nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

That’s the one. What I find incredible is that this is all developing as predicted. Do we suddenly think that they might not have a crack at corporate credits sometime in the not too distant future? Perhaps even some rationally priced equities. All the while hoovering the one thing they know the best. .

-

Yep, 1.4-1.5x’s seems to be the limit. Consistent with what many of us view as a proxy on FV and the maximum price that gives you a shot at 10% returns IMHO.

-

Book Value Calculation: Total Shareholders' Equity: $601.7 billion Class A shares outstanding: 553,302 Class B shares outstanding: 1,325,090,508 Class B to Class A conversion ratio: 1,500 to 1 Total equivalent Class A shares: 553,302 + (1,325,090,508 / 1,500) = 1,436,696 Book Value per Class A Share: $601.7 billion / 1,436,696 = $418,811 Book Value per Class B Share: $418,811 / 1,500 = $279.21 P/B Calculation: Book Value per Class A Share: $418,811 Market Price per Class A Share: $641,435 P/B Ratio = $641,435 / $418,811 ≈ 1.53

-

Conference call notes. Transcript attached Financial Performance and Outlook Peter Clarke highlighted sustainable operating income: "For the first time in our 38-year history, we can say to you we expect, of course, no guarantees sustainable operating income of $4 billion." Investment Portfolio and Strategy Wade Burton provided insights on the portfolio structure: "The investment portfolio stands at $66 billion at the end of the quarter, $37 billion is in fixed income, including USD 18 billion in Canadian treasuries and another $4.9 billion in mortgages. In addition, we have approximately $9 billion in cash and short-term investments, duration is 2.7 years, including cash and the yield is 5.1%." WB on current market conditions:"The high prices of stock markets means opportunities are not pouring our way in marketable securities. And the small size of this part of our portfolio reflects that. Our team continues to screen through stock markets worldwide, looking for value, which will no doubt emerge. But in the meantime, our private and strategic investments provide excellent earnings and our fixed income portfolio continues to produce strong interest income with rates well above 4%." Hidden Book Value Clarke highlighted unrealized gains not reflected in the book value: "As mentioned in previous quarters, our book value per share of $980 does not include unrealized gains or losses in our associate investments and our consolidated investments, which are not mark-to-market. At the end of the second quarter, the fair value of these securities is in excess of carrying value by $1.5 billion, an unrealized gain position or $68 per share on a pretax basis." Key Investments Performance Eurobank: Burton noted: "We're expecting well over $1.2 billion in net income in 2024. The balance sheet has never been stronger with Basel III fully loaded core Tier 1 of 16.2%." He added, "The bank has also paid its first dividend in more than 16 years, a EUR 0.09 per share dividend, which resulted in a $128 million dividend payment to Fairfax." Poseidon: Burton highlighted: "Poseidon owns 184 cargo ships, all with long-term contracts and with the average life of the contracts around 9 years... It's amazing looking back in 2019, Poseidon made $0.80 a share in net income. This year, it's on track to making $1.60, a double, a fantastic performance." Risk Management and Recent Events Peter Clarke addressed analyst concerns: "Very little impact we expect from those two events. Beryl, especially, we don't see -- it's more of an attritional cat loss for us we expect in the third quarter." Casualty Reserving Clarke reassured: "Our companies have done a wonderful job managing the cycle, writing much less business during that period and then expanding in the hard market years, 2000 and onwards. So of our $34 billion net reserves, about 80% are in these hard market years." Growth Outlook Clarke explained: "Growth has slowed down in the first 6 months of 2024. I think on a gross basis, we're up about 1% on a net basis, 3%. That of course, excludes the Gulf acquisition." Gulf Insurance Outlook Clarke provided insight: "We've been invested in Gulf for the better part of 12 years. And if you look over that time period, they produce consistently combined ratio below 95%, I think, on average, about 94%. So that -- we'd expect it would run at that rate going forward and in the future." Capital Allocation and Share Buybacks Clarke confirmed: "Our companies grew almost 16% per year over the last -- since 2019, and we supported that growth through capital generation of the insurance companies. Now with that premium leveling off last year and this year, it's producing excess capital and strong dividends to Fairfax.And we've been using that to buy our shares. We think they're at great prices, and we'll continue to do that going forward” Jen Allen: "So Jaeme, we did receive additional dividends in the quarter. On a YTD basis, we do provide disclosure in our MD&A under the liquidity section. So I'll refer you to that for the additional dividends that were received." Acquisitions Regarding the Sleep Country acquisition, Clarke stated: "We think Sleep Country will be a great investment over the long term and are very happy that their talented team led by Stewart Schaefer, will join the Fairfax Group." FRFHF Q2 24- Transcriptt.pdf

