nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Occam’s razor springs to mind.

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Some notes on Green et al attached. Nothing new to those who have thought a bit harder about the pros and cons of Indexing than I have The_Passive_Investing_Debate-2.pdf -

159.9 is post tax for sure and conservatively I assumed the $35m is pre-tax. This is a bit of a moving feast, but I take your point. APR at this point is noise but is surprisingly material noise.

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Not specifically. What strikes me about Algos, Quants, and Indexing is that they tend to converge on the crowded trade. The discussion made me think about how, in investing, it can never truly be ‘set and forget.’ Indexing, in particular, reminds me of an AI training data set that works well in the early days but becomes corrupted as more of the data becomes self-referential. If there are no rational price setters, what is there to index? The same applies to algos unless they are programmed as rational actors rather than mere positioning exploiters. There’s a potential outcome here not unlike portfolio insurance in 1987. -

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

The latest We Study Billionaires with Scott Barbee is worth a listen. some interesting comments on Indexing that I need to dig into some more. transcript attached https://podcasts.apple.com/au/podcast/we-study-billionaires-the-investors-podcast-network/id928933489?i=1000664914692 Summary: In this episode of "The Investor's Podcast," Scott Barbee, the manager of Aegis Value Fund, shares insights into value investing, his experiences navigating market cycles, and his concerns about current market trends. The conversation highlights Barbee's disciplined approach to investing and the challenges of maintaining a value-oriented strategy in a market increasingly driven by momentum and speculation. Value Investing's Resilience: Barbee emphasizes the enduring relevance of value investing, even as it has fallen out of favor in recent years. He argues that purchasing stocks below their intrinsic value provides a margin of safety that is crucial, especially during periods of market turbulence. Despite the dominance of high-growth tech stocks, Barbee has stayed true to his value investing roots, which has allowed his fund to outperform over the long term. Key Quote: "When you buy things that are under intrinsic value and you're waiting for the prices to get up to intrinsic value, it's more of an investing kind of orientation... I’ve always had the value philosophy." Navigating Market Crises: Barbee recounts the challenges of managing his fund during the financial crisis of 2007-2009, when the Aegis Value Fund saw a significant drawdown. Despite the market's volatility, he remained confident in his investments, which were trading at deeply discounted valuations. His experience highlights the importance of staying disciplined and focused on fundamentals, even when the market is in turmoil. Key Quote: "That was a tough time... The fund went down about 72% during that period... But these companies were trading at valuation levels... They were absurdly cheap." The Risk of Indexing and Market Distortion: One of Barbee's most striking insights is his concern that the rise of passive investing and indexing may be distorting the market. He suggests that the massive inflows into index funds have led to the overvaluation of certain stocks, particularly those in the S&P 500's "Magnificent 7." This could be creating a market where prices are less reflective of fundamental value and more driven by the mechanics of index investing. Key Quote: "I think a lot about the work of Michael Green and Einhorn... Horizon Kinetics has done some great work on the impacts of this immense fund flow that's been going into passive... There's this belief that, oh, we can just set it and forget it... But now you have these stocks having ripped higher." Concerns About Tech Stock Valuations: Barbee expresses significant concern about the sustainability of the high valuations in the tech sector, particularly with regard to companies like NVIDIA. He points out that while these companies have shown strong earnings growth, the massive energy consumption and infrastructural demands they create could pose serious risks in the future. Key Quote: "I find clearly within NVIDIA... there's been strong earnings growth. But the sustainability of that, I would put in some question... Each chip requires as much energy as one household... There's going to be the emergence of bottlenecks to the ability of these companies to continue to grow." Opportunities in Underpriced Assets: Despite his concerns about the current market environment, Barbee sees opportunities for those with the mental agility to pivot away from overvalued stocks and into sectors or companies that are currently undervalued. He suggests that these areas may offer better long-term returns, particularly if the market corrects. Key Quote: "There's a real opportunity here for somebody that has that mental agility to switch into things that are much, much cheaper and perhaps get a double run... They could be pretty nasty, I would think." We Study billionaires - Scott barbee (1).pdf -

