Here's the Q&A from the CC for those interested

Prem Watsa

[Audio Gap] your name and your company name and try to limit your questions to only one so that it’s fair to everyone on the call.

Okay, Dale, we're ready for your -- questions.

Question-and-Answer Session

Operator

We will now begin the question-and-answer session. [Operator Instructions]. Our first question comes from Jeff Fenwick from Cormark Securities. Your line is now open, you may proceed.

Jeff Fenwick

So, as you say, an interesting time in the markets and good opportunities for stock pickers. So my first question really is just around, your general thoughts on investment rotation. And are you being very active here and maybe selectively trimming some positions and looking for some new opportunities? And I guess the one I certainly get a lot of questions on rates, not surprisingly it’s Blackberry. So any comments on I guess the allocation and perhaps Blackberry specifically?

Prem Watsa

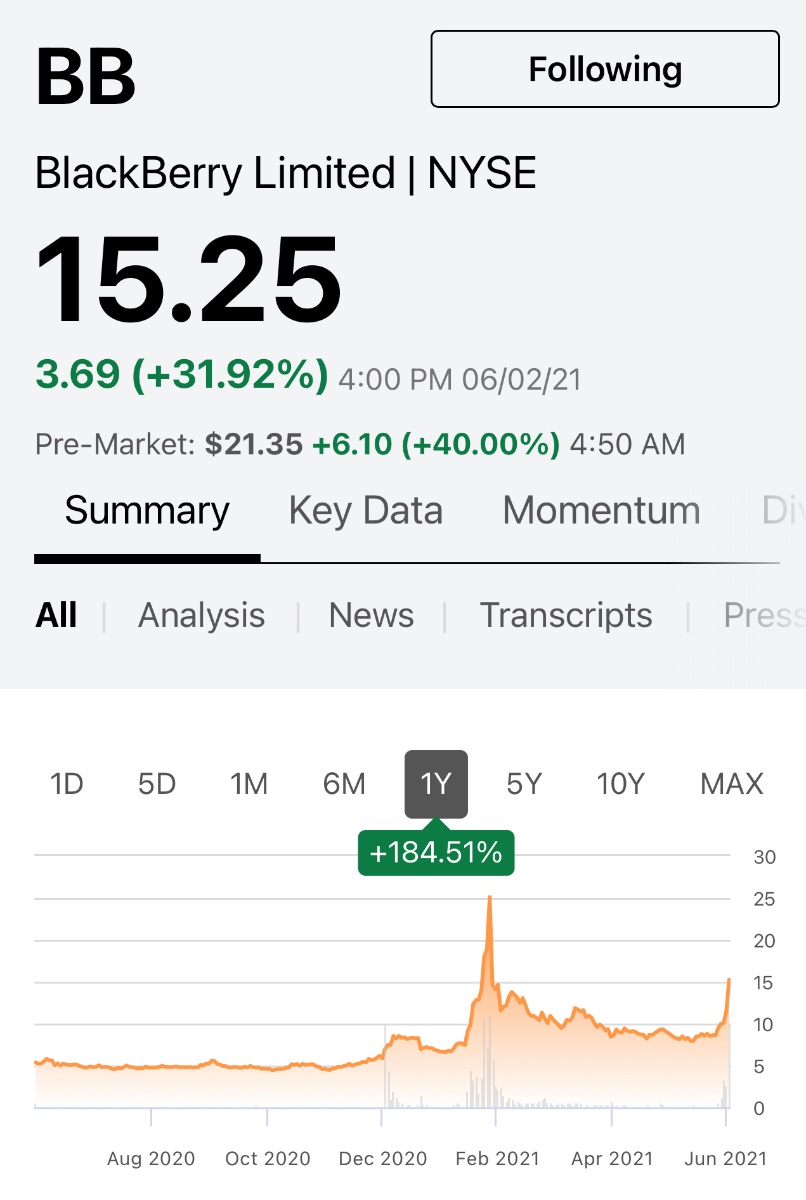

Yes, Jeff just on Blackberry, it's gone up and down. So just a couple of points. First of all, we don't comment on our securities purchase or sales, you know that. I will just say, two points. One, there are insiders and have insider obligations on Blackberry; and two, Blackberry closed on December 2020, closed the year, December ‘20 at 6.625.

