Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Dinar , here are Fairfax's numbers as of Dec 31, 2023. In my equity spreadsheet summary I include the FFH-TRS at its current notional (market) value of +$2 billion. This bumps the value of Fairfax's equity portfolio to $19 billion.

-

@Hamburg Investor good questions. I am modelling $1 billion in ‘net gains from investments’ in 2024. When i built my forecast, the rough math was $500 million from FFH-TRS ($250/share x 1.96 mn shares) and another $500 million from the mark-to-market equity holdings ($7 billion x 7% return on portfolio). From my perspective, a total of $1 billion is the important number. There are numerous ways to get there… i identified one potential path above. Given the continued increase in Fairfax’s share price to start 2024, my forecast of $1 billion in total gains is looking pretty conservative right now. But things can change fast. And there will be puts and takes for all buckets as the year plays out. With my 2024 forecast i want to lean out a little, but not get too far in front of my skis. In terms of forecasting for 2025, there is more uncertainty - we are forecasting for two years. Yes, i am modelling a slightly lower ‘net gains from investments’ number in 2025 - primarily bacause i think the contribution from FFH-TRS will slow in 2025 (compared to 2024). High conviction? No. Just what seems like a reasonable guess. Importantly, trying to guess what Fairfax is going to do with capital allocation is quite difficult looking out to 2025. Does Fairfax take a big swing (like buying a big bank in India?) or do they play it safe like they have been doing the past couple of years and continue to buy out minority partners (insurance and equity holdings). The risk / reward set-up is quite different for shareholders.

-

Starter position in Saputo SAP.TO. In recent days it has dropped to my buy price of under C$26. They have been working on a turnaround for the past 3 years. They think the benefits should start showing up in results beginning in the April to June quarter (Q2 of calendar 2024). Each quarter more tailwinds should flow to reported results. This company is pretty hated right now. The management team has been consistently over promising and under delivering for the past 5 years. The Saputo family controls the company. They will keep at it until the fix happens. The question is in 1H 2024 are investors going to get another rug pull? Or have financial results hit bottom and are now poised to move higher over 2024?

-

As per @glider3834's suggestion I want to add Sporting Life to my spreadsheet that tracks Fairfax's large equity holdings. It is a consolidated holding and it has a carrying value of $82 million. However, the carrying value for the 'other' bucket for 'Consolidated Stocks - Consolidated' holdings in the summary below has a value of zero. This suggests to me that the values for Sporting Life is not included in the summary below provided in Prem's letter in Fairfax's annual report? Is this also the case with AGT Food Ingredients?

-

@Maverick47 I agree. I think underwriting profit at Fairfax is about 20% of its various income streams. I think most P/C insurance companies are closer to 40% or more. So moving forward, a really bad year for catastrophes will affect Fairfax much less than peers. In fact - counterintuitively - long term Fairfax investors should probably be hoping for a really bad cat year. It would likely extend the hard market and Fairfax would likely be a big net winner over time. This is a big difference from 'old Fairfax' and 'new Fairfax.' New Fairfax looks like it is becoming a much more financially resilient company. In terms of financial stability, Fairfax is getting to a very good place. The different earnings streams are growing meaningfully in size and new streams are getting built out. I think Fairfax has been executing a strategic plan that we are just now starting to fully grasp.

-

@Thrifty3000 you bring up a very good point. As you are aware, I only ever look at (use) 'effective shares outstanding'. I have not spent much time looking at (or thinking about) fully diluted shares. And that is because I don't know how to think about fully diluted shares at Fairfax. Do you have a mental model / framework for how to understand fully diluted share count at Fairfax and what it all means for Fairfax investors? I do notice that each year Fairfax buys back shares and not all of them are retired. Lot's of good questions / comments on Fairfax today. Keep them coming!

-

@gfp good question. I have some questions of my own as to how Eurobanks dividend will flow through Fairfax's income statement and balance sheet when it starts. But before I get into the accounting, here is a general thought. I am hoping Fairfax continues to grow the 'interest and dividend' bucket. I think it is generally viewed by investors to be the most important income stream for a P/C insurer (with underwriting profit being a close second) because it is usually not very volatile year to year. As more of Fairfax's earnings come from 'low volatility' sources we should see multiple expansion. My assumption is when Eurobank starts paying a dividend it will drop into 'interest and dividends' for Fairfax. If this is not the case, someone please let me know. As I have said many times before, I am not an accountant - so there will be errors in how I look at things. And that is a real strength of this board - we are all to learn from each other and improve our understanding/analysis. What happens to 'share of profit of associates' for Eurobank? Is this number each quarter affected by the dividend payment? The short answer is I don't know. Perhaps you or someone else can enlighten me? Is share of profits of associates an income statement item (share of pre-tax net income)? And the dividend a balance sheet item (return of capital)? My understanding is Fairfax's carrying value for Eurobank will get updated each quarter as follows: Eurobank prior quarter carrying value + share of profit of associates - dividend amount paid to Fairfax. If this is not accurate, please let me know. The other question I have regarding the Eurobank dividend is, once approved, how will it be paid out... quarterly? or will it be in a lump sum? Thanks again for the question.

-

@wisowis good question. The "Other (revenue - expenses)" bucket has had significant noise the past couple of years. In 2023 Consolidated investments produced pre-tax income of $271 million but the 'reported' number was $46 million. Losses from Grivalia, Boat Rocker and Farmers Edge were $204 million in 2023. There was a significant write down on Farmers Edge of $133.4 million in 2022. I don't think these one-time losses will continue at this level moving forward. Consolidated investments produced revenue of $6.6 billion in 2023, up from $5.6 billion in 2022. This bucket of holdings is growing like a weed. There is likely a little more pain coming from Farmers Edge but once Fairfax takes it private my guess is they will do something to (finally) stop the losses/bleeding. Boat Rocker has a carrying value of $84 million and a market value of $24 million so we could see another modest write down here. The past couple of years, Grivalia Hospitality has been spending heavily to build ultra-luxury resorts with minimal money coming in; I think this may have changed late in 2023 as they now have 5 resorts (I think) open for business = revenue. Thomas Cook India is smoking. Recipe, Sporting Life, AGT Food Ingredients and Dextera all look to be chugging along. Once the significant bleeding stops I think people will be pleasantly surprised by the earnings that this bucket will be able to deliver in the coming years. Regardless of reported earnings in recent years, I think significant value is building in the holdings in this bucket. At some point in will show up in reported earnings. And it will likely 'surprise' people like what happened a couple of years ago with the spike in earnings from the 'share of profits of associates' bucket. Therefore, I think my estimate of $150 million in 2024 and $200 million in 2025 is quite conservative. ---------- FFH 2023AR: "As the table on page 15 shows, the consolidated investments include the following: Recipe, Fairfax India, Grivalia Hospitality, Thomas Cook India, Dexterra Group and Boat Rocker Media. Our consolidated investments are significant, producing total revenue of $6.6 billion and pre-tax income of $271 million in 2023. Fairfax India had pre-tax income of $380 million, Recipe $38 million, Thomas Cook $27 million and Dexterra $29 million. Those were offset by losses at Grivalia of $66 million, Boat Rocker $26 million and Farmers Edge of $112 million which included impairments of $64 million." FFH 2022AR: "As the table on page 13 shows, consolidated investments include the following: Recipe, Fairfax India, Grivalia Hospitality, Thomas Cook India, Boat Rocker Media, Dexterra Group and Farmers Edge. Our consolidated investments are significant, producing total revenue of $5.6 billion, EBITDA of $743 million and pre-tax income of $303 million (excluding a $133 million writedown of Farmers Edge) before minority interest in 2022." FFH 2022AR: "Operating income of the Non-insurance companies reporting segment increased to $184.9 in 2022 from $78.2 in 2021. Excluding the impact of the non-cash goodwill impairment charges on Farmers Edge recorded during 2022 of $133.4, operating income of the Non-insurance companies reporting segment increased significantly by $240.1 to $318.3 in 2022, principally reflecting higher share of profit of associates at Fairfax India, higher business volumes at Thomas Cook India, and improved margins and higher business volumes in the Restaurants and retail operating segment and at AGT. This significant improvement of $240.1 from the Non-insurance companies reporting segment reflected the easing of COVID-19 restrictions that had previously negatively impacted this reporting segment with the increase in operating income in 2022 driven by increases reported in all underlying operating segments."