-

FFH for me too, to save a post rotation was from MKL

-

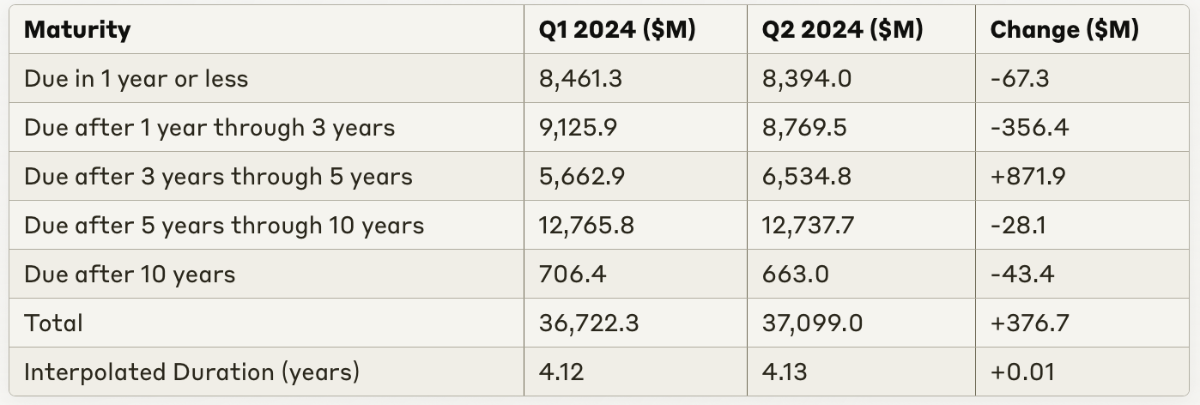

I realise you are talking post 30 June but this was the composition of the bold portfolio Q1 to Q2. Interpolated duration computed on the midpoint of each bond category. Inaccurate but shows not much change quarter on quarter.

-

Great results and meaningful contributions from Eurobank and Poseidon. Eurobank Contribution: Q1: $79.3 million Q2: $126.1 million ($5.68 per share) Poseidon Contribution: Q1: $34.8 million Q2: $66.5 million ($3.00 per share) From the 2023 AR “Poseidon is expected to make net earnings in excess of $400 million in 2024 and $500 million in 2025. We carry our 43% ownership in Poseidon at $1.7 billion - 10x 2024 expected earnings or 8x 2025 expected earnings.”

-

7974.T Nintendo. Small add. Earnings tomorrow, hopefully we get a similar short term reaction as last quarter.

-

Tidy set of results out of Eurobank. MS upgraded their price target to €2.68 (+13.5%). Or around $3.5bn+ in terms of Fairfax’s stake. Note attached and summary as follows: 1. Eurobank beat estimates, with adjusted net income 16%/9% above Morgan Stanley/consensus estimates. NII and expenses both better than expected. 2. The bank raised guidance: - FY24 ROATE to ~16.5% (from ~15% previously) - Core operating profit to >€1.6bn (from >€1.5bn) - NPE ratio lowered to ~3% (from <3.5%) 3. Key financial metrics: - Net interest income: €561mn (-2% QoQ, +4% YoY) - Net fee and commission income: €147mn (+8% QoQ, +4% YoY) - Operating expenses: €228mn (flat QoQ, +3% YoY) - Provisions: €73mn (+2% QoQ, -18% YoY) - Adjusted net profit: €349mn (-9% QoQ, +2% YoY) 4. Asset quality improved, with NPE ratio at 3.1% and coverage at 93.2%. 5. Capital position remains strong with CET1 ratio at 16.2%. 6. Performing loan growth accelerated to €0.8bn in Q2, driven by SEE operations and Greek corporate lending. 7. Eurobank completed acquisition of a 55.9% stake in Hellenic Bank. Risks to Upside - Faster-than-expected loan growth, driven by EU funds and macro recovery in Greece - Higher-than-expected fee and commission income growth - Stronger macro drives NPE levels below our expectations Risks to Downside - Early-stage recovery in macro environment is vulnerable to external shocks - Absorption of EU funds is weaker than expected EUROBANK_20240731_1544.pdf

