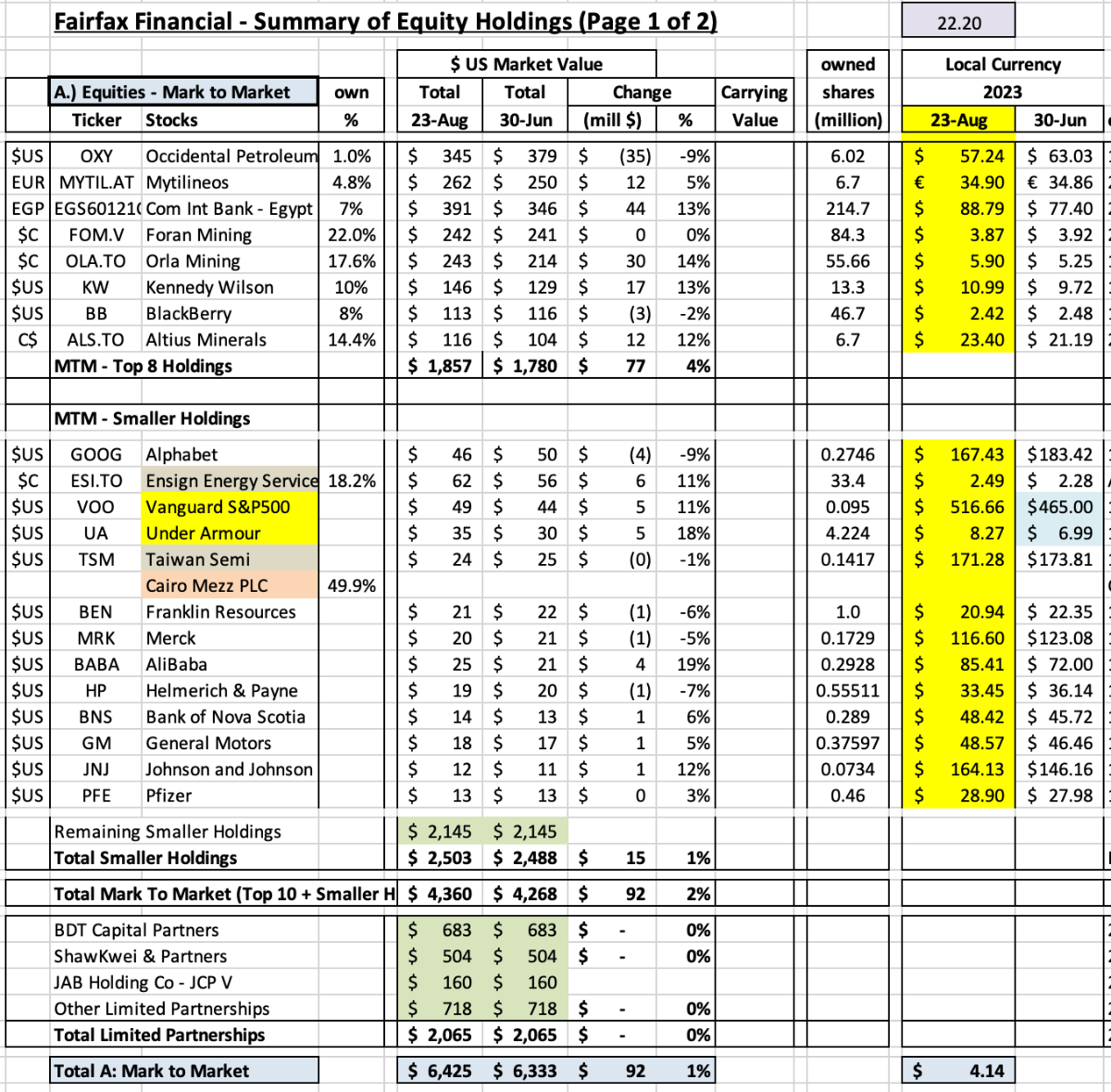

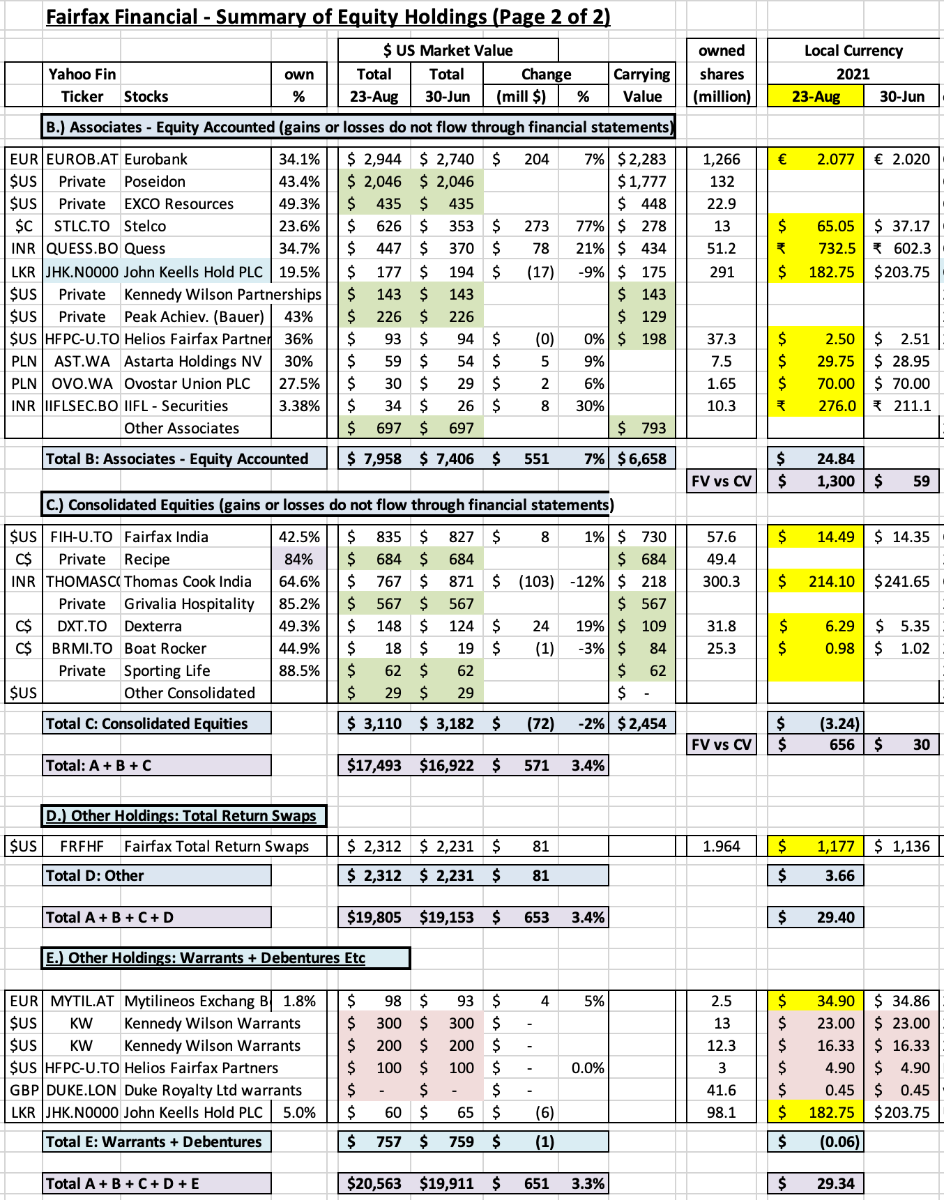

Change in value of Fairfax’s equity portfolio QTD (July 1 – Aug 23) 2024 Fairfax’s equity portfolio (that I track) increased in value QTD in Q3 (to Aug 23) by about $650 million (pre-tax) or 3.3%, which is a solid result. It had a total value of about $20.6 billion at August 23, 2024. After being a headwind in 1H 2024 (US$ strength), currency flipped to being a tailwind in Q3 (US$ weakness). Notes: I include the FFH-TRS position in the mark to market bucket and at its notional value. I also include warrants and debentures that Fairfax holds in the mark to market bucket. My tracker portfolio is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 46% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 54% are Associates and Consolidated holdings. Over the past couple of years, the share of the mark to market holdings has been shrinking. This means Fairfax's quarterly reported results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of about $650 million = $29/share The mark to market change is an increase of about $172 million = $8/share. The change in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports each quarter. What were the big movers in the equity portfolio Q1-YTD? Stelco is up $273 million. Fairfax will book an estimated pre-tax gain of $390 million on the sale of its 13 million shares in Stelco. The sale is expected to close in Q4 2024. Eurobank is up $204 million. Currency is a tailwind QTD (strong Euro). The FFH-TRS is up $81 million and is now Fairfax’s second largest holding at $2.2 billion. Quess continues its big move higher, and is up another $78 million. Market value of $447 million now exceeds carrying value of $432 million. Thomas Cook India, down $103 million, gave back some of its recent gains. Market value of $767 million significantly exceeds carrying value of $214 million. Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $2.0 billion pre-tax ($88/share), up about $300 million QTD. The 'excess' of FV to CV has been materially increasing in recent years. This is one good example of how book value at Fairfax is understated. Excess of FV over CV: Associates: $1.3 billion = $59/share Consolidated: $656 million = $30/share Equity Tracker Spreadsheet explained: We have separated holdings by accounting treatment: mark to market, associates – equity accounted, consolidated, other Holdings – total return swaps. We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. This spreadsheet contains errors. It is updated as new and better information becomes available.

-

+1. The P/C insurance model pioneered by Buffett (leverage float) is simple to understand. And difficult to execute well.

-

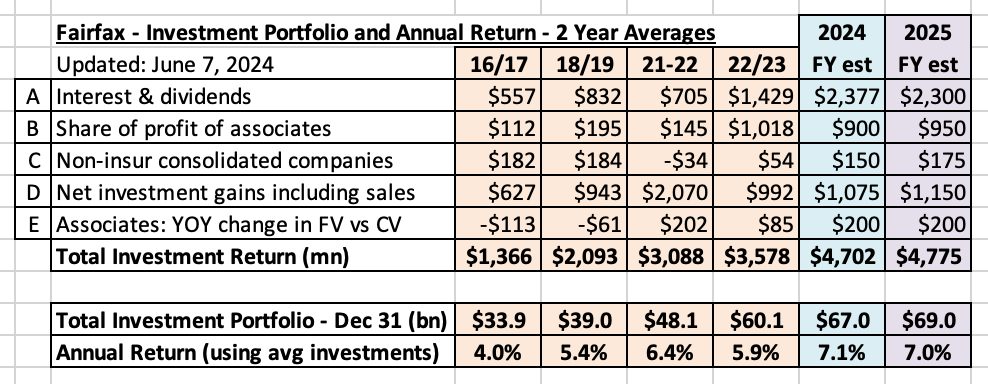

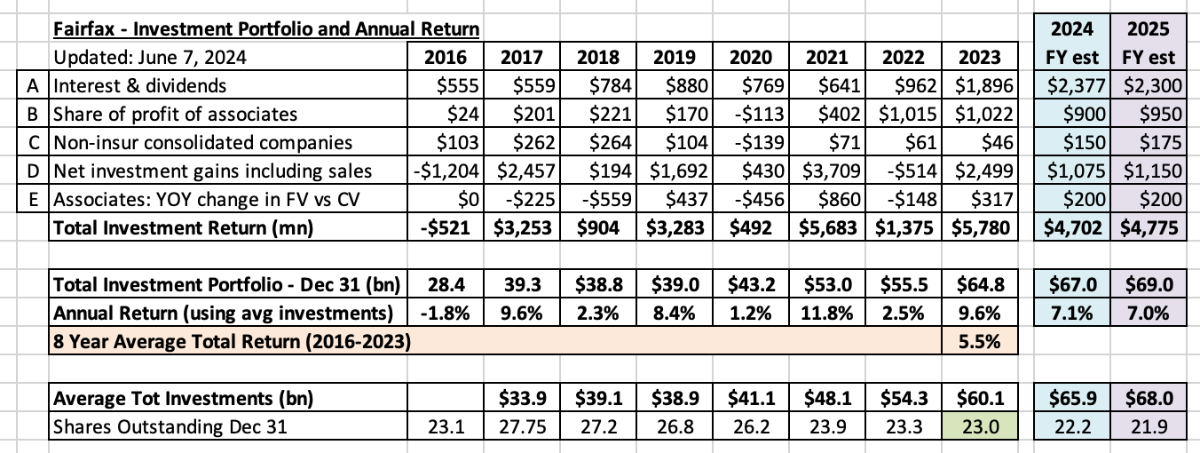

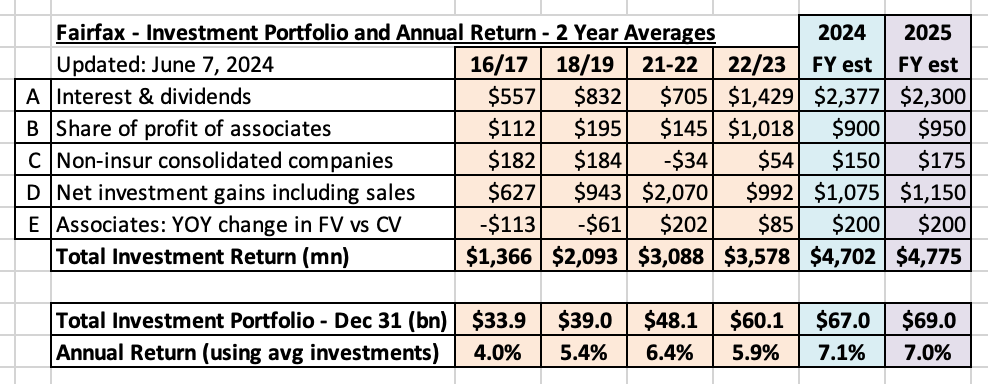

For board members who think 5% is a good 'normalized' return to use for Fairfax for its investment portfolio... let me stir the pot a little. From 2016 to 2022, Fairfax had four severe headwinds battering its investment portfolio: 1.) Zero interest rates 2.) Significant losses from the equity hedge/short positions 3.) An equity portfolio that was stuffed with shitty companies 4.) Historic bear market in bonds in 2022. Despite these 4 significant headwinds, from 2016 to 2022, Fairfax still earned an average return of about 5.4% on its total investment portfolio. Today, none of those headwinds exist. Some have been eliminated (equity hedge/short). And others have reversed and become tailwinds: 1.) Interest rates have normalized to much higher levels. It is highly unlikely they return to the lows of a few short years ago. 2.) Fairfax's equity portfolio has been fixed and is much higher quality (in terms of earnings power). My guess is a 5.4% return on the investment portfolio was a trough (smoothed) number for Fairfax. Today, Fairfax is earning about 7% on its investment portfolio. If we continue to get a few large asset sales in the coming years (likely, given what we have seen the past 10 years) then I think 7% is a reasonable baseline estimate to use looking out the next 3 to 5 years. and yes, the results will be volatile from year to year. Here is the data for each year (from which the averages in the above table were calculated).