-

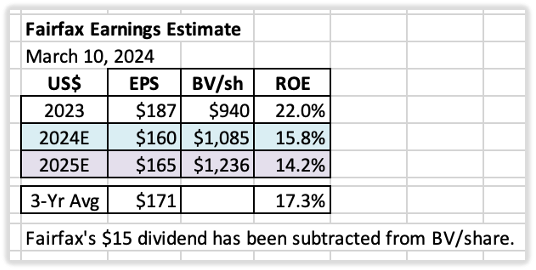

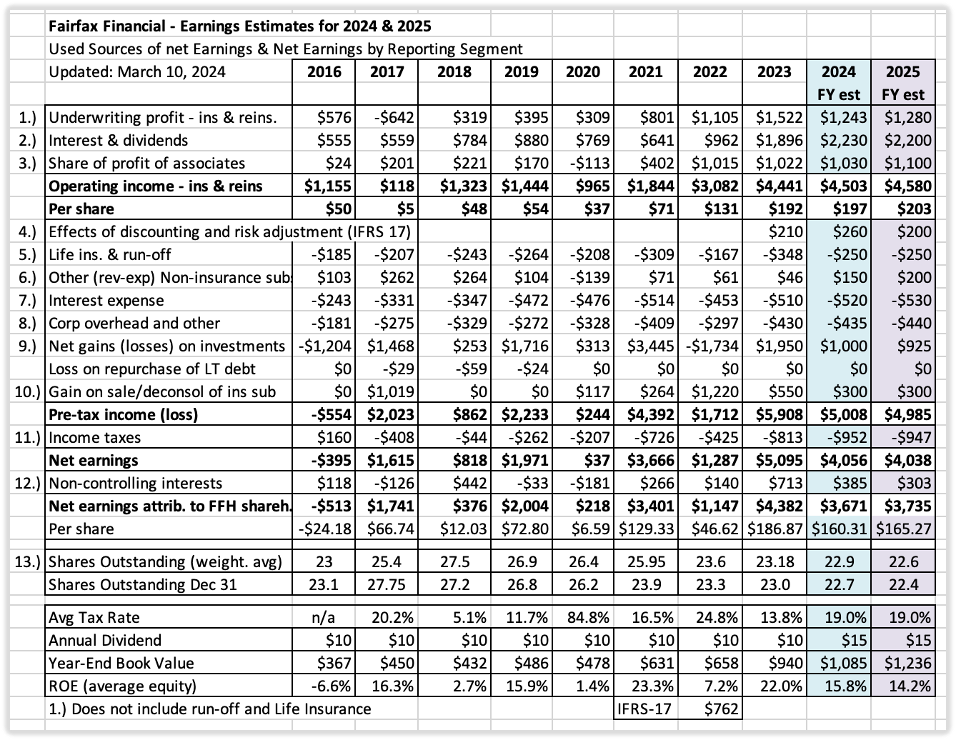

Earnings Estimates – Two Year Summary for 2024 & 2025 Below is an update to my two-year earnings estimate for Fairfax. Please note, forecasts are a guess at a point in time. To state the obvious, things are constantly changing. As a result, my earnings forecasts quickly become outdated. These forecasts are intended solely for entertainment purposes – please keep this in mind. Since my last update, Fairfax has released both Q4 earnings and their 2023 annual report. This allows us to finalize results the 2023 year and update our forecasts for 2024 and 2025. Summary My current estimate is Fairfax will earn about $160/share in 2024 and about $165/share in 2025. For reasons outlined further below, I think both of these estimates have been constructed using mildly conservative assumptions. 2024 & 2025 Forecast A hard piece to forecast with Fairfax is capital allocation. Fairfax is currently generating a significant amount of earnings. But we don’t know today how the future cash flows will be invested: Grow insurance (continuation of hard market) Buy out minority partners in insurance? Equities or fixed income? Buy back a meaningful amount of Fairfax stock? Other? Looking at the last 5 years, the management team has done an outstanding job with capital allocation. My guess is they will continue to make good decisions (on balance) and this will benefit shareholders – likely providing a tailwind to my forecasts for 2024 and 2025. Using Yahoo Finance as a guide, analysts are collectively estimating that Fairfax will earn about US$148/share (C$200) in 2024 and US$157/share (C$211) in 2025 (using $0.742 US$/C$ exchange rate). Why are analyst estimates below my forecast? From what I can see, most analysts are assigning little benefit to future earnings and Fairfax’s proven capital allocation skills. Most analysts will include these benefits into their earnings estimates after Fairfax has announced something. I am assuming interest rates remain roughly at current levels (at March 10, 2024). Of course, this will likely not be the case. But given the duration of the fixed income portfolio is now closer to the duration of the insurance liabilities, changes in interest rates (up and down) might kind of balance out (in ‘net gains/losses on investments’ and ‘effects of discounting and risk adjustment- IFRS 17’) Below is an 8-year snapshot for Fairfax. It communicates in a concise manner the dramatic transformation that has happened at the company, beginning around 2021. There has been a spike in operating income per share – it has increased from an average of $39/share over the 5-year period from 2016-2020, to $192/share in 2023. This much higher amount now looks like the new baseline for the company. For 2024, my estimate has operating income increasing to $197/share, which is a 400% increase from the average from 2016-2020. Normalized earnings at Fairfax have moved to a much higher level – and, importantly, this level looks sustainable. What are the key assumptions? 1.) Underwriting profit: Estimated to come in at $1.24 billion in 2024. Net written premiums growth of 12% in 2024 and 3% in 2025. This is being driven by: Continuation of the hard market, which we estimate will add $1 billion of NWP. The Gulf Insurance Group (GIG) acquisition, which will add $1.7 billion of NWP. Combined ratio (CR) of 95% in both 2024 and 2025. Catastrophe losses: 2024 will be a more normal year (higher than 2023). Fairfax continues to modestly shrink their total catastrophe exposure. Reserve releases: continuation of the positive trend observed in 2023. 2.) Interest and dividend income: Estimated to increase to a record $2.2 billion in 2024 and 2025 Interest and dividend income in Q4 2023 was $536.6 million; this provides a good baseline (starting point). GIG adds about $2.4 billion to the total investment portfolio in 2024. A tailwind. Eurobank will start paying a dividend in 2H 2024. A tailwind. Rate cuts by global central banks would be a headwind in 2H. 3.) Share of profit of associates: Estimated to increase to a record $1.03 billion in 2024. Earnings at Eurobank, Poseidon, Stelco and Fairfax India, in aggregate, should continue to grow nicely. EXCO (nat gas prices) could be a headwind. GIG will be a small headwind as it is now consolidated. 4.) Effects of discounting and risk adjustment (IFRS 17): The two key drivers for this bucket are the trend in net written premiums of the insurance business and changes in interest rates. Net written premiums growth of 12% in 2024 should be a tailwind. I am modelling for interest rates to remain flat. This bucket is among the most difficult to model – therefore, my confidence level in my estimates is low. 5.) Life insurance and runoff: This combination of businesses lost about $348 million in 2023. I expect earnings in 2024 to be a little better – a lower loss of $250 million - with life insurance being a modest tailwind. 6.) Other (revenue-expenses) - non-insurance subsidiaries: Recipe, Dexterra, AGT, Grivalia Hospitality, Boat Rocker, Farmers Edge etc. This combination of businesses earned $46 million in 2023. I expect earnings to be better in 2024, coming in at $150 million. This bucket is poised to grow nicely for Fairfax in the coming years. It could surprise to the upside. Yes, the results will be lumpy. 7.) Interest expense: At $520 million, a modest increase to prior year of $510 million. 8.) Corporate overhead and other: At $435 million, a modest increase to prior year of $430 million. 9.) Net gains on investments: Estimated to come in around $1 billion in 2024. The big driver will be the FFH-TRS position. $250 x 1.96mn shares = $500 million? Remaining mark to market holdings of $7 billion x 7% return = $500 million? 10.) Gain on sale/deconsol of insurance sub: This is where I put the large asset sales/revaluations. In 2023, it was the sale of Ambridge and the revaluation of GIG for a total of $550 million. In 2024, I am modelling a gain of $300 million. Perhaps Fairfax (finally) gets approval from regulators in India to move their ownership in Digit from 49% to 68% and this generates a sizable gain. A Digit IPO might also result in a write up of Fairfax’s position. Bottom line, this bucket is a wild card. But Fairfax has a long history of surfacing significant value hidden on its balance sheet. $300 million per year seems like a conservative average estimate. I am including insurance and non-insurance here together (even though the title says insurance). 11.) Income taxes: estimated at 19% (historical average rate) 12.) Non-controlling interests: I am expecting Fairfax to take out one of its minority partners in 2024. The leading candidate is Brit. My second choice would be increasing their ownership in Allied World to 90% (from 83.4%). In the past, I used an average rate of 11% (amount of net earnings that was allocated to non-controlling interests). This has been reduced to 9.5% in 2024 and 7.5% in 2025. This change increases the amount of net earnings going to Fairfax shareholders. 13.) Shares Outstanding: Estimated that effective shares outstanding will be reduced by 300,000 shares per year for 2024 and 2025. This is the same amount as 2023. Notes: ‘Underwriting profit’: Includes insurance and reinsurance; does not include runoff or Eurolife life insurance. ‘Interest and dividends’ and ‘share of profit of associates’: Includes insurance, reinsurance and runoff. ————— Return on Equity Calculation Return on equity (ROE) is calculated below using ‘average equity’ which is: (PY ending BV/share + CY ending BV/share) / 2 I think most of the industry (other P/C insurance companies, analysts) calculate ROE using an average number for equity. So, this likely makes my ROE estimates more comparable with industry numbers.

