Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@nwoodman , I agree, Eurobank does look cheap today. I think the banks in the region are selling off due to concerns about falling NIM. Having said that, Eurobank’s stock price has held up well (better than peers). My post earlier was focussed on Hellenic Bank and developments in Cyprus. There are many other interesting angles to Eurobank: 1.) What do you think Eurobank now does with capital return? Do they continue with the 50% payout that they discussed previously? - Because of the significant cash outlay involved in taking Hellenic Bank private, perhaps they do something similar to last year = 30% payout? What do you think the split will be between dividend and share repurchases? - My guess is they will try and do a dividend payout amount similar to what they did this year. Start to build a reputation as a stable, consistent dividend payer. 2.) Hellenic Bank stopped paying a dividend due to Eurobank’s take-over. They are way over capitalized. After Eurobank gets complete control, I wonder if Hellenic Bank doesn’t pay a big dividend to Eurobank - that kind of pays part of the take-out price. Hellenic Bank has been hugely profitable the past 2 years and it was largely just building on their balance sheet (yes, they did purchase CNP Cyprus). The negotiations between Eurobank, Demetra amd Logicom must have been intense. The other big stake was purchased from the Cyprus Union of Bank Employees (ETYK), the Cyprus Bank Employees Welfare Fund, the Cyprus Bank Employees Health Fund and the Financial Sector Provident Fund. This negotiation was likely equally intense. But once it was done, it seemed to be the catalyst to get the agreement with Demetra and Logicom done. Impressive that Eurobank was able to get this deal done. It will be interesting to see how quickly they move to rightsize the three companies (Eurobank Cyprus, Hellenic Bank and CNP Cypus). They will likely be very thoughtful in what they do. My guess is they see enormous potential in what they have in Cyprus. 3.) Expansion of wealth management at Eurobank. This will be something to watch. Perhaps this is where we see future acquisitions. Combined with a slow and steady build-out - like they have been doing this year. 4.) The partnership between Eurobank and Fairfax certainly looks like it is working for both companies. It allows the Eurobank team to think long term when making decisions. It also allows them to take calculated risks to grow their business. Very unusual for a publicly traded company - and especially a bank - in that region. I hope it continues to cement at Fairfax (and Hamblin Watsa) the importance of management when they make new equity investments. I think Fairfax ‘gets it’ more today than they ever have.

-

@Redskin212 , I think the success they had with Bank of Ireland is what led them to invest in Eurobank. The difference is Ireland rebounded from their property crisis relatively quickly. So Fairfax’s investment in Bank of Ireland also popped higher pretty quick. Eurobank has played out very differently. Greece did not quickly rebound from its depression (after Fairfax made their initial investment). And Fairfax’s initial investment in Eurobank got completely wiped out by the ECB. But that has all changed over the past 4 years. I wonder if Eurobank is now Fairfax’s best stock investment ever (in terms of total gain). Even after the big gain, it’s interesting/informative that Fairfax has not sold down its Eurobank position. Fairfax likely views the stock as still being significantly undervalued (especially given the current set-up with Hellenic Bank acquisition).

-

@intothebreach , i appreciate the comment. You are welcome. At the end of the day, i post on topics that are of interest / timely / that i want to lean more about. Posting the articles to the board really helps me to focus (I want to get them close to being accurate). And the comments from other board members often provide some additional insights which improves our understanding even more. It really has been a virtuous circle over the past 4 years.

-

Look at gambling today. Now that it has been legalized, has its usage/penetration among the population increased? Yup. And by a lot. And it is just getting started. The question I have: If you legalize drugs will we not see usage spike? Especially with young adults / kids? Legalizing it would simply be a science experiment. And for it to work we are counting on government getting it right. Culturally, much of North America is NOT aligned with legalizing drugs (way too uptight). The tail risks look massive to me - and they are skewed to the downside.