-

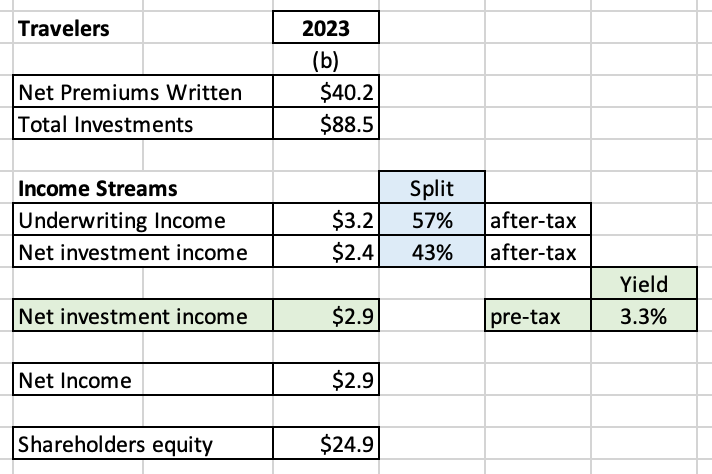

@73 Reds , to better understand some of the variables at play, let's look a Travelers 2023 numbers and compare them to Fairfax. When looking at Travelers 2023 numbers two things jump out: Underwriting income represents 57% of their income streams (like most P/C insurers, they only have 2 income streams). The yield (pre-tax) on their investment portfolio is about 3.3% (using the YE value of investment portfolio). Travelers is earning peanuts on its $88.5 billion investment portfolio - about 3.3%. It is expected to increase a small amount in 2024 ($200 million, which will bump the average yield to about 3.5%). This is because they are investing solely in fixed income. And it looks to me like they match the duration of their fixed income portfolio with their insurance liabilities. Now compare Travelers to Fairfax. Fairfax is earning about 7% on its investment portfolio - double what Travelers is earning (see the chart at the bottom of the post). That is a massive gap. Fairfax is earning much, much more on their investment portfolio for a couple of reasons: 1.) They do not restrict their investments to bonds/fixed income. 2.) They are an active manager - they look to exploit dislocations/volatility (wherever it shows up). 3.) They are very good at what they do. Comparing Fairfax and Travelers you really get some good insight into the power and value of the business model Fairfax that is successfully executing today. Below is a summary of investment returns for Fairfax. The returns have been smoothed over 2 year intervals to smooth out the annual volatility and make it easier to understand.

-

I have completed another update of my book/collection of posts on Fairfax. It contains lots of updates since the last version was published 2 months ago. The big change is the chapter on asset sales - all of my recent posts (over about a month) have been added. All other new posts from the past couple of months have also been added. Go to the first post at the top of this thread to access the updated PDF and Excel documents. I don't re-read the entire document when I post updated versions. If you see any big errors please let me know. The document now almost 500 pages. My goal is not size - but I will continue to add material that I think adds value for those interested in learnings more about Fairfax. Please note, not everything in the book has been brought up to date. That would have required a couple of months of work… and by the time it was done, much of it would be out of date again. My current plan is to keep updated parts of the document as time goes by. It continues to be a working document for me. The bottom line, this document should be a much better resource for board members / investors than what existed before. I hope you find it useful.

-

@Maverick47 when it comes to P/C insurance, I wonder if the overall market is a little more rational today than in the past. I look at all the shitty P/C insurance companies that Fairfax has purchased over the past 38 years - these have ALL been turned around. This does not mean there is not fierce competition. So we will see.

-

@nwoodman, I completely agree. “Ultimately Fairfax will turn out to be an OK or great investment based on their capital allocation, same as Berkshire. This means “don’t lose capital”.” Fairfax is a good underwriter and at a 95CR, underwriting income still only represents about 20% of their various income streams. About 80% comes from investments. So yes, Fairfax is levered much, much more to investments. I think underwriting income is something like 45% of the income streams for most P/C insurers, with investments driving the other 55% (mostly interest income). So Fairfax is also much more levered to the investment side of the business than peers. This also means earnings at Fairfax are impacted much less by the insurance cycle than other P/C insurance peers. My guess is this is not well understood by Mr Market.

-

@nwoodman I thought this would be interesting to dig into a little: “I am in the combined ratios revert to 100 camp.” Now i should say… i am not a P/C insurance guy. So i look forward to feedback from others who know much more than me on this topic. There is a lot of discussion on the board about Fairfax’s CR normalizing to 100 because ‘that is what always happens to P/C insurance.’ When i look at ‘P/C insurance’ I don’t see a homogenous business. Rather, i see a collection of very different businesses: - Personal lines or commercial? - Reinsurer or primary insurer? - Standard or specialty? - Is the business skewed to short tail (property or auto) or long tail (professional liability or workers comp)? And then you have to overlay lots more important factors: - geographies (US, UK, Europe, MENA, India…. Etc). This is a big one (getting bigger for Fairfax.) - reserving history The bottom line, I don’t think there is a ‘P/C insurance market.’ It looks to me like there are many (hundreds?) of P/C insurance markets. Especially for a global company like Fairfax. As a result, I think it highly unlikely that global insurance markets enter a synchronized soft market. instead, maybe we get rolling soft markets? A good example is workers comp in the US. I think it has been in a soft market for the past 5 years. This is significant business for Fairfax that looks poised to start to grow again in the coming years (just not sure when). Intact Financial just warned about outsized catastrophe losses in Canada in Q3. They are the 800lb gorilla here - perhaps this extends the hard market another year here in Canada. Bond yields have come way down in recent months. Central banks are easing - so yields could move even lower in the coming months/year. Many insurers were not able to roll a significant amount of their portfolio into longer dated bonds at peak rates (perhaps they missed the window). Lower bond yields moving forward will likely result in more discipline from most P/C insurers (they will need a solid CR to deliver the ROE expected by Wall Street). WR Berkley keeps getting asked on conference calls if the ‘hard market’ is over. They keep saying the P/C insurance market (in the US) is splintering into ‘markets’, each with its own cycle (some soft, some hard and others in between). Now we could get a really bad year for catastrophes and Fairfax’s CR might temporarily pop over 100 for that year. Perhaps we get two of these in a row - anything is possible. But do we get 4 or 5 years in a row? Never say never, but that seems highly unlikely. Why? Because Fairfax looks too diversified (line of business, geography etc). The diversification is beneficial not just in terms of catastrophe exposure. It is also really beneficial in terms of the insurance market cycle (does India’s auto market run lock step with that of the US)? The other really big factor is reserving. We could see reserve releases in the coming years surprise to the upside (especially if inflation comes down hard and stays low for years) - this might actually drive CR’s even lower for Fairfax (into the low 90’s, like we saw a decade ago). Not my base case. But not crazy talk either. Bottom line, i think we have pretty good line-of-sight as to what a ‘normalized’ CR is for Fairfax in today’s environment. But 4 or 5 years from now? I don’t have a strong opinion. But that is the same for all P/C insurers (not just Fairfax). Now it could be that i am completely out of my league - i have not owned Fairfax through a brutal hard market. So my view might simply be like a Disney movie. So i will continue to closely monitor the situation. What i do care deeply about: Is Fairfax a disciplined underwriter? How disciplined/good are they? I think the insurance cycle in the US will matter for Fairfax’s stock price (and all P/C insurers). If we get word that the hard market in the US has ended and P/C insurers are losing their discipline my guess is ALL P/C insurance companies will get taken out behind the woodshed. Which would probably give Fairfax the opportunity to buy back all the shares they want at very attractive prices. What i love about Fairfax right now is their flexibility/optionality - ability to flip the script - to actually benefit from what looks like a bad thing.

