Viking

-

Posts

4,928 -

Joined

-

Last visited

-

Days Won

44

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@vinod1 with earnings growth of 5% are you not essentially saying Fairfax’s capital allocation will be poor moving forward? Part of the reason I am so optimistic on Fairfax today is: 1.) the cash flows are front loaded. We know with a fairly high confidence level that they are going to deliver record operating earnings 2023-2025. Buffett teaches us when valuing a company the TIMING of future cash flows is exceptionally important (the sooner the better - the higher the valuation a company should get). 2.) the opportunity set to deploy capital is very good today and i suspect is about to get even better: and Fairfax has +$3.5 billion that will be re-invested each year moving forward in a very good investment environment. Bond yields are at 15 year highs. Small cap stocks are trading at bear market lows. If we get a recession all equities will go on sale (and already cheap equities will get stupid cheap). When it comes to capital allocation today, Fairfax is like a major league hitter getting lobbed softballs. As a result, I will be surprised if earnings growth is 5% per year moving forward. You also bring up ‘one time’ losses. Fairfax’s results will be volatile. Especially if we get a recession (no idea if this happens). My view is volatility is a good thing for Fairfax - smoothing results out over a couple of years. The TRS-FFH purchase in late 2020/early 2021 is a great example. They masterfully took advantage of extreme volatility in Fairfax shares - extreme pessimism. Another great example was selling corporate bonds and shifting to government bonds and shortening duration to 1.2 years in late 2021. They sold at the top of the fixed income bubble. The extension of their fixed income portfolio to 3.1 years in October looks exceptionally well timed. Selling Resolute at the top of the lumber cycle? Brilliant. Selling pet insurance for $1.4 billion…. Nuts. Lots of these decisions are $1 billion decisions… they are ‘needle movers’ for Fairfax and its shareholders. Fairfax investors fear volatility. I think they might have it backwards. Especially given how Fairfax is positioned today (strong balance sheet and record operating earnings). Investors in Fairfax should be praying for volatility. With both insurance and financial markets. Thriving in volatile markets - this looks to me like it is likely a significant competitive advantage for Fairfax today compared to peers.

-

@StubbleJumper we are not that far apart. I do appreciate the opportunity to discuss and debate. I sometimes will take a bit of an extreme view to create the opportunity for push back. I wonder if we are going to learn that Fairfax was criminally under earning on its assets from 2010-2020. And that its earnings power is much higher than anyone imagined. Which just means the returns being generated today are not as abnormally high as they look. Just a theory… we will know more in a few years. i also wonder what the value of active management is today (in terms of alpha - returns in excess of a benchmark). Howard Marks comments in his most recent memo that cost of capital matters again - it didn’t from 2008-2021. Another theory i have is the alpha being delivered by Fairfax’s management team is much higher than investors realize. They look ideally positioned to benefit from the current high interest rate / volatility environment - and much better than peers (including BRK). Again, we will know more in a few years. I also wonder about the quality of the underwriting and the insurance business. It looks to me like Fairfax might be slowly moving up the quality scale (compared to peers). Not elite. But better than they were. Another crazy theory. All three ‘theories’ likely impact my view of Fairfax’s earnings potential over the next 5 years. We will see.