-

@Hamburg Investor i agree that very low interest rates especially 2017-2020 negatively impacted the returns of the fixed income portfolio. The elephant in the room for Fairfax was the equity hedges / short positions. The equity hedges were in place from 2010-2016 and the last short position was removed in 2020. Over an 11 year period (2010-2020) these collective positions lost Fairfax an average of $494 million per year. This is when Fairfax was a much smaller company. Fairfax got the position size wrong. And the duration. That was straight out bad investing. I have also talked an nauseam about the many terrible equity investments made from 2014-2017. The first investment in Eurobank ($444 million - went to zero). Commercial International Bank - Egypt ($330 million - opportunity cost - dead money for a decade), Exco Resources, Fairfax Africa. APR, Farmers Edge and AGT. All of these investments performed poorly after purchase. Many needed more money from Fairfax to keep the lights on. A few needed more money multiple times. Some of these investments also needed management help. What i have listed here are a collection of terrible investments. And not because of zero interest rates or any external factor. Fairfax messed up. At the time their equity selection process was badly flawed. IMHO, Fairfax’s issues had nothing to do with value investing being out of favour. At the same time, Fairfax was doing lots of very good things. Insurance was growing like a weed. The pivot was made in insurance in India from ICICI Lombard (position was monetized) to Digit (start-up was seeded). Investments in India were performing well - Fairfax India was launched. It’s like Fairfax was suffering from some bipolar corporate disease from 2010 to 2017. Of course, not all investments are going to work out. Fairfax’s problem in 2017 is too many of its equity investments were sub-par (remember, Blackberry and Resolute Forest Products were some of legacy investments that were the big dogs back then). I think something changed at Fairfax in late 2017 or early 2018. It’s like Prem had finally had enough of the crap and bs with the equity holdings/process. From 2018 forward, Fairfax has put a premium on buying companies that were very well managed. And financially sound (i.e. not likely to need more cash from Fairfax to keep the lights on). At the same time, Fairfax looked at its existing equity holdings and saw them for what they were - and then Fairfax got to work to clean up the mess. I think Prem also delivered the message - new capital would now be allocated primarily to the best opportunities/managers (15% return target was now expected). Six years later it is amazing the progress that Fairfax has made. Today, as a group, the equity holdings are well run. And they are profitable - meaning they don’t need money from Fairfax to remain a going concern. They are using retained earnings to drive their growth. Fairfax is also using retained earning to make new purchases and drive new growth. 2024 might be an inflection point for the performance of the equity portfolio (as a group). Are there still a few issues? Yes. CIB still resides in Egypt. There will always be a few issues in every equity portfolio. But the issues are shrinking is size every year. And the flowers in Fairfax’s equity portfolio are blooming and getting bigger every year. And new flowers are getting planted. The quality of the insurance business has never been better. The quality of the equity portfolio has never been better. The bond portfolio is perfectly positioned. The management team is executing exceptionally well - capital allocation has been superb the past 5 years - regardless of what has been going on in the macro environment (actually they have been exploiting it). Size is not an issue for Fairfax (and shouldn’t be for the next decade). I am looking forward to seeing what kind of ROE Fairfax can deliver in the coming years - my guess is it will be better than most are thinking today. It really is stunning the turnaround they have pulled off the past 5 years.

-

Thanks for the heads up. This one looks large enough. I’ll likely add it tomorrow

