Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Here is a quick summary of the changes in Fairfax's 13F filing. I have guessed at the average prices. The subtractions were much bigger than the additions.

-

@73 Reds The fact that Fairfax has been able to attract (and keep) shareholders of your quality gives me confidence that they are moving in the right direction. I agree with you - I think Fairfax has learned a great deal over the past 10 years. They have also had some important personnel changes (adding Wade Burton/Lawrence Chin, subtracting Paul Rivet, promoting Peter Clarke to name just a few). Lots of investors don't want to invest in Fairfax today (or hold their shares long term) because of the very visible mistakes Fairfax made in the past. Given what we have seen from the management team at Fairfax over the past 6.5 years, I think the past mistakes actually make Fairfax a much stronger company today. As an investor, given what we know today, it makes me more confident in their future - it makes me want to invest in the more. It is really counter intuitive. The cost of Fairfax's past mistakes was bourne by shareholders from 2010 to 2020 - and it was not pretty. Someone buying Fairfax shares in 2020 or later have been big beneficiaries of Fairfax's past mistakes - Mr. Market was irrationally pessimistic. What were the big mistakes? The disastrous equity hedge/short 'decision' cost the company dearly (financially and reputation ally). But it also exposed a massive flaw in their investing framework. Blackberry was an unmitigated disaster. As was Abiliti-Bowater investment. Both of these investments exposed more flaws in their investing framework. Sandridge Energy, Fairfax Africa, APR Energy, Farmers Edge were all terrible investments. These investments exposed more flaws in their investing framework. These all became great teachable moments for Fairfax. Bottom line, Fairfax looked in the mirror and didn't like what they saw - they recognized they were the problem. Ending the equity hedge in late 2016 was the start and also the most important move (it was the biggest drag on results). By 2018, it was clear Fairfax started putting a much premium on management (Seaspan/Sokol and Stelco/Kestenbaum investments). In late 2020, Fairfax closed out its last short and very publicly promised not to repeat the equity hedge/short disaster. Around 2020/2021, Fairfax also stopped being a piggy bank to underperforming equities in their portfolio - generating cash flow became the new mantra. If they got cash from Fairfax it usually required restructuring by the company, a pound of flesh (increase in Fairfax's ownership on very favourable terms) etc. Fast forward to today and you have a MUCH stronger company. Investors have never actually seen this version of Fairfax before. Fairfax today looks like a star athlete that has just entering their prime. With Fairfax, there is a good change we haven't even seen their best performance yet. And that is why I push back so much on people on this board who think Fairfax is at 'peak earnings' today. Peak? I think we are just getting a glimpse of what they can do. The crazy thing is Fairfax's stock is priced today like the company will be going into a steep earnings decline looking out 3 or 4 years. A big decline? WTF? So even if I am completely wrong in my outlook for Fairfax, the stock will likely still perform reasonably well moving forward. And if I am right... well that would result in significant upside - that I am getting for free today. What a wonderful set-up. And that is why I love investing so much.

-

@wondering A lot of the discussion points in my posts are fluid… things that looks interesting that could go in different directions in the future. I am not sure what Fairfax’s thinking is on weightings within the equity bucket (mark to market, associate or consolidated). I agree with your summary: “My thinking was always Fairfax are value hunters and they will go where they see value. Period. The way they hold the investment in secondary.” i would add a little to your comment: Fairfax also seems to like the true value of their holdings to be reflected in book value (at least looking at it from an historical perspective). Having said that, i wonder if they do not want to have some non-insurance consolidated holdings. ‘Bond type’ holdings that spit out cash. As a important offset to the P/C insurance business. But even here, if there is an opportunity to realize a big investment gain (like take take Recipe public in the future) my guess is they will do it. I think there has been a trend in the general market towards more private and fewer public holdings. Fairfax has many deep pocketed partners. Perhaps part of what is happening at Fairfax i s just a microcosm of what is going on in the larger marketplace (towards more private holdings). It might also be a reflection of Fairfax’s size - as Fairfax gets bigger it makes sense when they make investments they will own bigger stakes in companies (+20% or more) which will push more investments into the associates bucket or (50% or more) the consolidated bucket. And some holdings are just better suited to be held as private holdings - versus public. AGT Food Ingredients is a great example if this - their business is too volatile and none of their peer group are publicly traded. I think taking Recipe private was smart for the business - my guess is they needed to restructure their operations after 10 years of acquisitions and this is difficult to do as a publicly traded company (they got started on this in the 2 years before Fairfax took them out). Of interest, when i calculate Fairfax’s splits (mark to market, associate and consolidated) i include the FFH-TRS in the mark to market bucket. If you exclude that holding (it is a derivative), the mark to market bucket is even smaller. And within the remaining holdings in the mark to market bucket, you have the significant limited partnership holdings that total $2 billion - BDT, ShawKwei, JAB etc. The true mark to market ‘common stock portfolio’ is $4.5 billion out of $20 billion in ‘equities’ and +$65 billion in total investments.

