All Activity

- Past hour

-

I’m sure AI has the capacity to do amazing things, and it reflects exactly how I feel about human beings in general. Humans are exceptional creatures with seemingly infinite potential. In the past, our species has multiple-times displayed great levels of strength, intelligence, adaptability, all in order to overcome enormous obstacles. I’m sure that with current technology we could do similar things squared in the future. However, many of the things that I see today: the enormous asset bubbles, broken politics, huge global imbalances and debt levels, stupid behavior being encouraged, will all have to revert before we can get to that point. It will be extremely painful, so painful that I often fear it may drive people completely crazy. And we’re already acting quite coo-coo. Humans have done some stupid stuff getting us here.

-

https://www.engadget.com/2212152/meta-facebook-instagram-eu-addictive-design-finding/ https://www.cnbc.com/2026/07/10/meta-instagram-facebook-addictive-design-breach-eu-laws.html Seriously, Europeans--this is what your leaders are focusing on???

-

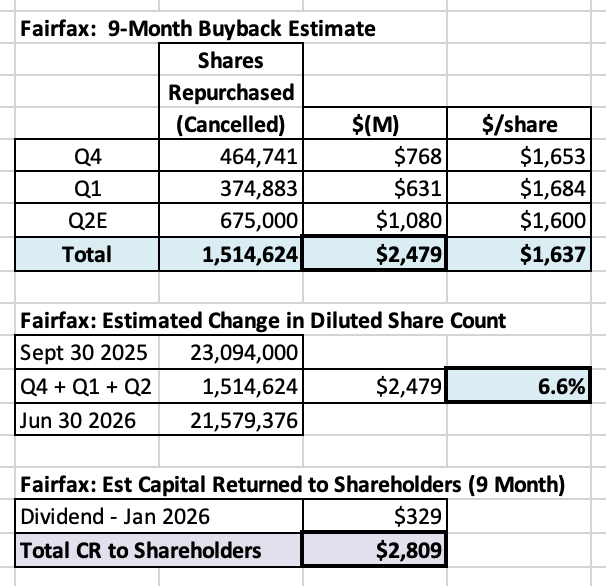

It appears Fairfax has been very busy on the share buyback front over the past 9 months (Q4-2025 + Q1 + EQ2-2026). We will get confirmation on Q2 amounts when Fairfax reports results. Shares repurchased: 1.5M, for $2.48B, or ~$1,637/share Diluted share count reduced: 6.6% Total capital returned to shareholders (including dividend): $2.81B Clearly, Fairfax feels their shares are trading at a very attractive valuation. And they are acting with conviction. ---------- Shareholder Friendly Management It is counterintuitive, but for long-term shareholders a low share price can actually be a gift — if the company is aggressively repurchasing shares. This is especially true when the discount persists for years. Buffett highlighted two major benefits. 1. Higher Per-Share Intrinsic Value This is straightforward arithmetic. When a company repurchases undervalued shares, the ownership stake of remaining shareholders increases. Intrinsic value per share rises immediately. 2. A Signal of Shareholder-Friendly Management This second benefit is more subtle — and often underappreciated. When management consistently repurchases stock below intrinsic value, it signals disciplined, shareholder-oriented capital allocation rather than empire building. Over time, investors reward this behavior with a higher valuation multiple. Buffett explained it this way in Berkshire Hathaway’s 1984 Annual Report: “The companies in which we have our largest investments have all engaged in significant stock repurchases at times when wide discrepancies existed between price and value. As shareholders, we find this encouraging and rewarding for two important reasons - one that is obvious, and one that is subtle and not always understood. The obvious point involves basic arithmetic: major repurchases at prices well below per-share intrinsic business value immediately increase, in a highly significant way, that value. When companies purchase their own stock, they often find it easy to get $2 of present value for $1. Corporate acquisition programs almost never do as well and, in a discouragingly large number of cases, fail to get anything close to $1 of value for each $1 expended. “The other benefit of repurchases is less subject to precise measurement but can be fully as important over time. By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. “This upward revision, in turn, produces market prices more in line with intrinsic business value. These prices are entirely rational. Investors should pay more for a business that is lodged in the hands of a manager with demonstrated pro-shareholder leanings than for one in the hands of a self-interested manager marching to a different drummer...” Warren Buffett – Berkshire Hathaway 1984AR

-

Totally. Bundles with live TV are now just as, if not more expensive than most cable packages were

-

Why would they cancel? YouTube TV is $65 and $85/m respectively. If Netflix charged me $40/m and it included current content and sports I would drop YouTube TV in a minute.