-

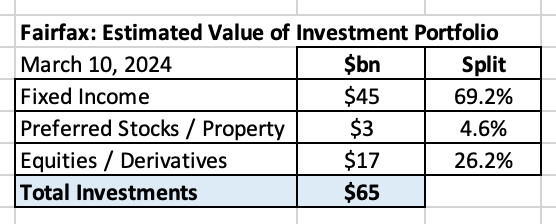

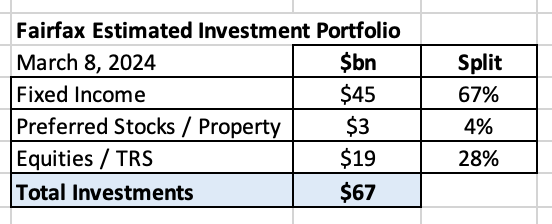

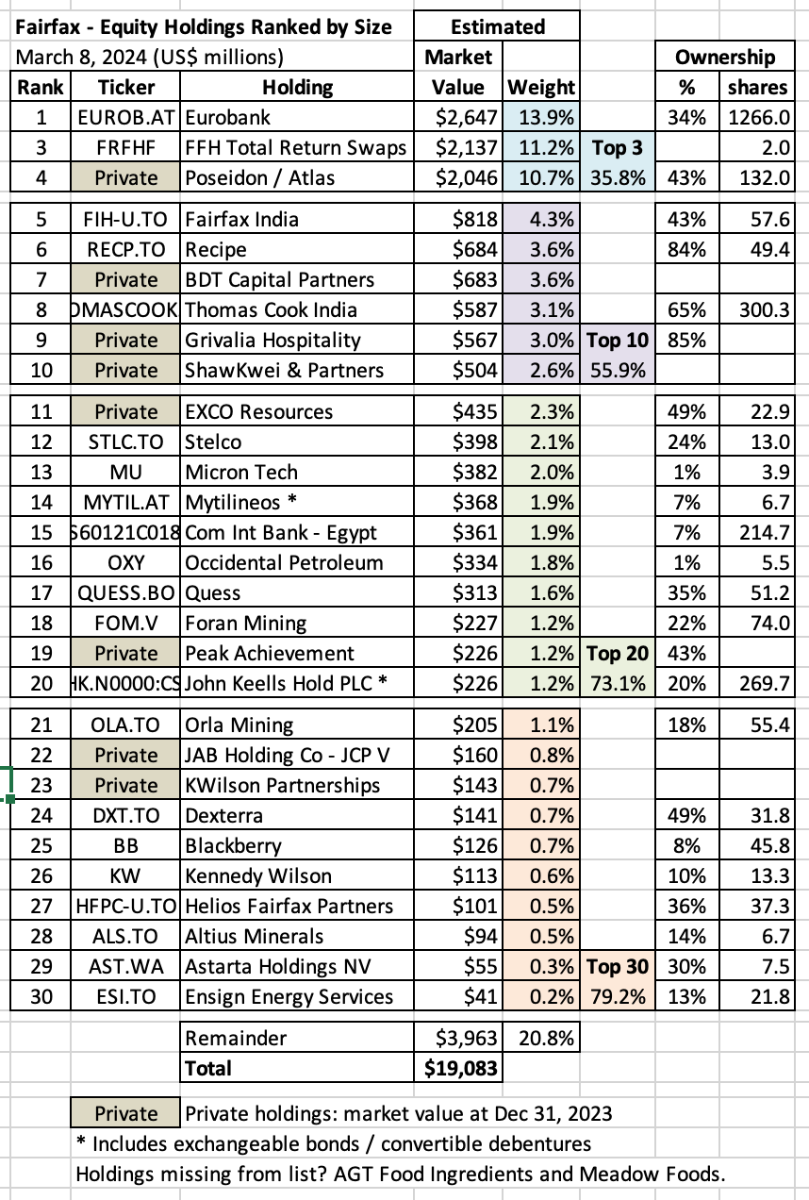

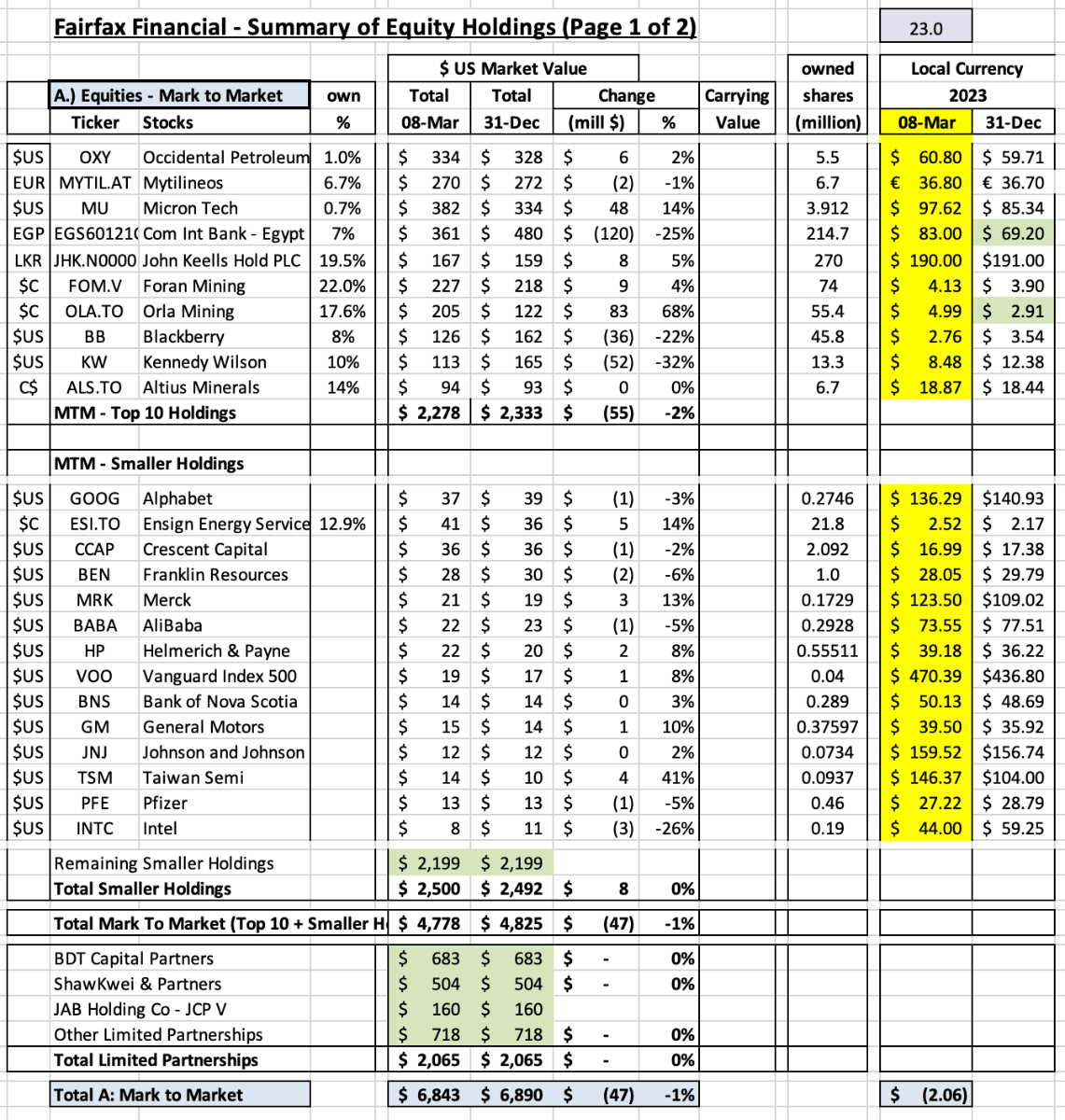

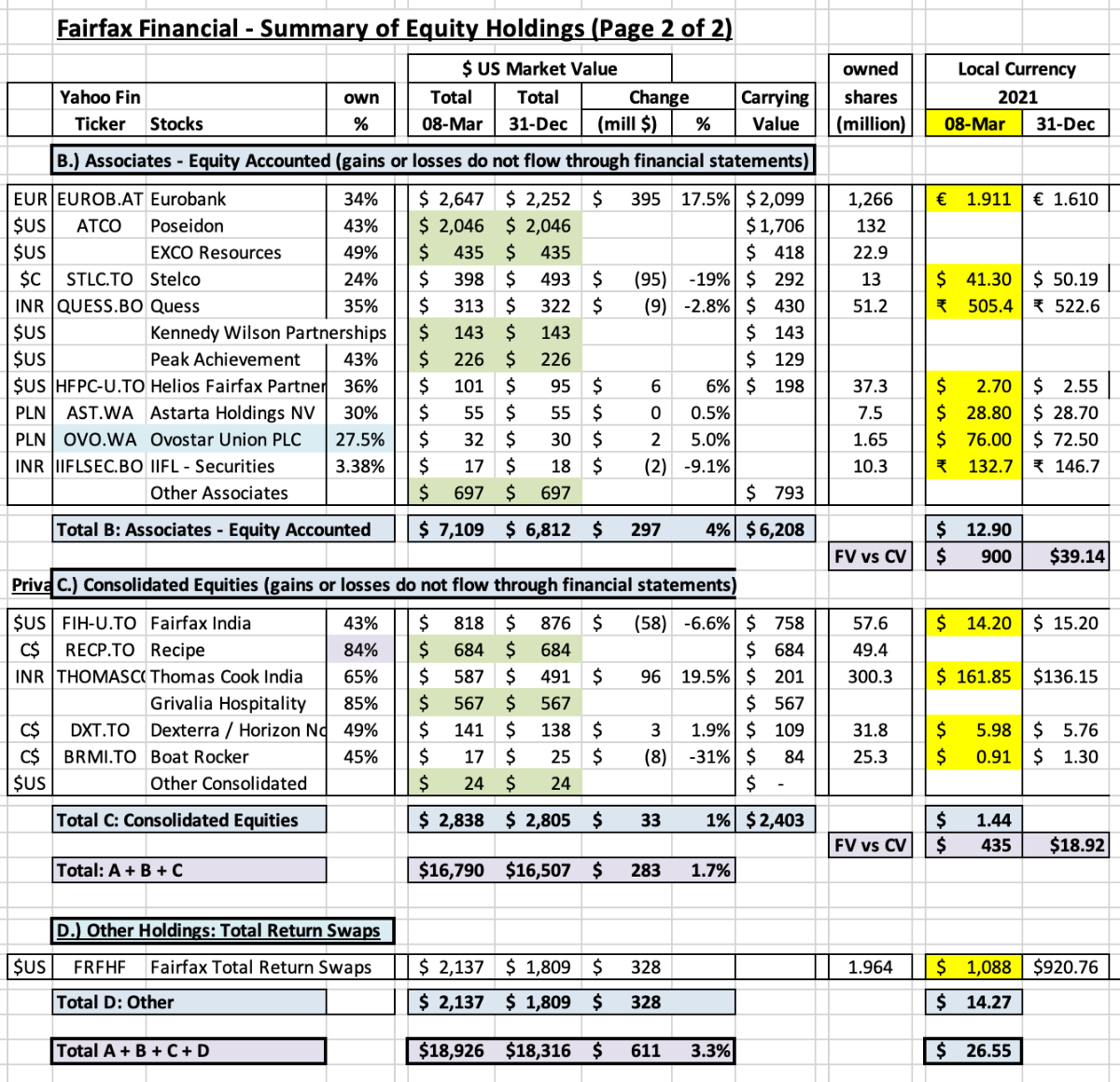

As of March 8, 2024, my guess is Fairfax has an investment portfolio that totals about $67 billion, with the split being roughly as follows: In this post we review the holdings in the equities ‘bucket.’ To value a holding, we normally use current ‘market value,’ which is the stock price at March 8, 2024, multiplied by the number of shares Fairfax owns. For private holdings we use Fairfax’s latest reported market value, which was Dec 31, 2023. Derivative holdings, like the FFH-TRS, are included at their notional value. Additional notes: Mytilineos *: includes exchangeable bonds John Keells *: includes convertible debentures What holdings are missing from my list below? AGT Food Ingredients and new purchase Meadow Foods (2023) are two that come to mind. I just have no idea what they are worth. Let me know if you have an estimate. Ok, let’s get to the fun part of this post. What are some of the key take-aways? Below are mine. What are yours? 1.) Fairfax has a pretty concentrated portfolio The top 3 holdings make up 36% of the total The top 10 holdings make up 56% of the total 2.) Steady improvement in quality of the top holdings over the past 6 years: What happened? New money has been invested at Fairfax very well (FFH-TRS, buying more of existing holdings) Some high quality businesses have continued to execute well (Fairfax India, Stelco) Some businesses, after years of effort, have turned around (Eurobank). Some businesses that were severely affected by Covid have emerged stronger (Thomas Cook India, BIAL) Some businesses were restructured/taken private (Exco, AGT) and are now performing much better. Some low quality businesses were sold/merged/wound down (Resolute Forest Products, APR, Fairfax Africa). Some low quality businesses have shrunk in size due to poor results (BlackBerry, Farmers Edge, Boat Rocker). The important point is the quality of Fairfax’s largest holdings have steadily been increasing. And this should result in higher overall returns from the equity portfolio in the coming years. 