Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

+1 The interesting thing is older people (boomers) in Canada do not want anything to change... they have it very good today. The economic malaise (to put it politely) is not affecting them - so I get why they will vote Liberal (giving them another 4 years).

-

@Ulti , I am not as optimistic as you. GDP per capita in Canada is flat over the past 10 years? Why? I see 2 reasons: Housing bubble - not a productive use of resources Liberal government taking the government hard left - the federal Liberal government has become the NDP (in terms of its policies). Canada's economy is broken (capitalism is the devil and government is the solution). Its fiscal situation is terrible. The Liberals are likely going to win the election. Carney is Trudeau light. Nothing substantial is going to change with Carney at the helm (in terms of direction/policy). He is running a great campaign... He reversed some obviously unpopular things (like the carbon tax on consumers) but not because he thinks it is bad policy but because it is not popular. He says we need to build pipelines - but he will not repeal bill C69, which effectively makes it impossible to build a pipeline. Carney's solutions ALL have a similar logic: 'government is the answer.' Remember, this is the same government who created many of the problems (remember - GDP per capita in Canada has been flat for the past 10 years). I think we are going to get financial repression in Canada in the coming years - highish inflation (3%) and very low interest rates. Terrible for savers (like my 93 year old mother-in-law) and great for highly leveraged borrowers (like the federal government). In terms of what to invest in, everyone needs to figure this out for themself. There is no right thing to do... it depends. I started raising cash two months ago. I have deployed a little recently (in XEQT, a global ETF) but I am in no hurry. I continue to really like Fairfax (it looks like a great defensive holding in the current environment, which sounds a little bizarre given this is Fairfax). Best of luck

-

One of the big reasons communist governments fail (eventually) is because central planning usually does not work for advanced economies (we'll see in the next decade is China is able to pull it off). (Yes, central planning can work great in the early stages of economic development). Why doesn't it work? Resources are not allocated optimally/efficiently. And corruption becomes endemic. What we are seeing play out in the US in recent weeks is mind blowing. Yes, that sounds like hyperbole but I don't think it is in this case. Who is allocating resources? 'Donald Zedong.' Think about that long and hard. Corruption is ramping massively in size and scale - in plain sight of everyone - and is becoming normalized/institutionalized. Think about that long and hard. With these two developments is the US better off today than it was 2 months ago? The US is devolving into a banana republic (politically and economically). And there is nothing people can do about it. Because most people don't want to do anything about it. And the people who do are largely powerless. (The House/Senate/Courts are largely powerless/not equipped to deal with these developments.) Two months ago, the narrative was 'American exceptionalism.' I was drinking that Kool-Aid. Today? I feel like I am watching a slow moving train wreck - that will be playing out in the coming years (it is likely just getting started). That is simply amazing. PS: I have no doubt the US will get through this period. But it will likely be a poorer country with less influence on the global stage - the opposite of 'American exceptionalism.' (And all countries will likely be worse off.)

-

I just finished listening to it... good overview of the current situation. Great title: 'Nobody knows. (Yet again.)'

-

“Everyone has a plan until they get punched in the face.” Mike Tyson (philosopher) President Trump has just punched financial markets in the face. In the process he has created unprecedented uncertainty - and that is now driving historic volatility. We have 3.6 years to go. What is an investor to do? Look for two things: 1.) Play defence: Find certainty. What does this mean? Find stocks that are: Not impacted by tariffs (like P/C insurance) Not impacted by a slowing economy (like P/C insurance). Certainty has always been a super important part of the valuation process (just ask some guy named Warren Buffett). Stocks with a high degree of certainty get a premium valuation. In the current environment, these stocks will be even more highly valued - as a result, due to their scarcity, valuations/multiples for these stocks will likely expand in the coming years. 2.) Play offence: Find stocks that will benefit from high/extreme volatility. The current extremely volatility environment is an active managers wet dream. A value investors Super Bowl. It is almost the exact opposite set-up to the 'zero interest rate' regime that we had for +10 years. Except active management/value investing is dead. Who does that anymore? Are there any stocks that check both boxes? Very few stocks have the ability to play both ends of the court (defence and offence) in Trump’s new reality game show. The few that can will have the opportunity to deliver spectacular outperformance over the market averages in the coming years. Got any names? Yes. Fairfax Financial. P/C Insurance stock. Not impacted by tariffs. Only mildly impacted by a slowing economy. As a result, earnings are largely locked and loaded for the next couple of years (the certainty part). But here is the kicker… When it comes to capital allocation, the execution from the senior management team at Fairfax has been best-in-class over the past 5 years (they are active managers/value investors). And the stock is cheap. So you get certainty on sale. And if you place your order today you will also get a call option on volatility for free.

