Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Sale of Riverstone Europe – 2019 to 2020 – Improving the Quality of the P/C Insurance Business Below is instalment 3 in my review of asset sales at Fairfax from the past 7 or 8 years. My goal is to provide some additional insights - that should provide a little more colour into the transformation that has happened at Fairfax (especially earnings). And help us better understand what might be coming in the future. Please share your thoughts / insights. First, a quick review: Capital allocation Capital allocation is the most important responsibility of a management team. Why? Capital allocation decisions are what drive the long-term performance of a company and important metrics like reported earnings, growth in book value and return on equity. In turn, these metrics drive the multiple given to the stock by Mr. Market - and finally the share price and investment returns for shareholders. When done well, capital allocation does two important things: Delivers a solid return. Improves the quality of the company. Asset Sales Asset sales are one part of capital allocation that separates Fairfax from its peers. In selling an asset, Fairfax is essentially trading a stream of future cash flows for a lump sum today. Why sell an asset? Sometimes another company - who is willing to pay up - values an asset at a much higher value than you do. There also can be important strategic reasons to sell an asset. Asset sales have been a very important part of Fairfax’s capital allocation framework, realizing significant value for Fairfax and its shareholders over the years. ———— Riverstone Europe – 2019 to 2020 – Improving the Quality of the P/C Insurance Business In two different transactions, Fairfax sold the biggest piece of its run-off business, RiverStone Europe, for announced total proceeds of about $1.5 billion. In December of 2019, Fairfax sold 40% of RiverStone Europe to OMERS for $599 million. In December of 2020, CVC Capital Partners bought 100% of RiverStone Europe - taking out both Fairfax and OMERS. This was a significant sale for Fairfax for a couple of reasons: It dramatically shrunk the size of Fairfax’s run-off business by more than 70%. In turn, the sale likely materially reduced Fairfax’s exposure to long-tail insurance liabilities (a good thing in the high inflation world of today). For P/C insurers, run-off businesses are generally considered to be low quality. Selling RiverStone Europe improved the overall quality of Fairfax’s remaining P/C insurance business. 2019/2020 was also a time when Fairfax was short on cash. Their investment portfolio was underperforming. The timing of this sale was very good. By late 2020, it was clear the hard market in P/C insurance had arrived. Fairfax was aggressively expanding its P/C insurance business - to do this some of the insurance subs would needed more capital. The proceeds from the sales of RiverStone Europe would be put to very good use. Essentially, Fairfax was able to sell the majority of its run-off business for a fair price. And use the proceeds to then aggressively grow its P/C insurance business in a hard market. They were able to shift a significant amount of capital from a low quality business into high quality businesses. Well at least that is what it looks like they did (looking at it today). ————— A short review of Fairfax’s run-off business Fairfax had two run-off operations: The Resolution Group (TRG - US) and RiverStone Europe. Run-off has historically been a very large part of Fairfax’s total P/C insurance business. It looks like the run-off business peaked out at 25% of Fairfax’s common shareholders’ equity at December 31, 2014 - nine short years ago. Today (December 31, 2023), the runoff business represents 1.8%. That is a massive reduction in size. The first big step down (to 14%) happened in 2017 - that is the year Allied World was purchased. The second big step down (to 4%) happened in 2019, when Fairfax sold 40% of RiverStone Europe to OMERS (and RiverStone Europe was deconsolidated). But it is also interesting to note that since 2020, Fairfax has continued to shrink the size of its runoff business (in both absolute and percentage terms). Does this make Fairfax a higher quality P/C company than it was in the past? Yes, I think it does. But I am not an insurance expert. I would love to hear what other board members think. What is runoff? “Run-off portfolio refers to insurance policies or reinsurance contracts terminated but for which the Insurer or the Reinsurer remains liable for until the final settlement and payment of the claims. It may be a business or a territory for which the Insurer or Reinsurer is no longer operating but where contracts or liabilities are still in force.” “Due to these outstanding claims or the potential claims to be notified, the Insurer or Reinsurer must set up reserves; especially for long tail businesses (such as motor liability, medical malpractice, and general third party liability). These risks are highly volatile. Moreover, discontinued run-off businesses must respect Solvency 2 rules. Their management requires resources. Run-off liabilities may require significant equity at the expense of the development of new businesses.” Source: CCR RE https://blog.ccr-re.com/en/what-is-run-off PWC Global Insurance Run-off Survey https://www.pwc.com/gx/en/industries/financial-services/publications/global-insurance-run-off-survey.html Why did Fairfax sell RiverStone Europe? RiverStone Europe was a quality business. It was well run and profitable. But it also wanted to grow - and to do that it needed capital - and a lot of it. But in the years before 2021, Fairfax did not have a lot of excess capital. And with the hard market, any excess capital Fairfax did have was going to go to its traditional P/C insurance business - not runoff. The solution? Sell RiverStone Europe for a fair price. And then use the proceeds to aggressively grow the traditional P/C business in the hard market. And that is what Fairfax has done. What a smart strategic pivot. The sale was also a very good move for RiverStone Europe. It looks like they have been growing like a weed the past couple of years and are very profitable. This sale looks like it was a win for everyone involved. RiverStone International - 2023AR https://www.rsml.co.uk/wp-content/uploads/2024/05/RIHL-Consolidated-2023-Annual-Report.pdf Was it a mistake for Fairfax to sell RiverStone Europe? My view is Mr. Market does not like P/C insurance businesses that have a big run-off business. For a whole bunch of reasons. As a result, it was highly unlikely they were ever going to value a ’good’ run-off business appropriately. We all think Fairfax should trade at a much higher multiple than what it is trading at today. That likely would not happen if the runoff business was still 20 to 25% of shareholders’ equity. Of note, with the sale, Fairfax did give up a significant amount of investments ($2.375 billion at Dec 31, 2019). ————— Details of RiverStone Europe’s Sale To CVC From Fairfax’s 2020AR “Late in 2020 we announced the sale of RiverStone Europe (owned 60% by us and 40% by OMERS) to CVC Capital Partners. RiverStone Europe is an industry leader in run-off insurance services, and CVC’s scale and vision will give RiverStone Europe, under the continued leadership of Luke Tanzer and his management team, the opportunity to further grow the business. Nick Bentley and Luke are also very supportive of this transaction, based on their strong belief that it is the best way for RiverStone Europe to continue to grow and pursue run-off transactions. RiverStone Europe was born out of the acquisition of Sphere Drake Insurance Company. Due to performance issues, in 1999 it was put under the management of RiverStone. For the first ten years RiverStone Europe was kept busy with many of our own run-off portfolios including Sphere Drake Bermuda, Skandia UK, CTR and the Kingsmead Agency at Lloyd’s. By 2008 they drove down the reserves and were down to only 53 staff and $100 million in capital. Instead of closing the operations we pivoted from internal run-off to third party acquisitions. They did their first deal in 2010 and have never looked back. They have completed over 20 transactions bringing in over $5 billion of assets and producing a great return on capital, which allowed us to sell the company at $1.35 billion. RiverStone Europe is a great story of success, first directly under the leadership of Nick Bentley and then for the last twelve years Luke Tanzer. We wish Luke and all employees at RiverStone Europe much success in the future.” “We began equity accounting RiverStone Barbados in 2020, so its investment portfolio is no longer consolidated. Within its investment portfolio are positions of many of the common stocks listed in the common stock holdings table above. For example, RiverStone Barbados owns 9.7 million shares of Fairfax India that are not included in the 41.9 million shares of Fairfax India we show in the common stock holdings table (combining both would give us 51.6 million shares or 34.5% ownership). The same can be said for a number of other holdings such as Atlas, BlackBerry, Commercial International Bank and Recipe. As part of the sale of RiverStone Barbados to CVC, we have the opportunity to purchase these securities over the next two years, at December 31, 2019 prices.” “At our RiverStone run-off operations, led by Nick Bentley, while not recently active in U.S. run-off acquisitions (other than some small very successful captive insurance deals), the team has been very busy focusing on our U.S. legacy reserves, especially asbestos claims. Although we needed to strengthen reserves again in 2020 (about half of the previous year), the team continues to deliver significant value and savings from its dedicated focus and best in class experience – I can assure you these reserves are in good hands. As mentioned previously, late in 2020 we announced the sale of our remaining interest in RiverStone’s European business to CVC Capital Partners. Luke Tanzer and his entire team at RiverStone Europe had a very busy year, closing five run-off deals. They are excited to continue to expand in the very active UK run-off market, and again, we wish them all the best going forward.” ———— More information from Fairfax’s 2020AR Sale of RiverStone Barbados to CVC Capital Partners "On December 2, 2020 the company entered into an agreement with CVC Capital Partners (‘‘CVC’’) whereby CVC will acquire 100% of RiverStone (Barbados) Ltd. (‘‘RiverStone Barbados’’). OMERS, the pension plan for Ontario’s municipal employees, will sell its 40.0% joint venture interest in RiverStone Barbados as part of the transaction. On closing the company expects to receive proceeds of approximately $730 for its 60.0% joint venture interest in RiverStone Barbados and a contingent value instrument for potential future proceeds of up to $235.7. Closing of the transaction is subject to various regulatory approvals and is expected to occur in the first quarter of 2021. Pursuant to the agreement with CVC, prior to closing the company entered into an arrangement with RiverStone Barbados to purchase (unless sold earlier) certain investments owned by RiverStone Barbados at a fixed price of approximately $1.2 billion prior to the end of 2022." Contribution of European Run-off to a joint venture "On March 31, 2020 the company contributed its wholly owned European run-off group (‘‘European Run-off’’) to RiverStone (Barbados) Ltd. (‘‘RiverStone Barbados’’), a newly created joint venture entity, for cash proceeds of $599.5 and a 60.0% equity interest in RiverStone Barbados with a fair value of $605.0. OMERS, the pension plan for municipal employees in the province of Ontario, contemporaneously subscribed for a 40.0% equity interest for cash consideration of $599.5, based on the fair value of European Run-off at December 31, 2019 pursuant to a subscription agreement on December 20, 2019, and entered into a shareholders’ agreement with the company to jointly direct the relevant activities of RiverStone Barbados. At closing on March 31, 2020, the company deconsolidated the assets and liabilities of European Run-off from assets held for sale and liabilities associated with assets held for sale on the consolidated balance sheet respectively, which included European Run-off’s unrestricted cash and cash equivalents of $377.8, and commenced applying the equity method of accounting to its joint venture interest in RiverStone Barbados. The company recorded a pre-tax gain on deconsolidation of insurance subsidiary of $117.1 in the consolidated statement of earnings, comprised of a gain of $243.4 on the disposal of 40.0% of European Run-off and a gain of $35.6 on remeasurement to fair value at the closing date of the 60.0% of European Run-off retained, partially offset by foreign currency translation losses of $161.9 that were reclassified from accumulated other comprehensive income (loss) to the consolidated statement of earnings. The deconsolidation of European Run-off increased the company’s non-controlling interests by $340.4 at March 31, 2020 as RiverStone Barbados holds investments in certain of the company’s subsidiaries as described in note 16."