-

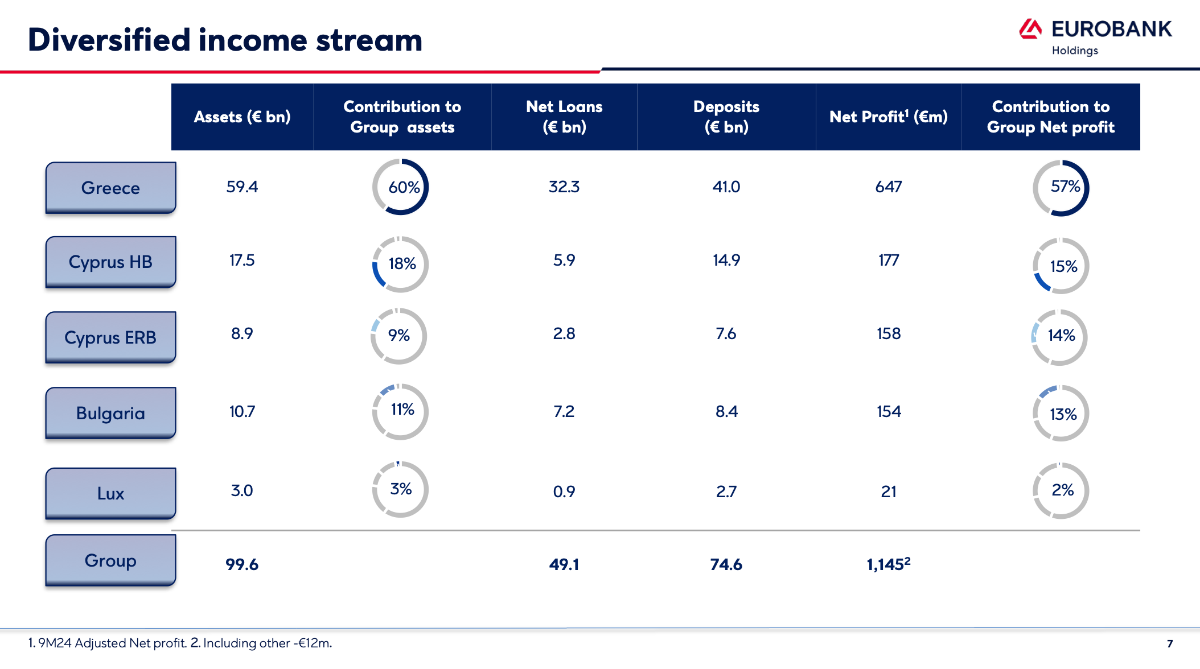

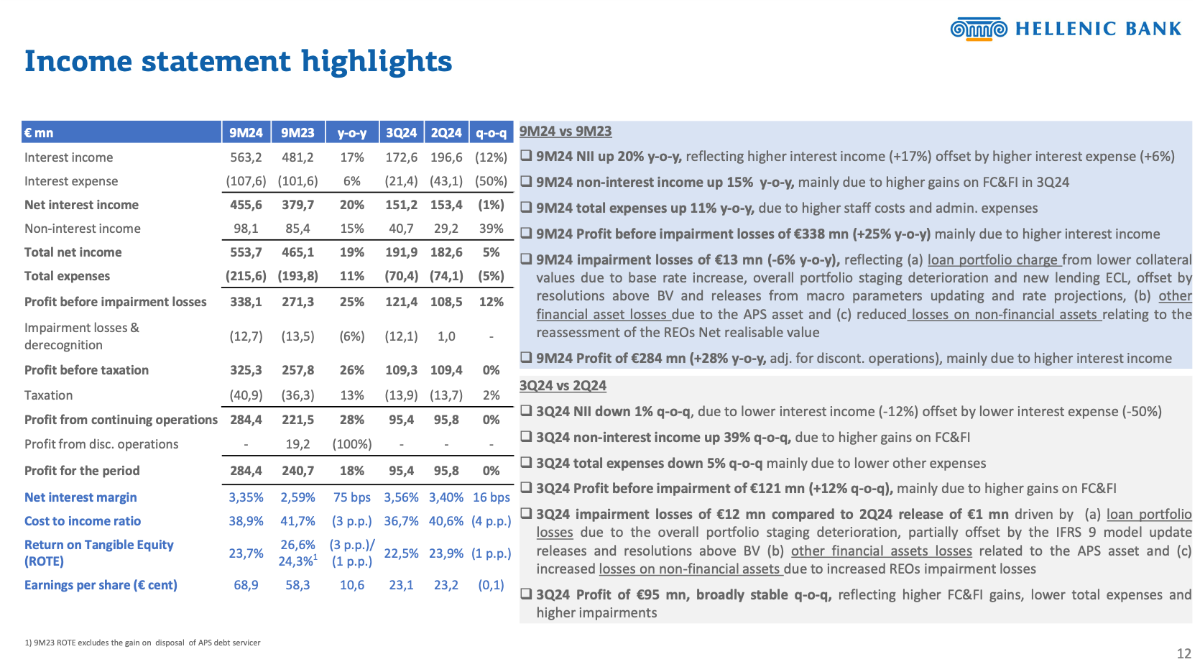

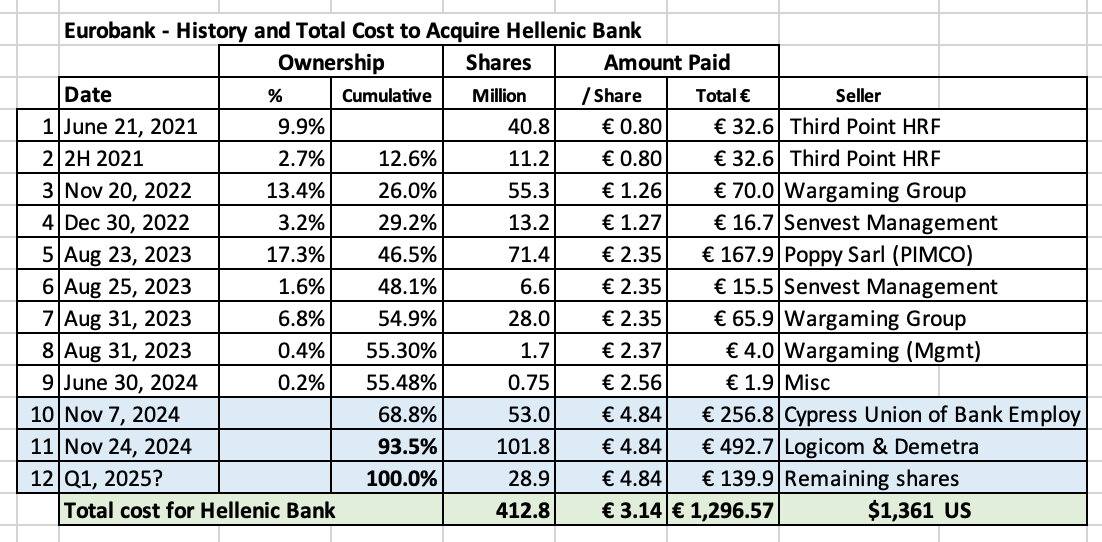

Eurobank Update - The Hellenic Bank acquisition is a game changer Introduction Over the past 3.9 years, the market value of Fairfax’s position in Eurobank has grown from $900 million to $2.7 billion, an increase of $1.8 billion or 204%, which is a CAGR = 33%. Yes, that has been exceptional performance. As a result, Eurobank has been a home run investment for Fairfax and its investors over the past 4 years. Fairfax’s total equity portfolio has a market value of about $20 billion. With a market value of $2.7 billion, Eurobank is a 14% position for Fairfax. This makes Eurobank Fairfax’s largest equity holding - by far. If your largest positions perform well then your total portfolio return will probably also do well. Despite its stellar performance the past 4 years, Eurobank looks like it is very well positioned to continue to perform well in the coming years. In the rest of this post we will look into the past (what happened at Eurobank?) and then we will pivot and look into the future (what does the future of Eurobank look like?). What happened at Eurobank? Two things happened at Eurobank to spike its earnings and stock price: The management team at Eurobank continued to execute exceptionally well. Their strategic decisions over the past 6 years have been especially good. External forces in Greece shifted from major headwinds to major tailwinds: The EU abandoned its zero interest rate regime. Higher interest rates spiked interest income for banks. Politically, Greece pivoted hard to more of a capitalist/free market economy. Pro-business reforms have resulted in Greece having one of the top performing economies in Europe in recent years and this is expected to continue in the coming years. Greece’s economy has gone from depression to rapid growth. The result of these two developments saw Eurobank deliver a 378% return to investors over the past 3.9 years. What does the future of Eurobank look like? After such a stellar run, is Eurobank’s stock now priced for perfection? My guess is no. For a couple of important reasons: Greece’s economy is poised to do well in the coming years. Eurobank’s management team is excellent. That is a great combination. Importantly, the management team at Eurobank has already set the table for Eurobank to continue to deliver strong results in the coming years. What did they do? A bunch of things. In the rest of this post we are going to focus on one of their strategic decisions - the purchase of Hellenic Bank in Cyprus. Cypress Scale matters in banking. A lot. Eurobank is very well positioned in Greece and Bulgaria. In 2023, Eurobank made the decision to exit Serbia, and sell its bank (that had #8 market share). Smart. Eurobank also had a presence in Cyprus (the # 3 bank). Eurobank decided Cyprus was a country it wanted to grow in. So in 2021 it acquired a small stake in Hellenic Bank, the #2 bank in Cyprus. Over 2022 and 2023, Eurobank increased its ownership in Hellenic Bank to 55%. And in the last two weeks, to 94%. The takeover of Hellenic Bank will be completed in Q1 2025. This is a game changer for Eurobank. Eurobank Cyprus and Hellenic Bank make Eurobank a powerhouse in banking in Cyprus. In 2024, Hellenic Bank also expanded into insurance with the acquisition of CNP Cyprus. But we are getting ahead of ourselves. Let’s review the Hellenic Bank acquisition. Hellenic Bank Eurobank obtained full control of Eurobank on November 25, 2024 with the takeout of the 2 remaining large shareholders. Eurobank acquires full control of Hellenic Bank https://knews.kathimerini.com.cy/en/business/eurobank-acquires-full-control-of-hellenic-bank Price paid matters. Eurobank will pay a total of about $1.36 billion to acquire 100% of Hellenic Bank. It has been a 4-year journey. The table below shows each of the moves made by the management team at Eurobank. Slow. Steady. Methodical. How much is Hellenic Bank earning? Hellenic Bank is poised to earn about $772 million total in 2023 and 2024 = $386 million on average. Eurobank is paying about 3.36 x expected average 2023/2024 earnings. That is exceptional value. Is Hellenic Bank over earning? We will get our answer to this question in the coming years. Interest income is likely over earning (with the ECB cutting interest rates). But Eurobank has many levers to pull to significantly grow profits in other areas. What are some tailwinds to profitability of Hellenic Bank/Eurobank Cypress? 