-

I have learned over the years to trust my 'spidey senses' when they start tingling. They started tingling about two months ago as we began to understand the enormity of what Trump has planned. My solution was to simply increase my allocation to cash. If I am wrong, I miss a little upside. If I am right I get to buy low (maybe crazy low). Not a complicated strategy. This is standard operating procedure for me for +20 years and it has served me well. In the current environment it is critical to have a strategy (investment framework) that fits how you are wired and your current life situation. I have enough (that 'life situation' thing). The key risk to my portfolio is I do something stupid that blows it up. That risk has nothing to do with Trump - it is all on me. My point is investors have to be rational and take responsibility for their actions and be prepared to live with the consequences of their decisions. Eyes wide open. You have done a great job of reminding board members of this basic fact/reality. There is a great deal of uncertainty in the current environment. This likely means we will see a great deal of volatility for at least the next 3.5 years. This environment is an active managers wet dream. A value investors Super Bowl. It is almost the exact opposite of the 'zero interest rate' regime that we had for +10 years. I am trying to remain inquisitive and open minded to where we go from here. Best of luck to other board members.

-

+1 , I agree. With the announcements last week (reciprocal) and the one Saturday (electronics), it does not appear to me that Trump is actually changing anything. In both cases he is simply delaying the implementation. IMHO, the risks have not changed. As you said in an earlier post, rallies are a wonderful opportunity to tweak portfolios.

-

Not sure if this has been posted. Here is a short take on tariffs from the Economist. i liked the comment about what tariffs do to a domestic economy - it gets fat and lazy. Yes, the (‘protected’) US car industry back in the 1970’s was a train wreck. I think of that time/industry every time I hear the slogan ‘Make America great again.’

-

@73 Reds , good question. I am going to defer to @SafetyinNumbers. He is much more dialled into this topic than I am. One thought: what Fairfax does will likely depend on the size of the opportunity. When crazy good opportunities come along, Fairfax can get VERY creative (in terms of how they source capital).

-

We will see where financial markets go from here. Bottom line, it is probably a good time to review/start to think a little more about Fairfax’s fixed income portfolio. My schedule is going to be busy for the next 10 days so a deep dive will have to wait until after then. Here are some quick thoughts: What will be the impact of the big drop in treasury yields? Fairfax will see two opposing impacts: Large investment gains (driven by the increase in value of bonds). Offsetting impact of IFRS 17. What will be the size of the investment gains? What will be the size of the offsetting impact of IFRS 17? More on this in a future post. (Short answer: as of today, YTD perhaps a net benefit of $250 million?) Do we get a recession in the US? Probably not. But the risk is increasing. This means credit risk is becoming more important. How does this impact Fairfax? Fairfax’s bond portfolio is heavily skewed to government bonds - it is very conservatively positioned. Especially when compared to other P/C insurance companies (who are heavily weighted to corporate bonds). Do we see credit spreads blow out? If this happens, Fairfax will have the opportunity to Sell their government bonds - and realize a big investment gain. Buy corporate bonds at mouth watering yields. Bottom line, the fixed income portfolio is getting a little more interesting. —————- A review of some of the risks of investing in bonds Interest rate risk - rising interest rates cause bond prices to fall. Duration matters a lot with this risk. Spiking interest rates impact long duration bond portfolios much more than short duration portfolios. Credit risk - the risk the issuer may default on one or more payments. Market dislocations / recessions matter a lot with this risk - events that cause credit spreads to blow out. Inflation risk (purchasing power risk) - the risk that inflation is higher than the total return received on the bond. Unexpected inflation is what matters with this risk. Especially if the inflation is high and persists for years. Reinvestment risk - the risk that at maturity, the proceeds will be reinvested at a lower rate than the bond was earning previously.

