Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@dealraker , did you get an answer? Because that was one of the questions I had preparing this post... (I always thought he - the Markel family - still owned a bunch).

-

@73 Reds , I think a 'buy and hold forever' approach has serious drawbacks. Buffett's successors are going to inherit some big problems. The more I think about it the more I think a mix is needed: Buy and hold forever Buy low and sell high (more classic Graham) My guess is Fairfax views P/C insurance as buy and hold forever, with the caveat that they will sell businesses like pet insurance, if they offer is stupid high. Bottom line, I like that Fairfax - when it comes to capital allocation - have not painted themselves into any corners. Gaynor, it trying to clone Berkshire Hathaway is painting himself (and Markel) into corners - that seems kind of dumb to me...

-

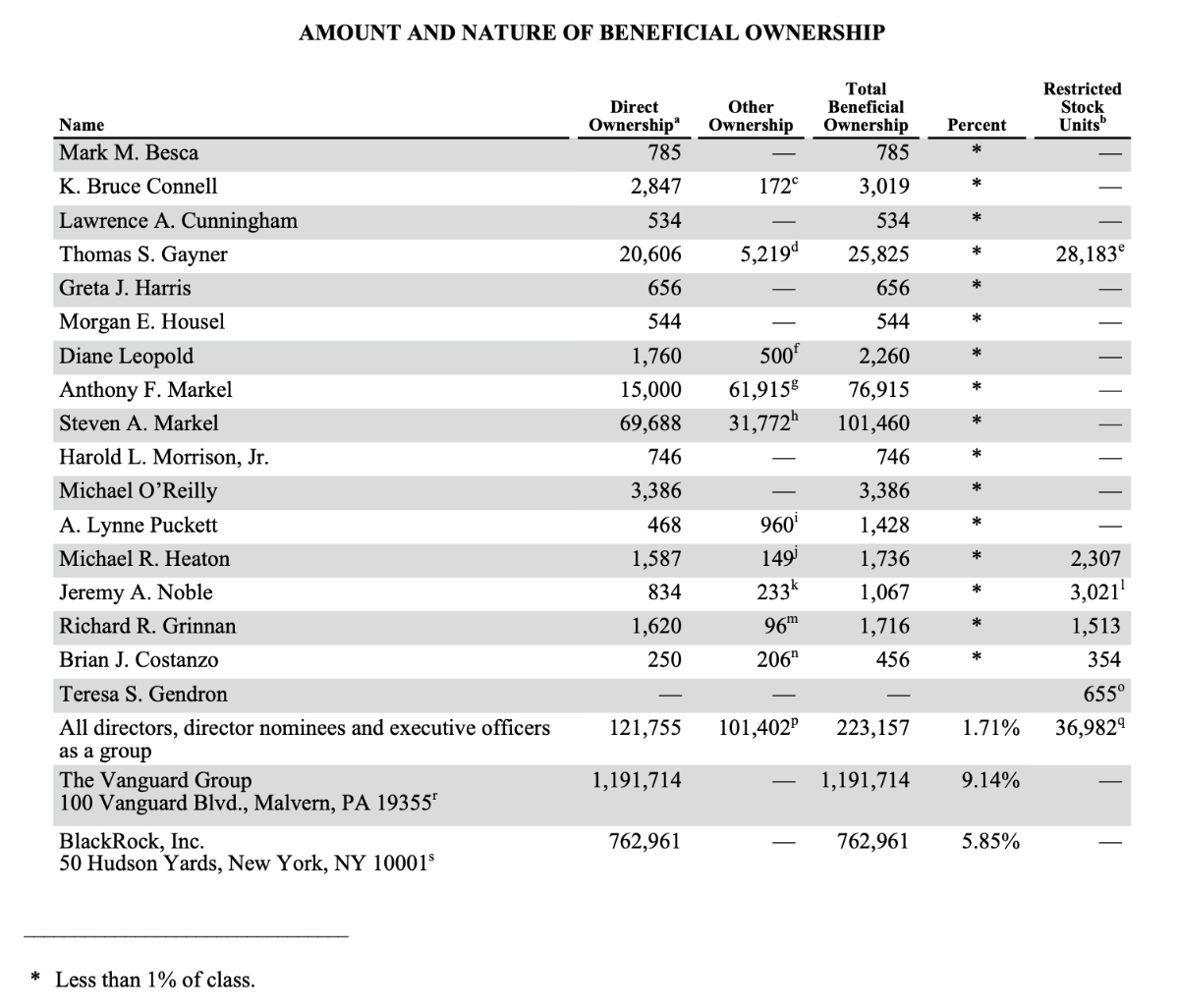

Part 2 of our long post on Markel... What is really going on at Markel? I think there are two root causes to Markel’s current issues: Succession planning gone wrong. Loss of family control. The first one should be fixable. The second, not so much. Both will have important implications for Markel’s future. Succession planning gone wrong For decades, Markel was exceptionally well run. It had a pretty simple formula: A leading specialty insurance business + invest wisely (Gaynor’s long term record investing in equities has been very good). But the last 8 or 9 years? It appears Markel is having a bit of a midlife crisis. It has lost its way in its core specialty insurance business. And it is trying to build a third stool to its business - Ventures - and become a conglomerate like Berkshire Hathaway. Markel’s struggles today highlight the difficulties and the importance of transitioning from a founder led company to a non-founder led company. Clearly, something has been lost. Hopefully Markel is able to figure it out. But hey, at least Markel is still controlled by the Markel family. So they will be given the time needed to right the ship. Right? Wrong. This used to be the case. This is no longer true. Loss of family control How much of Markel does the Markel family own? At March 14, 2024, the two Markel brothers (Anthony, age 82 and Steven, age 75) owned/controlled 178,375 shares, which is about 1.3% of total shares outstanding (13.8 million). The two Markel brothers also seem to be slowly selling shares each year, which is interesting. All directors, directors nominees and executive officers as a group owned 1.7% of Markel’s outstanding share (at March 14, 2023). Needless to say, from a stock ownership perspective, I think it is safe to say that the Markel family is no longer in control of Markel. (Source - From notice and proxy statement for Markel’s 2024 annual meeting) It is interesting to compare this to Fairfax. Prem’s economic ownership stake in Fairfax is about 9.5%. And his voting control position is more than 40% (due to multiple voting shares). He is also grooming his son/daughter. Fairfax will continue to be a family controlled company for the foreseeable future. But what about Berkshire Hathaway? Is Buffett not giving most of his shares to various charities? Who will be selling chunks every year? Bottom line, it doesn’t look to me like Berkshire Hathaway will have a controlling shareholder. Especially 10+ years after Buffett is gone. Now maybe the sheer size of Berkshire will act as a deterrent to activist shareholders. Or maybe it will be a catalyst - the short term financial rewards of breaking up Berkshire Hathaway could be huge (especially if the company - like Markel - hits some pot holes and begins a stretch of underperformance). ————— The question that is usually asked is the following: ‘Is family control a good thing?’ With what is going on with Markel today, perhaps the better question is: ‘Can the business model survive without family control.’ My view is Markel’s current business model (investing in equities and Ventures) requires family control to be sustainable over the long run. The equity part of the equation is hard enough. There is a reason other P/C insurance companies don’t do it - despite the fact that it will deliver higher returns than a bond only portfolio over the long run (if done well). But trying to also build out a Ventures portfolio - that is even more difficult. These investments are much more illiquid and much of the value creation is not captured in accounting results (EPS and BV) in the short term. Once again, we can look to Buffett for guidance. “Our equation is different. With 47% of Berkshire’s stock, Charlie and I don’t worry about being fired, and we receive our rewards as owners, not managers. Thus we behave with Berkshire’s money as we would with our own. That frequently leads us to unconventional behavior both in investments and general business management.” Buffett Shareholder Letter - 1984 Buffett is telling us that having a control position is what gives him the peace of mind/ability to invest in equities and to buy entire businesses. He is the GOAT. And he thinks this is important. And that is because Buffett understood that investing in equities was volatile - and could result in short term underperformance (short term = a couple of years). At the same time, he also understood that when buying control positions, it might take 5 or more years for the economic value to be reflected in the accounting results (eventually showing up in investment gains). But because he had a control position, he was able to make decisions that he knew would pay off in the long term. Gaynor is good… but he s no Buffett. When it comes to buying both equities and buying control positions. If Markel’s share price underperforms for a few years… well, the Wall Street vultures will probably start clamouring for change… and for value to be surfaced. And what do you know… that is exactly what seems to be playing out today. Now that the Markel family is no longer in control of Markel, having an equity heavy investment