-

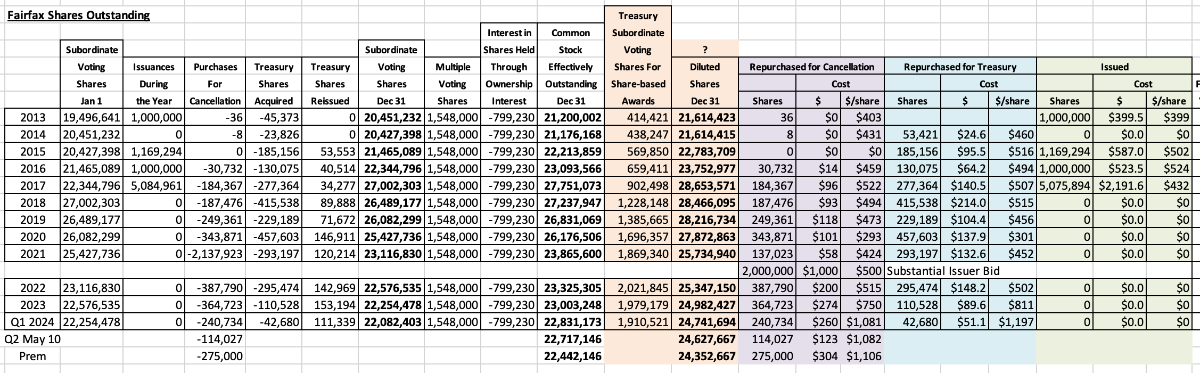

@glider3834 I am looking forward to seeing what the June 30 share count is when Fairfax reports Q2 results. If they keep the current pace of buybacks up there is a good chance they will reduce effective shares outstanding by +1 million in 2024 to 22 million (or less). Fairfax historically only buys back stock when they think it is trading at a cheap valuation. And i think they can value the company pretty well. I continue to think the piece that investors are getting wrong is the quality of the insurance AND the quality of the investment portfolio (much improved and best in company’s history) - and the multiple that warrants. But Fairfax gets it - hence why they continue to buy back stock hand over fist in 2024. Buying back stock at current prices is like shooting fish in a barrel (from a capital allocation perspective).

-

My oldest daughter (24) is in Toronto visiting a couple of fiends. What is she doing? My younger daughter's (21) response (at the bottom) cracked me up. Fairfax is definitely a family affair in our house PS: my kids TFSA's are 100% in Fairfax (since they were opened a couple of years ago). They are very happy shareholders (they look at their account balances).

-

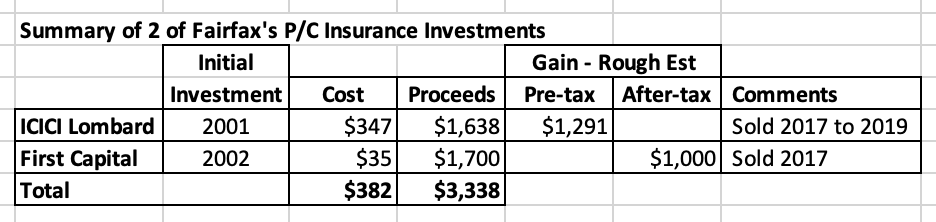

Below is instalment 2 in my review of asset sales at Fairfax from the past 7 or 8 years. My goal is to provide some additional insights - that should provide a little more colour into the transformation that has happened at Fairfax (especially earnings). And help us better understand what might be coming in the future. Please share your thoughts / insights. First Capital – August 2017 – The Amazing Mr. Athappan First Capital provides many outstanding examples of what Fairfax does well as a company. But three really stand out: The incredible power of partnering with outstanding people – and letting time and compounding work its magic. The benefit of being opportunistic – sometimes a buyer is willing to pay a truly obscene price for an asset. International focus – In 2001 Fairfax seeded ICICI Lombard (India). In 2002 Fairfax seeded First Capital (Singapore). Both have become home run investments for Fairfax and its shareholders. ————— In 2017, Fairfax sold First Capital for $1.7 billion and booked a $1 billion gain after-tax. The amount Fairfax received from this sale was a complete shocker at the time. First Capital was sold for more than 3 times book value. As part of the deal, Fairfax also established a strategic partnership with Mitsui Sumitomo, making a great deal even better. At the time, First Capital was the largest P/C insurer based in Singapore. In 2016 it had shareholders’ equity of $473 million and gross premiums written of $384 million. The CR was 86.4% and underwriting profit was $41 million. Fairfax’s initial (and only) investment in First Capital was $35 million in 2002. This investment had a CAGR of about 30% over a 15-year period. Wow! The bottom line was Mitsui Sumitomo was willing to pay a king’s ransom to become the largest P/C insurer in Singapore. 2017 was also a time when Fairfax was short on cash. Their investment portfolio was underperforming. And they were at the tail end of their aggressive international P/C insurance expansion - their $4.9 billion purchase of Allied World closed in July 2017. The sale of First Capital was announced in August of 2017. Importantly, First Capital was sold at more than 3 times book value. Allied World was purchased at 1.3 times book value. Over the past 7 years, Allied World has become a wonderful acquisition for Fairfax. What was First Capital such a big success story for Fairfax? The amazing Mr. Athappan. Fairfax picked the right partner way back in 2002. Mr. (Ramaswamy) Athappan was an incredible leader/partner/entrepreneur. Not only did he build First Capital from scratch, he also has his fingerprints all over Fairfax’s many insurance acquisitions in Southeast Asia over the past 15 years. After the sale of First Capital, Mr. Athappan (and his son Gobi) continued to manage Fairfax’s diverse collection of P/C insurance holdings in Southeast Asia. Of interest, the purchase of Singapore Re (the 72% Fairfax did not already own) for $103 million in 2021 is looking like it was timed perfectly, right before the onset of the hard market in reinsurance. Unfortunately, Mr. Athappan passed away in May of 2024 at the age of 78. In June 2024, Mr. Athappan’s son, Gobi, was appointed Chairman and CEO of Fairfax Asia. The Athappan gift keeps on giving to Fairfax and its shareholders. Fairfax Asia is a significant platform for Fairfax in a very important region that should continue to grow nicely in the coming years. Mr. Athappan was one of the founding members of the $1 billion club at Fairfax - individuals who have built enormous value for Fairfax and its shareholders over the years. ————— Mr. Athappan’s legacy: Fairfax Asia ————— Link to Mitsui Sumitomo’s presentation on acquisition of First Capital in August 2017. https://www.ms-ad-hd.com/en/ir/ir_event/event/presentation/main/06/teaserItems1/00/linkList/0/link/20170824_info_e.pdf ————— Quote from Fairfax’s press release on May 23, 2024. “Over the past 22 years, Mr. Athappan has been a driving force in developing Fairfax’s insurance operations in Southeast Asia. He made invaluable contributions to the success of Fairfax and Fairfax Asia over these years through his leadership, mentorship and guidance. “Mr. Athappan was an exceptional leader with an incredible track record of success. He was a trusted and valued colleague, but most importantly, he was a very good friend of mine and many others here at Fairfax,” said Prem Watsa, Chairman and Chief Executive Officer of Fairfax. “To his family members and loved ones, we send our deepest condolences on the loss of a very special person.” ————— Comments from Prem about the sale of First Capital from Fairfax’s 2017AR. "...Mr. Athappan has had an incredible record with us in building First Capital. We provided $35 million in 2002 to let him establish First Capital; 15 years later, with no additional capital having been added, he had grown First Capital to be the largest P&C company in Singapore and with the Mitsui Sumitomo deal, gave us back $1.7 billion. That’s a compound rate of return of approximately 30% annually. A fantastic track record by Mr. Athappan!” Prem explains why Fairfax agreed to sell First Capital. “For the past two years, Mr. Athappan has come to me saying that he had taken First Capital as far as he could in the commercial property and casualty business in Singapore and that he needed a partner like Mitsui with a brand name to build the personal lines business. I refused him twice as I really did not want to sell First Capital. His continued persistence, his position as the founder of the company, and the fact that he would continue to run Fairfax Asia and First Capital and we would have a 25% quota share in the business of First Capital going forward persuaded us, with unanimous support from our officers and directors, to form a global alliance with Mitsui Sumitomo Insurance Company and sell First Capital to them. We worked very closely with Matsumoto san, the Senior Executive Officer of International Business of Mitsui Sumitomo, and his team, and the partnership is going very well. Through our cooperation agreement with Mitsui Sumitomo, we have been working together on a number of fronts including opportunities on reinsurance, shared business and products and innovation to name a few. We are very excited to be a partner with Mitsui Sumitomo. Total proceeds from the sale of First Capital were $1.7 billion, resulting in an after-tax gain of $1.0 billion. I do want to emphasize that we agreed to this global alliance and sale only because of its truly unique circumstances and we do not see this being repeated! Our companies are not for sale, period!”

-

Did Fairfax not sell Easton to Rawlings? If it can happen in baseball why not hockey? https://sgbonline.com/rawlings-to-purchase-easton/ Transaction Details (Easton sale to Rawlings) The transaction is subject to the satisfaction of customary closing conditions, including the receipt of U.S. regulatory clearance. In 2018, Newell Brands Inc. sold Rawlings to a fund managed by Seidler Equity Partners (SEP), a private investment firm based in Marina del Rey, CA, for $395 million. Major League Baseball co-invested in the purchase. Rawlings, founded in 1887 and based in St. Louis, MO, comprises the Rawlings, Miken and Worth brands. Peak Achievement Athletics was acquired by two private equity groups, Sagard Holdings Inc. and Fairfax Financial Holdings, in bankruptcy proceedings in February 2017. The company is the parent of Bauer Hockey, Easton Baseball/Softball, Cascade Lacrosse and Maverik Lacrosse. Peak Achievement Athletics. The Easton hockey and cycling businesses are owned by other entities.