3.) What rate of return should this collection of equity holdings be able to deliver in 2024? 12% return x $19 billion = $2.3 billion share of profit of associates ($1.05 billion) dividends ($200 million) ‘other’ consolidated non-insurance co’s ($100 million) investment gains ($650) for associate holdings, change in excess of carrying value to market value ($300 million) This looks like a reasonable target for 2024, looking at the solid prospects/earnings profiles of the current holdings. 4.) A slow shift away from mark-to-market holdings. Today, less than 50% of the total portfolio is held in the mark-to-market bucket. Back in 2019, my guess is closer to 80% of the total portfolio was held in the mark-to-market bucket. This shift should have the effect of smoothing Fairfax’s reported results moving forward, especially during bear markets. As a reminder, in Q1, 2020, Fairfax had $1.1 billion in unrealized losses (when the equity portfolio was much smaller). As more holdings shift to the ‘Associates’ and ‘Consolidated’ buckets, it is the trend in underlying earnings at the individual holdings that will matter to Fairfax’s reported results and not a stock price - earnings are much more consistent than a stock price. Lower volatility in reported earnings should help Fairfax’s valuation (as volatility is considered bad by Mr. Market). This shift will also start to create a Berkshire Hathaway problem for Fairfax: over time book value will become an increasingly poor tool to use to value Fairfax. Why? The value of the ‘Associates’ and ‘Consolidated’ companies captured in book value each year will fall short of the increase in their true economic value. Fairfax India is a good example of this today. Eurobank is a holding to watch moving forward. Bottom line, Fairfax looks very well positioned today. But the story gets better: like the past 6 years, I expect the quality of Fairfax's equity holdings to continue to improve in 2024. That will improve future returns. And, like a virtuous circle, the growing cash flows will be re-invested growing the companies even more. Thoughts? Am I missing something? What number below is most wrong? Why?

