Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Luca I like all three investments. See below for comments. 1.) BDT has been an outstanding long term investment for Fairfax. “We continue to invest with Byron Trott through various BDT Capital Funds. Since 2009, we have invested $978 million, have received $979 million in distributions and still have investments with a year-end market value of $683 million. Byron and his team have generated fantastic long-term returns for Fairfax, and we very much look forward to our continued partnership.” 2.) ShawKwei looks like it has been a solid long term performer. The fact Fairfax is adding new capital suggests they like the prospects. “Since 2008 we have invested with founder Kyle Shaw and his private equity firm ShawKwei & Partners. ShawKwei takes significant stakes in middle-market industrial, manufacturing and service companies across Asia, partnering with management to improve their businesses. We have invested $536 million in two funds (with a commitment to invest an additional $64 million), have received cash distributions of $217 million and have a remaining value of $504 million at year-end. The returns to date are primarily from our investment in the 2010 vintage fund, which, though decreasing 8.8% in value in 2023, has generated a 12% compound annual return since 2010. The 2017 vintage fund, which has drawn about 84% of committed capital to date, increased 23.1% in value in 2023 but has a compound annual return of 3.5% since inception. We expect Kyle to make higher returns on monetization of his major assets.” 2.) Grivalia Properties gets an incomplete from me today. It is a bet on the jockey play. George Chryssikos has had the Midas touch for Fairfax in Greece - making them +$1 billion so far. I am inclined to give Fairfax the benefit of the doubt on this one - my guess is it works out ok. We should know much more in 2024 as more resorts come on line. “Grivalia Hospitality, under George Chryssikos, had a strong year of execution as two assets, including its largest, opened for business. The One & Only resort in Athens is a flagship in ultra-luxury hospitality and we are the proud owners. If you haven’t booked your summer vacation yet – you know what to do! 2024 will see one additional asset come into operation – which will take the operating portfolio to five. These include Amanzoe in Porto Heli, ON Residence in Thessaloniki, Avant Mar in Paros, One & Only and 91 Athens Riviera in Athens. Focus now turns to operational and service excellence for these resorts with Greece forecast to receive a record number of tourists in 2024. George has another five high end hotels in development over the next few years. George has an outstanding track record in real estate and as I said last year, he has already made us $1 billion! We expect George to repeat that accomplishment with Grivalia Hospitality over time! At year end we carried Grivalia at €513 million for our 85% stake.”

-

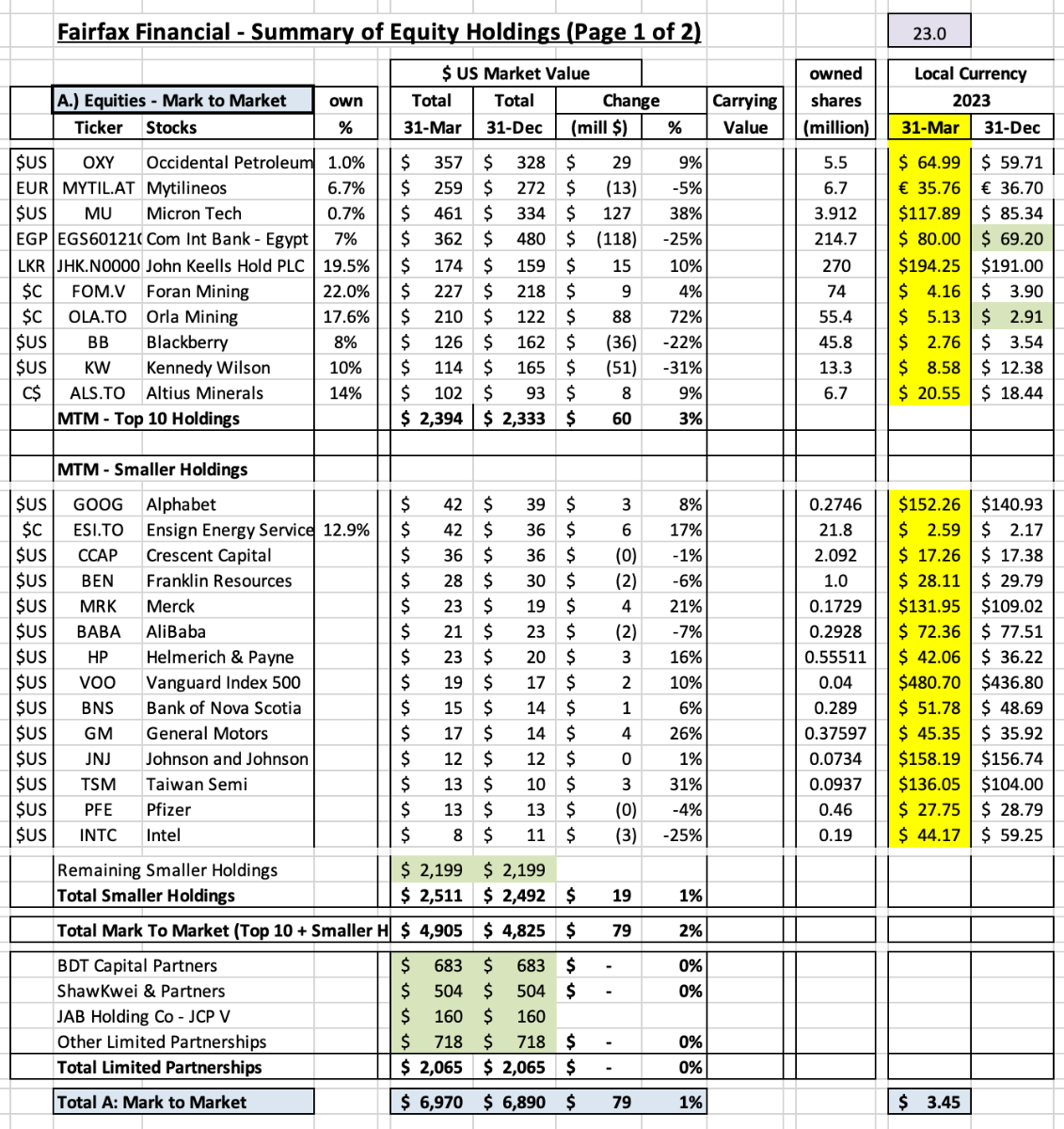

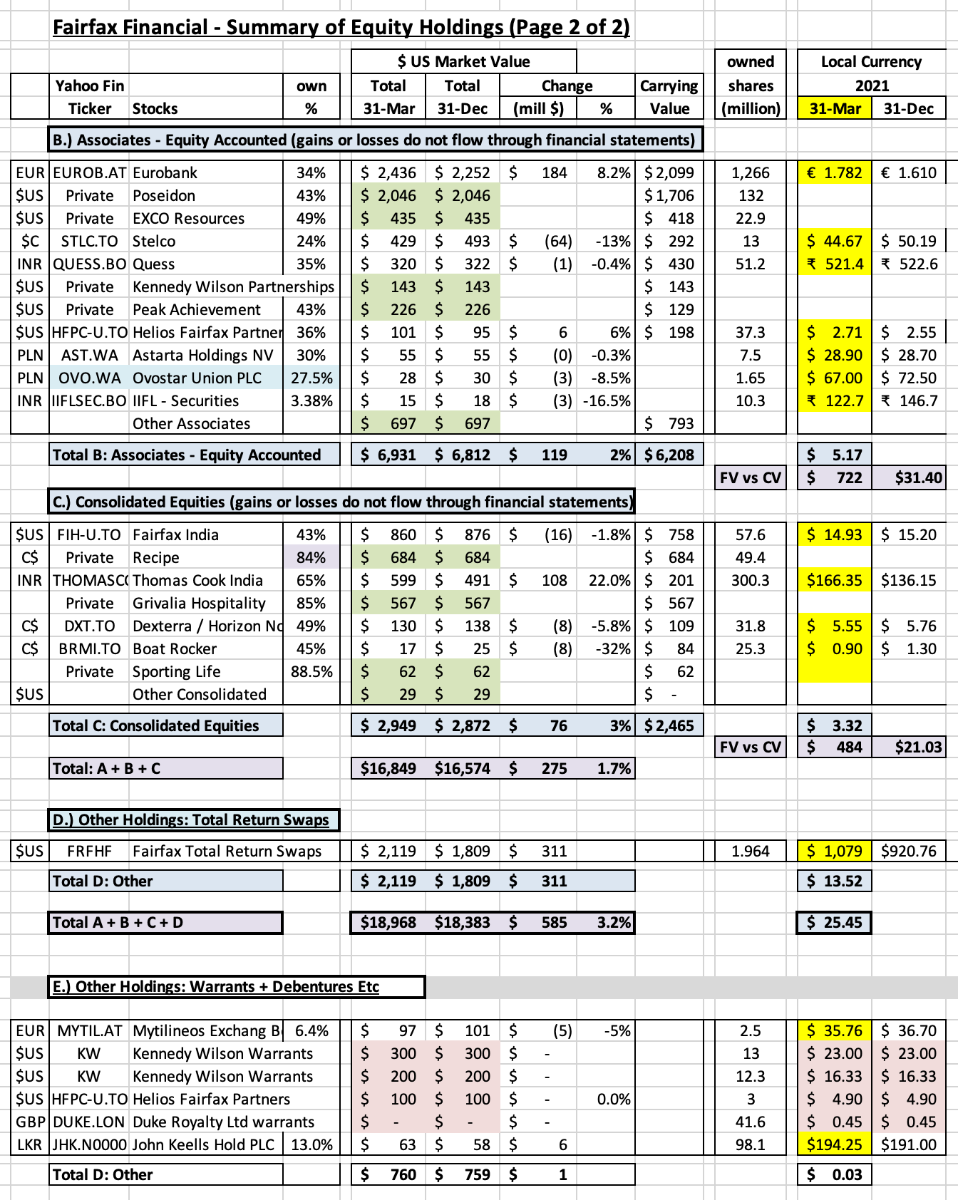

Below is a chart updating Fairfax's top equity holdings to March 31, 2024. The total is about $19b. What stands out? - Concentrated. - International. - Cyclical. - Most holdings are well managed with solid prospects. That is a big, big change from what the portfolio looked like back in 2017. 6 years of hard work (fixing problems) and making good decisions (with new investments) is really starting to shine through. - Overall quality continues to improve. Higher quality means higher future earnings. We are seeing this show up in the different growing income streams at Fairfax. Total return of 15% = $2.85b. This looks attainable for Fairfax in 2024. Please note, my definition of 'quality' is very loose: will the holding be able to deliver Fairfax a return of 15% per year? And lumpy is ok. We know Fairfax's fixed income portfolio is locked and loaded for the next 4 years. If Fairfax's equity portfolio is able to start returning 15%... well guess what that means for Fairfax's total return on investments? Yes, a big number. 7.5% is probably a good base number to use for the next couple of years. Fairfax is also much more levered to investments (in terms of total earnings) than most P/C insurers. So earnings monster returns on its investment portfolio is a big deal.