1.) Grow the top line - Hellenic bank has a number of things it can do to grow its top line. There is a significant opportunity to grow Hellenic Bank’s loan book. Expansion into insurance In April 2024, Hellenic Bank announced it was making a major expansion into insurance (life and P/C) in Cyprus with the purchase of CNP Cyprus for €182 million. This deal is expected to close in Q1 2025. Acquisition of CNP Cyprus solidifies Hellenic Bank's dominance in Cypriot insurance market https://knews.kathimerini.com.cy/en/business/€182m-deal-marks-hellenic-s-strategic-move-into-insurance-sector Hellenic Bank has lots of excess capital – this looks like a smart move. This move also fits very well with Eurobank/Fairfax (Fairfax owns Eurolife, one of the largest life insurance companies in Greece). Slide from Hellenic Bank’s Q3 2024 earnings presentation 2.) Reduce expenses - merge Eurobank Cyprus and Hellenic Bank On November 26, 2024 it was reported that Eurobank will be merging Hellenic Bank with Eurobank Cyprus. This will be a multi-year process and should lead to a stronger bank in Cyprus. Over time, it should also result in significant cost savings. Remember, there is also a third leg to this stool - and that is Hellenic Bank’s insurance acquisition. There are really three businesses to be integrated in Cyprus: Eurobank Cyprus, Hellenic Bank and CNP Cyprus. Hellenic Bank to merge with Eurobank following €1.2 billion deal https://cyprus-mail.com/2024/11/26/hellenic-bank-to-merge-with-eurobank-following-e1-2-billion-deal/ 3.) Synergies The synergies from combining the three businesses should be significant. We already mentioned cost savings. But importantly, there will also be cross-selling opportunities which should result in revenue growth. Summary Eurobank has made a number of significant strategic decisions in recent years. The biggest was the decision to aggressively expand in Cyprus with the purchase of Hellenic Bank. With the announcements the past couple of weeks, all of their hard work is quickly coming together. When Eurobank reports 2024 year-end results next year, we will also get their 2025 business plan. It will be very interesting to see the integration plans for their operations in Cyprus and what the new business/profit outlook is. Cyprus will likely drive a big part of the growth (top and bottom line) for Eurobank in the coming years. But the real lesson of Hellenic Bank is the impact that an exceptional management team can have on business results. Especially over a couple of years. And in a region like Greece (coming out of a depression). The management team at Eurobank looks like they are the real deal. It will be interesting to see what they do in the coming years. ————— Hellenic Bank - Q3-2024 Earnings Presentation https://www.hellenicbank.com/-/media/hbc/announcements/2024/november/9m/9m24_fr-presentation_final.pdf ————— Slide from Eurobank’s Q3-2024 Earnings Presentation The slide below shows the balance sheet of Eurobank and the impact of adding Hellenic Bank. (Eurobank consolidated Hellenic Bank in Q3, 2024, with a control position of 55.5%. In Q1, 2025, its control position will increase to 93.5%.) ————— Presentation on Eurobank by CEO Fokion Karavias in April 2024 Eurobank: A turnaround story https://www.ivey.uwo.ca/media/hznli5um/keynote-fokion-karavias.pdf

-

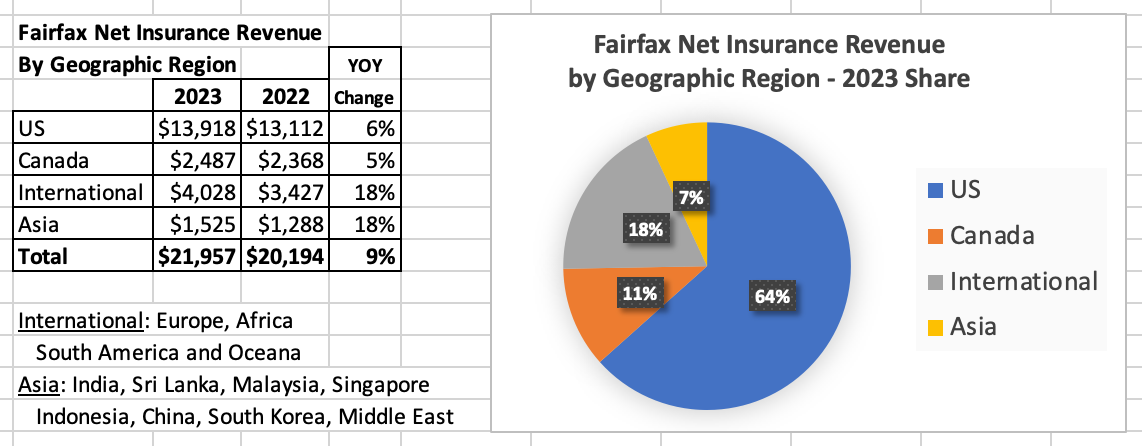

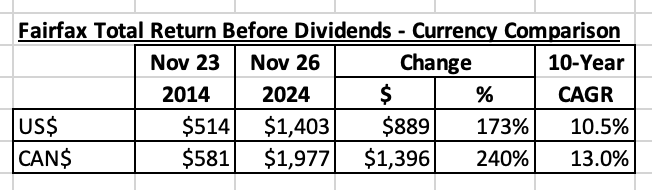

Well, if you are a Canadian investor, you now have another really good reason to own Fairfax - protection from a weak Canadian $. Truth be told, the Canadian $ has been weak for a decade. But the weakness appears to be picking up a little steam. What does 'protection' look like? Over the past decade, US investors have made a solid return owning Fairfax. The 10-year CAGR has been 10.5% (not including dividends). Canadian investors? They have earned a much better return. The 10-year CAGR has been 13% (before dividends). Fairfax has provided Canadian investors with solid protection from an ever-weakening Canadian $. How does Fairfax offer protection? Only 11% of Fairfax's insurance revenues come from Canada. But the news is even better. Guess where Fairfax's biggest revenue region is? At 64%, it is the US. Fairfax is well positioned to benefit from a strong US economy in the coming years. Fairfax has many tailwinds right now. For a Canadian investor, we can add yet another - it provides solid protection from a weak C$. PS: if I was a fund manager in Canada and I HAD to own Canadian stocks (i.e. Canadian equity fund)... why would I not own Fairfax?

