Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

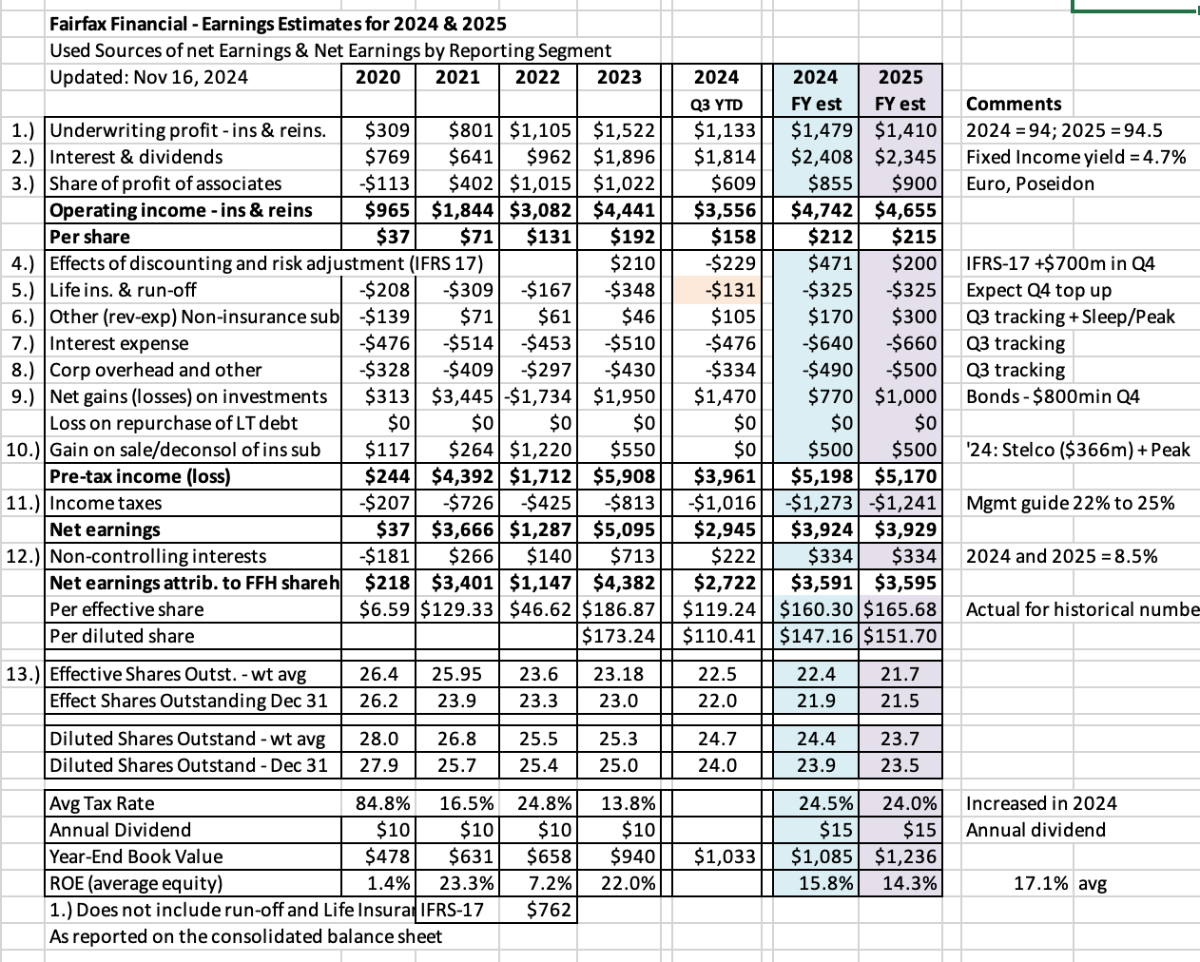

@Dazel , my last earnings update was mid-November. My guess then was basic earnings would come in around $160/share. I think $160 to $165/share is a reasonable number to use as a 'normalized' level of earnings for Fairfax today. There will be lots of puts and takes in Q4 (some of these have not been incorporated into my mid-Nov update); - do we see growth resume in net premiums at Odyssey and Brit? - spike in interest rates further out on the curve will likely be a modest headwind (unrealized losses on bonds > IFRS impact on insurance liabilities). - mark to market investment gains = $200 million? - Stelco sale = $366 million gain - Peak revaluation = ? gain - AGT Food Ingredients sale of rail business = ? gain - currency will be a headwind, perhaps meaningful (US$ strength) - adverse development at runoff of $150 to $200 million? - tax rate has been a headwind (22 to 25% guide, from low 20%) - fall in shares outstanding is a tailwind Bottom line, my guess is we get a good quarter.

-

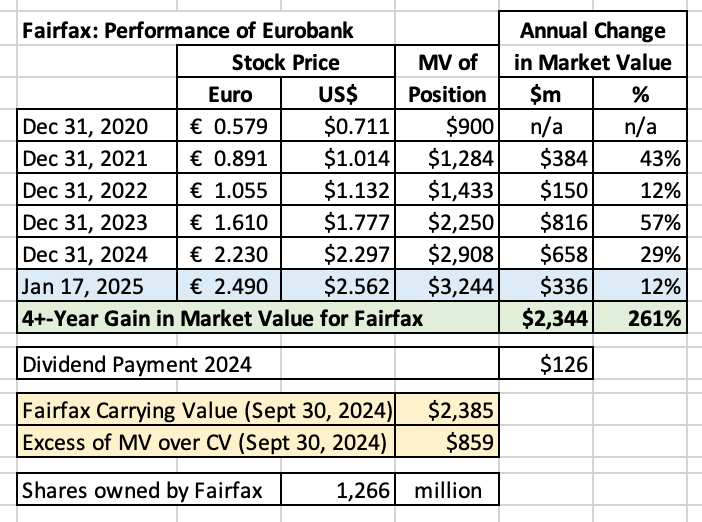

@nwoodman , got it! Thanks for the explanation. In terms of how much of Eurobank that Fairfax owns, perhaps we can use the dividend payment as a guide. Fairfax received 34.6% of the total dividend payment ($128/370). From Fairfax's Q3 earnings report. "On July 31, 2024 Eurobank paid a dividend of approximately $370 (€342). The company’s share of that dividend was approximately $128 (€118), which will be recorded in the company's consolidated financial reporting in the third quarter of 2024 as a reduction of Eurobank's carrying value under the equity method of accounting."

-

@nwoodman, thanks for highlighting magnitude... US$200 million is a meaningful amount. At what point would something like this require Fairfax to update its carrying value on Eurobank (to their selling price)? That would trigger a massive unrealized gain. I wonder if this also ties into capital return at Eurobank moving forward. We will find out shortly what Eurobank has planned (for 2024 earnings): Continue with dividend Buy back stock Perhaps Eurobank wants to buy back stock. Perhaps the Greek regulator signalled that Fairfax would need to get their ownership position below 33% before approving a buyback. It is nice that Fairfax was able wait a year to do this - Eurobank's stock is much higher.

