Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

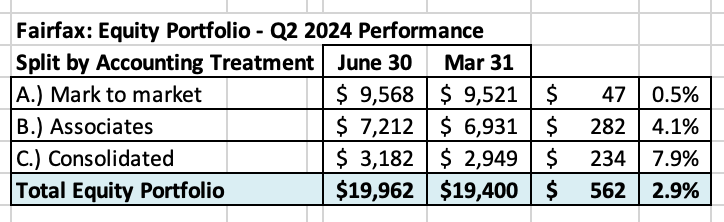

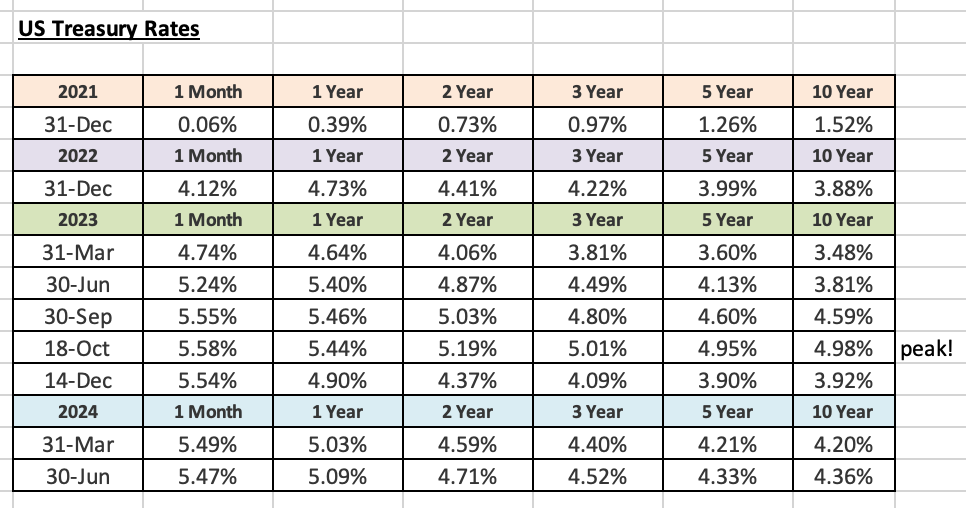

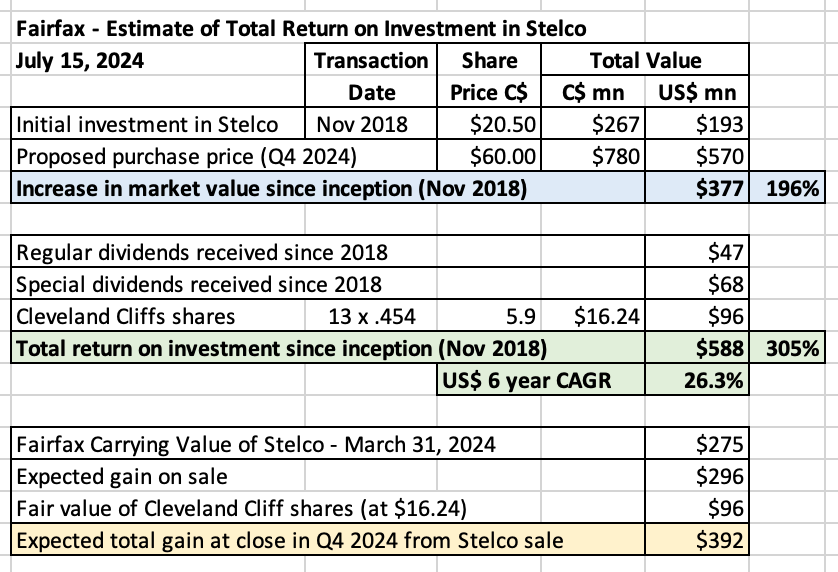

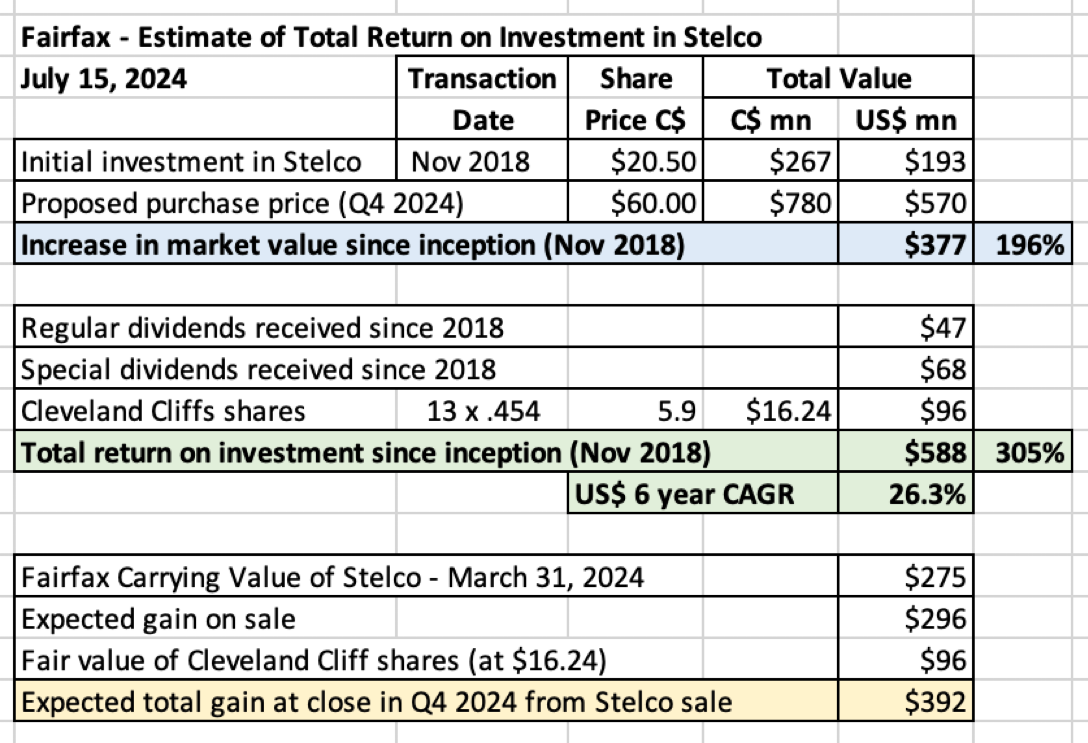

Fairfax Q2 Earnings Preview Below are a few of the things i will be watching for when Fairfax reports after markets close today. Anything missing from my list? 1.) Digit IPO How does Fairfax have the position marked? Has Fairfax been able to sort out its final ownership position out with regulators? 2.) Insurance What is growth in net premiums written? GIG + organic… What is CR? What is level of reserve releases? Commentary on hard market? Cyber? 3.) Interest and dividend income Is it still growing? Interest and dividend income was $589.8 in Q1 2024 (and $536.4 million in Q4 2023). Is Fairfax’s investment in Kennedy Wilson’s debt platform continuing to increase in size? 4.) What is share of profit of associates? Eurobank? Chug, chug, chug? Poseidon? Are we seeing green shoots? 5.) Equities What are investment gains from equities? The equities I track suggests mark to market gains will be small in the quarter (see next point). Please note, mark to market equities in Fairfax India jumped quite a bit in Q2 - this should be a tailwind (it was a headwind in Q1). This is not captured in my model. For Associate holdings, what is the excess of market value to carrying value? This is value that is not being captured by book value. 6.) Capital allocation Asset sale / purchase: any commentary? Sale of Stelco. A nice investment gain is coming in Q3. Purchase of Sleep Country. Update on effective shares outstanding Under 22.4 million? 275,000 purchased from Prem in Q2. any commentary? Do we see Fairfax buy back another chunk from one of their minority partners in Brit, Allied or Odyssey? 7.) What is book value per share? The dividend payment in January will dent this by $15/share. 8.) Impact of change in interest rates on reported results? US Treasury rates closed out Q2 very close to where they closed out Q1. There will be two impacts: Fairfax’s fixed income portfolio IFRS 17 reporting How will it shake out? Not sure - but not concerned.

-

Why would Fairfax want to take Fairfax India private (buy out existing shareholders)? I can think of one good reason - Fairfax gets a deal. Now if Fairfax gets a deal i am not sure how Fairfax India investors also get a deal (or at least feel like they are getting one). Other than ‘good deal,’ I am having a hard time coming up with a good reason why Fairfax would want to take Fairfax India private: 1.) Fairfax already controls it. 2.) Fairfax owns 42.5% of the company. 3.) Fairfax India is very well managed. 4.) The performance of Fairfax India has been very good - measured as growth in book value. 5.) Fairfax India owns a jewel of an asset (BIAL) which represents more than 50% of Fairfax India’s total value. Fairfax India has been an exceptional investment for Fairfax. 1.) Fairfax has increased its ownership in Fairfax India from 28.1% to 42.5% at a very low average cost. That is an increase of 50% since inception. 2.) As i said earlier, the BV of Fairfax India has increased materially since inception. This is a double win for Fairfax. Future prospects for Fairfax India look very good. 1.) BIAL looks ideally positioned. 2.) An Anchorage/BIAL IPO is planned. 3.) IDBI rumours continue to swirl (what that acquisition would look like i have no idea). 4.) India’s economy looks set to rip in the coming decade. Why does Fairfax need to do anything? Especially if they have to pay fair value?

-

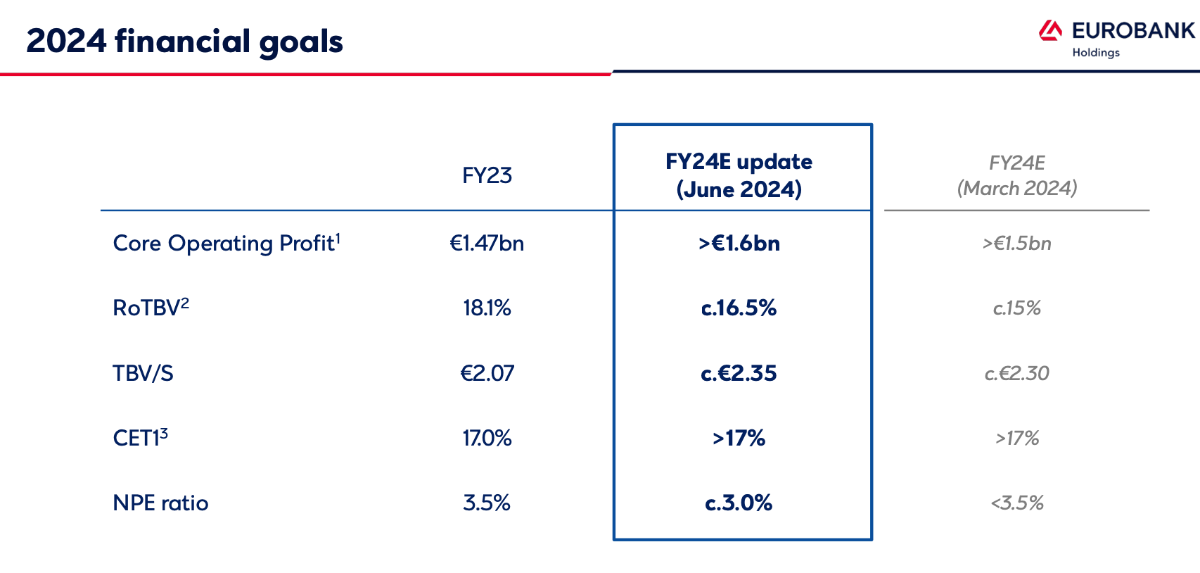

@nwoodman thanks for sharing. The management team at Eurobank continues to underpromise and overdeliver. As you pointed out they raised full year guidance initially provided in March. The updated guidance is below. https://www.eurobankholdings.gr/-/media/holding/omilos/grafeio-tupou/etairikes-anakoinoseis/2024/2q2024/2q2024-results-presentation.pdf

