Spekulatius

-

Posts

15,073 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

I had no idea how bad it is: https://www.csis.org/analysis/threat-chinas-shipbuilding-empire If the war between the US and China lasts longer the US Navy has no chance, imo.

-

I think PDD is a good recovery bet, even though ai have some concerns. (No CFO). I do think it’s more likely to bounce than BABA which seems to be more mired in restructuring. It does seem like PDD days of rapid growth are over but they can switch to start returning cash to shareholders.

-

How are the 25% tariffs working for Canadian crude exports via pipelines in the U? I don’t think Canadian producers are going to eat a 25% tariff tax. Can they move the crude elsewhere or do they have to shut in wells . each would be tough to do short terms. Also this would lead to product shortages in the US and some US refineries may need to shut down until they retool for different crude grades. I wonder if this has been thought through? Mr Market seems to think that none of this is going to happen, but I am not so sure.

-

Thats sounds about right. I think companies like Apple, Tesla, Nike and Starbucks will be elbowed out of China by team China. Cheaper domestic competition and not so subtle nudging from the CCP will do it, it’s just a matter of time.

-

-Your best investments for 2024 and beyond-

Spekulatius replied to Luke's topic in General Discussion

I think STNE has a good chance of being a 50% gainer 2025. Just needs a bit help from better macro in Brazil () but even the self help from buybacks should lead to a better valuation overtime time. -

I wonder about Anduril and how efficient they are run. They do a lot of acquisitions just like other contractors and allegedly have only about $1B in revenues (which are low margins defense) and presumably a $30B market cap. A lot of their stuff doesn’t look that special - for example the Replicator drones have competition from several sources like AeroVironment and Teledyne and others.

-

Tariffs are a VAT tax on imports basically. It will work just like a VAT which is a tax on consumption of import goods.

-

Might be time to get long the right kind of drugs since RFK shoots up Heroin, consumes ZYN (long $PM), Elon is a Ketamine junkie and probably tries all drugs and Trump itself is on Adderral or something similar. Time to make Amerika high again.

-

DOGE has no authority its just a 2 person think tank. These type of constructs have been around many times before and so far none have made an impact. We will see if this one is different, but I think not.

-

Sign of the times. We are a banana republic.

-

The Less-Efficient Market Hypothesis by Cliff Asness

Spekulatius replied to Viking's topic in General Discussion

Just chiming in here:

-

Rigs are getting more efficient, especially shale rigs . The progress in technology and the industrialization of shale are deflationary forces. The US has no Monopoly on shale either, there were many shale fields in the world, the best know ex US is actually in Argentina which are not just world champions in Soccer, but even more so shooting themselves in the foot. Maybe Mileu can change that and that would like make Argentina a net exporter of energy as well. We also have China massively moving toward alternative energy (solar etc) to become less dependent on hydrocarbons , I presume partly for national security reasons. The power of the OPEC for sure is dwindling.

-

The USA and many other countries do not recognize ICC but it is a sign that Israel is losing the war here in the views of many around the world and I think it does matter. Netanyahu has overplayed is cards and now is on the same list than Putin is (who still travels around freely by the way. I say this as someone who is sympathetic to Israel , but they are making a mistake in Gazah. On a related note, I am also curious why no Hamas leaders or Iranian leader is there.

-

Even if Europe doesn’t fix itself, some European companies will be fine.