-

I think the comparisons between Berkshire Hathaway (1980's/1990's version) and Fairfax are relevant but only at a very high level - kind of as a 'theoretical' thought exercise: Use P/C business model: access leverage provided by float. Structure: Small head office - handles capital allocation. Decentralized - operating companies run the businesses. Need quality companies (insurance and non-insurance)/strong management. Capital allocation: not restricted to bonds. This is an enormously powerful set up for a moderately sized/smallish company. Like Berkshire Hathaway in the 1980's and 1990's. And Fairfax today. What is interesting is how much Fairfax today differs from Berkshire Hathaway (1980's/1990's version). The big difference is how they do capital allocation - Fairfax has a very different approach today than the younger Berkshire Hathaway. My view is when it comes to capital allocation Fairfax's style today is much more like Henry Singleton's (in that it is unconstrained). Of course, Fairfax is executing very differently than what Singleton did at Teledyne back in the day (because the companies and the opportunity set are very different). Another big difference is Berkshire Hathaway has always been a conglomerate with a P/C insurance business. Fairfax has remained primarily a P/C insurance company. Bottom line, Fairfax has been compounding capital at an exceptional rate for the past 4 years. For many reasons, they look very well positioned to continue to deliver exceptional results/returns in the coming years ( @Dazel 's version 3.0). We could see a decade of outperformance from Fairfax that resembles the outperformance of a much younger Berkshire Hathaway.

-

Today, investors in Fairfax are getting a trifecta of benefits. 1.) As per your numbers above, total earnings from investments are growing at around 7.5% per year. Yes, float/leverage magnify the benefits of this rate of return for Fairfax. But two more important things have been happening in recent years. They need to be added to your total figures above: 2.) Takeout of minority partners in insurance. - This has the effect of increasing the amount of your numbers that accrue to common shareholders. - Others on this board have stated that taking out minority shareholders in insurance is like doing a share buyback. 3.) Meaningful share buybacks - This has the effect of increasing the amount - per share - to 1.) + 2.) above. Per share numbers pop meaningfully higher. The total is getting bigger. The amount of the total that accrues to common shareholders is getting bigger. To cap it off, the per share total that accrues to common shareholders is even bigger. Each of these three activities are additive in their impact/benefit to Fairfax. Bottom line, Fairfax is doing three things at the same time that are all increasing per share value for shareholders. I think it is really hard for analysts/investors to fully grasp what Fairfax is doing right now with capital allocation. These activities are very low risk. And together, they enable Fairfax to deliver a conservative mid-teens ROE. For Fairfax, it is like shooting fish in a barrel. In the current environment there are few values in equity or private markets. The fact that Fairfax is able to deploy a significant amount of capital in such low-risk / solid return activities is impressive. That is the beauty of taking on minority partners when they made their big insurance acquisitions (plus the sale of 9.9% of Odyssey to buy back 2 million shares at $500). Now that they have limited opportunities to redeploy near record earnings into equities that can simply instead use the funds to takeout their minority partners. This is a great example of how the management team at Fairfax is thinking long term. Sometimes it takes investors years to fully grasp what they are doing. We will get a bear market in stocks at some point in the next couple of years… So Fairfax will get a wonderful opportunity to invest a significant amount in equities in the future. They are being very disciplined and opportunistic. The senior team at Fairfax have been putting on a clinic the past 4+ years in how to do capital allocation. Yet, their stock continues to trade at a multiple that is well below peers. Love it. I would love to see them do more of the same in 2025 (continue to buy-out minority partners and buy back another 4 to 5% of shares outstanding).

-

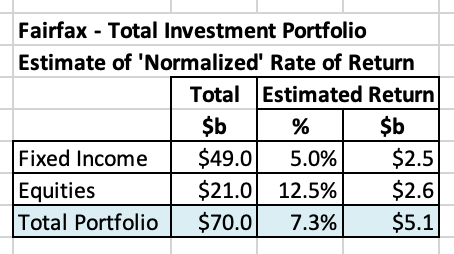

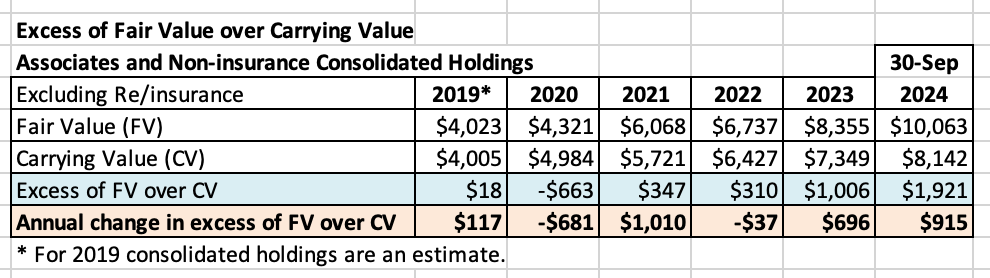

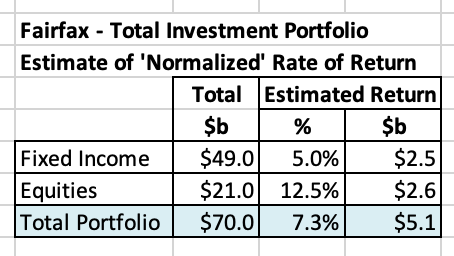

Fairfax is once again earning its historical rate of return on its investment portfolio = 7.5% to 8% per year range. Below is the very straightforward math for Fairfax to deliver a 7.3% return on its total investment portfolio. The return on the investment portfolio is lumpy, for a number of reasons. But what analysts/investors tend to do is: Focus exclusively on accounting. Quarterly estimates. This leads them to largely ignore the parts that are volatile year-to-year (investment gains being one example). This is a dumb way to try and analyze a company like Fairfax. But understandable (whatever you forecast any one year - let along quarterly - is sure to be wrong). As a result they are likely materially underestimating the increase in business value that is happening at Fairfax today. Bad analysis is generally not a good way to value a stock. But that doesn't stop analysts and investors from trying. Using this kind of 'logic' is probably the primary reason many investors missed out on the big run in Berkshire Hathaway's stock in the 1980's and 1990's: They grossly underestimated the economic earnings that were rolling in each year. They also underestimated the effects of compounding (when those economic earnings are invested rationally). I am looking in the mirror when I write this - I followed Berkshire Hathaway closely for years... and also missed out on making the big money for the two basic reasons I state above. The key to investing is not to make mistakes... it is to not keep repeating them. Chronically underestimating the underlying economic performance of a company like Fairfax is not being conservative. It is bad/flawed analysis. The fundamental problem is likely a lack of understanding on the part of analysts/investors of the difference between accounting earnings and economic earnings for a company like Fairfax. Of the two, economic earnings are the more important (and the more difficult one to calculate). ----------- The key income streams that generate the economic return on the investment portfolio for Fairfax are: 1.) Interest and dividends 2.) Share of profit of associates 3.) Investment gains (both realized and unrealized), including those from asset sales and asset revaluations 4.) Pre-tax net income earned from non-insurance consolidated companies Bucket 3.) is, of course, the most volatile. This list above captures the 'accounting' income streams. But there are more. 5.) Excess of FV over CV for non-insurance associate and consolidated companies Fairfax actually gives us this number each quarter. It is meaningful ($1.9 billion at September 30, 2024). This should make it easy for analysts/investors. (But most instead fumble the football.) 6.) The fair value mark for some of the equity holdings are much too low. Fairfax India Grivalia Hospitality 7.) At the same time, some of the equity holdings of Fairfax India are much too low (yes, this is a big of a mind-bender). BIAL 8.) Phantom holdings Fairfax has a number of holdings that have disappeared from view. The poster child here is perhaps AGT Food and Ingredients. What has happened at this company since Fairfax took it private. What is its carrying value? What is its fair value? My guess is it is a good example of where accounting value is underestimating its economic value - perhaps meaningfully. Meadow Foods is probably another holding to watch in the coming years. 9.) Private holdings masquerading as marke to market holdings Fairfax has about $2.1 billion dollars invested in private/limited partnerships like BDT, ShawKwei, JAB Holdings. These show up in the market to market bucket but the holdings of these companies are generally not publicly traded companies. These are more like private holdings - where value will be surfaced over time (as assets are sold/revalued). How much value is 'hiding' within these holdings, waiting to be unlocked in the coming years? 10.) Where does Eurobank's dividend payment to Fairfax show up in my 1.) to 7.) above? It is a significant number (almost as big as the total of dividends in the interest and dividend bucket). What about the dividend payments from Poseidon? Where do they hit the income statement (so we can include them in our calculation of the annual return Fairfax is earnings on its investment portfolio). This could be a $200 million per year 'income stream' for Fairfax moving forward. I am sure I am missing more important items that are generating economic returns for Fairfax each year on its investment portfolio. My point is Fairfax is currently on a glide path to earn an economic return of 7.5% to 8% (on average) on its investment portfolio on average in the coming years. But what about volatility? That's bad right? This is the kicker - if volatility returns to financial markets, my guess is Fairfax will deliver an even higher average return. They are all cashed up. And they are being very patient (with capital allocation). They are ready to pounce. Most people still think volatility is bad for Fairfax. My view is it is likely the opposite.