-

@Thrifty3000 @Junior R thanks for the posts above. Looking at this purchase through a health and wellness lens is a helpful take. Having just been through this exercise we ended up spending 5k+ (The Rest territory) on a mattress and don’t regret it at all . Something that you use for 6-8 hours over 7-10 years makes nickel and diming pointless IMHO. We ended up going through a Sleep Country equivalent here in Oz, service and range were a factor in our choice of retailer. The cheaper providers just felt shonky by comparison. I also wonder if Fairfax might be able to support the debt component at a more competitive rate too. Those credit rating upgrades are a beautiful thing. It becomes a bit of virtuous circle as they start adding relatively stable cashflow generators too. This purchase is growing on me, thanks for all the commentary. Hopefully we can look back and distinguish this from their other crappy retail investments.

-

Rumours are circulating that the decision on the final bidders is getting close. Big jump in IDBI’s share price yesterday. “New Delhi: Authorities are at an "advanced stage" of wrapping up the process to identify "fit and proper" buyers for a majority stake in IDBI Bank and the strategic sale of the state-run lender is expected to be concluded this fiscal, Tuhin Kanta Pandey, secretary, Department of Investment and Public Asset Management (DIPAM), said on Tuesday.” https://m.economictimes.com/industry/banking/finance/banking/in-final-stage-of-identifying-idbi-bidders-tuhin-kanta-pandey/amp_articleshow/111996803.cms

-

Some more colour on Regulation 379/2014, I think this is what gives Eurobank the edge here as the possibility of delisting is highly likely: Regulation 379/2014 of the Cyprus Securities and Exchange Commission specifies certain minimum share dispersal criteria for companies listed on the main market of the Cyprus Stock Exchange: - At least 25% of the shares proposed for listing must be held by the wider public (free float requirement) - The shares must be held by at least 300 natural persons or legal entities So this regulation aims to ensure a minimum level of diverse public ownership for companies listed on the CSE main market. The 25% free float requirement prevents a small group of insiders from holding all or most of a publicly listed company's shares. And the 300 person minimum helps ensure the shares are reasonably widely held rather than just technically meeting the 25% threshold among a very small number of public shareholders. These provisions promote shareholder diversity and broader public participation in the ownership of listed companies on the Cyprus Stock Exchange main market. Key thresholds: Based on Cypriot corporate law, the following shareholder approval percentages are required for various corporate actions: Ordinary Resolution (over 50% approval required): - Appointment and removal of company directors - Alteration of the company's share capital (increase, consolidation, division, sub-division, cancellation, conversion of paid-up shares into stock) - Appointment and removal of auditors Special Resolution (at least 75% approval required): - Amendment of the memorandum of association - Amendment of the articles of association - Change of company name Reduction of share capital - Variation of shareholders' rights (unless a higher threshold is specified in the articles of association) Extraordinary General Meeting (EGM): Shareholders holding at least 10% of the paid-up capital with voting rights can requisition the directors to convene an EGM. This right cannot be waived or varied by the articles of association. So delisting is likely and Eurobank has the right to fire the existing board and put their own directors in. I can’t find any further minority protections. I guess they can argue oppression but that is difficult with takeover clearance given and other sophisticated investors already accepting lower bids. @hoodlum as you say, the market is giving developments the

-

Eurobank hung onto its highs and closed as a $3bn+ position for Fairfax for the first time 3 coffees in and still can’t get my head around the purchase of ZZZ now. Seems to me this should have been a blood in the streets acquisition if they were going to do it all. The consolation is they are paying prices last seen 7 years ago. It should work out OK at this price but seems lower quality than what I would have hoped for given the deal size.