-

@73 Reds sorry, i have not spent any time on what you ask. What i do know is they have been actively reducing their exposure to the catastrophe part of the business in recent years (primarily at Brit i think). I know other board members have posted on this topic in the past so hopefully they will chime in with their thoughts. ————— Here is an exchange during the Q&A from Fairfax’s Annual Meeting this year: Unknown Shareholder …my question is for Mr. Clarke, if he can answer. As a layman investor, I believe that, if a hurricane 5 catastrophic event happens to direct hit to Miami City, that might be a $500 billion event. I wonder if you agree with me. And Fairfax cost will be 1%. That's what I believe as a layman investor. And if this even happens twice in a row in 2 years, how Fairfax can see their balance sheet... V. Watsa So before Peter answers. That's exactly right. We look at stuff like that. And if it happens, how are we going to survive that? So the big [ plus ] on these events is their limits, right? And so we really focus on the worst case events, from mainly Odyssey and Allied, but Peter? Peter does all the modeling and looking at it all the time. Peter? Peter Clarke Sure. Yes, no, as Prem said, we're focused on our catastrophe exposure, of course. And it starts with our insurance operations. The #1 thing is they have to manage their risk appetite within their capital base, but on top of that, we do a lot of work at the Fairfax level aggregating the exposures. And we really look at PMLs. So this is your probable maximum losses. And over the last 3 or 4 years, from our premium growth, we've benefited greatly from the diversification we now have within that 30 billion of premium that we write. And we can really absorb -- we can absorb significant catastrophes and still show an underwriting profit. Like the last couple of years -- this past year, cat losses were marginally down, so we had a fairly good year, but the year before that, we had probably -- I think we had 1.3 billion of losses, and over 1 billion the year before, and still posted underwriting profit. So as our premium base got bigger, we have more margin in the business for catastrophe losses, but our exposure has stayed relatively flat. So we do look at it. Northeast wind is one of our largest exposures. Southeast hurricane wind again is another one, so we're all -- we're on top of that. We look at it all the time and starts with our companies, yes. We have a team at the head office that we look at it. And of course, he's all into the details as well, so... V. Watsa That's the one risk that can destroy our company, so we are all focused on it all the time. You mentioned Miami. Of course, Houston, California earthquake, right, those are all big item, but one that you worry about -- there's a windstorm coming along, what he was saying, northeast wind. It's coming along the coast and hitting New York, rarely happened. It's happened once or maybe twice. Coming along -- it doesn't come into the -- it doesn't come inland, comes along and then comes into New York, which would be the -- we think, the worst one, and -- but we look at all of that all the time. So your question is a good one. That's something you have to do. You have to survive, stuff like that.

-

I think investment gains are 'devilishly' difficult to forecast over any one or two year span. However, I think it gets easier as you build an estimate over a longer time frame (like 3 or 4 years). If you go back 10 years, it is pretty easy to calculate an average for 'investment gains.' It could be separated into large 'one-time' gains and more 'normal' mark to market changes. But Fairfax's investment portfolio is much, much larger today than 10 years ago. The size of the equity portfolio is also much larger. And the quality of the equity portfolio (in term of earnings power) is also much better. So my guess is the size of 'investment gains' coming from the equity portfolio in the coming years will be much larger than what it has been in the past. In the past, it was crazy the significant value that Fairfax was able to surface with very timely asset sales from the insurance bucket of holdings: First Capital, ICICI Lombard, Riverstone Europe, pet insurance and Ambridge. None of the significant gains from each of those sales were built into earnings models before they happened. This does not include significant asset sales that have happened in the investment portfolio. I think this is instructive. Asset sales are a great example of just how different Fairfax and Berkshire Hathaway execute their business models. Fairfax has realized significant value over the years from asset sales (and it has also been a significant source of cash for the company). The beauty of Fairfax's active management/value investing model is they simply take what Mr. Market is giving them at the time. Insurance one day. Equities another day. Fixed income another day. Sometimes the value creation is rapidly growing the P/C insurance business in a hard market. Other times it is buying an asset at a low valuation (insurance or investments). Other times it is selling an asset at a premium valuation (insurance or investments). it is a little bizarre how some investors think Fairfax’s opportunity set is going to suddenly disappear in the coming years (or that they are suddenly going to get incredibly stupid).