-

@Crip1 I think your instincts / questions are sound. My read is the US is just getting started. Trump has lots of low hanging fruit - and he is prepared and motivated. My guess is US economic/profit growth will continue to be much stronger than the rest of the world in 2025 and probably in 2026. So here area couple of thoughts: 1.) I think you might be early. Which sometimes can mean you also end up being wrong. 2.) What is the catalyst that makes your idea work? I don’t see one today. In fact, I see new headwinds forming. I actually recently kind of did the opposite of what you are thinking… I sold my holdings in XIC.TO (100% Canadian stocks) and shifted it largely to XEQT.TO (45% S&P500, 24% Canada, 31% rest of world). I also hold VO and VOO. If Canada elects a Conservative government? In my mind, that would be a catalyst - a reason to be more interested in buying Canadian stocks. But we are probably 7 to 9 months away - with a lot of unknowns. My strategy today is to have some cash to be able to take advantage of any volatility that materializes in companies/sectors I like. Bottom line, I am not trying to over think it.

-

@LC , you bring up something that is both interesting and often stated/discussed. "Most economic theory and business experience would suggest not to expect long term underwriting profitability for the industry as a whole." This might be a great example of how theory often diverges from what actually happens in the real world. I think the real question is what is actionable for an investor from this insight? There are two general ways to go in our thought exercise: 1.) Over time, the combined ratio of all P/C insurance companies will revert to 100. 2.) Over time, the CR of all P/C insurance companies will average 100, but with the following split: - the CR of low quality P/C insurance companies will average a number above 100 - the CR of high quality P/C insurance companies will average a number under 100. In the second example, low quality insurance companies will likely see higher top-line growth in soft markets (net premiums written). And high quality insurance companies will see lower top-line growth in soft markets. And vice versa. My point is I think there is a broad assumption that 'revert to 100' means all P/C insurance companies will see their CR go to 100 (and likely higher). I agree that we could see CR tick higher for high quality P/C insurance companies I am not convinced it has to go to 100 (or higher). The other important variable are reserving practices - and reserve releases. High quality P/C insurance companies have likely been building reserves in the 5-year hard market. This could buffer their reported CR in a soft market. And, of course, we will get a 'historically' bad year for catastrophes at some point in the coming years (we just don't know what year). So there will be volatility from year to year (sometimes a great deal). I am talking about a smoothed CR (perhaps over a 3 to 5 year period).

-

@Maverick47 , as I have said many times before, I am not an accountant. Like you and others on this board, I am simply trying to keep learning so I can better understand the performance and value the company. Sometimes I get it wrong - so I would really appreciate other board members letting me know when I make a mistake. (I have thick skin... what is important other than me is getting things right.) As we keep peeling the onion back another layer there are sometimes accounting peculiarities that become useful/helpful to understand. One other nuance for associate holdings that has been mentioned on the board before is there is a one quarter lag in when an associate holding reports and when Fairfax reports. Fairfax's reporting (share of profit of associates) is one quarter behind what is actually happening at the associate holding. Now I am not sure if this is true for all associate holdings but I think it is the case with Eurobank and Poseidon... PS: I am planning on digging a little more into the insurance side of Fairfax (sometime the next month or so). I know that is your specialty so I will be looking for your feedback/input

-

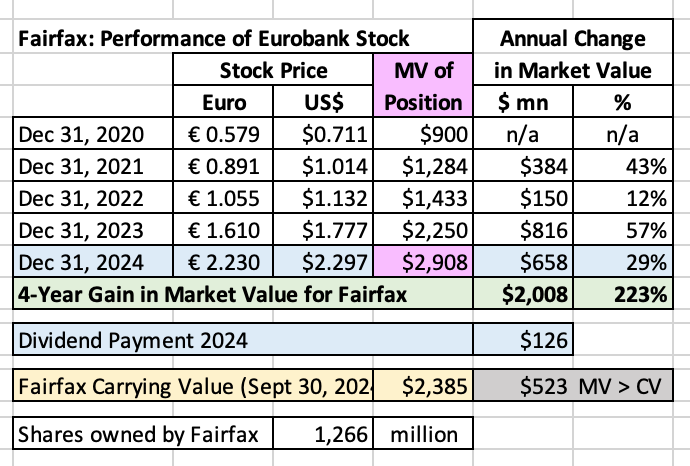

Mr. Market is starting to warm to Eurobank's purchase of Hellenic Bank. Fairfax's position in Eurobank has increase $336 million 17 days into 2025. Yes, early days. But it is a positive development. Fairfax's carrying value for Eurobank will likely come in at around $2.5 billion at December 31, 2024. That would put excess of FV over CV at about $750 million. This is economic value that is being created by Fairfax that is not being captured in accounting value: EPS, BV or ROE. Fairfax received a dividend payment from Eurobank of $126 million in 2024. Because Eurobank is an associated holding: This payment did not show up in 'interest and dividends' for Fairfax. Fairfax's carrying value for Eurobank was reduced by $126 million. Eurobank's dividend payment caused the excess of FV to CV to increase.

-

@Hoodlum The Hellenic Bank CEO presented at a bank conference (material below is from your link). It looks like there are lots of opportunities to grow top line and bottom line at Hellenic Bank - it will be a multi-year process. ---------- Meanwhile, Hellenic Bank announced this week that the acquisition of CNP Assurances will also be finalised in the first quarter of 2025. This development, the bank stated, will establish it as “a leading financial group with a strong presence in both the banking and insurance sectors in Cyprus”. “Customer service, financing growth, completing the merger, and expanding operations remain our priorities for 2025,” Louis said. What is more, he pointed out that Cyprus would serve as the group’s headquarters for expansion into the East, “where wealth is being created”. Louis added that the goal is to “promote Cyprus as an attractive base for foreign investors“. Louis also spoke about the importance of strengthening trust between banks and society. “Despite the criticism they face, banks support society and development, listening to the needs of the state and investing tangibly in the country’s future,” he said. “The banks are supporting and financing Cypriot businesses and households, with Hellenic Bank’s total lending in 2024 reaching €1.1 billion,” Louis added. However, he cautioned that lending now takes place under “a much stricter supervisory framework and demanding criteria to avoid past mistakes”. Furthermore, Louis provided commentary on the role that banks play in attracting investors. “The services sector is a significant asset that we must preserve and strengthen by ensuring stability in our tax and legal framework, which should not create uncertainty for potential investors,” he stated.