-

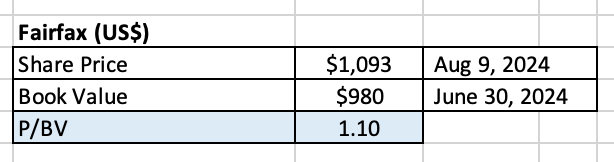

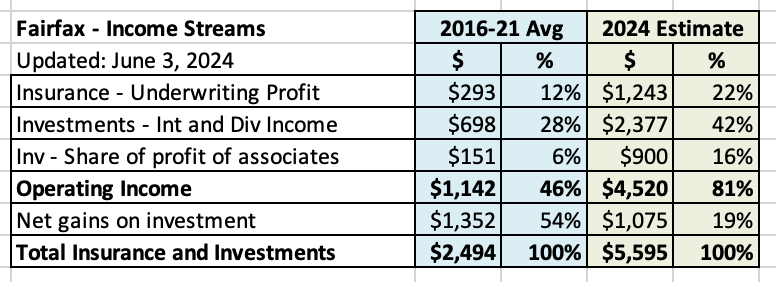

Volatility and Fairfax - Part 2 Earlier this week we began our exploration of volatility in financial markets and the different ways it impacts Fairfax. Given the size of the topic, we broke our analysis into two parts/posts. In our first post, we introduced the concept of volatility and then explored the following: Part 1: Fairfax’s ability to profit from volatility Clink the link to read Part 1: https://thecobf.com/forum/topic/20517-fairfax-2024/page/72/#comment-574244 Below is part 2 of our discussion of volatility. Part 2: The impact of volatility on Fairfax’s short term reported results ‘New Fairfax’ Fairfax as a company has undergone a number of important changes ‘under the hood’ over the past 5 years. These changes have make the company a very different animal from the company that existed previously. To help differentiate between the two versions, I call Fairfax as it exists today ‘New Fairfax’ and the Fairfax from +5 years ago ‘Old Fairfax.’ Volatility of Fairfax’s reported results The historic reported results (earnings and book value) of ‘Old Fairfax’s’ were always VERY volatile. Not just the quarterly results, but also the annual results. This was due to a number of reasons - largely related to its business model but also how Fairfax was executing the business model. Moving forward, my guess is the reported results of ’new Fairfax’ will be much less volatile than what investors are used to. Why? There has been a significant change in the size of the income streams that Fairfax generates - with a massive shift to lower volatility, higher quality operating earnings. The management team at Fairfax has been making many important changes ‘under the hood’ that suggests reported results in many of Fairfax’s individual income streams should be less volatile moving forward. Let’s dig into each of these a little more. Fairfax’s results are now being driven by high quality operating earnings Let’s first look at the time period from 2016 to 2021. Over this 6 year period, Fairfax’s biggest income stream was investment gains and it represented an average of 54% of all of Fairfax’s income streams. Operating earnings (interest and dividend income, underwriting income and share of profit of associates) averaged 46%. From 2016-2021, investment gains were - by far - the most important income stream for Fairfax. This income stream was also exceptionally volatile. In turn, this caused Fairfax’s reported results to swing quite dramatically from year to year. ‘New Fairfax’ This split - investment gains vs operating earnings - has changed dramatically over the past four years. As Prem said very loudly at the AGM this year: ‘Fairfax has been transformed.’ Operating income (interest and dividend income, underwriting income and share of profit of associates) has exploded in size at Fairfax over the past 3 years. It averaged $1.1 billion per year from 2016 to 2021. In 2024 it is estimated to come in at around $4.5 billion, an increase of $3.4 billion. This is a massive increase. Operating income is considered by Wall Street to be the ‘high quality’ source of earnings for P/C insurance companies - because they are considered to be predictable and durable sources of income. On the other hand, given their unpredictability in the short term, investment gains are considered to be a ‘low quality’ source of earnings. Today, operating income is Fairfax’s largest income stream - it now represents 81% of Fairfax’s total income streams. Investment gains now represent 19% of Fairfax’s income streams. There are two really important points: The total size of Fairfax’s income streams has exploded in size. All of the growth has happened in the operating income bucket. This has profound implications on how changes in financial markets will affect Fairfax’s reported results (earnings and book value) in the future (when compared to the past). Fairfax’s reported results will likely be much less volatility than in the past. But there is more to the volatility story. Let’s take a closer look at what has been going on under the hood at Fairfax Fairfax has three economic engines: P/C insurance Investments - Fixed income Investment - Equities Let’s review some of the changes that have happened in each of these buckets in recent years. P/C insurance Runoff is now a much smaller part of Fairfax’s total P/C insurance business. In 2016, the runoff business represented 20.5% of shareholders’ equity at Fairfax. In 2023, runoff represented 1.9% of shareholders’ equity. Fairfax has been shrinking its total catastrophe exposure (as a company) in recent years, especially at Brit. The hard market in P/C insurance has now been going on for 4.5 years - Fairfax should be well reserved. All things being equal, this suggests that Fairfax’s reported underwriting results will likely be less volatile in future years than they were in the past. Investments: Fixed income As required by regulators, Fairfax began using IFRS 17 accounting on January 1, 2023. Moving forward, when interest rates change, IFRS 17 (and how it accounts for insurance liabilities) will largely work as an offset to changes in the mark to market value of Fairfax’s fixed income portfolio. It will not be an exact offset (one goes up the same as the other goes down and vice versa). But it should smooth out the swings quite a bit. This suggests that large changes in interest rates should result in less volatility in Fairfax’s reported results (earnings and book value) in future years than in the past. Investments: Equities Since 2020, the composition of Fairfax’s equity portfolio has changed dramatically. Non-insurance consolidated (private) equity holdings has substantially increased in size in recent years. Recipe and Grivalia Hospitality were added to this bucket in 2022 and the Sleep Country acquisition was just announced. This group of holdings has increased in recent years to now represent about 20% of the total equity portfolio (including Sleep Country). Associate equity holdings has also substantially increased in size in recent years - to about 35% of the total equity holdings (not including Stelco now that it has been sold). Fairfax’s two largest equity holdings are in this bucket: Eurobank as of January 1, 2020 and Poseidon (formerly Atlas/Seaspan) as of Q1 2020. The non mark to market group of holdings has increased significantly in size over the past 5 years. The majority of Fairfax’s equity holdings (about 55%) are no longer mark to market type holdings. The quality of the equity portfolio has also improved materially Back in 2018, Fairfax’s equity portfolio was stuffed with many ‘problem’ equity holdings. Over the past 5 years Fairfax has done a great job of dealing with all of its poorly performing equity holdings. As a result, the overall quality of the equity portfolio has improved dramatically. There are two really important points: The quality of Fairfax’s equity portfolio has improved dramatically over the past 5 years. Over the past 5 years, the composition of Fairfax’s equity portfolio has shifted from mostly mark to market holdings to mostly non mark to market holdings (at about 55% in 2024). This suggests a big sell-off in equity markets should result in much less volatility in Fairfax's investment gains (losses) and reported results (earnings and book value) in future years than in the past. Remember, investment gains is now also a much smaller income stream for Fairfax as a percent of total income streams. So a much smaller income stream will also be much less volatile - this is a double impact. Summary Many important changes have happened at Fairfax over the past number of years: Operating income, at about 80%, is now - by far - Fairfax’s largest income stream. The P/C insurance business continues to improve in quality and shrink its catastrophe exposure. The implementation of IFRS 17 will smooth results in the fixed income portfolio. The equity portfolio has improved dramatically in quality and significantly shifted away from mark to market type holdings. All of these changes should make Fairfax’s future reported results (earnings and book value) much less volatile than in the past. Important: this does not mean that Fairfax's reported results will not have some volatility to them in the future. The point is the volatility should be much less than what we have seen in the past. Volatility and market multiple This is important because for Wall Street, earnings volatility and market multiple are linked at the hip. All things being equal, the stocks of lower volatility businesses (from an earnings perspective) usually receive a higher multiple. And the stocks of higher volatility businesses usually receive a lower multiple. My guess is Wall Street does not yet fully grasp the changes that have happened at Fairfax that will lower the volatility of future reported results (when compared to the past). As a result, ‘lower volatility’ is likely not yet priced into Fairfax’s stock. This provides another important tailwind for long term investors. Fairfax's Valuation Fairfax is trading today at a trailing P/BV multiple = 1.1 Fairfax has delivered the best growth in book value per share among P/C insurance peers over the past 5 years. We also know that Fairfax's book value is materially understated (gain from Stelco sale + excess of market value over carrying value of equity holdings). Fairfax is poised to deliver mid teens ROE in 2024 and the coming years. And now we know Fairfax's future reported results will likely be much less volatile than in the past (meaning they are of much higher 'quality'). All of this warrants a trailing P/BV multiple of 1.1? Really? Is it any surprise that Fairfax has been VERY aggressive taking out shares YTD in 2024 at a slight premium to book value?