-

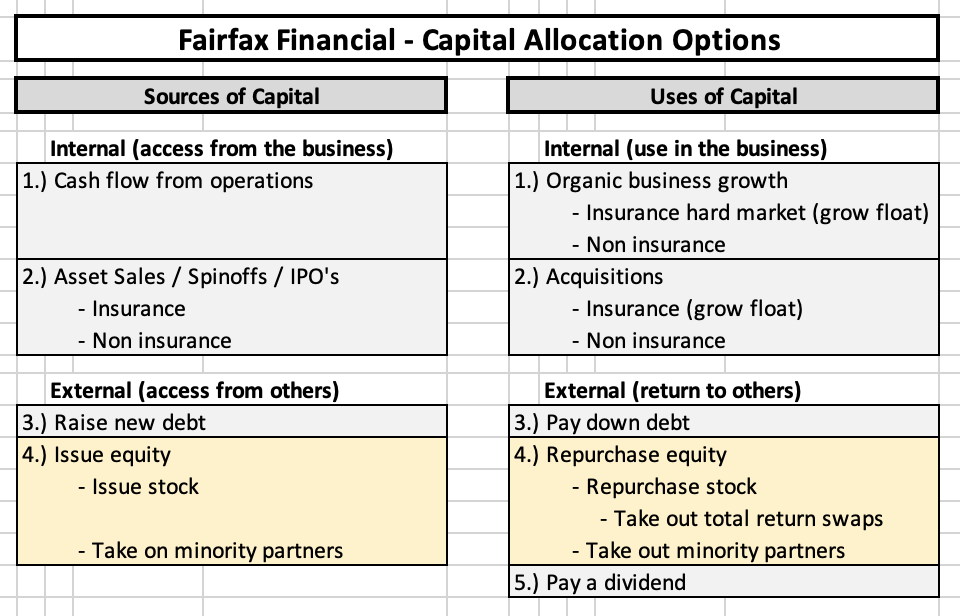

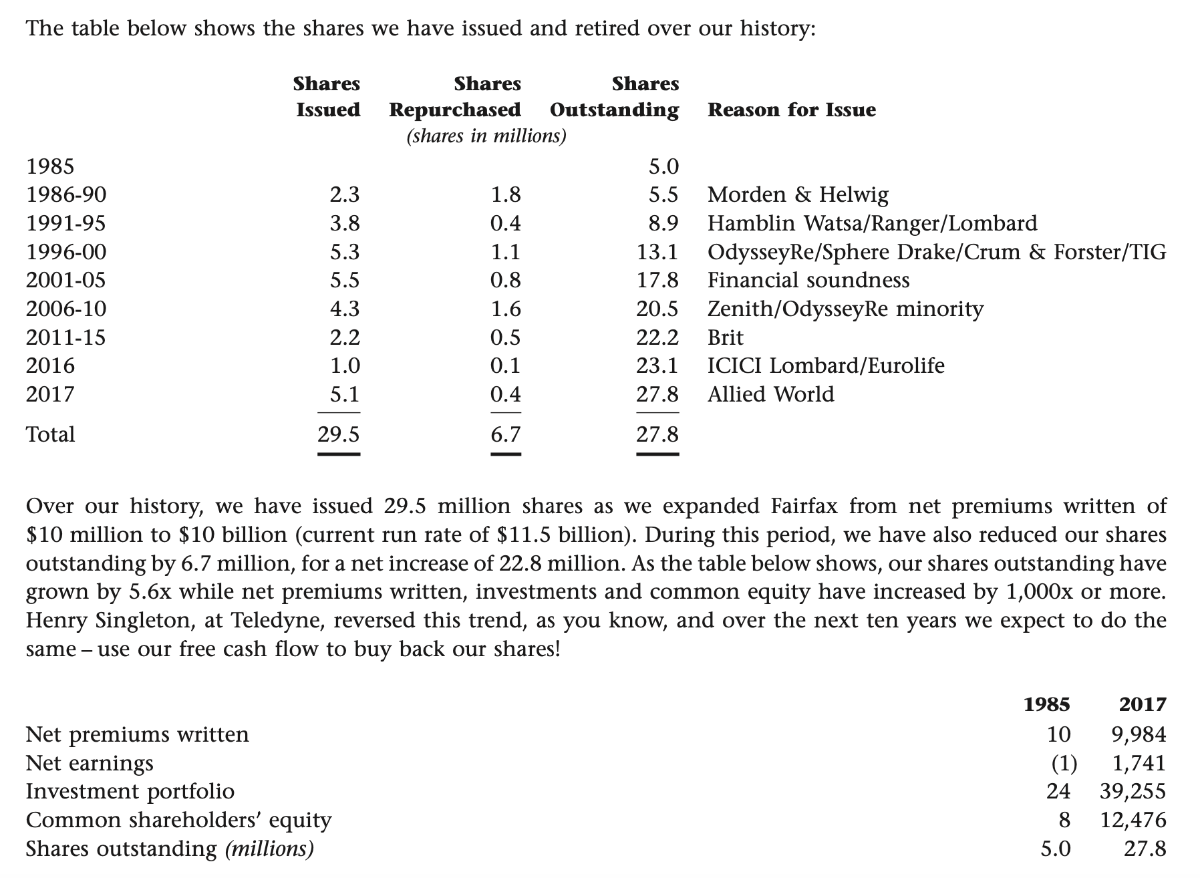

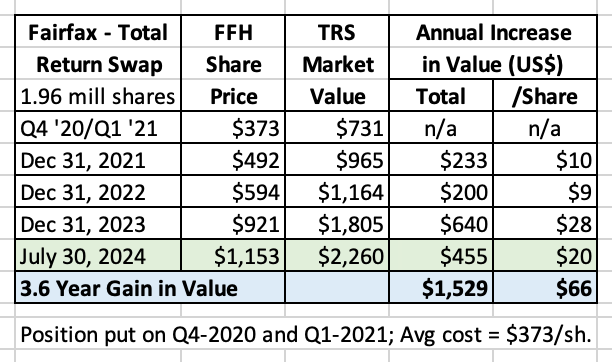

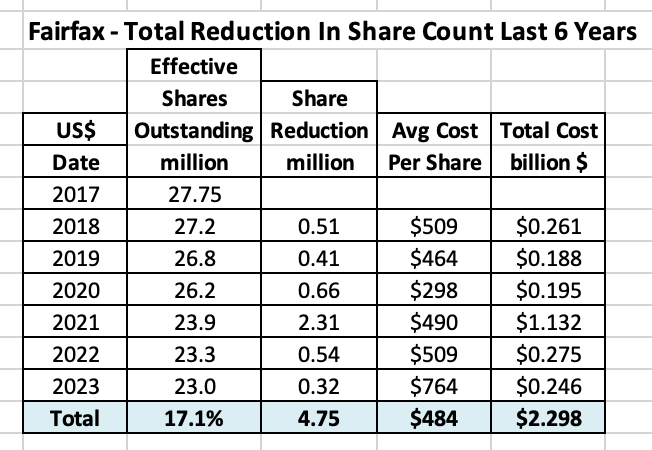

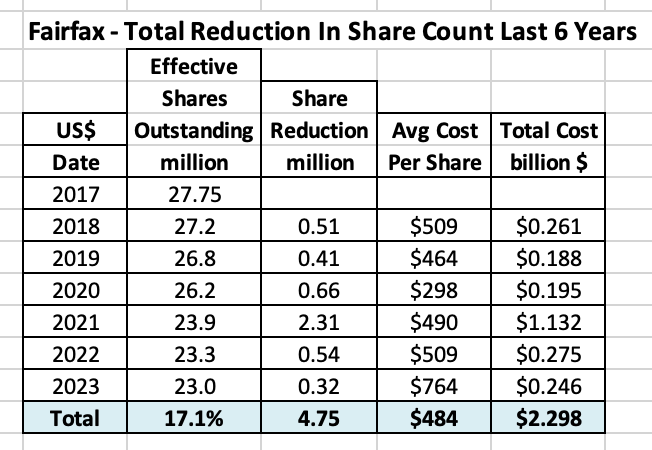

Fairfax - The Influence of Henry Singleton “History never repeats itself, but it does often rhyme.” Mark Twain In my last post I did a short review of Henry Singleton. He has been an important influence/mentor to Fairfax. Today we are going to try to connect some of the dots. We are going to focus on capital allocation and one tool in the capital allocation toolbox - shareholders’ equity. And how, when it is used properly, it can build significant long term per share value for shareholders. But remember… when comparing the present with the past we will never find an exact ‘repeat.’ That is not the point/objective of doing this exercise. However, if we look closely, we can find important examples of where the present does indeed ‘rhyme’ with the past. And that, in turn, can help improve our understanding of Fairfax - what they are doing and what they might do in the future. --------- Link to my previous post on Henry Singleton https://thecobf.com/forum/topic/20517-fairfax-2024/page/65/#comment-572533 ---------- Let’s start with the big picture A CEO has two basic responsibilities: Operations (run the business) Allocate capital When allocating capital, the basic choices available to the management team at Fairfax have been captured in the table below. In this post, we are going to focus on one tool in the capital allocation toolbox - shareholders’ equity - both as a source of capital (issuing stock) and as a use of capital (repurchasing stock). Shareholders’ equity The playbook of how a management team can use shareholders’ equity to drive long term per share value for shareholders is pretty simple: Issue stock when it is overvalued - and buy assets that are undervalued. Buy back stock when it is undervalued. Be aggressive at extremes (overvaluation and undervaluation). Keep doing both as long as conditions remain favourable. There are two key reasons this strategy works so well: Mr. Market’s behaviour can very irrational at times - and it can persist for years. The management team knows what the intrinsic value of the company is - it has a big information advantage over Mr. Market. The proper execution of this strategy over time can lead to extraordinary results for long term shareholders. Henry Singleton taught us this when he ran Teledyne. ————— Fairfax Financial - Shareholders’ Equity - A 38-Year Journey Let’s review how Fairfax Financial has used shareholders’ equity over their 38 year history to see what we can learn. We will break our analysis into two time-frames: Phase 1 - 1985 to 2017 - Building out the P/C Insurance Platform Phase 2 - 2018 to today - Optimize the Operating Businesses and Aggressively Shrink the Share Count Phase 1 - 1985 to 2017 - Building Out the P/C Insurance Platform In 1985, the year it was founded, Fairfax began its journey with 5 million shares outstanding. From 1985 to 2017, Fairfax: Issued 29.5 million shares Repurchased 6.7 million shares As a results, effective shares outstanding at the end of 2017 were 27.8 million (5 + 29.5 - 6.7) - they increased by a total of 22.8 million over the previous 32 years. Over the first 32 years of their existence (from 1985 to 2017), share issuance was used aggressively as a source of cash - and this cash was used to grow Fairfax’s global P/C insurance platform. From 1985 to 2017, Fairfax issued a total of 29.5 million shares. Shares were generally issued at a premium to book value (sometimes a significant premium). Proceeds were used to buy other P/C insurance companies trading at a much lower valuation. Bottom line, looking at share issuance in aggregate, Fairfax got good value. Share buybacks have also been a meaningful use of cash for Fairfax. From 1985 to 2017, Fairfax repurchased a total of 6.7 million shares. Repurchases were 22% of issuance - over the years, for every 5 shares that were issued, Fairfax repurchased 1 share back. Share were generally repurchased when Fairfax’s stock was trading at a discount/on sale. Like with share issuance, Fairfax got good value when they repurchased shares. So in general, Fairfax issued stock when its shares were trading at a high valuation and used the cash to buy P/C insurance companies that were trading at a much lower valuation. Fairfax also bought back modest amounts of stock at times when its shares were trading at a low valuation. This looks like it was textbook application of the principals of what a management team should do. Is there a way we can actually measure how successful this strategy has been? Yes. We can look at the change in long term per share book value (BVPS). From 1985 to 2017, Fairfax increased: the share count at a CAGR of 5.5%. common shareholders equity at a CAGR of 25.8%. BVPS at a CAGR of 19.5%. Using its stock to drive the growth of its P/C insurance platform resulted in enormous long term per share value creation for shareholders. From Fairfax’s 2017AR: ————— An important strategic change in 2017 With the purchase of Allied World in 2017, Fairfax officially completed the aggressive 32-year build out of their global P/C insurance platform. Moving forward, Fairfax would be focused on two things: Continue to do smaller bolt-on P/C insurance acquisitions. Optimize its existing insurance operations and investment portfolio. Truth be told, Fairfax got to work optimizing its insurance operations back in 2011, when Andy Barnard was appointed President and COO to manage Fairfax’s total insurance business. When it comes to investments, fixed income has always been a strength of Fairfax. The issue at Fairfax in 2017 was its equity portfolio - it was stuffed full of underperforming companies, many of which were significant cash drags (they were not delivering cash to Fairfax - they needed cash from Fairfax). By optimizing the insurance operations and investment portfolio Fairfax would be able to improve the ‘cash flow from operations,’ the most important source of cash. What was the company planning on doing with the future free cash flow? In the 2017AR, Prem told investors what was to come - Fairfax intended to get much more aggressive with share buybacks. “Henry Singleton, at Teledyne, reversed this trend (of growing share count), as you know, and over the next ten years we expect to do the same - use our free cash flow to buy back our shares!” At the time, Prem was laughed at (pretty loudly) for what he said. Let’s look at what has happened at Fairfax since then. Phase 2 - 2018 to Today - Optimize the Operating Businesses and Aggressively Shrink the Share Count What did Fairfax do? 2018-2023: Aggressively reduce the share count Effective shares outstanding at Fairfax peaked at 27.75 million in 2017. Over the past 6 years (to December 31, 2023), Fairfax reduced effective shares outstanding by 4.75 million, or 17.1%, at an average cost of $484/share. From 2018 to 2023, Fairfax was able to repurchase a significant amount of shares at a very low valuation. This is a great example of exceptional value creation by the management team at Fairfax. What does this do to the important per share metrics? Here is Prem’s slide from Fairfax’s AGM in April 2024. Before moving on, we are going to take a minute to review a couple of things Fairfax did in 2020 and 2021. Because they provide some great insight into how Fairfax thinks about and executes capital allocation. ————— Classic Fairfax - Turning Lemons into Lemonade Fairfax’s share price got historically cheap in 2020/2021. I won’t get into the reasons as to why that happened (I have covered that topic in detail in many past posts). 