Having said that, in 2019, the technology stocks were doing really well and have been doing very well for some time, as you know, Jeff. And the shift to value investing has begun, and then COVID came at us in 2020 in March. And it was significant. 180 countries that closed down their economies. We didn't know what was going to happen. And stocks -- particularly value-oriented stocks or stocks companies sensitive to the economy crashed.

Since that, we’ve come back, and now we've got vaccines coming, we've got testing. We just think the shift to value investing will take place over time. And that's already begun in November with the announcement of the Pfizer vaccine. Many, many vaccines have come to play, countries are getting back to normalization. I don't know exactly when, but that will happen. And the economies will come back.

And so we, of course, are stock pickers. We expect to make money on the things that we've invested in the past, and we are constantly looking at better opportunities. So this is what we've done with 35 years. We've got a tremendous track record. We've got a very good investment team led by Wade Burton and Lawrence Chin. And we're excited, Jeff, about what will happen in the next two years?

Jeff Fenwick

Okay, and maybe my next question, I'd like to focus on capital and uses of capital. Obviously, you highlighted how the balance sheet has strengthened after your RiverStone sale. As we look into this year with the insurance markets remaining hard, are you thinking about your first priority, I guess is pushing more capital down into the operating units? Are we looking at a similar magnitude of investment down there? I think it was $1.4 billion. Or maybe you might look more at doing something like share buybacks here if the stock is still trading below book value?

Prem Watsa

Yes, so the first thing to say is that insurance is our business -- core business. As you said, we put a ton of money in 2020 in the insurance companies. We don't think they need any more money now. Of course, our investment portfolio is coming back up as additional plus. But we've made them self-financing at the end of the year. And I'd expect them to grow significantly, when they grow they grow over time, right? So when you write premiums at -- you earn it over more than a year as the year comes forward.

So the insurance business is well primed, it reminds me of 2001 and what happened in 2002, after September 11th, some differences of course at all times. But as we said prices are going up, they're going up over all over the world and the terms are going up. We have capital. We purposely did the 14% on Brit so that we have another $375 million in case we need it. But at the moment we don't expect we need any money from the holding company or our insurance companies. They're well capitalized and financed and ready.

And most importantly, many companies are pulling back, Jeff, that our management team who run the companies are ready to expand and are expanding significantly as you saw in Allied and Northbridge and Odyssey already.

Jeff Fenwick

And I guess, maybe a comment on share buybacks then, if you have some capital available for that?

Prem Watsa

Yes. So share buybacks is always our first financial soundness, first -- a good opportunity to simplify insurance companies. Second, is share buybacks. And that's what we always look at, we had this opportunity, as we mentioned on the total return swap, it's an investment that we made. I've said before many times that our stock prices are incredibly cheap for the record that we've had. We go through phases though, we're not looking at every three months, every quarter, we are up 10%, or 5%. That's not how we run our company. But our long-term record is perhaps one of the better ones you’ll see. And so we play -- stock is cheap. So we've had a total -- but we looked at the potential investments that were available to Fairfax in our investment portfolios, we thought Fairfax was among the best, if not the best. And so we bought 1.4 million shares as we said in a total return swap and -- as an investment, we bought that as an investment. So we look at all possibilities, Jeff. And see what the future will bring.

Operator

The next question comes from the line of Juni Ra, Private Investor.

Unidentified Analyst

I have two questions. So for the total credit swaps, when is the expiry date for that and during the Reddit fiesta, did you guys take advantage by hedging any of your investments?

Prem Watsa

Sorry, when you say, the credit swaps, you mean these total…?

Unidentified Analyst

The Fairfax price. Yes, yes, so the total ones, yes, sorry.

Prem Watsa

Yes, total return swaps, yes. They are one year swaps and we've historically been able to extend it for as long as we like.

