Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

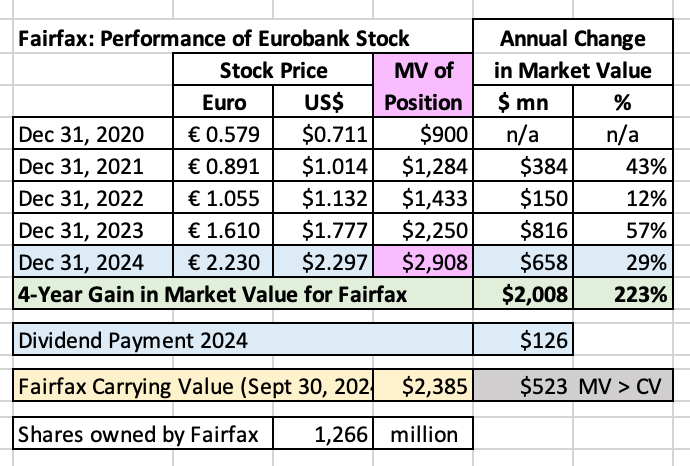

I am almost done putting together my ‘Top 10’ list of the most important things/events that drove shareholder value at Fairfax in 2024. My post should be out in the next couple of days. Eurobank deserves a special shout out. What it has accomplished/delivered over the past 4 years is amazing - it has delivered a total return of $2.1 billion to Fairfax shareholders (increase in market value + dividend paid). In 2024, it delivered a total return of $784 millon, or 35%. So it must be over valued today. Right? Wrong. It is still very (dirt?) cheap. (Tangible book value at Sept 30, 2024 was €2.27/share.) Importantly, it will be taking Hellenic Bank private in 2025 and this sets the table nicely for the next stage in the growth of the company (top and bottom lines). The management team at Eurobank has been making all the right moved for years now - and this should tell investors something. Bottom line, Eurobank is turning into one of Fairfax's best-ever investments. And it looks like it is just getting started. PS: one week into 2025, Eurobank's stock is up another $150 million.

-

@Redskin212, congratulations on your retirement. Here are some additional thoughts: One of my rules with financial planning is to try and keep things as simple as possible. That is one of the things I am trying to optimize for. I find professionals tend to add lots of complexity (which makes sense because that also justifies what they want to get paid). Retirement planning is like a marathon - I try and learn one or two important things a year. So I try and pace myself. Planning software is helpful - but my experience is it is very limited looking out 5 or 10 years (so much stuff can change in one year). YouTube has some very good channels - I exclusively follow Canadian channels because legislation/accounts/taxes are so different between Canadian the US. I keep curating my playlist (adding and subtracting channels depending on what I am trying to learn).

-

@Junior R, good question. When we were looking to rent (early 2021) lots of houses were available (compared to how tight the market normally is here in Vancouver). That helped (landlords appeared to be motivated/more flexible). We were very transparent with what we were doing (we used our real estate agent - who was also a friend - as a personal reference to help show our story checked out). I also shared our brokerage account statement with our landlords (I did not give them a hard copy). The big cost if we had purchased 3.5 years ago would have been the opportunity cost. I have been able to average a return of 35% each of the last three years. On $1 million that is $350,000 per year; on $2 million that is $700,000 per year. If we do buy a home again, I probably will use some debt to make the purchase. But our situation (no day job) does create challenges. And I generally hate having to deal with banks.

-

@Junior R , I am just starting to learn about estate planning and retirement planning. Early days. It's like light bulb went off in late 2023. I am learning there are lots of layers - so keeping things as simple as possible is very important. In terms of our decision to sell our house, it was primarily driven by our decision to move from the suburbs into the city (Vancouver). We made the decision in early 2021 when our youngest made the decision to go to UBC. This meant all three of our kids would be going to UBC. So my wife and I decided to move to the fun part of Vancouver (close to Kits). We have rented for the past 3.5 years and enjoy it. We did't buy for a couple of reasons. The big one was probably because houses where we were moving to cost $2.75 million (the old fixer-uppers cost this much). Our rent was $5,000/month. Bottom line, it was much, much, much cheaper to simply rent than to own. Personal wise, moving has been one of our great decisions (for both me and my wife). We love where we live today - it is a great fit for our current life stage. Financially, it has also turned into one of our best ever decisions. Because when we got the significant proceeds from our house sale (this was back in Covid when people were desperate to move into the suburbs which drove prices to the moon) I was following a little know P/C insurance company called Fairfax Financial. The proceeds from our house sale mostly - over time - went into this one investment... and have largely remained there. Bottom line, we have been very fortunate. Will we buy another home one day? Yes, I think we will. But it will likely be a terrible financial decision. and that is because of two reasons: 1.) I suspect the easy money has been made with real estate in Canada - for now (in terms of price appreciation). 2.) I am pretty good at compounding financial investments. We could buy a nice duplex for C$2 to $2.5 million. But that would be $2 to @2.5 million I wouldn't be able to invest. So if we buy one day, it will be primarily for personal/lifestyle reasons. We will do it with the expectation that it will likely simply break even from a financial perspective. Which is OK (it is what it is). What I do is think about things enough that I have a rough plan. When the stars align - and a light bulb goes off - that is usually my trigger to do something big. Regarding buying a primary residence - the lightbulb has not gone off (yet). But I remain open minded to the possibility.

-

I do my tactical trades primarily in my (and my wife's) RRSP and LIF accounts. There are no issues with the number of trades you do (not that I plan on doing lots of tactical things during the year - it will depend on what opportunities surface). I also hold most of my index funds (VOO and XIC) in these accounts. I keep my best ideas for my (and my wife's) TFSA and non-registered accounts - these are currently heavily weighted to Fairfax (and have been for the past 4 years). These accounts are for buy and hold type investments. ---------- From a tax planning perspective, I have also been trying to manage the significant tax liability building in our non-registered accounts (they are 100% Fairfax). Each year, for the past 3 years we have been selling a chunk of Fairfax in our non-registered accounts (typically when it hits an all time high). We have been able to repurchase the shares within a couple of months at the same or lower price. As a result, the number of shares we own in these accounts has generally stayed the same (to my surprise). And we do pay a modest amount of tax each year. But the tax liability today is much lower than it would have been if we have done nothing (it would be quite large today). I highly value the flexibility this gives us to use the funds in the non-registered accounts should we so decide (perhaps we decide to become a property owner again). I hate being in a straight-jacket (like having a massive tax liability on funds I might want to use one day). In 2024 I pulled a lot of $ from my LIF/RRSP's to pay any taxes owed. These accounts are getting way too big. So my focus in 2024 and moving forward is to draw these accounts down to fund our living and any tax payments (and let my non-registered accounts compound). The funning thing is despite my best efforts to draw them down the RRSP/LIF's keep getting bigger in size. A great problem to have. In Canada, we only pay tax on 50% of the capital gain. Despite the fact that she was a stay at home mom, my wife and I have most of our investment accounts split equally (started this process 25 years ago with spousal contributions to RRSP's). When we sold our house a few years ago, the proceeds were split equally into two non-registered accounts. Today, having the accounts balanced out over two people helps a lot when managing withdrawals / tax liability each year. ----------- My goal isn't to pay zero taxes. My goal is to have my assets compounding in the right vehicles (#1 = TFSA; #2 = non-registered; #3 = RRSP; #4 = LIF; #5 = RESP (as our kids are almost done university). Actually, our #3 priority today is to seed our 3 kids TFSA and FHSA investment accounts. I am pulling $ from my RRSP/LIF to do this (and yes, paying the tax bill). Estate planning - but 30 years earlier than most people likely do it. Getting a significant amount of $ transferred into these accounts when out kids are still under 25 years old seems like such a no-brainer thing to do. This pretty much guarantees they will be able to retire in their 50's, if not sooner (not that they understand that right now ). One of my big learnings in 2024 was you can have too much in RRSP/LIF accounts. Once they hit a certain size they can become the tail that wags the dog. Not good, especially later in life (+70). (Now having too much money in RRSP/LIF accounts is the problem we are all trying to create when we are younger... so, please, don't shed any tears for me an my newfound problem Another goal is to have our assets split equally between my wife and me. And to also have them weighted towards TFSA, non-registered accounts, with the remainder in RRSP/LIF's. Each year I try and make one or two 'tweaks' with how we withdraw/manage our tax situation. This simple approach has worked out very well over the years - and helped keep our supertanker (financial situation) generally pointed and moving in the right direction.

-

Exited two of my short-term tactical trades: CFP.TO (today) and Fairfax India (last week). Average gain was about 6%. Held in tax-free accounts. Holding period was 2 or 3 weeks. Happy to start rebuilding a modest cash weighting.

