Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

When it comes to capital allocation, Fairfax has been putting on a clinic over the past 5 years. The interesting thing is the stock is cheap. So investors are getting best-in-class capital allocation for free. For investors, that is like shooting fish in a barrel.

-

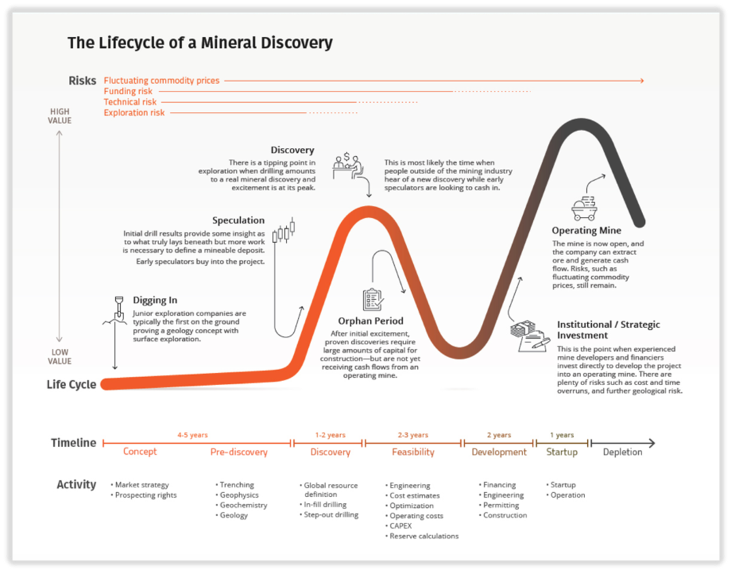

Foran – Using the Venture Capital Playbook in Mining Hat tip to @SafetyinNumbers for the VC / Lassonde Curve insights... Introduction Eldorado Gold completed its acquisition of Foran Mining on April 14, 2026. For Fairfax, this transaction marks the successful monetization of a high-conviction, multi-year investment. The headline return is compelling. But the more instructive story lies in how that return was generated. To understand what happened, it helps to view the investment through two lenses: Venture capital The Lassonde Curve Part I — The Outcome Fairfax initiated its investment in Foran in August 2021 added to the position five additional times, deploying a total of$234 million. At closing (April 14, 2026): Market value: ~$504 million Total gain: ~$270 million Return: ~115% Timeframe: ~3 years (weighted average) This is an exceptional outcome—particularly for a capital-intensive, early-stage mining asset. But focusing solely on the return obscures the more important point: the process that produced it. Part II — Framing the Investment This was not a conventional public equity investment. Foran had two defining characteristics: A venture-like profile (early-stage, capital-intensive, uncertain) Commodity exposure (inherently cyclical) Equally important was Fairfax’s partnership with Pierre Lassonde—the central figure behind the Lassonde Curve and a long-time architect of value creation in the mining industry. Part III — The Lassonde Curve as a Roadmap The Lassonde Curve describes how value typically evolves across a mining project’s lifecycle: Discovery → excitement and rising valuations Feasibility → reality sets in; valuations compress Development → capital intensity peaks; valuations trough Production → cash flow emerges; valuations re-rate The key insight: The most attractive risk-adjusted opportunities often appear in the middle—when uncertainty is highest and investor interest is lowest. This framework provides a roadmap for capital allocation. Understanding the Mining Life Cycle - the Lassonde Curve https://smallcapinvestor.ca/the-lassonde-curve-understanding-the-mining-life-cycle/ Part IV — Entry: The “Orphan Period” Fairfax began building its position in 2021, during the feasibility/development phase: The asset was proven but not yet built Capital requirements were significant Market sentiment was weak This is the “orphan period”: Maximum uncertainty Maximum capital intensity Minimal investor sponsorship Fairfax leaned into this dislocation with a venture-style approach: Built a 22.6% ownership