-

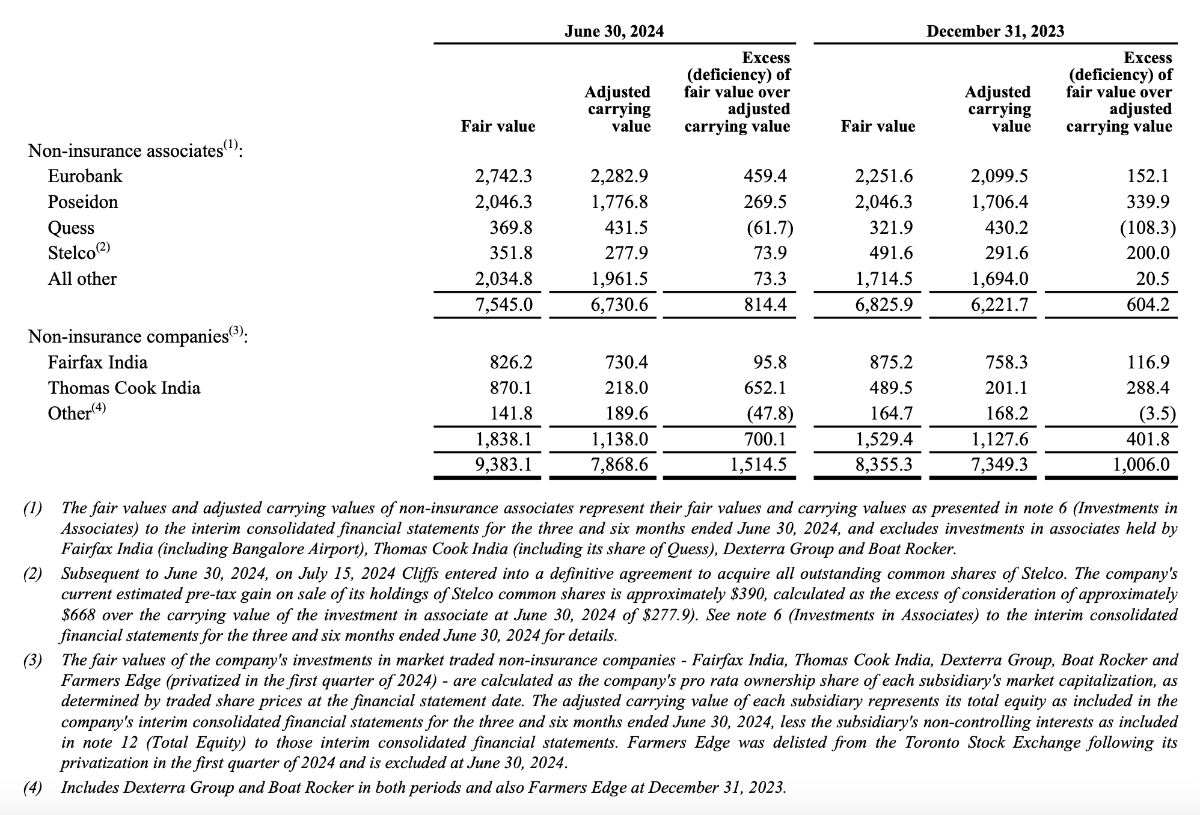

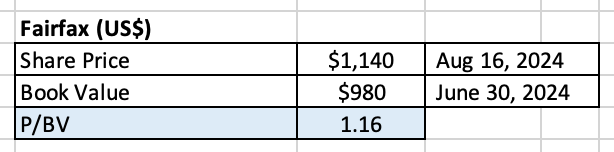

I did a small edit to my long post from Sunday. I thought it would be useful to include more details for the Fairfax portion of the post. The edited portion is below. It is timely because I am updating my earnings forecast for Fairfax for 2024 and 2025 (small changes). As I work though my earnings update, one item keeps jumping out to me - and that is the excess of fair value over carrying value for Fairfax's non-insurance associate and consolidated holdings. Something that is not even included in my earnings update. What is the problem? Over the first 6 months the excess of FV over CV had increased by more than $500 million = +$20/share pre-tax. The total is $1.5 billion = $68/share (pre-tax). When I think about 'normalized' earnings for Fairfax I include the excess of FV over CV - it is value that is being built by Fairfax over time. And as we have learned with Fairfax over the years, they will find a way to monetize this value (so that it is reflected in EPS and BVPS). When we look at published earnings forecasts for Fairfax (2024, 2025, 2026, 2027 etc) we need to remember that an important component is NOT BEING INCLUDED. As a result, EPS understates the economic value that is being created each year. Probably by about $10/share. And this gap will likely widen in future years. Why will it widen? 1.) Fairfax has a large and growing amount allocated to equity investments. 2.) The share count is materially shrinking each year. 3.) The quality (in terms of earnings power) of this collection of holdings has never been better in Fairfax's history - significant value is now being created/compounded each year by this collection of holdings and a large piece of this value creation is not being captured in EPS or BVPS. Large investment gains are coming in the future In the coming years, Fairfax will be monetizing the excess of FV to CV. And the investment gains will likely be higher when they do - because the intrinsic value of many of these holdings is higher than the FV. This is really hard for most investors to understand - it's like the 'spoon bending mind scene' in the Matrix movie. When they happen, these large investment gains will be incremental to current EPS estimates. They will catch analysts and investors by surprise. EVEN THOUGH WE KNOW THEY ARE COMING. This is one good example of how investors are underestimating future earnings for Fairfax. And estimates of future earnings determines the value of a stock. So investors continue to undervalue Fairfax's stock today - probably significantly. Of course Fairfax 'gets it.' and that is why they are being so aggressive with stock buybacks - even at a small premium to book value. Stelco is a good current example. At June 30, 2024, Stelco had a FV = $351.8 million and a CV = $277.9 million; excess of FV over CV = $73.9 million. On July 15, Stelco was sold to Cleveland Cliffs for about $668 million. Fairfax will book an investment gain of about $390 million. The actual investment gain ($390m) is significantly more than the excess of FV over CV at June 30, 2024 ($73.9m). With a CV = $277.9, Stelco was being significantly undervalued on Fairfax's balance sheet at June 30, 2024. Now that the sale has been announced, the $390 million gain will now get included in EPS and BVPS. And everyone is shocked and/or surprised... who could have know that something like this was going to happen? The 'investment gains' spring at Fairfax is getting coiled ever tighter. Lots more of these 'suprises' are coming in the future... We just don't know the timing or the details. Most investors though will continue to pretend they don't exist. This approach will simply give some investors a big advantage when it comes to understanding Fairfax (future earnings) and assessing its current valuation. Sale of Stelco Holdings Inc. (From Fairfax's Q2-2024 earning report) On July 15, 2024 Cleveland-Cliffs Inc. ("Cliffs") entered into a definitive agreement with Stelco to acquire all outstanding common shares of Stelco for consideration of Cdn$70.00 per share (consisting of Cdn$60.00 cash and Cdn$10.00 in Cliffs common stock). Closing of the transaction is subject to shareholder and regulatory approvals, and satisfaction of other customary closing conditions, and is expected to be in the fourth quarter of 2024. The company's current estimated pre-tax gain on sale of its holdings of approximately 13 million common shares of Stelco is approximately Cdn$531 ($390), calculated as the excess of consideration of approximately Cdn$910 ($668 or $51 per common share) over the carrying value of the investment in associate at June 30, 2024 of approximately Cdn$379 ($277.9). ============ Below is the edited piece from my post on Sunday. Here is the link to the complete post: https://thecobf.com/forum/topic/20517-fairfax-2024/page/75/#comment-575416 What does all of this have to do with Fairfax? Fairfax has a significant portion of its equity portfolio in equities (about 30%). Over the past 5 years, Fairfax has been shifting from mark to market type holdings to associate/consolidated holdings. The proposed Sleep Country acquisition is the latest example of this trend. A gap between the fair value and the carrying value of these holdings has been growing in recent years. It is sizeable today – at June 30, 2024, the excess of FV over CV was $1.5 billion, or $68/effective share (pre-tax). Importantly, the excess of FV over CV has increased by $508 million over the first 6 months of 2024. This value creation is not captured in EPS or BVPS. And there is likely a sizeable gap between intrinsic value and fair value, as we recently learned with the sale of Stelco (it was sold for much more than ‘fair value.’ What did Fairfax have to say on the matter in their Q2, 2024 earnings report? Excess (deficiency) of fair value over adjusted carrying value "The table below presents the pre-tax excess (deficiency) of fair value over adjusted carrying value of investments in non-insurance associates and market traded consolidated non-insurance subsidiaries the company considers to be portfolio investments. Those amounts, while not included in the calculation of book value per basic share, are regularly reviewed by management as an indicator of investment performance. The aggregate pre-tax excess of fair value over adjusted carrying value of these investments at June 30, 2024 was $1,514.5 (December 31, 2023 - $1,006.0)." Stock buybacks Fairfax has also been very aggressive with stock buybacks in recent years. And they have picked up the pace so far in 2024. "During the first six months of 2024 the company purchased for cancellation 854,031 subordinate voting shares (2023 – 179,744) principally under its normal course issuer bids at a cost of $938.1 (2023 - $114.9), of which $726.5 (2023 - $70.4) was charged to retained earnings." Fairfax Q2-2024 Report This year Fairfax has been buying back stock at an average price of $1,098/share. At Q2-2024, book value was $979.63. Fairfax is buying back a meaningful amount of stock at a price that is higher than book value. This will likely continue moving forward. Why are they doing this? Fairfax understands its book value is understated.