-

@Hamburg Investor i don’t have a lot of insight as to why P/C insurers trade at the multiples they do compared to other industries and the market as a whole. P/C insurance is a pretty small sector and i don’t think it is followed all that closely by most investors. But i think i can spot cheap. Fairfax is trading at about 1.1 x BV (est March 31, 2024) or at a PE of 6.5 x (est 2024 earnings). Of all the valuation measures, P/BV appears to be the most important. Multiple expansion has been happening for Fairfax over the past couple of years - investors are warming to the Fairfax story. If Fairfax continues to deliver solid results in 2024 and 2025 my guess is we will see multiple expansion continue.

-

Telecom in Canada is in a price war. Shaw’s sale to Rogers, forcing Freedom Mobile’s sale to Quebecor, appears to have unleashed a sprint for market share. Canada is the land of oligopolies. The kind that tend to play nicely in the sand box. So investing in Canada’s oligopolies has generally been pretty good for investors. How times have changed. BCE is trading today at C$44.00, where it was trading back in 2013. Its dividend yield is 8.5%. Telus is trading at C$21.20, where it was trading back in late 2014. Its dividend yield is 7%. Bottom line, telecom stocks are getting killed. Again. They all got taken out behind the woodshed late last year. I don’t follow the Canadian telecom industry all that closely. Although i will say my telecom bill (cell, internet and TV) has come down materially over the past year. The current environment is great for consumers - not so great for shareholders. Is the current competitive dynamic the new normal for Canadian telecom companies? Or will they become rational actors again? Has something structurally changed in this industry that means profitability moving forward will be permanently lower? Or is the current price war just a temporary bout of insanity among the major players? I bought more BCE today and i added to my Telus position last week. Do board members have favourites in the sector? Rogers? Quebecor?

-

How is the Fed going to cut rates with inflation over 3%?

Viking replied to ratiman's topic in General Discussion

The problem is we have been taught to believe that it is the Fed’s job to fight inflation. If the Fed throws in the towel on fighting inflation - what happens next? Brave new world? We KNOW the politicians (of all parties) will not do anything - until catastrophe hits. It really is an interesting set up. i think we are learning that fiscal policy trumps monetary policy in todays environment when it comes to inflation. And those in charge of fiscal policy are going to deny it to their dying breath. That suggests to me that inflation will probably remain elevated. Especially if central banks start to ease (that will stimulate interest rate sensitive sectors of the economy like housing). The bond market just might be the thing to watch moving forward. After all, bond investors have the most to lose if inflation gets out of control. And my assumption is they are not idiots - but i really have no idea. -

@This2ShallPass , i come at it in a very different way. of course, there is no ‘right way’. How should we define quality when looking at a holding? Here are a few things that come to mind: How good is the management team? Capital allocation? Is the company profitable? Is growth funded via retained earnings? What does its balance sheet look like? Leverage? Other considerations (geography, political/economic situation etc)? What has Fairfax’s return been since purchase? What are the future prospects of the business? Fairfax’s return potential looking forward? What are the returns the equity portfolio is delivering over time? Fairfax has talked about having a 15% target/hurdle rate for its equity investments. The equity portfolio is about $19 billion. A 15% return = $2.85 billion. Can Fairfax hit this target in 2024? I think they can. They actually could exceed it. Dividends = $170 million Share of profit of associates = $1.03 billion Other / Non-insurance consolidated holdings = $150 million Mark to market investment gains = $1 billion Realized one-time investment gains = $300 million Change in excess of fair value over carrying value for associate and consolidated holdings = $200 million Total = $2.85 billion Of course, these 6 buckets do not capture the total increase in the intrinsic value of all equity holdings each year. And realized one-time investment gains might come from insurance holdings (like a Digit IPO). So my estimates above might be off a little. Bottom line, it looks like Fairfax’s 15% return target for its basket of equity holdings is roughly attainable in 2024. My guess is this comes as a surprise for most Fairfax shareholders. What happened? The answer gets back to my ‘higher quality’ thesis for the equity holdings. Fairfax has been working its ass off the past 5 to 6 years improving the overall quality of its basket of equity holdings. It takes years for that work to show up in reported results. And that is what we are now seeing. We are learning what the true earnings power of the equity portfolio is today. The interesting thing is my guess is Fairfax is not done in its move up the quality ladder with its collection of holdings. This bodes well for higher future returns. Total Return on Investment Portfolio Fixed income yield = 4.7% Equity return = 15% Total return on investment portfolio = 7.4% Fairfax’s fixed income portfolio looks locked and loaded to deliver an average yield of +4.5% for the next 3 years. The equity portfolio looks poised to deliver a return of around 15%. This suggests Fairfax may be able to deliver a total return on the investment portfolio of around 7.4% the next couple of years. My guess is most investors think a return of 7.4% is unsustainably high. I don’t think it is - at least for the next 2 or 3 years. Further out? That will depend on the capital allocation decisions. Fairfax has been hitting the ball out of the park for the past 5 or 6 years. That is the main reason why they are poised to earn 7.4% in 2024. If they continue to make good capital allocation decisions i don’t see why total return on the investment portfolio can’t stay in the 7.5% range for the next 5 years. Is that baked into the expectations of investors today? No, i don’t think it is.