-

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

I am not an expert on all that Pollievre has planned but: - Eliminate the GST on new builds. That will be an immediate 5% reduction in cost. I think that is significant. - Unshackle oil and gas production / particularly liquefied natural gas. Energy production is a key part of the Canadian economy. - Stop demonizing capitalism stop telling Canadians that the government is the solution to their problems. - My guess is the Conservatives will be reversing many of the recent laws the Liberals have introduced that makes it pretty much impossible to develop Canada’s resources. - My guess is the rapid growth of government agencies will slow. And better accountability/governance practices will be put in place. It should be very obvious to Canadians that the Liberals can’t actually run anything. - My guess is small businesses will be valued and not treated simply as piggy banks (a vehicle for the government to extract money from). - Crime - the current laws allowing repeat offenders to skip jail (so they repeat offend) is a joke (not the funny kind). - Safe supply of drugs - this has been a mess in BC. My guess is the Conservatives will return to a more traditional approach (in terms of federal support). - Immigration - the Liberals have messed this up so badly over the past 5 years, my guess is there will be many things a Conservative government can do to get it back on the rails. The Liberals have implemented so many disastrous policies over the past 9 years the Conservatives will be busy for years correcting the mistakes. Will the Conservatives go to far? Well if they do they will only be in for 4 years. Bottom line, Canada has shifted far further to the left than people seem to realize. If we stay that way, our economic well being will continue to decline. What is worse is the drumbeat message - capitalism is evil and the government is the answer. That will be a catastrophe for my kids generation. In short, the Liberals have been a slow moving train wreck. Canada needs a big change in direction. IMHO. -

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

Just a quick update... over the weekend/past couple of days I decided a 28% cash weighting was too aggressive. I am at 15% cash today - that feels better/more appropriate. I added mostly XEQT. So essentially I flipped XIC (100% Canada) for XEQT (44% US, 24% Canada, 32% rest of world). The net result is I have materially decreased my exposure to Canada. Got my cash weighting to about where it usually sits. And increased my exposure to US and rest of world. -

@Hamburg Investor, you make a great point - "sometimes one really outperforms the others..." Investing is like driving a car on the freeway. Some days, you get stuck in a bad traffic jam. Other days, it is clear sailing. These days with Fairfax, it certainly feels like Prem and crew has an open lane, the gas pedal pressed to the metal, with a lot of open road ahead.