-

+1, that works

-

Yes it all seems quite frothy but not when the industry you are playing in is growing at high single digits. Their ability to grow premiums has varied but I would say it is closer to 20% CAGR off the current base say 2-3 x’s the industry. We also haven’t seen what they can do on the investing side. Do I think it will be trading at 8x’s book in 10 years absolutely not. Can I see it at 2x’s book and multiples of its current size, absolutely. Based on Fairfax’s history, are they likely to use their shares as cheap currency, if the price is really ahead of itself, probably. A great situation indeed

-

FWIW Citi On Go Digit General Insurance Initiates Buy Call, Target Rs 425 Valuing Company At 8x, FY26 Book On RoE Rising To 15-16% In FY26-27 From Nearly 7% In FY24 Expect Stable 13% Decadal CAGR In Ex-crop Non-life Premiums, Aided By Health & B2B-Oriented Biz If anyone has the note available, please post or PM me. Thanks in advance

-

Awesome and congratulations. I set up my retirement account around this time which was predominantly Berkshire also. Still remember Buffett announcing he was doing buybacks like it was yesterday. Well done with the additions too, done right it makes this a double digit compounder

-

This has been my feeling for a while now. Just not sure whether this line of thinking is all that constructive. I think it is much better to be forward looking, and appreciate the changes that have taken place while preserving a framework that has served them well. Hat’s off to @Viking in this regard.

-

5844.T Kyoto Financial Group

-

Another IRR 20%+ pre-tax? 12.2m shares @ 20.5 in 2018. Say $65 adjusted sale price in 6 years. I think it’s fair to say that this is supportive of the 15% CAGR thesis. Well done.

-

Absolutely, it’s a question of how much of a discount should apply. I think the current discount offers a margin of safety. It’s around 70% of NAV today and if you like the companies that is invested in then it seems a fair price. One that likely does 10-12%+ returns.

-

So does this get delayed now with Eurobank backstopping their shares? All seems a bit cute. I guess you work with the board and raise the offer price or sit tight for 6 months and see where the share price is at. EDIT: or they all get left hanging and delisted as a result of less than 25% in the hands of the public. “Additionally, the board highlighted the minimum dispersal criteria applicable in the case of the main market where the company is listed, as per Regulation 379/2014 of the Cyprus Securities and Exchange Commission, which requires “at least 25 per cent of the shares proposed for listing to be held by the wider public and by at least 300 natural or legal persons”. Difficult to tell but if Logicom does have a minor holding then between the two entities they may have 25% “Based on the information provided in the search results, there is no indication that Logicom has a direct stake in Eurobank. The key relevant details are: 1. Logicom Group is the largest shareholder of Demetra Holdings Plc, owning 29.62% of its shares. Demetra Holdings in turn owns 21.33% of Hellenic Bank's shares, making it the second largest shareholder after Eurobank. 2. Some sources mention that Logicom, along with Demetra Holdings, collectively hold around 25% of Hellenic Bank's shares. This suggests Logicom may have a small direct stake of around 3-4% in Hellenic Bank in addition to its indirect ownership through Demetra.” This would leave only 20% in the “wider public”. In summary: “The board highlighted that if Eurobank's ownership increases substantially, Hellenic Bank may not meet the Cyprus Stock Exchange's minimum free float requirement of 25% of shares being held by at least 300 minority shareholders. This could lead to the bank's shares being suspended from trading or delisted entirely” With 55% of the shareholding Eurobank can pass ordinary resolutions. They need another 20% and they can pass special and extraordinary resolutions I.e. do whatever they want. Here’s hoping that the threat of a delisting and the subsequent illiquidity flushes out that 20%.

-

Funnily enough I actually side with management, they are invested in decent businesses that are keepers.. Happy to see this trade as a quasi ETF with a negative cost banking interest. Silchester makes some good points and creates the right kind of tension to keep management focused. It all seems like a nice problem to have. The upside here is some semblance of a banking NIM, backstopped by the securities of decent companies. I think this will give a return on and of your money but damn it was cheap 12-24 months ago. That would have been an investment with G&D bragging rights. Either way it’s been fun getting to know some of the many great businesses in Kyoto and gives me an excuse to go visit.

-

Don’t think this deserves a thread so will post a summary of their latest shareholdings filing here along with the delta from 31 March 2024. In the doc there is a link to their filings which I ran thru ChatGPT for a translation, may save someone time in the future Kyoto Financial Group Securities Holdings.pdf

-

True, thanks for posting the articles. There is a lot to cover in this space, the insight on ILS was really interesting. Whichever way you cut it this market is not necessarily following the usual playbook. I would stop short of saying it is different this time, but insurance pricing power, like energy prices all feed into inflation, with a commensurate effect on lesser players ability to write. I may be at risk of repeating myself, but like Berkshire, Fairfax now has access to a considerable amount of quantitive and qualitative economic data. I think the path to $100bn (say 3X) of equity is easier, not harder than what they have experienced to date. There really is a critical mass that leads to some pretty great outcomes IMHO.