stake (121.9 million shares) Funded the project across multiple rounds Accepted illiquidity and volatility Part V — Acting Like a Venture Capitalist Fairfax’s behavior closely resembled that of a lead venture investor: Provided growth capital through critical stages Absorbed development risk others avoided Positioned for a discrete value inflection In mining, value creation is rarely linear. The Lassonde Curve makes this explicit: a large portion of value is realized late in the development cycle—and often abruptly. Part VI — Exit: Capturing the Re-Rating The acquisition by Eldorado represents a classic inflection point: Major development risks were removed The asset became attractive to a strategic buyer Market value began to reflect underlying economics Rather than waiting for full production, Fairfax exited at the re-rating phase—a textbook outcome. Result: ~$234M invested ~$504M realized ~115% return This aligns precisely with the Lassonde framework: a meaningful share of value is realized before production, once key uncertainties are resolved. Part VII — Rolling Forward: From Asset to Platform The transaction structure is equally important. By received shares in Eldorado: Gains were effectively crystallized (tax-efficiently) Liquidity improved materially Risk profile declined Optionality increased This mirrors a venture investor exiting into a strategic acquirer: From concentrated, high-risk exposure To ownership in a diversified, cash-flowing platform The Bigger Picture Foran is not an isolated case. It fits a broader pattern of successful commodity monetization by Fairfax in recent years: Resolute Forest Products (2022) – Sold at a premium valuation at peak of lumber cycle. Stelco (2024) – Sold at a premium valuation during strong M&A market in NA steel. Orla Mining (partial, 2025) – 25% stake sold at a +250% gain. Foran Mining (2026) – acquired by Eldorado Gold Bottom Line Viewed through the Lassonde Curve, this was a highly disciplined capital allocation exercise: Entered during peak pessimism Funded through the most capital-intensive phase Exited at the point of value recognition The involvement of Pierre Lassonde is not incidental—it reinforces how closely the investment followed the framework he helped formalize. This was not a passive investment in a mining company. It was: A venture-style deployment of capital Executed alongside experienced operators Guided by a clear roadmap of value creation Carried through with patience and discipline Foran is another data point supporting a couple of broader conclusions: Within its investment management business, Fairfax has quietly built another differentiated capability—operating at the intersection of venture capital, commodities, and long-term capital allocation. More broadly, when it comes to capital allocation, Fairfax has been executing exceptionally well for more than 5 years now. Foran is just the latest example.