-

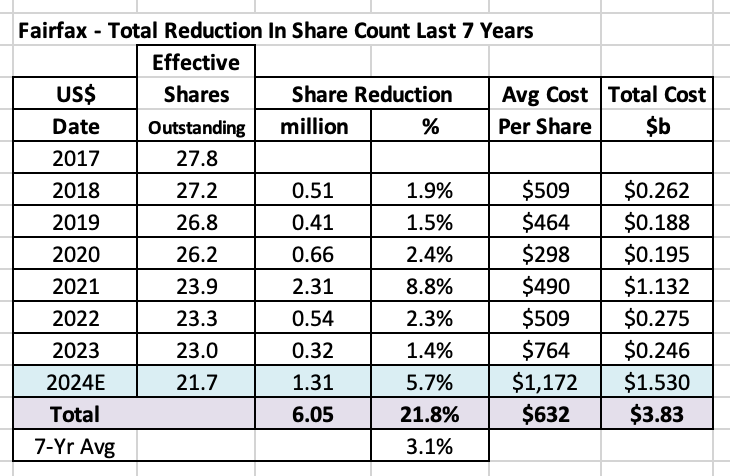

2024 Top 10 List - Part 2 5.) Asset sale - Stelco Asset sales are an important tool in Fairfax’s capital allocation toolkit. Why sell an asset? Sometimes another company - who is willing to pay up - values an asset at a much higher value than you do. This is what happened in 2024. Taking advantage of the consolidation happening in the North American steel industry, Stelco was sold to Cleveland-Cliffs at a nosebleed-high price. The timing of the sale was perfect - President-elect Trump is threatening to impose blanket 25% tariffs on Canada, which would hurt the business of a Canadian steel producer like Stelco. The sale of Stelco to Cleveland-Cliffs closed on November 1, 2024. What kind of a return did Fairfax generate from its 6-year investment in Stelco? It must have been terrible… After all, only an idiot would invest in a steel producer. That ‘investment’ has dogs with fleas written all over it. Fairfax needs to get with the program and stop investing in shit companies like Stelco. Right? Well, before we jump to any conclusions, sometimes it helps to actually look at the numbers/facts. So let’s do that. In November 2018, Fairfax invested $193 million in Stelco. Over the past 6 years, Fairfax earned a total return of $544 million from its investment in Stelco, or 282% = 6-year CAGR of 25%. Outstanding. When they report Q4, 2024 results, Fairfax is expected to book an investment gain of $366 million (pre-tax) from the sale of Stelco. The sale of Stelco is reminiscent of when Fairfax sold Resolute Forest Products in 2022 - at the peak of the lumber cycle - also for a nosebleed-high price. Over the years, asset sales have delivered considerable value to Fairfax and its shareholders. 6.) Meaningfully grow another income stream - ‘non-insurance consolidated companies’ Fairfax has 5 income streams that feed through to earnings: Underwriting profit Interest and dividend income Share of profit of associates Non-insurance consolidated companies Gains from investments (realized and unrealized) Of the 5 income streams, ‘non-insurance consolidated companies’ is by far the smallest. However, over the past 3 years, Fairfax has been materially adding to this group of holdings. 2022: Took Recipe private and significantly increased their stake in Grivalia Hospitality. 2023: Purchased Meadow Foods (UK). 2024: Purchased Sleep Country and significantly increased their stake in Peak Achievements. Beginning in 2025, like a coiled spring getting released, we should see earnings from non-insurance consolidated companies grow significantly. This will give Fairfax another large and growing income stream. From 2019 to 2023, income from ‘non-insurance consolidated companies’ averaged about $24 million per year. 2024 is estimated to come in at about $170 million. My current estimate for 2025 is $300 million. Details of two of Fairfax’s large equity investments in 2024: Sleep Country - new purchase / take private On October 1, 2024 Fairfax acquired Sleep Country for purchase consideration of $880.6 million (Cdn$1.2 billion). The purchase consideration was made up of two components: cash of $562.7 million and new non-recourse borrowings of $317.9 million. Sleep Country is a Canadian specialty sleep retailer with a national retail store network and multiple e-commerce platforms. Peak Achievements - took out partner Sagard. On September 30, 2024, Peak announced that Fairfax had bought out partner Sagard. The purchase will see Fairfax will double their ownership stake in Peak from 42.6% to 85.2%. It appears Fairfax paid total consideration $325 million for Sagard’s 42.6% stake. This values Peak at $763 million. We will get details when Fairfax reports 2024 year end results. From an accounting perspective, Peak will shift from an associate to a consolidated holding. Peak’s stable of brands includes Bauer Hockey, Cascade Lacrosse and Maverik Lacrosse. 7.) Total investment portfolio per share continues to grow mid-teens Fairfax’s total investment portfolio is estimated to finish the year at a record $70 billion, or $3,226 per share. Year-over-year, the increase in the total investment portfolio is 8.1%. On a per share basis, the increase is 14.6%. Over the past 5 years, Fairfax has increased the per share size of its investment portfolio at a CAGR of 17.3%. How much is Fairfax earning on its investment portfolio? My estimate is Fairfax earned about 7.9% on its average total investment portfolio in 2024. The average return was 10.2% in 2023. Of interest, from 2016 to 2022, Fairfax earned an average return of about 4.9% on its total investment portfolio. The big increase in the rate of return of Fairfax’s investment portfolio is being driven by much higher bond yields and a much better performing (higher quality) equity portfolio. Importantly, the big increase in return looks sustainable. Moving forward, 7.3% to 7.5% looks like a reasonable number to use as a ‘normalized’ rate of return for Fairfax’s investment portfolio. Note, for equity holdings, this includes ‘excess of fair value over carrying value’ for associate and consolidated holdings. Fixed income = 5% The 10-year US treasury is currently yielding 4.8% Equities = 12.5% The quality (measured by earnings power/management) of Fairfax’s equity portfolio (in aggregate) has improved markedly over the past 5 years. This bodes well for future returns. Sequence of returns matters. In 2024, Fairfax’s total investment portfolio per share grew to a record $3,226/share. At the same time, Fairfax is earning a very high rate of return on its investment portfolio. 8.) Increasing the amount of Fairfax’s total earnings that accrue to common shareholders Takeout of minority partners in insurance subsidiaries Not all of Fairfax’s earnings today accrue to common shareholders. This is primarily because Fairfax has minority partners in some of its P/C insurance companies. However, in recent years, given its robust earnings, Fairfax has been slowly and methodically buying out its insurance partners. These transactions increase the amount of Fairfax’s earnings that go common shareholders. In three separate transactions in 2024, Fairfax spent a total of $674.7 million to increase its ownership of its insurance businesses. These are solid uses of cash for Fairfax. The transactions are very low risk (obviously, Fairfax knows the assets) and they offer a solid rate of return (whatever was being paid to minority partners). Taking out the minority partners also simplifies Fairfax’s structure and makes the company easier to understand. Bottom line, these transactions increase the amount of Fairfax’s earnings that accrue to common shareholders - it increases their economic ownership of the company. Gulf Insurance Group - 2 transactions Increased ownership from 90% to 97.1% at a cost of $126.7 million. Annual payment of $165 million to Kipco (payment one of four, as part of its takeout in 2023). Brit Insurance On December 13, 2024, Fairfax announced that it had increased its ownership in Brit from 86.2% to 100% at a cost of $383 million. As the hard market slows, these types of transactions are an elegant way for Fairfax to continue to grow its insurance business - the part that accrues to common shareholders. 9.) Increase in excess of FV over CV Reported numbers matter a great deal. But what we care about more than accounting results is economic performance over time - because this gives us a better understanding/insight/estimate of that elusive concept called ‘intrinsic value’. Over the past 5 years, Fairfax has been materially growing out its collection of associate/consolidated equity holdings. Today, Fairfax has more than $21 billion in equity investments and more than $11 billion (53%) are now associate/consolidated holdings. The economic value (market/fair value) of these holdings has been increasing faster than their accounting or ‘carrying value.’ Fortunately, Fairfax helps us connect the dots when they report results. One example is the company’s disclosures for ‘excess of fair value over carrying value’ for non-insurance associate and consolidated holdings. In 2019, the fair value and carrying value for associate/consolidated equity holdings were both about $4 billion - the excess was a tiny $18 million. Nothing to see here. At September 30, 2024, for associate/consolidated equity holdings the fair value was $10.1 billion and the carrying value was $8.1 billion. The excess had ballooned from $18 million in 2019 to $1.9 billion ($86/share pre-tax) at September 30, 2024. Fairfax’s reported book value was understated by this amount. Over each of the past 4.75 years, excess of FV over CV has increased by an average of about $400 million per year ($18/share pre-tax). Fairfax’s reported earnings each of the past 4.75 years have been understating the true economic performance of the company. The good news is much of this value will end up in EPS and book value - but it will take time. Fairfax could sell an asset, like they did with Stelco in Q4, 2024, and this will crystallize the value (that is hiding in plain sight). Fairfax could also do something that requires an asset to get re-valued (closer to market/fair value) - we might see this with Peak Achievement and Fairfax’s takeout of partner Sagard in Q4, 2024. My current estimate is Fairfax will earn about $160/share in 2024. This excludes excess of FV over CV. Over the first 9 months of 2024, excess of fair value over carrying value increased $900 million ($41/share pre-tax). Bottom line, the performance being generated by Fairfax in 2024 is much better than what is reported by simply looking at reported earnings per share numbers. This also means Fairfax’s reported ROE is also understated. Investors need to keep this in mind when valuing the company and evaluating the performance of the management team. 10.) Significant share buybacks In 2024, Fairfax got much more aggressive on the share buyback front. In 2024 it appears Fairfax reduced effective shares outstanding by 1.3 million, or 5.7%, to 21.7 million. The cost was likely $1.53 billion = an average of $1,172 per share. From a capital allocation perspective, buying back stock was, by far, Fairfax’s largest ‘use of cash’ in 2024. The shares were purchased at a very attractive price. My estimate is Fairfax book value will finish 2024 at about $1,085/share. If we include excess of fair value over carrying value for consolidated and associate equity holdings (this is not captured in book value), Fairfax has been able to buy back shares in 2024 at an average price that is slightly more than 1 x estimated ‘adjusted’ 2024 year end book value. That is very cheap for a high quality P/C insurance company. Over the past 7 years, Fairfax has reduced effective shares outstanding by 6.05 million or 21.8%. The cost was $3.83 billion and the average price paid was $632 per share. Share repurchases over the past 7 years have delivered exceptional value to Fairfax and its shareholders. As Warren Buffett teaches us, it is the per share metrics that matter. The effect of materially reducing effective shares outstanding is to amplify the positive benefits/effects of many of the items in our Top 10 list. Here is what Warren Buffett had to say in his 1980 shareholder letter about a company using its retained earnings to buy back stock: “(We can’t resist pausing here for a short commercial. One usage of retained earnings we often greet with special enthusiasm when practiced by companies in which we have an investment interest is repurchase of their own shares. The reasoning is simple: if a fine business is selling in the market place for far less than intrinsic value, what more certain or more profitable utilization of capital can there be than significant enlargement of the interests of all owners at that bargain price? The competitive nature of corporate acquisition activity almost guarantees the payment of a full - frequently more than full price when a company buys the entire ownership of another enterprise. But the auction nature of security markets often allows finely-run companies the opportunity to purchase portions of their own businesses at a price under 50% of that needed to acquire the same earning power through the negotiated acquisition of another enterprise.)” As a result of buybacks in 2024, Fairfax shareholders now own 5.7% more of a company that has also substantially increased in value in 2024. (Note: I estimate that in Q4 Fairfax repurchased and retired 292,000 shares at an average price of $1,380.) Significant dividend increased In January 2024, Fairfax increased their dividend from $10 to $15 per share. Average stock price = $1,150 Dividend yield = 1.3% Amount spent by Fairfax = $363 million The dividend had been $10 since 2011. The increase in the dividend was important symbolically - it signalled to investors that Fairfax had indeed turned the corner as a company. From Fairfax’s Press Release Jan 3, 2024: “Given Fairfax’s substantial growth since it inaugurated a US$10 per share annual dividend 14 years ago, and given Fairfax’s current position of foreseeing strong earnings for the next few years based on insurance company underwriting income, locked-in interest and dividend income and income from associates, we felt it was appropriate to raise our annual dividend this year to US$15 per share, and we believe that this should be a sustainable level,” said Prem Watsa, Chairman and Chief Executive Officer of Fairfax. Total payout yield Buybacks = 5.7% Dividend = 1.3% Fairfax’s total payout yield was 7.0% in 2024. Significant. ————— Miscellaneos Insurance: Digit Insurance - In May of 2024, Digit successfully completed its IPO (at 274/share). At Dec 31, the company had a market value of $3.4 billion (316.55/share). Ki Insurance - Ki was launched as an insurance startup by Brit in 2020. Blackstone is an equity partner. It is being reported that Ki has now achieved critical mass and is large enough that beginning in 2025 it will operate as a standalone company within Fairfax. Investments: Bangalore International Airport (BIAL) - In December 2024, at a cost of $250 million, Fairfax India increased its equity interest in BIAL from 64% to 74%. BIAL is the third largest and one of the fastest growing airports in India. AGT Food Ingredients - In November 2024, AGT sold its shoreline rail and bulk handling infrastructure to GCM Grosvenor. From the news release: “This sale returns significant capital to AGT…” We should get the financial details resulting from this sale when Fairfax reports year-end results. Increase in debt. Fairfax has always used a modest amount of debt to grow shareholder value over the long term. As strong earnings have been generated in 2024 (and shareholders’ equity has increased), Fairfax has also taken on more debt. Not a concern. But something to continue to monitor. Preferred share holdings were reduced by $250 million. Funded with C$ borrowings (average interest rate of about 5%). Runoff: Continues to see sizeable adverse prior year reserve development top-ups each year, with the majority typically happening in Q4. Total amount was $259.4 in 2023. “…principally related to latent hazard claims stemming from recent incremental increases in litigation activity and its associated costs.” From Fairfax’s 2023AR. Not a concern (it is what it is). But it is something to continue to monitor. Personnel Changes: Prem Watsa steps away from conference calls: Beginning with the Q1 call in May, 2024, conference calls are now handled by the trio of Peter Clarke (President and COO), Jen Allen (CFO) and Wade Burton (President and CIO, Hamblin Watsa). In June 2024, Gobi Athappan was appointed Chairman and CEO of Fairfax Asia (following the passing of his father, Ramaswamy Athappan).