Unidentified Analyst

And then on the [Reddit] question, were you guys able to lock in any of the gains by taking any kind of hedging or was there no opportunity because of just a short period of time?

Prem Watsa

So as I said, right, I made the point that on Blackberry insiders, and we have inside obligations, and we never talked about sort of sales of our securities.

Operator

Our next question comes from the line of Tom MacKinnon from BMO Capital.

Tom MacKinnon

My question is about the selling of 14% of Brit to OMERS. I mean -- and I think you're quite -- your reasoning was, we got $375 million as a result of that and that's just in case we need it. Remember, earlier in 2020, you went to the debt market sort of in case you need it. Why are you selling off a 14% of Brit like in the height of some good hard markets here? Why wouldn't you use debt?

Prem Watsa

Yes, it's a very good question, Tom. We just want to be financially sound and we've done a very good relationship with Brit, with OMERS. You know that we had 40% on RiverStone UK that we sold to OMERS for $600 million and so they're taking $225 million and they're reinvesting $375 million in Brit. And we just think we've got a better relationship. If we bought back Tom, if we had about 89%, almost helped us in the past and we had 89%, that’s how we did the full of 14%. We bought all of it, I think back in 2020 and so we sold this 14% back. It's the $375 million possible potential, we're going to refine that sometime, which we've always done on debt issues that are coming in the next three years. We think it's just a good mix.

Tom MacKinnon

And so if anybody said, you're selling off an insurance -- part of an insurance company in what would appear to be pretty good insurance markets in order to improve liquidity versus going to the debt market, how would you answer that question?

Prem Watsa

I'd answer that by saying that we've done this before. And we have the ability to buyback that 14% from almost -- we've got many targets that we can buy it in a year and two years or three years. So it gives us a lot of flexibility, Tom. And the debt markets are bad, we understand that.

Operator

The next question comes from the line of Mark Dwelle from RBC Capital Markets.

Mark Dwelle

A couple of questions. On the Barbados, the sale of the Barbados business, you had mentioned briefly and it was mentioned in the press release about a plan to buyback or part of the agreement requires the buyback of 1.2 billion of investment assets. Could you just elaborate on that a little bit? Why is that being left out there? It seems like $1.2 billion is not an insignificant amount that presumably the holding company will need to come up with within the next couple of years in order to fund that purchase?

Prem Watsa

So, basically, we had a stock portfolio in RiverStone UK, and we could have sold it in December, or whenever in 2020. Our feeling was that it was very undervalued. So we have the ability, 1.2 billion is based on 2019 prices, year-end prices or 2022, we've got the ability to sell it or buy it back. It just -- we think it will be -- right now the 1.2 billion is very much what it's worth in the stock market, meaning the stocks in that portfolio are very much worth 1.2 billion. And we expect it to do very well. And so we can sell it if we want, or we can hold it. And we did -- we just think value investing is coming to the core.

The companies that we own are going to be -- are exceptionally undervalued in our minds. So take that, it just sold. But we think they're exceptionally valued. So it's actually undervalued and we think they're going to do pretty well. So we didn't want to sell it at these prices, but that's basically that.

Mark Dwelle

These are primarily -- these are common equities, or these are private equity holdings?

Prem Watsa

No, these are predominantly common stock positions that we have.

Mark Dwelle

My second question relates to executing the total return swap with respect to Fairfax shares. I guess, I was just curious why you pursue that structure, rather than just buying back the stock, if you felt like that was the good opportunity? I mean, is this a capital constraint that you couldn't really buy back that much?

Prem Watsa

We have to be careful, right? So not so much -- yes, we have to be very careful in terms of how much we can buy back. When we looked at Fairfax as a stock price and looked at everything else that we could buy, which is not over return swap on Fairfax. Right now, we paid US$344 per shares, our book value is $478. I mean, if you want the math, just on our book value basis, we'd have about $200 million gain. And Fairfax stock price for book value is worth another 200 million. We just think it's a terrific investment and our total return swap structure was a very good way for us to do it. And so we did it.