-

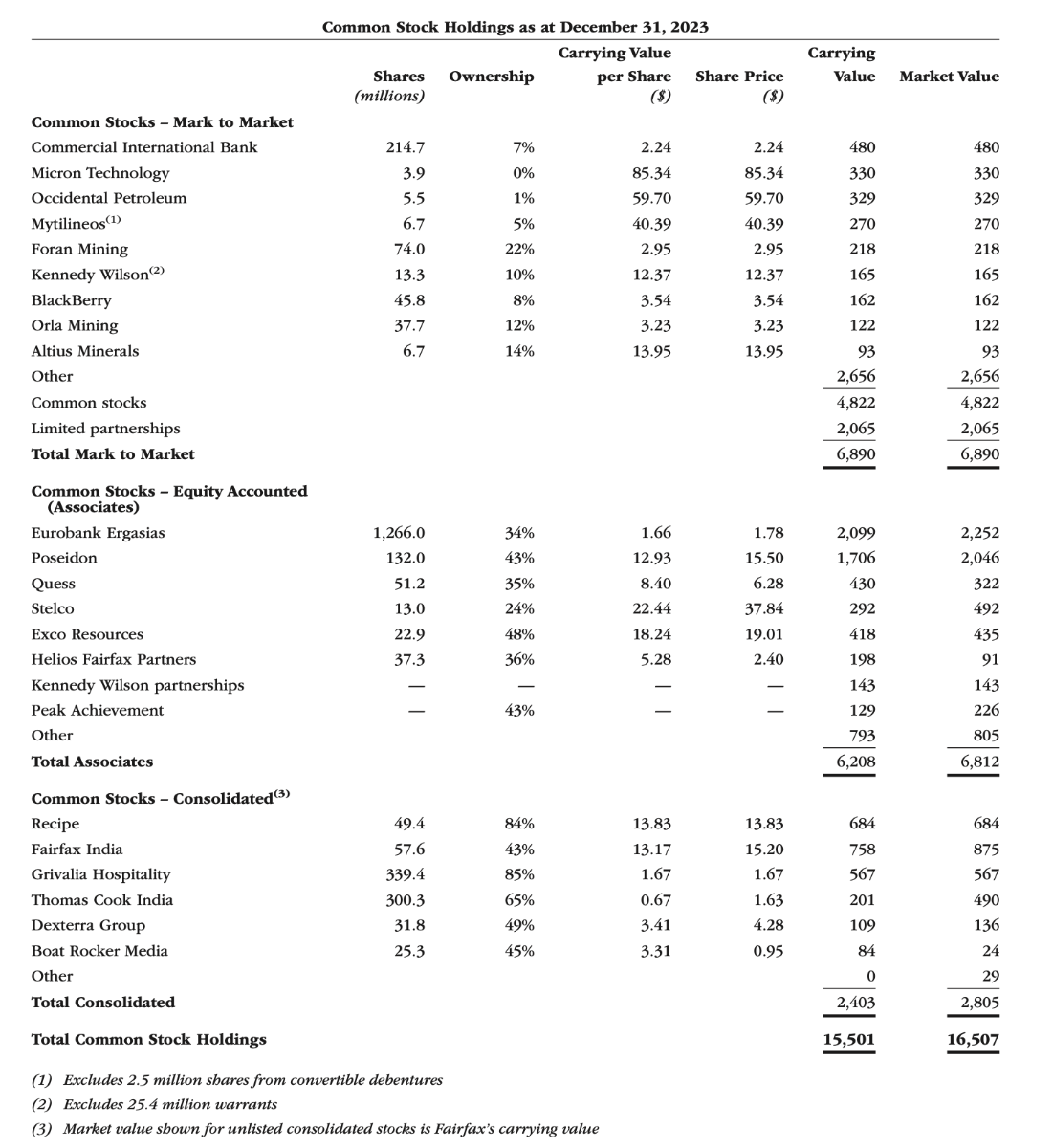

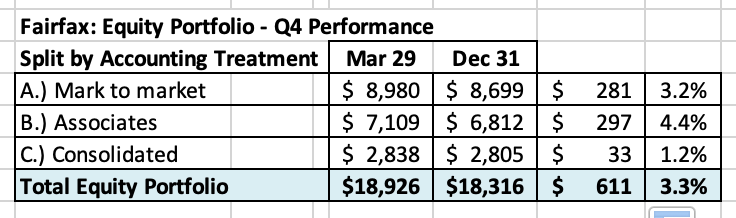

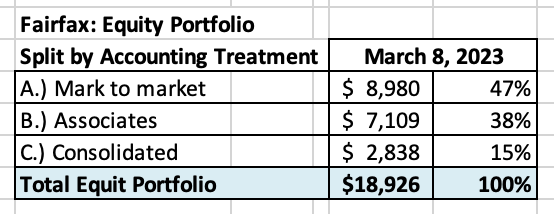

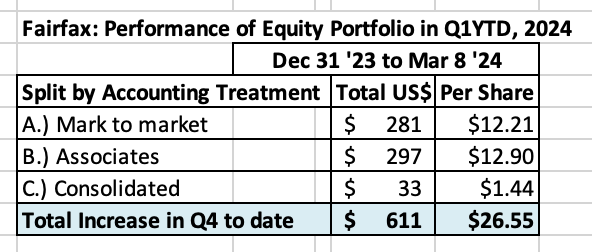

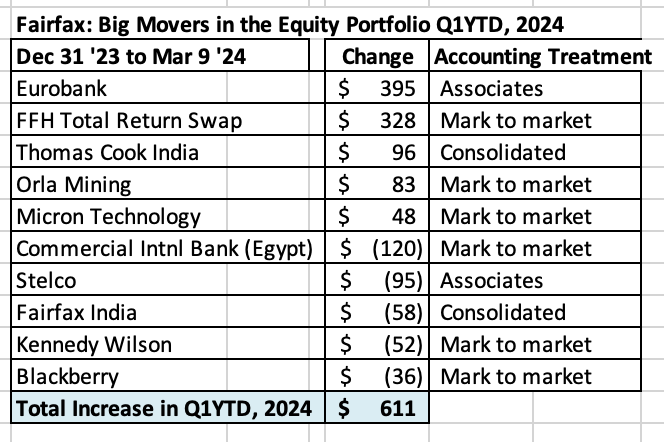

Now that Fairfax's annual report is out I am able to update a few things. I thought I would start with the equity holdings. The AVLN position (from the Riverstone UK sale) was completely exited by year end 2023. As a result, the significant noise from this holding has been eliminated. We now have a clear view of exactly what Fairfax's position is in its various equity holdings. I wonder how much Fairfax spend exiting the AVLN position in 2023? My guess is it was a significant use of cash. ---------- What was the change in value of Fairfax’s equity portfolio to March 8, 2024? March 8, 2024 Fairfax’s equity portfolio (that I track) had a total value of about $19 billion at March 8, 2024. This is an increase of about $611 million (pre-tax) or 3.3%. I include the FFH-TRS position in the mark to market bucket and at its notional value. My tracker portfolio is not an exact match to Fairfax’s actual holdings. My summary has been updated to include information from Fairfax’s 2023 annual report. My tracker portfolio is useful only as a tool to understand the rough change in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 47% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 53% are Associate and Consolidated holdings. Over the past couple of years, the share of the mark to market portfolio has been shrinking. This means Fairfax's quarterly results will be less impacted by volatility in equity markets. Split of total gains by accounting treatment The total change is an increase of $611 million = $26.55/share The mark to market change is an increase of $281 million = $12.21/share. The change in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports results each quarter. What were the big movers in the equity portfolio Q1-YTD? Eurobank is up $395 million and it is now Fairfax’s largest equity holding at $2.6 billion. The FFH-TRS is up $328 million. This position is now Fairfax’s second largest holding. Thomas Cook India is up 96 million. TCIC continues its strong performance. Commercial International Bank is down $120 million. Egypt devaluated its currency 40% on March 7. Well run bank. Country is an economic mess. Excess of fair value over carrying value (not captured in book value) For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1,335 million or $58/share (pre-tax). Book value at Fairfax is understated by about this amount. Associates: $900 million = $39/share Consolidated: $435 million = $19/share Equity Tracker Spreadsheet explained Holdings have been separated by accounting treatment: mark to market, associates – equity accounted, consolidated, other Holdings – total return swaps. We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. This spreadsheet contains errors. It is updates as new and better information becomes available. Fairfax Mar 8 2024.xlsx

-

I just listened to the Eurobank 2023 YE conference call. Their aggressive actions the past 3 years have positioned the bank exceptionally well. They are being very conservative with their estimates for 2024-2026. They have so many catalysts to boost earnings over guidance in 2024 and future years. The management team is laser focussed and is executing very well. Why is Eurobank being so conservative? 1.) They need to get the Hellenic Bank acquisition approved by regulators. Status quo is the best way to do this. Cypress is a different country… and local people tend to be very protective of critical institutions like banking. 2.) Once approved, Eurobank will need to make a mandatory tender offer for the @45% of Hellenic Bank they do not own. So obviously Eurobank doesn’t want to drive the acquisition price even higher (by announcing big cost and revenue synergies prematurely). Once Cypriot regulators approve the deal and after they own as much of the company as they can get - only after this happens - will Eurobank management more freely communicate on cost and revenue synergies. At least that is how things look to me. They are keeping their head down for now. Smart. On the dividend, Eurobank expects to get confirmation from the regulator in May. They provided an estimate of €0.09/share. Fairfax owns about 1.224 billion shares. €0.09 x 1,224 million shares = €110 million = US$120 million. That would be a material increase in total dividends received by Fairfax (from all sources) - perhaps an increase of about 80%. It would also be a material increase to ‘interest and dividends’ (from all sources) of about 5% - significant. In Fairfax’s 2021 Annual Report, Prem mentioned that the average cost of Fairfax’s position in Eurobank was US$0.94/share = $1.1 billion. Fairfax made their first investment in Eurobank in Dec 2014. So, about 9 years later Fairfax could be getting a dividend yield of about 11% (from its cost base). And as @nwoodman pointed out earlier, this could increase quite a bit in the next couple of years. The Eurobank acquisition has delivered other significant benefits to Fairfax over the years - like their 80% ownership of Eurolife (Eurobank stills owns 20%). I don’t have a strong opinion on how Grivalia Hospitality is going to work out (Eurobank and GH management still owns 21.5%). But anything George Chryssikos has touched has worked out very well for Fairfax and its shareholders. Link to Eurobank’s conference call: https://www.eurobankholdings.gr/en/investor-relations/financial-results-pages/financial-year-2023 PS: my share count is different from @nwoodman . I will update my numbers after Fairfax releases their annual report.