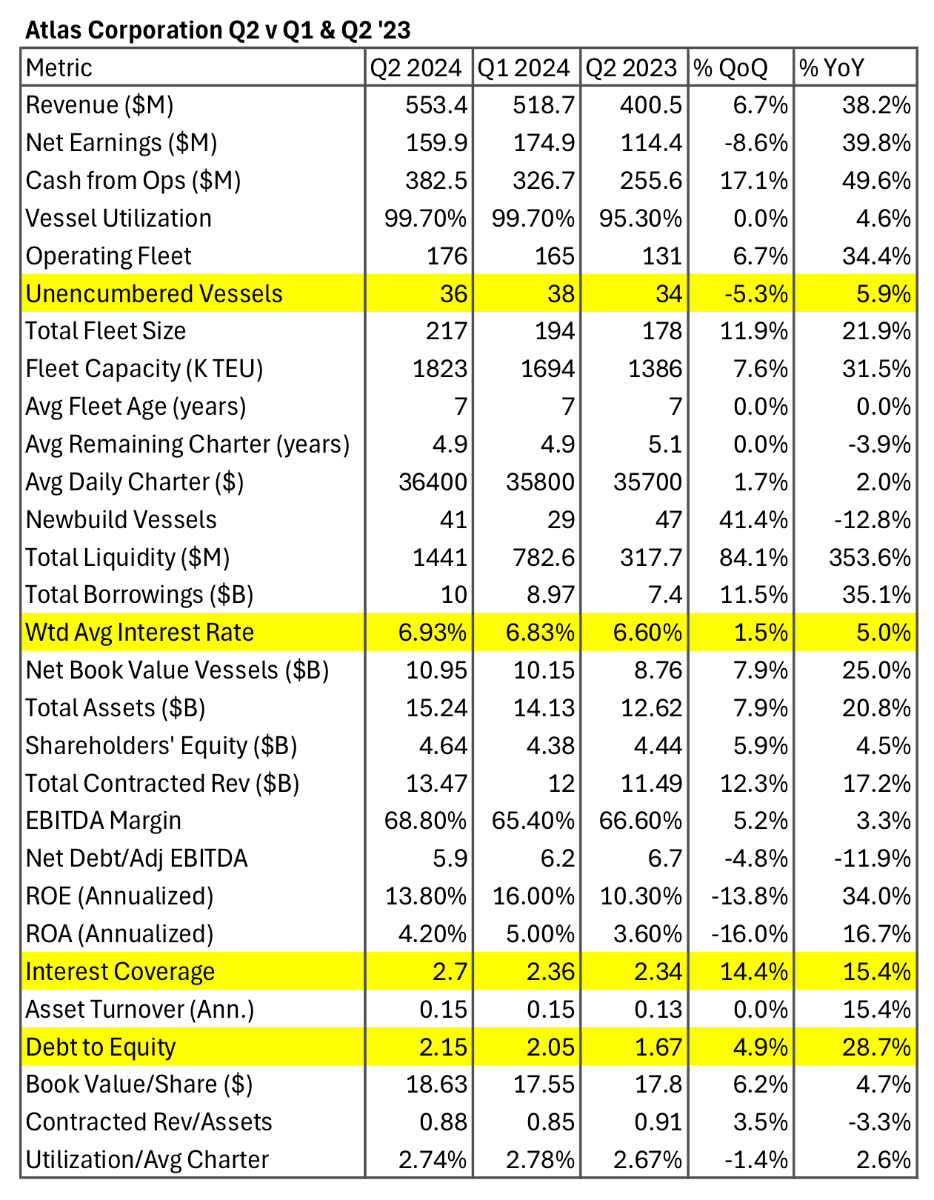

Looking at the numbers a bit more closely there was a contract settlement with APR Energy that juiced this quarter and is non-recurring. A settlement with Ambar Energia, S.A. significantly influenced the quarter's profit for APR Energy and Atlas Corp as a whole. Settlement Amount: The total settlement was $55 million. Immediate Impact: Of this $55 million, $35 million was new income not related to existing receivables. This $35 million would directly impact the profit for the quarter. Profit Recognition: The financial report states: "Since APR Energy has no further obligations under the contract, the full settlement has been recognized into income in the current period." Quarterly Revenue: APR Energy's total revenue for Q2 2024 was $49.8 million. The $35 million settlement represents a substantial portion of this revenue. Overall Impact: In the consolidated financial summary for Atlas Corp, the total net earnings for Q2 2024 were $159.9 million. The $35 million settlement represents about 22% of this total net earnings. Unusual Nature: This settlement is a one-time event and not part of regular operating income, which makes it particularly significant in assessing the quarter's performance. So adjusting: Reported Net Earnings for Q2 2024: $159.9 million One-off Settlement Amount: $35 million (We're using the $35 million figure as this is the portion that wasn't related to existing receivables) Adjusted Net Earnings: $159.9 million - $35 million = $124.9 million Still puts earnings around $300m for the first half though. As I said above, hopefully this all becomes a bit clearer in the coming quarters. The good news is it seems to be more accretive than I was hoping for this year.