-

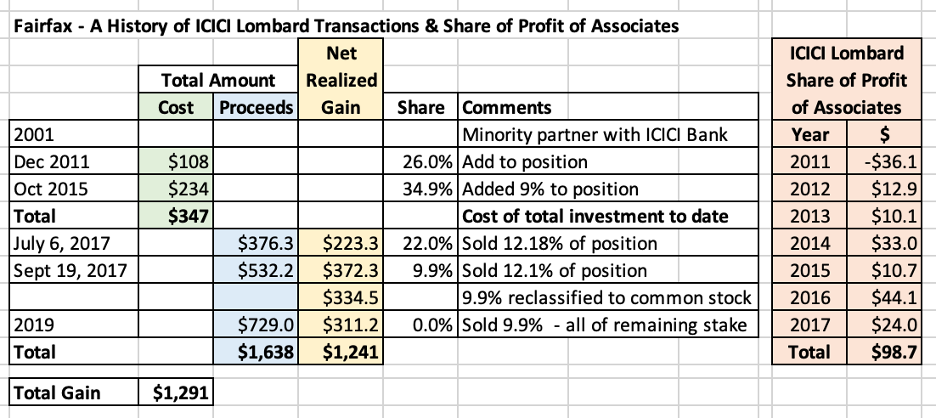

Over the next 2 weeks my plan is to review a number of Fairfax's asset sales from the past 7 or 8 years. My view is Fairfax continues to be a misunderstood company. What to do? Educate investors. Explain to them what has actually been happening at the company over the past 7 years. This will also provide much needed colour regarding the transformation that has happened at Fairfax (especially earnings). And help us better understand what might be coming in the future. Please share your thoughts / insights. Future posts will review the following sales: First Capital, RiverStone Europe, Pet Insurance, Bank of Ireland, Corporate Bonds in late 2021 and Resolute Forest Products. Let me know if there are other 'sales' from the past 7 or 8 years that should be included/would be interesting to dig into. The focus is to provide more information on the breadth and quality of the decision making that has been happening at Fairfax for a long time now. ---------- ICICI Lombard – 2017 to 2019 – A Strategic Pivot in India ICICI Lombard presents many outstanding examples of what Fairfax does well as a company: 1. How strategic they are in their thinking. Back in 2001 who was thinking about investing in India? Fairfax was. 2. How long term they are in their thinking. This investment did very little (return wise) for the first 10 years of its existence. 3. The importance of picking the right partner. Fairfax nailed this by choosing to partner with ICICI Bank. 4. Having a decentralized structure. Fairfax was not actively involved in operating the company. But we have an added and unexpected twist: 5. The ability to pivot strategically when the facts change. What Fairfax accomplished with its P/C business in India over the past 7 years has been nothing short of epic. They completely disrupted what was a very successful situation/business model. Clayton Christensen (author of ‘The Innovator’s Dilemma’) would be proud. In 2016/17, Fairfax abruptly changed the strategic direction of their P/C insurance business in India. And they were successful. They have created billions of dollars in shareholder value in the process. But more importantly, they have secured their future in the growing P/C insurance market in India. Given the growth that is expected from the Indian economy in the coming decades, that is a big, big deal. What happened? Beginning in 2017, Fairfax executed a brilliant strategic pivot - away from longtime partner ICICI Lombard and to startup Digit. This was a very strategic, calculated, rational, gutsy, high risk / high reward decision. What was the financial impact? From 2017 to 2019, Fairfax sold their entire 34.9% stake in ICICI Lombard for proceeds of about $1.6 billion. Between realized gains and share of profit of associates it looks to me like they generated a total return of about $1.3 billion pre-tax (I think minimal tax was paid due to the tax jurisdictions where the ICICI Lombard positions were held). In 2017, Fairfax seeded Digit. At December 31, 2023, Fairfax’s Digit position (49%) had a cost basis of $154 million and a fair value estimate of $2.265 billion = CAGR of 62%. In Q2-2024 Digit completed its IPO in India, so we should get a valuation update when Fairfax reports Q2 results. The bottom line is Fairfax harvested gains of around $1.3 billion (from the sale of ICICI Lombard) and have generated additional gains of +$2 billion (in Digit). That is $3.3 billion in shareholder value creation in the last 7.5 years. And they own a significant stake/control position in one of the fastest growing P/C insurers in India. The timing of Fairfax’s sale of ICICI Lombard is also important – 2017 and 2019. Total proceeds were $1.6 billion. Unlike today, this was a time when Fairfax needed the cash. Fairfax commented that some of the proceeds from the 2019 sale would be used to support the insurance subsidiaries grow in the hard market (that was just getting started). Bottom line, Fairfax was able to put the proceeds from the sale of ICICI Lombard to good use. Why did Fairfax pivot from ICICI Lombard to Digit? The facts changed. Fairfax’s partnership with ICICI Bank was the perfect fit from 2001 to 2016. But not in 2017. ICICI Bank wanted to take ICICI Lombard public - and they didn’t want to reduce their ownership position to below 55%. To go public, at least 25% of the shares needed to be owned by retail investors/public. This meant Fairfax would have to reduce its ownership in ICICI Lombard from 34.9% to 20%. Going public would reduce Fairfax’s ownership in ICICI Lombard by 42%. Fairfax is a P/C insurance company. They were looking to expand their P/C insurance business/exposure in India - not reduce it significantly. What was the solution? Seed startup P/C insurer Digit - and partner with Kamesh Goyal. Importantly, Fairfax would have a control position in Digit – which is something they never had with ICICI Lombard. This move would require Fairfax to reduce their ownership in ICICI Lombard to 9.9%. India does not want cross ownership of P/C insurance companies. If you own a large position in one, the max position you can have in a second is 9.9%. ———— A short history of Fairfax’s investment in ICICI Lombard Fairfax began its insurance journey in India in 2000. That was the year the government in India opened the property and casualty insurance industry to foreign investment. Fairfax partnered with ICICI Bank, a large private bank in India, and created a joint venture called ICICI-Lombard. Fairfax invested $10 million for an interest of 26% in the new venture, the maximum allowed by Indian law at the time. ICICI-Lombard experienced rapid growth in the years that followed and by 2006, they had become the largest private general insurance company in India with a 12.5% market share. Over the years Fairfax made numerous capital infusions to support the growth of ICICI-Lombard and maintain their ownership at 26%. In 2015, the Indian government allowed foreign ownership in insurance companies to increase to 49%. That year Fairfax purchased an additional stake of 9% in ICICI-Lombard from ICICI Bank for $234 million; this increased Fairfax’s ownership in ICICI-Lombard to 34.9%. ————— Comments from Prem on ICICI Lombard from Fairfax’s 2017AR. “ICICI Lombard is an Indian insurance company that we began in 2001 from scratch as a minority partner with ICICI Bank. Over the following 16 years, ICICI Lombard went on to become the largest non-government-owned property and casualty insurance company in India. Until fairly recently, our ownership interest was limited to 26% by government mandate. About three years ago, the government allowed the foreign ownership to go to 49%, which resulted in our going to 35% by buying 9% from ICICI Bank. Since then, given ICICI Lombard’s intent to go public, ICICI Bank wanting to control ICICI Lombard with at least 55% ownership, and Indian law requiring that the public own at least 25% of a public company, our ownership would be reduced to a mere 20%. As property and casualty insurance is our core business and we are very optimistic about the growth prospects in India, and as Indian law does not permit an ownership of 10% or more in more than one insurance company, we agreed with ICICI Bank that we would reduce our interest in ICICI Lombard to below 10% so that we could start our own property and casualty company in India, Digit. ICICI Lombard is a great company led by an exceptional leader, Bhargav Dasgupta, and we wish them much success in the years to come. We have thoroughly enjoyed our partnership with ICICI Bank and its CEO Chanda Kochhar and we wish them also much success in the future.” “The reduction in our equity interest in ICICI Lombard from 35% to 9.9% resulted in cash proceeds of $909 million plus our continuing to own 45 million shares of ICICI Lombard worth $450 million at the IPO (now worth about $550 million) resulting in an after-tax gain of $930 million.” Comments from Prem on Digit from Fairfax’s 2017AR. “As I mentioned in the section on ICICI Lombard earlier, we are very excited to welcome Kamesh Goyal and his more than 240 employees at Digit to Fairfax. Kamesh built Bajaj Allianz from scratch to be the second largest non-government-owned P&C company in India and then spent a total of 17 years at Allianz, the last five years in Munich operating at the highest levels. He is building a digital property and casualty insurance company in India, which was created in December 2016 and has begun actively selling policies. We are very excited about the prospects of Digit.” From Fairfax’s 2017AR. On July 6, 2017 the company sold a 12.2% equity interest in ICICI Lombard General Insurance Company Limited (‘‘ICICI Lombard’’) to private equity investors for net proceeds of $376.3 and a net realized investment gain of $223.3. On September 19, 2017 the company sold an additional 12.1% equity interest through participation in ICICI Lombard’s initial public offering for net proceeds of $532.2 and a net realized investment gain of $372.3. The company’s remaining 9.9% equity interest in ICICI Lombard was reclassified from the equity method of accounting to common stock at FVTPL, resulting in a $334.5 re-measurement gain. Comments from Prem on the exit from the ICICI Lombard investment from Fairfax’s 2019AR. “We sold our last remaining position in ICICI Lombard in 2019 for $729 million. As I mentioned to you in our 2017 annual report, we helped build the largest private property and casualty company in India with our name, Lombard, very much continuing in the future. It has been a very profitable investment for us and we wish the management team, led by Bhargav Dasgupta, much success in the future.” From Fairfax’s 2019AR. “During 2019 the company sold its 9.9% equity interest in ICICI Lombard for gross proceeds of $729.0 and recognized a net gain on investment of $240.0 (realized gains of $311.2, of which $71.2 was recorded as unrealized gains in prior years), primarily related to the removal of the discount for lack of marketability previously applied by the company to the traded market price of its ICICI Lombard common stock.”

-

Fairfax sells remainder stake in ICICI Lombard ending 18 year run

Viking replied to Viking's topic in Fairfax Financial

I am doing an update of Fairfax's investment in ICICI Lombard. In doing my research, I came across this old thread. What have we learned over the past 5 years? Back in 2017, Fairfax nailed the pivot of their P/C insurance business in India - in hindsight, the move was exceptional. It has generated billions in shareholder value. Probably more importantly, it secured a bright future for Fairfax's P/C insurance business in India for the coming decades. When Fairfax reports Q2 results we should get an update on what their stake in Digit is worth. Digit is trading up nicely since successfully completing their IPO. @petec you were spot of with your comments back in 2019. Well done. -

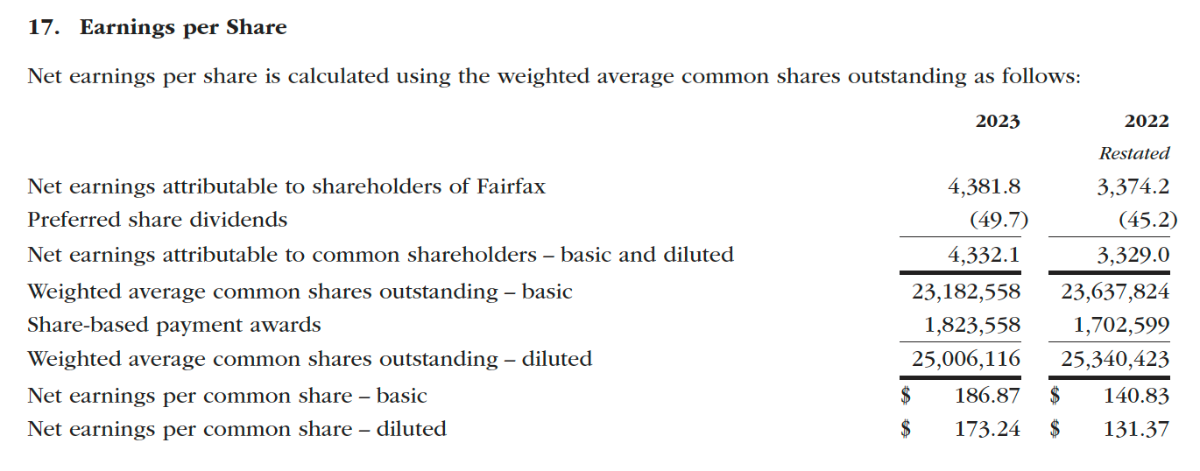

@TB Regarding the risks of investing in India, (you point to one) if you are that uncomfortable (you sound quite concerned) then you probably should just stay clear of Fairfax. I try and deal in facts and fundamentals. The successful Digit IPO happening is a fact. That suggests to me that the current tensions between the Canadian and Indian government are not impacting Fairfax. Now if we get new information/facts that suggest otherwise I will update my perspective/view. But to speculate and then try and layer that speculation onto an investing thesis... well investing is hard enough - good luck with that. Where are interest rates going to go? How bad will hurricane season be? Will a key person at Fairfax get hit by a bus? The things you could worry about is large. But that is true for every investment out there. In terms of diluted shares, your 25 million number is the weighted average for 2023. The 24,352,667 number in my table is my guess of where diluted shares might be at May 10, 2024. I have 2023 year end diluted shares at 24.98 million. But as is the case with everything I share, people need to do their own due diligence - and make sure the numbers are accurate. I am human. (Ask my wife )