-

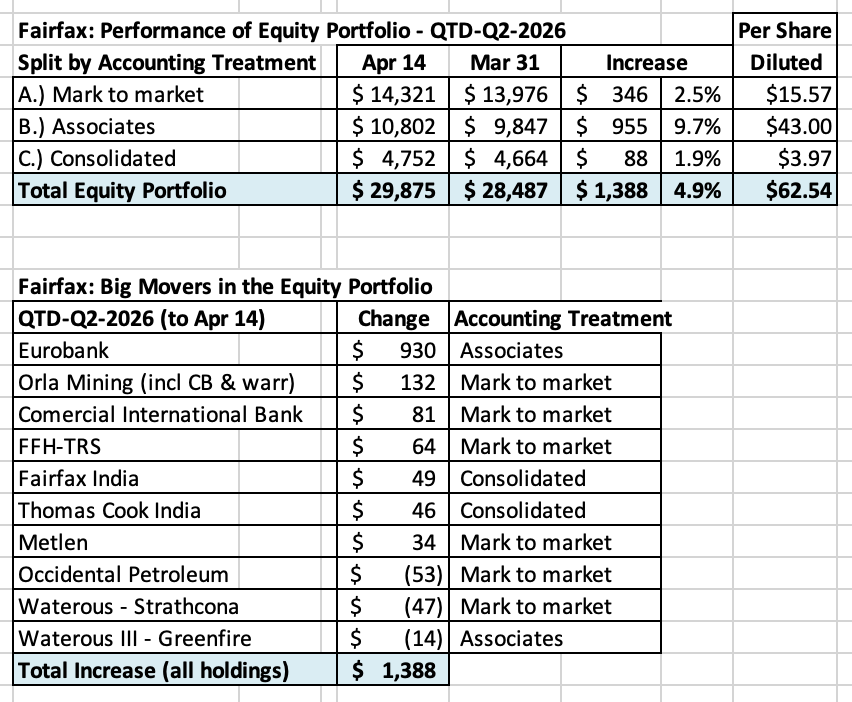

How are Fairfax's equity holdings performing QTD-Q2 2026 (two weeks in to April 14)? The holdings I track are up about $1.4B or $63/share. Yes, it is only 2 weeks into the quarter. And lots will change in the coming weeks and months. Regardless, that is a significant increase. The driver, not surprisingly, is Eurobank. But lots of holdings are up nicely. The holdings that are down are, not surprisingly, the oil holdings. These holdings are down modestly after posting big gains in Q1.

-

Fairfax’s Annual General Meeting - A Final Summary It will be great to see everyone at the AGM next week. Below is an updated summary that I post each year. Of note, there are still spots available to the dinner on Wednesday night (keynote speaker: David Thomas). Tickets: https://www.eventbrite.com/e/17th-annual-cobf-fairfax-financial-shareholder-charity-dinner-tickets-1982885759685?aff=oddtdtcreator Introduction Fairfax’s annual general meeting (AGM) will be held on April 16, 2026 in Toronto, Ontario. I’ve attended the past three meetings. I initially went to better understand the business. Now I go as just as much to see and spend time with friends. Fairfax has a first-class group of shareholders - wicked smart and super nice. The “super nice” part has been the bigger surprise for me. One of the interesting things I have learned from attending the AGM (and the various activities during the week) is I am not a freak. I have been able to meet a large group of people who are kind of wired just like me - people who love the art/craft of investing. This note outlines what the AGM offers, where the real value lies, and how to think about whether it’s worth attending. Where to Find Information on the 2026 Event? The AGM is available both in person and virtual via live stream. Fairfax (including details of how to attend virtually): https://www.fairfax.ca/press-releases/fairfax-announces-hybrid-annual-shareholders-meeting-details-april-6-2026/ The Corner of Berkshire and Fairfax: https://thecobf.com/forum/topic/21593-2026-annual-shareholders-meeting/#findComment-652738 Fairfax India (including details of how to attend virtually): https://www.fairfaxindia.ca/press-releases/fairfax-india-announces-hybrid-annual-shareholders-meeting-details-april-6-2026/ The Meeting Itself At its core, the AGM offers direct access to management. You’ll hear from: Prem Watsa (CEO) and Peter Clarke (COO) Leaders across the P&C insurance subsidiaries Executives from key equity holdings The format is straightforward: A brief formal business meeting A presentation by Prem An extended Q&A session (typically ~2 hours) The Q&A is useful. It is candid, wide-ranging, and often reveals how management is actually thinking—not just what is written in reports. But the real value emerges over time. Attend multiple years and you start to see patterns: How management thinks about risk How capital allocation evolves Whether narrative and results align That kind of pattern recognition doesn’t come from reading filings alone. Fairfax’s 2025 AGM presentation https://www.fairfax.ca/wp-content/uploads/2025/04/Fairfax_AGM_2025.pdf Scuttlebutt: A Differentiated Information Edge Arrive early. Stay late. The hour before the meeting is one of the most valuable parts of the day. Senior executives from across Fairfax’s global operations (insurance and equities) are available for informal