-

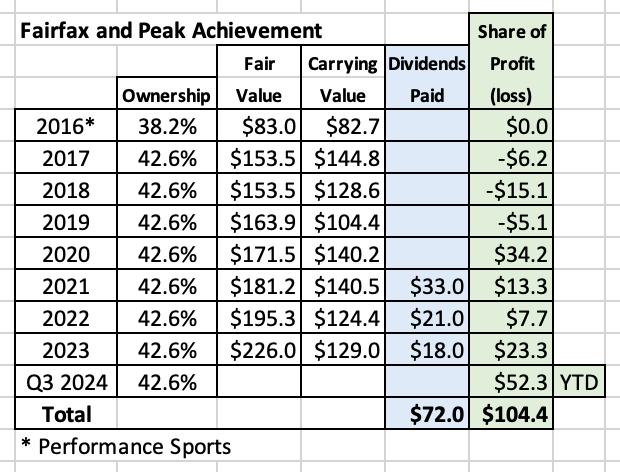

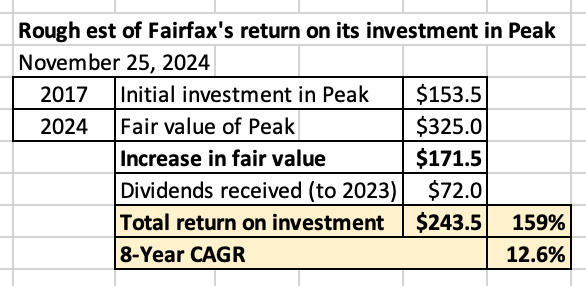

Peak Achievement Athletics - The rebuild has been completed On February 28, 2017, Fairfax partnered with Paul Desmarais III and his team at Sagard Holdings to purchase Performance Sports Group out of bankruptcy for total proceeds of US$575 million. The company was subsequently renamed Peak Achievement Athletics. Performance Sports Group was a leading developer and manufacturer of sports equipment: Hockey - Bauer (#1 player) https://ca.bauer.com Baseball - Easton (#3 player) Lacrosse - Cascade and Maverik (combined, #1 player?) https://cascademaverik.com Performance Sports Group completes sale of substantially all of its assets to investor group led by Sagard and Fairfax Financial - Article from Feb 27, 2017 https://www.torys.com/en/work/2016/10/52382aeb-7e85-42dd-903c-309be9bb261a Why did Performance Sports Group go into bankruptcy? The primary problem wasn’t the business. It was the management team in place at the time - their decisions were terrible (changing their distribution strategy in Canada for Bauer and grossly overpaying for Easton are just two examples). Click the link below for details. Behind the bankruptcy of Performance Sports Group - Article from November 10, 2016 https://www.nhbr.com/behind-the-bankruptcy-of-performance-sports-group/#:~:text=Graeme%20Roustan%2C%20who%20blames%20the,time%20to%20arrange%20a%20sale. Details of the partnership In 2017, Fairfax and Sagard each invested $154 million (C$204 million). Each company held a 42.6% equity interest and 50% of the voting rights in Peak. The investment was accounted for using the equity method. It was not disclosed who owned the remaining 14.8% equity position in Peak. It is interesting that Performance Sports was purchased for total consideration of $575 million and Fairfax and Sagard only invested a total of $308 million (for their 85.2% interest). Who is Sagard Holdings? Sagard is a global multi-strategy alternative asset management firm active in venture capital, private equity, private credit, and real estate. https://www.sagard.com Sagard was launched in 2002 by the Desmarais family, which controls Montreal-based financial services giant Power Corp. of Canada. The aim was to invest in entrepreneurs and support the growth of middle-market businesses there. Fairfax has built out a wonderful capital allocation platform When deciding what to do with its $69 billion investment portfolio, Fairfax has build out an exceptionally diverse platform within the company that allows it to go to where the opportunity is at any given point in time - in public or private markets. In the case of Peak, Fairfax invested in the private market and like an alternative asset management firm. Fairfax’s partnership with Sagard is another good example of the many partnerships/relationships that Fairfax has been patiently building out over their 38 years of existence as a company. The benefits of what Fairfax has created are far reaching (future deal flow being just one example). The key take-away is Fairfax is extremely flexible with its capital allocation framework. This should lead to better diversification (lower portfolio risk) and better total returns over time. Today, Fairfax’s capability when it comes to capital allocation (structure, expertise, partnerships) is unique in the P/C insurance industry. It has become an important sustainable competitive advantage for the company. Back to our story. Strengthen Easton - 2020 In October of 2020, the Easton unit of Peak was acquired by Rawlings Sporting Goods. Easton was the #3 player in baseball and Rawlings was the clear #1 player. In the deal, Peak received $65 million in cash and a 28% stake in Rawlings. Importantly, this deal was done when Covid was raging and demand for all sports equipment (baseball, hockey and lacrosse) had fallen dramatically. Peak got a timely cash infusion and ownership in a much larger, stronger baseball company. The turnaround at Peak The turnaround at Peak took a number of years. Covid likely stalled their transformation by a couple of years. But over time, Peak returned to profitability. This can be seen from the distributions that started to happen to the two partners, Fairfax and Sagard. Below are the numbers that Fairfax has reported over the years for its investment in Peak. The sale of Rawlings stake - 2024 In Q2-2024, Peak sold its minority position in Rawlings Sporting Goods. A sale price was not disclosed. However, in Q2-2024, Sagard reported receiving a dividend of $60 million from Peak. Fairfax reported YTD September 30, 2024, share of profit of associated of $52 million, and said the elevated amount was due to the sale of Rawlings. Fairfax takes out partner Sagard There were rumours that Peak was being shopped. It is interesting that Fairfax ended up being the buyer. From an article in the Globe and Mail on August 24, 2024: “Sagard and Fairfax acquired Bauer out of bankruptcy in 2017 for US$575-million and are targeting a US$800-million exit, according to one of the sources. Bauer’s EBITDA is just more than US$100-million annually, the source said.” https://www.theglobeandmail.com/business/article-ccm-bauer-true-hockey-sale/#:~:text=Sagard%20and%20Fairfax%20acquired%20Bauer,to%20one%20of%20the%20sources. On September 30, 2024, Peak announced that Fairfax had bought out partner Sagard. The purchase will see Fairfax will double their ownership stake in Peak from 42.6% to 85.2%. Fairfax paid $325 million for Sagard’s 42.6% stake. This values Peak at $763 million. Power Corp (owner of Sagard) provided the financial details of the transaction: “On September 30, 2024, Peak announced that Fairfax will acquire Sagard’s 42.6% interest in Peak. On close of the transaction, the Corporation expects proceeds of approximately US$325 million, and to recognize a gain in net earnings of approximately US$195 million. The transaction is expected to close in the fourth quarter of 2024, subject to customary closing conditions.” Why did Fairfax buy out Sagard? Here are some thoughts: Fairfax likes the management team. Fairfax likes the long term return potential of the business. Culture wise, Peak is a good fit for Fairfax. The takeout of Sagard is following a very familiar playbook for Fairfax. Over the past 4 years, the majority of their capital allocation decisions has involved them buying more of stuff they already own. This is a very effective strategy for the following three reasons: The investment they are making falls into their circle of competence. They are able to value the asset well, allowing them to buy with a margin of safety. Growing the size of current investments allows them to concentrate in their best ideas. This is capital allocation 101 - simple, smart and effective. The kind of capital allocation preached by Warren Buffett, Charlie Munger and Peter Lynch. Here is what Wade Burton (President, Chief Investment Officer, Hamblin Watsa) had to say on Fairfax’s Q3-2024 earnings conference call: “We did make one significant announcement in the quarter. We bought out our main partners