Spekulatius

-

Posts

15,073 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

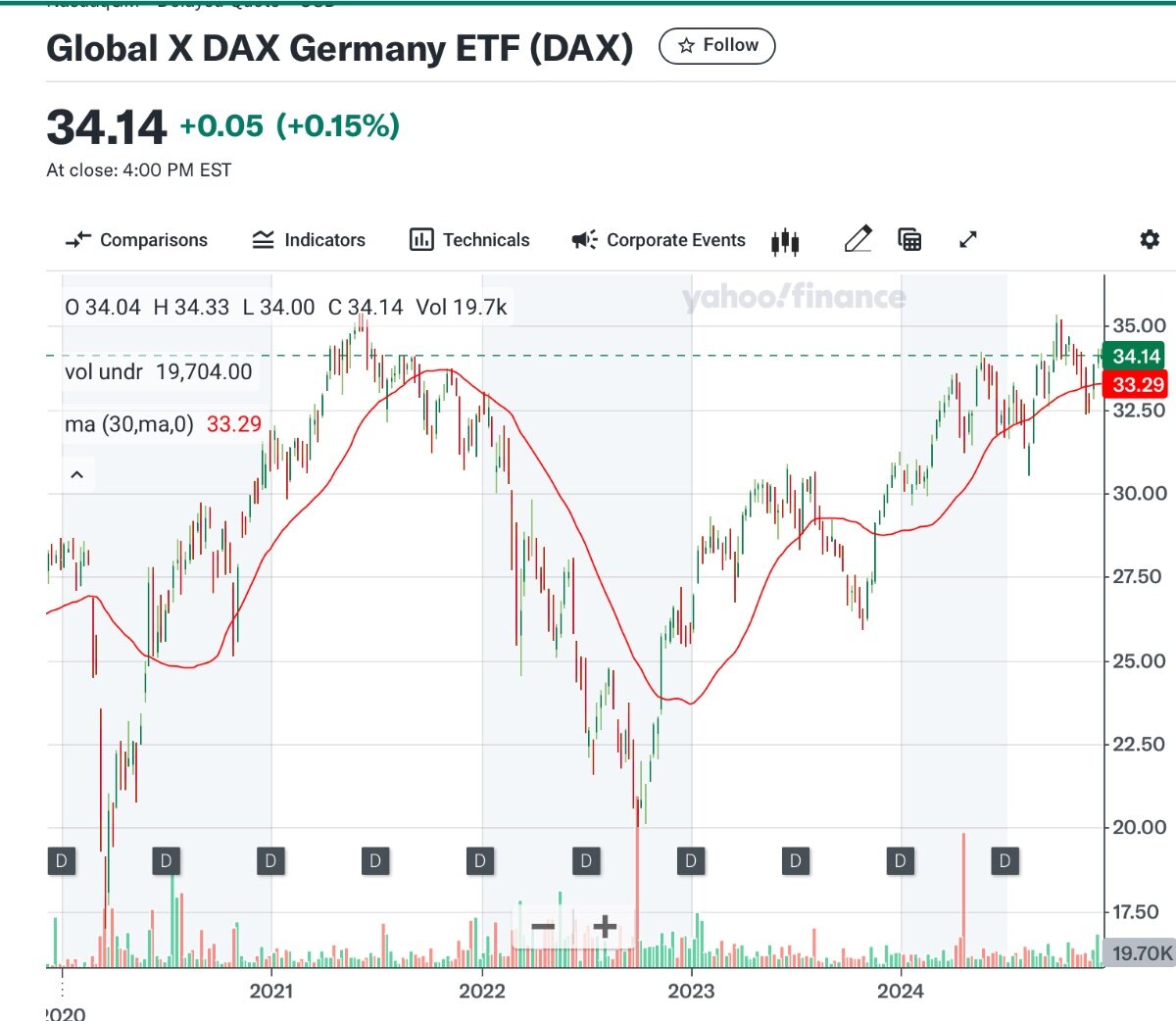

Up 70% since the lows from 2022. So money can be made here. What caused the surge was the appreciation of a few stocks like SAP and Siemens.