-

+1 I really do appreciate the opportunity to debate with other board members. We have a wonderful community of smart, thoughtful investors

-

@nwoodman you make some great points: 1.) Fairfax's past mis-adventures and scar tissue. Making mistakes can be a wonderful educator. My guess is past mistakes have actually made Fairfax a stronger company today. And they are still recent enough that management likely still is feeling their sting. And I like that. 2.) Great point about 'access to information'. Given how Fairfax thinks and operates this (they think about the economy and macro) getting real time information from the various businesses they own should help. 3.) You have spoken many times in the past about relationships/deal flow. What Fairfax did with Kennedy Wilson ($4 in real estate mortgages) last year provides perhaps the best recent example. Fairfax has spend decades building out their partnership/relationship networks. This should be another tailwind moving forward.

-

@Munger_Disciple , I don't think anyone is assuming that Fairfax will deliver a long term ROE of 20%. Today, I think there is a pretty good chance that Fairfax can deliver a 15% ROE over the next 3 years. Important: in my ROE 'calculation' I include excess of fair value over carrying value for the equity holdings. That does not show up in earnings or book value, but I think it is value creation that needs to be captured. Year 4 and further out? My guess is Fairfax will continue to do well, but I have no idea how well. There are too many unknowns. But I don't need to know what Fairfax will do in 4 or 5 years. Because in 3 years time (August 2027) I will have a very good handle on what I think Fairfax can do from August 2027 to 2030. What I do with my Fairfax position will be driven primarily by what I think I KNOW. Not what I don't know. What your analysis is missing is the reflexivity thing that George Soros is so famous for (I hope I don't get this wrong). But let's assume the CR for all P/C insurance companies go to 100 for years - not a one year blip caused by record catastrophes. If this happens, the share prices for many P/C insurers will get killed. This will likely present the perfect opportunity for a flush with cash player (like Fairfax) to make a big P/C acquisition at an attractive price. Soft insurance markets are a great time to grow via acquisition. That is exactly what Fairfax did from 2015 to 2107 - they used the then soft P/C insurance market to build out their global P/C insurance footprint (the fact they were able to do this when they were cash poor is amazing). In a soft insurance market Fairfax will also have the ability to shift capital to more productive uses. Like 2020, maybe Fairfax's share price gets taken out behind the woodshed. This will simply give Fairfax the opportunity to take out a meaningful amount of shares at a very attractive price (perhaps below book value). Whatever boogeyman we can think of for Fairfax there is a flip side to it - something Fairfax can use to its advantage. The worse the boogeyman the better the opportunity. Now could we see high volatility over the short term (say 12 to 24 months) in the share price? Yes. But that would simply create the opportunity for significant long term value creation (via significant buybacks). I am not assuming Fairfax will always make the most optimal decision moving forward and always come out smelling like roses. But I am also not doing the opposite - I am not assuming the worst because that is what Buffett says will happen. Fairfax tends to make their best investments (capital allocation) when adversity strikes. It is very counter-intuitive. Active management, volatility, unconstrained capital allocation and the power of compounding is a very potent combination. Especially when you are flush with cash - this is the new variable for Fairfax.

-

@StubbleJumper I am not trying to put words in your mouth - so please correct me if I am off base. Fairfax's future is like the multiverse in a Marvel movie. Fairfax has an infinite number of futures. 94CR is one. 4% interest rates is another. But there are an unlimited number of variables - many of which are very important. What your analysis largely ignores is management. It assumes Fairfax is a leaf getting blown by the wind - and where Fairfax goes will be determined by the wind. I completely disagree. I think the biggest factor that will determine Fairfax's future is not 'fate' (the wind) - it is management and the decisions they make. Why has Fairfax and Berkshire Hathaway performed so well over the past 38 years? Was it because of the P/C insurance cycle? Or the interest rates available on sovereign debt? Both companies excelled because of the P/C insurance model and the excellent decisions made by the management team over time. ----------- IMHO, what your mental model is completely missing is what we don't know - what the management team at Fairfax will do, especially when adversity (= opportunity) strikes. That is the same line of thinking that caused my to completely miss out on Berkshire Hathaway as an investment for decades - I couldn't see with certainty what Buffett was going to do so I way underestimated the value he was going to create in the subsequent years.

-

The problem with mean reversion is that logic assumes the past business model is largely the same as the current business model. Let's go back to 2010 when Fairfax put on the equity hedge/short trade. 'Reversion to the mean' logic would have lead a 'rational' investor to expect a 15% ROE type of performance from Fairfax over the next decade (2010 to 2020). Of course that did not happen. Fairfax significantly underperformed. Why? Mostly because of decisions made by the management team. Yes, zero interest rates was also a headwind. The Fairfax of today is very different than the Fairfax that existed 10 years ago and even more different than the Fairfax that existed 20 years ago. My view is the current version of Fairfax is the best yet (in the 20 years that I have followed the company). That suggests to me that future returns (the next 5 years) should be good, and there is a solid chance that they could be very good. Will Fairfax's results 'revert to the mean'. I have no idea. What matters to me is management and the decisions they are making (capital allocation etc). And what that is doing to the fundamentals of the business.

-

@nwoodman , what i find so fascinating about Fairfax is how much has been changing over the past 4 years. And with all the cash they are generating today (and the coming years) my guess is more good ‘surprises’ are coming. Because the historical information doesn’t help us very much - and this is what most investors rely on the most to guide them in their decisions. With my posts i am often trying to figure out and get ahead of what is perhaps coming next - stuff that is not on investors radar today that will be in another year or two. Eventually, the pace of change will slow and Fairfax will likely become a more normal, boring, simpler company to value.