in Peak Achievement, an athletic wear and equipment company focused on hockey and lacrosse. It is an outstanding business operating in a highly consolidated industry, well run by Ed Kinnaly and his team, incredible track record, and we paid a fair price. We think we will make a very good return over the long run for our shareholders, and importantly, Ed runs the company very much in tune with the Fairfax culture.” “Looking back over the last two years, we’ve made three significant long term equity investments, one in Meadow Dairy, a dominant milk ingredients company in the U.K. that is doing very well; another in Sleep Country, a dominant mattress distributor and retailer in Canada; and now a third, Peak, a dominant sporting goods company focused on hockey and lacrosse. All immediately are or will contribute to our earnings, and we believe all will continue to contribute more and more as their businesses progress.” The non-insurance consolidated companies income stream at Fairfax gets bigger Fairfax continues to make material additions to its collection of non-insurance consolidated company holdings. In 2022, it took Recipe private. In 2023, it purchased Meadow Foods. In 2024, it took Sleep Country private. Peak was an associate holding for Fairfax. On close, Peak will become a consolidated holding. These additions are materially growing the size of this income stream for Fairfax. Here is what Jennifer Allen (Vice President, Chief Financial Officer) had to say on Fairfax’s Q3-2024 earnings conference call: “As Wade noted, with our recently announced Sleep Country and Peak Achievement transactions, we expect the operating income from our non- insurance companies reporting segment will grow in the future periods, reflecting the operating income diversity these investments will add to the segment.” Is a sizeable investment gain coming for Fairfax at close? Sagard is reporting that they expect to book an investment gain of $195 million when the deal closes. Perhaps this is what we also see from Fairfax. At December 30, 2023, Fairfax had a carrying value of $119 million for its 42.6% stake in Peak. Revaluing this to $325 million would result in a significant investment gain. How has Fairfax done with their investment in Peak? My math says Fairfax has generated a total return of about $243 million on its $154 million initial investment in Peak over the past 8 years. This is a CAGR of 12.6%. The dividends received of $72 million is to December 30, 2023. It is likely that Fairfax has received another dividend payment from Peak in 2024 (especially given the sale of their stake in Rawlings). We will likely get an update from Fairfax when they release their 2024 annual report. ————— Notes from Fairfax annual and quarterly reports: 2024 Q3 Report Consolidated share of profit of associates of $609.3 in the first nine months of 2024 principally reflected share of profit of $343.7 from Eurobank, $163.0 from Poseidon and $52.3 from Peak Achievement (principally reflecting its sale of Rawlings Sporting Goods), partially offset by share of loss of $60.1 from Sanmar Chemicals Group. 2023AR Fairfax continues to jointly own Peak Achievement with our partner, Sagard Holdings. Peak’s core brands are Bauer, the leading hockey brand, and Maverik, a leading lacrosse brand. Peak also owns a minority investment in Rawlings, which is the number one brand in baseball. Fairfax paid $154 million for its stake in Peak in 2017. Since that time, EBITDA has increased steadily in the hockey and lacrosse businesses, and Fairfax has received $72 million in dividends. Hockey participation growth continues post-pandemic and exciting developments such as Bauer’s partnership with the new Professional Women’s Hockey League are expected to drive incremental girls’ participation. More to come under CEO Ed Kinnaly’s leadership, with opportunities in direct-to-consumer, apparel and training. We carry Peak on our balance sheet at less than 5x free cash flow. 2020AR Fairfax continues to jointly own Peak Achievement with our partner, Sagard Holdings led by Paul Desmarais III. Peak’s core assets are Bauer, the leading hockey brand, and Easton, the number three manufacturing player in baseball. During 2020 Peak merged Easton with Rawlings, the clear number one manufacturer in baseball. The transaction resulted in $65 million cash paid to Peak, while retaining a 28% stake in Rawlings. Peak is now partnered with Rawlings’ controlling shareholder, Seidler Equity Partners. Fairfax recognized a $15 million gain on the sale of Easton which closed just before year end. 2017AR On March 1, 2017 the restructuring of Performance Sports Group Ltd. (‘‘PSG’’) was substantially completed after all of the assets and certain related operating liabilities of PSG were sold to an intermediate holding company (‘‘Performance Sports’’) co-owned by Fairfax and Sagard Holdings Inc. The company’s $153.5 equity investment in Performance Sports represents a voting interest of 50.0% and an equity interest of 42.6%. On April 3, 2017 Performance Sports was renamed Peak Achievement Athletics Inc. (‘‘Peak Achievement’’). 2016AR Also, early in 2017 we partnered with Paul Desmarais III and his excellent team at Sagard Capital to purchase Performance Sports. Performance Sports is the owner of the leading names in hockey, baseball and lacrosse equipment: Bauer, Easton and Cascade. ————— Notes from Power Corp’s annual and quarterly reports: Power Corp Q3, 2024 Interim Report Peak: Sagard held a 42.6% equity interest and a 50% voting interest in Peak at September 30, 2024 (same as at December 31, 2023). Peak designs, develops and commercializes sports equipment and apparel for ice hockey and lacrosse under iconic brands including Bauer. The Corporation’s investment is accounted for using the equity method. During the second quarter of 2024, Peak disposed of its minority interest in Rawlings Sporting Goods Company Inc. (Rawlings), a leading brand in baseball. In July 2024, Sagard received a distribution of US$60 million from Peak. On September 30, 2024, Peak announced that Fairfax will acquire Sagard’s 42.6% interest in Peak. On close of the transaction, the Corporation expects proceeds of approximately US$325 million, and to recognize a gain in net earnings of approximately US$195 million. The transaction is expected to close in the fourth quarter of 2024, subject to customary closing conditions. Power Corp 2017AR On February 27, 2017, Peak Achievement Athletics Inc. (Peak), an acquisition vehicle jointly controlled by Sagard Holdings and Fairfax Financial Holdings Limited, completed the acquisition of the assets of Performance Sports Group, Ltd. for total consideration of US$575 million. Peak designs and markets sports equipment and apparel for ice hockey, baseball, softball and lacrosse under iconic brands including Bauer and Easton. At December 31, 2017, the Corporation had invested $204 million (US$154 million) in Peak. Sagard Holdings holds a 42.6% equity interest and 50% of the voting rights in Peak. The Corporation’s investment is accounted for using the equity method. ——————