-

@StubbleJumper why do you think 1.) a 95-96CR is not sustainable over the next 5 years? What if Fairfax IS becoming a better underwriter? 2.) interest rates today are ‘favourable’? What if interest rates are simply back to normal? 3.) power of compounding is dead? it also appears you think Fairfax (and its equity holdings) will not invest record earnings well moving forward… $3.5 billion per year in earnings is a big number… it could deliver $350 million ($15/share) in incremental earnings to Fairfax each year if it is invested wisely. 2023 + 2024 + 2025 - year after year etc. You appear to be completely discounting the power of compounding looking forward… Yes, the hard market will end at some point. Yes that will slow top line organic growth. But why does that mean CR has to immediately increase to 100 or higher? Yes, interest rates have increased from when they were zero. Why do we think they will be going back there? People are anchored to the financial regime from 2008-2021. What if the next 10 years is different? Maybe we ARE in a structurally higher inflation environment. Which suggests we are also in a higher interest rate environment. Cost of capital matters again. Active management matters again. Since 2018, Fairfax has excelled with active management. Why do we think they are all of a sudden going to get stupid? Do i know how the future is going to unfold for Fairfax? No, of course not. I see a range of outcomes - some good and some bad. With a ‘baseline’ forecast i try and find the middle ground in the forecast. Some items will be too high; some will be too low. I also try to work with facts as much as possible. Do i know how the insurance cycle is going to work out? Ot the economy? Or interest rates? Macro? I have no idea. So why would i assume it all turns against Fairfax? My guess is there will be both puts and takes. What i see on the board is lots of pessimism. But no balance. No discussion of what might go better than expected. So i view people on the board as being too bearish in their outlook for Fairfax’s earnings moving forward. i don’t equate bearish with being conservative. Conservative would include a more balanced discussion of positives and negatives. I enjoyed listening to Howard Marks most recent memo: Further Thoughts on Sea Change - https://www.oaktreecapital.com/insights/memo/further-thoughts-on-sea-change ————— PS: look at Eurobank. Look at the turnaround at this company the past 5 years. Look at what it is earning today (a record amount) and what it is doing with those earnings (purchase of Hellenic Bank). My guess is EPS will increase 20% in 2024. They likely will be instituting a dividend in 2024 and payments to Fairfax could be $80-$90 million. This will increase total dividends received by Fairfax by 50%. It is meaningful. Not built into my $150 ‘normalized’ number. Digit? Do people think we are done with this investment? My guess is it is likely to deliver significant incremental value to Fairfax shareholders moving forward. GIG is a great real time example. This purchase will increase top line. And float. And investments. Fairfax is done after the GIG acquisition? Because we don’t know with certainty what they are going to do we assume they are going to do nothing? These are just three quick examples. Fairfax has so many levers to pull to drive value for shareholders moving forward with insurance and investments. My guess is they are going to continue to execute well. But i remain open minded.

-

Is the US economy set for another Roaring ‘20s?

Viking replied to james22's topic in General Discussion

@Jaygo I look back 40 years ago to when i was a teenager. Quality of life for the average person in Canada today is much, much better in my opinion. Much has changed so there are big winners and losers. As i age out, the losers are much easier to see than the winners… so it is natural to feel that we collectively are worse off. So what is better? Education is infinitely better and cheap. Health care is better. Women have much more opportunity. Net worth of anyone who owns real estate is through the roof (most Canadian families). These are just a few examples that quickly come to mind. I remember the recession in the early 1980’s (I was a teenager trying to find a job). GDP declined 3.2%. Inflation was +10% and the unemployment rate peaked out at 12%. All the hand wringing today about the current economy/situation cracks me up a little… it reminds me of the scene in Crocodile Dundee. Perspective is important. My view is what doesn’t change over time is the opportunity for people to live a great life (here in Canada). Every generation, the model to live a successful life changes in important ways. And every generation 20% of young people figure it out and earn/live a great life; 20% crash and burn and 60% are going through the motions. My guess is it was the same 100 years ago. And the same 200 years ago. I tell my kids they should want to be in the 20% that lives a great life. The rub is the model of the past generation here in Canada (real estate) probably will not work for them - they need to figure out the new model. Your future reality is (usually) the sum of the choices you make. Personally, i think a great current opportunity for young people is to take advantage of all the tax free accounts being offered by the government… tax free compounding (plus low fee self-directed accounts and low fee ETF’s) starting in your early 20’s is a lay-up in terms of achieving financial independence - in about 20-25 years if you work at it (knowledge/skill/desire). -