-

@Thrifty3000 I think we can all agree that ‘baseline’ earnings for Fairfax will be very robust for at least the next three years. That is simply based on the facts - what we know today. I don’t think that is a controversial thing to say. Yes, there are downside risks. But there is also a good chance we get some upside surprises (one example: asset sales/revaluations resulting in large investment gains). For the next couple of years, i think the ‘risks’ are skewed to upside surprises for Fairfax. Parts of your analysis ignores what we know today. Is that a rational way to try and value Fairfax? Or put another way… if you had done this exact same analysis three years ago would it have helped you or hurt you in trying to value Fairfax? Especially when it came to position size (the ‘how undervalued’ a company is part of investing). PS: by ‘baseline’ earnings I mean earnings excluding unknown/extraordinary events.

-

@nwoodman thanks for pointing out the obvious to me... I did not realize Poseidon's earnings were tracking that high. At Fairfax's AGM in April, Sokol was sounding very optimistic about Poseidon'e near term prospects (earnings growth next couple of years)... looks like things are playing out as he expected. If Poseidon is able to earn $640 million per year, that would put Fairfax's share at about $277 million (43.3% ownership). For Poseidon, at June 30, 2024, Fairfax had a carrying value of $1.78 billion (and a fair value of $2.05 billion). Earnings yield on carrying value is 15.6% ($277 / $1.78). That is a pretty good return for a pretty stable leasing business kind of masquerading as a container shipping company. I think it might be time to do an update on Poseidon My guess is Fairfax's stake in Poseidon is worth much more than its carrying value of $1.78b. Just another example of Fairfax's book value being understated. Fairfax knows this - and this likely explains why they continue to buy back a significant amount of Fairfax shares at a premium to book value. Investors are likely underestimating how much 'hidden value' actually exists on Fairfax's balance sheet today.

-

Interesting. With the former rapid new-build growth phase coming to an end I was wondering what the next act was for Atlas/Sokol. But given the size of the company today, 27 new builds is not a crazy big number, especially looking out a few years. The delivery dates are out a fair bit at 2027 and 2028. Chug, chug, chug... It will be interesting to see where interest rates go from here. If they continue lower Atlas could be a beneficiary - they may be able to secure some reasonable long term rates.

-

@73 Reds I completely missed the big money when looking at Berkshire Hathaway over the years. Why? Largely because of what you so eloquently posted above - “yet-to-be-had ideas and acquisitions.” I way underestimated the P/C insurance model and the value that Buffett would generate over time from Berkshire Hathaway’s earnings and the power of compounding. I am trying to not make the same mistake a second time - this time with Fairfax. And that is another one of the things that i love about investing - the ability to apply lessons from the past to the present.