Mark Dwelle

I don't disagree with you that it was a good a good strike price, I guess it was really -- the form of the transaction rather than just actually buying the shares, using a derivative instead is just -- it's a little bit unusual. I haven't usually seen that with most of the companies that I've followed. So that was really my main question.

Prem Watsa

Yes, so, Mark, our point is just that we wanted to keep up -- we could -- where you have more than $1 billion in cash and the only company once -- or almost have down $375 million, we just wanted to be financially sound, and in all ways, as opposed to use that cash at this point in time.

Operator

Thank you. The next question comes from Jaeme Gloyn from National Bank Financial. Your line is now open. You may proceed.

Jaeme Gloyn

So first question is just around the Farmers Edge IPO, that seems to be -- that'll be coming out pretty soon here. Can you maybe talk about some of the other industries or companies that you're looking to maybe tap into this pretty robust IPO market as a way to realize on value in some of those holdings?

Prem Watsa

Jaeme we’re not allowed to say too much until they file and till they're done. So Farmers Edge, as you know has filed. We'll be filing some more, you'll be able to guess them. And we'll be filing them in India, in Fairfax India. Many of them there. And we've got some really good companies and we've developed them over time. And Dexterra is a classic where the old Horizon North is called Dexterra, we have 49%. And we expect that to be a very successful company over time.

So we have many of them. And when you look at our non-insurance companies, some of you analysts are worried about the fact that we don't make any money, we look like the losses. But we don't show the gains and the gains come over time. So when you look at our investment portfolio, you know that Jaeme, we've got common shares. If we have more than 20%, they become associates. If you have a 40% interest numbers like that, in the case of Thomas Cook, 65%, then you have to consolidate it.

So in our annual report in 2020 -- for the period 2020 annual report will come out in a few weeks, we're going to show it to you so that you can -- we're going to take another attempt to show you our common stock positions. And then some of them are just common stock, some are associates, some are consolidated, gets a little confusing, but that's the accounting IFRS, we have to follow the accounting rules. But we're going to show that to you in a way that I think will be easier to understand. And over time all of these investments, some do very well in a short period of time, and some take longer. And we just were patient long-term investors.

Jaeme Gloyn

Okay, great, thanks. And then just following up looking into the insurance sector as we think about COVID-19 risks and losses and reserving there. Yes, I would expect that loss reserves would diminish as the vaccine rollout unfolds. But can you talk about maybe some of the exposures in event cancellation and business interruption?

Prem Watsa

Yes, so event cancellation Jaeme we've taken the next six months. These event cancellation policies have very few, if any, and be written after March 2020. And so we've looked at the -- Brit has look forward and Allied were the two. And we've basically written up the first six months, where we think they’ll be written. So we don't expect that to be of any significance. But as I said in my comments that, there is that uncertainty, but we don't expect it to be very significant.

Jaeme Gloyn

Okay, and then on BI as well, do you have a quick comment to sort of frame that risk, like you just did with events cancellation?

Prem Watsa

Which risk again Jaeme, sorry?

Jaeme Gloyn

Business interruption.

Prem Watsa

Oh, business interruption, yes. Business interruption is an international risk that you have, so it's outside North America. We've taken most of the hit, you'll see that like 50%, 60% of the gross numbers that we've set up are IBNR, right? So that's reserves that are not allocated, incurred but not reported that we expected to come. We've been concerned as you’ve all through our history, we've been conservative. And so we expect that even in the case of business interruption. And there are some lawsuits and there's regulatory bodies making decisions, you have to watch how they come through. But we think all-in-all right now we’re well reserved.

Operator

The next question comes from [Mikhail Porter], a Private Investor.

Unidentified Analyst

I believe that it is time that you step down from having primary investments, responsibilities. I know that Jamie manages some capital, Wade manages some capital. We all know that those are very small portions of the capital base. And I think you are always quoting your long-term track record, but I can -- I know when the man is out of tune with the markets and I also think that it was a huge mistake if you did not take the BlackBerry gift that was given to you by the market. And I also don't think that you're doing deep analysis on your holdings.