conversation. This allows you to: Conduct real scuttlebutt Ask direct, unscripted questions Cross-check what you’ve read vs. what you hear At the end of the meeting, food and beverages are served for lunch. Lots of people mingle afterwards for an hour or two. Conversations continue. For a serious investor, this is a genuine edge—qualitative, nuanced, and hard to replicate. Fairfax India: Worth the Extra Day The Fairfax India AGM (held the day before) is smaller but equally valuable. It follows a similar format to the Fairfax AGM (go early… stay late). Hosted by Ben Watsa (Chairman) and Gopal Soundarajan (CEO), it provides: Direct access to management of underlying holdings A more focused, intimate setting High-quality insight into the stock portfolio If you’re making the trip, it’s worth attending both. Fairfax India’s 2025 AGM presentation https://www.fairfaxindia.ca/wp-content/uploads/2025/04/Fairfax_India_AGM_2025.pdf The Shareholder Base One of Fairfax’s underappreciated assets is its shareholders. They tend to be: Long-term oriented Curious and engaged Willing to share ideas Many travel from across Canada and internationally (as far away as Australia). Over time, the AGM becomes less about the formal meeting and more about the relationships built around it. A number of informal, investor-organized events take place throughout the week. This is where much of the real interaction happens. The Broader “Fairfax Week” The AGM is just one piece of a larger ecosystem. During the week, there are: Informal meetups Structured investor events Ticketed dinners From a cost perspective, these are minor relative to the overall trip. The real question is whether the time is worth it. In my experience, it has been—consistently. Norm (one of those first-class people I mentioned earlier) puts together a summary each year: https://stingyinvestor.com/FairfaxWeek2026.html A Practical Note On the Wednesday before the AGM, there are typically two dinners: A Fairfax-hosted, invite-only event The CoBF shareholder charity dinner (open, ticketed, usually sold out) Tickets: https://2026_COBF-FFH_Shareholder_Dinner.eventbrite.com Some years they’re held at the same hotel. Don’t mix them up. Summary: Why Attend? Fairfax’s AGM is not just a corporate event—it is an information ecosystem. For investors, it offers three clear advantages: Direct Access to Management Extended Q&A and repeated exposure build a deeper understanding of leadership, culture and strategy. Scuttlebutt and Qualitative Insight Informal interactions with executives provide valuable information. High-Quality Investor Network The shareholder base itself is a valuable asset—serious, intellectually engaged, long-term oriented, and collaborative. These benefits compound. The more you attend, the more valuable it becomes. Final Thoughts It has been another wonderful year for Fairfax and their shareholders. Being able to celebrate at the AGM with friends what has been unfolding at Fairfax these past couple of years has been priceless. And my view continues to be that Fairfax still has many good years in front of it - the company looks to me like it is just entering its prime. If you’re considering attending the AGM, go. Engage. Ask questions. Introduce yourself. The investment insight is valuable. The relationships are what bring you back. Looking back, deciding to attend was one of the better decisions I’ve made in recent years.