-

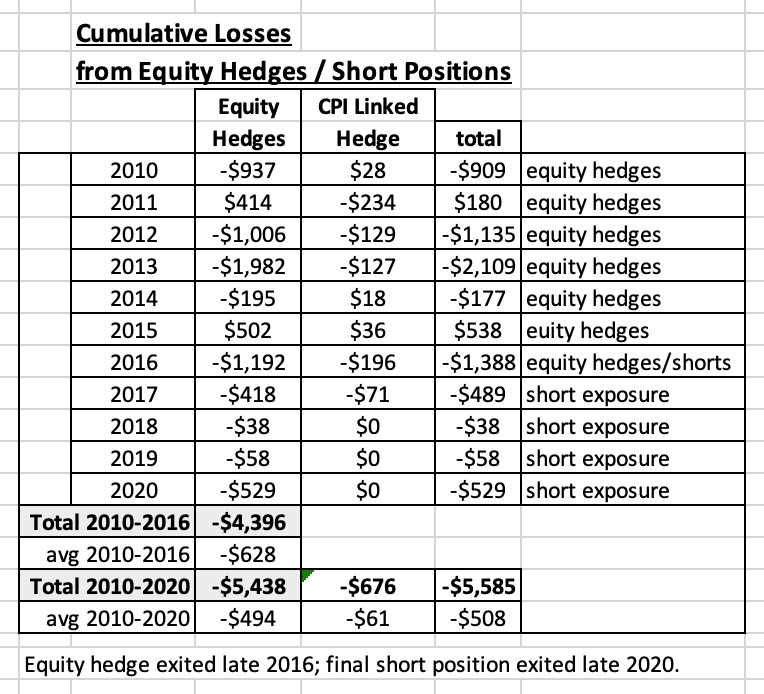

When I evaluate Fairfax's investment decisions, my watch out is an 'equity hedge/short' type decision. Something really big. From 2010 to 2020, Fairfax's equity hedge/short positions cost the company a total of $5.4 billion in losses = an average of $494 million per year. The equity hedge position was removed in late 2016. This position was the big issue. From 2010 to 2016, the equity hedge/short positions cost Fairfax a total of $4.4 billion in losses = $628 million per year. The last short position was removed in late 2020. From 2017-2020, the short positions cost Fairfax a total of $1.04 billion = $261 million per year. Exiting the equity hedge position in 2016 was a massive win for shareholders. Exiting the last short position in late 2020 was a big win for shareholders. The bottom line, at the start of 2021, the chains of the equity hedge/short positions had been completely removed from the company. It was like a $494 million annual expense that the company paid from 2010 to 2020 had been removed and Fairfax became $494 million 'more profitable' every year moving forward. The crazy thing is this 'investment' only stunted Fairfax's growth from 2010 to 2020. It really was amazing what Fairfax was able to still accomplish from 2010 to 2020 - especially the significant build out of their P/C insurance business. (The many shitty equity holdings on the books at the time was another headwind - making Fairfax's performance even more impressive.) What this shows is the incredible earnings power that exists within Fairfax - that P/C insurance (float) + active management of the investment portfolio (equities etc). Of course, 2010 to 2020 was a lost decade for Fairfax shareholders. So I am not trying to sugar coat what happened when it comes to the share price. No equity hedge/short positions. The equity portfolio has been cleaned up. The future looks bright - I can't wait to see what the Fairfax team can deliver in the coming years. What does it mean for today? Sleep Country has been a hot topic among board members - I sense lots of angst. To be honest, I don't understand all the angst. 1.) The management team at Fairfax has been executing exceptionally well since 2018. This is a long enough time for me - they have re-earned a certain amount of trust. 2.) We have no visibility into why they bought Sleep Country. There likely were many factors involved (P/C insurance capital levels, taxes, strategic fit within investment portfolio, strategic fit within total company, valuation, future prospects etc) - and we are largely in the dark. And no, I do not expect the management team at Fairfax to have to 'justify' every decision they make to investors. 3.) Sleep Country is a small purchase. It represents about 2% of Fairfax's investment portfolio and 6% of its equity portfolio. 4.) Sleep Country looks to be well managed. It is a strong franchise (in Canada - and I know this is hard for those outside of Canada to understand). It is profitable. The issue is some don't think it will earn enough (to justify the purchase price). Today, do I love the Sleep Country purchase? No. But do I dislike it? No. The bottom line, it is a non-issue for me - if Fairfax thinks this is a good decision, given their track record since 2018, I am ok with it. Done. Obesssing about small potatoes (Sleep Country) runs the risk of me losing sight of the bigger picture of why I am invested in Fairfax - I try and be careful about what (and how much) I let into my head. My watch out for Fairfax and their investments is an equity/hedge short type of decision that I don't like. Something that costs them +$500 million per year - for years. That WILL get my attention. The power of Fairfax's business model today is VERY IMPRESSIVE. Given the level of earnings, they are going to be making lots of billion dollar decisions in the coming years. They are going on the offensive. I can't wait. And I am going to try and be open minded when we learn what they are doing...

-

@73 Reds thanks for the feedback. I am going to dig into the 'company specific' part of your comment with my next post. My guess is lots of Fairfax's current shareholders are still seeing the ghosts of Fairfax's past. This will lead them to manufacture 'company-specific' issues that don't actually exist (and lead them to sell their position). This is one of the reasons why I expect Fairfax shares to be more volatile going forward (particularly to the downside). And as I said, that will likely provide Fairfax with a wonderful opportunity to take out a meaningful amount of shares in the coming years. "know what you own" - bingo! That is the key that unlocks the treasure chest.