-

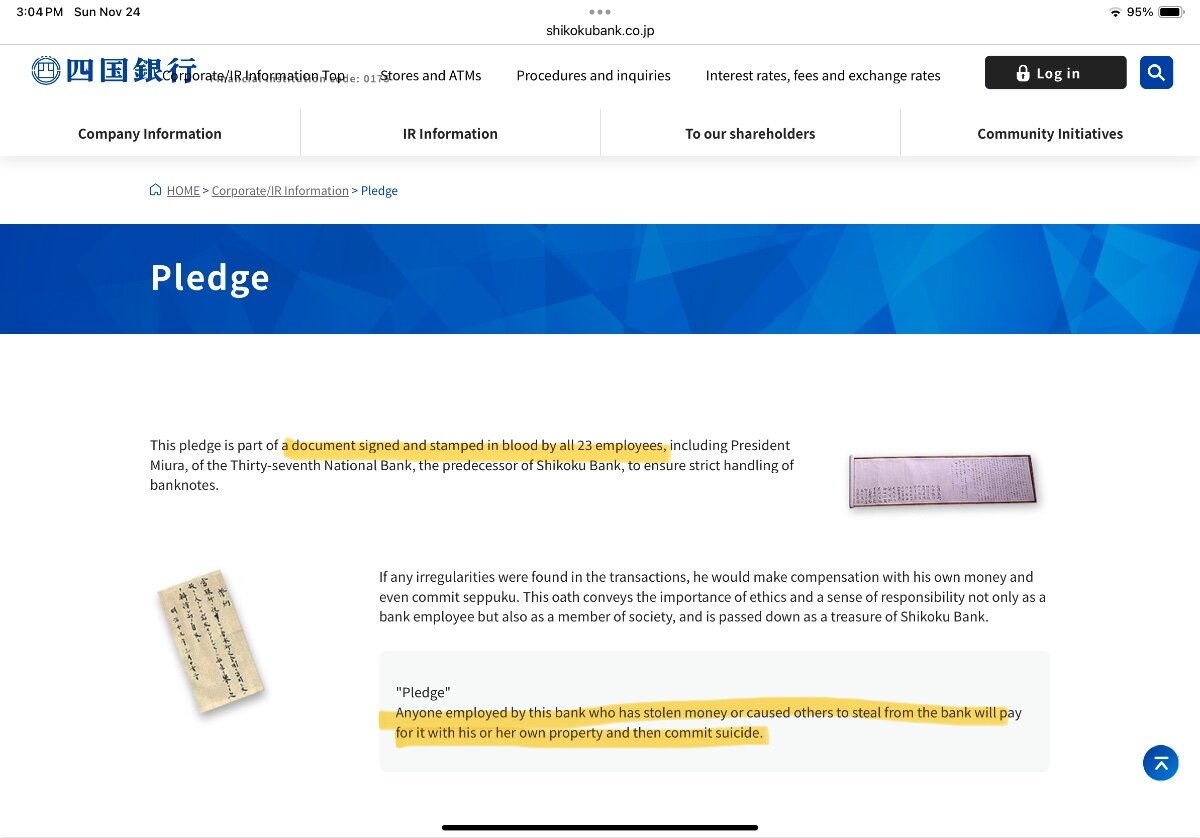

That could hurt: https://www.shikokubank.co.jp/profile/seiyaku.html

-

No idea. German politics is strange and it is likely that left and right wing parties gain ground ( if you can really distinguish between left and right as they seem to have some common objectives) https://www.politico.eu/article/germany-superstar-sahra-wagenknecht-far-left-far-right/ We could end up with a Weimar Republic situation again (worst case). Best case is that the CDU gets a stronger mandate (still needs a minority partner to govern) and actually breaks away from Merkels and Scholz policies, because those for sure aren’t working.

-

We are pretty close to 1999/2000 sentiment with record high equity valuations - not just tech (see WMT, FICO etc), US exceptionalism, large cap vs small/mid cap outperformance. Then on the other side, lot of other country stock markets are very cheap, Europe, Latam maybe China or even in US markets, if you get off the beaten tracks. I don’t know if we are in 1998, 1999 or 2000 but ai think we are closer to the top then the bottom in sentiment here, that’s for sure (to paraphrase Howard Marks)

-

-Your best investments for 2024 and beyond-

Spekulatius replied to Luke's topic in General Discussion

I have heard rumors about that, but no definite press release. Word is also that TPB nicotine pouches aren’t very good. Anyways, this was a stuck Investment from 2021. I bought it as a stealth weed stock and then it started to trade like all the other weed stock and went from ~$35 to $20 Bought a bit more and took some tax loss’s and rebought and now it went to $50 and even $60. IRR Ok, but not so great either but the stock looked really cheap at $20 so felt stupid to sell, even if it did seem to go nowhere. It was a couple percent position so no game changer. -

Yes,of course. Al, ballistic missiles are hypersonic, , but generally hypersonic missile are those that are either powered or glide and can control the direction upon descend so they are harder to intercept. Patriots system have been quite capable of intercepting the powered hypersonic Khinzal missiles that Russia came up with earlier. You don’t hear much about those any more. The bigger issues are the many glide bombs that Russia uses en Masse and that are cheap to retrofit on existing dumb bombs apparently.

-

I guess they will escalate to unannounced inspection very quickly. Sort of like “Afraid of the ghost” . It’s probably a subtle hint of being afraid of ghouls from the government. Here is another story from China when we visited our Chinese subsidy: My boss wanted to make a little smalltalk and ask the other manager who spoke a little English: ”How is your wife?” Answer: “ She is ugly!” We quickly looked at each other than at the translator and changed the subject. We later talked with the translator when the other manager wasn’t around. The translator translated everything word for word for us but neither he nor the Chinese manager understood the intend (he was around when above happened ), but as it turns out “saying my wife is ugly or not pretty “ is just being modest in China. It would be impolite and bragging to say “ My wife is pretty”. He also misunderstood the question thinking it pertains to his wife looks, not as polite small talk or genuine interest.

-

Nothing about Adani’s bribery charges from the cheerleaders here as one would expect: https://www.justice.gov/usao-edny/pr/billionaire-chairman-conglomerate-and-seven-other-senior-business-executives-indicted

-

Can buying over-valued stocks be value investing?

Spekulatius replied to jfan's topic in General Discussion

This type of “investing” is what Graham calls speculation. It can be done in an intelligent way but it’s not investing. It’s not a new thing either and has been done pretty much since the stock market was invented. John Law and the Mississippi company is the first example I know, but he probably wasn’t the first one. Ponzi did not invent the Ponzi scheme either. -

It takes you 3 minutes of google search to determine that the above stats from X are grossly incorrect as far as energy sources are concerned. First he mixes up total energy consumption with power consumptions which is RWE’s business. Germans power generation is more than 50% renewables. You can actually go straight to RWE website and look at sources https://www.rwe-production-data.com/en/map https://www.cleanenergywire.org/factsheets/germanys-energy-consumption-and-power-mix-charts

-

What are you listening to ? (Music thread)

Spekulatius replied to Spekulatius's topic in General Discussion

German Neo Punk from Weimar: Good stuff. -

Seem more a problem for the US than Europe or Sweden. This was financed by US investors, entrepreneurs are from the US and they set up shop in Sweden because I assume tax incentives and because the market was supposed to be there: I interviewed for battery startup job in the US and was surprised to learn that they were working with another battery startup in Norway that seems to be financed entirely from US VC’s.