2020 and 2021 was a great time for Fairfax to buy back a meaningful amount of its stock. The problem Fairfax had at the time was they were cash poor. What to do? Classic Fairfax - get creative. Fairfax made two brilliant moves in late 2020 and 2021. 1.) Fairfax Total Return Swap In late 2020/early 2021, Fairfax established a position in a total return swap giving it exposure to 1.96 million Fairfax shares at an average price of $373/share. Although not technically a buyback, establishing this position serves as the next best thing. This position gave Fairfax exposure to 7.5% of its effective shares outstanding (26.2 million at Dec 31, 2020). That is a massive position. 2.) Dutch Auction In late 2021, Fairfax executed a dutch auction and repurchased 2 million Fairfax shares at $500/share. To fund the repurchase, Fairfax sold a 9.99% equity stake in their largest P/C insurance company Odyssey Group to CPPIB and OMERS for proceeds of $900 million. This was a wicked smart way to quickly source a significant amount of cash from trusted, external sources. In turn, this allowed Fairfax to capitalize on a short term opportunity (share price trading at crazy low price). https://www.fairfax.ca/press-releases/fairfax-announces-us1-0-billion-substantial-issuer-bid-and-sale-of-9-99-minority-stake-in-odyssey-group-2021-11-17/ How have these two moves worked out? 1.) The FFH-TRS position is up $1.5 billion over the past 3.6 years (before carrying costs). This has turned into one of Fairfax’s best ever investments. 2.) Fairfax’s book value is $945 at March 31, 2024. Buying back 2 million shares at $500/share only 2.5 years ago was a steal of a deal for Fairfax and its shareholders. Both of these moves executed by Fairfax scream Henry Singleton. They were: Very creative - establishing TRS and selling 9.99% of Odyssey to external partners. Very rational - Fairfax’s stock was trading at a historically low valuation. Highly opportunistic - seize the moment. Executed in scale. Both of these moves were of a significant size. Very unconventional - both were classic Fairfax moves. Most impressively, these two deals were executed at a time when investors in Fairfax were literally ‘freaking out.’ But the management team at Fairfax was not ‘freaking out.’ Instead, the management team at Fairfax saw the opportunity and made two outstanding investments - the temperament the senior management team displayed during these dark times shows, among other things, great character. This should speak volumes to investors about the quality of the management team in place at Fairfax. This bodes well for the future. It should also be noted that before Fairfax made either of these two investments, Prem told Fairfax shareholders very loudly that he thought Fairfax’s shares were dirt cheap. In June of 2020 he purchased $149 million in Fairfax shares at an average price of $309/share. https://www.fairfax.ca/press-releases/prem-watsa-acquires-additional-shares-of-fairfax-2020-06-15/ ————— OK, let’s circle around and get back on track. Has Fairfax continued to buy back its shares in 2024? My guess is when Fairfax reports Q2 results later this week, effective shares outstanding will come in at less than 22.4 million at June 30, 2024. Fairfax is on track to reduce effective shares outstanding by 1 million in 2024. This is at a much higher pace than we have seen in recent years. Why is the pace of buybacks picking up in 2024? I can think of two reasons: 1.) Low valuation: Fairfax’s stock continues to trade at a cheap valuation - its valuation is well below that of peers. 2.) Record free cash flow: Fairfax is now generating a record amount of free cash flow. It is coming from two sources: Record cash flow from operations (primarily operating income) Significant cash from asset sales Since 2018, Fairfax has been working hard at optimizing its cash flow from operations. Importantly, the equity portfolio has been fixed. All three of Fairfax’s economic engines are now performing at a high level at the same time - and they have never been positioned better for the future: Insurance Investments - fixed income Investments - equities Asset sales have historically been an important source of cash for Fairfax (and investment gains). This strength of Fairfax continues. The most recent example was the just-announced sale of Stelco. In 2023, it was the sale of Ambridge. In 2022 it was the sale of pet insurance and Resolute forest Products. All four sales were executed with the buyers all paying a premium price. As a result, Fairfax is generating record free cash flow. And this looks set to continue in the coming years. Summary From 1985 to 2017, Fairfax was focussed on building out its global P/C insurance footprint. To fund this growth, Fairfax used its stock - usually issued when the stock was trading at a premium valuation. In 2017, with the Allied World acquisition, Fairfax was officially done building out its global P/C platform. The focus of the company shifted to optimizing the cash flow from the insurance operations and investment portfolio. From 2018 to today, Fairfax has reduced effective shares outstanding by more than 19%. Fairfax was very opportunistic and shares were repurchased at a very low valuation. Over the past 38 years, Fairfax has put on a clinic on how to use shareholders’ equity to build long term per share value for shareholders. Henry Singleton would be proud of what they have been able to accomplish. But the Fairfax story is still being written. Free cash flow at Fairfax has exploded over the past three years. The size and certainty of future earnings have both markedly improved at Fairfax in recent years. Buffett teaches us that certainty is the key variable to properly value an investment. At the same time, Fairfax’s management team is best in class among P/C insurance companies - measured though the growth in book value per share over the past 5 years. Fairfax continues to trade at a significant discount to P/C insurance peers. Given what we know, this makes no sense. And if we know it, I think it is safe to say that Fairfax knows it. As a result, like Henry Singleton, it would not surprise me to see Fairfax continue to buy back a meaningful amount of Fairfax’s stock in the coming years. After all, Prem told us what the plan was all the way back in 2017. PS: This post is long. Thanks for hanging in there and making it to the end. As I was writing, it became clear to me that the influence of Henry Singleton on Fairfax goes far beyond just shareholders' equity (issuing stock at a premium valuation and then buying it back at a low valuation). Henry Singleton's influence on Fairfax was likely much bigger - how to structure the company, how to run the operations (focus on cash generation) and how to think about capital allocation (be rational, use all the tools in the toolbox, be creative, go big, don't be afraid to be unconventional etc). And to focus on building long term per share value for shareholders.