-

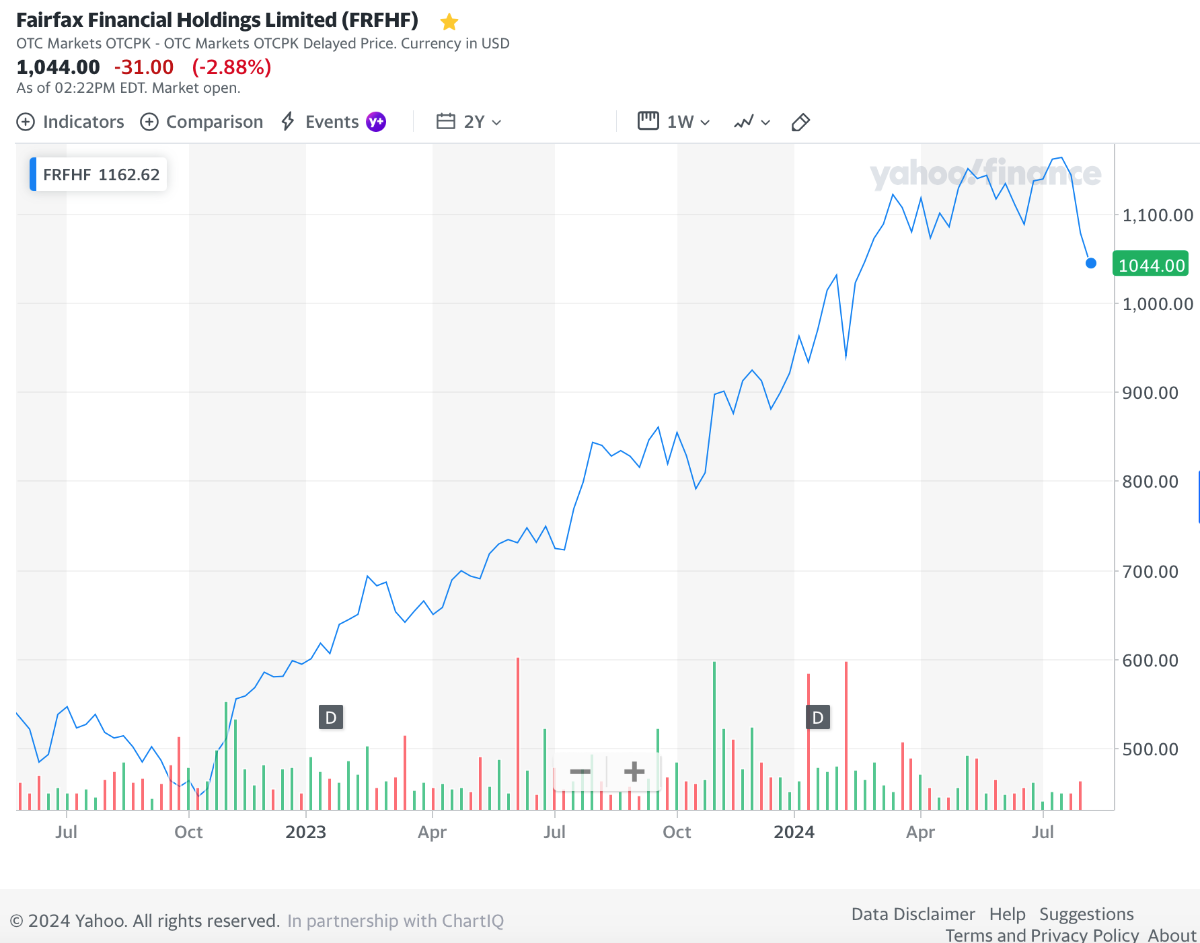

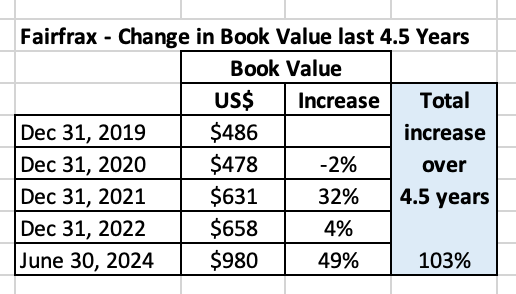

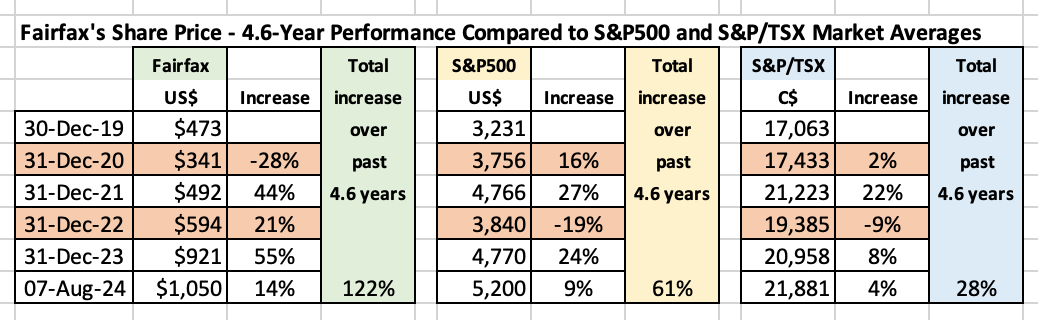

Financial Market Volatility - is it good or bad for Fairfax? (And no, this is not a trick question.) “Everyone has a plan until they get punched in the mouth.” Mike Tyson After a long absence, volatility in financial markets is picking up. The next bear market in stocks is coming - we just don’t know when or how nasty it will be. A big chunk of Fairfax’s investment portfolio is in equities (25% to 30%). Therefore, extreme volatility has to be bad for Fairfax… right? Well, maybe not. In this post we will dig into the volatility thing to see what we can learn. We will look at volatility in two very different ways: 1.) Fairfax’s ability to profit from volatility. 2.) The impact of volatility on Fairfax’s short term reported results. Given the importance of the topic, we are going to break our analysis into two posts. Part 2 should be published in the next couple of days (I have some family in town so it might be delayed). ————— Volatility - Part 1: Fairfax’s ability to profit from volatility Introduction Is extreme volatility in financial markets good or bad for a Fairfax investor? Active management matters again How has Fairfax performed aver the past 4.5 years? Volatility - Part 2: The impact of volatility on Fairfax’s short term reported results. 'New Fairfax' To come in the next couple of days. ————— Introduction Wall Street defines risk in terms of volatility - the higher the volatility, the greater the risk. Warren Buffett thinks how Wall Street looks at risk/volatility is nuts. Buffett defines risk very differently - he defines it in terms of permanent loss of capital. Importantly, Buffett’s definition is also largely focussed on the long term. Buffett looks at volatility through the lens of Mr. Market - he views volatility over the short term as opportunity. Volatility is something to be exploited by an investor. And extreme volatility? Well, that is usually where you find the really fat pitches (that ‘back up the truck’ thing). Fairfax and volatility If history can be used as a guide, long term shareholders of Fairfax should be praying for a shitstorm in the coming months (in the markets in general) and for the company’s stock to get taken out behind the woodshed. Volatility in Fairfax's stock price (in both directions) has historically been a gift for long term investors. Now don’t get wrong… I loved the relentless move higher in the share price that we have seen since October 2022, when the stock was trading at $450. We saw an increase of +150% in 22 months. Fairfax’s stock was like a goat climbing straight up a steep mountain. But investing isn’t a Disney movie. Nothing goes straight up forever. Given its dramatic move higher, Fairfax will likely trade more like a regular stock moving forward. And the average stock fluctuates about 50% (lows to highs) over the course of a year. As of today (August 7, 2024), Fairfax’s stock is down about 11% over the past week or so. ‘Investors’ are trying to read the animal entrails to determine what is going on (what is causing the short term volatility). Me? I have no idea what is causing the sell off. But I love it. Why? That is what we will explore in this post. ————— Is extreme volatility in financial markets good or bad for a Fairfax investor? Now this is a great question. With lots of interesting layers. How you answer this question really depends on your time frame: Are you a short term or a long term investor in Fairfax? For example, if Fairfax’s stock dropped 20% - well, that would likely be a terrible result for a short term trader(note I did not say investor). Who wants to own a stock as a short term investment that drops 20%? No one. But is a 20% drop in Fairfax’s share price bad for a long term investor? No, I don’t think it is. But more than that, given the current set-up, I think it would likely end up being a very good thing for a long term investor. Why? Because Fairfax would be able to take out a meaningful number of shares at a very low price. Today Fairfax is generating a record amount of free cash flow. And as the hard market in P/C insurance slows, the P/C insurance subsidiaries are generating excess cash - and they are now sending it to Fairfax (as growth in P/C insurance is slowing). Fairfax is all cashed up. And this look like the case for the next 3 years or so (3 years is as far out as our crystal ball can see). What will Fairfax be doing with all that cash? On the Q2, 2024 conference call Fairfax provided an update on their capital allocation priorities: Priority #1 - maintain a strong financial position. Priority #2 - buying back a meaningful amount of stock (that Henry Singleton thing we wrote about last week). Priority #2 used to be funding the growth of the P/C insurance companies (this has been the case since late 2019). With the hard market slowing this is no longer the case. This is a big change in priorities. So far in 2024, Fairfax has reduced effective shares outstanding by 820,000 (3.5%) at an average price of US$1,098/share. Fairfax are value investors. As a result, they only buys back shares when they can be purchased at a discount to their intrinsic value. So Fairfax thinks its shares trading at $1,100 are cheap. Fairfax’s stock closed today at $1,050. It is down 11% over the past week (after hitting an all-time high of $1,178 on July 31, 2024). If it continues to fall from here, Fairfax will get a wonderful opportunity to take out a meaningful number of shares at a very low price. Buying back a meaningful quantity of shares on the cheap is a great ‘use of capital’ for long term shareholders. When it comes to share buybacks, the lower Fairfax’s share price goes the better. The timing of buybacks Does this mean Fairfax is going to buy back a massive amount of shares in Q3, 2024? No, of course not. They might. And they might not. It is impossible to predict how many share Fairfax will repurchase in any given quarter. Fairfax has lots of good uses for its free cash flow. But i think it is a good bet that if Fairfax’s shares remain at a very low valuation that Fairfax will buy back a meaningful quantity over the next 12 to 24 months. Of course, this assumes the long term fundamentals of Fairfax’s business are not deteriorating. And I don’t think they are. But there is much more to this story - it gets even better. —————— Active management matters again When it comes to capital allocation, Fairfax is an ‘active manager.’ And they use all the tools in the capital allocation toolkit (sources and uses of cash). As we learned from Warren Buffett, fat pitches usually come at times of extreme volatility. Over the past 4 years we have had 2 bear markets in stocks (2020 and 2022) and an epic bear market in fixed income (2022/2023). How did Fairfax perform over the past 4.5 years - when Mr. Market was panicking? Fairfax made many of their best investments in ‘shit storm’ type of environments: In 2020, initiated the TRS position (getting exposure to 1.96 million Fairfax shares) at $373/share). In 2021, took the average duration of their fixed income portfolio to 1.2 years. In 2021, bought back 2 million Fairfax shares at $500/share. In 2022, took Recipe private at a very attractive price. In 2023, invested $4 billion (with Kennedy Wilson) in PacWest real estate loans (with a total return of about 10%). In 2023, extended the average duration of their fixed income portfolio to about 3 years. Fairfax also made many smaller moves from 2020 to 2022, taking advantage of very low prices, to increase their ownership in well run companies they already owned (including Fairfax India, Thomas Cook India and John Keells). The bottom line, over the past 4.5 years Fairfax has been able to exploit periods of extreme volatility, making many outstanding investments that have generated wonderful returns for Fairfax and its shareholders over time. Importantly, Fairfax was able to do this when they were cash poor. That is no longer the case. Fairfax is currently generating a record amount of free cash flow - and this looks set to continue for the next 3 years (as far out as my crystal ball looks). Now when the stock market sells off 20% it generally doesn’t feel great. And we will not know in advance with certainty what moves Fairfax will be making. But if history is any guide, extreme volatility in financial markets will likely provide Fairfax with many wonderful opportunities that they can aggressively exploit. As I said earlier, long term Fairfax shareholders should welcome extreme volatility and the opportunities it presents to Fairfax - this is often when Fairfax makes its best investments. ————— How has Fairfax performed aver the past 4.5 years? We can evaluate management by looking at a simple, yet highly instructive, metric: increase in book value per share. Change in book value per share (BVPS) As a reminder, we had bear markets in stocks in 2020 and 2022 and a historic bear market in bonds is 2022/23. This should have been terrible for Fairfax shareholders... right? This is Fairfax after all... Despite the extreme volatility in financial markets over the past 4.5 years, Fairfax was able to increase BVPS by 103%. Impressively, the volatility was heavily skewed to the upside (the biggest annual decrease in BVPS was only 2%, in 2020). Given the volatility in financial markets over the past 4.5 years, are these the annual or total results you would have expected for Fairfax? No, of course not. Fairfax’s performance over the past 4.5 years was much, much better than expected. I think there is an important lesson to be learned from this - extreme volatility is not the devil that many Fairfax watchers think it is. Change in share price In 2020, Fairfax’s share price was down 28%. This was what I like to call ‘old Fairfax.’ Fairfax had just started executing its turnaround but it was not yet recognized by Mr. Market. Sentiment in Fairfax hit rock bottom in 2020. But look at what happened to Fairfax in 2021, 2022, 2023 and so far in 2024. Fairfax’s absolute and relative performance has been outstanding (putting it lightly). The management team at Fairfax has been executing exceptionally well - among other things, they have been feasting on extreme volatility in financial markets. And this strong performance is being rewarded by Mr. Market. ----------- Part 2: The impact of volatility on Fairfax’s short term reported results To come in the next couple of days...