-

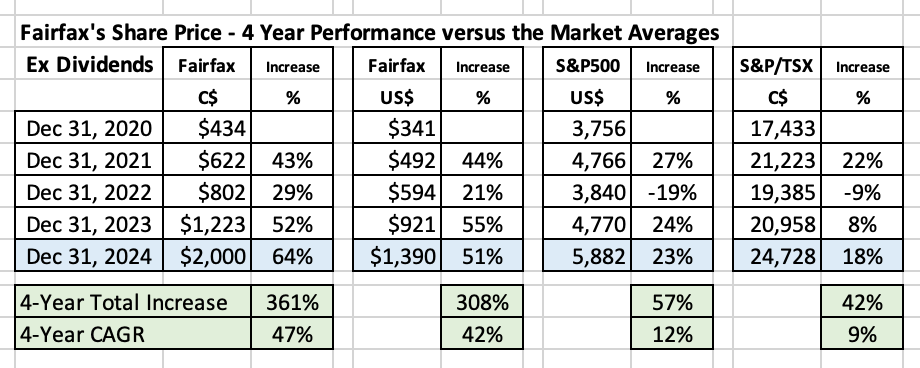

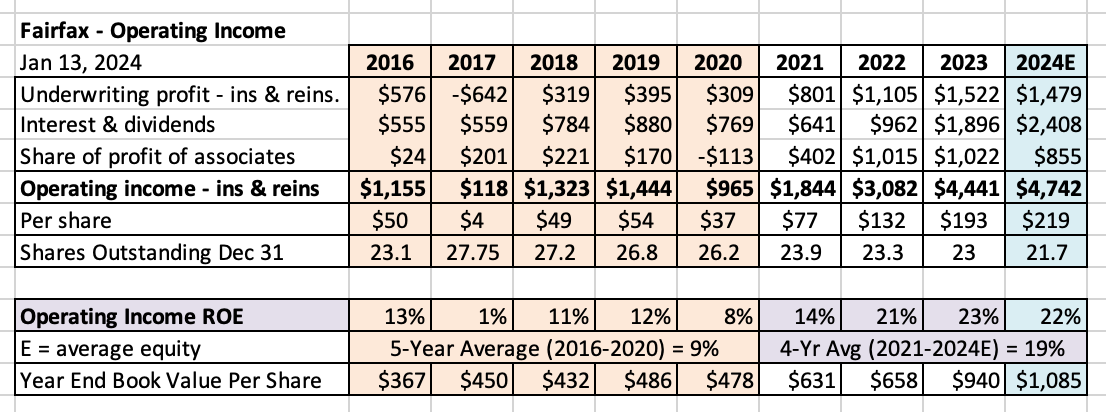

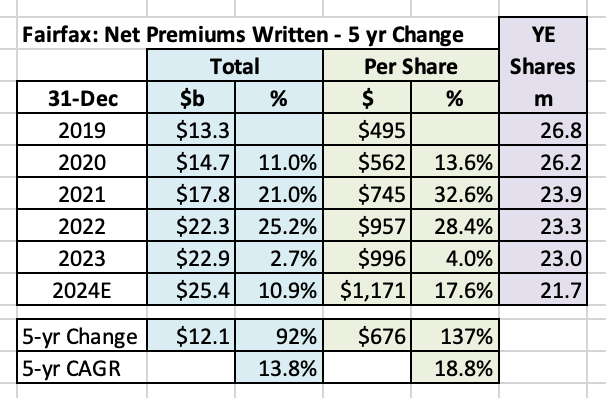

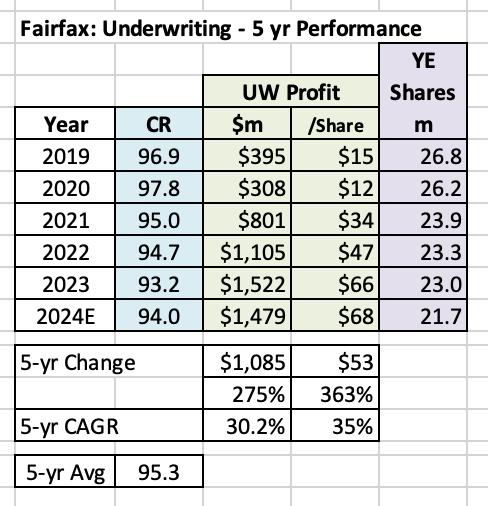

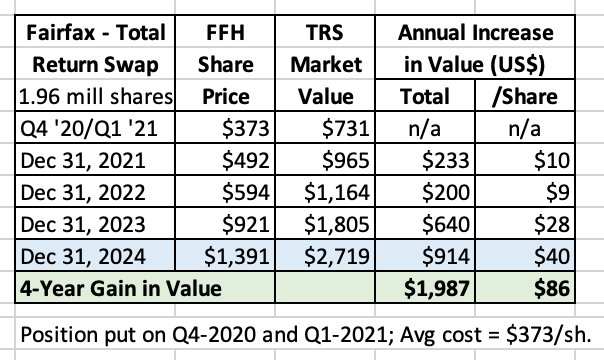

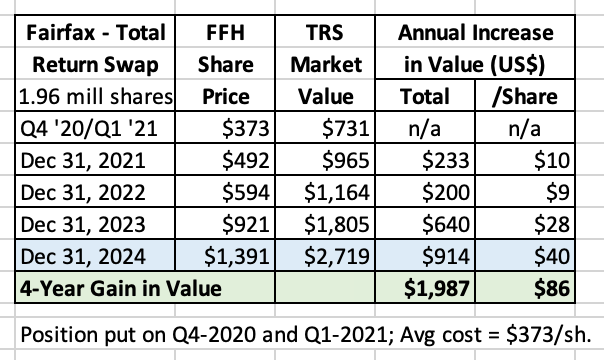

2024 Top 10 List - Part 1 Beginning in 2019, at the end of each year I have put together a ‘Top 10’ list of the most important things/events that happened at Fairfax during the year that drive long term per share value for shareholders. The lists when read together provide an interesting and informative 6-year chronological perspective of Fairfax’s evolution and transformation as a company. It really is amazing what they have been able to accomplish over a relatively short period of time. To read my ‘Top 10’ lists from 2019 to 2023, click the link below. They are in Chapter 14 of my book/PDF on Fairfax. https://thecobf.com/forum/topic/20253-fairfax-financial-volume-2-90-of-the-best-posts-all-in-one-document/#findComment-526661 ————— 2024 Top 10 - The emergence of a high quality company 2024 was another very good year for Fairfax and its shareholders. It was a deceptively good year - other than share buybacks, Fairfax didn’t do anything that was overly flashy or that really stood out. Rather, in 2024, the company quietly went about doing its business. But here is the really interesting point - when you look under the hood, Fairfax was very busy in 2024. From an operating perspective, both of its engines - insurance and investment management - continued to execute very well. From a capital allocation perspective, the senior management team at Fairfax also continued to execute very well. As a result, significant retained earnings were put to good use in 2024. Here are some additional thoughts: Impressive breadth of activities - Fairfax pulled on many different levers across all parts of the company. Complementary - At year-end, we can see and better appreciate how everything Fairfax did fits together like the pieces of a puzzle. Patience/discipline - Fairfax did not force things - during the year they took what they were given. This is a sign of the maturity of the company. The key point: When you stack our top 10 list - one item on top of the other - you begin to grasp what an outstanding year 2024 really was - significant long term per share value was created for shareholders. So when you read the top 10 list below try and do this: for each item, try and visualize how it impacts Fairfax’s income statement and balance sheet. And when you are done reading the complete list, try and do the same thing, but this time incorporating all 10 items together. If you can do this, you will more fully appreciate what Fairfax was able to accomplish in 2024. Quality High quality and well run companies make it look easy. Of course it’s not. But that is what we have been seeing from the team at Fairfax for each of the past 4 years. And that is probably the biggest takeaway in 2024 for investors - we can now say with a fair bit of confidence that Fairfax is a high quality company. Its P/C insurance business is high quality. Its investment management business is high quality. And its senior management team is one of the best in the business. In short, likely for the first time in its history, Fairfax has become a ‘triple threat’ P/C insurance company. This is important because the level of ‘quality’ is what ultimately determines future results (and growth in intrinsic value) - and this is what determines how a company is valued by investors (the multiple). Before we get to our Top 10 list, how did Fairfax’s stock perform in 2024? Fairfax’s stock was up 51% and 64% (C$) in 2024. Fairfax also paid a $15 dividend, so shareholder returns were slightly higher. Over the past 4 years, Fairfax’s stock is up 308% and 361% (C$). It has also paid total dividends of $45/share. The performance of Fairfax’s stock over the past 4 years has been outstanding - in absolute terms and when compared market averages (and peers). Although it has improved in recent years, the valuation of Fairfax’s stock continues to lag that of peers. This suggests to me the ‘quality’ part of the Fairfax story is not yet recognized/appreciated by investors. ————— Top 10 'events’ driving shareholder value in 2024 I have tried to prioritize the items in our Top 10 list - from most important to least important. I have also grouped related items. And I have also tried to tell a story - to provide readers with context. As a result, I have played with the order of some items (most notably, share buybacks, which likely should have been #2 on the list this year). Bottom line, the Top 10 list should be viewed as pieces to a puzzle - the key is to try and focus on the picture that is produced when all the pieces have been put together. What is missing from my list? I look forward to hearing what other board members think. Ok. Let’s get started. 1.) Record operating income Operating income at Fairfax averaged $1 billion from 2016 to 2020. In 2021, it almost doubled to $1.8 billion. In 2022, it tripled to $3.1 billion. In 2023, it quadrupled to $4.4 billion. At the beginning of 2024, many investors questioned if this much higher level of operating income was sustainable. We got our answer in 2024: yes. Not only is it sustainable - it is growing. Especially per share. Operating income is expected to come in at around $4.7 billion in 2024 - a new record for Fairfax. This is an increase of 7% over 2023. Operating income is valued so highly because of all the sources of earnings it is considered durable/sustainable and predictable. Per share metrics are what really matter. Because of all the share buybacks that Fairfax has done over the past 4 years, the increase in operating income per share has been much higher. From 2016 to 2020, operating income averaged $39/share. In 2023 it was $193/share. In 2024, it is poised to come in at around $219/share. This is a 462% increase in 4 years (over the average from 2016 to 2020). The increase in operating income per share over the past 4 years has been breathtaking. In 2024, operating income per share increased 13.2% (over 2023). The significant share buybacks that Fairfax did in 2024 almost doubled the rate of growth per share. More on share buybacks later. Assumptions built into 2024 estimated results: Underwriting profit: Growth in NPW = 11%; CR = 94% Interest and dividend income: Average yield = 4.9%; Average duration = 3.5 years. Share of profit of associates: Driven by Eurobank and Poseidon (Atlas) Importantly, over the past 2 years, operating income has averaged $4.6 billion per year. This is likely a good number to use to estimate ‘normalized’ operating income for Fairfax for the coming years. Over the past 4 years, Fairfax has delivered an average ‘operating income ROE’ of 19%. This is more than double the average from 2016 to 2020 of 9%. Yes, Fairfax has been ‘transformed’. 2.) Net premiums written per share continues to grow high-teens Fairfax’s net premiums written is estimated to finish the year at a record $25.4 billion. Year-over-year, the increase is 10.9%. On a per share basis, the increase is 17.6%. The big driver of the increase in net premiums written was the consolidation of Gulf Insurance Group. Fairfax also continued to grow its insurance business in the hard market. Over the past 5 years, Fairfax has increased the per share size of net premiums written at an impressive CAGR of 18.8%. How about underwriting? Fairfax’s combined ratio is estimated to come in at about 94% in 2024. The combined ratio average over the past 5 years is 95.3%. In 2024, underwriting profit per share is estimated to come in at $68/share, a new record for Fairfax. This is very good performance. Bottom line, Fairfax has a high quality insurance business. And it has been growing like weed. 3.) Performance of Fairfax Total Return Swap - 1.96 million Fairfax shares Fairfax established its total return swap position - giving it exposure to 1.96 million Fairfax shares - in late 2020 and early 2021. The average cost was US$373/share. In 2024, this investment delivered a return of $914 million (before carrying costs) or 50% (calculated using its 2023YE notional value). Since inception (over the past 4 years) this investment has delivered a total return of $2.0 billion (before carrying costs). It has become one of Fairfax’s best-ever investments. Yes, this is a ‘non-traditional’ type of investment for a P/C insurance company to make. When it comes to capital allocation Fairfax today looks like a modern version of Henry Singleton’s approach when he ran Teledyne (he was also very open minded and creative in how he approached and executed capital allocation when he ran Teledyne). 4.) Performance of Eurobank With a 2024YE market value of $2.9 billion, Eurobank is Fairfax’s largest equity holding. In 2024, the market value of Fairfax’s stake increased by $665 million. It is up $2 billion over the past 4 years. Eurobank began paying a dividend in 2024. The payment to Fairfax was $126 million. In 2024, Eurobank delivered a total return to Fairfax of $784 million (increase in MV of $658 million + dividend of $126 million). This is a total return of 35% (compared to 2023YE market value). In late 2024, Eurobank announced that it would taking Hellenic Bank private. Hellenic Bank is the second largest bank in Cypress. Greece is expected to have one of the better performing economies in Europe. The is a very good set-up for Eurobank. Context: The total equity portfolio delivered another solid year of performance for Fairfax in 2024 Fairfax’s equity portfolio had an average size of about $19 billion in 2024. Fairfax’s two largest investments, Eurobank and FFH-TRS, represent about 26.5% of the total equity portfolio. In 2024, these two investments on their own delivered a total return to Fairfax of $1.7 billion ($784 + $914 million) = 8.9% return on the total average equity portfolio of $19 billion. The remaining equity holdings (73.5%) also performed well for Fairfax (on balance). Bottom line, Fairfax’s total equity portfolio delivered another solid year of results in 2024. ---------- To read Part 2 go to next post in thread...