-

Book value is the ‘North Star’ used by Wall Street to value P/C insurance companies. Why? One big reason is it is wicked easy. Book value per share for a company is usually an easy number to find (unless you are a company called Berkshire Hathaway or Markel). Slap a market multiple on it (usually the company’s historical/past multiple) and… it’s like magic… you KNOW what a P/C insurance company is worth. Compare your estimate with the company’s current share price and you KNOW if the stock is fairly priced, undervalued or overvalued. Investing is very easy. Is investing really that easy? Maybe it is. But sometimes this approach above gets ‘it’ completely wrong. What are the big problems with the approach above? Here are a couple: Sometimes book value does not tell investors what they think it does. Sometimes the historical/past multiple is not the appropriate number to use. A great set up for an investor is to find a P/C insurance company where two things exist: Book value is materially understated. The multiple being attached to book value is too low. In this post, we will dig into book value to see what we can learn. What is book value? Book value is a proxy for what a company is worth should it be liquidated. It is calculated as follows: Assets (A) - Liabilities (L) = Equity/book value (E). The biggest asset of a P/C insurance company - by far - is its investment portfolio. For most P/C insurance companies, the investment portfolio is invested mostly in fixed income instruments, like bonds. Fixed income investments are relatively easy to value. This provides a fair amount of accuracy/certainty when calculating book value for a typical P/C insurance company. Book value and market multiple P/BV is a good measure to use to compare P/C insurance peers. The ‘rule of thumb’ when it comes to book value and multiple for P/C insurance companies is as follows: P/BV = 1 x = This is likely a low quality company. P/BV = 2 x = This is likely a high quality company. Finding a quality P/C insurance company that is trading at a P/BV multiple of 1 x is usually a very good thing - as this likely means it is being undervalued. What can cause book value to not be accurate? To answer this question, we are going to focus on the asset bucket. What if assets are being undervalued on a company’s balance sheet? This will cause book value to be understated. Markets are efficient But I can hear your response… “markets are efficient.” Mr. Market KNOWS when assets are being undervalued on a company’s balance sheet. As a result, book value, multiple and market price will reflect all that is known. Therefore it is not possible for an investor to profit from this set-up. This might be the case for most large companies. However, I doubt it is the case for all companies. Especially smaller companies that are not followed very closely by investors and the investment industry. Peter Lynch and asset plays To help him with his analysis, Peter Lynch separated all of his investments into 6 categories. One of the categories was ‘asset plays.’ An asset play is a company that has a valuable asset(s) that Wall Street is ignoring. What does this have to do with P/C insurance companies? There are lots of things that can cause book value to be understated at a P/C insurance company. Below is one example. Not all P/C insurance companies put most of their investments into fixed income securities. A few put a large chunk of their investment portfolio into equities - both publicly traded and private/consolidated holdings. The market value of some equity holdings might be much higher than their carrying value - this difference will not be captured in book value. And it could grow for years and even decades. Ok, that is enough theory. Let’s pivot to the real world. ————— Warren Buffett, Berkshire Hathaway and book value For more than 50 years, Buffett was book value’s biggest cheerleader. He educated two generations of investors to use book value as the core input to: Quickly/easily value Berkshire Hathaway (in a very rough way). Evaluate the performance of the company’s management team over time (change in BVPS). To understand the importance of book value, all an investor had to do was read the opening paragraph of Buffett’s iconic shareholder letters. Buffett wrote pretty much the same introduction every year for decades. Here is an example from Berkshire Hathaway’s 2017AR: “Berkshire’s gain in net worth during 2017 was $65.3 billion, which increased the per-share book value of both our Class A and Class B stock by 23%. Over the last 53 years (that is, since present management took over), per-share book value has grown from $19 to $211,750, a rate of 19.1% compounded annually.” Warrant Buffett - BRK’s 2017AR Warren Buffett’s very public rug-pull on Berkshire Hathaway shareholders But something suddenly changed in early 2019. In Berkshire Hathaway’s 2018AR, Warren Buffett made a very public divorce from book value. Holy shit Batman! Given book value’s importance to Berkshire Hathaway and its investors for over 50 years, this was a seismic event. Buffett is no dummy. He must have had very good reasons for doing this. Below is what Buffett had to say on the matter in Berkshire Hathaway’s 2018AR: “Long-time readers of our annual reports will have spotted the different way in which I opened this letter. For nearly three decades, the initial paragraph featured the percentage change in Berkshire’s per-share book value. It’s now time to abandon that practice. “The fact is that the annual change in Berkshire’s book value – which makes its farewell appearance on page 2 – is a metric that has lost the relevance it once had. Three circumstances have made that so. “First, Berkshire has gradually morphed from a company whose assets are concentrated in marketable stocks into one whose major value resides in operating businesses. Charlie and I expect that reshaping to continue in an irregular manner. “Second, while our equity holdings are valued at market prices, accounting rules require our collection of operating companies to be included in book value at an amount far below their current value, a mismark that has grown in recent years. “Third, it is likely that – over time – Berkshire will be a significant repurchaser of its shares, transactions that will take place at prices above book value but below our estimate of intrinsic value. The math of such purchases is simple: Each transaction makes per-share intrinsic value go up, while per-share book value goes down. That combination causes the book-value scorecard to become increasingly out of touch with economic reality. “In future tabulations of our financial results, we expect to focus on Berkshire’s market price. Markets can be extremely capricious: Just look at the 54-year history laid out on page 2. Over time, however, Berkshire’s stock price will provide the best measure of business performance.” Warren Buffett – Berkshire Hathaway 2018AR Berkshire Hathaway changed as a company Warren Buffett purchase Berkshire Hathaway in 1965. Since then the company has changed dramatically. In 1967, Buffett purchased National Indemnity, which added the P/C insurance business model to the company. The float was invested over the years into publicly traded equities and to buy non-insurance companies. Over the years, the gap between the market/fair value and the carrying value of many of Berkshire Hathaway’s holdings has significantly widened - to the point where Buffett thought book value had lost its relevance as a useful metric for Berkshire Hathaway’s shareholders. A second important reason Buffett recently decided it was time for Berkshire Hathaway to start aggressively buying back its stock. Of course, stock would only be repurchased at prices that were below Buffett’s estimate of intrinsic value - so buybacks would be a good ‘use of cash’ for Berkshire Hathaway and its shareholders. However, the stock would be repurchases at a premium to book value (1.2 x or more). This would cause BVPS to actually go down. Over time, this ‘causes the book-value scorecard to become increasingly out of touch with economic reality.’ Buying back a significant amount of stock above book value over many years will mess up the informational value in the BVPS measure for investors. My guess is this a very hard concept for most investors to grasp. So what do you do if you are Warren Buffett? You go cold turkey and stop talking about and publishing book value and BVPS metrics. Buffett said that book value had ‘lost the relevance it once had.’ For long standing Berkshire Hathaway shareholders (of which there are many), it was like getting a bucket of ice water poured on their heads. What was an investor to use as a replacement to value Berkshire Hathaway and evaluate its management team? The change in its share price over time. Moving forward, Berkshire Hathaway shareholders should use Wall Street/ Mr. Market as their primary guide. WTF? Really? I get that book value has its flaws. But to flush in down the toilet as a useful tool and replace it with Wall Street/Mr. Market just seems a little bizarre/extreme. But I digress. And who am I to disagree with Warren Buffett? What does all of this have to do with Fairfax? Fairfax has a significant portion of its equity portfolio in equities (about 30%). Over the past 5 years, Fairfax has been shifting from mark to market type holdings to associate/consolidated holdings. The proposed Sleep Country acquisition is the latest example of this trend. A gap between the fair value and the carrying value of these holdings has been growing in recent years. It is sizeable today – at June 30, 2024, the excess of FV over CV was $1.5 billion, or $68/effective share (pre-tax). Importantly, the excess of FV over CV has increased by $508 million over the first 6 months of 2024. This value creation is not captured in EPS or BVPS. And there is likely a sizeable gap between intrinsic value and fair value, as we recently learned with the sale of Stelco (it was sold for much more than ‘fair value.’ What did Fairfax have to say on the matter in their Q2, 2024 earnings report? Excess (deficiency) of fair value over adjusted carrying value "The table below presents the pre-tax excess (deficiency) of fair value over adjusted carrying value of investments in non-insurance associates and market traded consolidated non-insurance subsidiaries the company considers to be portfolio investments. Those amounts, while not included in the calculation of book value per basic share, are regularly reviewed by management as an indicator of investment performance. The aggregate pre-tax excess of fair value over adjusted carrying value of these investments at June 30, 2024 was $1,514.5 (December 31, 2023 - $1,006.0)." Stock buybacks Fairfax has also been very aggressive with stock buybacks in recent years. And they have picked up the pace so far in 2024. "During the first six months of 2024 the company purchased for cancellation 854,031 subordinate voting shares (2023 – 179,744) principally under its normal course issuer bids at a cost of $938.1 (2023 - $114.9), of which $726.5 (2023 - $70.4) was charged to retained earnings." Fairfax Q2-2024 Report This year Fairfax has been buying back stock at an average price of $1,098/share. At Q2-2024, book value was $979.63. Fairfax is buying back a meaningful amount of stock at a price that is higher than book value. This will likely continue moving forward. Why are they doing this? Fairfax understands its book value is understated. Fairfax appears to have contracted the ‘Berkshire Hathaway disease.’ Book value is less useful than most investors realize - as a tool to use to value the company or evaluate the performance of the management team. And over time, book value will become even less useful. A couple of things suggest the impact on Fairfax will likely be more muted than Berkshire Hathaway: It is not clear that Fairfax wants to go full-on Berkshire Hathaway towards operating companies. But we will see what they do in the coming years. Fairfax has been keen over the years to surface significant hidden value via asset sales/asset revaluations. Berkshire Hathaway has largely been buy and hold forever, especially when it comes to the operating companies it owns. Fairfax’s current valuation Fairfax is trading today at P/BV multiple of 1.16 times. This is significantly lower than P/C insurance peers. This also does not include the estimated $390 million gain that is coming from the sale of Stelco. Or the earnings QTD. Or the significant undervaluation of the equity holdings (publicly traded and private/consolidated). Bottom line, despite the monster increase in the share price over the past 4 years, Fairfax’s stock looks like it continues to trade at a large margin of safety. How much is book value understated at Fairfax We can estimate some of the undervaluation for Fairfax. For associate/consolidated holdings, Fairfax does provide a fair value calculation for most holdings. This can be compared to their carrying value to come up with one measure of undervaluation for the group of holdings. But as helpful as this is, on its own it is incomplete. For some holdings, their ‘intrinsic value’ is likely much higher than Fairfax’s reported ‘fair value.’ What investments? My top 3 today would probably be: Poseidon, Grivalia Hospitality and BIAL. What about the P/C insurance holdings? Fairfax sold its pet insurance business in 2022 and realized a $1 billion gain (after tax). They also sold of Ambridge in 2023 for a sizeable gain. In 2021, Fairfax sold 10% of Odyssey for $900 million. Odyssey is NOT carried at a value of $9 billion. My guess is Fairfax's P/C insurance companies are carried on the balance sheet at a discount to their true value (and the gap could be significant for some assets). If so, this would just be another example of how Fairfax's book value is understated today. What do other board members think? Is Fairfax's book value understated? If so, how much? What is causing/driving the 'undervaluation?' Watch buybacks It will be interesting to see: If Fairfax remains aggressive with stock buybacks moving forward. The P/BV multiple they will pay. This will provide investors with important insight into how the management team at Fairfax values the company and its stock. =========== Intrinsic Value and Book Value - From Berkshire Hathaway’s Owner’s Manual The excerpt below is from Berkshire Hathaway’s Owner’s Manual - 1999 (this was the version that was on Berkshire Hathaway’s web site on August of 2024) INTRINSIC VALUE Now let's focus on two terms that I mentioned earlier and that you will encounter in future annual reports. Let's start with intrinsic value, an all-important concept that offers the only logical approach to evaluating the relative attractiveness of investments and businesses. Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life. The calculation of intrinsic value, though, is not so simple. As our definition suggests, intrinsic value is an estimate rather than a precise figure, and it is additionally an estimate that must be changed if interest rates move or forecasts of future cash flows are revised. Two people looking at the same set of facts, moreover - and this would apply even to Charlie and me - will almost inevitably come up with at least slightly different intrinsic value figures. That is one reason we never give you our estimates of intrinsic value. What our annual reports do supply, though, are the facts that we ourselves use to calculate this value. Meanwhile, we regularly report our per-share book value, an easily calculable number, though one of limited use. The limitations do not arise from our holdings of marketable securities, which are carried on our books at their current prices. Rather the inadequacies of book value have to do with the companies we control, whose values as stated on our books may be far different from their intrinsic values. The disparity can go in either direction. For example, in 1964 we could state with certitude that Berkshire's per-share book value was $19.46. However, that figure considerably overstated the company's intrinsic value, since all of the company's resources were tied up in a sub-profitable textile business. Our textile assets had neither going- concern nor liquidation values equal to their carrying values. Today, however, Berkshire's situation is reversed: Now, our book value far understates Berkshire's intrinsic value, a point true because many of the businesses we control are worth much more than their carrying value. Inadequate though they are in telling the story, we give you Berkshire's book-value figures because they today serve as a rough, albeit significantly understated, tracking measure for Berkshire's intrinsic value. In other words, the percentage change in book value in any given year is likely to be reasonably close to that year's change in intrinsic value. You can gain some insight into the differences between book value and intrinsic value by looking at one form of investment, a college education. Think of the education's cost as its "book value." If this cost is to be accurate, it should include the earnings that were foregone by the student because he chose college rather than a job. For this exercise, we will ignore the important non-economic benefits of an education and focus strictly on its economic value. First, we must estimate the earnings that the graduate will receive over his lifetime and subtract from that figure an estimate of what he would have earned had he lacked his education. That gives us an excess earnings figure, which must then be discounted, at an appropriate interest rate, back to graduation day. The dollar result equals the intrinsic economic value of the education. Some graduates will find that the book value of their education exceeds its intrinsic value, which means that whoever paid for the education didn't get his money's worth. In other cases, the intrinsic value of an education will far exceed its book value, a result that proves capital was wisely deployed. In all cases, what is clear is that book value is meaningless as an indicator of intrinsic value.