-

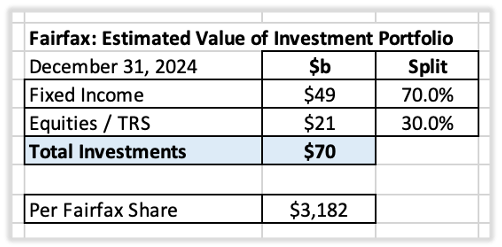

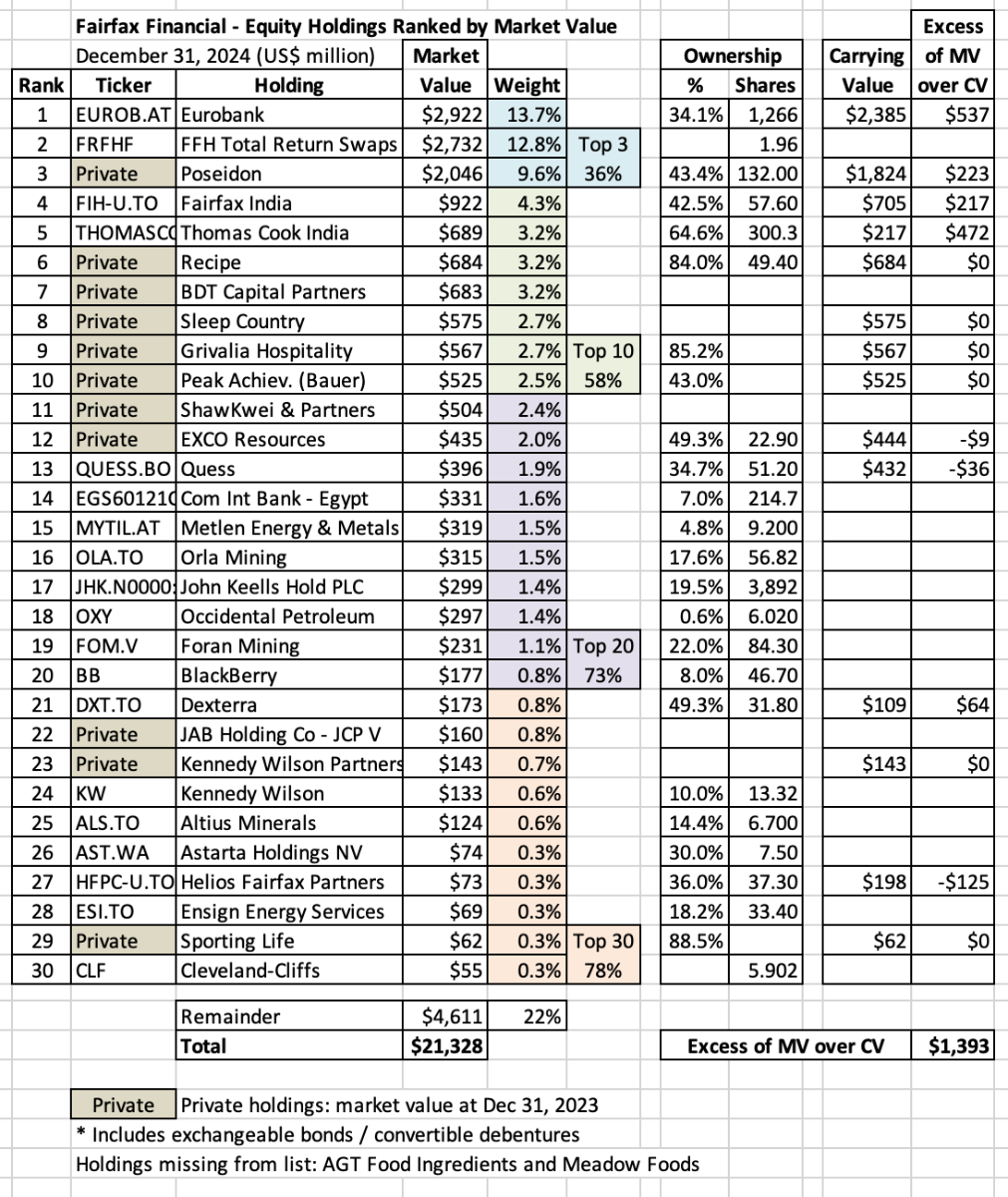

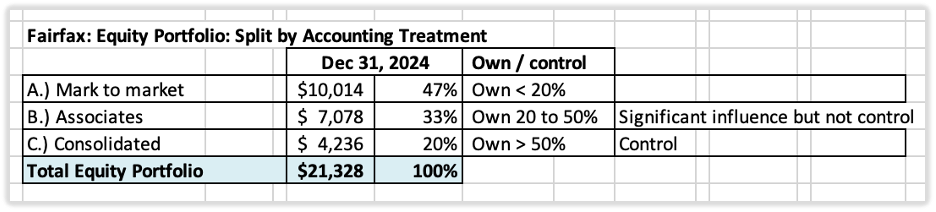

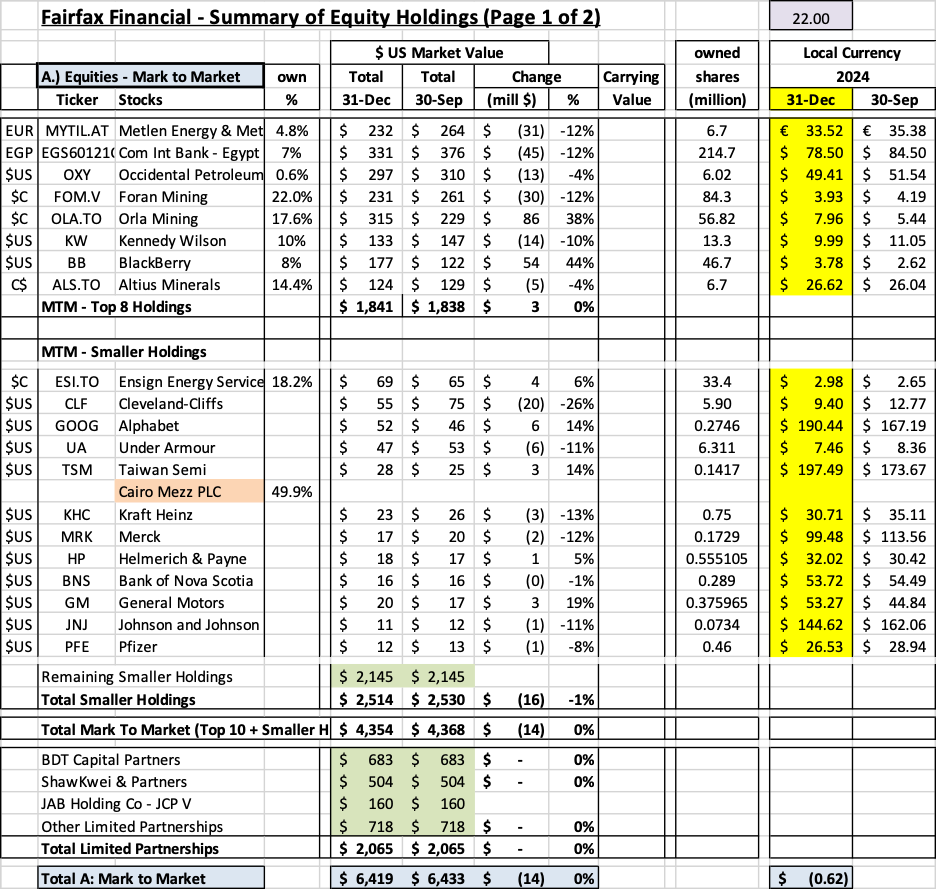

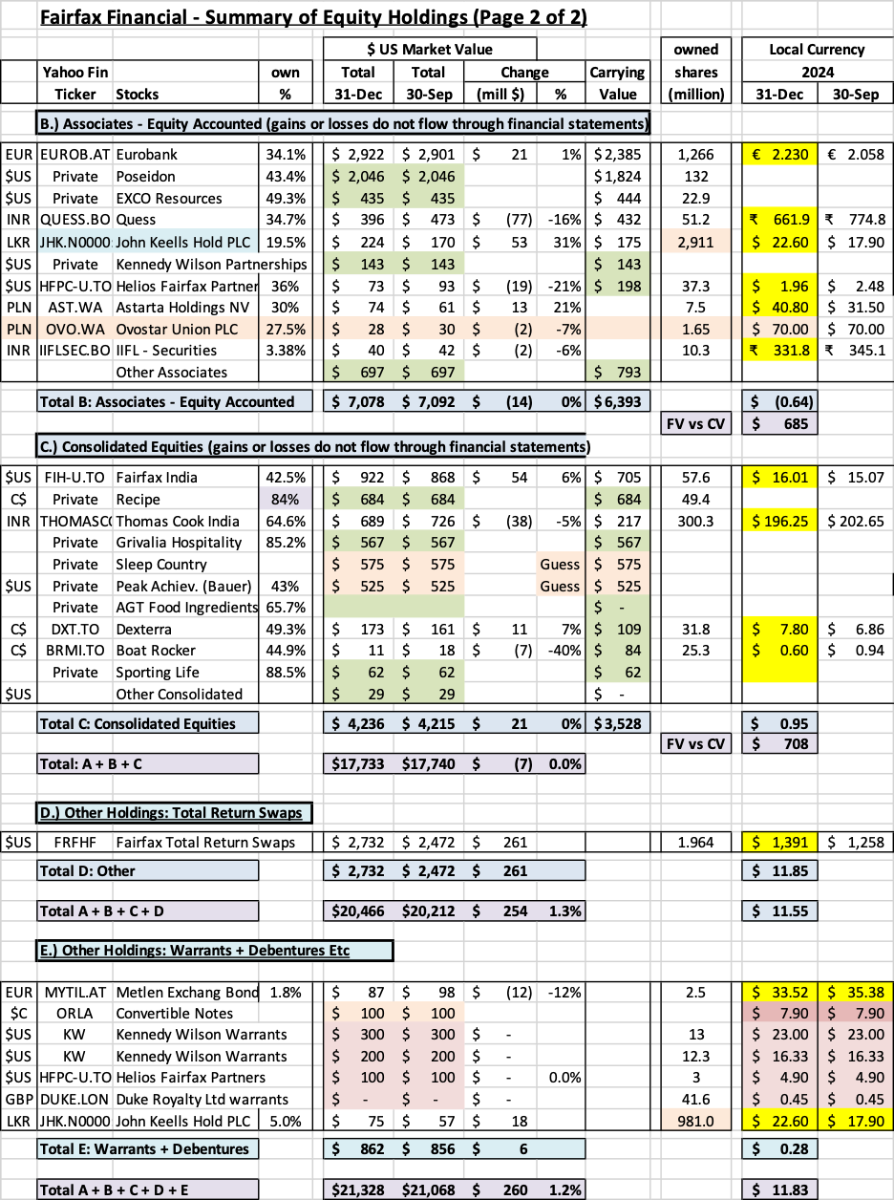

Equity Holdings – Size Ranking at December 31, 2024 Fairfax has a total investment portfolio of about $70 billion. Fixed income is about 70% of the portfolio and equities are about 30%. Fairfax is currently generating a total return of about 7.5% to 8% on its total investment portfolio. That is much better than P/C insurance peers who choose to invest primarily in fixed income. Of interest, Fairfax’s fixed income portfolio is positioned much more conservatively than peers - it is invested primarily in treasuries/government bonds. The significant outperformance of Fairfax’s investment portfolio versus peers is driven in large part by its equity portfolio (although Brian Bradstreet and the fixed income team at Fairfax might not totally agree with this). Over the past 7 years, Fairfax’s equity portfolio has experienced a dramatic transformation. What happened? Poorly performing holdings were dealt with - fixed, restructured, sold, taken private, merged or wound down. New money was invested wisely. Fairfax’s equity holdings today are: Very well managed. Profitable. Have solid balance sheets. As a result, the ‘quality’ of Fairfax’s collection of equity holdings has never been higher (in terms of management, fundamentals and prospects). And we are seeing this quality now shine through in terms of the performance and the increase in the value of these holdings. As a result, the return Fairfax is earnings from its investment portfolio has popped higher. The holdings are well positioned. This bodes well for future returns. ————— In this post we provide a list of Fairfax’s 30 largest equity holdings. To value a holding, we normally use current market value, which is the stock price at December 31, 2024, multiplied by the number of shares that Fairfax owns. For private holdings we use Fairfax’s latest reported market/carrying value, which was September 30, 2024. The FFH-TRS position is included at its notional value. Additional notes: Mytilineos *: includes exchangeable bonds John Keells *: includes convertible debentures Sleep Country - this purchase closed in Q4, 2024. My carrying/market value of $575 million is a guess. Peak Achievements - Fairfax doubled its position in Q4, 2024. My carrying/market value of $525 million is a guess. The carrying/market values of both Sleep Country and Peak will be updated when we get actual numbers from Fairfax when they report year-end results. What holdings are missing from my list below? Private holdings, AGT Food Ingredients and Meadow Foods, are two that come to mind. Ok, let’s get to the fun part of this post. What can we learn from looking at a list of Fairfax’s largest equity holdings? 1.) Fairfax has a pretty concentrated portfolio The top 3 holdings make up 36% of the total. The top 10 holdings make up 58% of the total. 2.) Mr. Market probably dislikes (hates?) lots of the stocks that are on this list A Greek bank? What is a P/C insurance company doing buying a total return swap on its own shares? A container shipping company? Significant investments in an emerging market like India? Greece? Significant investments in resource / commodity producers? I could go on. But here is the key point. Ask Mr. Market (the detractors) if they actually follow any of Fairfax’s 10 largest holdings. My guess is they don’t. I love it when people have strong opinions about something they know nothing about. That Greek bank has increased in market value by $650 million in 2024 and $2 billion over the past 4 years. That TRS has increased in market value by $900 million in 2024 and $2 billion over the past 4 years. That shipping container company just completed a massive new-built expansion program - cost to build today has shot up 30% (from what they recently paid). Through Fairfax India, they now own 69% of Bangalore International Airport (BIAL) the 3rd largest and fastest growing airport in India. One of their commodity holdings, Stelco, was sold in Q4. Over its 6 year holding period, this investment delivered a total return of $568 million (CAGR of 25.5%). Bottom line, Fairfax’s equity holdings have been performing exceptionally well in recent years. 3.) Fairfax is not Berkshire Hathaway Over the past 58 years, Warren Buffett / Berkshire Hathaway has been the GOAT. As a result, all P/C insurance companies today are evaluated by how much they clone Warren Buffett. Of course, there will only ever be one Warren Buffett - and he can’t be cloned (no matter how hard Tom Gaynor at Markel might try). Here is the really interesting point. Warren Buffett/Berkshire Hathaway is not the only person/company to build great wealth by exploiting the P/C insurance business model. I know this might sound like heresy to all of those investors who worship at the alter of Warren Buffett. Here are a few other individuals/companies that have built great wealth for themselves and their shareholders over decades (my list is not comprehensive… there are more): Shelby Davis Peter B Lewis / Progressive Hank Greenberg / AIG Tisch family / Lowes Bill Berkley / WR Berkley Markel family / Markel Prem Watsa / Fairfax Financial The important point is they all did it in very different ways - there is no one/right way. Buffett has been so successful for so many years that today lots of investors now think Buffett’s methods are the only way - his methods have become the accepted orthodoxy. And companies like Fairfax are evaluated and measured primarily by how much they emulate Warren Buffett’s style and approach - they are not measured and evaluated primarily on their own merits (management, fundamentals, results and prospects). Using Warren Buffett / Berkshire Hathaway today as the filter to screen/evaluate all other P/C insurance companies (especially those who invest in equities) is stupid. But it sounds smart. So it will likely continue. As a result, lots of investors are missing out on investing in other wonderful opportunities in P/C insurance. So if you look at Fairfax’s top equity holdings and you hear yourself saying ‘Warren Buffett wouldn’t do that’… well, good luck with that type of ‘analysis’. Of course, bad analysis by Mr. Market creates enormous opportunity for those able to think for themselves - and that is what we have seen play out at Fairfax and its share price over the past 4 years. 