-

@TB Your first question is very timely. But I am going to answer the second question first: "(b) India exposure - is this a risk given the political tensions between Canada and India governments?" Your guess is as good as mine. It didn't seem to affect the Digit IPO. It seems like tensions might be easing. We will have our answer in a couple of years. @TB What do you think? Does it worry you? If so, in what way? Your first question is one I have been thinking more about. "(a) Looks like the share awards and diluted shares are going up year on year; should the investments be marked to diluted shares outstanding." I recently updated my share tracker to better understand what has been happening with the diluted share count (it is attached below). The short answer is, yes, using diluted shares is likely a better way to calculate per share metrics. Minority interests should also likely be included as well - I am pretty sure @glider3834 has pointed this out before. I use 'effective shares outstanding' in pretty much everything I do because that tends to be how Fairfax looks at things (and I have built my models years ago using their stuff as a starting point). Bottom line, investors need to do the analysis (and uses a share amount / minority interest) in a way that works for them. Dilution really jumped in 2020 and 2021 when Fairfax's stock price went insanely low. Dilution the past 2 years appears to have slowed quite a bit. @TB What do you think? Should diluted share count be used everywhere? Regarding diluted share count I would also love hearing what other board members think. I am not an accountant. And I have never seen details of how Fairfax's share based compensation program is structured (how the awards are made; what the vesting period is etc). I think it is long term in nature. I think Fairfax also has an employee stock purchase plan - my guess is Fairfax probably has a sweetener kicks - but again, I do not know the details (if there is a sweetener, is there a vesting period etc).

-

@73 Reds Thank you for taking the time to post. I like theory. But I like to live in the real world - and getting 'real world' examples/frameworks that others use to achieve 'success' is priceless. @gfp I want to expand on something you said: "I'm a firm believer that the tax bill can make people better long term investors who might be otherwise tempted to meddle." I agree that this is probably true for lots of people. I also think the more simple a person can keep the investing process the better. Not having to think about taxes can be a big benefit. Canada today has an enormous number of tax free accounts (TFSA, RRSP, FHSA, RESP). For younger Canadian board members (or older board members with kids/family members) there is a clear path to building enormous wealth - and that is fully utilizing the gift that the Canadian government has decided to provide. The reason I bring this up is because over my investing career I have not been a 'buy and hold' type of investor. Being able to compound wealth in tax free accounts for the past 20 years has been a game changer for me and my family. Now I have been holding a very concentrated position in Fairfax since the end of 2020 and I think the company has a bright future - so perhaps Fairfax will become my first long term hold. Most of my Fairfax position today is held in my taxable and TFSA accounts (the accounts I do not want to trade in). ---------- Buffett greatly admired Walter Schloss. Schloss estimated his average holding period was about 4 years. 'Why we invest the way we do.' https://thetaoofwealth.wordpress.com/wp-content/uploads/2016/01/why-we-invest-the-way-we-do-by-walter-schloss.pdf A Superinvestor of Graham-and-Doddsville http://www.fordhamgabellicenter.org/wp-content/uploads/2021/12/Walter-Schloss.pdf What really struck me reading 'Why we invest the way we do' was how your early life experiences/set backs often sets/highly influences your investing framework for the rest of your life. It helps me better understand young family members (who have grown up in a world of plenty).