-

@Gamma78 I am not sure buying back stock will close the valuation gap. Look at Henry Singleton… he was able to buy back stock at favourable prices for a decade. Look at Berkshire Hathaway… they could have bought back meaningful amounts of stock many times over the past 50 years at good prices. There are two questions that need to be answered: 1.) what is causing the valuation gap for Fairfax (versus peers)? 2.) will stock buybacks cause the valuation gap to close? What is causing the valuation gap for Fairfax (versus peers)? - complexity of business model Fairfax uses. Lots of people don’t understand it. - non-traditional business model Fairfax uses. Lots of people don’t like it. Just look at the blowback on the board from the Sleep Country acquisition. - not Berkshire Hathaway. Lots of investors will not be happy with Fairfax until they become a clone of Berkshire Hathaway. - hangover from past mistakes. Trust, once lost, is slow to rebuild. There are more. What do other people think? Will stock buybacks cause the valuation gap to close? - buybacks will likely stop the stock from getting crazy cheap. - i am not convinced buybacks on their own will get Fairfax’s stock to more fair valuation (like 1.5 x BV). - investors/analysts are underestimating the size of earnings and the impact of reinvestment and compounding over time - so they are continue to undervalue Fairfax today. It’s like the movie Groundhog Day playing out each year. As a result, like 2024, i think Fairfax in the coming years will be able to continue to buy back a meaningful amount of stock at a great price. They could reduce effective shares outstanding by 1 million in 2024 at a price of about 1 x year end BV. That is crazy. This is really a best case scenario for long term shareholders of Fairfax. It’s like shooting fish in a barrel. Growing earnings. Materially lower share count. Like a goat going up a mountain, the important per share metrics will keep moving higher. Could investors fall in love with Fairfax again? Yes. Of course this could happen. But Fairfax will need to continue to execute well. And even then, given their style of investing, it will likely take a couple of years.

-

Poseidon is starting to look interesting to me again. The moat for this company is likely its ownership structure (collection of solid owners). Fairfax’s initial investment was likely a bet on the jockey - Sokol. The near term set-up looks interesting: - monster phase of new-build expansion strategy is almost done. - shipping rates once again are very high - so renewal rates should be solid. And perhaps this helps lock in longer average duration on leases. - interest rates easing - perhaps this helps them get their debt situation/profile optimized for the next 3 to 5 years. It looks like Poseidon’s business has stabilized. Sokol talked a good game at the Fairfax AGM. Perhaps we start to see a small tailwind develop for earnings. I wonder what Sokol has planned next for Poseidon.

-

I think share buybacks are an important input. Fairfax is open/keen to buy back stock - and a significant amount. Especially in their current phase as a company - they are likely done with big P/C acquisitions and they have robust/record free cash flow. Fairfax has reduced effective shares outstanding by about 19% over the past 6.5 years (since share count peaked in 2017). Effectively they are aggressively shrinking the size of the company. My guess is Fairfax could continue to trade at a discount to peers for years (due to complexity of business, etc). If this happens, Fairfax will have a the opportunity to continue to buy back a meaningful amount of stock over the next couple of years (3% per year). Long term shareholders of Fairfax should be praying that the stock stops going up so much Over a decade this strategy really starts to add up. One big benefit is it keeps the company small. And that makes it easier to outperform - it keeps the opportunity set large. And the impact from good decisions can be material. ————— I also don’t think Fairfax wants to become a conglomerate. It wants to have some wholly owned non-insurance businesses. Cash cows. Like Recipe and Sleep Country. This provides a steady income stream for the company that is not tied to the insurance cycle. And it provides assets that could likely be quickly liquidated at a fair price should the need ever arise. But i don’t think Fairfax wants to aggressively grow the company in the conglomerate direction. ————— This all suggests to me that Fairfax will not likely follow in Buffett’s footsteps in terms of capital allocation (in a big way) at least over the next couple of years. I see Fairfax doing more of the same (what we have seen from them since 2018). The one caveat is if we get a big stock market sell off - at the same time Fairfax is flush with cash. Back in 2008? I think they loaded up with large cap ‘quality’ US stocks - only to sell a couple of years later (for a very nice gain) because they needed cash to offset the losses from the equity hedge/short position (with hindsight, they sold their positions way too early - they admitted this in one of the later annual reports). —————- i think effective shares outstanding will be less than 22.4 million at Q2, 2024. We will know in a couple of days.

-

Management is a moat (look at Jamie Dimon) - look at what the management team at Eurobank has done over the past 5 years. Yes, Greece electing a pro-business government has helped. And the end of zero interest rates. But I think focussing too much on 'moat' can box an investor in (that hammer thing Munger liked to talk about so much). All of Fairfax's equity investments are investments. At the end of the day, what I really care about is what kind of a return the equity investments will generate for Fairfax over the next 3 to 5 years. What was Stelco's moat? That is debatable (perhaps it was one thing - Kestenbaum). And what a great investment for Fairfax. Overly focussing on moat when looking at Stelco would have probably messed an investor up. Fairfax has lots of investments like Stelco. Trying to evaluate them primarily through the lens of a moat misses the key point - Fairfax's business model is very different than Berkshire Hathaway's (or how Fairfax execute's within the model). Both companies are very good. It's like having two kids as a parent. One kid does something a certain way and is really good at it. And a parent keeps wishing the other kid, who is successful in their own right, would be more like the first kid (at that certain thing). For a parent, this approach is usually not a recipe for success. If both kids are successful - be happy. And appreciate/embrace their differences.

-

Who is Henry Singleton? And why should a Fairfax shareholder care? “The failure of business schools to study men like (Henry) Singleton is a crime." Warren Buffett (quote from John Train’s book The Money Masters) Fairfax’s business model has been inspired by many great businesspeople/investors over the years. Who are some that immediately come to mind? Here is my top 3 list: Ben Graham - Value investing framework. Warren Buffett - P/C insurance model (float); operating structure. John Templeton - Go international; buy at the point of maximum pessimism. Did I get the top 3 right? Let me know what you think. Who should be #4 on the list? I think it might be Henry Singleton. What did Fairfax learn from Henry Singleton? How to think about - and do - capital allocation. The big picture part of capital allocation. Use all the available tools (both ‘sources of cash’ and ‘uses of cash’) and use them at the right time. And go big when appropriate. (Another more recent thing is optimizing the cash that is being earned by the operating businesses.) Who is Henry Singleton? Henry Singleton is an individual who is not well followed. That is interesting given his amazing accomplishments over his lifetime. Below is a short biography from Wikipedia: “Henry Earl Singleton (November 27, 1916 – August 31, 1999) was an American electrical engineer, business executive, and rancher/land owner. Singleton made significant contributions to aircraft inertial guidance and was elected to the National Academy of Engineering. He co-founded Teledyne, Inc., one of America's most successful conglomerates, and was its chief executive officer for three decades. Late in life, Singleton became one of the largest holders of ranchland in the United States.” https://en.wikipedia.org/wiki/Henry_Earl_Singleton What was Henry Singleton’s track record? Here is how William Thorndike, author of The Outsiders, sums up Henry Singleton’s track record: “Singleton left behind an extraordinary record, dwarfing both his peers and the market. From 1963 (the first year for which we have reliable stock data) to 1990, when he stepped down as chairman, Singleton delivered a remarkable 20.4 percent compound annual return to his shareholders (including spin-offs), compared to an 8.0 percent return for the S&P 500 over the same period and an 11.6 percent return for the other major conglomerate stocks. “A dollar invested with Henry Singleton in 1963 would have been worth $180.94 by 1990, an almost ninefold outperformance versus his peers and a more than twelvefold outperformance versus the S&P 500…” William Thorndike - The Outsiders Here is what Warren Buffett, a pretty hard marker, had to say about Henry Singleton: "Henry Singleton of Teledyne has the single best operating and capital deployment record in American business." Warren Buffett Bottom line, when it comes to building long term per share value for shareholders, Henry Singleton is one of the all-time greats. What were Henry Singleton’s greatest strengths? Singleton was exceptional at both core jobs of a CEO: Operating the business Capital allocation Singleton’s overarching objective was to maximizing long term per share value for shareholders. Corporate structure A key part of Singleton’s success was the corporate structure / operating model he set up at Teledyne: Operating businesses Decentralized Entrepreneurial Capital allocation Centralized Small head office Does this structure look familiar? The inspiration for Berkshire Hathaway’s corporate structure likely came from Henry Singleton and Teledyne. Fairfax also employs this same structure. Operating businesses Singleton was very good at operating businesses - putting in place the right structure, incentives and people. And the focus of the operating businesses was on cash generation, especially when the company completed the acquisition phase of its growth in the late 1960’s. This last point is critically important because optimizing cash feeds the ‘sources of cash’ part of capital allocation. Capital allocation In the rest of this post we are going to focus on the greatest strength of Singleton - capital allocation - because it is not well understood. And because it perhaps offers great insight into how Fairfax operates today. Singleton’s Capital allocation framework Singleton was a trailblazer when it came to capital allocation. What made Singleton stand out from peers at the time? Open minded/range - he was open to using all tools in the capital allocation toolbox (for both ‘sources of cash ‘ and ‘uses of cash’). Flexible - he was open minded / he adapted to changing circumstances. Rational/analytical - he used the right tool for the right job at the right time. Opportunistic/conviction - big opportunities were exploited very aggressively (he had a temperament that allowed him to do this). Independent thinker/contrarian - he often did the opposite of what conventional wisdom suggested was the right thing to do at the time. Unconventional - it did not matter to him that Wall Street did not/frowned on some of his methods / the use of certain tools. Control: it is important to note that Singleton was firmly in control of Teledyne. This control gave him the freedom to execute his unconventional approach to running Teledyne. Shareholders’ Equity - the genius of Henry Singleton We are going to focus on what Henry Singleton is known for most - his aggressive/prolific management of the company’s stock - both in issuing stock and buying it back. Singleton followed a pretty simple playbook: When stock is overvalued - aggressively issue stock and use it as currency to grow the business (buying other companies when they are available at much lower valuations). When stock is undervalued - use much higher cash flow from the business to aggressively buy back shares. Singleton had two distinct phases: 1.) Aggressively issue Teledyne stock (1960 to 1968) - executed at an average PE of 25x Allowed Teledyne to get much more back (value of companies being purchased) than what he was giving up (value of Teledyne’s stock). Singleton bought 128 companies using Teledyne’s stock; he massively expanded the size and scale of the company. 2.) Aggressively buy back Teledyne stock (1971 to 1984) - executed at an average PE of 8x Allowed Teledyne to get much more back (value of Teledyne’s stock) than what he was giving up (using cash in some other way). He bought back stock using tender offers (not open market purchases). Reduced shares outstanding at Teledyne by 90% by the time he was done. Unlike today, in the 1970’s buying back stock was viewed very negatively by Wall Street - it was viewed as a sign of weak/poor business prospects/management. What really stands out with Singleton is: The scale in which he operated when executing a winning strategy - both the massive number of shares he issued and the massive number of shares he then repurchased. Each phase lasted/was executed over a full decade. The discipline he demonstrated: shares were only issued at a premium valuation and repurchased at a low valuation. Singleton had an unfair advantage ‘Good artists borrow. Great artists steal.’ Picasso/Steve Jobs What company did Singleton understand better than any other? Teledyne - his own company. He also understood the company much better than Mr. Market and Wall Street. Singleton took Benjamin Graham’s insight on Mr. Market and the stock market in general and applied a unique twist - he applied it to Teledyne’s stock. The end result was amazing per share value creation for long term shareholders. Was Singleton taking advantage of Teledyne’s shareholders? Warren Buffett often talks about buybacks along moral lines - at least when it comes to Berkshire Hathaway and how the company thinks about its own shareholders. My view is this is more good marketing from Buffett than anything else. Buffett loves it when companies he owns buy back a bunch of their own stock - Apple is a great current example. And we know he thinks very highly of Henry Singleton. In recent years, Buffett has relented and has started buying back Berkshire Hathaway stock in meaningful quantities. The truth is long term shareholders of Teledyne made out exceptionally well - they made a fortune holding Teledyne stock over the decades. Bottom line, shareholders’ equity is an exceptionally important tool in the capital allocation toolbox that management teams can use to grow per share value for shareholders. If it is such a good idea why is it not used more? The interesting thing is most management teams are terrible in their execution of this strategy: they tend to issue their own stock at low valuations and buy back their stock at high valuations. These activities destroy long term per share value for shareholders. Most companies don’t utilize this strategy more aggressively because they are terrible at it. What does all this have to with Fairfax? Not all companies are terrible at executing this strategy. That is what we will explore in our next post. —————- Twenty Punch Investments https://www.twentypunchinvestments.com/p/henry-singleton-and-teledyne —————- A Case Study in Financial Brilliance - Teledyne by Leon Coopermam https://fundamentalfinanceplaybook.com/wp-content/uploads/2019/02/leon-cooperman-case-study-henry-singleton-teledyne.pdf —————- Henry Singleton: A Capital Allocation Masterclass in Three Acts by Kingswell https://www.kingswell.io/p/henry-singleton-a-capital-allocation —————- The Outsiders | William Thorndike | Talks at Google