-

I first bought shares in Fairfax back in 2003. Since then I have been an active trader of the shares. I was largely out of the shares from around 2012 to 2018 (as I did not like what they were doing with their investment portfolio at the time). I started buying shares again in 2019 but sold everything (all my stock holdings) in early 2020 when it was clear to me that Covid was going to be a massive problem. I bought Fairfax stock again in October 2020, and backed up the truck in November when we got new a vaccine had been approved for Covid. I have had a pretty concentrated position in Fairfax since late 2020. This the longest I have ever continuously held a stock (let alone a concentrated position).

-

@Junior R , thanks for posting this. I was wondering if Fairfax would stay aggressive on the share buyback front with big run-up we saw in the share price in Q4 (now trading in the US$1,350 range). The answer is yes. This is good news on a couple of fronts: 1.) Suggests Fairfax continues to see their shares undervalued at current prices (US$1,350). 2.) This could provide a floor for the stock should we see a big sell off in the general stock market (this would likely give Fairfax a nice opportunity to take out a meaningful number of shares). 3.) From a capital allocation perspective, perhaps we see Fairfax continue to prioritize share buybacks in 2025. It is a very low risk / solid use of capital.

-

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

Perhaps the biggest short term challenge Canada has today is we are being governed by a historically inept Liberal party/government. The policies they have put in place over the past 9 years are now throwing sand in the gears of the economy. At the same time, the current government executes foreign policy based on what they think will help them in the polls. As a result, Canada's standing in the world has likely never been lower than it is today. One example? Trudeau and the Liberals have been very vocal - they think Trump is an idiot. And to top it off, the Liberals just decided to suspend parliament and begin a long leadership race. And in a couple of weeks Donald Trump will take office. We know he is going to hit the ground running. And he has a long memory (for those who come after him). So the big problem Canada has today is our economy is already on its knees, we are leaderless, we have very publicly poked the Donald (and others) and we have very little leverage. As a result, it is very difficult to be rational and to try and figure out how things might play out for Canada in the coming months. It is almost impossible to do when the country is being run by a bunch of fools - because they are most likely to do something that will actually make the situation worse. Now before board members get nervous, no, I am not looking for a bridge to jump off of. Eventually Canada will figure things out. My guess is most Canadians want a change in government - and that will happen at some point between now and October. But in the meantime I have decided to fasten my seat belt - just in case the ride starts to get bumpy. Crisis = opportunity. Well, at least it does for those who are prepared (don't lose their mind) and have cash. -

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

@SharperDingaan , your post is very timely. For the past couple of years I have largely avoided thinking too much about macro. This has kept me more fully invested than I normally would have been. With hindsight, that has been a good decision - financial markets have been VERY strong the past 2 years and returns have smoked. However, I decided in recent days to get much more defensive with my portfolio. Why? Macro concerns have reached a point where it seems kind of reckless to ignore them. Important: I am coming at this as a Canadian investor. My spidey sense are tingling again - and I have learned over the years to pay attention when that happens. What are my concerns? - The recent spike in interest rates in the US. - The very weak Canadian economy - it has been weak for years. - The housing bubble in Canada also looks like it might be 'ending' (and these events tend not to be good for the economy). - The threat from Trump to impose blanket 25% tariffs on Canada. - The political turmoil in Canada - the federal Liberal party put itself and the country into a straight jacket for the next 6 months. With this set-up, what could possible go wrong? At the same time, the Canadian stock market (S&P/TSX) is trading near all-time highs (4% off highs). It is priced for sunny days ahead. I am much more constructive on the US economy moving forward than the Canada economy. What did I do? Over the past couple of days I have moved to a 28% cash position in my portfolio. Most of my selling has been XIC.TO (my Canadian ETF/index holding). In the coming days and weeks I will read/learn/process and decide how I feel about things and my decision/positioning of my portfolio. The bottom line the risk/reward seems pretty skewed to the downside for the Canadian economy. Importantly, I don't have to be fully invested. Actually it's kind of dumb for me to be fully invested. Capital preservation is more important to me these days than rate of return. Much of my portfolio is in tax-free accounts - so I can move in and out of positions and not have to worry/think about tax implications. If I change my mind I will simply start buying back XIC.TO. If it runs higher in the meantime I can live with that. At the same time, we could also see some very well run Canadian companies get taken out behind the woodshed. If I am fully invested it would be difficult to take advantage of this situation. I love the optionality that cash provides. -

Sorry, my post was unclear… I meant to say: “And if Trump has filled the Fed with people who prioritize loyalty to Trump over fighting inflation.”

-

When i was getting started (back in my late 20’s), I did not think i was particularly intelligent/smart when it came to investing. I did a finance degree is school (joint major business/economics and minor in political science) and learned about stuff like the bank act (nothing about investing) so my formal education did not help at all (but it also did not teach me any bad habits). But I did like money/investing… a lot. And I wanted to do well. And I was action oriented (and a risk taker). So that drove me to try. And i was terrible. My first big investment ($5,000) was Bre-X and it promptly went to zero. Ended up being one of my best investments ever. Because it taught me quickly that i knew nothing about investing. It also taught me one of the most valuable lessons right when I was getting started - the difference between speculating and investing. But I was lucky. I hate (really hate) to lose money. And i realized i needed to learn how to invest. Enter Warren Buffett, Peter Lynch and Burton Malkiel. And after many hours and years of hard work and the rest is history. But my first three years managing my own money had negative returns (I have tracked my returns for each year going back 30 years). Year 4 was +35%… that was how long it took me to start to figure investing out (a framework that fit my intellect and how I was wired).

-

Well, we have certainly been getting some pretty wicked volatility in bond markets in recent months. I wonder if Brian Bradstreet and the fixed income team at Fairfax has ever invested using TIPS. Locking in a yield on the 10-year treasury that is 2.25% higher than inflation historically has been a pretty smart thing to do. But I don’t understand how that kind of investment might impact their insurance liabilities. That size of TIPS premium (+2.25%) typically does not last. Regardless, Fairfax is getting a nice opportunity to extend duration at what look to be pretty decent rates. The risk is if inflation spikes higher. And Trump has filled the Fed with people who prioritize loyalty to Trump over fighting inflation. If this was easy, everyone would be rich

-

Fairfax's second largest equity holding is FFH-TRS. This holding is up $914 million in 2024. Over the past 4 years it is up $2 billion. Now let's put Eurobank and FFH-TRS together. Together they are up $1.7 billion in 2024 ($784+$914). And $4.1 billion over the past 4 years. WOW! Fairfax's average total equity portfolio was probably about $20 billion in 2024. Eurobank and FFH-TRS represent about 26.5% of the total. In 2024, these two investments delivered a total return of 8.5%. Guess what Fairfax's equity portfolio delivered in 2024? A number much higher than 8.5%. Two investments delivered that. Fairfax has another 73.5% in equity investments that are - as a group - performing well (some very well). At the start of 2024, investors were WAY TOO PESSIMISTIC in their estimates of what Fairfax's equity portfolio would deliver in 2024 and future years. My guess is that remains the case today.

-

+1. Both Eurobank and especially Hellenic Bank are overcapitalized. My guess is the management team at Eurobank is licking their chops - and already has a plan in place to 'solve' that problem. Another large dividend? Begin sizeable share buybacks? More acquisitions? (After they close on and digest Hellenic Bank)

.png.0e19190a04a2c48d4dec8dee009300b8.png)