portfolio will likely be challenging enough - very strong equity market returns the past 2 years have provided a reprieve (and likely inflated BV at YE 2024)… but another bear market in stocks is coming. What will Jana (and the rest of Wall Street) say when that happens? The Ventures part is the real head scratcher (with no family control). It looks to me like the decision to grow Ventures might prove to have been a strategic mistake. But there is another related problem. Buy and hold forever Over time, economic value that has been created will show up in accounting results - via capital gains. But buy and hold forever slows this process down. This has not been a problem for Buffett. He has created so much value, that if some of it is not recognized right away… well, who cares. But, as we said earlier, Gaynor is not Buffett - his results will not be nearly as good. He can’t afford to wait like Buffett. This is not a criticism of Gaynor… no one will be as good as Buffett. But for Gaynor to want to clone Buffett in this regard… well that is a problem. Markel will look like it is underperforming compared to peers. And that will not sit well with Wall Street or Markel shareholders. I much prefer Fairfax’s approach in this regard. It is more classic Graham. Buy stuff when it is cheap. Sell it when it is expensive. Rinse and repeat. Importantly, this strategy more quickly/continually surfaces the significant economic value that is building on Fairfax’s balance sheet with its equity and control positions. And once it shows up in accounting results (EPS and BV) it gets reflected in the valuation of the company and the share price. ———— Another Mistake made - historic bond bond bubble / bear market If we are going to discuss mistakes made at Markel in recent years, we need to discuss one more forced error. Most P/C insurance companies made this same error. Because most everyone did it… well, it is something not usually discussed today in polite company (especially among analysts). Markel has a ‘policy’ of matching the average duration of its bond portfolio with the average duration of its insurance liabilities. This kind of makes a lot of sense most of the time. When does it not make sense? When a historic bubble in bonds is blowing. Like what we saw in 2020 and 2021. The 5 year US Treasury traded at a yield below 40 basis points for much of 2020. The 10 year treasury traded at a yield below 70 basis points for much of 2020. What were P/C insurance companies doing in 2020 and 2021? They were busy buying bonds - and making sure they were matching the maturity to their insurance liabilities. If that meant buying the 5 year US Treasury at a yield of 0.5% that is what they did. Because they were prudent insurance companies, after all, not market timers or ‘macro’ investors (that would be terrible). What were P/C insurance companies missing? Apparently they did not understand some arcane concept called duration risk. What was the mistake? When interest rates went to zero (across the curve) in 2020 and 2021, investors were not getting paid for taking on duration. There was no margin of safety when purchasing bonds with duration. Taking on duration opened you up to significant losses - of a size large enough to impact the balance sheet. What happened in 2022? The inflation genie got out of the bottle and interest rates spiked higher. The value of bonds got torched, especially those with a longer duration. And because most P/C insurance companies invest primarily in bonds, their balance sheets got torched - with book value per share at most P/C insurance companies falling 10% to 20% in 2022. Yes, it wasn’t a solvency issue for most P/C insurance companies (although it could have been for some if 2021/2022 had been historically bad for catastrophes). Buffett talks about accounting value often being different from economic business value. Interest rates spiking in 2022 was a great example of serious destruction of economic value at P/C insurance companies - that was not reflected in the accounting results (like EPS and ROE). Buffett thought it was idiotic to buy duration in 2021. Why? Value investing 101. And this was not Buffett’s first rodeo with spiking interest rates… a similar thing happened in the mid 1980’s. He wrote about it in his shareholder letters then (and the damage it did to insurance companies balance sheets then). Gaynor is a value investor. He is trying his best to clone Berkshire Hathaway. He should have known better. Policies and procedures are good. But they can’t become a straight jacket. Or used as an excuse for lazy thinking. This is a judgement thing… and it does not look good on Gaynor. It cost Markel +$1 billion - in 2022 BV fell by 10% (and stunted growth in BVPS for years). Even today, their fixed income portfolio yield is low (3.2% for ‘fixed income securities’, which does not include ‘short term investments’ which is 4.8%) - the earn through of higher rates has been slow. Like Berkshire Hathaway, Fairfax recognized that bonds were in a bubble and investors were not being paid to take duration. In late 2021, Fairfax reduced the average duration of their fixed income portfolio to 1.2 years. In Q4, 2021, Fairfax sold $5.2 billion in corp bonds (acquired in March/April 2020) at yield of 1% and booked an investment gain of $253 million. BVPS at Fairfax actually went up in 2022. Some pundits have called what Fairfax did a ‘macro bet.’ It wasn’t. It was simple value investing. And basic risk management - protecting the balance sheet - something that is critically important to an insurance company. Especially at the beginning of a hard market. ————— What happens next? What will happen next with Markel? It is impossible to know. Nothing. Sell Ventures. Sell the whole company. Bottom line, it appears the company is in play. And Wall Street loves it. Fairfax (and Berkshire Hathaway) should be paying attention to what is going on at Markel today. Markel is providing an important teachable moment for Fairfax and Berkshire Hathaway, their boards (and their shareholders).