-

The CVR's from Resolute are interesting. The size of the duties on deposit with US government at the Canadian lumber producers is nuts right now. I think Canfor alone is approaching $1 billion in duties on deposit - and the softwood lumber duty just went up again. Today there appears to be no political will to get this issue resolved (in either country). But there is significant value there (duties on deposit). Tick, tick, tick... 'Duties on deposit' does not appear to be priced into any of the stocks today of the Canadian lumber producers. ---------- In 2006, the first softwood lumber dispute between the US/Canada was resolved. About 20% of the duties on deposit went to the US and 80% went to the Canadian producers. The irony is West Fraser used their windfall gain to fund/kick start their aggressive move into the US South. With hindsight, the softwood dispute/duties imposed by the US were the best thing that ever happened to the large BC producers - it motivated them to think different, which lead them to expand beyond BC. Less than 20 years later, West Fraser, Canfor and Interior have morphed from being large BC lumber companies (back in 2006) to being 3 of the top 4 lumber producers in North America today (and 3 of the largest in the world). And the BC lumber industry is in a massive secular decline (driven by mountain pine beetle and, more recently, terrible provincial government policy). https://www.westfraser.com/sites/default/files/MD%26A_2007.pdf

-

@petec Great summary - of a topic that has a fair bit of complexity and is not well understood.

-

@gfp thank fro the info. I did take a quick look at the Odyssey filing that you recently attached - lots of good information in there - but didn't think to use it here