-

This is interesting and it’s actually more about replacing Swift than the USD per se. From a BRICS perspective, it makes sense to challenge SWIFT imo. SWIFT runs on USD so the threat to the USD is more indirect than direct. Also, looking at the trade flow, Brazil has a trade deficit with the US, South Africa has a smallish export surplus, Russia doesn’t give a damn so there is China, which gets tariffs anyways. So in my opinion, if the BRICS want to play, they could and just retaliate with similar tarrifs and would come even or ahead except China, which is getting the tariff treatment anyways. I think the question is if it’s worth the trouble. https://ustr.gov/countries-regions/americas/brazil#:~:text=U.S. goods and services trade,up 58.8 percent from 2021.

-

If you wait from solution from Lagardère or Draghi or Macron you are looking at the wrong people. I think its more likely they some countries come up with solutions or even more micro level companies will come up with their solutions long before those three will even know about it.

-

It matters because the much of the difference in stock market performance did not come from a differential in economic growth but from multiple expansion in the US and compression elsewhere. Even the economic growth in the US is partly fueled by increased fiscal deficits that are much larger than Europe’s.

-

Just one think tanks opinion after one year of Milei being in office: https://www.freiheit.org/one-year-javier-mileis-economic-policy I think they make a good point about Milei being too focused on inflation. Inflation is more a symptom than the disease and of course just like with fever, you need to stop it, but Argentina needs also to work on pro growth stuff like firing up exports (the overvalued of the Peso facilitated by him to limit inflation hampers this) and a few other things. Gutting the education system doesn’t sound like a great idea either since it basically stunts growth in human capital. The economy also needs to turn around next year if his agenda is in trouble, because the a erase person is suffering quite a bit here and needs to see some tangible benefits, imo.

-

I am pretty sure that allowing Walmart to sell Fentanyl by the pound would make the drug epidemic worse not better. There is a paper about the Fentanyl epidemic in Estonia where shutting down the supply was key to reducing the drug problem, but of course no panacea. What is interceding about Estonia is that the country is so small and also has pretty good records that one can actually see the impact of shutting down one major supply source which happened to be domestic. https://pubmed.ncbi.nlm.nih.gov/32416523/ But what do I know - cirumstances are always different and what may work in one country may not work in another. However data like this can be useful to determine a course of action.

-

We must be getting close:

-

Well everything else depreciates faster due to higher inflation. This is certainly true for EM currencies but not for the Japanese yen and the Euro. I think the Japanese yen is quite undervalued in terms of purchasing power, the Euro a bit less so. Then we have an influx in USD due to safe haven aspects, negating the trade deficits.

-

Might be the top tick for the USD which has been very strong lately. FWIW, the USD is used for about ~50% of the global trade and that has not changed much over the last few years.