-

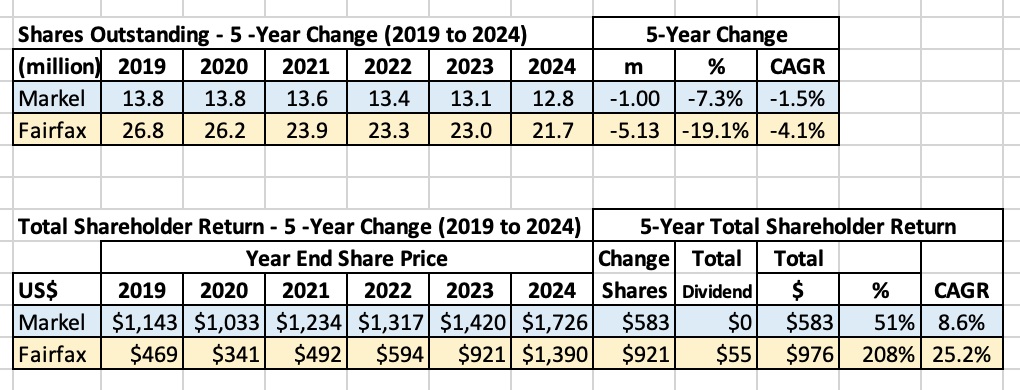

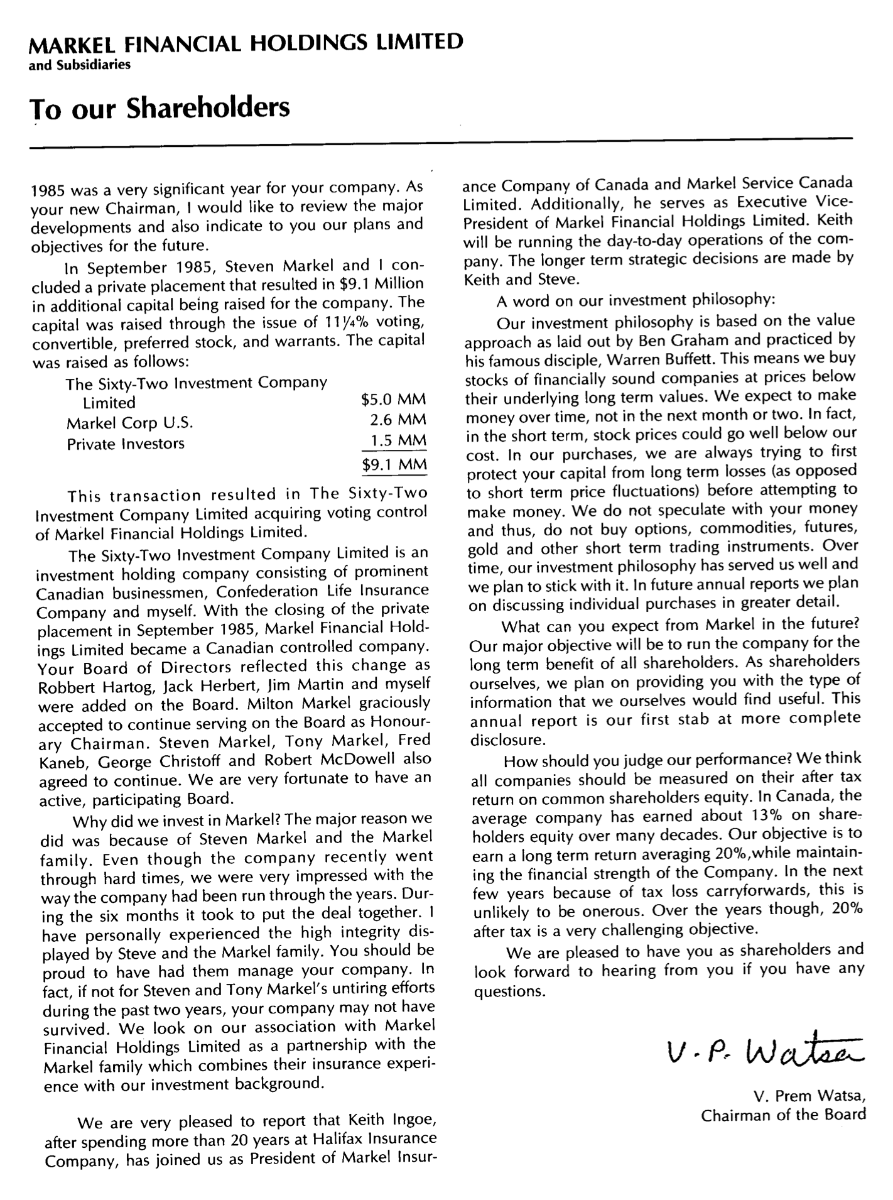

Markel - A Deep Dive I follow Fairfax very closely. Markel not so much. So you have been warned. What is happening at Markel today looks like it might be important. My thoughts below are very top-line. And subject to change as we get more information / see how things play out. I am putting this post in the Fairfax thread because I also weave Fairfax and Berkshire Hathaway into the story. Why should a Fairfax shareholder care about what is going on at Markel? There are two broad reasons for a Fairfax shareholder to pay attention to what is happening at Markel. The first is for practical reasons. Peers - It is important to follow other P/C insurance companies. This can provide important insights into what is going on in the industry in general (commentary on hard market, etc). Berkshire Hathaway / Markel - These two companies have business models that are closer to Fairfax’s than other P/C insurance companies. Among other things, they invest a large part of their investment portfolio in equities / control positions in other non-insurance companies. These two companies can provide an additional layer of insight. The second is for sentimental reasons. The history of Fairfax is closely intertwined with that of Markel, especially in the very beginning and first 15 years. ————— Let’s explore the second reason first. This will be short. Sentimental Of interest, Markel was responsible for Fairfax’s entry into the P/C insurance business 40 years ago. Fairfax actually started out as Hamblin Watsa, an investment counselling company, which was established in 1984. Prem teamed up with Tony Hamblin, who was his boss when he was working in the investments department at Confederation Life. In 1985, Hamblin Watsa (via The Sixty Two Investment Company), made their first P/C insurance purchase - a control stake in Markel Financial (Canada). Steven Markel (from Richmond, Virginia) was instrumental in getting this deal done and he agreed to help run the company until a new president could be found. The name change from Markel Financial (Canada) to Fairfax Financial happened in 1987. In 1990, the two businesses separated (Markel US and Fairfax). Until 1998, each (Steven Markel and Prem Watsa) served on the other's board. “I consider him (Steve Markel) one of the founders of Fairfax." Prem Watsa Source: Fair and Friendly - The First 25 Years of Fairfax Financial And as they say, the rest is history. There is much more to the Markel / Fairfax relationship / story. That would make for a fun and interesting future post. Let’s get back to our topic for today. ————— Practical Munger - invert "Be consistently not stupid, instead of trying to be very intelligent." Charlie Munger Inversion involves looking at a problem or decision from the opposite point of view so, for example, rather than focusing on achieving success, Inversion encourages you to consider how to avoid failure. https://modelthinkers.com/mental-model/inversion A good way to avoid failure is to learn from the mistakes of others. So you can avoid them. With that context, let’s now look at what is going on at Markel. ————— Below is a summary of what we will review in this post Markel Group - An update The activist appears Markel drops a bomb on (long term) shareholders Is a low share price the problem? What are the real problems at Markel? Succession planning gone wrong? Loss of family control? Another Mistake made - historic bond bond bubble / bear market What happens next? ————— Markel Group - An update Markel was listed on the NASDAQ exchange in December 1986 with an IPO offered at $8.33 per share. Today, the stock trades at about $2,000 per share. Over the past 39 years, the CAGR in Markel’s share price has been 15%, making it one of the top performing public companies. Outstanding. The Markel family was responsible for over seeing the majority of this run. Steven Markel currently serves as Chairman of Markel’s board. But something appears to have changed at Markel in recent years. And not in a good way. Markel appears to be making some mistakes. Most importantly, its crown jewel, specialty insurance, has been underperforming. In September, 2023, Insurance Insider did a deep dive into Markel and its business. It goes into detail of what Markel’s issues are. We have copied some of the key points below and provided a link to the article. “It’s a good business.” “However, the firm has made repeated missteps in its insurance M&A strategy, with a huge Wrong Side of History Bet on ILS in 2015-18, following on from a so-so deal for Bermudian Alterra and the challenged acquisition of Terra Nova. “Its US E&S business remains strong, but it has arguably lost something intangible that it once had (and Markel is a company that believes in the value of intangibles). Here, Markel chose diversification rather than doubling down just ahead of a Golden Age of US specialty. That choice was reflected in its decision to let Allied World – ultimately sold to Fairfax – go when takeover talks were held in 2016. “Crucially, the firm’s share price has underperformed since the Financial Crisis, lagging the stronger specialty insurers massively and also behind the S&P 500. Some of this likely reflects its desire to walk the Berkshire path of investor relations without the gravitational pull of Buffett, and some of the challenges of getting full value ascribed to its non-insurance “Venture” businesses when it reports as an insurance company.” Click the link below for details. Markel: Trying to be Berkshire without Buffett https://www.slipcase.com/view/inside-in-full-markel-trying-to-be-berkshire-without-buffett/3 ————— The activist appears In November, 2024, activist investor Jana Partners appeared on the scene. On December 14, 2024, CNBC (in an article by Kenneth Squire) provided a good summary of Jana and why they have targeted Markel. We have copied some of the key points below and provided a link to the article. “Jana is a very experienced activist investor founded in 2001 by Barry Rosenstein. The firm made its name by taking deeply researched activist positions with well-conceived plans for long term value. Rosenstein called his activist strategy "V cubed." The three "Vs" were" (i) Value: buying at the right price; (ii) Votes: knowing whether you have the votes before commencing a proxy fight; and (iii) Variety of ways to win: having more than one strategy to enhance value and exit an investment. Since 2008, the firm has gradually shifted that strategy to one which we characterize as the three "Ss" (i) Stock price – buying at the right price; (ii) Strategic activism – sale of company or spinoff of a business; and (iii) Star advisors/nominees – aligning with top industry executives to advise them and take board seats if necessary.” What is Jana calling for? “Jana called on Markel to improve its insurance operations and explore a separation or sale of its private investments business (Ventures). The firm also noted that the entire company presents an attractive acquisition target for larger insurers.” Click the link below for details. Activist Jana calls on Markel to focus on insurance. Here's how the firm can help create value https://www.nbcchicago.com/news/business/money-report/activist-jana-calls-on-markel-to-focus-on-insurance-heres-how-the-firm-can-help-create-value/3624425/?os=ios%2F%3Fno_journeystrue&ref=app ————— Markel drops a bomb on (long term) shareholders When Markel reported YE 2024 results on Feb 5, 2025, they also delivered a surprise ‘update’ for shareholders. Below are a few highlights: “…we believe the value and potential of our combined group of businesses is not fully reflected in our current stock price. “In December 2024, JANA Partners publicly shared their perspectives on Markel Group and offered suggestions we might consider. We took this as an opportunity for broader self-reflection, in line with our commitment to the ‘zealous pursuit of excellence.’ “…we have decided to conduct a review of our business. It will be an opportunity to reflect on the changes over the past two years and ensure our goals and direction align with our shareholders' priorities. “The board will lead this review, assisted by external consultants and advisors. Our foremost focus will be the performance of our market-leading specialty insurance business. Insurance is at the heart of what we do, and we're fully committed to supporting areas within insurance that are excelling while also addressing underperformance. “Additionally, as part of the review we will consider ways to simplify our structure, optimize our approach to capital allocation, and enhance our disclosures. During this period, we expect to focus capital deployment on repurchasing shares under the recently announced $2 billion stock buyback program.” Click the link below for the complete release. Markel Group Inc. provides update for its shareholders https://ir.mklgroup.com/investor-relations/news/news-details/2025/Markel-Group-Inc.-provides-update-for-its-shareholders/default.aspx ————— In November 2024, an activist investor shows up. And in February 2025, Markel announces they will be conducting a review of their business, with the help of external consultants and advisors. Holy shit Batman! External consultants and advisors? Really? I wonder what Charlie Munger would say? (I think I know…) Is this what well run companies do? Nope. Clearly, the board/senior team at Markel don’t know what to do. Or they do know… and they are unable to do it on their own. How did Markel’s shares respond to the ‘update’ provided by Markel? Of course, Wall Street cheered the news - the shares finished the day up 8%. The volume of shares traded tripled. It appears Wall Street is now in control of the company. And maximizing short term value for shareholders is the new objective. What about long term shareholders? Of course, Wall Street doesn’t give a shit about them. —————- So what is the big problem at Markel today? Well one of the lead lines in Markel’s press release was the following: “…we believe the value and potential of our combined group of businesses is not fully reflected in our current stock price.” The big problem appears to be a low share price. But is a low share price really a problem? No. A low share price is a gift. What? Says who? Some guy names Warren Buffett. Apparently, Tom Gaynor has never heard of this guy (Buffett), because if he had he would not be complaining about his share price being too low right now. Instead of complaining (and bringing in expensive ‘external consultants and advisors’ to tell him and the board what to do) he would be vacuuming up as many Markel shares as he could - and counting his lucky stars at his good future. But I can year you retort: ‘Markel is buying back shares.’ Yes, they have been buying back shares. But how much? Over the past 5 years Markel has reduced shares outstanding by 1.5% per year. Not much. Especially if you think your shares are dirt cheap (which Markel evidently does). Let’s look to Buffett again for guidance. "Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble." - Warren Buffett. Capital allocation 101 When your shares are dirt cheap, any self respecting value investor knows that is the time to back up the truck. Buybacks increase the per share intrinsic value for long term shareholders. And the action is low-risk / high certainty capital allocation activity. This is an example of jumping over a one foot hurdle. And the longer the shares stay cheap the better (or so says that Buffett guy). It just means management can buy back more. But Markel has just tipped its hand to Wall Street. And by announcing a ‘review’ they have also caused the stock to increase significantly in value. It’s like asking the grocery store to raise prices before you do your shopping. So now Markel gets to complete with Wall Street/short term traders for shares - which of course just means they will now be paying a much higher price. What about Markel shareholders? Isn’t a low share price good for them too? Especially if it stays low for a long time? Well, this is really only true if management at Markel isn’t asleep at the wheel - and is actually buying back shares - and in volume. Which they aren’t. So I guess that partly explains why some Markel shareholders are getting a little testy. And why an activist like Jana is getting the time of day from anyone. As an aside… Fairfax has had a similar problem - a share price trading well below its intrinsic value. Their solution? Over the past 5 years (2019 to 2024), they have bought back 19.1% of their shares outstanding, paying an average price of $630/share. They also got exposure to another 1.96 million via FFH-total return swaps at $373/share (meaning they effectively ‘took out’ 26.4% of shares outstanding at an average price of $560/share). From a capital allocation perspective, buybacks have been Fairfax’s biggest use of cash over the past 5 years. The per share value creation has been enormous (shares were purchased significantly below intrinsic value). Over the past 5 years, Fairfax’s has generated a total shareholder return of 208%, or a CAGR of 25.2%. As a result, Fairfax shareholders are pretty happy campers these days. Over the same time period, Markel has delivered a total shareholder return of 51%, or a CAGR of 8.6%. —— Buffett on share buybacks Below is what Buffett had to say about share buybacks in his 1984 shareholder letter (published February 1985). “The companies in which we have our largest investments have all engaged in significant stock repurchases at times when wide discrepancies existed between price and value. As shareholders, we find this encouraging and rewarding for two important reasons - one that is obvious, and one that is subtle and not always understood. “The obvious point involves basic arithmetic: major repurchases at prices well below per-share intrinsic business value immediately increase, in a highly significant way, that value. When companies purchase their own stock, they often find it easy to get $2 of present value for $1. Corporate acquisition programs almost never do as well and, in a discouragingly large number of cases, fail to get anything close to $1 of value for each $1 expended. “The other benefit of repurchases is less subject to precise measurement but can be fully as important over time. By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. This upward revision, in turn, produces market prices more in line with intrinsic business value. These prices are entirely rational. Investors should pay more for a business that is lodged in the hands of a manager with demonstrated pro-shareholder leanings than for one in the hands of a self-interested manager marching to a different drummer. “The key word is “demonstrated”. A manager who consistently turns his back on repurchases, when these clearly are in the interests of owners, reveals more than he knows of his motivations. No matter how often or how eloquently he mouths some public relations-inspired phrase such as “maximizing shareholder wealth” (this season’s favorite), the market correctly discounts assets lodged with him. His heart is not listening to his mouth - and, after a while, neither will the market.” —— Is a low share price really the problem at Markel. No, of course not. But it might be a symptom of bigger problems. To read part 2 - go to the next post in this thread (directly below).