-

For the remaining purchase capacity I believe you would also need to include the shares purchased for Treasury. There were 25k shares purchased in Q4 and 52k shares purchased in Q1. I am not sure what was purchased for Treasury in Q2.

-

I believe they’re opportunistic with even the shares purchased for comp so it has some lumpiness

-

I noticed that total dollar value of Shares Purchased for Treasury dropped from $240M in 2024 to $189M in 2025. I am not sure of the reason for this drop as I would expect the total dollar amount to gradually grow over time as the number of employees increase. So the total dollar amount that is purchased for treasury in 2026 could vary as well.

- Today

-

During all of 2025 they purchased 118k shares for Treasury. In Q1 this year they purchased 52k shares for Treasury. I believe we may see additional purchases for Treasury this year. (corrected number of shares)

-

I know but I think it’s relevant.

-

They repurchased a million shares! Plus it was a joke!

-

Yeah, it all works 'great' for the USA : cbc.ca - Politics [July 8th 2026] : Ottawa sidelines foreign firms in $4.9B army vehicle competition Subtitle : Carney government moves to bolster domestic defence industry. - - - o 0 o - - - Lead by example! - - - o 0 o - - - The Planet D [July 9th 2026] : Canada BANS USA: $4.9B Army Deal PROVES Trump Has FAILED - - - o 0 o - - - I wonder if this - perhaps? - has something to do with - arhh-hmm - a certain bridge, or what?

-

I assume they have less shares to buy for employees than they did 5 years ago because the stock has moved up faster than total comp.

-

I don’t think that’s the right framing. I know I’m in the minority in this view but the evidence suggests they think about the insurance subsidiaries investment decisions i.e. bonds/equities different from the holdco capital allocation decisions which would include buybacks, minority interests and buying insurance companies. There is no rush on the minority interests as the financing cost is fixed. Like the TRS it’s just a form of funding. That being said, I think we’ll see them buy Allied World minority interest in this quarter likely when the proceeds of Eurolife are received.

-

Good for Canada. And good for them shifting back to a sensible energy policy. https://amgreatness.com/2026/07/09/could-canadas-energy-future-match-the-majesty-of-its-rockies/

-

Some folks are in line for a big pay day then!

-

IMHO, people are a lot more varied and complex than they can come up with labels for. People like to easily 'bin' people into 'normal' and 'abnormal' to make their lives easier. Most people think black and white, whereas some of us think in probabilities, with Gaussian curve dominating this space. If it's not covered by the 80% Gauss, they think that's 'abnormal', and would like to come up with a label for it, whether it's introversion, ADHD, autism, or whatever new fangled 'new' term they think they have 'recently discovered'. There's an incentive for the academics to try to come up with 'new' stuff, whether in nutrition, psychology, and sometime even in medicine in order to justify their own existence. Keep Gauss and the perverse of occasional academic incentive in mind, and it's much easier to differentiate true abnormality from just 'outside the norm'. Digesting other people's experiences(ex. Reddit, forums) also helps a lot. Again, just MHO.

-

Depends on how transformative AI can be.

-

Very true..... OR the so-called "expert" talking heads could just be all wrong, driven by their hatred of Trump. I've never seen so many experts root for failure - over and over - never stopping. Personally, I think if you just listened to Scott Bessent since the inception - you could just see the LONG term plan for the economy looked very promising. The difference between Bessent's fiscal policy and Biden's fiscal policy was ALWAYS night and day. Don't credit Trump - credit Bessent - and ignore the "talking heads" that have an ax to grind against Trump.

-

Couldn't stand the pain of reading bad earnings releases anymore and sold MTY Food Group.

-

Funny because I’m thinking the exact opposite.

-

A bit out of scope, but isn't one of Hyperliquid's end goal is to get everything financial onto their platform, implying that "everything financial" will be tokenized on their platform? I'm new to tokenization and Hyperliquid, so feel free to spank me. I can use an education. @thowed's article was very eye-opening, but unfortunately half of it was Greek to me.

-

Thrilled they're smashing the buyback button. It's the best when you're convinced a stock is trading at a third or maybe half of (a growing) intrinsic value and mgmt makes it easy to sit on your ass. Back to the beach...

-

Sold a bit of meta to raise some cash for businesses with negative price action

-

We may be on the cusp of a significant rise in the standard of living over the next generation that all the current political wrangling will be looked on as past noise.