-

Iran is adding to their list of demands (release of blocked assets). Every week the straight remains closed their position strengthens. What is Trump's analysis and assessment of the situation? Wisdom from Buffett: "If you've been in the poker game for 30 minutes and you don't know who the patsy is, you're the patsy."

-

+1

-

Good discussion of where the war with Iran is at.

-

Is the ceasefire 'agreement' unravelling? Oh, wait... nothing was actually put down on paper. What could possibly go wrong?

-

Looks like a lot of wood left to chop... The fact that the two sides have reached a ceasefire, will be negotiating shortly and the straight is opening is very positive.

-

This deal largely flips Fairfax’s exposure in Foran from copper to gold (El Dorado is 85% gold and 15% copper). Fairfax obviously was happy with the transaction. This deal meaningfully increases Fairfax’s exposure to gold. Orla is their 4th largest equity holding $1.3B). They will soon add El Dorado ($500M). This would put Fairfax’s exposure to gold at about $1.8B, or 6.3% of the total equity portfolio. As @SafetyinNumbers mentioned, El Dorado will provide much better liquidity (likely making it easier for Fairfax to exit the investment in the future).

-

Well, if shipping is able to get back to normal in the Straight of Hormuz in the coming days and weeks that will be very good news for the global economy. Here is the really interesting part: both sides are 100% convinced they have won! Has that ever happened in a war of this size and magnitude before? Now that is a real mind bender. It will be very interesting to see how the next two weeks play out. For the other perspective (in terms of what was agreed to to get the cease fire), below is what Iran is saying:

-

What is the problem Iran is trying to solve? (When I say Iran, I mean the IRGC). They explained what they want - people need to re-read the list. It is frightening. Yes, Iran is getting bombed back to the stone age… but it doesn’t seem to matter. And that is likely because they know the noose is tightening around the neck of the global economy - and it will become intolerably tight in a couple of weeks. Fanatics aren’t rational - I don’t know why people expect them to be. Fanatics also welcome pain/sacrifice (including their own death and the death of their family members) - as a necessary price to pay to achieve their objectives. The West is hopelessly naive in grasping this reality - it is incomprehensible so it is discarded as a helpful construct to understand the situation. Iran would be idiots to stop the war today when they are weeks away from possibly getting much of what they want - they are positioning for the next 50 years. What is another couple weeks or months? Think of how their sacrifices today will be celebrated by future generations (sounds appealing to a fanatic). The US has a very different problem. Up until now, they have been largely insulated from the economic consequences of the war. And financial markets have given Trump largely a free pass. Trump has been telling everyone since the war started that it will be over in weeks. Most Americans are angry it started. Time is NOT the friend of the US. And it appears they have squandered 5 weeks already (they have allowed Iran to set and tighten the noose over the straight). Much of the rest of the world is in deep shit. This is where the pain will be increasingly felt. As the pain gets intolerable, Iran will start picking these countries off one by one (cutting side deals) - which is what we have been seeing. Those countries will give Iran whatever it wants. Remember - life is energy. Again, what a crazy set up.

-

As the war continues, it is impacting the politics of each of the Gulf Countries. Some countries, like Bahrain, could see significant unrest which could lead to regime change (with a fundamentalist pro-Iran government taking control). No, this is not imminent. But the fault lines are there and an earthquake is happening. These are the unintended consequences that often result from war (who knew? everyone will ask). Iran understands these internal political risks each country in the Gulf is dealing with and will fully exploit them. The middle east is a shit storm at the best of times. Iran is praying that this turns into a religious war. Jews against Muslims. Christians against Muslims. Shia against Sunni. Simmering religious/historical regional hatreds + escalating war = potential powder keg. In the West we look at this war in a very narrow way: got to deal with the ‘nuclear’ problem. Forces are being unleashed that threaten to remake the middle east. And what emerges might be much worse than what existed 5 weeks ago. Yes, unintended consequences can be a bitch. There were good reasons past administrations did not directly attack Iran. More importantly, the milk has been spilt. Where do we go from here? Both sides continue to think they are winning - as a result they are getting more entrenched with their demands. Part of the problem is they are playing two entirely different games (with completely different objectives and time frames). The next 2 weeks could prove decisive. Do we see escalation (full blown regional war with boots on the ground) with regime change becoming the new stated objective. Or do we see deescalation? Crazy times.

-

@ourkid8, to be clear, Iran coming out of this war in a much stronger strategic position would be a catastrophe for the region and the world. My assessment of what is going on with the war is simply me calling balls and strikes as I see the pitches coming in (that ‘be rational’ thing).

-

It’s like a person who kicks their best friend in the nuts. Then calls him out in front of everyone. And then - without talking to the friend first - walks into a bar and starts a bar fight. And then when it goes badly blames the whole mess on his friend. That is no way to run a country. You can’t make this stuff up. I keep saying it: There are parts of Trump that I like. There are parts of Trump that are an unmitigated disaster. The ‘disaster’ is swallowing the ‘good.’ This is becoming more and more apparent…