-

@Buffett_Groupie, I just wanted to say… I really appreciated you asking the question you did at the AGM last April. That took a lot of guts. And you handled it with class. Fairfax needs to hear from shareholders like you - so they don’t get complacent. Especially now that they are on a hot streak. I look forward to chatting with you again at this year’s AGM!

-

With all the discussion around Markel lately, time for a trip down memory lane. Do you know what Fairfax Financial was actually called in 1985 (year 1)? Markel Financial. The name didn't change to Fairfax Financial until 1987. Of interest, the Markel family was responsible for Fairfax’s entry into the P/C insurance business 40 years ago. Fairfax actually started out as Hamblin Watsa, an investment counselling company, which was established in 1984. Prem teamed up with Tony Hamblin, who was his boss when he was working in the investments department at Confederation Life. In 1985, Hamblin Watsa (via The Sixty Two Investment Company), made their first P/C insurance purchase - a control stake in Markel Financial (Canada). Steven Markel (from Richmond, Virginia) was instrumental in getting this deal done and he agreed to help run the company until a new president could be found. It was only in 1987 that Markel Financial (Canada) changed its name to Fairfax Financial. (Source: Fair and Friendly - The First 25 Years of Fairfax Financial) And as they say, the rest is history. Below is Prem's first letter to shareholders. The really interesting thing to me is it reads like he could have written this letter today - I think that says something about the character of the man.

-

@gfp , thank you for the comment. (You know your stuff...)

-

@Maverick47, I learned lots from your post... As I am sure you can appreciate/recognize, sometimes I like to stir the pot. I get an idea / develop a thesis that I think might make sense and I throw it onto the wall at CofBF to see if it might stick. Feedback from other posters, like you, is much appreciated. It is great to be able to discuss important ideas/themes with smart people like you.

-

@This2ShallPass, after reading your comment, I remembered another important point mentioned by @nwoodman in the past - the importance of deal flow. My guess is Fairfax’s phone is ringing often these days. ————— I added the following paragraph to my post above: The many relationships/networks they have established also likely helps big time with deal flow ( @nwoodman has pointed this out before). My guess is Fairfax is viewed as being an ideal partner for other competent capital allocators (Fairfax wants to be a passive investor/partner). That is important with all the capital Fairfax will have to allocate in the coming year(s).

-

@Gregmal From the Markel thread “Yea but the insider ownership percentage at Berkshire ex-Buffett sucks!” ————— The question that most investors asked in the past was “Is having a controlling shareholder good or bad” for Berkshire Hathaway, Fairfax and Markel. It was heavily debated, especially when it came to Fairfax. But it looks to me like investors might have been asking the wrong question. The more relevant/immediate question might be: “Does BRK, FFH and MKL need a controlling shareholder to be able to execute their business model (investments in equities/control positions in businesses) over the long term.” I think the answer is likely yes. I think Buffett said as much in his 1984 shareholder letter (published Feb 1985). “Our equation is different. With 47% of Berkshire’s stock, Charlie and I don’t worry about being fired, and we receive our rewards as owners, not managers. Thus we behave with Berkshire’s money as we would with our own. That frequently leads us to unconventional behavior both in investments and general business management.” What’s interesting is we are kind of getting a teachable moment with Markel right now. Because they apparently no longer have a controlling shareholder (shows you how closely I have been following Markel). We will see what the ‘external consultants’ have to say. And what Markel actually does. Perhaps its all smoke… Family control is not an issue for Fairfax. Prem is grooming his son/daughter to take over one day. The Watsa family has voting control and that is not going to change. But what about Berkshire Hathaway? Is Buffett not giving most of his shares to various charities? Who will be selling chunks every year? Bottom line, it doesn’t look to me like Berkshire Hathaway will have a controlling shareholder. Especially 5 or 10 years after Buffett is gone. Berkshire Hathaway is a wet dream for activist private equity shops in the US - Berkshire Hathaway is an aging, massive conglomerate - the largest in history. Soon to be run by an unknown (Yes, Greg Abel is an unknown). Bagging Berkshire Hathaway would be like scaling Mount Everest. The short term rewards of breaking up Berkshire would likely be massive (its called ‘value creation’). Munger teaches us that incentives matter… activist private equity shops will be all horned up once Buffett is gone… waiting for their chance to pounce (likely together). Once they got started, and the numbers kept growing (value creation) and the stock started to move higher what could stop them? The money would be too big. What about long term shareholders? Who cares. When your job (CEO/senior management) is on the line… well, you fall into line. Especially if your performance has been sub-par for a few years. Markel’s stock popped 8% once they announced their strategic review. As a result, other than @bearprowler6 , i think Markel’s decision was widely applauded. Both the board and management at Markel have given it their full support. Long term? Who gives a shit right now. Let’s see what we can do to get that share price higher! Hello? Berkshire Hathaway shareholders are you paying attention?