-

Quite the lollapalooza if they get a credit re-rating in conjunction with a drop in rates. As it is, they look like they will blow past the FY profit forecast of $400m that Prem mentioned in the 2023 annual, next quarter, even without a drop in rates. Now that is truly managing expectations Using Seaspan's last public share count: The last reported number of outstanding shares for Seaspan before going private was approximately 249.2 million shares. Forecasted annual earnings (based on Fairfax's projection for Poseidon): $400 million Theoretical EPS = $400 million / 249.2 million = $1.60 per share. This is the number that Wade was referring to in the CC. If we take the run rate to date for the first 6 months $321m and double it for the remaining 6 months that would give an annualised profit of $641.8m or $2.58 per share. Perhaps there is revenue/expense mismatching going in the quarter or costs associated with bring new vessels on. It will be fascinating to see next quarter's results.

-

Really depends on how the acquisition affects the MCT calculation (Canada) or RBC (USA). If these ratios are still in acceptable ranges then absolutely. I think this is the ultimate end game. I always saw Shaw Carpets as a bit of a P/C clawback. Perhaps I will come to see bedding the same Edit: or conversely you wanted some real time data on household formation. Real time macro data can be quite helpful.

-

In the good old days of the last decade it was around 18-20%. More like 10-12% these days From their Q2 “Coal volumes decreased 29% and 25%, respectively, in the second quarter and first six months of 2024 compared with the same periods in 2023 primarily due to lower natural gas prices, which displaces coal as a fuel used by utilities.” https://www.bnsf.com/about-bnsf/financial-information/pdf/performance-summary-2q-2024.pdf

-

Cheers, that makes good sense. If the seasonal trend continues and this get’s closer to 1x’s sales, then it looks more appealing.

-

For those playing along at home 1. Ship Operating Expenses: Increased from $96.0 million in Q1 to $114.9 million in Q2, reflecting a 19.7% increase. This rise can be attributed to the growth in the fleet of operating vessels. 2. Depreciation and Amortization: Increased from $112.3 million in Q1 to $131.1 million in Q2, a 16.8% increase. This is primarily due to the continued expansion of the fleet and the reclassification of certain leases from operating to financing. 3. General and Administrative Expenses: Increased from $13.3 million in Q1 to $19.8 million in Q2, reflecting a 48.9% increase. The Q2 increase can be partially attributed to a gain recognized in the current period related to the settlement of a contingent consideration asset. 4. Operating Lease Expenses: Decreased from $22.7 million in Q1 to $14.1 million in Q2, a 37.9% decrease. This reduction is mainly due to the reclassification of certain leases from operating to financing as a result of purchase options being exercised for several vessels. 5. Interest Expense: Increased from $129.1 million in Q1 to $153.1 million in Q2, reflecting an 18.6% increase. This increase is driven by an increase in outstanding debt and other financing balances, as well as an increase in benchmark rates on these financings .

-

I might be reading to much into the purchase but I get the impression that Fairfax likes the management as much as the company. The CEO of Sleep Country Canada Holdings Inc. (TSX: ZZZ) is Stewart Schaefer. He was appointed as the CEO in April 2021 and has been a part of the company since 2006. Before becoming CEO, Schaefer served in various roles, including President of Dormez-vous and Chief Business Development Officer. He has been instrumental in driving the strategic vision and growth of the company, overseeing strategic partnerships and mergers and acquisitions. Stewart Schaefer has a long history in the sleep industry, having founded Dormez-vous in 1994, which was later acquired by Sleep Country. His leadership has been pivotal in Sleep Country's success, particularly in expanding its e-commerce business and forming new partnerships. Out of all their retail and restaurant investments this one seems to be less of a turn around and more along the lines of a decent business at an OK price. I hope it is a sign of things to come. Stable recurring cashflow/income from non-insurance businesses will definitely help with any re-rating and P/B multiple expansion. Besides there is always the very real possibility that, depending on where we are in the retail cycle, they are getting value that is equivalent to repurchasing their own shares. The consumer is definitely under significant pressure at the moment.

-

Good point, naming continuity seems to be a high priority, along with “everyone keeps their jobs” for three years. From my reading I think Kotak is going to walk. Do we know anything about NBD Emirates? I didn’t know they were in the running until last week.