-

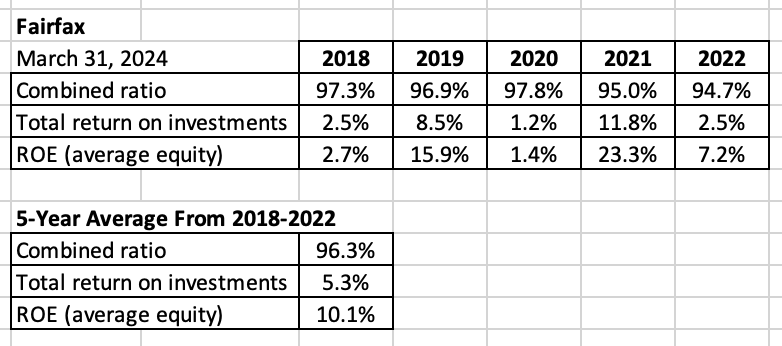

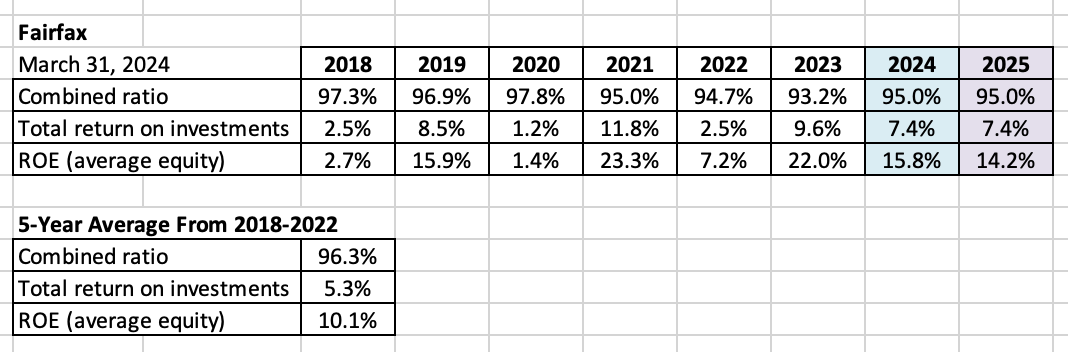

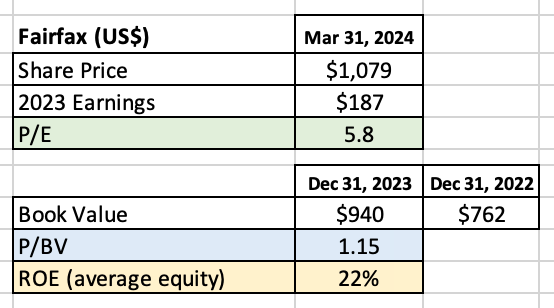

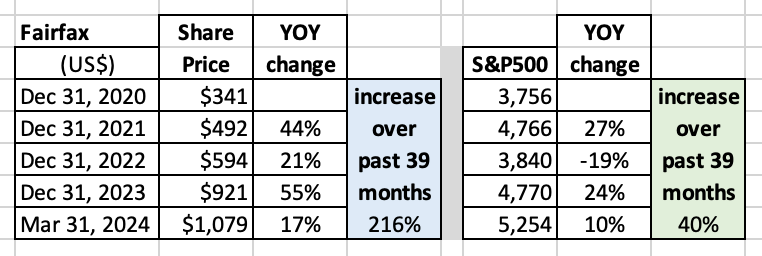

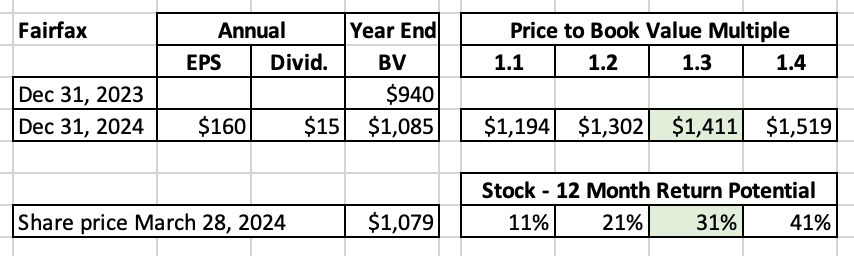

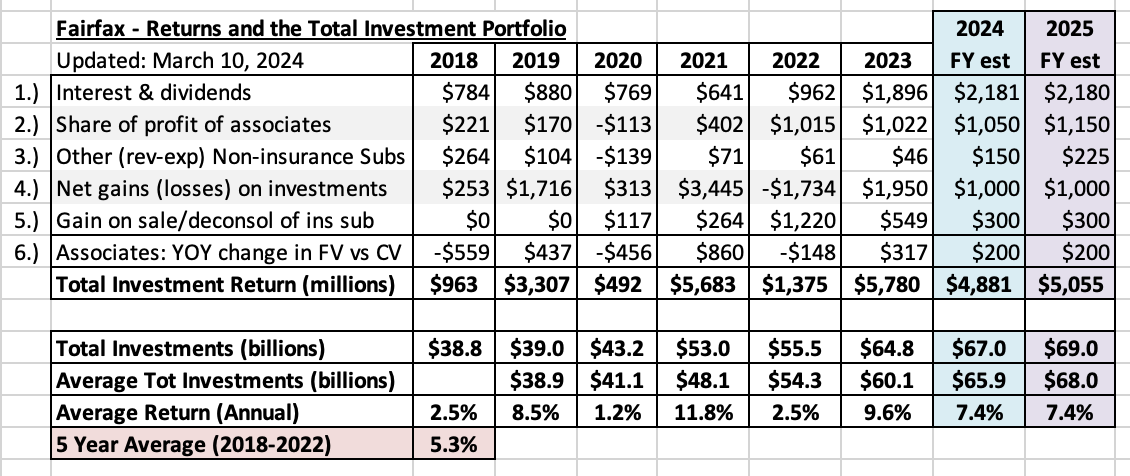

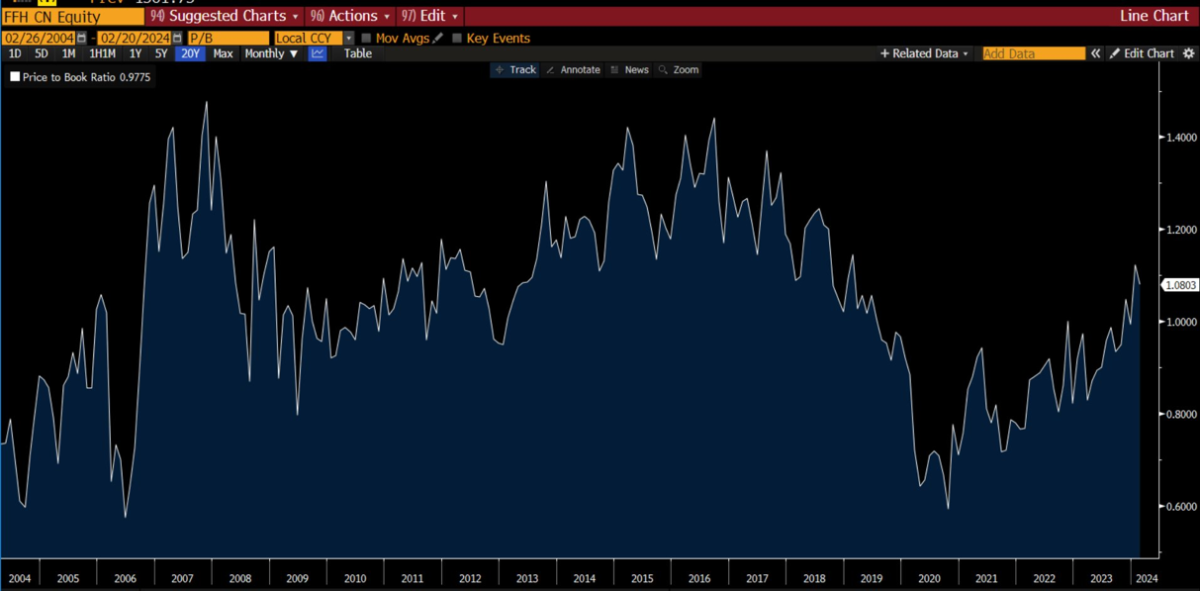

How to value Fairfax - a shorthand method There is usually no one ‘right way’ to value a company. Using multiple methods can provide for a more robust analysis. Weighting the different methods can also be helpful. For the past 3 years i have been valuing Fairfax primarily through the lens of a turnaround. What about today? Much has changed at Fairfax over the past 3 years. Most importantly, the company stopped doing the things that were causing its underperformance. It has also fixed most of the problems that were residing in its equity portfolio. The management team/Hamblin Watsa has been putting on a clinic in capital allocation. The insurance business has been quietly chugging along. Weave it all together and Fairfax’s two businesses - insurance and investment management - are now performing at a high level and delivering record earnings. And they both look very well positioned for the future. Bottom line, the turnaround at Fairfax is over. Mission accomplished. Truth be told, the turnaround at Fairfax was probably completed a year ago. So what is the best way to value Fairfax today? I think we can start to value Fairfax not primarily as a turnaround but more like a normal P/C insurance company. Historical results are starting to become useful for investors as an indicator of future performance. The picture of the earnings power of ‘new Fairfax’ is slowly coming into focus for investors. What are the key metrics we should be looking at to value a P/C insurance company? The two most important metrics are: Return on equity (ROE) Price to book value (P/BV) ROE tells us how the company is performing. P/BV tells us how Mr. Market is valuing that performance. Looked at together, these two metrics can provide us with a great deal of insight into how Mr. Market is currently thinking about a company and how it is being valued. We can unpack ROE. ROE can be looked at as the product of two components: Combined ratio (CR) Total return on the investment portfolio (TRIP) In this post we will explore Fairfax’s CR, TRIP, ROE and P/BV to see what they tell us about how the company’s stock is currently being valued by Mr. Market. ———— In 2019, Woodlock House Family Capital wrote an article on Fairfax that i have always liked. At the time, it provided a fair assessment of the company. It also provided a short and concise way to value the company using estimates of the combined ratio, total return on investments, ROE and P/BV. And i love ‘the horse story’ as a useful mental model when it comes to both life and investing. https://www.woodlockhousefamilycapital.com/post/the-horse-story ————— So let’s apply the simple framework outlined by Woodlock and see what we can learn about Fairfax’s valuation today. First, let’s start by looking at the past. How did Fairfax do from 2018 to 2022 (average over the 5 year period) CR = 96.3% TRIP = 5.3% That combination of results delivered an average ROE of 10.1%. The ROE was very volatile. This is because investment gains (losses) was the biggest component of Fairfax’s various income streams from 2018 to 2022 (on average). We had bear markets in stocks in 2018, 2020 and 2022 and an epic bear market in bonds in 2022. Of interest, despite the crazy volatility in financial markets Fairfax still delivered an average ROE of 10.1% - this performance is likely much better than most investors would have guessed. How did Fairfax do in 2023? CR = 93.2% TRIP = 9.6% That combination of results delivered an ROE of 22% Fairfax’s performance in 2023 (CR, TRIP and ROE) was a significant improvement from the company’s 5-years average (2018-2022). Was this outperformance a simply the result of a bunch of one-time events? Or is something else going on? Are these much better results sustainable? To answer these questions, let’s review what happened in 2023 at a very top-line level. Insurance operations: The hard market in insurance that started in late 2019 continued to be a tailwind. The quality of Fairfax’s collection of insurance companies continued to improve. Investment management: The yield of the fixed income portfolio increased from an average of 2.5% from 2018-2022 to 4.4% in 2023. This is massive increase in yield. In 2023, Fairfax increased the average duration of its $45 billion fixed income portfolio from 1.6 to more than 3 years. This locks in the much higher yield for the next 3 or 4 years. Interest income has exploded higher and the higher amount is sustainable. At $2.4 billion, Fairfax’s largest equity holding is Eurobank. The Greek economy is now one of Europe’s top performing economies. Eurobank has increased substantially in value over the past 36 months and the company looks very well positioned. It is trading today at 6 x EPS - despite the big move higher the stock is still cheap. At $2.1 billion, Fairfax’s lsecond largest ‘equity’ holding is FFH - Total Return Swaps (giving Fairfax exposure to 1.96 million Fairfax shares). This position has been an exceptional performer for Fairfax over the past 36 months - and it looks very well positioned looking forward. Despite the big move higher the stock is still cheap (more on this below). The overall quality of Fairfax’s remaining collection of equity holdings ($14.5 billion) has improved considerably over the past 6 years. Bottom line, Fairfax’s insurance businesses and investment portfolio has never been better positioned in its history than it is today. This suggests the exceptional results Fairfax delivered in 2023 (driven by the CR and TRIP) are not one-time in nature. Rather, it appears Fairfax is entering a period where it could earn a ROE over the next couple of years that is structurally higher than the one it delivered in the recent past (2018-2022). What is my forecast for Fairfax for 2024? CR = 95% TRIP = 7.4% (details are provided at the end of the post). This combination of results would deliver an ROE of about 15.8%. Over the next couple of years, Fairfax is positioned to deliver an average CR of about 95% and a TRIP of around 7.4%. That combination of reported results should result in an ROE that averages a little better than 17% (2023 to 2025). Importantly, the volatility of this ROE should be less than what was seen from 2018-2022. This is because interest and dividend income has become the largest income stream for Fairfax. Share of profit of associates has also become a very important income stream. Importantly (from a volatility perspective), gains (losses) from investments is no longer the most important driver of earnings for Fairfax. What multiple should a consistent 15% ROE be valued at? Something starting at around 1.3 x book value seems like a low but reasonable target multiple to use for Fairfax looking out 12 to 24 months. How is Fairfax valued today? Fairfax is trading today at a P/BV of 1.15 x (book value at Dec 31, 2023). For Q1 analysts estimate Fairfax will earn C$59.56/share = US$44.00/share (from Yahoo finance). If we subtract the $15 dividend that was paid by Fairfax in January we can estimate Fairfax’s BVPS at March 31, 2024 = $969/share. This puts Fairfax’s ‘real time’ P/BV at about 1.10 x. Is a P/BV multiple of 1.10 x reflective of a company that is delivering an ROE of 15% per year? No, a 1.1 x multiple is usually assigned to P/C insurance companies that are poorly managed and expected to deliver poor results in the future (an ROE of less than 10%). What is the disconnect? Yes, Fairfax delivered an exceptional ROE of 22% in 2023. Mr. Market is beginning to grasp the fact that Fairfax’s earnings have materially increased. But it looks to me like Mr. Market does not yet believe the higher earnings (and ROE) are sustainable. Mr. Market likely expects Fairfax’s ROE to quickly return to its historical level of 10%. And for the ROE to be very volatile. It also should be pointed Fairfax’s stock has increase 216% over the past 3.25 years. Clearly Mr. Market has been warming to the Fairfax story over the past couple of years. Let’s look into the future. My current estimate is for Fairfax to earn $160/share in 2024 and $165/share in 2025. I view these estimates as being a reasonable base case (being not overly aggressive or overly conservative). Using my earnings estimate, it is straight forward to calculate an estimated 2024 year-end book value for Fairfax (we will subtract Fairfax’s $15 dividend that is paid in January of each year). We can then