-

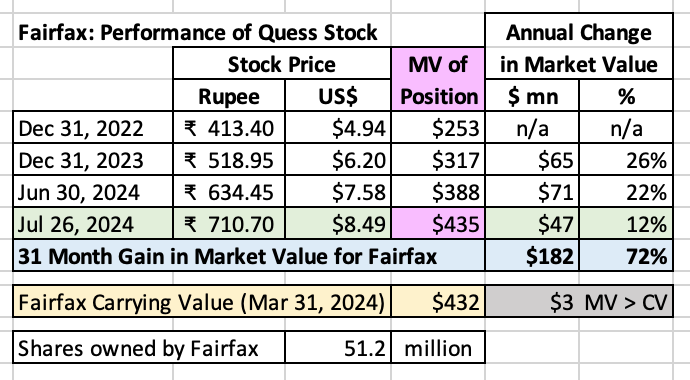

Stock of Quess, India’s leading business services provider and former high flyer, has recovered over past 2.5 years. Fairfax's stake is worth $435m. MV is once again greater than CV. Like when IIFL did it, Quess’ planned split into 3 companies in 2025 looks like a smart move. Of interest: Quess is Fairfax's #12 largest equity holding. Quess' stock price was 855 rupee at Dec 31, 2021.

-

@glider3834 That is great info. Canada had a housing bubble. And because of how our mortgage market is structured, much higher interest rates have had a big impact on those with a mortgage, especially those with a large mortgage. But only about 20% of mortgages ‘reset’ / are affected each year… so it has taken time for higher rates to bite. My guess is for mortgage holders things will get worse over the next 12-18 months. Our mortgage market looks like it was structured like the US back in 2004-2006 with all those adjustable rate mortgages… the shit didn't hit the fan in the US until enough of the resets happened - and that took much longer than people thought (the ponzi scheme was up at that point). Canada won’t be hit as hard as the US because you can’t walk away from your mortgage here - and we don’t have a bankruptcy culture. People will do anything they can yo hang on to their property here - including stopping spending on pretty much everything else. The Canadian economy has been driven by the housing bubble over the past 7 years or so. New building starts have cratered. But lots of existing projects have to be completed - so the impact of higher rates has been slow to hit construction (but it is coming - if rates remain at current levels). Immigration / international students / temporary foreign workers has been adding 1 million new Canadians each year for the past couple of years - that should be a tailwind to GDP growth. But GDP per capital is the same today as it was back in 2017. And there is growing demands for the government to return to historical levels of new Canadians (total of about 400,000 per year). If they do that it will be contractionary as the numbers of some groups could go negative year over year - as people get kicked out of the country. My read is the economy in Canada is sick. We just might remain at stall speed for a few years. I really have no idea. The rub is the Bank of Canada. They have now dropped rates twice. This might be where the improving consumer confidence is coming from. They are going to keep dropping interest rates as fast as they can. If they are able to cut 100 or 150 basis points and the 5-year fixed mortgage rate drops below 4% - perhaps as low as 3.5% - later this year or early next year, our real estate market could really take off again. And that would drive a bunch of other things (wealth effect etc). That is the bull case for Sleep Country. The Bank of Canada has an inflation target of 2 to 3% and i think they want to run it as close to 3% as possible. Canada has too much consumer debt and the elegant way to solve that is to run elevated inflation for 5+ years (we are 3 years in). The problem with this approach is if inflation runs too hot again - gets back north of 4% or more - well people will see what they are doing and their credibility would be shot. Bottom line, I am not optimistic or pessimistic. My guess is Canada muddles through.

-

@73 Reds thank you for the comment. Regarding Berkshire Hathaway, i am a novice when it comes to understanding the company. So my comments are very high level. And they could be way off base. BRK appears to me to be a conglomerate today. Insurance is now one of many businesses. Float is a benefit, just much less of a benefit than it was 20 or 30 years ago. My read is for the past 5 years, perhaps longer, Berkshire Hathaway has been primarily run like a trust - with the focus on preserving the wealth of Berkshire Hathaway’s many, many long term and very wealthy shareholders (who have big tax issues if they sell). Berkshire Hathaway is no longer focussed primarily on building long term per share value for shareholders. Now this might change when Buffett is gone. But it adds a great deal of complexity for the new guy - because if he does something different and it doesn’t work out right away… well his job will just get that much more difficult. As per usual, i am probably way overthinking things. And i like to go to extremes sometimes when posting on the board - to test drive ideas… (thanks for pushing back Anyways, i don’t own BRK shares today. When i do, i usually hold it as a bond substitute.

-

I think the headwinds for Berkshire Hathaway have been growing over the past decade. The problems? 1.) The size of the company. 2.) its capital allocation policies - it looks to me like Buffett has painted himself into a corner. The problem is he likely has also painted his successor into a corner. An couple of examples: - buy and hold forever works best when you are growing rapidly - and earning returns of 20% per year. The queens in your portfolio dominate your dogs. But when you become an elephant and your growth slows - and your returns slow - your dogs become a bigger part of the total portfolio. The buy and hold forever mantra no longer works for BRK - but Buffett made promises decades ago to never sell. That bit of marketing is not going to age well. - not doing stock buybacks (starting much earlier and going heavier) has created the size problem for BRK today. But Buffett has couched buybacks in moral terms ‘taking advantage’ of BRK shareholders. Of course this is marketing. Buffett loves buybacks - look at Apple etc. Buffett also put Singleton on a pedestal and he was the king of buybacks. - is the focus on cash flow resulting in underinvestment at the companies? This appears to have been a big problem at Wells Fargo - they were more profitable than peers for year (and Buffett was constantly praising them) because they were underinvesting - and it blew up. It looks like the same thing has been happening at Geico - Progressive looks much better positioned from a technology perspective moving forward. Does BNSF have the same disease? Are the falling behind peers from a technology perspective? Anyways, i love Warren Buffett and i like BRK as a company. But i think they have some structural issues (some external and some internal) that might make it a challenge for them to outperform the S&P500 moving forward. I do think BRK will likely perform better than a balanced (stock and bond) portfolio. An alternative perspective…

-

Some initial thoughts: I think Sleep Country has been quite the success story over the past 30 years. Interesting to see Fairfax buying the whole company. This will be a significant add to the 'non-insurance consolidated' group of companies (Thomas Cook India, Recipe, Grivalia Hospitality, Dexter etc). It will be interesting to see if Fairfax keeps growing this bucket of companies. Fairfax has been heavily invested in this segment over the past decade, more recently with Leon's (the largest furniture retailer in Canada) and with The Brick before that. Bill Gregson, former CEO of the Brick, was probably involved. I wonder who the driver was of this deal: Prem / Wade / Other? Regardless, it will be interesting to hear what Wade Burton has to say about it on the Q2 conference call. Fairfax is buying Sleep Country at what must be at close to the bottom of the cycle. IF this is the kind of business you want to own - now is probably the right time to buy it. The housing market in Canada is terrible right now (interest rates ARE biting here). Another big private transaction. And another publicly traded holding is gone (Stelco). The publicly traded (especially the mark to market) part of Fairfax's equity holdings has been dramatically shrinking in recent years. The private part has been rapidly growing. Are more asset sales (like Stelco) on the way? What I want to know about Sleep Country (I know nothing about the company, other than it is usually where we shop - and have for decades - when we buy a new mattress set): How good is the management team? If they are good, are they all sticking around? What is the normalized earnings power of this business? How stable are earnings? What are the prospects for the business? What are the strategic reasons for this purchase? Cash cow type of business to be milked over time? Does this signify a trend to more aggressively grow the 'non-consolidated' bucket of holdings?