-

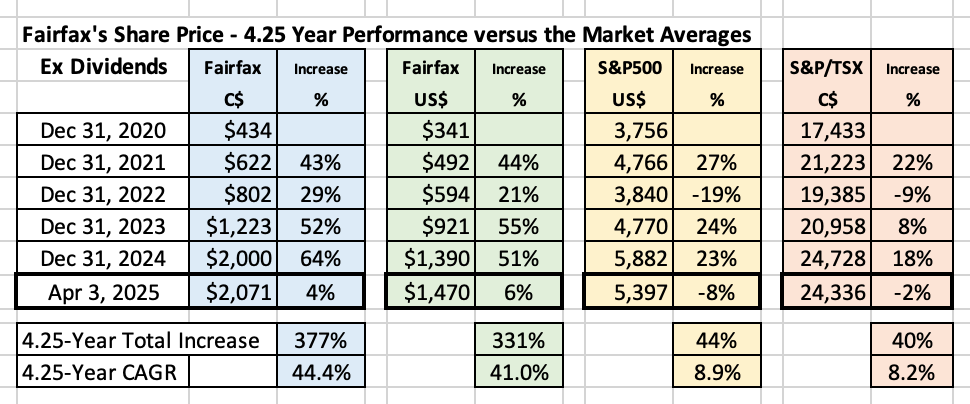

@dartmonkey , yes, as i put on the chart, the numbers are ex dividends. When I build my charts I am usually in a hurry… so I often use information that is super easy to obtain. There often is a ‘better’ way to look at things. Board members need to keep this in mind when they read my stuff.

-

@mattee2264 , you are assuming Trump is a rational actor. With a plan. Who can be trusted to honour a deal. What if this is not the case?

-

Guess what all those beautiful tariffs announced 2 days ago will be doing to prices for many of the goods the US imports? Not just the finished products... but also the inputs and raw materials? Now I am not a rocket scientist but I can do basic math. Now the really interesting thing with tariffs is what the protected domestic producers tend to do... when a tariff is introduced (raising prices on imports) they also raise prices (because they can). And once they get that benefit guess what happens to their political donations? It increases - they then actively lobby to ensure the beautiful tariffs stay in place. Now of course, there are lots of things going on in the economy at the same time. So there will be puts and takes.

-

@73 Reds , I agree: "Folks here on this board should be getting ready for an opportunity that doesn't often come along." Crisis = opportunity.

-

Well, today the US science experiment got another couple of data points. China increased tariffs on US goods by 34%. I know... what a shocker. And the S&P500 sold off another 6%. The sell-off in the S&P500 over the past 2 days has been epic. The tariff sell off has now wiped out a full year of gains in US equities. Good thing most Americans don't have a pension (like a 401k) that is invested in equities - if they did that would really suck. But hey, that is what success tastes like. Sorry if that isn't what you expected. And you better get used to it - because much more is probably coming. Bottom line, that is a massive amount of value destruction. It really is impressive. But hey, this is what Trump promised - so you'll eat it and you'll like it. The really interesting thing is we are only 2 days into this science experiment - the practical phase. The US economy hasn't even been impacted - yet. As Trump keeps promising, the best is yet to come. It looks pretty clear that inflation is going higher and growth will be slowing - and supporters of the president can't wait. It really is a surreal thing to watch. This is playing out like a slow moving train wreck. And lots of Americans are loving/applauding/supporting it. One of the things we are learning is that other countries don't like getting kicked in the teeth... I know, I know... what a shocker (another one). What is the next data point? What does Europe do. If they take China's approach... well, that is called a full on trade war. Something we haven't seen in 100 years or so. Why so long? Because it was so bad the last time it happened countries were smart enough to avoid it (that hand over a flame thing). So it appears we need to put that hand over the flame again. Yes I know, history sucks. So my guess is the US administration will be looking for a win this weekend. Well, if they are smart they will be. (Why are you laughing?)

-

+1. (If my wording is unclear, which it often is... please look at the chart.)