-

@SafetyinNumbers , I finally had a chance to read yours and Ryan's article... well done! I thought your article summarized the opportunity that exists with Fairfax today very well. I have subscribed to your sub stack and I look forward to reading future articles. Writing is a great way refine one's investment process and thesis for specific investments. As I have said before, feel free to use any of the material in my PDF/book in future articles (same with other posters on CofBF). At the end of the day, we are all trying to better understand Fairfax (and improve our own investment framework). The more people who write/participate in the dialogue the better Hopefully Ryan gets bit by the investing bug... He has a great mentor in you, which gives him a big advantage.

-

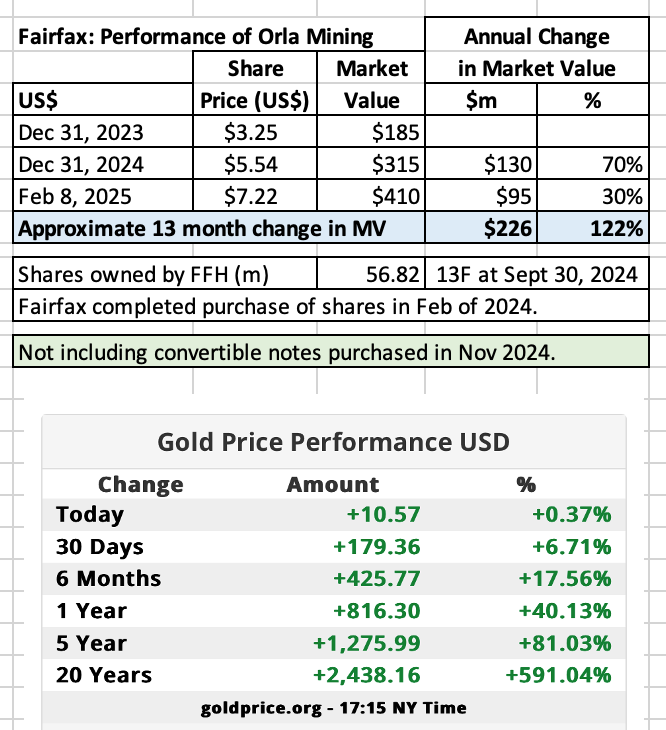

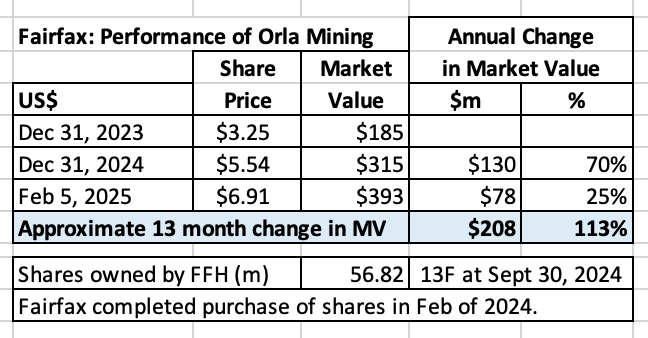

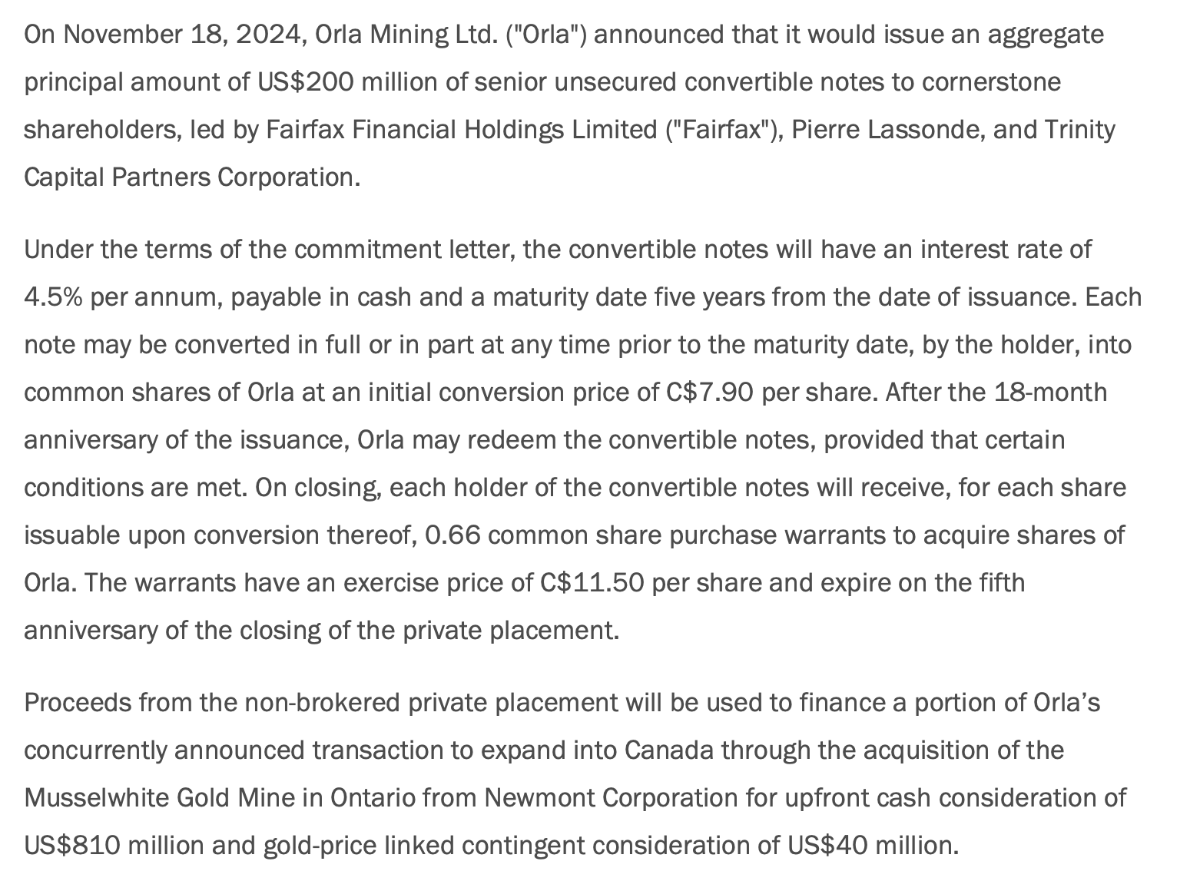

Gold prices are at record highs. In 2023, Fairfax built out its position in gold producer Orla Mining (partnering with Newmont Mining and Pierre Lassonde. How is its investment performing? It's up +$200m in 13 months, more than a double. This does not include the convertible notes they purchased in November. OLA.TO ORLA Orla provides a good case study of how Fairfax does business today: partner with the best in that field - in the gold space that is Newmont Mining and Pierre Lassonde. It is impressive the relationships/networks of expert external capital allocators that Fairfax/Hamblin Watsa/Fairbridge has slowly built out over the decades in many different industries and geographies. It is an important part of their moat - and it is grossly misunderstood/under-appreciated by the broader investment community. The many relationships/networks they have established also likely helps big time with deal flow ( @nwoodman has pointed this out before). My guess is Fairfax is viewed as being an ideal partner for other competent capital allocators (Fairfax wants to be a passive investor/partner). That is important with all the capital Fairfax will have to allocate in the coming year(s). This also highlights an important difference in how Fairfax allocates capital compared to Berkshire Hathaway. Fairfax is much more comfortable leaning on the expertise of others. Buffett instead prefers to rely on his own expertise. Looking forward, to when Prem and Buffett are gone, I think Fairfax's approach might work better/be more sustainable. What do others think? ----------- Orla's purchase of the Musselwhite mine in November is looking very well done. - https://wp-orlamining-2024.s3.ca-central-1.amazonaws.com/media/2025/01/Orla-Acquires-Musselwhite-November-2024.pdf

-

RBC Direct Investing as well. Bank account. And all investment accounts (all are self directed). If your total assets are over a certain size you get a higher level of service (Royal Circle). You get a dedicated 'helper.' And I get access to lots of their research (I am not sure if they still do this). When you call in to their help line with questions (I use the help line for simple questions) your call goes to the front of the queue and you also get one of their more experienced people. When I recently did my two LIRA conversions to LIF, my 'helper' did all the paperwork, met us for signatures, couriered the documents to Toronto and had them walked by a buddy to the correct department to get processed. We were doing the conversion in early December and he did not want to risk it getting delayed/lost (I wanted it processed by year end). ----------- Keeping things simple I have moved all of my family's banking to RBC. I am also telling family that wants help (with investing) to seriously consider moving their banking/investments to RBC. All my kids now understand the RBC platform and can also help each other with all the basic tasks (how to open an account, how to transfer funds, how to but a security, where to find the paperwork come tax time etc. I think keeping things as simple as possible is very important, especially for people who are not into personal finance.

-

Congratulations to all the owners of Fairfax India. Nice to see the stock (finally) moving materially higher. The value was always there… the only unknown is when it would be recognized in the share price. Fairfax India’s share price was always an enigma for me. It has always been a very well run company. BIAL is an amazing asset - owning 74% is brilliant capital allocation (they got their elephant gun out).

-

The share price of Orla Mining has been on fire the past 13 months. Gold has been in a strong uptrend for the past year. And a Trump presidency appears to be the latest catalyst. Fairfax finished building out their common share position in Feb of 2024. They own about 57 million shares = 18% of common shares outstanding (not including convertible note issued in Nov 2024). The market value of Fairfax's stock holding is about US$400 million today. It is up about $200 million over the past 13 months (+100%). In November, 2024, Fairfax also participated in a convertible notes offer by Orla of US$200 million (not sure how much of the $200 million that Fairfax purchased). There are three components to the convertible notes offer: Interest rate = 4.5% Convertible into shares of Orla at C$7.90/share Warrant = .66 share convertible at C$11.50/share At current market value, Orla is likely a +$500 million investment for Fairfax (including the convertible notes).