add a P/BV multiple to the year-end BV to come up with an estimate of where the shares could trade looking out 12 months. We can compare this estimate to Fairfax’s current share price to calculate the potential return for the stock. Below, we will look at four different P/BV multiples: 1.1, 1.2, 1.3 and 1.4 We will also use two different time frames: 12 months and 24 months. As stated earlier, I think Fairfax is poised to deliver an average ROE of about 15% over the next couple of years (high and consistent). Therefore, I think a P/BV multiple of 1.3 is a reasonable and conservative multiple to use to value Fairfax - looking out 12 and 24 months. But a range of multiples have been provided so readers can see multiple scenarios. Estimating the 1-year (12 month) potential return for Fairfax’s stock If Fairfax earned $160/share in 2024 and the stock traded at a P/BV of 1.3x in March of 2025, the stock would deliver a return of about 31% over the next 12 months. Estimating the 2-year (24 month) potential return for Fairfax’s stock If Fairfax earned $160/share in 2024 and $165/share in 2025 and the stock traded at a P/BV of 1.3x in March of 2026, the stock would deliver a return of about 49% over the next 24 months. Adding in the dividend of $15/share and the total return for shareholders would be about 50%. Not too shabby. Valuing Fairfax through the lens of a P/C insurer In 2023, Fairfax delivered a CR of 93.2% and a total return on investments of 9.6%. In turn this delivered an ROE of 22%. In the coming years the company looks poised to deliver an average CR of 95% and a total return on investments of 7.4%. This should enable the company to deliver an ROE of around 17% (2023-2025) with less volatility than past years. Today, Fairfax is trading at a P/BV multiple of about 1.10x (to estimated BV of $969/share at March 31, 2024). Given its past results and future prospects, this multiple looks very low. Bottom line, despite its monster run the past 3.25 years, the valuation of Fairfax’s stock continues to look very cheap. As Fairfax delivers on its potential, my guess is Mr. Market will continue to warm to the Fairfax story and slowly push the P/BV multiple the company trades at higher. As a result, future returns for investors in Fairfax will be driven by two factors: Earnings Increase in multiple And as we learned earlier, that is a great set-up for patient investors. ————— Fairfax: My three questions for 2024: To value a P/C insurance company, in addition to important objective criteria like ROE and P/BV, there are also important subjective criteria to consider: What is the quality of the insurance business? What is the quality of the equity holdings? How good is Fairfax at capital allocation? The answers to the three questions above will provide important inputs that feed into future earnings and ROE estimates. I have three separate theses: Fairfax’s insurance business is higher quality than investors generally think today. If correct, this suggests Fairfax’s future CR could come in better than is currently expected. Fairfax’s equity holdings (as a group) has improved markedly in quality over the past 6 years. I don’t think this fully recognized by investors today. This suggests to me that future results from the equity portfolio could come in higher than is currently expected. This suggests Fairfax’s TRIP could come in better than is currently expected. Fairfax is better at capital allocation than investors generally think today. If one or more of my theses outlined above proves true that would be a tailwind for future earnings at Fairfax. As Fairfax releases results each quarter in 2024 we will be given important clues. Bottom line, I think Fairfax is a higher quality company that is generally understood today. The good news is my ‘quality’ thesis for Fairfax is not priced into the shares today. Remember, Fairfax currently trades at a P/BV multiple of about 1.1 x. So if my thesis above is wrong there is likely limited downside. However, if my thesis is correct then there is significant upside as the shares get re-rated to a higher multiple. The risk/reward set-up today looks heavily skewed to the upside. ————— Estimating the total return on the investment portfolio Below is a chart that estimates the total return on Fairfax’s investment portfolio going back to 2018. It also has an estimate for 2024 and 2025. The key take-aways? Bigger + higher return: The investment portfolio increased in size from $39 billion in 2018 to $65 billion in 2023, which is an increase of 66%. Fairfax averaged a total return of 5.3% from 2018-2022. In 2023 the return was 9.6% and the estimate for both 2024 and 2025 is 7.4%. Fairfax is poised to earn a rate of return on its investment portfolio that is 40% higher than what it earned from 2018-2022. More consistent (less volatile): interest and dividends is now driving more than 40% of the total return. Share of profit of associates is now driving more than 20%. This will greatly reduce the volatility of investment returns in the coming years. In turn, this will greatly reduce the volatility of the ROE (compared to the past). 2024 Investment Portfolio Estimates - Key Assumptions: Interest and dividends: average fixed income portfolio = $46m x 4.7% yield Share of profit of associates: Eurobank = $440m; Poseidon = $180m; Fairfax India = $160m Other - non-insurance consolidated companies: includes Recipe, Thomas Cook India, Grivalia Hospitality, AGT, Dexterra, Sporting Life. Net gains (losses) on investments: FFH-TRS = $500m (1.96m x $250); mark-to-market equities = $500 million ($7b x 7%). Assume no change in fixed income portfolio. One time gain (sale/revaluation): $300m. This will be lumpy from year to year. Associates/consolidated holdings - YOY change in FV vs CV: Eurobank, Thomas Cook India, Stelco etc. The list above is not all-inclusive. Therefore, it likely understates the actual increase in intrinsic value that will be building at Fairfax’s various holdings over time (insurance and non-insurance). A Short Note on Volatility The past 2 years there has been a meaningful structural shift at Fairfax in total investment return towards what are considered higher quality sources. From 2018-2022, two items, interest and dividends and share of profit of associates, represented 48% of the total investment return each year. In 2024, the same two items now represent 66% of the estimated total investment return. It is the same (66%) for 2025. Bottom line, there should be significantly less volatility in Fairfax’s total investment return moving forward when compared the past. For most investors lower volatility = higher quality. And higher quality earnings deserves a higher multiple (P/BV). ---------- What does Fairfax's historical P/BV look like? Fairfax's stock trading today at a P/BV multiple of 1.1 x; this looks to be near the lower end of its historical range. Does this make sense given what we know about the company today? Source: COBF @MMInvestor0

-

Gang, great discussion on the FFH-total return swaps. Question for board members: at what P/BV will Fairfax begin to exit the position? I will wade in with my estimate after others have chimed in. What Fairfax does with this position in the coming year (s) will be very interesting to watch. What they do with this position will likely give us a good indication of how they view their stock's valuation: - keep the position in place as long as they view the shares as being undervalued. - exit the position when they assess the shares are approaching fair value. My guess is they will not want to hold the position if the shares are approaching fair value. It makes sense to me that they would start selling down the position when shares hit 95% of their fair value calculation. It is leverage - and as Buffett likes to remind us, leverage can cut both ways. But with the EPS estimate being so robust over each of the next three years (at least) they probably will be very patient. The wild card is all the cash Fairfax is earning right now. With buybacks, Fairfax has the ability to drive their share price higher and probably much higher. So they have an important element of control over their share price - which somewhat reduces the risk of holding this position. It really is a crazy good set up right now. --------- I am working on a valuation update post for Fairfax. I think the stock could return 50% over the next 24 months. If that happened the FFH-TRS would deliver a gain of $1 billion, or $500 million per year. That would be absolutely nuts. What is the math to get to a 50% gain over the next 24 months? (2024 EPS = $160 + 2025 EPS = $165) x 1.3 P/BV. Not a crazy estimate.