4.) Shift to private/associate holdings A seismic change has been happening with the composition of Fairfax’s equity holdings over the past 7 or 8 years. There has been a massive shift from publicly traded stocks to private/associate holdings. Today almost all of Fairfax’s largest equity holdings fall into the private bucket. And those that don’t fall into the associate bucket (which means Fairfax exerts significant influence). This shift at Fairfax reflects what has also been happening in financial markets in general in recent years - more and more capital is shifting from public to private markets, especially with large institutional investors. This is trend looks like it is just getting started. Today, Fairfax is generating an enormous amount of earnings. As the hard market in insurance slows, more of its excess cash will be allocated to equities. Many of the recent equity investments have been private: 2022: Purchase/take private of Recipe and significantly increase stake in Grivalia Hospitality. 2023: Purchase of Meadow Foods. 2024: Purchase/take private of Sleep Country and significantly increase stake in Peak Achievements. Fairfax is now of a size (earnings) where it has the ability to buy entire companies. The shift to private/associate holdings will have important implications for investors in how it impacts reported results (the income statement and balance sheet). Another meaningful income stream is being created: ‘Non-insurance consolidated holdings’ income stream will be spiking higher in the coming years. Less volatility in another income stream: As ‘mark to market’ equity holdings shrink in size as a percent of the total equity portfolio, we should see less volatility in the ‘unrealized investment gains (losses)’ income stream. In the coming years, the reported results of ‘new Fairfax’ will be much less volatile than what was experienced with ‘old Fairfax’. Will the shift to private/associate holdings create a Berkshire Hathaway type of problem for Fairfax? Will book value become a poor tool to use to value Fairfax? For Fairfax’s ‘consolidated’ and ‘associate’ equity holdings, over time, it is likely the increase in economic value will exceed the increase in accounting value. We can already see this happening. One example is at September 30, 2024, the excess of fair value over carrying value for consolidated and associate equity holdings was $1.9 billion. This will be something for investors to monitor and factor into their assessment of performance/valuation of the company in the coming years. 5.) Fairfax has fixed its ‘problem’ equity holdings from pre-2018 Back in 2018, Fairfax’s equity portfolio was littered with underperforming equity holdings. But around that time its like the senior team at Fairfax decided enough was enough. It looks to me like they ‘tweaked’ their investment framework and put more of a premium on: Partnering with strong management teams. Profitability. Financial strength. This new framework helped with new equity purchases. But what to do with poorly performing ‘legacy’ holdings? Fairfax rolled up their sleeves and got to work: AGT Food and Ingredients was taken private. APR Energy was sold to Atlas (for shares). Fairfax Africa was placed into runoff / merged with Helios. Resolute Forest Products was sold (at the peak of the lumber market). Farmers Edge went bankrupt. Blackberry debentures were exited. It took 7 years, but Fairfax has largely ‘fixed’ all of its poorly performing legacy equity holdings. These holdings were a significant and recurring drain of financial and management resources - they were a steady ‘use of cash’ of +$200 million per year for many years (cash infusions, write downs etc). It is like a $200 million annual expense has been eliminated. Fixing legacy holdings carries a double benefit for Fairfax: It removes a large annual expense. It has shifted a significant amount of capital to better performing companies/opportunities that are now delivering solid results/earnings - which are beginning to compound in value. Every equity portfolio will have a few poor performers. Fairfax’s problem back in 2018 was they had too many poorly performing holdings and they were large in size (many were top 10 holdings). 6.) The overall quality of Fairfax’s collection of equity holdings has never been better With regard to its large equity portfolio, the team at Fairfax and Hamblin Watsa has been on a 7 year journey of continuous improvement. As we reviewed in point 5.) above, legacy problem children were dealt with. And new purchases have been performing exceptionally well: Fairfax total return swap Stelco (sold this year, locking in an exceptional return) Seaspan/Altas/Poseidon BIAL Some of Fairfax’s equity holdings were also helped by external factors. Eurobank - election of pro-business government and return of strong economic growth in Greece. Fairfax India, Thomas Cook India and Quess - election of pro-business government and strong economic growth in India As a result, today, the quality of Fairfax’s collection of equity holdings has never been/looked better, in terms of: Management Fundamentals Profitability/earnings power Prospects This is doubly important, because the size of Fairfax’s equity portfolio at $21 billion - has never been bigger. Fairfax is delivering exceptional performance at the perfect time. It looks like the team at Fairfax / Hamblin Watsa / Fairbridge has the right investment framework in place and they are executing against it very well. Summary For the past 7 years, the overall quality of Fairfax’s collection of equity holdings has been slowly and steadily improving. The impact on earnings lagged initially. But after years of effort, the improvements made are now showing up in earnings. Importantly, Fairfax’s equity portfolio looks very well positioned to continue its strong performance in the coming years. This is a wonderful set-up for Fairfax shareholders.