-

“You make most of your money in a bear market, you just don’t realize it at the time.” Shelby Cullom Davis What is going on right now is a gift for investors, especially those who are younger.

-

@Castanza , great point. We have now had bear markets in the stock market averages in 2018, 2020 and 2022. And it looks like we might get another in 2025. The market averages were down 20% or more each time. Lots of individual stocks went down much more than 20% during each correction.

-

XEQT. This is a broad based ETF based in C$ (so appropriate for a Canadian investor). My cash is down to 35%. My view is stock picking is getting more difficult with Trump - he will now be picking the winners and losers (industries/stocks). So another variable has been added to the purchase decision. The beauty of an index fund is over time it will constantly rebalance - add more of the winners and subtract the losers. This particular ETF is also global (42% US, 25% Canada, 33% Europe/Asia), which I also like given the current set-up. XEQT is currently trading down 13% from its recent highs - that is a pretty steep drawdown for a broad based ETF. I wanted to start buying stocks earlier today… but I did not know what to add. I felt a little like a deer in the headlights. And then I got a blinding glimpse of the obvious… just buy a broad based index. Problem solved. Thank you John Boggle (although the ETF I bought is not a Vanguard product). https://www.blackrock.com/ca/investors/en/products/309480/ishares-core-equity-etf-portfolio

-

@cubsfan , did anyone know how Covid was going to play out in the first few weeks? No one had a clue. The reason stocks sold off 30% in weeks was because of the uncertainty. We are weeks into the current crisis (and yes, it is a crisis). We just entered the high uncertainty phase. No one has a clue how it plays out from here. Is it dangerous? Yes. How dangerous? We will only know once we get to the other side (and we are just getting started - this President has 3.75 more years to go). I love history. There are lots of examples of things starting small and then spiralling out of control. The tail risks of this fiasco getting out of control are increasing (not decreasing). That is not my base case. But every once in a while humanity does truly stupid things. This has that potential.

-

@73 Reds , I do appreciate your perspective. At the end of the day, I think it is unknowable how things play out from here (what we know today). You may be right. Or not. We will know more in the coming months. Bottom line, I have a lot of respect for Trump. He is motivated and he has surrounded himself with a loyal team. I think he is much more capable than you suggest (I don’t mean that in a good way). So I am trying not to underestimate what he might do (or how far he is prepared to go). Context is important; I only have financial assets (no real estate etc). As a result, I tend to be more cautious than most when uncertainty is high. Over 30 years of investing, I have learned to trust my ‘spidey senses’ when they start to tingle. As I learn more I will act accordingly (that ‘be rational’ thing).

-

A stock is supposed to be worth the discounted value of all the cash it will spin out in the future. Today it is impossible to know the amount of cash that most companies will be able to earn in the coming years. I don't think that is hyperbole. The level of uncertainty is very high. That means stocks are worth less - and maybe a lot less. Increasingly, we are learning there is no grand well thought out plan. One man is deciding how resources are going to be allocated in the largest economy in the world (and those of its largest trading partners). And this man is a nut-job (I don't think this is debatable). It looks to me like investors are 'whistling past the graveyard.'

-

Fairfax continues to be the gift that keeps on giving. Over the past 4.25 years, its stock has significantly outperformed the market averages every year, with more of the same YTD 2025. Its cumulative outperformance has been epic. Their CAGR (in C$) is now greater than the total return for both the S&P500 and the S&P/TSX. Nuts. To the entire team at $FFH.TO - thank you!

-

Well, the US science experiment is getting some new data. The S&P500 is down 4.66% and the Nasdaq is down 5.74%. These are historic one day moves. Needless to say, the stock market is not drinking the Kool-Aid. If fact, today it just threw up. Where do we go from here? Economic heaven, if you listen to Trump supporters. I remain unconvinced. But hey, I have been wrong once or twice in my life before. But I remain open minded and inquisitive (and with a cash weighting of 40%).

-

If you look at the last 2 years we have seen pretty dramatic volatility in fixed income markets (interest rates) in both directions (pretty wild swing in yields every 6 months across the curve). Was the extreme volatility terrible for Fairfax? No. Not even close. If anything it has had a net positive impact (looking at it from a big picture perspective).