-

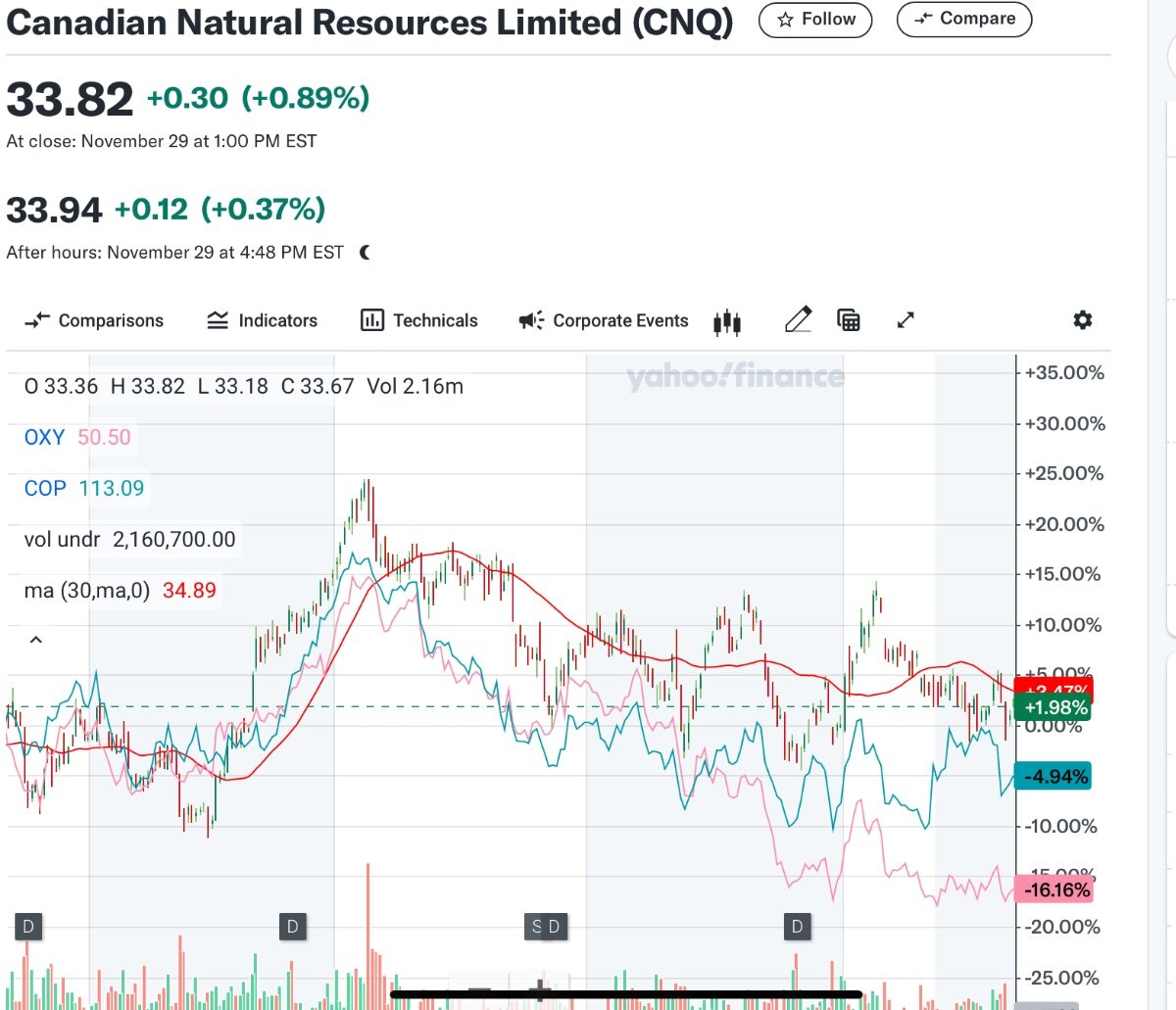

@sholland You are likely correct and Mr Market doesn’t believe it either. Canadian energy co have mostly outperformed US peers the last year despite issue like this and the carbon tax proposed by the Canadian government. So, I don’t think there is a trade here.

-

Construction Site Modular Building Companies

Spekulatius replied to Saluki's topic in General Discussion

It seems that these companies just rent out their balance sheet. I think there is more differentiation with equipment rentals. -

Does anyone here really understand PDD on a deep enough level and why it can keep growing? It matters more now because sequential growth has come a screeching halt, no capital returns, no CFO. It’s as black of a box that I have ever seen. Everyone can see that the numbers look good and the valuation is cheap, but that doesn’t mean one understands the business and if their competitive advantage has just become much smaller.

-

More in n t and shipbuilding. I do wonder if we should get Hyundai to set up a shipyard in the US and build the ships we need, similar to what we do with TSMC: In any case, working with the Japanese and the Koreans will be key.

-

Thx for clarifying . So all Canada would need tighten Visa policies? I don’t think the Bombardier killer drones that @SharperDingaan proposed will be feasible to seal Canadian borders.