-

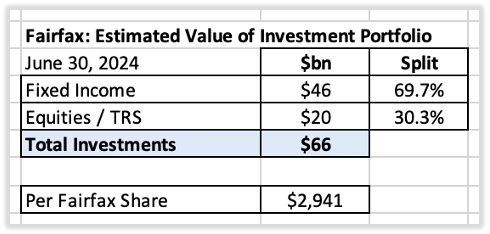

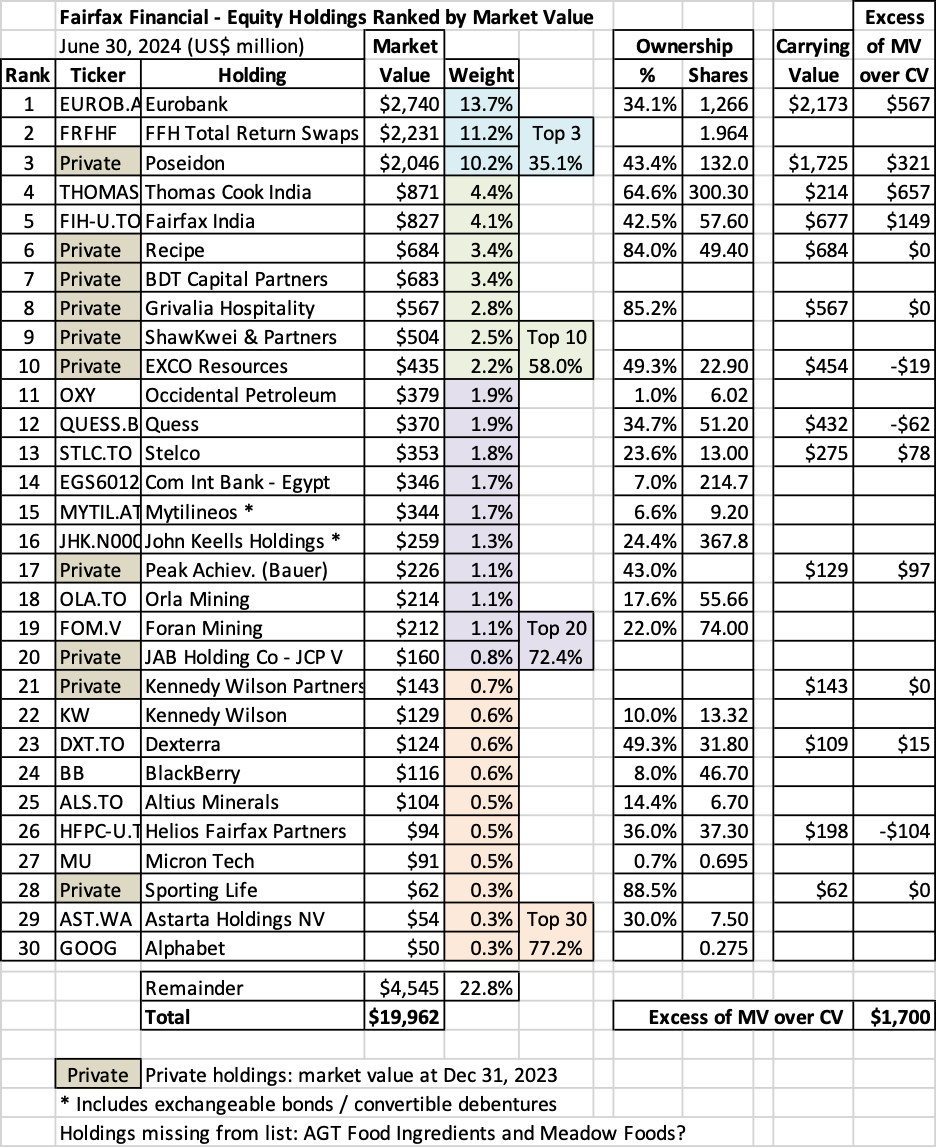

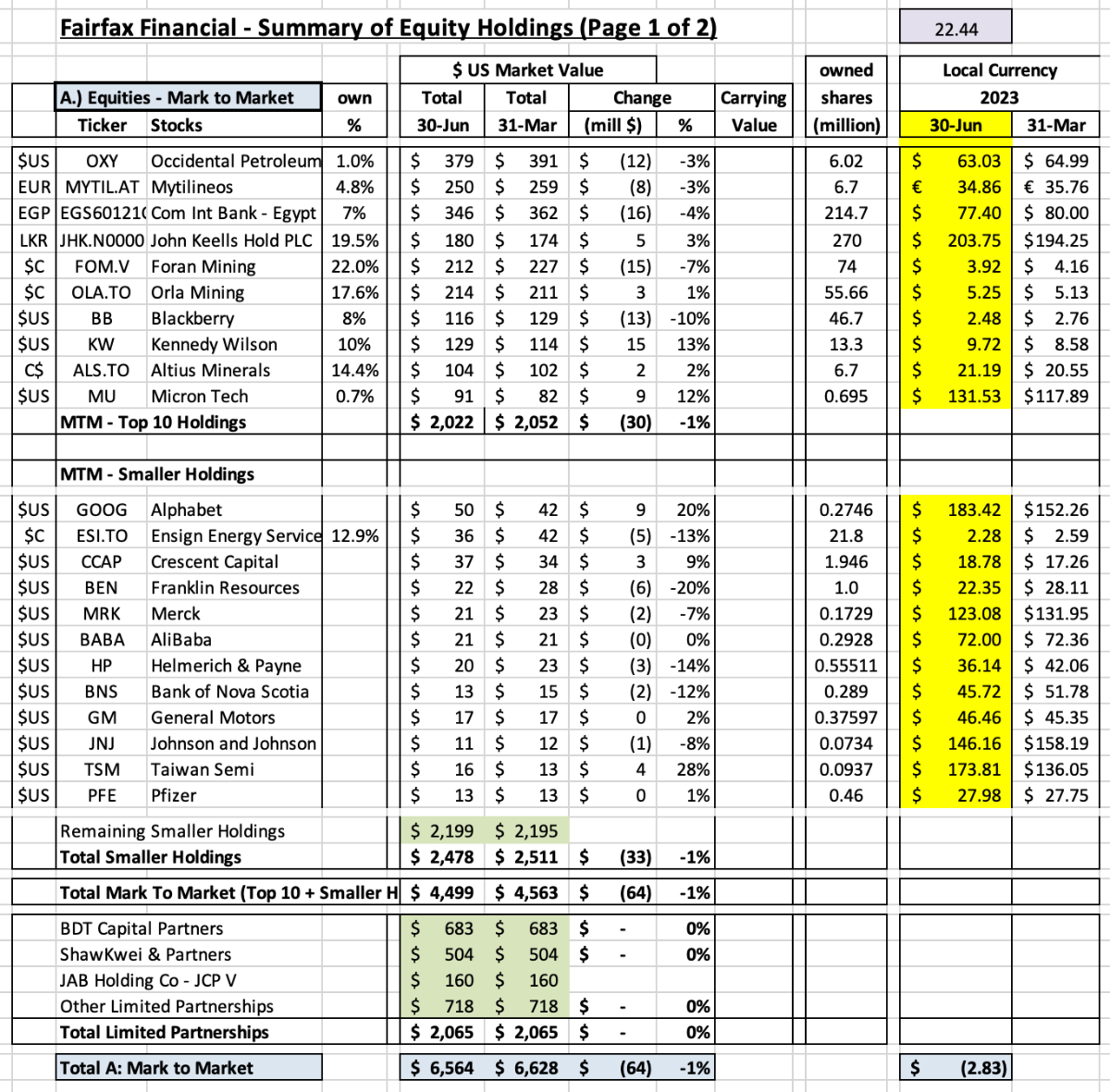

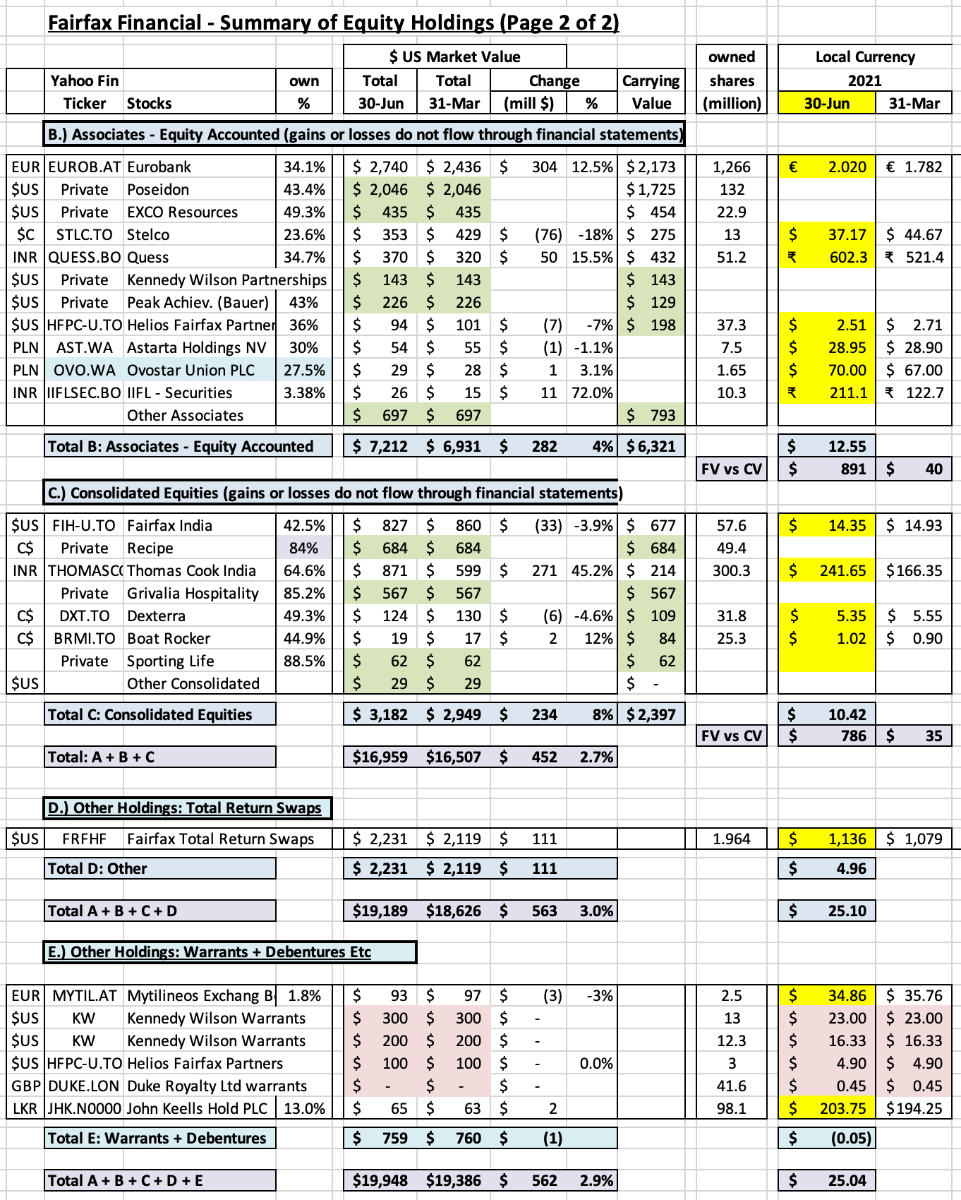

Fairfax's Equity Holdings – Size Ranking at June 30, 2024 Fairfax has a total investment portfolio of about $66 billion, with the split roughly as follows: In this post we review the holdings in the equities bucket. To value a holding, we normally use current market value, which is the stock price at June 30, 2024, multiplied by the number of shares Fairfax owns. For private holdings we use Fairfax’s latest reported market/carrying value, which was March 31, 2023. Derivative holdings, like the FFH-TRS, are included at their notional value. Additional notes: Mytilineos * : includes exchangeable bonds John Keells * : includes convertible debentures What holdings are missing from my list below? AGT Food Ingredients and newer purchase Meadow Foods (2023) are two that come to mind. Ok, let’s get to the fun part of this post. What are some of the key take-aways? 1.) Fairfax has a pretty concentrated portfolio The top 3 holdings make up 35% of the total. The top 10 holdings make up 58% of the total. 2.) Steady improvement in quality/earnings power of the top holdings over the past 6 years: What happened? Since 2018, new money has been invested very well by Fairfax (FFH-TRS, buying more of existing holdings) Some high-quality businesses have continued to execute well (Fairfax India, Stelco) Some businesses, after years of effort, have turned around (Eurobank). Some businesses that were severely affected by Covid have emerged stronger (Thomas Cook India, BIAL) Some businesses were restructured/taken private (Exco, AGT) and are now performing much better. Some low-quality businesses were sold/merged/wound down (Resolute Forest Products, APR, Fairfax Africa). Some low-quality businesses have shrunk in size due to poor results (BlackBerry, Farmers Edge, Boat Rocker). The important point is the overall quality of Fairfax’s largest holdings have been steadily improving – as a result, after years of effort, their earnings power has increased dramatically. This should result in higher overall returns from the equity portfolio in the coming years. 3.) A slow shift away from mark-to-market holdings. Today, less than 50% of the total portfolio is held in the mark-to-market bucket. Back in 2019, my guess is closer to 80% of the total portfolio was held in the mark-to-market bucket. This shift should have the effect of smoothing Fairfax’s reported results moving forward, especially during bear markets. As a reminder, in Q1 of 2020, Fairfax had $1.1 billion in unrealized losses (when the equity portfolio was much smaller). As more holdings shift to the ‘Associates’ and ‘Consolidated’ buckets, it is the trend in underlying earnings at the individual holdings that will matter to Fairfax’s reported results and not a stock price - earnings are much more consistent than a stock price. Lower volatility in reported earnings should help Fairfax’s valuation (as volatility is considered bad by Mr. Market). This shift will also start to create a Berkshire Hathaway problem for Fairfax: over time book value will become an increasingly poor tool to use to value Fairfax. Why? The value of the ‘Associates’ and ‘Consolidated’ companies captured in book value each year will fall short of the increase in their true economic value. Look at Fairfax's top 5 holdings; 4 of them are showing an excess of market value over carrying value of $1.7 billion. Thomas Cook India has a market value of $871 million and a carrying value of only $214 million (excess od MV over CV is $657 million). I wonder when Fairfax will start unlocking some of this significant hidden value. Bottom line, Fairfax looks very well positioned today. But the story gets better: like the past 6 years, I expect the quality of Fairfax's equity holdings to continue to improve in 2024. That will improve future returns. And, like a virtuous circle, the cash flows will be re-invested growing the companies even more.

-

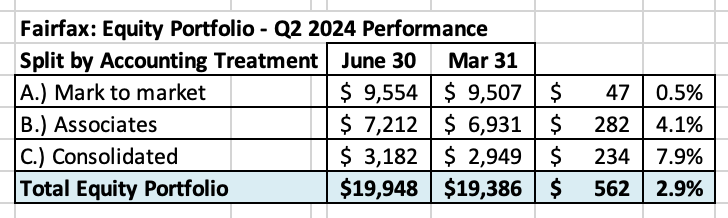

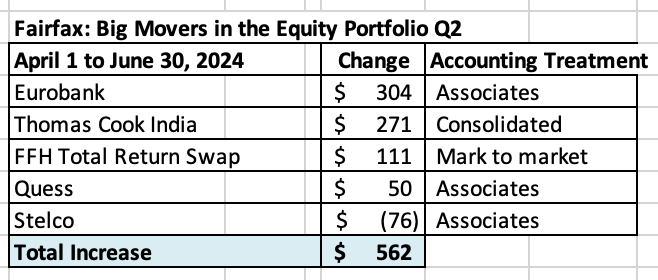

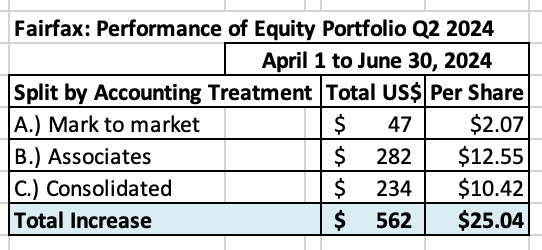

Fairfax’s equity portfolio (that I track) increased in value in Q2 by about $562 million (pre-tax) or 2.9%, which is a solid result. It had a total value of about $20 billion at June 30, 2024. Notes: Like Q1, my numbers for Fairfax India for Q2 will be off. In my spreadsheet I include the change in Fairfax India’s stock price (which declined $33 million in Q2). In Q4, 2023, Fairfax India sold a chunk of IIFL Finance which dropped its ownership position to 15.1%, which flipped the position from an accounting perspective from an Associates holding to a Mark to Market holding. IIFL Finance's stock had a big sell off in Q1 (a headwind) and it has rebounded nicely in Q2 (a tailwind). Bottom line, for Q2, I would expect Fairfax’s mark to market gains to be a little higher than my numbers driven by the increase IIFL Finance. Another wildcard will be Digit. It completed its IPO in Q2. When Fairfax reports Q2 results we should get an update on exactly how much Fairfax owns and how the position is valued (and it there were any changes). Digit is not an equity holding but depending on how the position is valued it may impact the gains (losses) that Fairfax reports. I include the FFH-TRS position in the mark to market bucket and at its notional value. I also include warrants and debentures that Fairfax holds in the mark to market bucket. My tracker portfolio is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 48% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 51% are Associates and Consolidated holdings. Over the past couple of years, the share of the mark to market portfolio has been shrinking. This means Fairfax's quarterly results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of about $562 million = $25/share The mark to market change is an increase of $47 million = $2/share. The change in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports results each quarter. (Note: see my comment on Fairfax India and IIFL Finance earlier in this post). What were the big movers in the equity portfolio Q1-YTD? Eurobank is up $304 million and it is Fairfax’s largest equity holding at $2.7 billion. Thomas Cook India is up $271 million and is now Fairfax’s 4th largest holding at $871 million. The FFH-TRS is up $111 million and is Fairfax’s second largest holding at $2.2 billion. Quess is up $50 million. Market value is $370 million (carrying value is $432 million). Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1.677 billion or $75/share (pre-tax). The 'excess' of FV to CV has been materially increasing in recent years. Book value at Fairfax is understated by about this amount. Associates: $891 million = $40/share Consolidated: $786 million = $35/share Equity Tracker Spreadsheet explained: We have separated holdings by accounting treatment: mark to market, associates – equity accounted, consolidated, other Holdings – total return swaps. We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. This spreadsheet contains errors. It is updates as new and better information becomes available.