-

Lucky. Just like when they sold Resolute at the top of the lumber cycle. Just like when they sold pet insurance when there was a mania in cats and dogs. Just like when the average duration of their bond portfolio was 1.2 years and bond yields spiked. Just like when they did a dutch auction and bought 2 million Fairfax shares at $500/share. I could go on… Maybe they aren’t lucky… maybe its skill… And if it is skill, the question becomes: “is it reflected in the stock price?” My guess is no. As a result, it is like an investor today is getting a free call option on this aspect of Fairfax. ( @Hoodlum , FYI, my comment above is not directed at you )

-

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

I realize Canada is a small country (40 million people). But here is one small example of what is happening in Canada right now. My guess is Canada was a pretty good market for US liquor producers. Not any more. The problem with products like liquor is lost sales are... well they are lost forever (it's not like consumers drink 2x the amount when the product is available again). And once you lose facings in a store (and consumers shift to another brand) your brand is permanently damaged. Liquor companies (and their employees) in the US must be thanking their lucky stars at their good fortune. Provinces respond to Trump tariffs by pulling U.S. liquor from shelves - https://www.cbc.ca/news/canada/toronto/ford-lcbo-tariffs-trump-1.7448423 -

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

Trump is gambling that countries will not push back. And that the impact of tariffs on the US economy will be minor. I am not so sure. He also has a timing issue - mid-term elections in the US are in less than 2 years. So he needs to move quickly - but moving quickly takes away his biggest piece of leverage - divide and conquer (extort/nail one country at a time). Canada has responded pretty aggressively. We will see what Mexico and China do. Trump said yesterday the EU is next (with tarriffs). The problem for Trump is if all the countries impose meaningful tariffs at the same time... well it doesn't take a rocket scientist to understand that at some point US consumers are going to start to feel pain. I am really interested to see what the stock market does this week. It has been whistling past the graveyard the past month - likely under the assumption that like in term 1, any pain from Trump's policies will be minor/short lived. Well, that is now starting to look unlikely. If the temperature is not brought down quickly (and Trump is the only one who can do that) this has the potential to metastasize. That the US could become broadly reviled in a country like Canada is nuts (but that is the path Trump/US is on). Yes, it is early days. So let's hope that a resolution/solution is found. -

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

Linamar is on my watch list (should the stock sell off significantly from here). Here is what Linamar’s CEO had to say about tariffs. Yes, her view is likely biased. But it is likely directionally accurate. It really is crazy town… a giant game of chicken. The tail risks are widening. Tariffs will halt North American auto production and trigger layoffs: Linamar https://www.theglobeandmail.com/business/article-tariffs-will-halt-north-american-auto-production-and-trigger-layoffs/ U.S. President Donald Trump’s 25-per-cent tariffs will quickly force North American auto plants to stop production, warns Linda Hasenfratz, executive chair of Linamar Corp., an Ontario-based supplier to the major automakers. Mr. Trump said he would impose the tariffs on Feb. 1 to correct trade imbalances and spur Canada and Mexico to improve their border security, despite warnings from economists the levies will drive U.S. inflation and damage the economy. The U.S. has a merchandise trade deficit with Canada of about $100-billion, but excluding Canada’s exports of oil the U.S. has a large trade surplus with Canada. The trade in cars and autos parts between Canada and the United States is about balanced, TD Bank economist Andrew Foran said in a recent research paper. Ms. Hasenfratz said the costs of the tariffs will be borne by her customers — car makers — who require highly specialized components. It can take 12 to 18 months to source and engineer alternative parts, she said in an interview. “It would just create an exorbitant amount of cost, and our customers can’t afford to absorb that,” Ms. Hasenfratz said in an interview Saturday. “Consumers certainly aren’t going pay it, so demand will disintegrate. So in my opinion, it wouldn’t be more than a week before we would see vehicle production in North America grind to a halt, and that means millions of people laid off, the majority of which would be in the U.S., and I can’t see how that’s a good thing for America.” -

25% tariffs on Canadian and Mexican imports.