-

@glider3834, thanks for bringing this forward. Ki had kind of fallen off my radar. Yes, it certainly looks like they are getting ready for something…. ————— 20TH MAY 2024 Ki welcomes Jan Christiansen as Chief Financial Officer Ki is excited to have Jan on board to set us up for long-term success. Jan’s role will centre around leading the growing financial function for Ki as well as being a key driver across transformation projects that will shape the strategic direction of the business. Previously to joining Ki, Jan garnered a wealth of experience in financial services businesses across the globe. Most notably he spent 20 years with Fairfax, Ki‘s lead shareholder, including 14 years as Chief Financial Officer for the Odyssey Group. Jan feels that “Ki’s unique value proposition is a once-in-a-lifetime chance to help shape the strategic direction of a business with seemingly endless possibilities. I find the culture at Ki to be very special. The positive atmosphere is contagious and inspires creative thinking, something I believe is critical to our success”.

-

The Less-Efficient Market Hypothesis by Cliff Asness

Viking replied to Viking's topic in General Discussion

It blows me away the quality of material that is available today to help/educate small investors. And of course, education is one of the keys to unlocking a great life. It is yet another example of how much better off we are today compared to when i was getting started back in the late 1980’s. Education opportunities are amazing (written/video). Cost have come way down (especially for those who do it on their own). Choices (broad based index funds) now allow small investors to outperform the majority of professional advisers without doing any work (that is nuts). Tax free/deferred accounts (also nuts). The end result is much higher after-tax returns. It’s like an incremental $500,000 just dropped on the lap of the average investor - versus what they would have earned if they were starting out 40 years ago. But here is the really interesting thing. Most people will largely miss it. Like most things in life, with investing you get out of it what you put into it. You do have to put in the work early on - and get your infrastructure set up. And build the proper financial habits, like ‘live below your means’. But once you get that done, you can largely put things on autopilot (learning one or two new things each year as your personal situation changes). We really are living in a golden age for building wealth with financial assets. Of course, young people stand to benefit the most. Because they have the most time ahead of them (thank you compounding). But there are also enormous benefits for people in their 40’s, 50’s, 60’s etc. People living past 100 is a fast growing cohort… -

“Market efficiency is a central issue in asset pricing and investment management, but while the level of efficiency is often debated, changes in that level are relatively absent from the discussion. I argue that over the past 30+ years markets have become less informationally efficient in the relative pricing of common stocks, particularly over medium horizons. I offer three hypotheses for why this has occurred, arguing that technologies such as social media are likely the biggest culprit. Looking ahead, investors willing to take the other side of these inefficiencies should rationally be rewarded with higher expected returns, but also greater risks. I conclude with some ideas to make rational, diversifying strategies easier to stick with amid a less-efficient market.” For those with a little lime on their hands and interest in the topic you have two options: Read the paper: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4942046 Listen to the podcast:

-

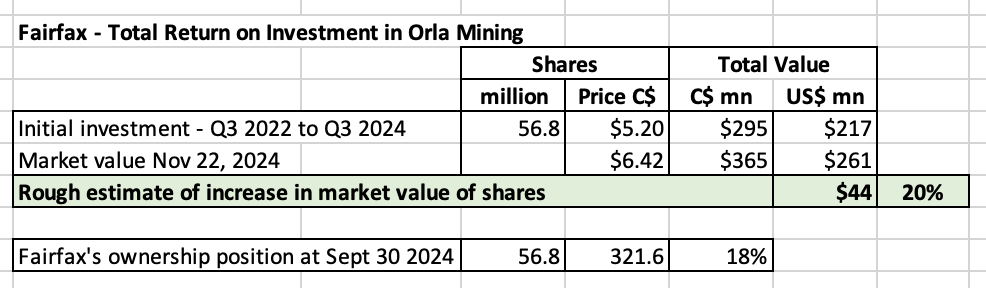

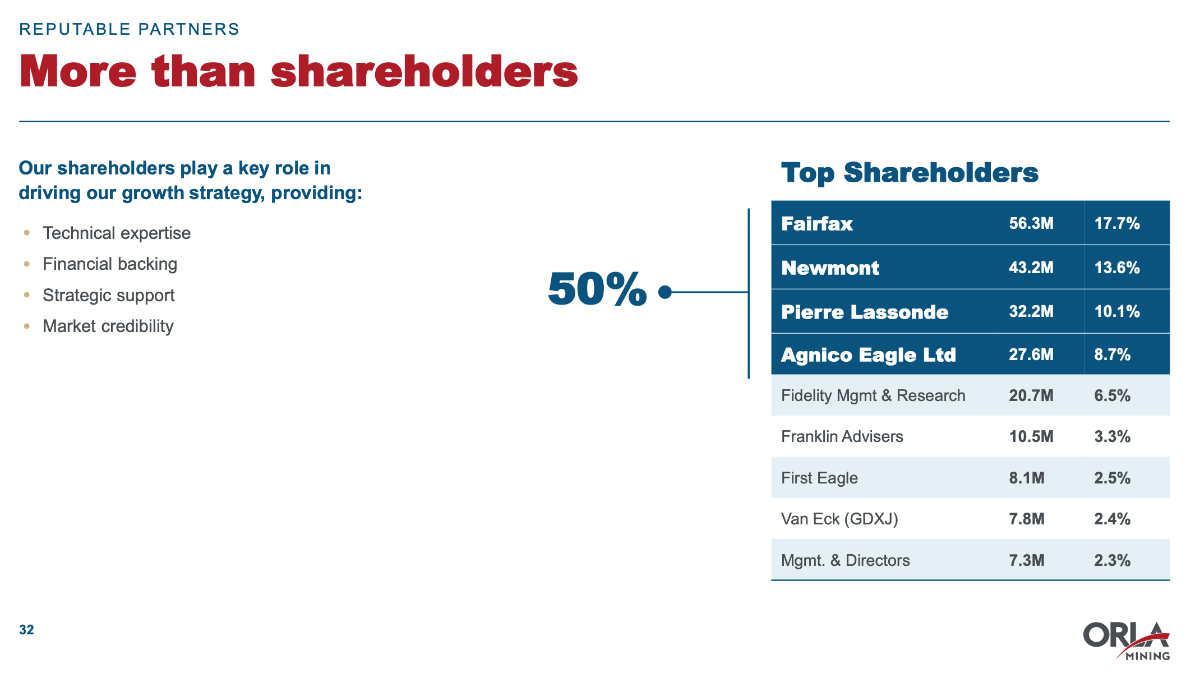

Orla Mining - Planting a Seed Orla Mining is Fairfax’s newest large resource/commodity investment. Fairfax quietly built up their position in Orla over the past 2 years (from Q3-2022 to Q3-2024), spending about $217 million. They own about 18% of the company. The investment today has a market value of US$261 million. The return on Fairfax’s investment to date has been about $44 million or 20%. The real play with this investment: That gold prices stay higher for longer. That the management team at Orla is above average. And will be able to expand the company from a single asset producer to a multi asset intermediate-sized producer. That the strong ownership structure (Fairfax, Newmont, Lassonde, Agnico Eagle) will also provide to be a competitive advantage. This allows the management team at Orla to be strategic and think long-term with its decisions. This should help ensure that the capital allocation decisions made by the management team at Orla are rational and very shareholder friendly (which is what we have seen with Orla's most recent acquisition). With its investment in Orla, Fairfax has planted another seed in its large equity portfolio. This investment has significant upside potential in the coming years. And if gold prices stay elevated, it could turn into a home run (a multi-bagger). Orla recently made a large acquisition - the Musselwhite gold mine in Canada. As part of the financing, Fairfax invested (not sure how much) in the US$200 million convertible note issuance: Coupon: 4.5%; Premium: 42%1; Term: 5 years Convertible at C$7.90 18-month non-call, callable at 130% of strike thereafter Warrant: 0.66x warrant exercisable at C$11.50 – Five-year term from closing This is likely a significant increase in the size of Fairfax’s investment in Orla Mining. The purchase of Musselwhite looks like another solid move by the Orla management team. There appears to be significant optionality to the purchase (significant opportunity for resource growth, which is part of the Pierre Lasonde playbook). Who is Orla Mining? Orla Mining Ltd. is a Vancouver-based company that acquires, explores, develops, and operates mineral properties to produce gold, silver, zinc, lead, and copper: Orla Mining's projects include: Camino Rojo: A 100% owned, operating oxide heap leach mine in Zacatecas, Mexico South Railroad: A feasibility-stage heap leach project in Nevada Cerro Quema: A pre-feasibility-stage heap leach project in Panama Musselwhite Gold Mine: An acquired project in Ontario, Canada CEO: is Jason Simpson, who has over 27 years of experience in mining engineering, project construction, and operations leadership. Non-Executive Chairman, Director: Mr. Jeannes served as President and Chief Executive Officer of Goldcorp Inc. from 2009 until April 2016. Orla recently announced a large acquisition: the Musselwhite Gold Mine Strategic expanansion into Canada. No upfront equity dilution, supported by cornerstone shareholders. Takes advantage of significant disconnect between forward and consensus gold prices. Significant opportunity for resource growth. https://orlamining.com/site/assets/files/6118/orla_acquires_musselwhite_nov_18_2024.pdf Bet on the jockey/partnering with outstanding investors It should be noted that Fairfax is not blindly throwing darts with their resource/commodity investments. They are partnering with other highly successful people / investors - some of whom have extraordinary long term track records. With Orla, Fairfax is partnering with Pierre Lassonde who is ‘recognized as one of Canada’s foremost experts in the area of mining and precious metals.’ Lassonde co-founded Franco-Nevada in 1985. Fairfax is also partnered with Lassonde with its investment in Foran Mining, a copper mining project in Canada. Jurisdiction The vast majority of the production for Fairfax’s resource/commodity investments is located in North America. This is a much lower risk jurisdiction than other parts of the world. My guess is this is not a fluke. All of Orla’s mines are located in North America.