I suspect that you probably don't do a lot of diving into the financials, the statements. You probably don't understand the microeconomics of the businesses you're buying. You probably are not talking to customers, suppliers, competitors, former employees. The investment business is a very competitive business. It's not like it used to be. I am not saying that, you should go out and buy technology stocks, but a sense when the man is not competitive in the field and is not working hard. And I think it's time that you step down from primary investing and I'm sure many of your associates agree with you but because they're Canadian, and tend to be nicer than Americans they don't say anything. And the banks don't ask you any difficult questions, because there's so few good companies in Canada, and they get financing fees from you. So they ask cowardly questions. Thank you.

Prem Watsa

Good points. You're entitled to your opinion, and we will let time decide that, okay? So thank you very much for your comment.

Operator

The next question comes from the line of [indiscernible], Private Investor.

Unidentified Analyst

My question is regarding Fairfax India. Could you please provide an update on your investment in Bangalore Airport? Are you still bullish about the prospects of that in investment given the situation with COVID and how it's going to evolve in the next two, three years? And also, could you provide an update regarding the deal you had with OMERS to sell stake at 2.7 billion valuation? And can we expect to like, has it closed or could you provide an update there? And also could you provide an update there? And also, could you tell us like whether we are still looking to do the IPO as it was written in the last annual report by the end of this year?

Prem Watsa

Yes. So Bangalore International Airport is a world class airport, going very well, the -- but stopped of course, during COVID. The business is coming back significantly, passengers are -- it's running at about 60% of capacity. And so the terminal is delayed, but the 2022, the second terminal will be built. The second runway is already built. And we expect it to -- we’re as excited about Bangalore International Airport as we always were. And we got our Toronto guy running it as you know, Hari Marar. And so this company will be on its way, in terms of it’s -- in terms of Fairfax India itself is a tremendous opportunity.

India is a land of opportunity. It's become very business-friendly. And Mr. Modi has come up with a very good budget. And we expect that our anchorage -- over time we’ll take it public, we think 2.7 billion, 2.8 billion for Bangalore International Airport 100% basis now is a very reasonable price. And so that's very, very possible.

In terms of the anchorage, approvals are still -- India there's a lot of approval, has to be the one more approval that is necessary and we think it will come soon. And so as excited customers in terms of Fairfax India. It has got lots of possibilities.

With that Dale let me take the last question, if you don't mind.

Operator

The next question comes from the line of Alan Parsow from Elkhorn Partners.

Alan Parsow

I just need a little bit of clarification if I can on the questions regarding Blackberry. I understand that you don't discuss changes in portfolio et cetera, regarding any of your positions. But there were filings made and this goes with regard to your inside comments, insider comments and directorship. There were some filings made in January, were six of the -- lots of Fairfax team sold their entire positions in Blackberry. I understand that's a subsequent event to the end of the quarter. But can you explain how they're able to sell their shares? And Fairfax may not be able to sell theirs? Or in the past, you’ve had two different positions in Blackberry, one convertible bonds and common stock. Are you saying you have restrictions on both of those for clarification for me, please?

Prem Watsa

The securities, SEC doesn't distinguish between convertibles and common shares. And in the case here, we are an insider. I am an insider, and Fairfax is an insider. Some of the people may not be insiders, and I don't know who you're referring to Alan, but some of them may not be insiders. And so they can do...

Alan Parsow

An example, Wade Burton, Roger Lace, I mean, there were significant investor people?

Prem Watsa

Yes, that's right. But the company is an insider. So we follow all these rules very carefully. And no one can sell anything unless they go through our legal department. And so we're very, very careful Alan in this type of situation. And because we don't talk about individual securities still till we’re done, that is how we run our affairs for 35 years. So you have to bear with us, Alan.

Prem Watsa

And I thank you for your question. I thank all of you. Dale, I think we're ready to go on to end the call. And as we've announced previously, for your safety and for the safety of all our employees from the global pandemic, our Annual Meeting will once again be held virtually on April 15th, at which time I look forward to answering again, all your questions. Instructions on how to join that webcast will be published on our website soon. So Dale thank you very much. This will terminate the call. Thank you.