@Spekulatius i think the fundamental problem for Fairfax is there is no consensus among analysts/investors of what the normalized earnings power is for Fairfax today. This in turn makes it impossible to come up with an intrinsic value. I think normalized earnings for Fairfax is about $150/share. And this should grow nicely in the coming years. Lots of people on this board think earnings this year at Fairfax are unsustainably high (and my $150 estimate is ‘peak earnings’). Lots of analysts agree - some are forecasting EPS to fall at Fairfax in 2024. Do they think Fairfax is going to destroy capital moving forward (mal-invest record earnings)? I think the biggest issue with valuing Fairfax today is the historical numbers are grossly understated and full of noise. 2023 is the first year where we are getting an accurate picture of what the different income streams at Fairfax can generate moving forward. It makes sense investors will need to see 2 or perhaps 3 years of growing earnings to ‘believe’ they are real and sustainable. Over time, as more investors come to understand the true earnings power of Fairfax the stock will get valued more appropriately. I suspect the narrative (story) will also continue to improve moving forward. When Fairfax stock is trading at 1.1 x BV, my guess is the analyst at RBC will increase his target to 1.1 or perhaps even 1.2 x BV. And he will have a couple of really good reasons justifying the re-rating…

-

Fairfax has had an amazing run the past 3 years - the stock is up about 200% - so it is hard to argue that the stock is unloved or even under-followed today (maybe i need to update my view on this…). That is an amazing increase. The response from the analyst at RBC highlights just how long it takes for the narrative around a company to change. It takes many years. A good example is Apple. Apple’s stock bottomed in 2013. It took 7 years - right through until 2020 - for the old narrative to be fully exorcised and for the new narrative to become entrenched. And a lot of money was made by patient shareholders. The key for investors in Apple during this period of time was to simply hold their position - to sit on their hands. That is probably the key lesson here: patience. As long as the story / fundamentals remain intact, holding though the update in narrative phase (also called multiple expansion) can be extremely profitable for shareholders. Growing earnings + increasing multiple + lower share count. This was Apple’s secret sauce and over a 9 year period it gave shareholders a 12 bagger.