-

“Good artists copy; great artists steal.” Picasso/Steve Jobs

-

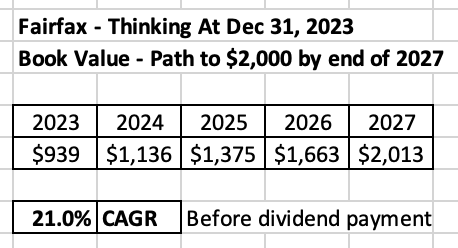

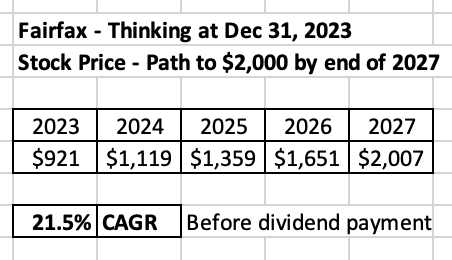

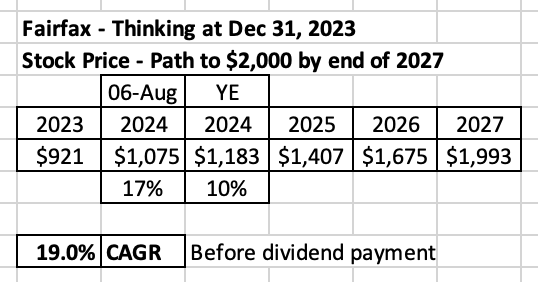

@Haryana, here is how I was thinking back in December. The question asked was pretty straight forward: "Will Fairfax book value or share price touch US $ 2000 before 2027 end." I voted "no." The book value part was the easiest. Fairfax would need to compound book value by about 22.5% (21% plus 1.5% to account for the dividend). That was higher than my base case back then. What about the stock price? This was a little harder. But not much. The share price would need to compound by about 23% per year (21.5% plus 1.5% to account for the dividend). That was higher than my base case back then. I do expect multiple expansion to happen (that is why it was harder). Where do we sit today regarding the share price? If we assume a 10% return for the last 5 months of 2024, the share price will still need to compound at about 20.5% from 2025-2027 (19.0% plus 1.5% to account for the dividend). That is still higher than my base case. What is my base case? From where we are today, I think Fairfax can deliver a CAGR of 15% over the next 4 years (including the dividend). If the stars align (a couple of large asset sales, continued multiple expansion, no big negative surprises etc) we could see a double in the share price over the next 4 years (including all dividend payments). BUT I DON'T FOCUS ON LOOKING OUT THAT FAR. My focus is on the next year or two - because that is what I can see with the most clarity. Looking a couple of years out, it really comes down to management - and i really like what the management team at Fairfax has been doing since 2018. So i am pretty optimistic about Fairfax’s prospects looking out 4 or 5 years into the future.

-

@Thrifty3000 This post is not directed at you When it comes to Fairfax, I find investors: 1.) get anchored to what happened in the past (especially the recent past). 2.) get anchored with apparent self-truths that aren’t actually truths. They then use those two faulty frameworks as important inputs into their valuation. And then they only apply it to Fairfax (not to peers). ————— 1.) Portfolio yield - Fairfax is earning a little over 7% today. I keep hearing how that is crazy high and it has to come back down - by a lot. What is the logic? Because it is too high. 2.) Combined Ratio - Fairfax is delivering a combined ratio of 94 to 95%. This has to revert to something closer to 100. What is the logic? Because insurance markets are competitive - because it is too low. The truth is… it is really all about probability distributions. - We can have a pretty good idea what might happen over the next 12 months. - We can have a good idea what might happen over the next 24 months. - We can have an idea what might happen over the next 36 months. Looking out 4 years or more for ANY P/C insurance company? There are too many variables to really have strong view.