-

On the Q3 conference call, Wade Burton said the average maturity was 3.7 years. And Peter Clarke said the average duration was 3.5 years. Wade Burton Thank you Peter, and good morning everyone. The investment results in the quarter were strong with interest and dividend income of $610 million, profits of associates of $260 million, and net gains on investments of $1.3 billion. With that said, there was not a lot of activity in the quarter on the investment side. Fairfax total investment portfolio now stands at $69 billion to end the quarter, with $49 million in fixed income and $20 billion in equities. Of the $49 billion in fixed income, $35 billion are in U.S. treasuries, other government bonds and cash. There is another $5 billion in mortgages and $9 billion in short dated investment-grade corporates. Including cash, average maturity is 3.7 years and the yield is 4.7%. With inflation steadying at or around the Fed’s target, the Fed cut rates 50 basis points in September with an eye to getting to a neutral stance. So many variables, including a very close U.S. election with widely differing policies between the two candidates, we are studying it all and watching it closely. For now, we continue to have a defensively positioned fixed income portfolio while still making very healthy, very robust interest income. For the $20 billion in equities, not much changed. Our core holdings and investments continued to perform well, all making good income against invested capital. Our experienced investment team is constantly searching for new opportunities, but as managers of insurance float, we have the very great benefit of taking a long term approach to investing. It means we can wait for prices to come to us, and we won’t invest unless we see a margin of safety. We did make one significant announcement in the quarter. We bought out our main partners in Peak Achievement, an athletic wear and equipment company focused on hockey and lacrosse. It is an outstanding business operating in a highly consolidated industry, well run by Ed Kinnaly and his team, incredible track record, and we paid a fair price. We think we will make a very good return over the long run for our shareholders, and importantly, Ed runs the company very much in tune with the Fairfax culture. Looking back over the last two years, we’ve made three significant long term equity investments, one in Meadow Dairy, a dominant milk ingredients company in the U.K. that is doing very well; another in Sleep Country, a dominant mattress distributor and retailer in Canada; and now a third, Peak, a dominant sporting goods company focused on hockey and lacrosse. All immediately are or will contribute to our earnings, and we believe all will continue to contribute more and more as their businesses progress. I will now pass it to Jen Allen, our CFO. ————— During the Q&A portion of the conference call. Jaeme Gloyne Yes, thanks. Since we’re on round two, maybe I can sneak a couple in here. First one is just around the duration of the fixed income portfolio - I don’t think it was disclosed in the results or the report. If you could just give us an update on how that duration sits and compared to the liabilities. Maybe thinking about the strategy here around fixed income, is it a little bit of wait and see on the election, or do you have some strategies, maybe you’re thinking about deploying more capital into longer dated maturities, shifting more into corporate bonds. Maybe you can sort of talk through how you’re thinking about the world on fixed income. Peter Clarke Sure. The duration on our bond liabilities are around 3.5 years, so it’s a little longer than it was last quarter, and if you look at our liabilities, it’s relatively close. We don’t match on purpose, but where we sit today, our liability duration is close to our asset duration. You can sort of see that in the IFRS 17 numbers, that we had a big loss on the discounting, about $750 million, $760 million that was offset almost--very closely with the $800 million-plus of gains on our bond portfolio, so we’re pretty much matched where we are today. As far as going forward, I think all that we could say on that is we’re very happy that the fixed income portfolio is very liquid and with a duration of 3.5 years. It gives us lots of flexibility for opportunities in the future. We don’t have any significant exposure on the corporate side - our corporate bonds are one to two years, very short dated, so that is an opportunity if credit spreads should widen in the future. Next question?

-

59 years old. Been on this board since around 2003. It has been like getting sprinkled with pixie dust...

-

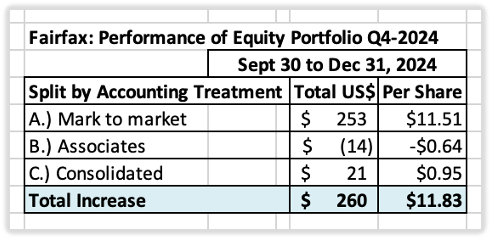

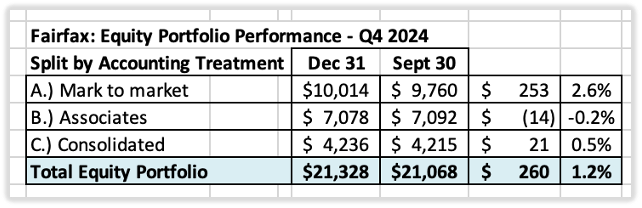

Estimate of change in value of Fairfax’s equity portfolio in Q4 - 2024 Fairfax’s equity portfolio (that I track) increased in value in Q4 2024 by about $260 million (pre-tax). It had a total value of about $21.3 billion at December 31, 2024. In Q4, currency (US$ strength) was a big headwind. How much of a headwind? About $340 million. If we ignore the change in exchange rates, Fairfax's equity portfolio would have been up $600 million in Q4. Notes: The FFH-TRS position is included in the mark to market bucket and at its notional value. The warrants and debentures captured are also included in the mark to market bucket. The ‘tracker portfolio’ is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). The ‘tracker portfolio’ does not include the following: Change in value of Digit, Fairfax's publicly traded P/C insurance company in India. Gain on sale of Stelco. Any gain on the revaluation of Fairfax’s legacy stake in Peak Achievement. Split of holdings by accounting treatment About 47% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 53% are Associates and Consolidated holdings. The Sleep Country and Peak Achievement (Bauer) acquisitions closed in Q4. We have included a guess of the carrying value for these two holdings – it will be updated when Fairfax reports Q4 results. Over the past couple of years, the share of the mark to market holdings has been shrinking. This means Fairfax's quarterly reported results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of about $260 million = $12/share (pre-tax) The mark to market change is an increase of about $253 million = $11.50/share. What were the big movers in the equity portfolio Q1-YTD? The FFH-TRS is up $261 million and is Fairfax’s second largest holding at $2.7 billion. Orla Mining – a gold miner – is up $86 million. Quess is down $77 million. It is still up solidly on the year. Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1.4 billion pre-tax ($63/share). The 'excess of FV to CV’ has been materially increasing in recent years. This is a good example of how book value at Fairfax is understated. Excess of FV over CV: Associates: $685 million Consolidated: $708 million Equity Tracker Spreadsheet explained: We have separated holdings by accounting treatment: Mark to market Associates – equity accounted Consolidated Other Holdings – total return swaps and warrants/debentures The value of each holding is calculated by multiplying the share price by the number of shares. All holdings are tracked in US$, so non-US holdings have their values adjusted for currency. I have attempted to estimate the new carrying value for Sleep Country and Peak Achievements (both transaction closed in Q4). These numbers are a guess - so they will be wrong. But hopefully, directionally, they are close. Given their size, I just wanted to get them on the spreadsheet. When Fairfax reports YE results we will get the right numbers. This spreadsheet contains errors. It is updated as new and better information becomes available.

-

@Red Lion, well said. Your post is full of juicy stuff. I agree with much of it. Like Druckenmiller says “be inquisitive and be open minded”. Psychology is a bigger problem than brains for most investors. My favourite part of what you had to say: ”The selling part is the hard part, and I've certainly left a lot of gains on the table by poor selling discipline or selling too soon. I've significantly improved my returns though by trying to feed the winners and weed the losers. I think very good long term returns will require adding to winners and holding.”

-

Ok. I have been know to use a little hyperbole on this board from time to time… but do we really think Prem has now re-ascended to ‘God-like’ status? That comment got a very loud laugh from me. Thank you! (I don’t think we are quite there... yet. Although I remain open minded ).

-

+1 (bitcoin is in my ‘too hard’ pile.)