-

The US has legitimate grievances when it comes to NATO. One of them is spending on military. This specific complaint is (finally) being addressed. There are parts of Donald Trump’s leadership that I agree with. But there are other parts of his leadership that are unmitigated disaster. For the US. And the West. Actions have consequences. Do stupid/destructive things - really bad shit happens. That is what we are seeing more and more with Trump and his policies. The good that he is doing is being swallowed up by the bad. @cubsfan, sorry, but ‘the US is a victim’ narrative is getting really stale. More and more, Trump (and his act/schtick/policies) is creating the exact problems that he is railing against. It is becoming more and more apparent to the rest of the world - and the rest of the world is adjusting. Here is what Charlie Munger had to say about developing a victim mindset (that Donald Trump is championing): "Whenever you think that some situation or some person is ruining your life, [think that] it’s actually you who are ruining your life. It’s such a simple idea. Feeling like a victim is a perfectly disastrous way to go through life. If you just take the attitude that, however bad it is in anyway, it’s always your fault and you just fix it as best you can – the so-called ‘iron prescription’ – I think that really works... Well you can say that’s waggery, but I suggest that every time you find you’re drifting into self-pity, I don’t care what the cause, your child could be dying of cancer, self-pity is not going to improve the situation… It’s a ridiculous way to behave, and when you avoid it you get a great advantage over everybody else, almost everybody else, because self-pity is a standard condition and yet you can train yourself out of it." ————— A consistent message I have said to my 3 kids for years now is if you life is not going the way you want it to, start by looking in the mirror - don’t start by looking to blame others. Most important, don’t develop a victim mindset.

-

Iran is playing the long game. The US is playing the ‘two or three’ week game. Time is Iran’s friend - in a massive way. And with each passing week that the current situation remains as is, the pain to the global economy will continie to build. At some point (when physical shortages in oil, LGG, refined products, fertilizers start to really bite in terms of much higher prices) the stock market is going to have its Wile E Coyote moment. Probably mid to late April (if we continue down this path). Guess what Trump will do then? Everyone knows the stock market is his most important barmeter of his own performance. (To deflect criticism, he will need to manufacture an even bigger problem - that should scare the hell out of everyone.)

-

Iran currently controls the Straight of Hormuz. This gives the IRGC enormous political and economic power. In an exercise of their growing power, they appear to ready to 'allow' oil from Iraq to flow out of the Gulf. Why would the IRGC do this? To expand their power/influence beyond Iran and into Iraq. The war in the Persian Gulf is morphing. With each passing week, the power of the US is diminishing. And the power of Iran is growing. Iraq is perhaps the latest example. There is a scenario where Iran emerges from the current conflict the dominant power in the Middle East. I am not sure this is what the US/Israeli's intended. (The chances of this outcome happening are growing with each passing week...) The problem with wars like this is they often tend to go in unexpected directions. It appears the US/Israeli's grossly underestimated Iran. Especially the shift in Iran's strategy/tactics over the past 8 months (to more hard line). The US cemented Iran's shift to a hard line approach when they took out the senior leadership (who were the moderates) on day one of the way - that strike was, with hindsight, a gift to the hardliners in Iran - who are now fully in control. The US got regime change in Iran all right... from moderates to hard liners. Yes, if the old Iran, run by moderates, did what they did... guess what a new Iran, run by hard liners, will be doing moving forward... And what the hard-liners have learned over the past 5 weeks is their strategy (escalation - close the straight and inflict damage on the Arab neighbours) is working fabulously well (all things considered). The result, is the US/Israeli's are dealing with a new paradigm in the middle east - an Iran that has enormous leverage that they are now willing to use for the first time ever. The is not the same Iran (IRGC) that existed 8 months ago. We are in uncharted territory. That has important implications for the global economy. So the US has a choice... escalate and hope that they get lucky and the war flips back in their favour. Or continue to watch Iran's power grow greater with each passing week. Of course, we are early days into this conflict (5 weeks). And things are very fluid - subject to change day to day and week to week. So it is impossible to know exactly how things will look in another year or so. But it is important to be open minded to the different potential outcomes.

-

+1

-

Good current events podcast - if you have some time to kill and want a big picture perspective (politics, economics, investing etc).

-

Well done. The past month’s volatility has been a traders dream.

-

Best summary of speech that I have seen: “Can I get my money back?” What did we learn? This war is far from being over. Can anyone say “boots on the ground?” Trump just explained the war to the American people. Based on what he said, I think the chances of escalation have actually increased. I thought the purpose of the speech tonight was to do the opposite.