-

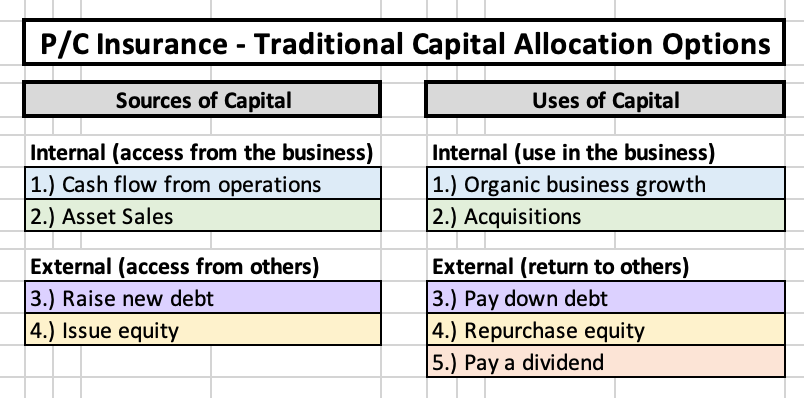

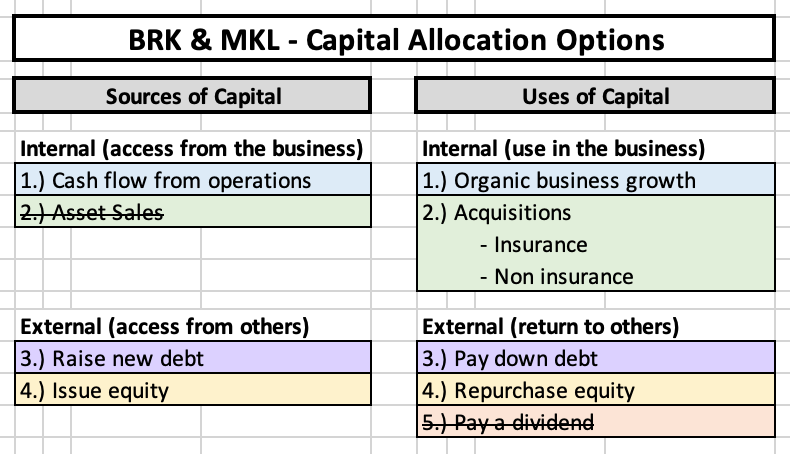

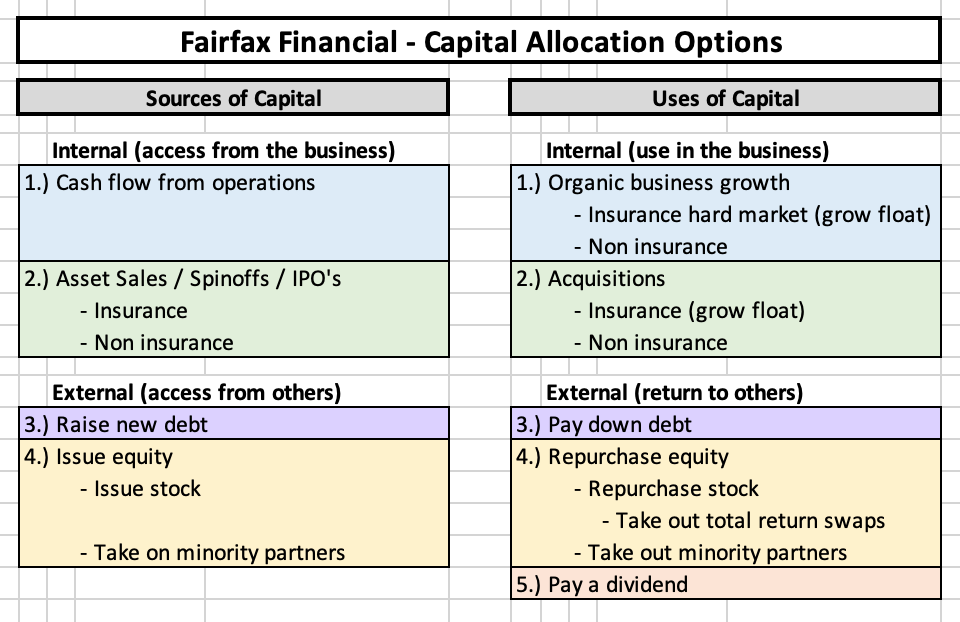

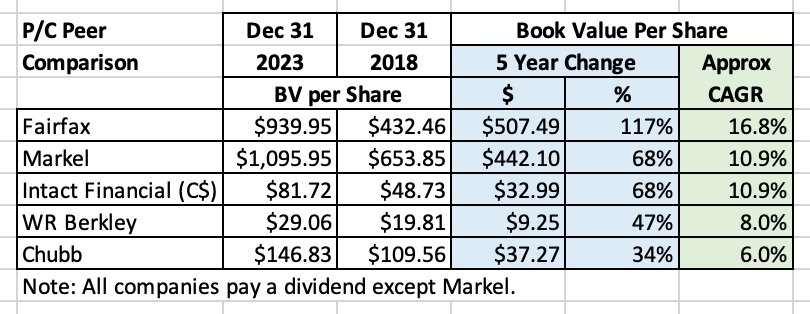

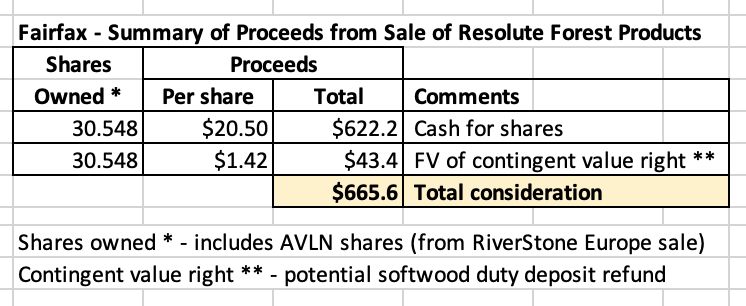

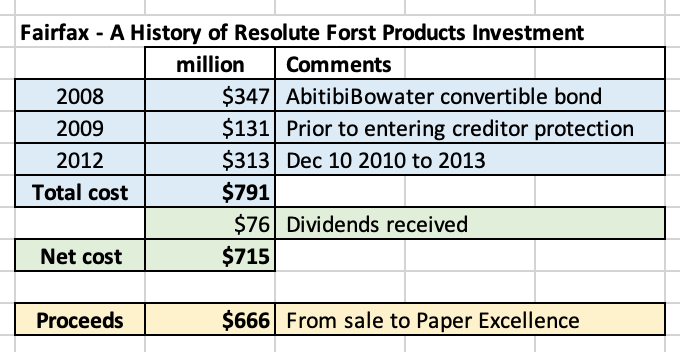

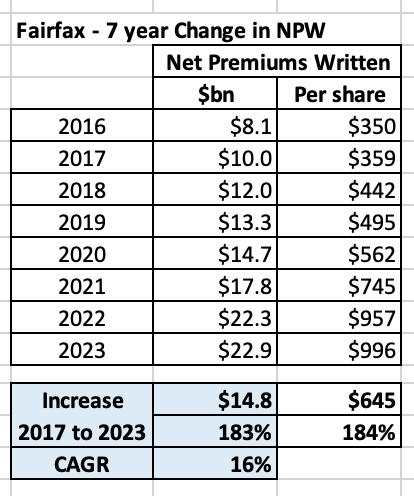

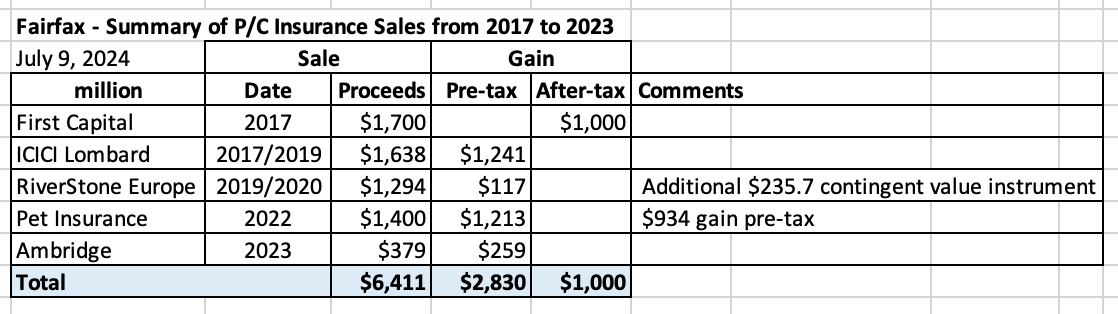

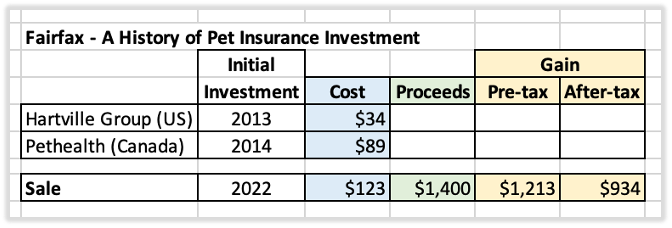

Fairfax - Unconstrained Capital Allocation All P/C insurance companies have two engines to drive earnings/business results over time: Insurance Investments Insurance Pretty much all P/C insurance companies try and do the same thing with their insurance operations - they try and generate an underwriting profit. Some are better at it than others. The combined ratio communicates how a company’s insurance business is performing. Investments Pretty much all P/C insurance companies generally do the same thing with their investment portfolio - they invest it primarily in bonds. The average yield on the investment portfolio communicates how a company’s investments are performing. Investors As a result, it is a pretty simple process for investors to evaluate most insurance companies. Warren Buffett Warren Buffett screwed everything up back in 1967 when Berkshire Hathaway purchased National Indemnity, a P/C insurance company. How did Buffett screw things up? Buffett knew something that apparently no one else at the time knew: equities earn a much higher return over time than bonds. So after he bought National Indemnity he began to put some of its investment portfolio into equities. And what was the result? Magic. Excess returns + compounding + time = exponential growth. And that is what happened to Berkshire Hathaway’s earnings and stock price. It was like Buffett had found a golden goose. Capitalism We all know how capitalism works. When someone discovers a better mousetrap - begins earnings outsized profits - everyone else will rush in and copy the better business model. And quickly compete the outsized returns away. And that is what happened. All the big P/C insurance companies began investing a part of their investment portfolio into equities and their returns over time improved markedly. And their investors made out like bandits. EXCEPT THAT IS NOT WHAT HAPPENED. Almost all P/C insurance companies did not copy what Warren Buffett was doing at Berkshire Hathaway. Why not? Are other P/C insurance companies run by stupid people? The fly in the ointment - Wall Street Volatility Efficient Market Hypothesis and Modern Portfolio Theory When it comes to equities, Wall Street says volatility is the same thing as risk. Stocks ARE volatile. So Wall Street decided this also meant that stocks were also very risky - and therefore more likely to go down in value. Of course, this is garbage. Here is what Warren Buffett had to say about risk at the BRK’s AGM in 1994: “We do define risk as the possibility of harm or injury. And in that respect we think it’s inextricably wound up in your time horizon for holding an asset. I mean, if your risk is that if you intend to buy XYZ Corporation at 11:30 this morning and sell it out before the close today, in our view that is a very risky transaction. Because we think 50 percent of the time you’re going to suffer some harm or injury. If you have a time horizon on a business, we think the risk of buying something like Coca-Cola at the price we bought it at a few years ago is essentially so close to nil, in terms of our perspective holding period. But if you asked me the risk of buying Coca-Cola this morning and you’re going to sell it tomorrow morning, I say that is a very risky transaction.” Short term focus Most P/C insurance companies are publicly traded companies. They are beholden to what Wall Street wants. Wall Street wants companies to hit quarterly earnings estimates - if a company misses, their stock usually gets punished. If this happens too many times, the CEO likely loses his job. Incentives matter. Most CEO’s want to keep Wall Street happy. As a result, they avoid volatility like the plague. The insurance business is volatile enough. Adding volatility to the investment side of the business is a bridge too far for most P/C insurance executives. So they have no interest in investing in equities. The odd ducks Well, there are a few odd ducks that decided to follow Warren Buffett’s lead: Markel Fairfax Financial What allowed these misfits to thumb their nose at Wall Street? Ownership structure Warren Buffett can do what he wants with Berkshire Hathaway because he is in control of the company. It just so happens the other two companies also have controlling shareholders: Markel - Markel family Fairfax Financial - Prem Watsa Long term focus This ownership structure allows each of these companies to focus on long term value creation for their shareholders. Higher lumpy returns (investing in equities) are preferred to lower smooth returns (investing exclusively in bonds). This can’t be right. This sounds too easy. How have these 3 companies performed over time? The long term performance of each of these 3 companies (since inception for each) has been epic. How did they achieve such impressive results? Their P/C insurance business was better than average (much better in the case of Berkshire Hathaway). But their outperformance overwhelmingly came from their investment results and their capital allocation decisions. What about today? A fork in the road. Berkshire Hathaway was so successful at investing in equities that it decided it wanted to own entire companies. This begat more success. Over the past 20 years, Berkshire Hathaway has morphed into a very successful conglomerate, with P/C insurance now only one part of a much larger company. Markel is doing its best to follow in Berkshire Hathaway’s footsteps and become a conglomerate itself. What about Fairfax Financial? Fairfax appears to have little interest in becoming a conglomerate like Berkshire Hathaway (notwithstanding their just announced purchase of Sleep Country). In fact, today Fairfax’s business model looks unique in the P/C insurance industry. Their uniqueness is not on the P/C insurance side of things. Here they have built one of the finest P/C insurance operations anywhere. They have a wonderful global platform. And they have forged a culture of strong underwriting discipline. All of this is similar to other well run P/C insurance companies. Fairfax’s uniqueness comes from how they approach capital allocation. Their approach is very different from traditional P/C insurance companies. And today it is also very different from the approach employed by both Berkshire Hathaway and Markel. When it comes to capital allocation, Fairfax is breaking new ground. Capital allocation Traditional P/C insurers At most P/C insurers, capital allocation is handled in a very traditional / straight forward manner. The basic options are captured in the table below. Berkshire Hathaway & Markel At Berkshire Hathaway and Markel, capital allocation is focussed on building long term shareholder value. But when it comes to capital allocation, certain options are not used and others are frowned upon. 1.) Assets are not sold. Buy and hold (ideally forever) is the goal. Therefore, this source of capital is generally not available. 2.) Equity is used in very limited way. Rarely is equity issued as a source of capital (looking at the past 10 years). Equity is used modestly used as a use of capital (share buybacks). 