-

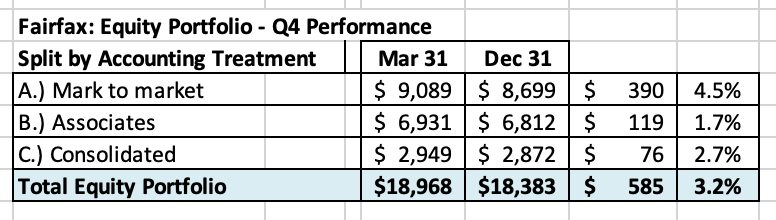

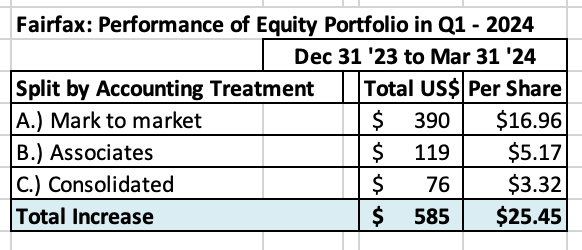

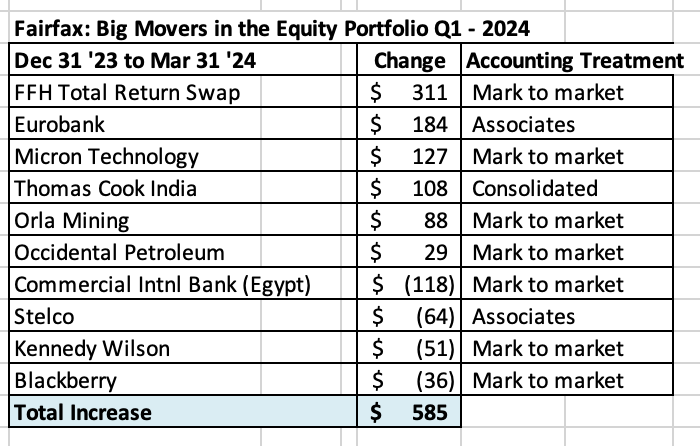

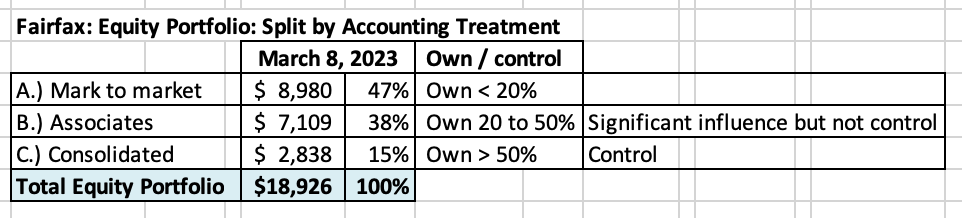

Change in value of Fairfax’s equity portfolio in Q1 - 2024 Fairfax’s equity portfolio (that I track) had a total value of about $19 billion at March 31, 2024. This is an increase of about $585 million (pre-tax) or 3.2%, which is a solid start to 2024. I include the FFH-TRS position in the mark to market bucket and at its notional value. My tracker portfolio is not an exact match to Fairfax’s actual holdings. My summary has been updated to include information from Fairfax’s 2023 annual report. My tracker portfolio is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 48% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 52% are Associate and Consolidated holdings. Over the past couple of years, the share of the mark to market portfolio has been shrinking. This means Fairfax's quarterly results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of $585 million = $25.45/share The mark to market change is an increase of $390 million = $16.96/share. The change in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports results each quarter. What were the big movers in the equity portfolio Q1-YTD? FFH-TRS is up $311 million. This position is now Fairfax’s second largest holding. Eurobank is up $184 million and it is now Fairfax’s largest equity holding at $2.4 billion. Micron Technology is up $127 million. It is now a top-10 holding at $461 million. Thomas Cook India is up $108 million. TCIC continues its strong performance. Commercial International Bank is down $118 million. Egypt devaluated its currency 40% on March 7. It is a well run bank. Country is an economic mess. Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1,206 million or $52/share (pre-tax). Book value at Fairfax is understated by about this amount. Associates: $722 million = $31/share Consolidated: $484 million = $21/share Equity Tracker Spreadsheet explained: We have separated holdings by accounting treatment: mark to market, associates – equity accounted, consolidated, other Holdings – total return swaps. We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. This spreadsheet contains errors. It is updates as new and better information becomes available. Fairfax Mar 30 2024.xlsx

-

@Parsad I wonder if Fairfax has not been a tale of two businesses over the past decade. My guess is the insurance operations have been slowly improving in quality since Andy was put in his role (overseeing all insurance operations) in 2011. Every year Fairfax makes a couple of tweaks to its insurance operations to improve them - in 2023 it was reducing Brit's catastrophe exposure. Bottom line, insurance has been a solid business at Fairfax for the past decade. When I describe Fairfax as a turnaround play I am really doing a dis-service to the insurance operations. Where the wheels came of Fairfax was on the investment side of the business. Yes, global central banks zero interest rate policies stunted the returns of the fixed income portfolio over the past decade (pre-2022). But fixed income wasn't really the problem. Fairfax's problems from 2010-2020 were twofold: 1.) equity hedges / shorts 2.) equity portfolio The first problem has been addressed. And, looking at the decisions the team at Hamblin Watsa has been making over the past 6 years, it looks to me like the second problem has also been addressed. At the AGM I would like to ask Wade Burton a question - what is the investing framework Hamblin Watsa uses today when investing in equities? Have there been any tweaks to the framework over the past 6 years or so?

-

@This2ShallPass , great discussion. I am preparing a longer post on this topic because I think it is important. Quick question: how do you define 'high quality'? What metrics/criteria do you look at to help you determine if a company is 'high quality'?

-

Looks to me like Fairfax is exiting an investment was probably not working out as hoped/expected. Time to move on. From Achmea’s website: - https://news.achmea.nl/achmea-and-fairfax-sell-canadian-start-up-onlia/ “Achmea and Canada's Fairfax Financial Holdings Limited have reached an agreement on the sale of online insurance agency Onlia to Southampton Financial Inc. (“SHFI”). Both parties expect that healthy growth and further development of the start-up will be better guaranteed outside the Achmea Fairfax combination. The financial impact of this transaction is limited. “Onlia was founded in 2018 as a joint venture between Achmea and Fairfax (both 50% shareholders). The online IT platform of InShared, Achmea's digital non-life insurer, served as the basis for this. Onlia now has around 24,000 customers and a premium turnover of €44 million with home and car insurance. Southampton will take over the entire customer portfolio, while respecting and continuing the existing contractual agreements regarding Onlia's services to customers. “SHFI is a holding company backed by strategic value-adding investors in the Canadian property and casualty distribution space. It provides strategic guidance and oversight, access to capital, new markets and back-end support services, including a leading-edge insurance technology platform to its portfolio companies, allowing them to focus on organic growth and to develop market leading insurance propositions serving the needs of a variety of consumers. SHFI shareholders are a group of industry veterans, (i.e. insurance companies, MGUs and brokerages) who benefit from an exceptional network and deep operational experience.”

-

What Is the Best Investment That You've Ever Made?

Viking replied to Blake Hampton's topic in General Discussion

@valueventures it should be noted that most of my investments are held in tax free accounts. Not having to think about taxes is a big deal. Simplicity usually leads to better results. Here are some random thoughts on concentration. Stanley Druckenmiller has some pretty good thoughts on this topic. 1.) My first large investment when i was much younger was Bre-X. Went to zero. And it was the best $5,000 that i ever spent. Because it taught me lots of great lessons… one being the extreme danger of concentration. Another lesson was it taught me the difference between speculating and investing. My Bre-X loss was very very painful - i hate to lose money. It motivated/pushed me to read: - The Warren Buffett Way - Hagstrom - The Intelligent Investor - Graham - One Up on Wall Street - Lynch - A Random Walk Down Wall Street - Malkiel I stole ideas from each of those 4 books and began to stitch together what eventually became my current investing framework - one that fits my psychology/how i am wired. This is critical. And i know it works. This is also critical. To be successful you need both. 2.) My sample size is very small (times i was very concentrated). The fact i did not blow up my portfolio is partly due to luck. How much? Impossible to know. Bottom line, the investing gods have been very kind to me. They aren’t always - you can be right and still blow up. Eyes wide open - if you are going to play the game this way. 3.) I do believe making concentrated bets can lead to extreme outperformance (of the market averages). My 20 year average return is about 20% per year. Not all of this outperformance is due to concentration. For example, I also pay attention to macro at times - this has worked out very well for me over the years but is likely a terrible idea for most people. As a stated earlier, most of my investments are in tax free accounts so i can easily make changes. 4.) I only concentrate in positions i think i understand extremely well - and where i think i have an angle/perspective that is materially different than Mr. Market. So i tend to fish in a very small pond (as people can see from my posts). Patience is important. Fairfax was a big position for me in 2003. And again from 2006-2009. And again in late 2020. Of interest, i was building a large position in Fairfax in late 2019. I thought things were getting better way back then - and the stock looked cheap. But i reversed course and went 100% cash in Feb of 2020 as Covid was rampaging its way across the globe and towards North America. I remember the day i sold everything. I was skiing with my son and a couple of his buddies at Cypress mountain in Vancouver. After a couple of runs in i told my son i needed to go into the lodge. It was clear/obvious to me that Covid was going to wreck financial markets. I sold every stock i owned that day. If i was right? I would miss the big downdraft. If i was wrong? I would miss a small gain - stocks hadn’t sold off yet. The risk/reward set-up for stocks was completely wrong (in my estimation). My son and i talked about it on the drive down the mountain - we both remember the conversation like it was yesterday (his buddies were passed out in the back of the van). I was lucky. Covid crushed stocks like Fairfax - in fact, Fairfax was still way down as late as October of 2020. Thankfully, Sanjeev was pounding the table and he got my attention (I started buying Fairfax again). When the Covid vaccine got announced in November of 2020 i got aggressive with my Fairfax position/research. 5.) I don’t like to be concentrated for extended periods of time. As a result, I was often too quick to take profits - although that likely saved me with Fairfax a couple of times. That cost me with Apple when i sold way too early (I exited right around the time Buffett started to buy). 6.) Really, really good ideas (needle-moving) only come along about once every 5 years or so - at least for me. I do invest in lots of other things - the collective returns on these ideas probably track whatever the market averages are doing. Which is making me question why bother? Why not put this part of my portfolio into index funds? 7.) I wonder if my being drawn to concentration as a strategy is not a psychological flaw - where i am simply looking for a quick way to building wealth. Concentration is also very easy. Am i just looking for something that is easy to do? 8.) as i move from wealth accumulation to wealth preservation my plan is to concentrate much less than in the past - use broad based index funds more. Today index funds are 30% of my total portfolio - i have already started down this path and i love it (so far). My plan is to get this over 60% in the next couple of years. -