-

No. My TFSA is for buy and hold. My swing trades are only in my RRSP/LIF accounts.

-

@Crip1 As a general rule, i prefer to own Fairfax over Fairfax India. Fairfax continues to be a monster position for me. About 25% of my total portfolio today is for shorter term/tactical trades and/or cash (all in tax free accounts). I was sitting on a fair bit of cash (over 15%) when Fairfax India dropped to $13.80 so i decided to make it a small 3% position. For these types of trades, I only buy positions in companies i am comfortable holding for the long term (because it’s not knowable WHEN the stock might move higher). And i keep my weighting small enough so that i can meaningfully add if the stock continues to sell off (I would have been comfortable taking my Fairfax India position to a 5% weighting - perhaps higher - if it had continued to fall to below $13). Fairfax closed Friday at US$1,090. That is getting close to a price where i might want to add to my position. We are also beginning hurricane season - so it would not surprise me to see the shares of all P/C insurers sell off IF we get a couple of big events. Bottom line, i want to have some cash on hand to take advantage in any temporary weakness that might happen in Fairfax shares. I like to flex my Fairfax position up and down (perhaps by 5% or 10%) depending on what the share price is doing. So given the weakness in Fairfax shares on Friday (dropping to an interesting level) and the opportunity to lock in a 2 week gain of almost 8% in Fairfax India i decided lock in the gain. i have done this with Fairfax India many times over the past 3 years. I love the optionality of having some cash on hand. One other factor was Canfor. The stock closed today at C$14.15. I think that is wicked cheap. I own a little (average price of $14.70). If it falls below $14 i will likely add. I have been in and out of Canfor probably 3 times already this year. Small 4% to 8% gains each time. Stelco is also at an interesting price (C$36.67). Sorry for all the detail. I just wanted to provide some information of a few of the variables that were/are rattling around in my head. It is sometimes a pretty fluid process for me. Lots of different variables at play. I am sure it looks pretty crazy to an outsider (someone not inside my head). But my process has usually worked out pretty well for me.

-

To close the loop, I exited my Fairfax India position today. The stock was up almost 8% in two weeks; not sure what caused the big increase Friday/today but I'll take it. The position was purchased in tax-free accounts (RRSP). I will be happy to re-establish a position should the stock aggressively sell off again.

-

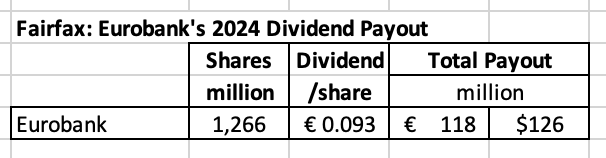

@glider3834 Thanks for posting this. On June 6, 2024, Eurobank announced it had received approval from the ECB to pay a dividend equal to 30% of Net Profit for 2023. The final distribution will be approved at Eurobank’s annual meeting on July 23 2024, with the cash likely to be distributed in August. Fairfax is expected to receive a payment of about $126 million. Because Eurobank is an associate holding the dividend payment will not show up in Fairfax’s reported results in ‘interest and dividend income’ – that bucket is for mark-to-market holdings. Eurobank paying an annual dividend is another new and meaningful income stream for Fairfax. For context, in 2023 Fairfax reported total dividends received (on common and preferred stock) of $134 million. Eurobank’s expected dividend payout almost doubles this amount. This is a watershed moment for both Eurobank and Fairfax. For Eurobank, the dividend payout is the final confirmation their turnaround has been successfully completed. Eurobank’s goal is to increase the payout ratio to 40% in 2025 (Net Profit for 2024) and 50% in 2026 (Net Profit for 2025). For Fairfax, Eurobank is a great example of the significant turnaround that they have been able to execute with their many poorly performing legacy equity holdings from 2014-2017. Hundreds of million is losses every year (write downs, capital infusions etc) from that collection of holdings has now been replaced with hundreds of millions in gains – the ‘swing’ might be as high as $500 million per year. A significant headwind to reported results has now become a significant tailwind. The turnaround at Eurobank the past 3 years has been epic. And now Fairfax is getting paid. It highlights why Fairfax is such a good partner: patient, demanding, loyal, long term. But this doesn’t mean Fairfax is a push-over… Eurobank had to do its part – its management team has executed exceptionally well, especially over the past 5 years. Importantly, Eurobank looks exceptionally well positioned with lots of solid opportunities to continue building shareholder value. Eurobank's Announcement https://www.eurobank.gr/en/group/grafeio-tupou/etairiki-anakoinosi-06-06-24#:~:text=million-,Eurobank announces ECB's approval for €342 million dividend payment,first payout in 16 years&text=Eurobank Ergasias Services and Holdings,or €0.0933 per share.

-

@PJM The attached Excel file has what I have for Fairfax India (FIH tab). It has not been updated for 2 years (2022?)? But it might be better than starting from scratch. The Fairfax India tab shows you Fairfax's increase in ownership over the years. The BIAL tab shows you Fairfax India's increase in ownership over the years. This file also contains my share information for most of Fairfax's equity holdings. Fairfax Charts - Subs.xlsx

-

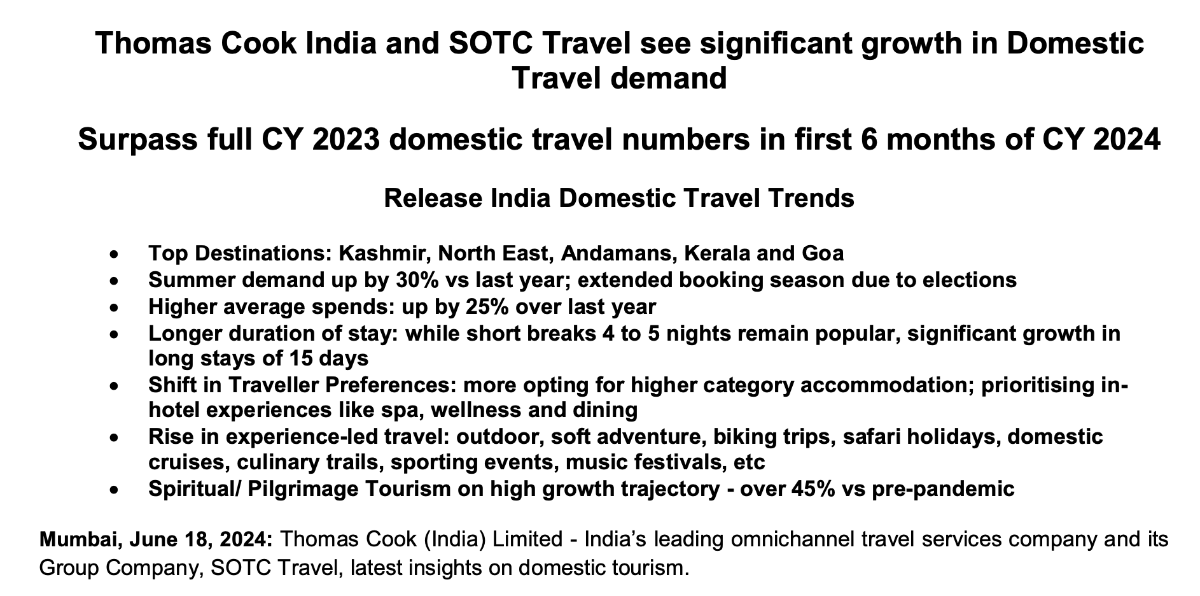

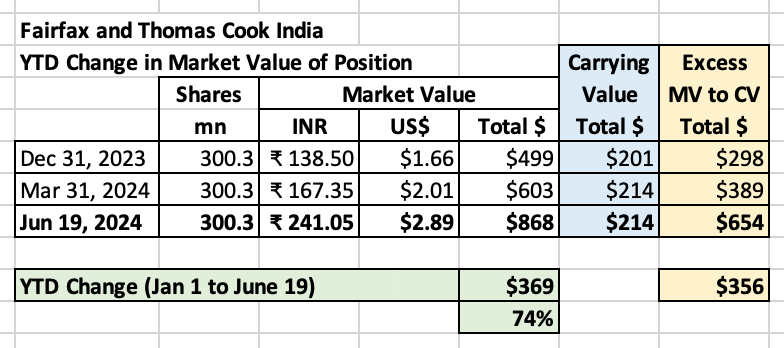

@nwoodman , thanks for the info. I was wondering what was spiking the share price of Thomas Cook India higher. Fairfax's stake in Thomas Cook India now has a market value of $868 million. It is up 74% YTD. TCI is now Fairfax's 5th largest equity holdings (after Eurobank, Poseidon, FFH-TRS and Fairfax India). Excess of market value to carrying value is about $654 million. Fairfax is getting so far offside with this holding (FV is so much higher CV) somebody better let Muddy Waters know because Fairfax is probably doing something terribly wrong with how they are marking this position on their books! Why is Thomas Cook India headed higher? Surpassing CY 2023 domestic travel numbers in the first 6 months of CY 2024. The runway looks very long for this holding. ----------

-

@ranimo When I look at Fairfax, when it comes to capital allocation, I value their track record from 2018 to present MUCH MORE than their track record 2017 and earlier. And the facts are clear - Fairfax's capital allocation since 2018 has been best in class (when compared to P/C insurance peers) and it's not even close. That is 6.5 years and running. Now I do closely monitor what Fairfax is doing. If they do something significant that I don't like - something that materially impacts the fundamentals of the business - then I will do what any rational investor would do: I would likely reduce my exposure. That is the same for every investment I hold. My recent investment in Fairfax India is not complicated: it was because I thought it represented good value. Yes, I also own Fairfax. Am I concerned about my total weighting (Fairfax India and Fairfax)? No.