-

Cheers. This stood out from the release “Despite the strong overall performance in Q2, we have been seeing a trend with our customers trading down to lower priced mattresses at SCC/DV with double digit declines in units in our highest price band. This trend has continued into Q3 2024, with the SCC/DV network experiencing negative (8.4%) SSS1 for the month of July, our biggest monthly decline seen this year, while our DTC SSS1 metric grew 30.0% in July 2024 tied to promotional discounting and accessory bundling," continued Schaefer. “ Metrics - quick and dirty. For me 1x’s sales 2x’s book would be the starting point based on 6% NM. Their margins are pretty tidy for this type of business. The net margins are: Q2 2024: 6.81% YTD 2024: 5.56% Based on Fairfax's takeover price of $35 per share: Transaction Value: Offer price: $35 per share Total shares outstanding: 33,901,254 Equity value: $1.19 billion (33,901,254 * $35) Enterprise value: Approximately $1.7 billion (as stated in the announcement) Price-to-Earnings (P/E) Ratio: Based on Q2 2024 diluted EPS of $0.46, annualized to $1.84 P/E Ratio = 35 / 1.84 = 19.0x EV/EBITDA: Using Q2 Operating EBITDA of $50.9 million, annualized to $203.6 million EV/EBITDA = 1,700 / 203.6 = 8.35x Price-to-Sales (P/S) Ratio: Based on Q2 2024 revenue of $232.5 million, annualized to $930 million P/S Ratio = 1,190 / 930 = 1.28x Price-to-Book Value: Total Shareholders' Equity (as of June 30, 2024): $463.8 million Price-to-Book Ratio = 35 / (463.8 / 33,901,254) = 2.56x EBITDA Margin: Q2 2024 Operating EBITDA margin: 21.9% Revenue Growth: Q2 2024 vs Q2 2023: 7.0% increase Same Store Sales (SSS) Growth: Q2 2024: 4.8% increase Dividend Yield (based on last declared dividend): Annual dividend: $0.948 ($0.237 * 4 quarters) Dividend Yield = 0.948 / 35 = 2.71%

-

Interesting. I see that as disciplined and not a negative. Go figure.

-

Feel for you, these brokers are goal-post-moving pricks. Possibly not a bad thing if you are new to margin though. Might be helpful to frame margin in the context of if this is happening to you, then what are the ramifications across the board for those that are carrying margin but are not so value orientated. Their actions and leverage feed into the machine and will affect you no matter what the IV of your investments are.

-

Ok I’ll play 1. Weak Hands (i) Margin, WTF it goes down! (ii) changes in margin policy, bugger I got a call/email 2. Margin debt at 2.8% of GDP, I don’t have any margin but aware of #1 3. Price=value, great run, lock it in, October generally sucks, hurricanes etc 4. Rate cuts, hard market is done, earnings after 3 years or so will be permanently impaired 5. Hmmm, Berkshire sold half their Apple, cashed to the gills, cool, will rotate given their conservative positioning and taking into account 1-4. Share price alone (ignore divs on the returns chart) this might be an even race 6. Not aware of the IDBI possibility, WTF 7. Aware of IDBI, hoped they wouldn’t make the list, here we go again 8. They are going to buy a Canadian mattress company, again WTF Point #2 was a bit of a revelation for me with 3% being a true red flag. Very easy to beaver away and collect positions on margin at appropriate valuations but get the rug pulled. During deleveraging there is no safe haven, your fellow shareholder may be getting called, tax matching, or simply panicking. Valuation may well be secondary consideration or not even feature. In order to not get shaken out I took some measures to ensure it couldn’t happen. Selling Fairfax would cause some significant tax implications that are not warranted given price to IV. Not adverse to paying tax at some point but not when this is still a <70 cent dollar and my best idea. https://www.gurufocus.com/economic_indicators/4266/finra-investor-margin-debt-relative-to-gdp https://www.owenanalytics.com.au/margin-lending?t&utm_source=perplexity

-

Sold minor positions plus Apple and Markel to eliminate margin in one account. Rotated Apple into Berkshire in the other.

-

This becomes somewhat of a circular argument https://www.reuters.com/markets/asia/boj-wont-raise-rates-when-markets-unstable-deputy-governor-says-2024-08-07/?utm_source=Twitter&utm_medium=Social

-

These short-covering rallies are just as fierce as the sell-offs. If this is a real deleveraging event then I am sure Mr. Market will offer up another opportunity.

-

Impressive as always. Happy hunting

-

You stand a good chance, the circuit breakers have been popping on the TSE

-

7974.T Nintendo, exited a gaggle of minor Japanese positions.

-

Isn’t that the very definition of a “Megacap”. Berkshire is a mere minnow. Edit: sorry if the subtlety of you comment was lost on me , it won’t be the first time.

-

That’s the one. What I find incredible is that this is all developing as predicted. Do we suddenly think that they might not have a crack at corporate credits sometime in the not too distant future? Perhaps even some rationally priced equities. All the while hoovering the one thing they know the best. .