3.) Neither company pays a dividend. Fairfax Financial Setting the table: The most important source of capital is 'cash flow from operations'.' Fairfax is generating a record amount of cash flow from operations - and this record amount is expected to continue (and grow) in the coming years. Unlike traditional P/C insurance companies and Berkshire Hathaway and Markel, Fairfax uses all the capital allocation options at its disposal. But there is even more. Fairfax is finding new and innovative ways to allocate capital. They are doing some things that haven’t been seen from a P/C insurance company before. Like bringing minority equity partners on board when making large P/C insurance acquisitions. Fairfax has taken Warren Buffett’s original idea and made it even better: unconstrained capital allocation. The restaurant menu is stocked with choices: Sources of capital. Uses of capital. Internal. External. When it comes to capital allocation, Fairfax’s top priority is to be securely financed. After that, the goal is to allocate capital in a way that it results in the greatest long term per share value creation for shareholders. The key with this approach is to be: Open minded. Flexible. Creative. Opportunistic. Conviction - go big. With this capital allocation framework you take what Mr. Market gives you. And that is what Fairfax has been doing. Delivering a master-class in capital allocation. Here are some recent examples of what Fairfax has done: More than doubled the size (per share) of the P/C insurance business (NPW) over the past 5 years from $442/share in 2018 to $996/share in 2023. In late 2020/early 2021, purchased total return swaps - getting exposure to 1.96 million Fairfax shares at $373/share. This investment has increased in value by $1.5 billion over the past 3.5 years. In late 2021, via dutch auction, bought back 2 million Fairfax shares at $500/share. At March 31, 2024, Fairfax’s book value was $945/share. In late 2021, sold $5.2 billion in corporate bonds and shortened average duration of fixed income portfolio to 1.2 years - which shielded Fairfax’s balance sheet from billions in losses when interest rates spiked in 2022/2023. In 2022, sold the pet insurance business and realized a $1 billion gain after-tax. In 2022, sold Resolute Forest Products for $626 million (plus $183 million CVR) at the peak of the lumber market. In 2023, took out majority partner (KIPCO) and increased ownership in Gulf Insurance Group from 44% to 90% for total consideration of $740 million, securing Fairfax’s future in growing MENA region. In late 2023, extended the average duration of fixed income portfolio to about 3 years, locked in record interest income of $2 billion/year for the next 3 or 4 years. In January 2024, increased dividend by 50% to $15/share. In June 2024, Fairfax’s P/C insurance company in India, Digit, completed its successful IPO. In July 2024, sold Stelco (pending approvals) for consideration of $666 million, an 87% premium to where the stock had been trading. The list above is just a start. It really is amazing what Fairfax has been able to accomplish over the past 5 years. What really stands out is the number of tools - the breadth of options - that they have in their capital allocation toolkit today. They are proficient at using all of the tools. And they are using all of them: Organic growth Acquisitions Asset sales IPO Stock buybacks And look at the size/magnitude of the activities - many were +$1 billion in impact. The per share value creation for shareholders has been impressive. Importantly, Fairfax is not trying to copy someone else - like Berkshire Hathaway. Instead, Fairfax is now blazing their own trail. They are focussed on doing what they are really good at. Fairfax looks like a star athlete that is just hitting their prime. They have building towards this moment for 38 years. ————— If you want to better understand what is happening at Fairfax today you might want to read the following book. And pay special attention to the chapter on Henry Singleton - someone who will be the topic of a future post. “An outstanding book about CEOs who excelled at capital allocation.” Warren Buffett The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success by William Thorndike https://www.amazon.ca/Outsiders-Unconventional-Radically-Rational-Blueprint/dp/1422162672

-

“I would much much prefer that on the equity component Prem and Fairfax act like Warren B.” @Gautam Sahgal I used to think along the same line as you. But i am not so sure anymore. The more i think about/study Fairfax the more i am coming to understand and appreciate their unique approach/strengths to capital allocation. When i was a new sales manager my focus initially was on fixing problems (problem employees or weaknesses of good employees). I learned over time that i had it ass backwards. I shifted and spent most of my time feeding my best employees (stars) and getting my weaker performers to focus on their strengths. I want to see Fairfax do what they are outstanding at: - Flexible - Creative - Unconventional - Conviction - Long term focus Look at some of Fairfax’s best investment the past 4 years: - total return swaps: 1.96 million shares at $373/share - dutch auction taking out 2 million shares at $500/share - managing average duration of fixed income portfolio - selling pet insurance for $1 billion gain after tax - selling RFP at peak pricing. - the Stelco investment (buy and sell). - i could go on. Asset sales are a big part of Fairfax capital allocation framework. As is seeding startups like First Capital, ICICI Lombard and now Digit. Would Warren Buffet have done any of these things? Fairfax also appears to have no desire to become a conglomerate. And they appear to be dramatically shrinking the size of the company (with all the buybacks). Not what Warren would do. Fairfax’s capital allocation has been exceptional since 2018. For the past 5 years Fairfax’s management team has been best-in-class among P/C insurers. They are on a hot streak. Do you tell a star basketball player how to shoot a basketball? (I.E. tell Larry Bird he would be a better basketball player if only he shot the ball like Magic Johnson?) They look singularly focussed on growing long term per share value for shareholders. I hope they continue to do the things they are really good at.

-

Prem just resigned from the board in Feb so it likely was not an option to sell before then. Moving forward my guess is Fairfax will treat BlackBerry like any other equity investment - hold it if they see it delivering on their (15%?) hurdle rate for equity investments. BlackBerry does play in some very interesting verticals. What i like is the remaining position is so small that even of it went to zero it wouldn’t matter to Fairfax. I would love to see them sell it. Just to get it off the books - like Resolute Forest Products. Just so we can stop being reminded about it every time we look at Fairfax’s collection of equity holdings. But that is based on emotion. The big learning for me in reviewing Fairfax’s investment exits/sales over the past 7 years is just how much they have improved their underlying business/profitability: - late 2016 - exited equity hedges - this was the big one - 2019 - APR sold to Altas/Poseidon - late 2020 - exited last short position - late 2020 - exit Fairfax Africa - 2022 - sold Resolute Forest Products - 2024 - exited BlackBerry debenture ($500 million) This was an amazing pivot - in both size and philosophy. Its a little crazy, but Fairfax exiting the equity hedges in late 2016 was the belling ringing moment for shareholders that results/performance had bottomed. The equity hedge (we probably should include the short positions as well) was the root cause of Fairfax’s decade of underperformance. Value in the business has been growing since they exited those 2 positions, and significantly in recent years. Since late 2018 it looks like Fairfax has been on mission to optimize its equity holdings. Stop the hemorrhaging of cash. Get rid of the dogs. Reallocate the cash to better opportunities. The job looks pretty much done to me. What now? Watch the cash roll in. And the intrinsic value build. My guess is we start to see more sales like Stelco - perhaps one per year - where Fairfax surfaces significant value. Great time to be a shareholder.