-

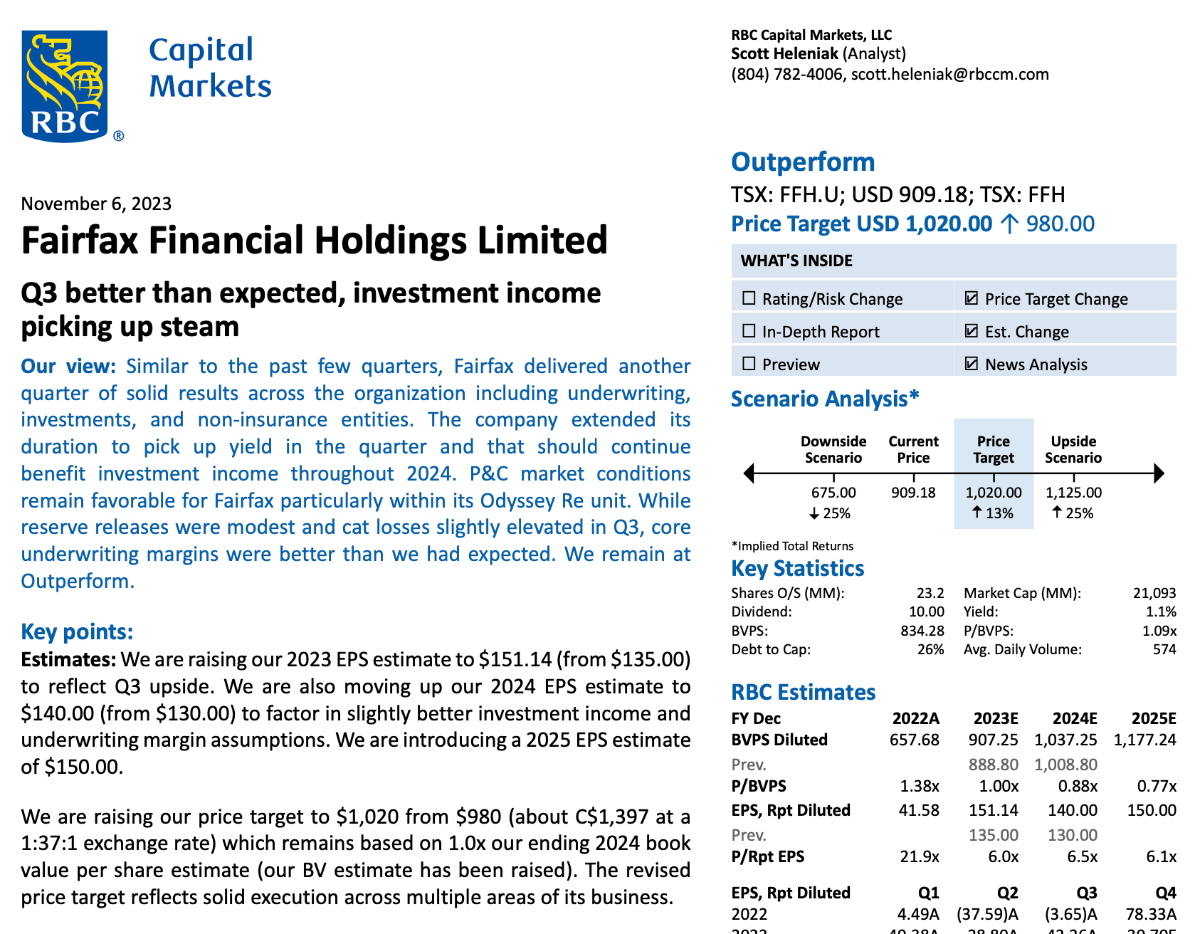

I received a response to my question to RBC regarding why they valued Fairfax at 1 x BV. Copied below is their response. I was impressed they got back to me. ----------