Viking replied to SharperDingaan's topic in General Discussion

At times like this, as an investor, it is important to be inquisitive and open minded. Be rational. Keep emotions in check. --------- Buckle up boys and girls, it looks like things are about to get real. The problem we all have today is a lack of information. Even Trump doesn't know what he is going to do (in the coming weeks/months). Politically, Canada's governing party (federal Liberals) is a historical mess (in every respect) - so it is highly unlikely they are going to handle the issue well (probably the opposite). So it is impossible to know with any certainty how this is ultimately going to play out. So what is an investor to do (particularly one in Canada)? Well, I have always been told that financial markets hate uncertainty... we will probably test that theory in the coming weeks/months. Having some cash on hand probably makes some sense. Both Canadian and US stock markets are trading back at all time highs (perhaps whistling past the graveyard?). Investors have had a wonderful opportunity the past week or two to get positioned a little more defensively. Bond yields have been heading lower in recent weeks (flight to safety?). We just might get some wicked volatility over the short term - some very well managed companies could get taken out behind the woodshed. Or not. I am trying to stay focused on understanding what is happening (and less on good/bad). So I can navigate through it as best as possible (just like past disruptions). -

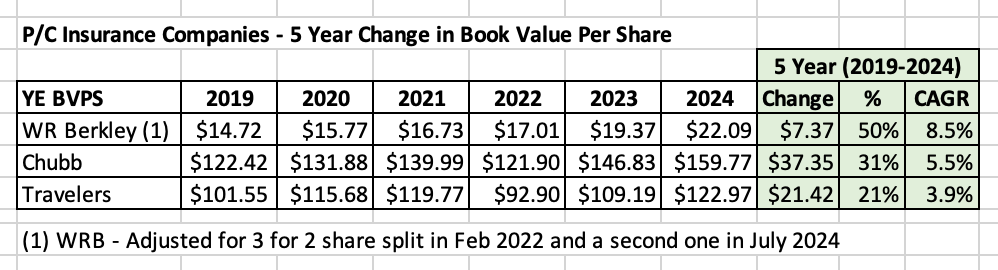

@Maverick47, thank for taking the time to share your very informative post. It is great to get thoughts from board members who understand the insurance side of things. Chubb is a really interesting company. The Greenberg family is as close to royalty in the P/C insurance industry as you will find. I enjoy listening to Evan Greenberg as he typically provides lots of interesting commentary. Having said that, he is also very good at marketing his firm. My all time favourite quote of Greenberg's was when he tried to explain the historic bear market in bonds as actually being a really good thing for the P/C insurance industry... at the same time their balance sheets were getting obliterated. There was no way to put lipstick on that pig... but he certainly gave it his best shot. Your post on Chubb is timely as I am in the process of updated my 'peer comparison' post. I will compare Chubb, WRB, TRV, BRK, MKL and, of course, Fairfax. The post will be out after all companies have reported Q4 results. 3 companies have reported... so here is a sneak peak... How have they performed over the past 5 years? Measured by CAGR of BVPS, performance has been pretty bad. The primary reason for the poor performance is the historic bear market in bonds. Balance sheets of P/C insurers have not yet 'recovered.' Perhaps this is a reasons the hard market is still rolling along. The really interesting thing to me is over the past 5 years all of these companies have reported good to very good ROE numbers. Of course, they like to focus on operating ROE (which removes the bad stuff like changes in bond values and currencies). Some companies like to remove the bad stuff (one time changes). What most P/C companies have been reporting over the past 5 years and what has actually been happening under the hood are two completely different things. What I like about BVPS is it strips away much of the noise. And it is the best way to compare companies. And I think a 5 year time frame is a good length of time to use to evaluate the performance of a management team. ---------- What about moving forward? This is where the story gets even more investing. And perhaps explains why Buffett is buying Chubb today. My guess is P/C insurance companies growth in BVPS over the next 5 years will be much higher than it was over the past 5 years. I think this for three reasons: The worst of the spike in interest rates is likely now fully reflected in book value (at December 31, 2024). Investment returns will be higher - driven by the big increase in interest rates. Underwriting income should be solid - slowing top line growth but we could see the start of meaningful reserve releases (on business written in hard market).

-

So we have heard from Chubb, WRB and Travelers. What have we learned? The hard market, that started in late 2019, is continuing. Investment income continues to expand. From a margin perspective, is this goldilocks for P/C insurers right now? I know, I know… I can hear you now… ‘It won’t last.’ and ‘Too good to be true.’ Of course, nothing lasts forever. But many people had the same concerns a year ago and they were wrong. Being years too early on a call is the same thing as being wrong.

-

Proceeds has been my main driver over the years. Having said that, I have always loved the process. I quit my day job at 40. The plan was to take a couple of years off and recharge my batteries and figure it out from there. But something unintended happened. Over the years, the our investments grew faster than our spending. As a result, managing our investments became my day job. Today, I am thinking more about capital preservation and less about return on capital. One strategy I have implemented over the past 18 months has been to shift a significant amount of my portfolio into broad based index/ETF's. I am willing to sacrifice some proceeds and put a significant part of my portfolio on autopilot. Having said that, I will still continue with the process - and make tweaks as I see fit. Bottom line, the split between proceeds / process has been an evolution for me... not something that is fixed. And it ebbs and flows based on what is going on. One example: At times of great market dislocation I will get very focussed on process (understanding what is going on) with the understanding that that is when great investments can be made (spiking proceeds). Times like that are like Super Bowl Sunday for investors.

-

@Malmqky, I appreciate the thought. I have already been paid very well over the past 4 years for my work on Fairfax (both monetarily and psychologically). So a hard no to any donations to me. And I have no special causes - most of my donations these days are going to younger family members (education and/or permanent savings) to help them establish their grubstake. I continue to get a great deal of value from the other posters on Fairfax on this board - as I have said before, in some ways the book is a bit like the Borg collective from Star Trek (with the book being the cube and the Corner of Berkshire and Fairfax being the Borg). I owe a great deal to other board members - in many respects I am just the front man. I am always looking for feedback. Interesting to me that the document seems to be slowly morphing into more of an actual book.

-

@Hoodlum , on bond volatility, I agree - given the bond portfolio and insurance liabilities are likely roughly balanced, the net impact to Fairfax should be pretty neutral. But the line items (where it shows up in the earnings report) will see some pretty big changes. Importantly, investment gains will take a big hit and IFRS 17 will see a big benefit from the big change in interest rates in Q4. AGT has become something of a 'phantom' type of holding since Fairfax took it private in Dec 2018. It has been chugging away for 6 years now. My guess is value has been building in this holding that is not being captured in Fairfax's reported results (and not captured in BV). So we will see if we get an update when the rail sale closes (with a possible dividend payment to Fairfax). I might be wrong. I would love to get an update on Grivalia Hospitality (what the assets are worth). My guess is that investment will work out well for Fairfax.