-

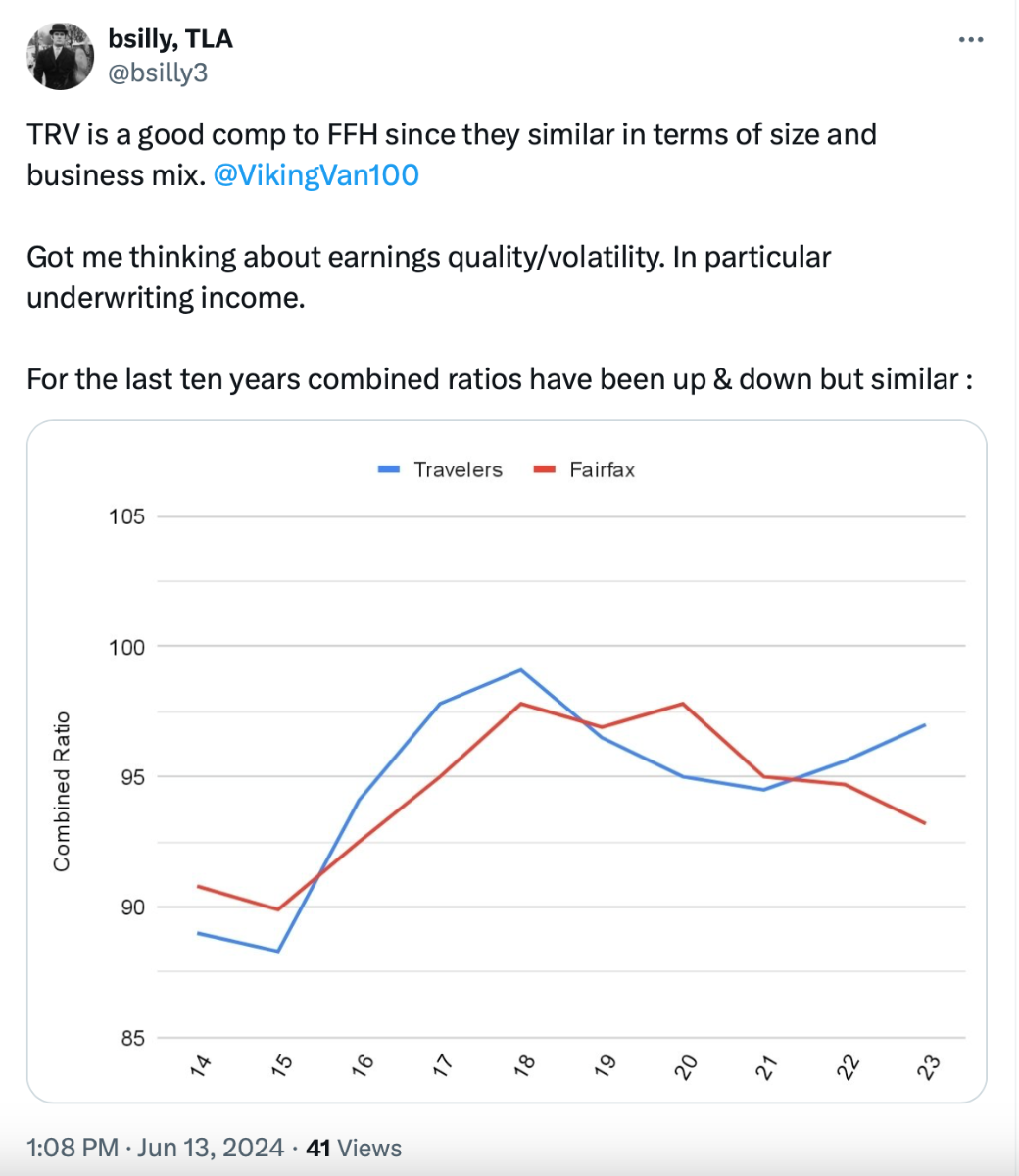

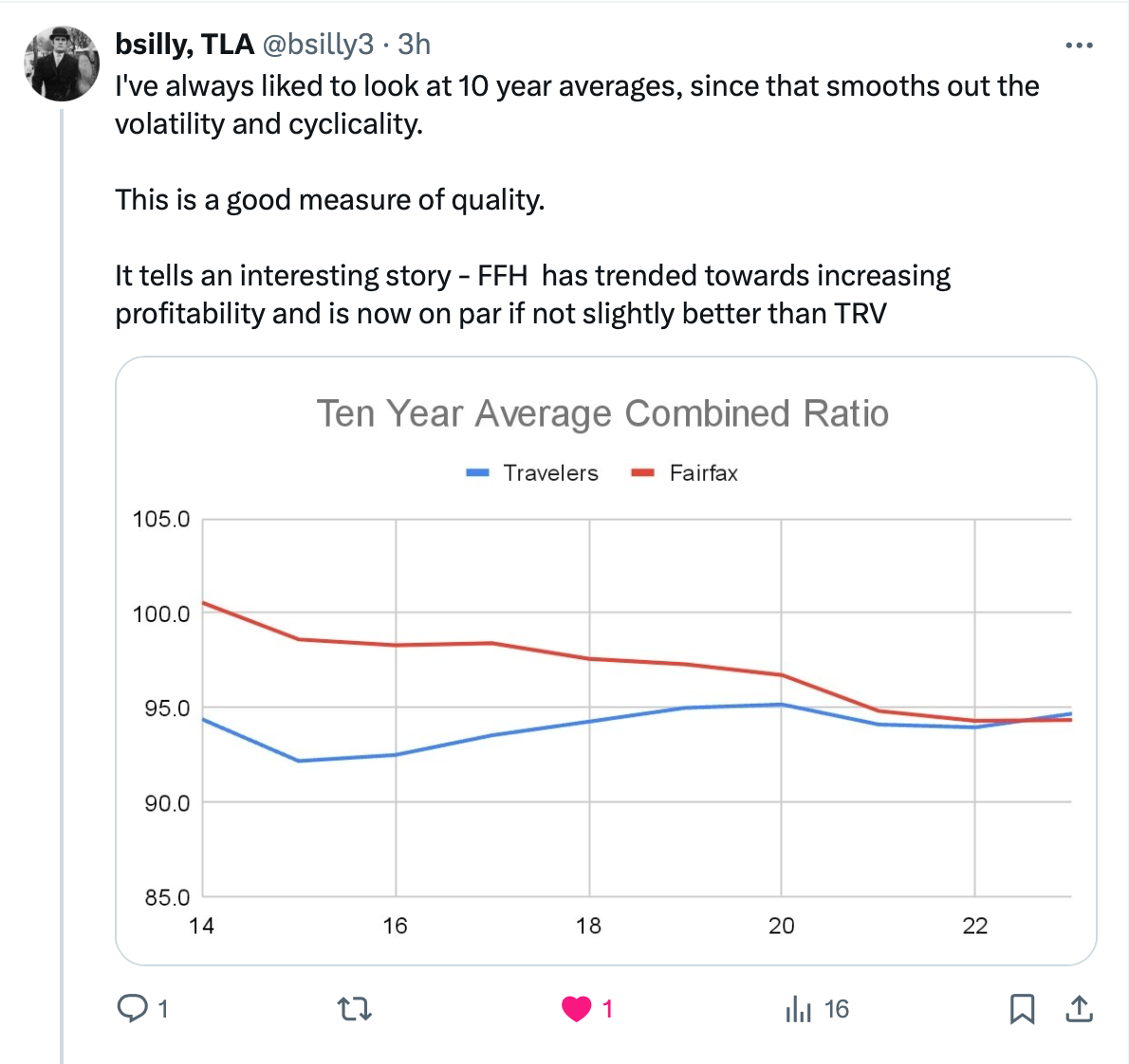

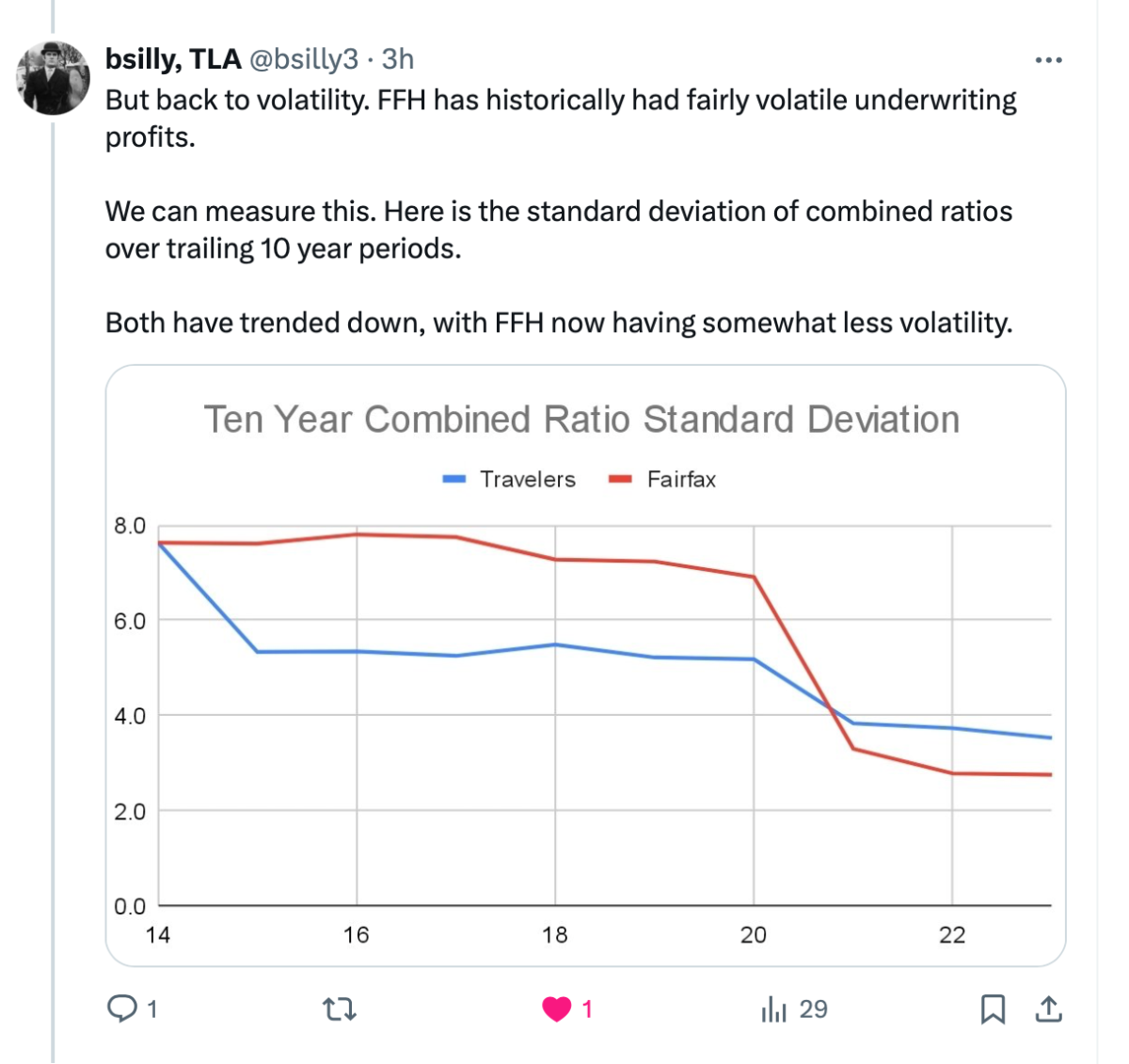

Below is an interesting thread (4 parts) posted by 'bsilly,TLA' on twitter today. I have a thesis that, under Andy Barnard, the quality of Fairfax's P/C insurance business has been slowly, incrementally improving over the past decade. bsilly's thread seems to support that idea. This is not priced into Fairfax's stock today. Just another tailwind. https://twitter.com/bsilly3/status/1801345889262571548 ---------- ----------- ----------- -----------