-

What a simply amazing year for Eurobank. Transformational. Their website is painfully slow right now? Below is a link to their full year results presentation. I think Eurobank is sandbagging their 2024 estimates. And that is the sign of a strong management team - underpromise and overdeliver. That is the same playbook they used in 2023 and 2022. They do not feel any pressure to be overly aggressive with financial targets. I am looking forward to seeing details of what the 25% payout (of 2023 baseline earnings) will look like - what the split is between dividend and stock buybacks. Eurobank is a $2.5 billion position for Fairfax today. A 15% return = $375 million; 20% = $500 million. This investment has quickly turned into a home run for Fairfax. And i think it is just getting started. A double in the stock price over the next 4 years is not a crazy target. https://www.athexgroup.gr/documents/10180/7345283/64_1619_2024_Greek_+English_3.pdf/eb92609a-213d-4272-91a7-435f35389bb4

-

I would expect any help that comes from Fairfax India will be structured in a way that is very beneficial to Fairfax India. Perhaps a similar playbook to how Fairfax helped out Thomas Cook India during Covid and John Keells during Sri Lanka’s economic crisis. A couple of years later, both of those incremental investments have worked out very well for Fairfax shareholders. It’s almost like a kind of vulture investing… except in a situation you understand exceptionally well. Fairfax’s ownership in IIFL Finance has come down quite a bit over the past couple of years. Fairfax sold all of their direct ownership position. And in Q4 2023, Fairfax India sold a big chunk of their stake (i think it raised around $150 million). Fairfax also exited their direct holding in sister company IIFL Wealth. And i think Fairfax India has sold down their position quite a bit as well.

-

@gfp Thanks. My master has been updated. My math says they have spent about US$61 million in Jan/Feb adding to their Orla position. It is about a $183 million position today.

-

@giulio that is a great article. I will update my spreadsheet to capture the new news. I really appreciate you (and everyone) pointing out things i have missed. Great community.

-

@dartmonkey i made the correction. Thanks for pointing it out (accuracy is important). I think lots of investor are very happy to see Fairfax significantly shrinking its investment/involvement in Blackberry. Moving in the right direction.