-

@TB When you say ‘Threats to the thesis playing out’ what is the time-frame you are using for the following: b) Weaker stonk markets in India and the US. ————— Anything can happen over a one or even two way period. That is only a ‘threat’ if you are a short term trader. ————— Fairfax has made their best investments when the shit was hitting the fan and Mr Market was losing their mind. Long term Fairfax shareholders should be praying for volatility. And, unlike the past, Fairfax now has record free cash flow raining down (and the insurance subs are generating excess capital) - this should enhance their ability to exploit volatility.

-

Great summary. Buffett says the most important thing in valuing a company is certainty. As you point out, we have that with Fairfax's free cash flow over the next 3 to 4 years. And it is a BIG and growing number. What do investors think? When it comes to Fairfax, they don't care about the next 3 or 4 years. Or the earnings. Or that fact Fairfax is allocating capital exceptionally well. Instead, they say... 'This is Fairfax!' And because it is Fairfax, they create new mental roadblocks - things that could go wrong. The new 'worry?' 'What will earnings be in 2027 or 2028?' 'With interest rates coming down over the past week, earnings at Fairfax are going to get killed in 3 or 4 years...' Really? I love it. It just means Mr Market is going to get Fairfax completely wrong - again. This will allow Fairfax to continue to buy back a significant number of shares at a low valuation. And that is a beautiful thing for long term shareholders. Long term shareholders already own 20% more of Fairfax (based on the stock bought back over the past 6.5 years). It looks to me like Fairfax is putting its foot down on the buyback accelerator - buybacks might continue at a very high level for the next couple of years. My guess is Mr Market can't wait to unload their Fairfax shares (that 'it's never a bad idea to take profits' thing). And this will allow Fairfax to continue to take out a meaningful quantity of shares at a low valuation. It really is a crazy good set up.

-

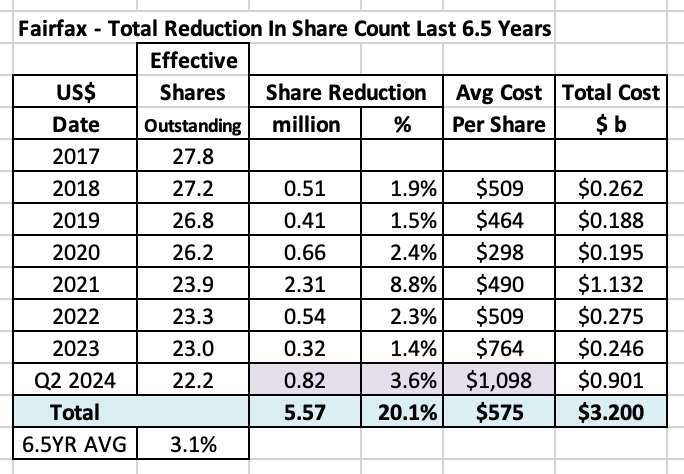

Perhaps the most important thing we learned from Fairfax's Q2 results (and subsequent conference call) concerned stock buybacks. Summary: Over the past 6.5 years, the size and profitability of Fairfax has increased dramatically. Fairfax has also been aggressively buying back a significant number of shares at a very low valuation. As a result, Fairfax shareholders now own 20% more of Fairfax’s much larger and much more profitable P/C insurance / investment operation. And it appears the company is putting its foot on the stock buyback accelerator... The big picture Three factors drive stock returns over the long term: Earnings Multiple Shares outstanding The last factor is often ignored by investors. Capital allocation Capital allocation is the most important function of a management team and stock buybacks are one of many options that are available. Share buybacks can be very beneficial for shareholders if they are done in a responsible manner (purchased at attractive prices) and sustained over many years. It is counterintuitive, but for long term shareholders a low share price can be a big benefit - if the company is buying back shares and in a significant quantity. Especially if it persists for years. How does Fairfax approach buybacks? Prem laid out Fairfax’s strategy regarding share buybacks in the 2018 annual report: “I mentioned to you last year that we are focused on buying back our shares over the next ten years as and when we get the opportunity to do so at attractive prices. Henry Singleton from Teledyne was our hero as he reduced shares outstanding from approximately 88 million to 12 million over about 15 years.” Prem Watsa – Fairfax 2018AR Fairfax approaches share buybacks from the framework of a value investor: buy back shares when they are cheap and back up the truck when they are really cheap. What has Fairfax been doing in recent years? Fairfax’s year-end ‘effective shares outstanding’ peaked in 2017 at 27.75 million. Fairfax issued a total of 7.2 million shares in 2015, 2016 and 2017 to help fund its aggressive international expansion in insurance. The new shares were issued at an average price of about $462/share. At June 30, 2024, the ‘effective shares outstanding’ at Fairfax had fallen to 22.2 million shares. Over the last 6.5 years (2018-Q2 2024), Fairfax has reduced its share count by approximately 5.57 million shares or 20.1%. The average price paid to buy back shares was about $575/share. That is a significant reduction in shares outstanding. Did Fairfax get good value with its buybacks? The average price paid for the shares repurchased by Fairfax over the past 6.5 years is slightly higher than the price that shares were issued at from 2015-2017. Fairfax’s book value at June 30, 2024 was $980/share. Fairfax’s intrinsic value is well above its book value. Fairfax has been able to buy back a significant number of shares at a very attractive average price – at a significant discount to book value and intrinsic value. Is Fairfax done with buybacks? In 1H 2024, Fairfax reduced effective share outstanding by 820,000 shares or 3.6%. That is significantly more than the average for the past 6.5 years of 3.1% (that is the annual increase). So far in 2024, Fairfax is buying back stock at 2 times the average pace from the past 6.5 years. Why is the pace of buybacks picking up? Likely for three key reasons: Robust cash generation: Fairfax is generating an enormous amount of free cash flow. The hard market in P/C insurance is slowing: The P/C insurance companies no longer need capital to grow. In fact, the opposite is happening – the P/C insurance businesses are generating excess capital, which is being sent to Fairfax. Cheap stock: Fairfax’s stock trades at a big discount to its intrinsic value (and peers). For the stock repurchased in 1H 2024, Fairfax has paid an average price of $1,098/share. This price is a slight premium to current book value ($980/share). Importantly, book value does not include the following: “At June 30, 2024 the excess of fair value over carrying value of investments in non-insurance associates and consolidated non-insurance subsidiaries was $1,514.5 million.” This is about $68/share pre-tax. “The company's current estimated pre-tax gain on sale of its holdings of approximately 13 million common shares of Stelco is approximately Cdn$531 million (US$390 million)…” Bottom line, in 2024 Fairfax has been buying back shares at around 1x 2024 year-end ‘adjusted’ book value (if we include the two items above). That is great value. On Fairfax’s Q2 conference call, Peter Clarke suggested that Fairfax would continue to be aggressive with stock buybacks. Over the past 6.5 years, the size and profitability of Fairfax has increased dramatically. Fairfax has also been aggressively buying back a significant number of shares at a very low valuation. As a result, Fairfax shareholders now own 20% more of Fairfax’s much larger and much more profitable P/C insurance/investment operation. This is just another example of the outstanding job the management team at Fairfax has done when it comes to capital allocation.