-

@SafetyinNumbers, I appreciate the comment (like those from others). The board has many great posters - like you - who add a lot of value when it comes to Fairfax. All board members benefit greatly from the information and different perspectives provided by everyone. The mid-point of my estimate = 17.5%, would result in a double in Fairfax’s stock price in a little more than 4 years. i will be very happy if this is what actually happens. Of interest, 33% of my/my wife’s portfolio is in Fairfax today (we have enough; and for us, given our ages, return of capital is now more important than return on capital). On the other hand, 75% of my kids portfolios are in Fairfax. The weightings in my kids portfolios perhaps provides a better indicator of how I think Fairfax will perform in the coming years. Bottom line, I don’t disagree with anything you say. Although I do think we could see more volatility in the stock price moving forward. At least I hope so. This will give Fairfax the opportunity to continue to be very aggressive on these are buyback front. Volatility in financial markets is Fairfax’s secret weapon. Especially now that they are all cashed up. You said: ‘… I think most would agree a market disclocation is likely over the next four years.’ This will likely be one of the keys to future ROE. The interesting thing is most investors will want to see it before they will believe/invest in it. That was the big mistake that I made with Berkshire Hathaway in the 1990’s and early 2000’s - I was waiting to see what Buffett actually did before I invested. Of course, by the time I saw it, everyone else saw it - and the stock traded higher. As a result, I was always one step behind. I was like a dog chasing its tail. My ignorance caused me to largely miss out on a wonderful multi-decade compounder. Fairfax has a proven best-in-class management team when it comes to capital allocation. Do we know exactly what they are going to do in the coming years? Nope. But like Berkshire Hathaway when it was in its prime, we don't need to know. And that is what makes Fairfax such a good investment today (especially at its current - cheap - valuation). It is very counter-intuitive.

-

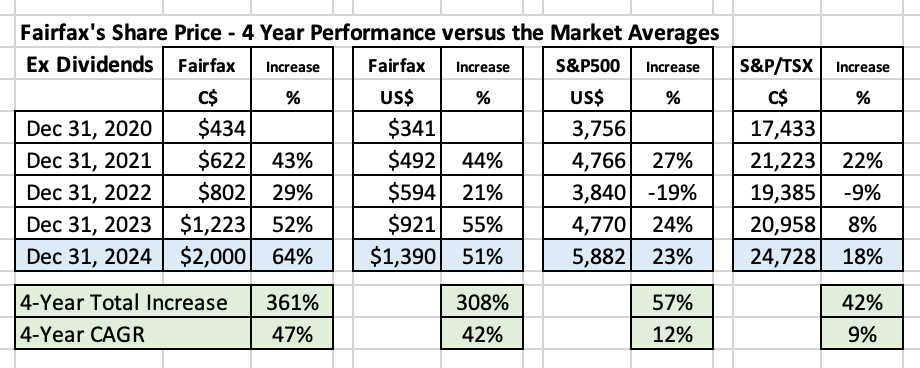

As we begin 2025, I think it is appropriate to first close the book on 2024. This is also the perfect time to reflect and be thankful. Fairfax just delivered another exceptional year - its stock increased 51% (US$) in 2024. Over the past 4 years the stock is up 308%, which is a CAGR of 42%. (Not including dividends.) Simply outstanding! Over the same 4-year timeframe, the S&P500 has increased a total of 57%, which is a CAGR of 12%. (Also not including dividends.) In C$ terms, Fairfax's results have been even better - the 4-year total return has been 361%, which is a CAGR of 46%. Over the same time frame, the S&P/TSX index had a total return of 42%, or a CAGR of 9%. Fairfax has also been an excellent hedge for a weak C$, which is very important for Canadian investors (like me ). Thank you to the entire team at FFH. Head office. The insurance subs. Hamblin Watsa. This group likely went through hell from 2010 to 2020. Fairfax's amazing performance the past 4 years is due to their efforts. Nice to see them having some success - they deserve it. All investors owe them all a big debt of gratitude. And thank you to all the posters on this wonderful forum - you are a 1st class group of investors. The opportunity to write / discuss / debate with other smart and genuinely nice people has been an absolute privilege. @Parsad, thank you for creating this wonderful forum more than 20 years ago - and managing it since then. Over the past 4 years, Fairfax has been on a truly epic run. I hope many people on this board (and in the company) have been able to capitalize and benefit from this run - and materially improve their financial / life situation in the process. What has been happening with Fairfax over the past 4 years is not normal. It is an anomaly. And for the past 4 years everyone on this board has had a front row seat to watch / write / debate the events as they have happened / in real time. Years from now, we are all going to look back and better appreciate how truly special these times are / have been. Does this mean we are done? Has the 'easy money' been made? No. I think in some respects Fairfax is just getting started. It currently looks to me like a much younger Berkshire Hathaway (small, P/C insurance remains the primary growth engine, generating sizeable earnings, best-in-class capital allocators). And the stock is still cheap (on a P/BV and PE basis), especially when we include excess of FV over CV for associate and consolidated holdings. I don't expect Fairfax to continue to compound at +40% per year. But I do think Fairfax can compound over the next 3 to 5 years at a CAGR of 15% to 20% per year. Earnings will drive most of the return. I think we will continue to get multiple expansion. And I think Fairfax will continue to be aggressive with share buybacks. Fairfax's insurance and investment management businesses have never been better positioned than they are today. The set-up for the company for 2025 looks outstanding. With others on this board, I look forward to having court side seats.

-

2024 was another very good year, +40.8%. What were the drivers? Fairfax - large core position and also taking advantage of two sell offs (tactical trades in Feb and Aug) Yes, Fairfax has delivered another amazing year. Nuts. Broad based index funds (VOO, VO and XIC) My decision to shift a significant portion of my net worth to index funds in Q4 2023 certainly paid off in 2024 given how strong financial markets were. Tactical trades These worked out pretty well - not surprising given how strong financial markets were... 'a rising tide lifts all boats...' At year end, here is where my portfolio sits: Fairfax = 33% Broad based index funds = 46% (mostly VOO, XIC with small amounts of VO, XEQT) Tactical trades = 20% (Fairfax India, Telus, Canfor, Saputo, Suncor) Most of my tactical stuff was bought very late in the year. Fairfax India briefly went to $15 and I got a few shares (not as much as I wanted). Telus and Saputo look like they got hit hard with tax loss selling. Canfor got hit over concerns over high mortgage rates in the US. And Suncor got hit, along with all the oil companies - oil/gas is a pretty hated sector. Cash = 1% I normally like to have a cash weighting of 15% to 20%. So I will be looking to bump this up in the new year (selling down my tactical holdings - which are all in tax-free accounts).

-

@yesman182, I have family coming over tonight for dinner... but to get you started, here is what Buffett had to say: “With the acquisition of General Re — and with GEICO’s business mushrooming — it becomes more important than ever that you understand how to evaluate an insurance company. The key determinants are: 1.) the amount of float that the business generates; 2.) its cost; and 3.) most important of all, the long-term outlook for both of these factors.” Warren Buffett – Berkshire Hathaway 1998AR The key is versus expectations. My view is Mr. Market views Fairfax's insurance business as low to average (at best) quality. You can also read Chapter 4 - Float Fairfax Financial Volume 2 - Dec 2 2024.pdf

-

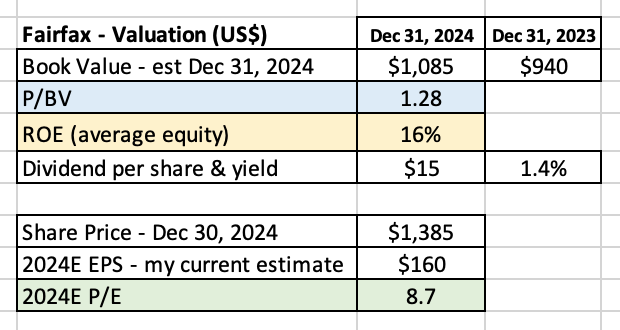

What makes Fairfax such an interesting investment over the past 4 years is it keeps changing right before our eyes. 1.) Back in 2020 it was a turnaround - the company had stumbled badly (putting it lightly) from 2010 to 2020 with the investment management side of the business. By the end of 2022, it was clear the turnaround had been successfully executed. - The equity hedge position had been exited in late 2016. - The last of the short positions had been exited in late 2020. - It was becoming increasingly clear their equity framework had been 'tweaked' around 2018 and the equity portfolio (taken as a whole) was slowly moving up the quality curve (in terms of management, business results and prospects). 2.) By early 2023, Fairfax had become a value play. Not a particularly well run company (that was the perception of most investors). But statistically very cheap (trading at 1 x book value). 3.) Today? - How good is its insurance business? - How good is its investment management business? - How good is its management team? What kind of company is Fairfax? To value Fairfax today, an investor has to get this right. Do investors have it right today? No, I don't think they do. They continue to underestimate the quality of the company. As a result, I continue to think Fairfax is undervalued. Fairfax is trading today at a P/BV = 1.3 and a PE of 8.7 (using my YE estimate for BV and EPS). That is cheap for an average company. If we include 'excess of FV over CV' for associate and consolidated equity holdings, Fairfax is trading today at a P/BV = 1.2 and a PE of about 8. That is wicked cheap for a high quality company. How much are they undervalued? That is, literally, the million dollar question. Of course, we will only get our answer with the passage of time. What has made Fairfax such as difficult investment for many investors over the past 4 years is it keeps changing right in front of our eyes. Being open minded and focussed on the facts and the improving fundamental has been critical. As 'the story' changed, the valuation model also needed to change. Just like today.

-

@TwoCitiesCapital , i appreciate the opportunity to discuss/debate. At the end of the day, we all have our own frameworks to understand/process the decisions that Fairfax has made in the past, what the results were and what it means for the company today and in the future. As a result, we are sometimes going to see things differently. And that is not a bad thing.