-

@Castanza , that was one of my favourite posts of the year. It resonated so much because it was a very similar playbook to what me and my wife did to build our grub stake when we were young. I was trying to explain this to my son the other day - that we would likely be able to do the same thing today (he was talking about how ‘tough’ it is for some of his young friends today).

-

The fact that Markel had the opportunity to take out Allied World but passed was likely an inflection point for both companies. Wonderful for Fairfax. Big mistake for Markel. Why Markel passed (or why Allied World said no thanks) would likely make a very interesting story. I thought it would be interesting to calculate about how much Allied is delivering to Fairfax today…(in terms of underwriting and the return of from its investment portfolio) it has been Fairfax’s top performing insurance business for two years running. Its performance has been top tier - simply amazing. I remember the cat losses the year they bought Allied - Fairfax was very unlucky with the timing of the purchase. But Allied certainly has delivered the last couple of years. I had a chance to talk to the guy running Allied at Fairfax’s 2023 AGM (the dog and pony show before the AGM) - he was a class act.

-

@nwoodman, great summary. Thanks for sharing. Bottom line, quality insurance companies should continue to do well in 2025. Except most don’t view Fairfax’s insurance business as high quality. And that is what creates the opportunity.

-

My guess is with Trump we are entering uncharted waters (at least in terms of the last 75 years or so) in terms of what a President will try to do. And people want change. So my guess is he will get a lot of rope, especially early. I think we are likely going to get a lot of different ideas/actions. Kind of like a bunch of science experiments all happening at the same time - where we aren’t really sure how they are all going to work out (individually or collectively). I agree. I think there is a risk inflation could surprise to the upside looking out 12 to 24 months. Except i also think Trump will not tolerate a Fed that does not do what he wants (another science experiment). Bond vigilante's? Like a game of ‘whack-a-mole’, Trump and his team will not sit idly by. But the US seems to want change. I think Trump is going to deliver - in spades. I am cheering for him and the US. I hope it works out / goes as planned. At the end of the day, we want people/countries to succeed. And perhaps there are parts of his plan that other countries can use to their advantage. But the next round of elections are only 2 years away… so pitter patter he better get atter. And i think he will.

-

@Xerxes Hopefully there are a lot of people on this board who have been able to make a little money on Fairfax's amazing 4-year run. And yes, the run we have seen in 2024 has been epic (after how much it had already gone up in 2021, 2022 and 2023). The crazy thing is the stock is still cheap. Yes, not as cheap as it was... but still cheap. Why is it still cheap? 1.) Its past performance (last 4 years), measured by change in BVPS, has been best in class among P/C insurance companies. 2.) Its P/C insurance businesses are better quality than is generally understood. 3.) Its investment portfolio is poised to delivering a return of +7.5% per year, which is exceptional. 4.) As a result, the company is poised to deliver ROE of 15% for each of the next 3 years. 5.) Its management team has been executing very well over the past 5 or 6 years. Its capital allocation has been exceptional (insurance and investments). This suggests ROE should continue to be very strong looking out 4 or more years. Yet, despite the historic increase, the stock continues to trade below peers (P/BV and PE). Given its past performance, outlook and strong management team, should Fairfax not trade at a premium to peers? The only reason to say 'no' is because it hasn't historically. But that isn't true. For many years, Fairfax traded at a significant premium to peers. Most investors just either don't know this, or they have forgotten. Fairfax has morphed from a turnaround to a value play. It is now morphing right in front of everyone's eyes into a quality play. (That is called multiple expansion for those of you who are not paying attention.) As Fairfax demonstrates that it is indeed a high quality company, it deserves to trade at a higher multiple. And the longer it continues to outperform, the better the multiple it should trade at. This process could run for years. Three things drive a stock price: Earnings Multiple Share count All three are working in Fairfax's favour today. Of the three, multiple expansion is the rocket fuel to the stock price. Just ask a company called Apple - multiple expansion happened continuously over an 8 year period.

-

@gfp I agree. And I think that is what makes using 'macro' as a core input pretty much a losing proposition for most investors. I think there are times when paying attention to macro matters - like when we get to historic extremes (like the 2006/07 housing bubble). I don't think that is where we are today.

-

@73 Reds , there is an easy solution to the problem you have highlighted... and it has been what governments have been doing for hundreds/thousands of years... and that is to inflate it away. I don't think it is all that complicated. Who are the losers? Savers/lenders. Who are the winners? Owners of assets - pretty much everything, excluding fixed income. That is bullish for stocks moving forward. Also bullish for commodities. Real estate (housing). And that is what we have seen over the past decade. Asset prices (in general) have been on fire. And I think the US has just elected a president who is likely to enact policies that could accelerate this trend (if inflation accelerates, my guess is he will do his best to not let the Fed increase rates). It really is a super interesting set up. We could get some pretty wicked volatility - which would be normal when you enter uncharted territory. "Everyone has a plan until they get punched in the face." Mike Tyson - modern day philosopher

-

@73 Reds , my crystal ball is about as good as the next person. Here in Canada, stocks have underperformed for a long, long time. So a 23% move in one year is nothing crazy in my mind. And in the US, if you get lower interest rates, lower taxes, less regulation, return of animal spirits (more business investment), acceleration in onshoring production of goods, and deficit spending from the government… how do stocks not go higher? So i am mildly optimistic for stock returns over the next year (XIC.TO and VOO). I would not be surprised to see a melt-up in stocks. Not my base case. But a possibility. Of course there are watch-outs, like there are every year. Geopolitical would be one. Trump doing something nuts would be another. Super high deficit spending by Western governments would be another - although this is likely more a 2026 or 2027 risk. Perhaps the biggest risk might be a resurgence in inflation later in 2025 or 2026 - this could be a big one because people now hate inflation - and the hand has just been over the flame, so the reaction to a resurgence in inflation from people (and bond/financial markets) could be dramatic. Bottom line, important to monitor. Bit nothing IMHO flashing red today. And looking further out, if Canada elects a Conservative government in October, 2025, that could release animal spirits in the Canadian economy (there are so many important things a new government could do to improve the economy). That would bode well for Canadian stocks for 2026. We could easily see a couple of years of above average returns for Canadian stocks.