-

I am not sure what all the outrage is about the fee structure at Fairfax India. It was communicated to shareholders when the company was created. And it has remained the same since then. If an investor doesn't like the fee structure there is a really simple solution: don't invest in the company. There are so many great opportunities out there why waste time and energy yelling and shaking your fist at the clouds? Investors who owned Fairfax India and were unhappy with management (pick the reason) all had a wonderful opportunity to exit their position in 2025 when the stock traded above $19 for over a month. Make a decision. Live your best life. The management team at Fairfax India is very good. The proof is the return they have generated on all the positions that have been monetized since the company was created. Many positions have been monetized over the years so can be used as one performance measure. Another performance measure? Look at the biggest holding (by far) BIAL. Of course, the crown jewel of Fairfax India is BIAL. Fairfax India has done an outstanding job of managing and growing their ownership of this amazing asset over the past 7 years. This asset has a carrying value that is well below it fair value. Yes, the IPO of Anchorage has been continuously delayed over the past 4 years (welcome to doing business in India). But BIAL has been growing nicely in value every year - so no IPO has actually worked out well for long term shareholders. I am not saying Fairfax India is perfect (no company is). The management team at Fairfax India are exceptional. The structure of the company is what it is.

-

Master Tracker & Quarterly Change in Market Value – Q1-2026 A Warning When looking at Fairfax’s equity holdings, what ultimately matters is the underlying business performance of those holdings over time – not the quarter-to-quarter change in market value. Short term (quarterly) changes in market value are inherently volatile and should therefore be viewed with an appropriate degree of skepticism. So why track quarterly changes at all? Because they are interesting and because they can provide early insight into one of Fairfax’s largest income streams—investment gains (and losses)—ahead of reported earnings. Importantly, over time (like a couple of years), changes in market value of the equity holdings should roughly match changes in intrinsic business value. Q1-2026 Summary Portfolio decrease: ~$486M (pre-tax), or 1.7%. Quarter-end equity value: ~$28.5 billion Fairfax’s equity portfolio performed very well over the first 2 months of 2026 (up more than $1 billion). War in the Persian Gulf broke out at the beginning of Match. This hit Fairfax’s equity holdings hard and the big gains reversed to a modest loss at March 31. Portfolio Composition by Accounting Treatment Mark to market = 49% Associate and consolidated = 51% Total Return by Accounting Treatment The mark to market bucket finished the quarter flat. The decline was centered in the Associate and Consolidated holdings. As a result, the impact on Q1 reported results (investments gains/losses) will be minimal. Major Movers – Q4 Strongest contributors: Fairfax’s various oil holdings (Strathcona, Greenfire and Occidental Pertoleum) finished the quarter up $390 million. Orla Mining (gold) was also up nicely. Laggards: Fairfax total return swap position was the biggest decliner, down $375 million, reflecting weakness in Fairfax’s share price. The decline in Fairfax’s share price in the quarter (11%) was similar to the decline experienced by many P/C insurance peers (Markel was down 11% and Intact Financial was down 12%). Indian stocks sold off pretty hard in the quarter, which impacted Thomas Cook India. Currency was also a headwind (strong US$). Excess of Fair Value Over Carrying Value (FV – CV) Estimate of excess of FV over CV at December 31, 2025: ~ $2.7 billion ~ $122 per diluted share (pre-tax) For context, this figure was ~ $3.1 billion at December 31, 2025. Despite the small decline in Q1, FV – CV for non-insurance associate and consolidated holdings has materially increased in size in recent years. It represents real economic value that is not captured in EPS or book value—clear evidence that accounting metrics understate Fairfax’s true economic performance. Note: Carrying values are as of Dec-31-2025, so FV-CV may be slightly overstated. Additional Notes on Tracker: Updated to include annual, interim and 13F reports and news releases FFH-TRS included at notional value Convertibles, warrants and debentures included in the mark to market bucket Digit (India) excluded (some of which is market to market) – shares down modestly in Q1 Currency was a modest headwind in Q1 – impact on reported results is complex (net of hedging) The tracker is not an exact match of Fairfax’s actual equity holdings. It is useful only as a rough guide (both for holdings and change in value).

-

+1