-

@TwoCitiesCapital , my view on this topic has evolved over the years. One of the keys with investing is the following: "It's not whether you're right or wrong that's important, but how much money you make when you're right and how much you lose when you're wrong," Druckenmiller told author Jack Schwager about what he learned from Soros. - https://markets.businessinsider.com/news/stocks/stanley-druckenmiller-13-most-brilliant-quotes-from-2019-2-1027989932#its-not-whether-youre-right-or-wrong-thats-important-but-how-much-money-you-make-when-youre-right-and-how-much-you-lose-when-youre-wrong-13 Fairfax made two big changes to their investment portfolio in late 2016 (after Trump was elected for the first time): 1.) They exited their equity hedges. 2.) They shortened the average duration of their bond portfolio - thinking inflation might be coming in the future. Let's look at the second decision, shortening the average duration of the fixed income portfolio. Yes, Fairfax's average yield was low. For the 5 years from 2017 to 2021, Fairfax's average yield was 2.4%. Let's assume this very defensive stance 'cost' Fairfax investors an average of 1% per year. This 'cost' was about $1.5 billion from 2016 to 2021 ($147.6 billion x 1%). From 2016 to 2021, Fairfax was active buying and selling its fixed income portfolio. In 2021, the realized more than $200 million in gains (when they sold all their corporate bonds at a 1% yield). So the total 'cost' to Fairfax was not $1.5 billion. When we include bond gains from 2016 to 2021 it was much less than this. Now we need to calculate how much Fairfax 'made' when interest rates turned in 2022. My guess is the average duration of the fixed income portfolio: 1.) Likely saved the company $2 to $3 billion in losses on their bond portfolio alone (this estimate might be low). 2.) Allowed extremely rapid earn through to interest income of much higher interest rates. How much of a benefit? I don't think an incremental $1 billion is a crazy number to use. 3.) Their positioning also allowed them to be extremely aggressive growing their insurance business in the hard market during 2022 (Fairfax had 25% growth that year). Value of this? A big number. Bottom line, I think when you actually run the numbers and include all the puts and takes, the decision to go short duration on the fixed income portfolio was a very good decision for Fairfax shareholders - even when calculated beginning in 2017. It was a small drag on earnings from 2017 to 2021. And then it worked out spectacularly well for Fairfax in 2022, 2023, 2024 and future years. What Fairfax did was value investing 101. Back in late 2016, Fairfax correctly surmised that investors were not being properly compensated for taking duration. With hindsight, they were right. They sized their investment appropriately. And as a result, they made Fairfax shareholders a lot of money.

-

@SafetyinNumbers , thanks for taking the time to explain the difference in GAAP and IFRS reporting, and how it is used by analysts. Very insightful

-

What people are dancing around is the following: Is it possible to learn from your mistakes as an investor? Yes? Or no? Let’s ask a really mind bender of a question: Can making mistakes make you a better investor? I think the best way to think about the equity hedge fiasco (2010 to 2016) is simply as a bad decision. Yes, the losses lasted for 7 straight years. And they were massive in size. But when the decision was reversed in late 2016, the losses stopped. The same could be said about the short positions that were held from 2010 to 2020. Lots of losses. But when the last short positions was exited in late 2020, the losses stopped. The same could be said about Fairfax’s poor equity decisions/holdings pre-2018. My read is Fairfax changed their investing framework around 2018. Partnering with strong management teams became more important. As did being in strong condition financially. And being profitable. The new equity purchases made beginning in 2018 to today have performed exceptionally well. And they were massive legacy equity holdings have all largely been fixed. It is a double whammy (in a good way). Back to our original questions: 1.) Did Fairfax learn from their 3 mistakes? Yes, i think they have. That is important, because it means they are unlikely to repeat them. 2.) Is Fairfax a better company today because of the 3 mistakes made? Yes, I think it is. That is important, because it gives us insight into the quality of the company and the senior team in place today - it has improved markedly. Why do I think this? Learning the lesson - past is prologue The best analog is when Fairfax last experienced great adversity - back in 2003 to 2005. The adversity was driven, in part, by losses in its shitty P/C insurance operations. Fairfax got through that trying time. And proceeded to learn the right lesson - stop buying low quality/under-reserved/statistically cheap P/C insurance companies often trading at big discounts to book value. And that is what happened. Even though most investors still don’t fully recognize that this happened many years ago. Both P/C insurance and investment management businesses have experienced extreme adversity (at very different times in the company’s history). Both times Fairfax learned the right lessons. Today we have a company that is battle tested. It is more mature. It is like a star athlete just now entering its prime. Its most trying times are behind it. ————— Some investors are waiting for Fairfax to revert to its old ways again. This view assumes they have not learned the right lessons. They did not revert with insurance. I am optimistic they will not revert with investment management part of the business. Time will tell.

-

@TwoCitiesCapital , I think one of Fairfax’s core frameworks is value investing. This includes insurance, equities and fixed income/bonds. If you look at the big moves Fairfax has made over the past 4 years, they have nailed every one of their large investments/capital allocation decisions: 1.) Aggressively expand insurance business in hard market. 2.) Reducing the fixed income portfolio to 1.2 years in late 2021. Extending to 3.5 years in Q3, 2024. 3.) Establishing the total return swap on 1.96 million Fairfax shares in late 2020/early 2021). 4.) Dutch auction: buy back 2 million Fairfax shares at $500/share. 5.) Asset sales: pet insurance, Resolute Forest Products, Stelco. I could go on… They are on a hot streak. If they see opportunities in fixed income, I hope they keep swinging away.

-

@gfp, I agree. This will be something to watch when Fairfax reports Q4 results. Fairfax is getting a great opportunity to extend the duration of their bond portfolio. A year ago, everyone was expecting interest rates across the curve to drop significantly. A year ago, I think the number one concern of Fairfax investors was a sharp decline in interest and dividend income. ‘That sucker has got to come down - and probably by a lot!’ What actually happened in 2024? Fairfax delivered record interest and dividend income. And in Q3 they extended duration to around 3.5 years. And they now have the opportunity to push the average duration to over 4 years if they want. This locks in high interest and dividend income in for the next 4 years. This highlights the challenges of trying to guess (with a high degree of conviction) what might happen 3 or 4 years out. There are too many variables at play to be able to do it consistently well. I think the key is assessing the quality of the management team - and how good they are at capital allocation. Figuring out how good a management team is - this is far easier (and more effective/useful) than trying to figure out where the economy or interest rates will be looking out 3 or 4 years.