@This2ShallPass you ask a great question: “is Fairfax’s equity portfolio high quality?” (I am paraphrasing your question so please correct me if i got it wrong.) This is a hard question to answer. Compared to what? Here is the question i am asking: “is Fairfax’s total equity portfolio increasing in quality?” Using a time horizon of 6 years or more, I think the answer to this second question is an unambiguous yes. Go back to 2017 and look at Fairfax’s equity portfolio. Blackberry was a big position (when you include the debentures). Exco. Fairfax Africa. Farmers Edge. APR Energy. AGT Foods. Mosaic Capital. Astarta. Resolute Forest Products. Recipe. Eurobank. Back in 2017, the drag on the equity portfolio was twofold: - many positions were poor performers - definitely not hitting Fairfax’s 15% return target. - many holdings were actually bleeding money - in total, hundreds of millions every year (losses, write-downs, etc). The underperformance/losses from equity portfolio was a material amount. For years, this depressed the total return Fairfax was earning on its equity portfolio. This bled through to Fairfax’s total results and structurally lowered earnings and ROE for years. This in turn lowered the P/BV multiple Mr Market assigned to Fairfax’s share price. Fast forward to 2024. It is amazing to me the transformation that has happened within Fairfax’s equity portfolio. When you look at the change that has happened over the past 6 years, it’s like someone came in and completely cleaned house. Think of a sports franchise where the GM and coach both get fired at the same time and a new regime takes over - with a new philosophy. With Fairfax, it looks to me like a new regime has taken over except we don’t know what happened internally (yes, i am talking metaphorically here). And it is pointless to speculate (and not fair to the people involved). Of course, i am exaggerating to make my point. And as per usual i am getting off topic. What were some of the changes? Internal 1.) restructured: Exco 2.) put into ‘run-off’: Fairfax Africa, Farmers Edge, Boat Rocker 3.) sold: APR, Mosaic, Resolute Forest Products 4.) take private: AGT, Recipe 5.) other: Blackberry $500 million debenture has been exited External 1.) Greece elected a pro-business government in 2019/2023: Eurobank Six years later, we are almost to the finish line. Farmers Edge and Boat Rocker might deliver another $50 million in losses/writedowns moving forward. The equity portfolio will always have a few laggards. Fairfax’s problem in 2017 was it was stuffed with problem children. Looking forward Importantly, it looks to me like Fairfax has a new framework for how it manages its equity portfolio. Hamblin Watsa is not a turn-around shop. A higher premium has been put on management. All holdings are now expected to deliver an acceptable return - Fairfax will no longer be a piggy bank for chronically underperforming units. Moving forward, capital will go to the best risk/adjusted opportunities. Bottom line, really like what i have seen from management since 2018. Why do we care today? If the quality of the equity holdings is materially better than it was pre-2017 then the return it will be capable of delivering moving forward will be much higher than in the past. The change is the key. Higher earnings = higher ROE = higher P/BV multiple. The best example of the improvement is the ‘share of profit of associates’ bucket. Driven by Eurobank, is is now delivering +$1 billion per year in pre-tax earnings. I think the non-insurance consolidated holdings are getting ready to pop higher in the coming years. And i think the table is getting set for Fairfax to start delivering higher than expected ‘gains on investments’ - unrealized and realized. The great thing is investors are currently expecting historical (low) returns from Fairfax’s equity portfolio - sustainable higher future returns is not built into Fairfax’s stock price today. Two things drive earnings at Fairfax: 1.) insurance - underwriting profit 2.) investments - average return on investments I think Fairfax’s insurance business and investment portfolio has been slowly, incrementally improving in quality since 2017. If my thesis is correct then future earnings will likely continue to surprise to the upside. It will take years for all the positive changes to fully flow through to earnings. As i stated already, higher earnings = higher ROE = higher P/BV multiple.

-

What Is the Best Investment That You've Ever Made?

Viking replied to Blake Hampton's topic in General Discussion

@valueventures if my writings have helped you then that is great to hear. But make no mistake about it, any success you have experienced from reading my writings actually has very little to do with me. Your success is primarily the result of your investment framework / actions. And the action thing is super important. That would be tip #1. But don’t confuse action with volume. I might make one big decision every couple of years. Now, of course, there is a lot more involved. But your question is so broad i think it is best answered in pieces. I hope other board members also chime in with their thoughts. ————— When i worked at Kraft Foods i was at a company sales convention. The guy running Kraft Canada had just announced his retirement and i was lucky enough to get invited to his send off. He said a few words…. Here is what i remember. Of course i am paraphrasing… “I am not smarter or more talented than most people. So how did i do it (become very successful - personally / professionally)? Whether you realize it or not, every day the train stops outside your door. You decide every day if you want to get on it or not. The reason i am in the position i am today is because 20 years ago i decided to get on the train. And 20 years later here is where it has taken me.” Most people rarely ever decide to get on the train. Their whole life. Even though it is stopping outside their door every day. They are much too risk averse. Calculated risk taking, with a bias to action, is extremely powerful when done well. Why? You think through all the bad things that can happen - they are usually knowable. And you usually way underestimate the good things. The ‘positive unintended consequences’ can be massive. The risk / reward is way, way more skewed to the upside than people think. Every big decision i have made in my life has worked out way better than i expected - and i have made a bunch. And much of the upside was unknowable when i made the decision - that is the mind bending part of ‘calculated risk taking.’ There is an important investment angle to this as well… ————- Now to be a risk taker, first you actually have to think about things. And in my experience this is where most people fall down. Most people don’t think enough about the important stuff. I remember doing performance reviews with staff. I would have them review themselves on their own. I would prepare their review on my own. And then we would get together and compare notes. Most of my staff disliked this format. Why? I learned over time that most people do not have the ability to jump out of their own skin and evaluate themselves in an unbiased way. And they also don’t actually have a plan when it comes to their career. Both of these things are important to being a successful investor. ‘Most people are grazing the planet waiting to die.’ I am not sure where i heard/read this. But it has stuck with me over the years. I use it as a self motivator (not to judge the choices of others). There are lots of ways to live your life - and there is no right or wrong way. But the choices we make do have consequences. And most people fail to grasp that doing nothing (grazing) is actually a choice. Sorry, this post just got way off base… -

@ICUMD thanks for sharing… your take makes a lot of sense.

-

@ICUMD below are some thoughts building on your post. 1.) prior to Modi’s election, Fairfax’s vehicle for investing in India was Thomas Cook India. That is why Quess started out there. After Modi was elected Fairfax decided they wanted to get much more aggressive investing in India. But they had a problem… Thomas Cook was the wrong vehicle / structure. Solution? Do what any rational actor does in investing - when the facts change - you pivot your strategy. And Fairfax India was born. Today Fairfax has an opportunity to make what could be a once in a generation purchase of a massive bank in India. But they have a problem. Fairfax India is likely the wrong vehicle / structure (as it exists today). What to do? What any rational actor does - pivot/update the strategy to fit the facts/reality as they exist today. 2.) i have long thought the ‘solution’ to Fairfax India’s big discount in recent years is for Fairfax to take it private. Step one - approach the remaining large shareholders and see if they are interested - and what price. Step two - take out remaining small shareholders - perhaps at BV. To fund a big price of the takeout, Fairfax India could sell down some assets. The real prize for Fairfax would be getting 100% of Fairfax India’s position in BIAL. As @Redskin212 notes, the perspective of insurance regulators likely matters. Regardless, India is shaping up to be a super interesting geography for Fairfax in 2024: - rumours regarding bid for big bank - Digit IPO - possible Anchorage IPO / next steps for BIAL - what all this means for Fairfax’s strategy in India - what all this means for Fairfax India