-

Fairfax is up 52% + dividend = 54% VOO is up 26% + dividend = 27% XIC.TO is up 21% + dividend = 23% Making money in 2024 has been like shooting fish in a barrel. Congratulations to all those investors who bought pretty much anything - because that is about all it took to do well this year. And i say that with all due respect…

-

Well, at least this is good news for Recipe and their +1,000 restaurants in Canada. Does Prem have Trudeau’s ear? “The government is proposing that the GST/HST be fully and temporarily relieved on holiday essentials, like groceries, restaurant meals, drinks, snacks, children’s clothing, and gifts, from December 14, 2024, to February 15, 2025.” The GST on restaurant meals in Canada is 5%. More for provinces with the HST (harmonized federal and provincial taxes). So this is a meaningful reduction. - https://www.canada.ca/en/department-finance/news/2024/11/more-money-in-your-pocket-a-tax-break-for-all-canadians.html# The current federal Liberal government has to be the worst federal government in Canadian history - at least in my lifetime. And we have had some bad ones. The current $250 cheque per adult + 2 month tax break (on a few things) is just the latest in their bat shit crazy management of the Canadian economy, especially over the past 6 or 7 years. I have tried to keep away from politics - but this Liberal government just keeps setting new lows. I am completely dumbfounded by what they say and do. Fortunately, Canada is less than 12 months away from a federal election - my only hope is that Trudeau stays on as leader of the Liberals. PS: My family will now be getting cheques for 5 x $250 = $1,250. Money we do not need. I suppose i should be celebrating…

-

@modiva , over my investing career I have always been comfortable with cash / cash equivalents. I flex my cash position up at times (when i like the risk/reward set-up). And i flex it back down at times (when i don’t like the risk reward set-up). It continues to amaze me how often ‘once in every 10 or 20 year’ investments come along (often one or two comes along every year). But to capitalize, you often need to have cash on hand. Today my cash weighting is about 15%. If markets continue to rip higher, I will probably increase my cash weighting to 20%. In terms of ‘safe’ assets, when it comes to equities, I think broad based ETF’s/index funds like VOO and XIC.TO fit. But only if you are a long term investor and ok with volatility, sometimes extreme volatility. About 50% of my portfolio is in broad based index funds. I am a new convert to this asset class, making my first purchases about a year ago. So far, I love it. I am also going to be doing some digging to see if I can find a balanced ETF/index fund that is 60% equities and 40% fixed income. My wife is VERY risk averse. A 100% stock ETF/index fund is not a good fit for her (should I no longer be around). So i want to find a fund (perhaps 2) that is a good fit for her and shift some of her assets into it. Just so she knows what to do if I get hit by a bus one day. If we get a melt-up in stocks, i like the idea of shifting into a balanced fund. I think this is also what Boggle did with his portfolio. My views on risk and concentration are evolving. Age and situation are definitely factors. As usual, i am trying to be inquisitive and open minded. Rational. And action oriented. Try stuff, see how I feel, make any necessary course corrections. For me its a pretty dynamic process.

-

@nwoodman, my problem is i am not an accountant. So it takes me some time (and lots of questions to others on the board) to get some things figured out. But we do get there eventually. As always, thanks for the help.

-

What i find very interesting is how a person is wired when it comes to things like risk management and portfolio concentration etc largely comes from their life experiences. The people who lived through the great depression (or people who have lost everything) are a great example. The chances of total loss might be small. But if the consequences are going to be severe... My guess is most people think they are being rational when it comes to risk management. More likely, they are unknowingly betting that something really bad doesn’t happen. For most people it won’t. And that will be confirmation for them that they were right. Even though they were actually wrong. They just got lucky. It is such a fascinating topic.

-

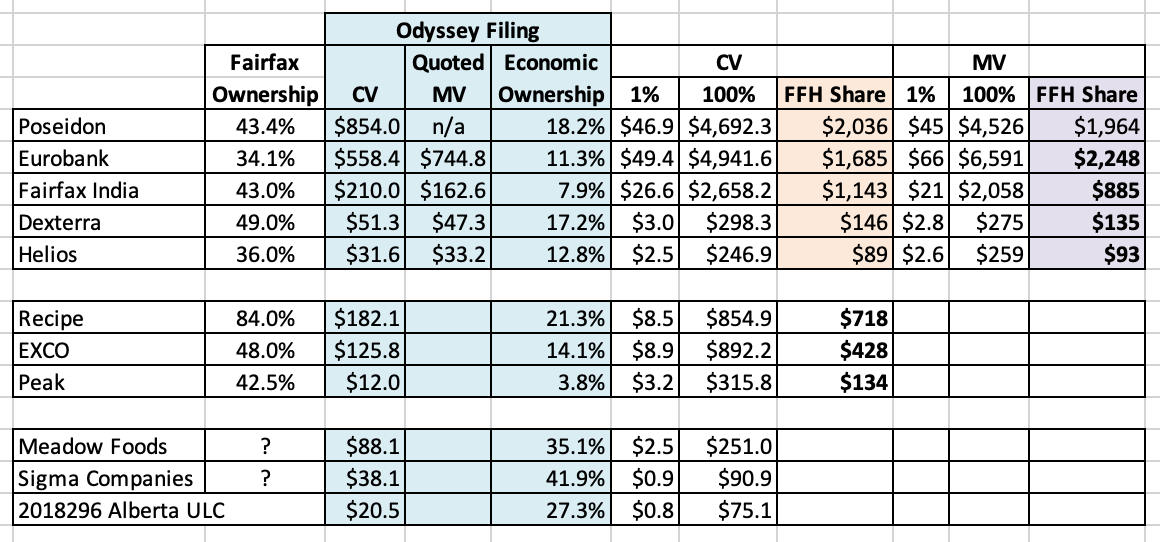

@glider3834 , this makes sense. When Fairfax reports their equity holdings in the AR, when they report non-insurance consolidated holdings they have a zero value for 'other'. It makes sense that is where AGT should be captured... and it looks like it is. Solves a riddle. Another question the Odyssey summary gives us is the approximate total value for Meadow Foods = $250 million (carrying value). I don't think we have ever been told how much Fairfax owns today. On the Q3 conference call, Wade Burton called out Meadow Foods as one of the large private investments over the past 2 years (along with Sleep country and Peak). It's interesting... when running my numbers, the carrying value that Odyssey reports (using US GAAP) did not match up with what Fairfax reports (using IFRS 17) for lots of the holdings. But the market values kind of did match up for most holdings. Which actually makes sense.

.png.0968168f6934ceeb3646afb9a0333372.png)