-

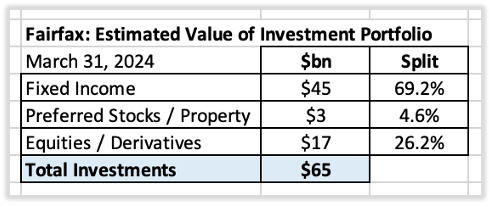

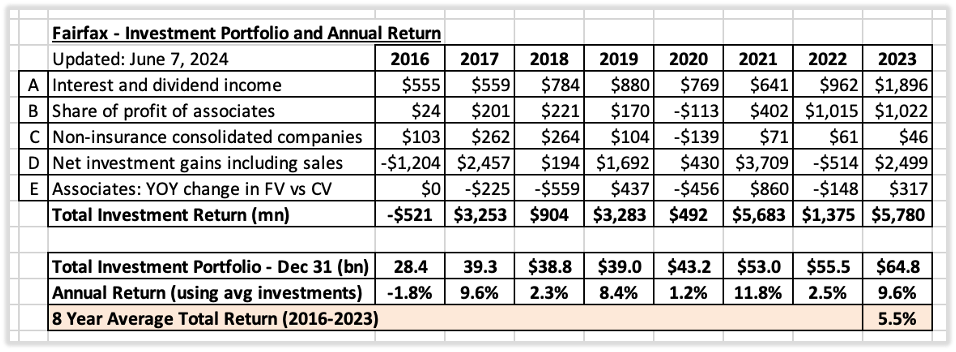

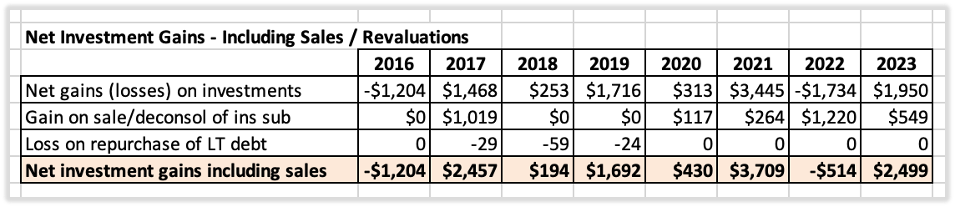

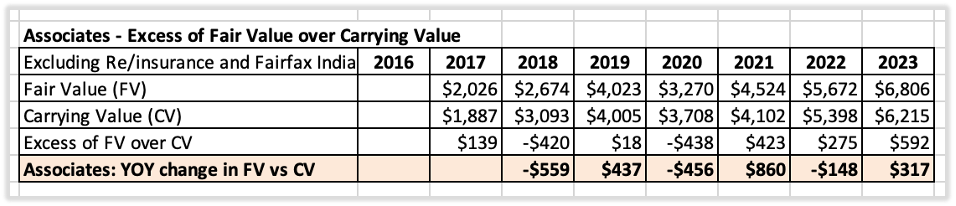

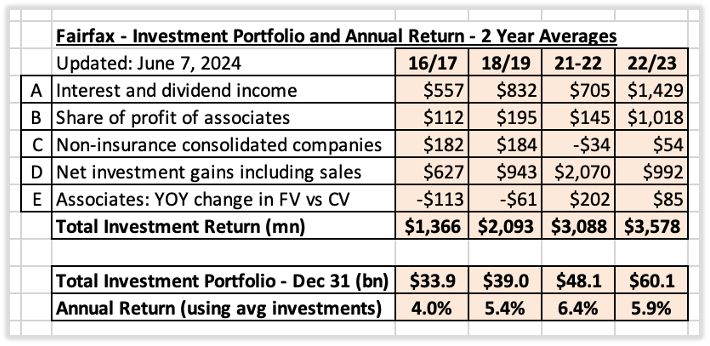

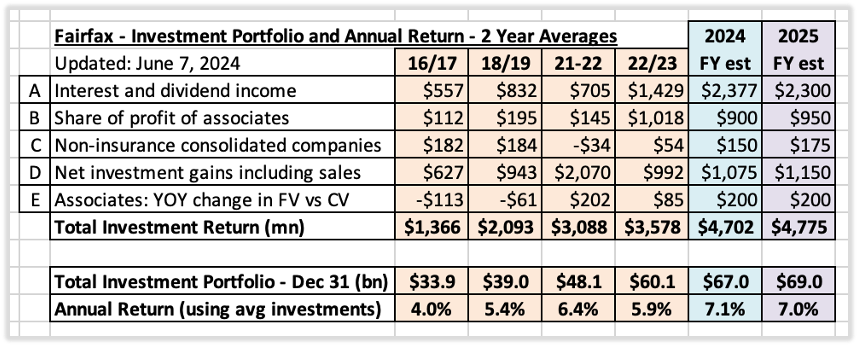

Investment Portfolio: A Review of Returns From 2016-2023 and Estimate for 2024 Two things drive earnings at Fairfax: The underwriting profit it earns on its insurance operations. The return it earns on its investment portfolio. In this post we will review the return Fairfax earns on its investment portfolio – in total dollars and as a percent. We will start by looking at the past (2016-2023). We will then use what we learn as inputs to help us build a forecast for 2024 and 2025. What is the value and composition of Fairfax’s investment portfolio? Fairfax has an investment portfolio with a value of about $65 billion at March 31, 2024. This does not include FFH-total return swap position (with a notional value of about $2.2 billion). Methodology The total investment return for Fairfax can be calculated using the following inputs: Income streams: A. Interest and dividend income Interest income earned from the fixed income portfolio. Dividend income earned the mark to market equity holdings. B. Share of profit of associates Fairfax’s share of pre-tax earnings from Eurobank, Poseidon, EXCO Resources, Stelco and Fairfax India. C. Non-insurance consolidated companies Pre-tax earnings from Recipe, Grivalia Hospitality, Thomas Cook India, AGT Food Ingredients, Dexterra, Sporting Life and Boat Rocker. D. Net gains (losses) on investments Unrealized gains from investment portfolio (stocks, fixed income etc). Large realized gains from asset sales and revaluations (including insurance). We also include one more item: E. Excess of fair value over carrying value: This captures the change in value each year of Fairfax’s associate equity holdings that is not captured in Fairfax’s financial statements (earnings or book value). We include it because this is real value that is being created each year. Historical returns: 2016-2023 For the 8-year period from 2016 to 2023, Fairfax earned an average total return on its investment portfolio of about 5.5% per year. That is a much better return than I would have imagined. Note: D.) Net investment gains including sales We have grouped three items into this bucket. All realized and unrealized gains, from both investments and insurance. And the losses from pushing out the maturities on long term debt. Note: E.) Associates: YOY change in fair value vs carrying value Equity holdings classified as ‘associates’ are valued on Fairfax’s balance sheet at their carrying value not their fair value (market value). Over the years, the fair value of this group of holdings has increased at a faster pace than it’s carrying value. This is value that is being created each year. At some point, Fairfax will harvest the gains. To allow us to focus on Fairfax’s investment portfolio, we have excluded insurance, reinsurance and Fairfax India from our calculations below. Historical returns: 2016-2023 – Calculated in 2-Year Averages If we look at Fairfax’s returns from this time period using 2-year averages we can smooth out much of the annual volatility and get a much clearer picture as to what has been going on under the hood. 2016 – 2017 Average annual return on the investment portfolio bottomed out at 4%. Last of the equity hedges was removed in late 2016 resulting in a $1.2 billion loss. 2018-2019 Average annual return improved to 5.4%. The return improved despite the bear market in stocks in December 2018. 2020-2021 Average annual return improved to 6.4%. The return improved despite the bear market in stocks in 2020 (that hit Fairfax’s holdings especially hard, given they were skewed to cyclicals). 2022-2023 Average annual return fell to 5.9%. However, this was an amazing return when we factor in what happened in 2022: Historic bear market in bonds. Bear market in stocks. Fairfax’s average return in 2022-2023 is actually much better than most investors realize. Why? Fairfax’s massive bond portfolio is mark to market (unlike most P/C insurance peers). Fairfax’s 2-year return of 5.9% includes the carnage caused by the greatest bond bear market in history in 2022. Summary (2016-2023): When viewed through 2-year averages it is clear that Fairfax’s total return on its investment portfolio has been steadily moving higher over the past 8 years. Looking forward: Estimates for 2024 and 2025 The significant headwinds that were holding down Fairfax’s returns from 2016-2023 are now gone. And significant new tailwinds have emerged. Fixed income: portfolio earned 5% in Q1, 2024. Equities: the earnings power of Fairfax’s $19 billion equity portfolio is shining through. My estimate is for Fairfax to earn a total return of about $4.7 billion in 2024, or 7.1% on its average investment portfolio of $65.9 billion. Importantly: Quality: Most of the return (70%) is now coming from high quality sources (interest and dividends and share of profit of associates). The much higher total investment return being delivered by Fairfax is sustainable and durable. Volatility: Given the sources, the return will also be much less volatile than in the past. ---------- Investments Per Share – The Trend From 2016-2023 What has been the growth profile of Fairfax’s investment portfolio? At December 31, 2023, Fairfax’s investment portfolio was $64.8 billion or $2,816/share. From 2016 to 2023, Fairfax’s investment portfolio (per share) has a CAGR of 12.6%. That is an impressive growth rate. A double whammy When it comes to Fairfax’s investment portfolio, two things are happening at the same time: The size of the investment portfolio is growing nicely over time. From 2016-2023, investments per share CAGR = 12.6%. The return being earned on the investment portfolio has increased to over 7%. In 2016/2017, the average return was 4%. This is a great set-up for Fairfax shareholders. The total investment portfolio should continue to grow nicely and a return of +7% looks sustainable in the coming years.

-

@ranimo To answer your question I need a little more information. When you say “basically, the risk that Prem loses his touch and keeps making errors in judgment”, can you provide specific examples of what his past errors in judgement were?

-

@rajpgokul Thanks for taking the time to share your thoughts. Very insightful.

-

@rajpgokul That was a very well done write-up of Fairfax India - one of the best that i have read. It was very rational, concise and hit on the key points. It is also great to get input from a local investor. Thank you for sharing. Please share anything else you have on Fairfax India/holdings or Fairfax/holdings. Do you have any thoughts on a potential IDBI bank bid by Fairfax India/Fairfax? I am wondering what kind of asset IDBI Bank might be? Something with a lot of potential? Decent management team? Or something probably best avoided? Is banking in general a good business in India? Is that industry well positioned to benefit/grow over the next decade (it looks like it from afar)? Fairfax controls CSB Bank… with my limited understanding of that holding… it appears quality of management has been key to its successful turnaround. Banking certainly appears to fall within Fairfax India’s (and Fairfax’s) circle of competence with CSB Bank (and Eurobank).

-

@Crip1 Good idea. I have reestablished a starter position in Fairfax India at $13.80. The publicly traded holdings have increased nicely so far in Q2 so we should see a nice bump in book value when they report Q2. BIAL continues to execute well. It’s a little surprising to me that the stock continues to trade below $14.