-

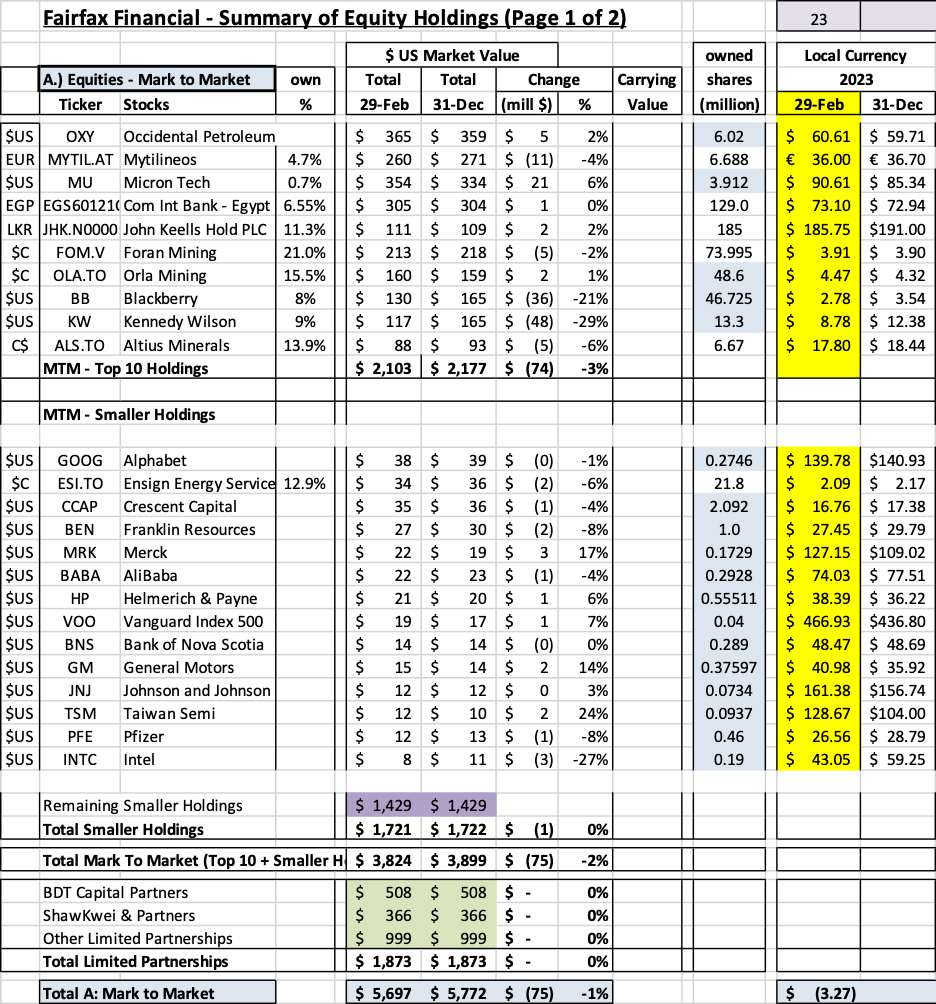

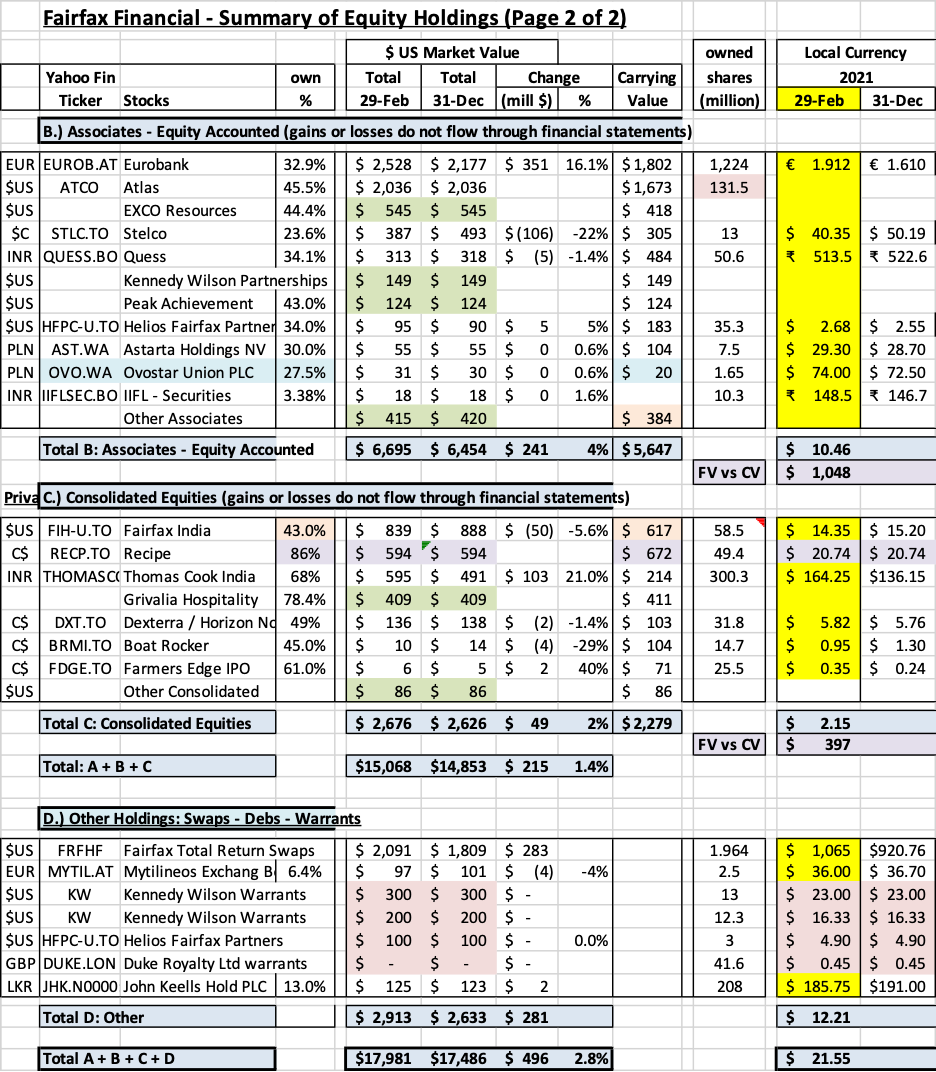

What was the change in the value of Fairfax’s equity portfolio to Feb 29, 2024? Fairfax’s equity portfolio (that I track) had a total value of about $18 billion at February 29, 2024. This is an increase of about $496 million (pre-tax) or 2.8% from December 31, 2023. The increase two months into Q1 works out to about $21.45/share. I include holdings like the FFH-TRS position in the mark to market bucket and at its notional value. I also include debentures and warrants in this bucket. My tracker portfolio is not an exact match to Fairfax’s actual holdings. My summary contains no information from Fairfax’s 2023 annual report, as it has not been released yet. As a result, my tracker portfolio is useful only as a tool to understand the likely directional movement in Fairfax’s equity portfolio (and not the precise change). Split of total holdings by accounting treatment About 49% of Fairfax’s equity holdings are mark to market - this includes 'A.) Mark to Market' and 'D.) Other Holdings' - and will fluctuate each quarter with changes in equity markets. The other 51% are Associate and Consolidated holdings. Over the past couple of years the share of the mark to market portfolio has been falling. This means Fairfax's quarterly results will be less impacted by volatility in equity markets. That is an important development. Split of total gains by accounting treatment The total change is an increase of $496 million = $21.55/share The mark to market change is increase of $206 million = $8.94/share. Only changes in this bucket of holdings will show up in ‘net gains (losses) on investments’ (along with changes in the value of the fixed income portfolio) when Fairfax reports results each quarter. What were the big movers in the equity portfolio Q1-YTD? Eurobank was up $351 million and it is now Fairfax’s largest equity holding at $2.5 billion. Eurobank reports results March 7. It will be interesting to see if they initiate a dividend. The FFH-TRS was up $283 million. This position is now Fairfax’s second largest holding. The investment is up a total of $1.356 billion over the last 3 years, which is a gain of 185%. Simply an amazing investment. Thomas Cook India delivered a very strong Q4 to cap off a stellar 2023. Fairfax’s position was up $103 million. People are travelling again in India! Kennedy Wilson was down $48 million. The company has been hit hard by concerns in office real estate segment. The value to Fairfax from this holding is not its equity exposure. The value is the extensive partnership the two companies have established over the past 12 years, most recently in significantly expanding the real estate debt platform. I wonder if Fairfax does not use the current weakness in KW's share price to materially and opportunistically increase its stake in the company in 2024. That was the playbook Fairfax used with a number of holdings that were negatively impacted by Covid in 2020 - and these incremental investments have worked out extremely well for Fairfax a couple of years later. Blackberry continues to shrink in size, down $36 million. Blackberry is now a $130 million position = 0.21% of Fairfax’s $60 billion investment portfolio. In Q1, Fairfax also ended its $150 million debenture investment in Blackberry and Prem resigned from Blackberry’s board. The debenture was a $500 million dollar position in Sept 2020. This is another good example of Fairfax exiting from a poorly performing legacy investment (financially and also in terms of involvement from the management team). Capital at Fairfax continues to shift to better opportunities. The clean-up of poorly performing equity investments looks largely completed – understanding that there will always be a few underperformers. Excess of fair value over carrying value (not captured in book value) Carrying value in this section is understated by quite a bit as it does not capture Q4, 2023. I will update this once the annual report is released. For Associate and Consolidated holdings, the excess of fair value to carrying value is about $1.445 billion or $62/share (pre-tax). Book value at Fairfax is understated by about this amount (less the tax impact). Below is the split. Associates: $1.048 million = $45/share Consolidated: $397 million = $17/share Below is a copy of my Excel spreadsheet (next 2 pages) if you want a closer look. Equity Tracker Spreadsheet explained: The summary below attempts to track all equity holdings at Fairfax. Each quarter the spreadsheet is updated to capture any ‘new news:’ purchases and sales. We have separated holdings by accounting treatment: Mark to market Associates – Equity accounted Consolidated Other Holdings – derivatives (total return swaps), debentures and warrants We come up with the value of each holding by multiplying the share price by the number of shares. Are holdings are tracked in US$, so non-US holdings have their values adjusted for currency. Important: the list is not complete. Some information we only get once per year when Fairfax published their annual report. Fairfax also makes changes to their portfolio each quarter. Fairfax Feb 29 2024.xlsx

-

Berkshire Hathaway has been one of the great investments of the past 60 years. We all knew Buffett was a genius. The business model was genius (using float from P/C insurance operations as cheap leverage). The company (outside of Buffett) was well managed. So why did so many people not get rich from owning Berkshire stock? What were the main reasons investors missed out on making big money? I have been asking myself this question recently. I have followed Berkshire Hathaway more than most over the past 30 years. i owned shares a number of different times in the past and have done ok with it as a trade. But i missed out on making the big money. I would appreciate hearing what others have to say. Did you nail your investment in Berkshire Hathaway? What enabled this? Or more likely, did you miss out on making a killing in Berkshire Hathaway? What did you do wrong? My obvious error was not owning a concentrated position and holding for decades. But that explanation doesn’t really explain anything that is useful. I think my big errors were: 1.) not understanding the power of compounding - in a Berkshire Hathaway context. My expectations of the future returns for BRK were much too low (how fast new income streams could be created from retained earnings). This led me to mis-value the stock. 2.) being too much of a market timer / trader - happy to take a quick short term gain. The reason i think about this question so much is I do not want to make the same mistake with Fairfax.

-

Buffett is a master communicator. He just lowered the expectations bar significantly for the future returns for two of Berkshire’s largest businesses - railroad and energy. This will be a big, big benefit to Abel when he takes over. Just imagine the outcry if Abel has said this post Buffett?

-

With the size of earnings at Hellenic Bank, it must be disappointing for minority shareholders to not get a big dividend payout right away. With all the cash building at Hellenic Bank, does this mean Hellenic will actually be able to fund a big piece of the takeout of the minority partners? W ————— Banking in Cypress is a duopoly with Hellenic Bank and Bank of Cypress with something like 80% share in most important categories when combined? Here are the results from Bank of Cypress - also outstanding. https://www.stockwatch.com.cy/en/article/trapezes/bank-cyprus-posts-almost-eu05-billion-net-profit-2023

-

My math says Eurobank paid an average of €1.78 to acquire 55.3% of Hellenic Bank over the past couple of years (awaiting regulatory approvals to become majority owner). In 2023, Hellenic Bank earned €0.88/share. Tangible book value at Hellenic Bank is €3.54/share at Dec 31, 2023, up 35% year over year. This is looking like a great investment by Eurobank. - https://www.hellenicbank.com/-/media/hbc/announcements/2024/february/12m2023/commentary-en.pdf

-

@Hamburg Investor Yes, i like to look at Fairfax in lots of different ways. None on their own are perfect. But looked at together, i think it is possible to sketch a pretty accurate picture of the company and its valuation. One of the lesson’s for me with Fairfax over the past couple of years is how long it takes for narratives to change for companies. Even when the facts are clearly saying something quite different. This is actually good news for investors. In situations where fundamentals are improving faster than what is being reflected in the narrative it means you have lots of time to learn and get your position size right.