-

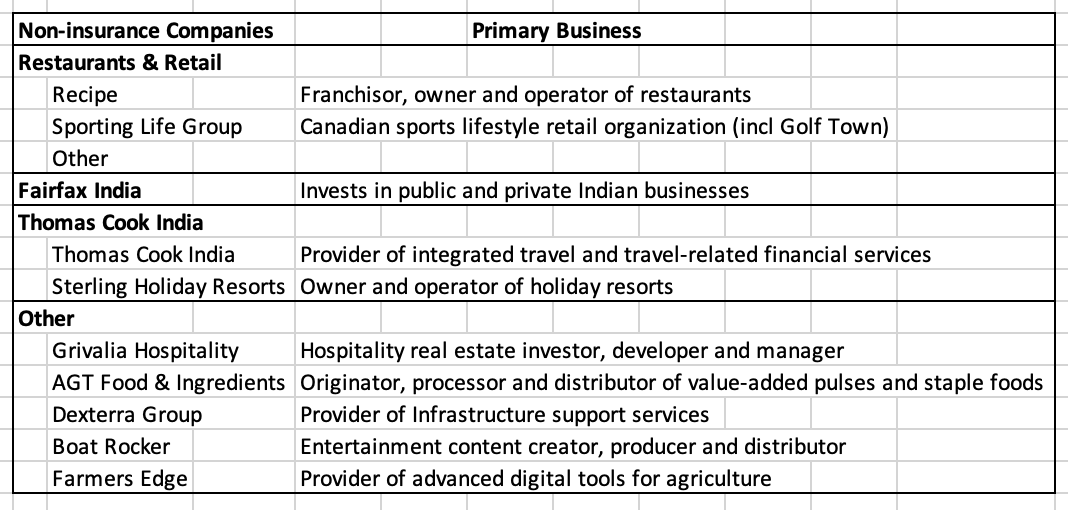

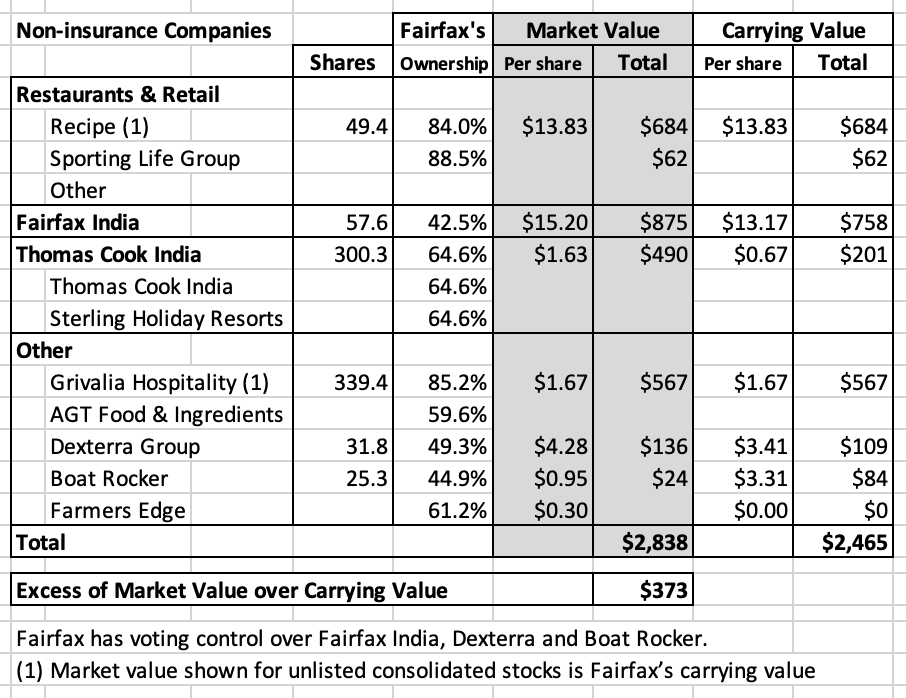

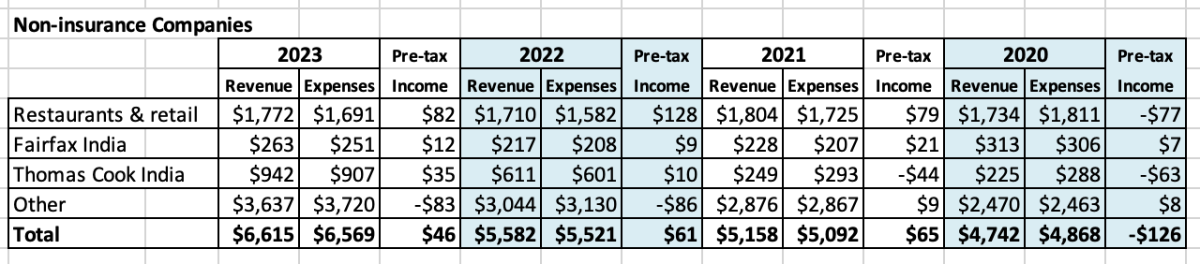

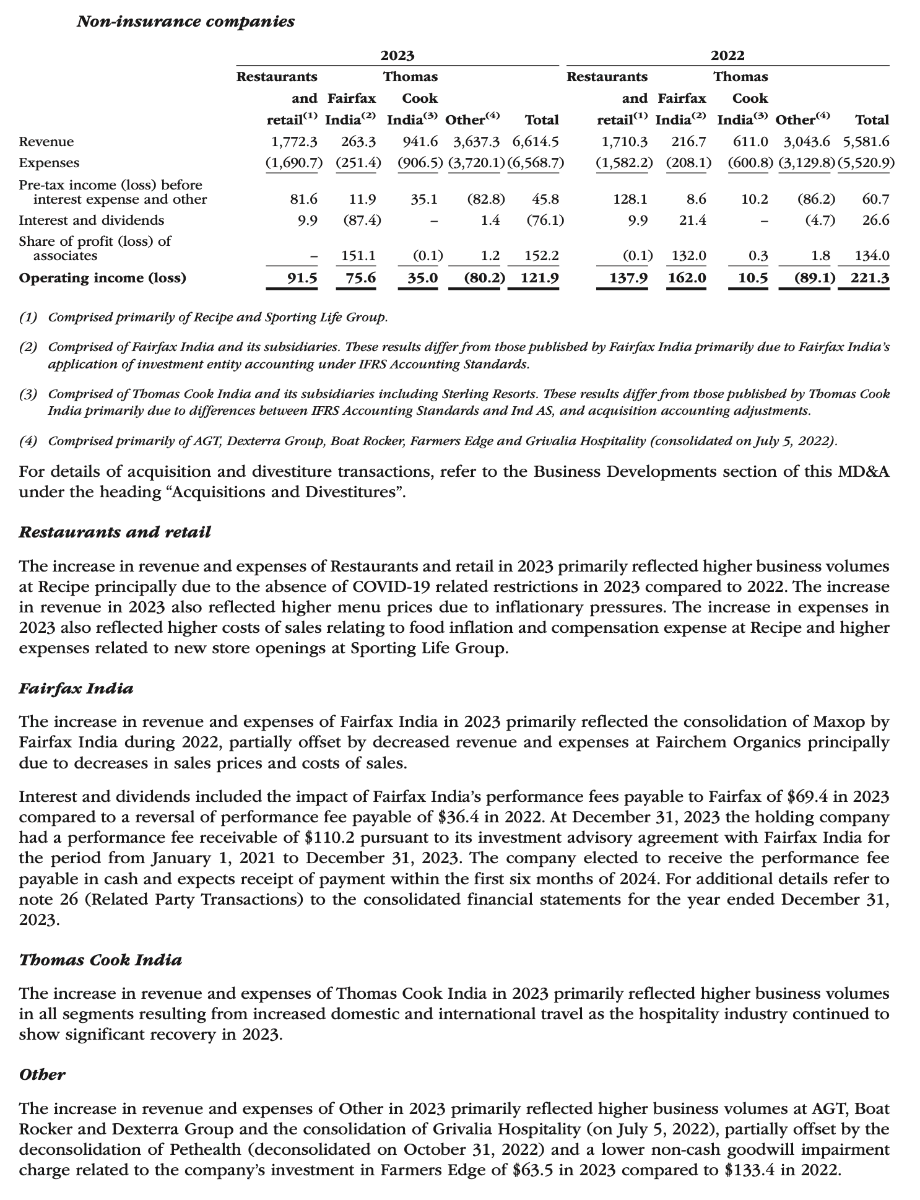

Operating Income of Non-insurance Consolidated Companies Over the past couple of years Fairfax has been materially increasing the size of its non-insurance consolidated holdings. Revenue and ‘normalized’ earnings have been moving higher. However, the improving results over the past 2 years has been masked by large temporary or one-time write-downs/losses - so most investors are not aware of the many positive changes that have been happening under the hood. My guess is the earnings power for this group of holdings will begin to shine through fully in 2024. In the coming years, this bucket is poised to become a much more important income stream for Fairfax - in terms of size and consistency. Let’s begin by getting some context. The big picture Fairfax has a very large equity portfolio – as of March 8, it has a total value of about $19 billion (including the FFH-TRS position at its current notional value of $2 billion). From an accounting perspective, equity holdings can be grouped into one of three buckets – based on how much of the company Fairfax owns and how much control it exerts. In this post we are going to review the equity holdings that fall into the ‘Consolidated’ bucket. These are the holdings where Fairfax owns more than 50% (or has more than 50% voting control) and therefore has a control position. The common stock ‘Consolidated’ holdings have a total value of about $2.8 billion, which is about 15% of Fairfax’s total common stock portfolio. I don’t think holdings like AGT Food and Ingredients and Sporting Life are included in the $2.8 billion. Bottom line, the group of ‘Consolidated’ holdings likely has a market value of well over $3 billion. From an accounting perspective, the results of ‘Consolidated’ holdings are captured on the Consolidated Statements of Earnings in the ‘Non-insurance revenue’ and the ‘Non-insurance expenses’ line items. What holdings are captured in this bucket? Below is a list of all the companies - with a brief description of their primary business - that are included in the ‘Consolidated’ bucket. Non-insurance companies This reporting segment is comprised as follows: Restaurants and retail – Comprised principally of Recipe, Golf Town, Sporting Life and Toys “R” Us Canada (deconsolidated on August 19, 2021). Fairfax India – Comprised of Fairfax India and its subsidiaries, which are principally NCML and Privi (deconsolidated on April 29, 2021). Thomas Cook India – Comprised of Thomas Cook India and its subsidiary Sterling Resorts. Other – Comprised primarily of AGT, Dexterra Group, Boat Rocker, Farmers Edge, Grivalia Hospitality (consolidated July 5, 2022), Pethealth (deconsolidated on October 31, 2022) and Mosaic Capital (deconsolidated on August 5, 2021). How much of each holding does Fairfax own? And what is the value? The information below is from page 15 of Fairfax’s 2023AR and captures what they call the ‘common stock holdings’. My guess is their list does not capture a couple of important holdings: AGT Food and Ingredients, Sporting Life and possibly Meadow Foods. We were given the carrying value for Sporting Life in a different section so I have added that. However, we were not given a carrying value for AGT or Meadow and I have not bothered to guess. So the total for both carrying value and market value in the chart below are likely understated by quite a bit. Interestingly, the excess of market value to carrying value for this collection of holdings is about $373 million. This number is also likely understated by quite a bit. What do the financials look like for this group of holdings? Over the past three years, revenue has increased 39% to $6.6 billion. However, pre-tax income has been low and stagnant, averaging about $60 million over the past three years. Below is the split by reporting segment. Notes: Pre-tax income (loss) before interest expense; excludes interest and dividends, share of profit (loss) of associates and net gains (losses) on investments. The majority of Fairfax India’s earnings fall into the ‘Share of Profit of Associates’ bucket. What is driving the significant top line growth? Improving fundamentals: Companies in this bucket of holdings were significantly impacted by Covid, which was a significant drag on results from 2020 to 2022. Recipe (full serve, dine-in restaurants), Thomas Cook India (travel) and Dexterra (facilities management). Results from these these companies rebounded in 2023. Significant new addition: Grivalia Hospitality was added in 2022 when Fairfax increased its stake from 33.5% to 78.4% at a cost of $195 million. The position was increased further in 2023 to 85.2%. Significant increases in ownership: in 2022, Fairfax increased its stake in Recipe from 46% to 84% at a cost of $342 million. In 2022, Fairfax increased its stake in Sporting Life from 71% to 88.5% (funded via retained earnings). There also were a few notable sales / deconsolidations: Restaurants & retail: Toys “R” Us Canada (deconsolidated on August 19, 2021) Fairfax India: Privi (deconsolidated on April 29, 2021). Other: Pethealth (deconsolidated on October 31, 2022) and Mosaic Capital (deconsolidated on August 5, 2021). Bottom line, top line should grow nicely in 2024 and future years. And now a much larger share of earnings for these companies will flow through to Fairfax shareholders. Pre-tax income at this group of holdings has been low the past four years due to significant temporary or one-time items. As mentioned already, Covid was a significant headwind for Recipe, Thomas Cook India and Dexterra from 2020 to 2022. Thomas Cook India had a fantastic 2023. Recipe continues to right-size its business/structure/systems after a decade of rapid consolidation. Farmers Edge took very large write downs in 2022 ($133.4 million) and 2023 ($112 million in losses) and the business is now carried at a $0 valuation. It was taken private by Fairfax in March of 2024. My guess is this business will stop bleeding money later in 2024. Boat Rocker also saw a write down in 2023 ($26 million). This is now a small holding for Fairfax. Grivalia Hospitality took a loss of $66 million in 2023. For the past couple of years, Grivalia has been investing heavily in building out its collection of ultra-high luxury resorts. 5 are now open. Revenue should materially increase in 2024. The company is pivoting its business from the investment phase to the operating phase which should lead to improving financial results. The significant temporary / one-time events of the past couple of years will likely decline in size moving forward. Headwinds will become tailwinds. And when they do, the earnings power of this collection of businesses will be released like a coiled spring. Summary The companies in this bucket of holdings have been undergoing significant positive changes over the past couple of years. (Just like the rest of Fairfax’s equity holdings.) Poor performers are being wound down. Underperforming companies have been executing turn-around plans for the past couple of years and improved results are starting to show up. New holdings have been added in recent years. And Fairfax owns more of existing holdings. Bottom line, the intrinsic value of the companies captured in this bucket has been increasing over the past three years. We should see earnings start to materially improve in the coming years. This group of companies is poised to become another meaningful and growing income stream for Fairfax. Earnings estimate for 2024 and 2025 My current estimate is for this collection of holdings to deliver pre-tax earnings of $150 million in 2024 and $200 million in 2025. For reasons laid out above, these estimates will likely prove to be very conservative. ————— A strategy question Do we see Fairfax continue to build out this bucket of companies? Do they aspire to become more of a holding company like Berkshire Hathaway in the coming years? Are there strategic advantages to Fairfax of having a few large wholly owned cash generating equity holdings to complement their P/C insurance business? What do board members think? I don’t