-

Target the Russian oil exports via the shadow fleet. Russia war funding comes from selling crude. Russian Oil will always find a way to leak out so the game is to reduce the amount force them to sell it very very cheap. There is ample supply world wide which China’s demand going downhill, so I think a reduction in supply is manageable. Most countries who seen a rapidly decline currency are seeing hyperinflation due to the switch to war economy where consumption and investment are replaced by war related production. Most countries where the currency goes to hell end up losing - the Southern states (Greyback), Deutsches Reich (Reichmark started to steep decline after Stalingrad). Another possibility is allowing them strikes on Russian Nsrgy infrastructure like the LNG facility in the Baltics and Refineries in Wolgograd or anything within reach of Storm Shadows. The latter would also reduce their supply of fuel to the front lines. It’s not escalation either because Russia has been hitting Ukraine’s infrastructure since the war started.

-

You claim the data isn’t correct? I believe the dems have been tone def to illegal immigration for too long and the pivot was too late. Trump is great at propaganda. He will sell the same economy that we have right now as the greatest ever (which it is) and MAGA folks will believe it after thinking the same state of affairs was shitty a one.

-

Problem was already fixed anyways - illegal border crosses were way down in October: https://www.cbsnews.com/news/u-s-mexico-border-migrant-crossings-reach-new-biden-era-low/

-

I look forward to my AI model to become a self conscious and improved version of myself long after I am gone. Thats probably how we are going to live forever and explore space by shedding out biological confinement first. Let’s go!

-

Everyone talks about Teppers China bet , but he also took a position Lyft. Lyft is a nice turnaround story that he seems to have caught perfectly.

-

Making drugs easily available means a whole lot more exposure and everyone will try them. I mean Fentanyl is readily available albeit not legally and it is cheap and see where it got us.

-

China is a lot more outward looking than it used to be. The world is indeed a smaller place and everyone can trade with each other or make war for that matter. They clearly want to become a hegemony, at least in Asia and Africa, if not on the entire world. Keep in mind that communism has it in its DNA to spread and Xi Jinping is a communist.

-

Funny way to frame the problem. If I interpret this right, the second row stands for Canada. All I see is that the numbers have dropped to record low levels from 358 to 44 (which Jan- Oct so 10/12 month) Extrapolating the YTD 2025 number to the entire year that 44*12/10=52.8 which is down which is just ~15% of last years number or down 85%. Ok it’s down a little less than Mexico but with numbers this small, the population size means a lot of error. What exactly is the problem here? Seems like the problem is essentially solved for both Mexico or Canada or maybe they stopped looking for terror suspects altogether. There is other data missing like how many terror suspect cross the border from the US to Canada

-

I think the right approach is to regard Chinese stocks as a trade and control risk with position size.

-

The Chinese shipyards are dual use, they produce both military as well as commercial vessels. The US shipyards are ancient rust buckets who only produce a ship here and there when they get an order. I think it takes about 10 years to get an aircraft carrier ready for deployment from start to finish. The time during WW2 was less than 12 month. I learned that at a tour on the US Hornet in Alemeda. The US had in WW2 production capacity for 10 aircraft carrier/ year, while the Japanese could do 1-2. Many people think that Japan lost the war in the battle of Midway, but they really lost it before it started because because the US had 5 x the shipbuilding capacity the Japanese had. Similary,if there is any extended engagement, the US would lose a naval war just by means of attrition. The US would need to do what the Japanese tried to do and end the war quickly. I think the us needs to restructure the industrial complex to become dual use for many things, especially ships and aircraft. The current system to produce small batches here and there can’t really produce a lot of stuff and we know that modern wars are not going to end quickly either and you need lots of stuff to fight and win.

-

Is it feasible though? Trump has not given any quantifiable criteria. How much migration is happening from Canada to the US? The border between the US and Canada itself is so long, it’s not securable. So basically Canada needs to control in-migration into Canada itself to prevent migrants to use Canada as a hub to get into the US. I am curious how this works in practice.