-

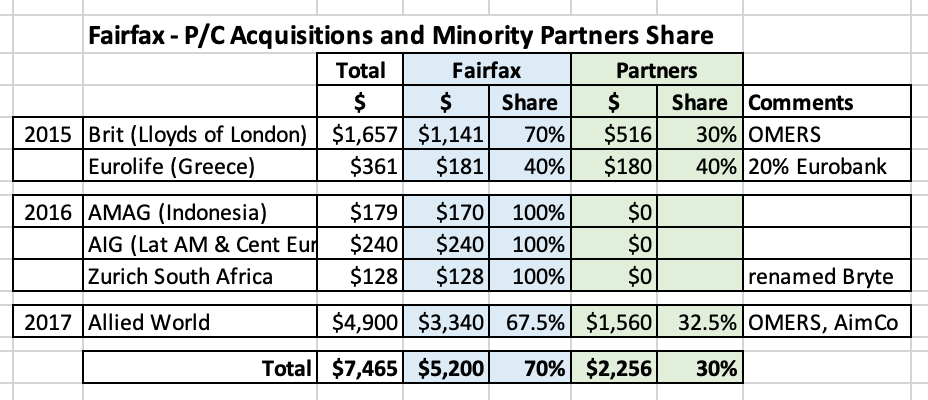

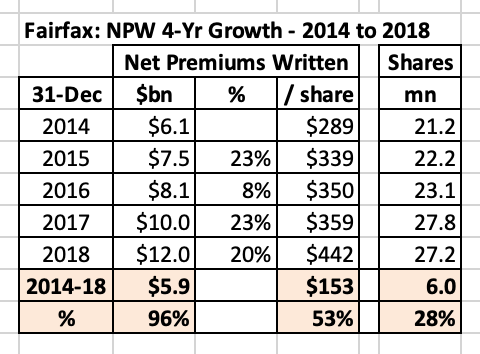

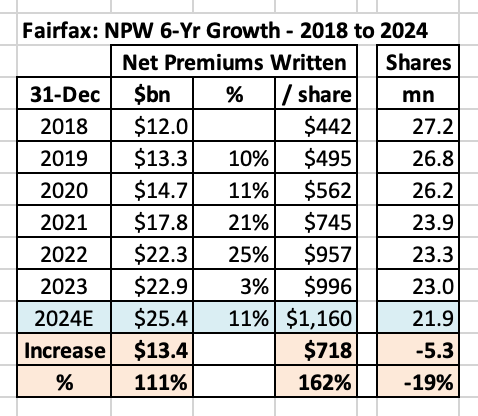

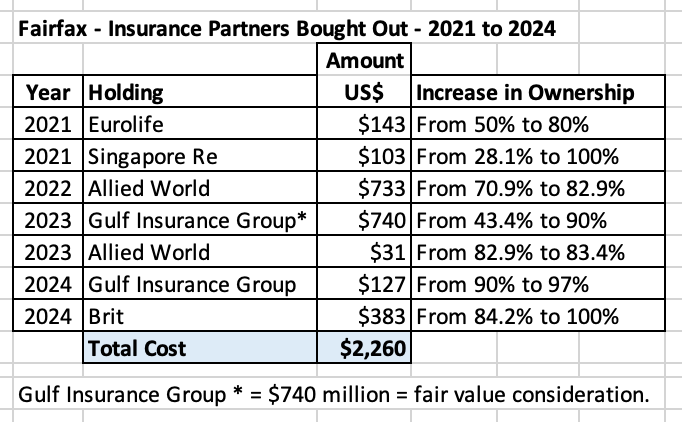

Is Fairfax a Growth Company? Part2 In Part 1, we looked at Fairfax’s insurance business and asked the following question: ‘Is Fairfax a growth company?’ Our answer, based on the growth of net premiums written over the past decade, was ‘yes.’ https://thecobf.com/forum/topic/20517-fairfax-2024/page/99/#findComment-592351 In Part 2, we will now dig into what happened at Fairfax over the past ten years to drive all that top-line growth in NPW. Part II: A short history of the growth of net premiums written (NPW) The 15.3% CAGR in NPW that Fairfax is poised to deliver from 2014-2024 has happened in two pretty distinct phases. Phase 1: Acquisitions – International expansion (2015-2017) Phase 2: Organic - Hard market (2019-2024) After we review these two phases, we will then look at what might be coming next, in phase three: Phase 3: Take-out of minority partners (2022-2026) As one would expect, there is some overlap with these phases. So, let’s get started and peel back the onion a little bit. What did Fairfax do? What was the cost? Was it good for shareholders? By digging a little deeper, we can learn more about Fairfax and how they do capital allocation looking through the lens of P/C insurance business. In turn, this will help us better understand and evaluate the performance of the management team. Phase 1: Growth via acquisitions – international expansion (2015 to 2017) Throughout their history, Fairfax has used acquisitions to help fuel its growth. Over a 3-year period, from 2015-2017, Fairfax made six different large P/C insurance acquisitions that cost a total of $7.5 billion. How did Fairfax pay for the acquisitions? At the time (2015 to 2017), Fairfax was short on cash as the investment side of the business was underperforming (losses from equity hedges/shorts and poorly performing legacy equity holdings… yes, sorry to keep picking that scab). To fund the acquisitions, Fairfax used the traditional funding sources: Equity: Raised $3.34 billion (7.2 million shares at $462/share). Debt: from 2015 to 2017, net debt increased $2.1 billion (the average interest rate on the new debt was about 4.55% and the average maturity was about 9 years). Asset sales have long been an underappreciated tool in Fairfax’s capital allocation tool box. From 2015 to 2017, Fairfax also raised significant cash with asset sales. Asset sales: $3.3 billion (Bank of Ireland, ICICI Lombard, First Capital, Ridley) The sale of First Capital deserves special mention. In 2017, Fairfax sold First Capital for $1.7 billion and booked a $1 billion gain after-tax. First Capital was sold for more than 3 x book value. In comparison, Allied World, Fairfax’s largest acquisition, was purchased for 1.3 x book value. Smart. And very accretive for Fairfax shareholders. But Fairfax wasn’t done with funding sources. They also got creative. They came up with a brand new way to source ‘other people’s money’. For the three larger purchases, Fairfax brought on minority partners - the big pension funds in Canada (OMERS and CPPIB). Minority partners: Raised $2.256 billion Minority partners funded 30% of the $7.5 billion total purchase price. How much did Fairfax grow from 2014 to 2018? In a soft P/C insurance market, NPW increased from $6.1 billion in 2014 to $12.0 billion in 2018, for total growth of $5.9 billion or 96% over 4 years. Yes, the share count did increase quite a bit during this time so growth per share in NPW was lower at 53% (more on this later). Capital allocation 101 Opportunistic: The timing of Fairfax’s acquisitions were close to perfect. Fairfax are a value investors. Not just when it comes to their investment portfolio. They look at their insurance businesses through the same lens. In 2015, they saw great value in buying other P/C insurance companies. Insurance was in a soft market. Well run companies were available at reasonable valuations. Conviction: Fairfax sized their bet appropriately - they backed up the truck. At December 31, 2014, common shareholders’ equity at Fairfax was $8.4 billion. Spending $7.5 billion on acquisitions over a three year period was an extremely aggressive move by the company. Creativity: Fairfax was very creative in how it raised the needed cash. At the time (2015-2017), Fairfax was short on cash (putting it politely). The investment management part of the company was severely underperforming. What to do? In addition to the usual actions (tap equity and debt markets) Fairfax also sold assets at premium valuations. And they brought on minority partners. The net result was Fairfax was able to double the size of their insurance business (net premiums written) in 4 short years from 2014 to 2018. Much of the growth was international. Fairfax now had a global P/C insurance platform. ————— Growth by acquisition can be good but it does carry risks. Did you overpay? Are there hidden issues such as poor reserving? Are there integration/culture issues? What is the best way for an insurance company to grow? The answer is a hard insurance market and that is what started in Q4 of 2019. Phase 2: Organic growth - hard insurance market (2019-2024) Hard markets for P/C insurers are very rare. The last one was in 2001-2004. So when they happen, you need to capitalize on them. Fairfax understood this and that is what they proceeded to do. What makes a hard market so good? The opportunity to charge higher premiums and to apply more stringent underwriting (more favourable terms and conditions on policies). For well-run insurers like Fairfax, a hard market is like getting a gift from the insurance gods. In late 2019, Fairfax was very well positioned to capitalize on the hard market. By then, the many large insurance acquisitions they had made from 2015 to 2017 had been fully integrated / digested. But to grow aggressively in a hard market an insurance company needs capital. Lots of it. So Fairfax from a capital allocation perspective, Fairfax prioritized supporting the growth of the insurance subs. How much did Fairfax grow over the 6-year period from 2018-2024? Net premiums written increased from $12.0 billion in 2018 to an estimated $25.4 billion in 2024, for total growth of 111% over six years. However, during this period the share count decreased by 19% so growth per share was much higher at 162%. That is rocket-ship-emoji type organic growth over a five year period. ————— We need to draw attention to two things Fairfax did in Phase 2: Organic Growth phase (2018-2024). Because they had a material impact on the insurance business. 1.) Fixed income - Side-stepping the historic bear market in bonds 2022 saw the greatest bear market in history in bonds. Most P/C insurers hold the vast majority of their investment portfolio in bonds. As a result of the spike in interest rates in 2022, the value of their bond portfolios got mauled. Book value for many P/C insurance companies fell by 20% to 30%. This had two effects: It lit a fire under the hard market in insurance (the losses on the investment side of the business put even more pressure to make money on the insurance side). It constrained their ability to capitalize on the hard market and grow their insurance business (the drop in book value lowered capital levels). What about Fairfax? In late 2021, Fairfax shifted the average duration of their fixed income portfolio to 1.2 years. Fairfax are value investors. In late 2021 they correctly surmised there was no margin of safety in owning duration in the bond portfolio. (Not surprisingly, Warren Buffett reached the same conclusion). As a result, in 2022, Fairfax largely avoided the historic bear market in bonds. This saved Fairfax shareholders billion in losses. As a result, Fairfax was one of the very few P/C insurance companies that actually reported an increase in book value in 2022. This allowed Fairfax to fully capitalize on the hard market - they grew NPW by a staggering 25% in 2022. (Fairfax since extended the average duration of its bond portfolio to about 3.5 years - it is now close to matching the average duration of its insurance liabilities.) Fairfax was able to side-step the greatest bear market in history in bonds. Saved the company billions in losses. And allowed them to fully capitalize on the hard market in insurance. Simply brilliant. 2.) Share Buybacks - How to use common shareholders equity to grow the insurance business As a reminder, to support its aggressive acquisition strategy in insurance from 2014 to 2018, Fairfax increased effective shares outstanding by 6 million shares at an average cost of about $462 per share. From 2018 to 2023, Fairfax reduced effective shares outstanding by 4.2 million at an average cost of about $503 per share. Fairfax was able to buy back 70% of the shares issued at a price that was about 10% higher than what they had been issued at - even though the intrinsic value of the company (measured through the lens of NWP/share) had substantially increased. Of the 4.2 million shares bought back, at the end of 2021, Fairfax spent $1 billion to buy back 2 million shares at $500/share. At the time, Fairfax still did not have a lot of excess cash. And what cash they did have was being used to drive growth at the insurance subs in the hard market. What to do? Get creative - again - and sell part of an asset to minority partners. Fairfax sold 9.99% of Odyssey to 2 large Canadian pension funds for $900 million. 9.99% of Odyssey was sold at 1.7 x book value. And the proceeds were used to buy Fairfax shares that were trading at 1.1 times book value (and Fairfax knew intrinsic value was much, much higher). Over the past 3 years, book value at Fairfax has exploded higher. Book value was $1,033 per share at September 30, 2024. (And yes, the intrinsic value of Fairfax is much higher than this). Fairfax’s shares are currently trading at about $1,400 per share. The buybacks made from 2018 to 2023 have delivered exceptional value to Fairfax shareholders. The key takeaway is Fairfax saw a wonderful opportunity and they once again sized their bet appropriately - they backed up the truck. And they found a creative way to execute it. In 2024, Fairfax continues to be very active on the share buyback front. I estimate they will reduce effective shares outstanding by another 1.1 million at an average cost of about $1,127 per share. Full circle. From 2014 to 2018, Fairfax grew effect shares outstanding by 6 million shares. From 2018 to 2024, they are on track to reduce effective shares outstanding by 5.3 million. The dilution caused by share issuance has almost been completely reversed. Importantly, the shares were repurchased at very attractive prices. Fairfax’s use of common shareholders’ equity (issue and then repurchase shares) to aggressively expand its P/C insurance business over the past 10 years has delivered outstanding value to long term shareholders. ————— A hard market is the best way for an insurance company to grow but they do not last forever. And it looks like the current hard market is slowing. Does this mean that the growth story at Fairfax is over? No. For a couple of reasons. One reason is Fairfax has set the table nicely for what will likely drive the next phase of growth for the company’s insurance business: the buying out of their minority partners. Phase 3: Take-out of majority/minority insurance partners (2021-2025) As we have discussed, there were times from 2014 to 2022 when Fairfax was capital constrained. But that all changed in 2023. Earnings at Fairfax exploded higher. Fairfax is now earning around $4 billion per year. Importantly, this level of earnings looks like the new ‘normalized level.’ Not only is it sustainable, it should grow nicely in the coming years. What will Fairfax do with this Smaug-like mountain of gold that is coming in each year? The hard market in insurance appears to be slowing. This means the insurance subs will likely not be needing as much capital. What else could Fairfax do? Now that they are all cashed up, we could see Fairfax take out their insurance partners. And guess what? This is what they have been doing. In recent years, we have seen Fairfax getting more aggressive in taking out their minority/majority insurance partners beginning with the Allied World (2022) and then Gulf Insurance Group (2023). And in December, Fairfax announced the takeout of its minority partner in Brit (2024). We will likely see this continue in 2025 and 2026. How much has Fairfax spent in recent years to take out its insurance partners? Over the past 4 years, Fairfax has committed to spend a total of $2.26 billion. Fairfax has been spending a significant amount of money, especially over the past 3 years, to take out its insurance partners. Let’s do a short review of each of these transactions. Eurolife 2018 & 2021 Eurolife Increased ownership from 40% to 50% and then to 80%. The last 30% was purchased from OMERS in 2021 for $143 million. Fairfax now owns 80% of Eurolife. Eurobank owns the remaining 20% of Eurolife. Singapore Re 2021 Singapore Re Paid $103 million to increase ownership from 28.1% to 96% (now 100%). In this example, Fairfax took out the majority partner. Fairfax now owns 100% of Singapore Re. Their buyout in 2021 was timed perfectly - it was done right before the hard market in reinsurance started. Allied World 2022 Allied World Paid $733 million to increased ownership from 70.9% to 82.9% In Q2 of 2023, paid $31 million to increase ownership from 82.9% to 83.4%. In 2022, Fairfax began the process of buying out its partners in Allied World. Given the sums involved it makes sense Fairfax will do this in a couple of bites and over a couple if years. Gulf Insurance Group 2023 Gulf Insurance Group Fairfax took out the majority partner, KIPCO, with this purchase. Fairfax increased their stake from 43.7% to 90%. Paid $740 million (‘fair value aggregate valuation’). In April of 2024, paid $126.7 million to increase ownership from 90% to 97.1%. Like with Singapore Re, Fairfax took out the majority partner (Kipco in this case). Fairfax now owns 97% of GIG. This purchase was very important strategically - it solidifies Fairfax’s presence as one of the largest P/C insurance companies in the important and growing MENA (Middle East / North Africa) region. Brit 2024 Brit Paid $383 million to increased ownership from 84.2% to 100%. Fairfax announced this transaction on December 13, 2024. Why is taking out insurance partners good for Fairfax shareholders? These purchases are a good ‘use of cash’ for Fairfax. They know the assets well (to state the obvious). From a capital allocation perspective, these transactions are very low risk / solid return for Fairfax. Majority partners - from associate to consolidated holdings In two of the transactions, Fairfax took out the majority partners. GIG was the larger purchase. This purchase has been driving the increase in NPW at Fairfax in 2024. Minority partners - equity accounted holdings The minority partners (OMERS and CPPIB) are getting paid for their investment (primarily via dividends in the 8% per year range?). Taking out the minority partners means the amount they are getting paid will now flow to Fairfax shareholders. Taking out the minority insurance partners increases the share of Fairfax’s earnings that accrues to common shareholders - it increases their economic interest in the company. For common shareholders, It increases the numerator in the earnings per share calculation. The ‘net earnings attributable to shareholders of Fairfax’ part. Buying back shares reduces the denominator in the EPS calculation. Doing both at the same time? Yes, the result is magic for shareholders. (What is happening at Fairfax today.) Taking out the minority partners also simplifies Fairfax’s structure and makes the company easier to understand. Minority partners - What is left? Fairfax has three large minority partner positions outstanding: Allied World at 16.6% Odyssey at 9.9% Eurolife at 20% (not included in the chart below because it is primarily a life insurer) Taking out the minority partners at Allied and Odyssey will increase the economic ownership of Fairfax shareholders by about 6.6% (measured by NWP). How much will it cost? The total cost to Fairfax will likely be a little more than $2 billion. —————- After all this, what did we learn? Growth investing is defined as identifying and investing in companies with above average growth prospects compared to the industry/peers. Over time, higher growth leads to higher earnings which usually leads to a higher stock price. For growth investing to work the company needs to be successful - does the growth and higher profitability actually happen? In Part 1 we learned that Fairfax is a growth company. The numbers are pretty clear. From 2014 to 2024: Net premiums written increased from $6.1 to $25.4 billion = CAGR of 15.3%. NPW per share increased from $289 to $1,160 = CAGR of 14.9% In Part 2 we learned how Fairfax achieved such high growth in its insurance business: From 2014 to 2018, growth was driven by acquisition. From 2019 to 2024, growth was driven by hard market. This growth was achieved: In both soft and hard insurance markets. In bull and bear financial markets (stocks and bonds) - many of their best decisions came during times of extreme volatility. When they were severely short on cash (2015 to 2021). Capital allocation When it comes to capital allocation, all the ‘usual’ tools in the toolbox were skillfully used: Equity Debt Asset sales Fairfax also discovered a new tool - minority partners. Fairfax has been: Open minded - read the situation well. Rational - fact based decisions. Flexible - used the right tools. Creative - found solutions to problems. Opportunistic - acted when the time was right. Conviction - sized their decisions appropriately. Long term focus - kept their eye on the prize - building per share value over the long term for shareholders. As a result, both capital allocation objectives were achieved: Increase in per share value for shareholders over the long term. Made the company stronger. Over the past 10 years, Fairfax has been delivering a clinic in how to grow a P/C insurance business. The picture Fairfax has been painting is starting to come into focus for investors - and it looks like a masterpiece. Their strategic vision, planning, creativity and execution has built Fairfax into a global insurance giant that looks exceptionally well positioned today. Based on what we have learned, when it comes to growing a P/C insurance company, I think we can reasonably conclude that the management team at Fairfax is best in class. What about the future? Most investors see the hard market slowing. So they naturally expect Fairfax’s top line growth (NWP) to also slow. But is that what history teaches us? No. History teaches us that Fairfax has been able to significantly grow its insurance business - regardless of where we are in the insurance cycle. The expectations of investors today is contradicted by what has actually happened at Fairfax over the past 10 years. Fairfax grew their insurance business at a CAGR of 15.3% when they were cash poor. And now that they are all cashed up we should expect the growth of the insurance business to flatline? That makes no sense to me. At a minimum, Fairfax should be able to grow its insurance business in the coming years at a rate that exceeds (double?) the growth we see in the overall P/C insurance market. There are some pretty simple things Fairfax can do today to grow the per share economic interest of shareholders: Continue to grow in the hard market. Yes, the rate of growth is slowing. However, with inflation staying elevated in the 3% range, we should see 3% to 5% growth in NPW in the coming years. Continue with bolt on acquisitions - like they have been doing. Take out of minority partners - Allied World, Odyssey and Eurolife. This will likely be a multi-year process. Share buybacks - Fairfax shares are still undervalued. Perhaps the pace of buybacks slows to around 2% per year. These 4 activities alone should drive high single digit / low double digit growth in Fairfax’s insurance business - the economic interest of long term shareholders. Importantly, this does not include the growth that will be coming from Digit. Management Fairfax is generating an enormous amount of free cash flow - and this is expected to continue in the coming years. They also have a best in class management team. That is a wonderful combination. Like they have done repeatedly in the past, I also expect that Fairfax will pull another rabbit out of their hat in the coming years - they will do something big that will build the per share value of their insurance business for long term shareholders. Something we don’t see today - but that will make sense a few years later. What will they do? We won’t know in advance. Because it will depend on what happens in insurance and financial markets. They will be opportunistic. As significant earnings continue to roll in year after year, Fairfax will have the capacity to do something large and transformative. Or perhaps the focus will shift to the non-insurance side of the business for the next couple of years. And that highlights the beauty of Fairfax’s business model (the P/C insurance model exploited so successfully for decades by Warren Buffett). Capital will go to the best risk adjusted opportunities. Insurance and/or investments. With a long term focus. Volatility will be exploited. As an investor, I can’t wait to see what Fairfax does. ————— Was 2010 to 2020 really a lost decade for Fairfax shareholders? Looking at it strictly through the lens of the stock price, yes, it was. However, looking at it through the lens of the insurance business, we get a very different answer - no, 2010 to 2002 was not a lost decade for Fairfax shareholders. From 2015 to 2019, Fairfax did a very good job of significantly growing its insurance business (and integrating the new purchases). This set the table for Fairfax to reap the significant rewards of the hard market that got rolling in 2020. The intrinsic value of Fairfax had been growing nicely at Fairfax from 2010 to 2020. But investors were so focussed on the mis-steps that were happening on the investment management side of the business that they completely missed the significant value that was being created on the insurance side of the business. They forgot that, at its core, Fairfax was still an insurance company. So when Fairfax fixed its problems on the investment management side of the business (the last short position was exited in Dec 2020), the true earnings power of the company was unleashed. Today, both businesses - insurance and investments - have never been positioned better.

AdjustedforMinorityPartners.png.ad588582a02c89c2745e34cf70049114.png)