-

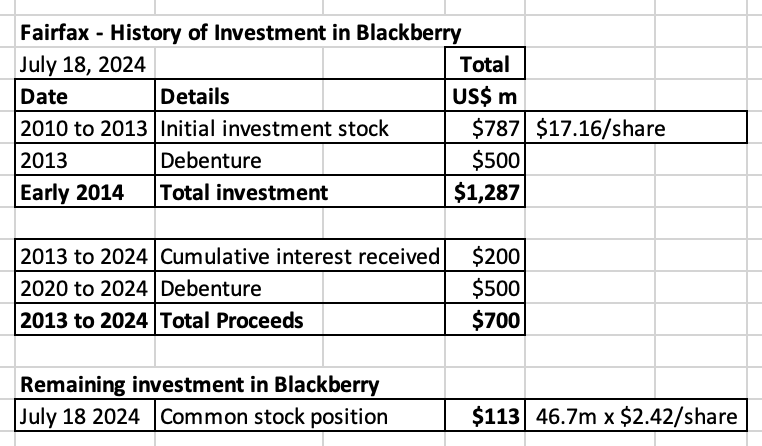

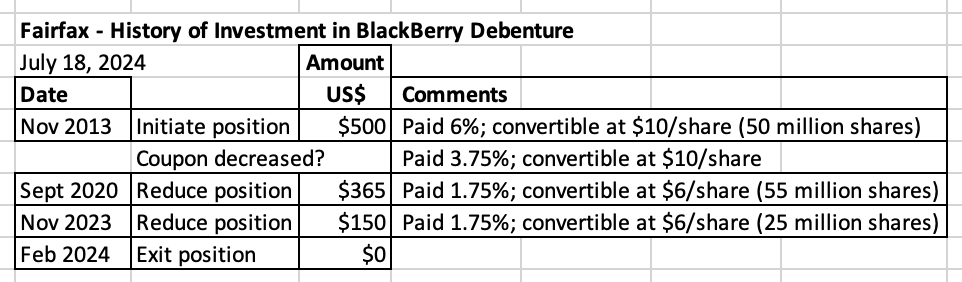

BlackBerry Debenture – 2020 to 2024 – Exiting a Big Mistake Blackberry has been one of Fairfax’s great investing mistakes (that is putting it politely). Fairfax began investing in BlackBerry in 2010 (it was called RIMM back then). By early 2014, Fairfax had invested a total of $1.287 billion. As of July 2024, Fairfax has received proceeds of about $700 million (interest and exit of debenture position). The value of the common stock position in BlackBerry, which Fairfax continues to hold, is $113 million. Bottom line, over the past 10 years Fairfax’s investment in BlackBerry has fallen in value by $474 million. Of course the financial cost to Fairfax and its shareholders has been much higher - when you factor in opportunity cost. Let’s assume in early 2014 that instead of investing in BlackBerry, Fairfax instead invested $1.287 billion in another company. Let’s assume that investment earned 8.5% per year (a modest hurdle rate). Today, that investment would be worth $2.9 billion. The ‘swing’ in value - what the BlackBerry investment is worth today ($813 million) versus what an alternative investment could have been worth ($2.9 billion) is $2.1 billion. That is a very rough approximation of how terrible the investment in BlackBerry has been for Fairfax. But the cost to Fairfax of its investment in BlackBerry goes well beyond financial. When you own such a large position is such a terrible investment the cost to the organization - in terms of resources and time - is likely enormous. On February 15, Prem announced his resignation from the Board of BlackBerry after serving since November 2013. Prem is a busy man (as are other people at Fairfax). The time spend on BlackBerry over the years added no value for Fairfax and its shareholders (in aggregate) - actually it appears to have subtracted significant value. Blackberry has also done significant repetitional damage to Fairfax - it was a high profile 10-year slow moving train wreck. Bottom line, the cost to Fairfax - financial, time, reputation - has been significant. Exiting a big mistake The fact that Fairfax has been materially reducing its exposure to BlackBerry over the past 4 years is a big deal. And great news for shareholders. In 3 separate transactions Fairfax has completely exited its $500 million debenture investment. Fairfax continues to hold its common share position, which today has a market value of $113 million. This holding is a market to market holding for Fairfax (so the significant losses have already been reflected in the financial statements over the years). Today, BlackBerry is Fairfax’s #24 largest equity holding at 0.6% of the equity portfolio (of $20 billion). BlackBerry is now a tiny investment for Fairfax. Fairfax shareholders can now put the BlackBerry investment behind them. Mistakes Mistakes are a fact of life when it comes to investing. What to do when you recognize you made one? Made sure you learn the lesson - so you do not repeat the mistake. And you probably exit the position and move on. What was Fairfax’s mistake with BlackBerry? When Fairfax made their initial investment in BlackBerry way back in 2010, they completely misjudged: The quality of the management team in place. The prospects for the company. Like with AbitibiBowater, when things got worse they then: Significantly increased the size of their investment. Thought they were a turnaround shop - and could ‘fix’ BlackBerry. I call this investing framework ’old Fairfax.’ Turning a lemon into lemonade Value investing framework: Right around 2018, it looks to me like Fairfax made important changes to their value investing framework. I have recently written about this so I won’t repeat myself. Bottom line, since 2018 Fairfax has been allocating capital exceptionally well. Shifting capital from poor investments to better opportunities: Exiting the BlackBerry debenture investment has freed up $500 million in capital that has been re-invested into better opportunities where Fairfax should be able to earn a much higher rate of return. When Fairfax does this it is like they are creating a new, growing income stream. Freeing up management’s time: The senior team at Fairfax has also exited a big headache. They can now spend their time on much more productive endevours. That is also a big win for shareholders. This move improves the overall quality and earnings power of the equity holdings. Over time this will result in more value creation for shareholders. Fairfax detractors They can’t let go. Yes, Fairfax has made some big mistakes. BlackBerry was a big one. But guess what... Fairfax has made many, many more great investments. And they appear to have stopped making big mistakes back in 2018. For the past 6.5 years, the team at Fairfax has been hitting the ball out of the park. At the same time they have been fixing ALL of the mistakes made in the past. Exiting the BlackBerry debenture is just one of many examples. As a result of this (and other developments), Fairfax has been transformed as a company. But some investors still refuse to see it - their dislike of the company is still too intense. Crazy but true. ————— Comments from Prem from Fairfax’s 2023AR: "That brings me to a major mea culpa! We began investing in Blackberry in 2010 and helped John Chen become CEO in November 2013 by investing $500 million in a convertible debenture at the same time. Blackberry had come down from $148 per share (down 95%) and had $10 billion in sales. I joined the Board in 2013. Our total investment in BlackBerry early in 2014 was $1.375 billion ($500 million in the convertible and $787 million in common shares). "When John joined the company, BlackBerry reported a loss of $1.0 billion – in one quarter and most analysts were predicting bankruptcy! BlackBerry was indeed in difficulty! John saved the company by quickly bringing it to breakeven on a cash basis and then on a net income basis. No CEO worked harder but, unfortunately, John could not make it grow! Revenues for the year ending February 2023 were $656 million. John retired from the company at the end of his contract on November 14, 2023 and I retired from the Board on February 15, 2024. We got our money back on our convertible ($167 million in 2020, $183 million in 2023 and $150 million in 2024) plus cumulative interest income of approximately $200 million. Our common stock position as of 2023 ($162 million or 8% of the company) which was acquired at a cost of $17.16 per share was valued on our balance sheet at $3.54 per share. Another horrendous investment by your Chairman. To make matters worse, imagine if we had invested it in the FAANG stocks! The opportunity cost to you our shareholder was huge! Please don’t do the calculation! No technology investment for me!"

-

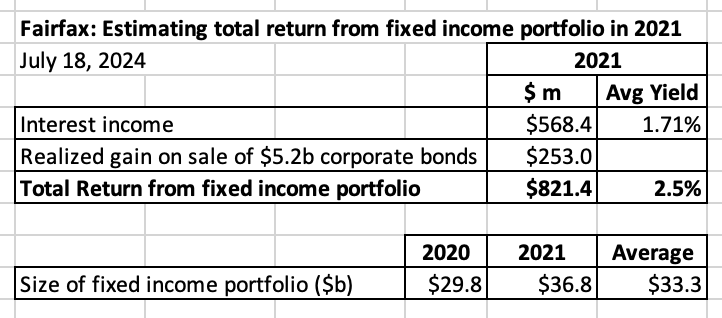

Corporate Bonds – 2021 – Value Investing 101 / Protecting the Balance Sheet Below is the next instalment in my review of asset sales at Fairfax from the past 7 years. My goal is to provide some additional insight into the transformation that has happened at Fairfax (especially earnings). And help us better understand what might be coming in the future. Please share your thoughts. ————— To set the table, below is a prescient quote from Warren Buffett from Berkshire Hathaway’s 2020AR: “And bonds are not the place to be these days. Can you believe that the income recently available from a 10-year U.S. Treasury bond – the yield was 0.93% at yearend – had fallen 94% from the 15.8% yield available in September 1981? In certain large and important countries, such as Germany and Japan, investors earn a negative return on trillions of dollars of sovereign debt. Fixed-income investors worldwide – whether pension funds, insurance companies or retirees – face a bleak future.” ————— In 2021, Fairfax sold $5.2 billion of corporate bonds and realized a $253 million gain. The bonds were sold at a yield of approximately 1%. Most of the bonds had been purchased in March/April of 2020 during the Covid panic which caused credit spreads (and yields) to spike temporarily. The greatest bond bubble in history 2020 and 2021, bonds were in the blow off top (bubble high) part of the greatest bull market in history. Like .com stocks in 1999, bonds were selling at crazy high prices (well over their intrinsic value) - and their yields were at record low levels. In 2020 and 2021, there was no ‘margin of safety’ when purchasing bonds, especially those of longer duration. Instead, there was actually a very high probability that future returns for investors would be terrible. In 2020 and 2021 the risks of owning bonds had never been higher. Like past bubbles, when it came to bonds, Mr. Market had lost its mind. Value investing 101 Value investing is the central framework used by Fairfax and is used in both of its core businesses: insurance and investments (equities and bonds). What is a value investor to do when a historic bubble is blowing ever bigger? A value investor sells. And that is what Fairfax did in 2021 when they sold $5.2 billion in corporate bonds. It was a brilliant move. And highly contrarian; especially for a P/C insurance company. Protect the balance sheet And they did another thing that was even better. They moved the average duration of their fixed income portfolio to 1.2 years (they had been doing this for years). They did this to protect their balance sheet - protect it from significant losses should bond yields unexpectedly rise. Who else was thinking along the same lines as Fairfax? Some guy named Warren Buffett who manages a company called Berkshire Hathaway. What about other P/C insurance companies? Most P/C insurance companies have a stated policy of matching the average duration of their fixed income portfolio with the average duration of their insurance liabilities. This makes good sense - almost all of the time. But it is a terrible thing to do in an historic bond bubble. So why did they continue to do it? Even when it was obviously becoming more and more risky? The institutional imperative What is the institutional imperative? Warren Buffett defines it in Berkshire Hathaway’s 1990AR: “the tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so.” Pretty much all P/C insurance companies match the average duration of their bond portfolio with the average duration of their insurance liabilities. What would be the consequences if this strategy blew up? There would be none - because they were all doing it. As a result they were all safe. Who could have known? What happened to P/C insurance companies when the bond bubble popped in 2022? When the bond bubble popped in 2022, the balance sheets of most P/C insurance companies got shredded - for many companies their book value fell 10% to 15% - for some it was more. The management teams at most P/C insurance companies had completely dropped the ball. Their risk management had been terrible. They were reckless and their shareholders would now pay a steep price. And what happened to the management teams? Nothing, of course. ‘Who could have known’ they all collectively said. How about Fairfax? Book value at Fairfax increased in 2022. Fairfax shielded their shareholders from billions in losses. That is outstanding risk management. Narrative Fairfax realized a nice gain of $253 million on their sale of $5.2 billion in corporate bonds in 2021. More importantly, by shortening the average duration of their fixed income portfolio to 1.2 years in late 2011, they protect their balance sheet - and shielded the company and investors from billions in losses. This is a great example of exceptional risk management. This is just another of many recent examples of how Fairfax has been running circles around the management teams of other P/C insurance companies in recent years. Fairfax’s growth in book value over the past 5 years has left peers in the dust. It is a testament to the benefits of active management. And value investing. And superior management. It is also an example of the benefit of having a majority/controlling shareholder. It’s not a fluke that it was all the publicly traded P/C insurance companies that were blindly following the herd over the cliff in 2020 and 2021. ———— Interest income update Interest income at Fairfax bottomed out at $568.4 million in 2021. When you add in the gain from the sale of $5.2 billion in corporate bonds, the total return on the fixed income portfolio was $821.4 million or 2.5% (calculated off the average size of $33.3 billion). Given the exceptionally low average duration of of the fixed income portfolio of 1.2 years at Dec 31, 2021, the earn though over the past 2.5 years from spiking interest rates has been much quicker for Fairfax than pretty much all other P/C insurance companies. As of Q1, 2024, interest income at Fairfax has ballooned to about $570 million per quarter and the yield on the fixed income portfolio (now $46 billion in size) is now 5%. It is amazing what the fixed income team at Fairfax has accomplished over the past 3 years. ———— From Fairfax’s 2021 Annual Report: “During 2021, we sold $5.2 billion in corporate bonds, mainly acquired in March/April of 2020, at a yield of approximately 1%, for a gain of $253 million. At the end of 2021, our fixed income portfolio, inclusive of cash and short term treasuries, which effectively comprised 72% of our investment portfolio, had a very short duration of approximately 1.2 years and an average rating of AA-.” Fairfax 2021AR

-