think Fairfax wants to go full Berkshire in the coming years. Unlike Berkshire, at the appropriate time, Fairfax sells assets - I expect Fairfax will monetize one or more of its non-insurance consolidated holdings in the coming years. And I suspect it is still a priority for Fairfax to grow its P/C insurance business. ---------- From Prem's Letter, FFH 2023AR: "As the table on page 15 shows, the consolidated investments include the following: Recipe, Fairfax India, Grivalia Hospitality, Thomas Cook India, Dexterra Group and Boat Rocker Media. Our consolidated investments are significant, producing total revenue of $6.6 billion and pre-tax income of $271 million in 2023. Fairfax India had pre-tax income of $380 million, Recipe $38 million, Thomas Cook $27 million and Dexterra $29 million. Those were offset by losses at Grivalia of $66 million, Boat Rocker $26 million and Farmers Edge of $112 million which included impairments of $64 million." From Prem's Letter, FFH 2022AR: "As the table on page 13 shows, consolidated investments include the following: Recipe, Fairfax India, Grivalia Hospitality, Thomas Cook India, Boat Rocker Media, Dexterra Group and Farmers Edge. Our consolidated investments are significant, producing total revenue of $5.6 billion, EBITDA of $743 million and pre-tax income of $303 million (excluding a $133 million writedown of Farmers Edge) before minority interest in 2022."

-

@This2ShallPass Fairfax has always been my preferred core holding for a whole bunch of reasons. Fairfax has been cheap since Covid hit in 2020 - so i have been way overweight Fairfax since then. And when i am way overweight Fairfax i am not really interested in holding a big position in Fairfax India. In addition to my core positions, i also will do some tactical trades with a small part of my portfolio. Stocks i think i understand pretty well. Positions of maybe 1% or 2% of my portfolio. Buy when they get cheap and sell when they run up for hopefully a quick 5% or so gain. My trades are done in tax free accounts. I call it mucking around. Fairfax India is a stock i usually trade in and out of a couple times a year. I haven’t this year because it hasn’t dropped to my buy price. Instead i have traded in and out of Canfor (CFP.TO) a couple of times already. And also Baytex (BTE.TO). I recently also bought some BCE.TO and T.TO (Canadian telecom stocks are hated right now). If i ever get my Fairfax weighting down to something more reasonable then i probably would take a closer look at Fairfax India as more than just a quick trade type of holding. I like management at Fairfax India a lot. And i love BIAL. My biggest issue with Fairfax India is liquidity. I find it very difficult to build out a position - without causing the price to move. My bigger concern is if i ever need to quickly liquidate my position. Solution? Keep it a small position.

-

@nwoodman I agree. However, I was quite surprised by how much (little) Fairfax paid to take out Recipe. Fairfax got a good to great deal. But at the time I thought they could have paid less and still got it through. Is this another new trend?

-

My view is Fairfax India has been a gift for investors for at least the past 5 years. The stock has been on perpetual sale. And for lengthy periods of time it has been available at obscenely low prices (sub $10). Performance fee? It is what it is. There are the facts as to how it works (the mechanics). But in terms of debating whether it is good or bad... well, from my perspective, it is kind of like trying to debate the weather. With any investment, fit is always paramount. If you don't like the fee don't invest in Fairfax India. I am not saying the fee structure is good or bad - each person needs to decide that on their own based on their analysis of the situation and how they are wired. Personally, the fee structure has never impacted my decision to invest in Fairfax India (I don't own any today, but I have held large positions in the past). 1.) To me the key question with Fairfax India is what is BIAL worth? The answer to this question is going to drive your future return on this investment over the next 5 years much more than anything else. 2.) The next question (linked to the first) is what does Fairfax India do with Anchorage and when? (This, of course, gets back to BIAL.) 3.) The emerging question is what is Fairfax India's involvement with the bid for IDBI Bank? This would be a massive purchase. Where is the significant $ going to come from? And what does that mean for current Fairfax India shareholders? I am pretty sure Prem said at the AGM last year that Fairfax India would not be issuing any new shares for less than book value (perhaps someone else can confirm/deny this). 4.) And finally, how serious is the current regulatory issue with IIFL Finance? That is Fairfax India's second largest holding and the stock has been bludgeoned lately.

-

@frommi congrats on your investment in Fairfax. I suspect many people on this board are sitting on pretty spectacular gains and wondering what to do. One of the keys to investing is to have a plan and then (usually) stick to it - and not keep moving the goal posts. My thesis with Fairfax has evolved over the past couple of years. The quality of the insurance business is higher than I thought (and getting better - I think). The quality of the equity holdings is also getting better (the dogs keep shrinking in size each year). Significantly extending the duration of the fixed income portfolio in 2023 was a big deal. The kicker is the size and quality of operating earnings is large and largely set for the next 4 years. When I weave it all together I think Fairfax deserves to trade at a higher multiple than it has over the past 10 years - 1.3 x BV on the low end. The fundamentals just keep getting better and better - that has been a surprise for me. I am just finishing a post on non-insurance consolidated holdings (coming in the next day or two). I think that bucket is the next coiled spring that is set to go off. Similar to what happened with 'share of profit of associates' a couple of years ago. Perhaps we see a new $400 million and growing earnings stream as soon as 2025? I am modelling $200 million in 2025. That is not on anyones radar right now. My point is there are still lots of different tailwinds. BV was $930 at Dec 31, 2023. Let's assume BV grows $150 in 2024 and 2025 (subtracting $15 dividend). That would get us to a BV of $1,230 at Dec 31, 2025. Apply a 1.3x BV multiple (at the low end in my mind) and we get a stock price of $1,600 in 24 months. Including dividends, that would deliver a return of 45%. Pretty solid return over 2 years. I don't think these are particularly aggressive assumptions. There are also a number of wild cards. One that intrigues me is @SafetyinNumbers speculation of what happens if Fairfax gets added to the Canadian benchmark index in 2024 or 2025. I think indexing is only going to become a bigger phenomenon in the coming years - so the lift to Fairfax's stock if it was to get added could be significant. The key risk today (company controlled) is capital allocation - after a couple of very good years, does hubris set in (again)? Not a concern today - but something I am monitoring. My post is not to try and talk anyone into not selling down a position. People sell for all sorts of reasons. The spike in Fairfax has taken most of us by surprise. I am still trying to understand what it all means. And yes, I have a big smile on my face as I think about it.

-

I think in the past @glider3834 has pointed out that there may be some tax loss benefits as well. But i am not an accountant so can’t speak to those sorts of things.

-

One step closer to being able to (finally) close the book on this perpetual money-losing holding. It would be interesting to know what the benefits are to Fairfax of taking it private.

-

@dartmonkey you are spot on. My current estimate has Fairfax's mark-to-market equity portfolio at about $9 billion. About $2 billion of this is the FFH-TRS. My earnings estimate for 'net gains on investments' is $1 billion for 2024: FFH TRS = $2 billion = $250 x 1.96 million = $500 million Remaining mark-to-market holdings = $7 billion x 7% = $500 million