-

This is Fairfax. We have been spoiled the past 18 months - that price action (pretty much straight up) is not normal. My guess is perhaps the stock is simply trading more along normal / volatile lines.

-

What is your top 3 business/finance/investing books you've read?

Viking replied to schin's topic in General Discussion

I think establishing an investing framework that; you are good at works is the most important thing when it comes to investing. In this regard, here are my 3 favourite books; 1.) Graham - The Intelligent Investor: Mr. Market and margin of safety 2.) Lynch - One Up on Wall Street: full of good stuff 3.) Malkiel - Random Walk Down Wall Street: for those who want the big picture (I don't agree with Malkiels conclusions) Steal the stuff that works for you. And then keep reading and learning... the rest of your life -

I hope the stock is selling off today because people are concerned about Fairfax's earnings in 2026 or 2027. Do people seriously think we are returning to a zero interest rate world? We might be. But I doubt it. Perhaps we get a growth slow down over the next year. And that causes global central banks to drop interest rates over the next year. But low rates will stoke economic growth. And I think secular forces are still inflationary: - very high government (deficit) spending - deglobalization - energy transition - geopolitical uncertainty / wars So my guess is we get a big head fake over the next year. Where people think inflation is licked. Rates go low and animal spirits kick in with a vengeance again. Only to re-kindle inflation. It might take 18 to 24 months to play out. What does this mean for Fairfax? We know they are locked and loaded for the next 2 or 3 years. After that? Who the hell knows? Good luck trying to invest today based on where you think interest rates might be in 3 years and what Fairfax will have done in the interim period. As investors, we typically want predictability and 'stability.' What I do know is volatility is usually very good for Fairfax. It provides them with great opportunity - and their execution in recent years has been stellar. It is very counter intuitive. Fairfax has a very unorthodox style / way of doing things. Mr. Market will find something they don't like (doesn't have to look hard with Fairfax.) It results in lots of volatility in the share price. If the share price stays low Fairfax will have the opportunity to take out a meaningful number of shares at a low valuation. And Fairfax has the cash. That is a wonderful set-up for long term shareholders. In the past, when Fairfax's shares sold off the company did not have the free cash flow to take out a meaningful number of shares. That is no longer the case. They are swimming in cash and they don't have a good alternative use for it.

-

Looks like volatility in Fairfax's share price is back. Love it. Fairfax's stock is currently trading at US$1,070. Book value at June 30 was $980/share. At June 30, Fairfax is sitting on non-insurance companies gains= $68/share pre tax They also will book a nice gain (incremental $300 million pre-tax?) when the Stelco sale is approved in Q4. Let's round the above two items to $60 after-tax. That puts adjusted book value at about $1,040. Fairfax's stock is trading today at a hair over 'adjusted' book value. The company is firing on all cylinders. They just released a great earnings report. They are positioned to do very well in the coming years. And they just told us that with the hard market slowing the insurance subs are generating excess capital that is being returned to Fairfax. They also just told us they think their shares are cheap and they will continue to buy them back. That is called shooting fish in a barrel. PS: Long term Fairfax shareholders are the big winners. From a capital allocation perspective, Fairfax has prioritized stock buybacks. The lower the share price the better.

-

I think you are just messing around…

-

What a great quarter of results. Fairfax delivered across all key metrics: Underwriting. Interest and dividend income. Share of profit of associates. Excess of FV over CV is $1.5 billion, up from $1 billion at Dec 31. This is $500 million (pre-tax) in value creation that is NOT captured in earnings (and $1.5 billion pre-tax that is not captured in book value). Estimated pre-tax gain of $390 million from Stelco sale should be coming in Q4. Effective shares outstanding reduced by more than 800,000 in 6 months? WTF? Love it. I need to better understand the impact of buying back stock at a slight premium to book value. Currency continues to be a headwind; about $200 million hit to book value in 1H 2024. That will likely reverse at some point (Trump election win?). Tax rate in the quarter looks higher than trend… ??? Let’s see what we learn on the conference call in the morning.

-

I was a very happy shareholder the day the deal was announced - i had my biggest one day gain in my portfolio to that point. A very big chunk of my portfolio was in ORH when Fairfax took ORH private. And one of the reasons i was so heavy at the time was there was a good chance that Fairfax was going to take it out. I think i was banging the table pretty hard on the opportunity. Not every shareholder is buy and hold But that was back in the day when i was a trader. Today i am an investor (wink, wink…)

-

@cwericb This is a really interesting topic. Fairfax has a value investing framework with everything that it does - with both insurance and investments. This means you buy low and sell high. It also means you opportunistically take advantage of Mr Markets frequent mood changes. As a Fairfax shareholder i want them to do this. When Fairfax took Recipe private they paid a 50% premium to where the stock was trading at the time. Now i think Fairfax got a good price. But at the time, i thought Recipe shareholders got a very good price. Poseidon is another interesting example. My guess is lots of Atlas shareholders were not happy with the takeout price. But did they get screwed? It might look like it in a few years when Fairfax starts to monetize its position. I think taking Atlas private has been a BRILLIANT move for Fairfax shareholders. I think it is much easier/better to operating Atlas as a private company - out of the public market spotlight. Especially given everything that has happened over the past 2 years (freight rates plummeting, interest rates spiking, freight rates spiking). Importantly it has removed an enormous amount of volatility from Fairfax’s reported results - that is a topic that deserves its own post. There are also the examples of when Thomas Cook India (Covid) and John Keells (currency crisis) needed cash infusions. Fairfax stepped up but demanded its pound of flesh (restructuring and increased ownership on very favourable terms). Early in 2022, Fairfax and Fairfax India took out a large player at $12/share - a criminally low price. Sorry for my rambling post. My point is over the past 5 years Fairfax has spent an enormous amount of money increasing its ownership in companies it already owns (including its own stock). Sometimes it flexes its position up and then back down (Thomas Cook India, Quess). Their moves have built enormous value for Fairfax shareholders. I hope they keep doing what they have been doing.