-

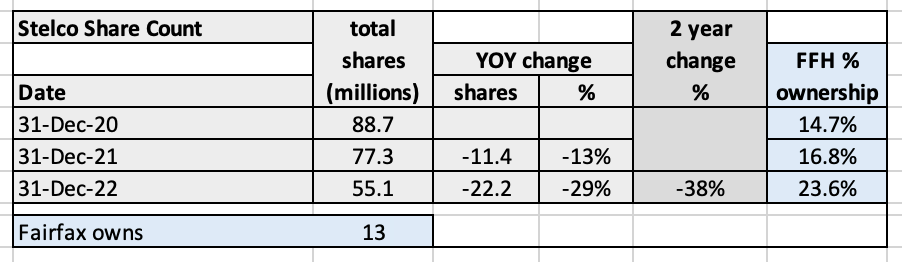

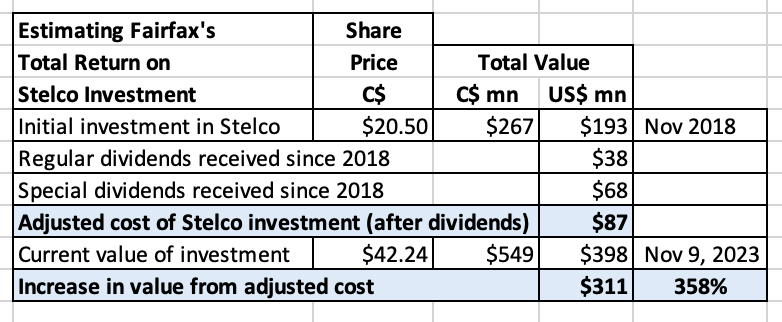

Nov 9: This post was updated to reflect the 12% increase in Stelco's stock price today. ---------- Stelco today (Nov announced another special dividend of C$3/share, along with the regular quarterly dividend of C$0.42/share. Fairfax will earn a total of US$32 million, payable Nov 28, 2023. That will provide a nice bump to interest and dividend income in Q4 when Fairfax reports. Below is an update to the summary I have posted before on Stelco. ---------- In November of 2018, Fairfax invested US$193 million in Stelco, buying 13 million shares at C$20.50. At the time, it was a deeply contrarian purchase. I did not like it. It screamed ‘old Fairfax’ to me: buy a bad business in a bad industry. Boy, was I wrong. What has made this such a good investment for Fairfax? The CEO of Stelco, Alan Kestenbaum. Since buying Stelco out of bankruptcy in 2017 (via Bedrock Industries) he has been putting on a clinic in capital allocation. (I'll come back to this.) Stelco Corporate Presentation Q3-2023 https://s201.q4cdn.com/143749161/files/doc_earnings/2023/q3/presentation/Q3-2023-Earnings-Presentation-FINAL.pdf Here is a little more information of Kestenbaum’s initial investment in Stelco in 2017. Purchase of Stelco out of bankruptcy: Bedrock gets steelmaker for less than $500 million https://www.thespec.com/business/stelco-deal-bedrock-gets-steelmaker-for-less-than-500-million/article_da943b70-1a93-5a35-acb4-92a6da05946a.html? How has the investment performed for Fairfax? Over the past 5 years, Fairfax has received dividend payments (regular and special) from Stelco of $106 million. This has reduced Fairfax’s cost base from $193 million to $87 million. Fairfax’s investment in Stelco has a market value today of $398 million. Fairfax’s investment in Stelco is up $311 million or 358%. That is an amazing return over a 5-year period. What are prospects for Stelco? Very good; just like for the big US steelmakers. Kestenbaum - Schooling the Steel Industry on Capital Allocation What did Stelco do with the earnings windfall from 2021 and 2022? He bought back stock 38% of shares outstanding. And he did not overpay. That was freaking brilliant. Fairfax’s ownership in Stelco has increased from 14.7% to 23.6% - with no new money invested. Two other brilliant moves by Kestenbaum: April 2020 - Minntac deal: 8-year supply agreement with option to purchase 25% of Minntac (the largest iron ore mine in the US) for $100 million – done when Covid was raging. June 2022: real estate sale of ‘Stelco lands’ for C$518 million. The timing of this sale is looking brilliant - at what might be close to the peak of Canada’s real estate bubble. ————— Comments from Prem about Stelco from the 2022AR. “2022 was an active and successful year for Alan Kestenbaum and the talented team at Stelco. The company ended the year with its second-best fiscal result since going public despite an approximately 50% decline in steel prices over the summer. Stelco is benefiting from the Cdn$900 million it has invested in its Lake Erie Works mill since 2017, which has made the mill one of the lowest-cost operators in North America. Stelco entered 2022 with an extremely strong balance sheet and put its capital to good use, completing three substantial issuer bids during the year, thereby repurchasing approximately 29% of its outstanding shares. These repurchases have resulted in Fairfax’s ownership increasing to 24% from 17% at the beginning of the year. In addition to share repurchases, Stelco paid a Cdn$3 per share special dividend and increased its regular dividend to Cdn$1.68 per share from Cdn$1.20 per share. Stelco maintains over Cdn$700 million of net cash on its balance sheet and we anticipate that it will continue to be active both investing in its operations and efficiently returning excess capital to shareholders. We are excited to continue as a significant investor in Alan Kestenbaum’s leadership at Stelco.” Prem Watsa – Fairfax 2022AR Details of Stelco’s Hamilton land sale in 2022, for proceeds of $518 million. “Stelco Holdings Inc. (TSX: STLC) (“Stelco” or the “Company”) announced today that its wholly-owned subsidiary, Stelco Inc., has successfully closed a sale-leaseback transaction with an affiliate of Slate Asset Management (“Slate”). Stelco Inc. has sold the entirety of its interest in the approximately 800-acre parcel of land it occupies on the shores of Hamilton Harbour in Hamilton, Ontario to Slate for gross consideration of $518 million. In conjunction with the sale, Stelco Inc. has entered into a long-term lease arrangement for certain portions of the lands to continue its cokemaking and value-added steel finishing operations at its Hamilton Works site in Hamilton, Ontario.” https://www.thespec.com/news/hamilton-region/all-of-stelco-s-hamilton-land-sold-in-deal-that-would-see-it-transformed-into/article_17a333af-8198-5f97-9866-8c61ed8f799f.html? Details of Stelco’s agreement with US Steel in 2020 to securing long term supply for iron ore pellets. Stelco Announces Option To Acquire 25% Interest In Minntac, The Largest Iron Ore Mine In The United States, And Entry Into Long-Term Extension Of Pellet Supply Agreement With U.S. Steel “Stelco will pay US$100 million, in cash, to U.S. Steel in consideration for the Option (the "Initial Consideration"). The Initial Consideration is payable in five US$20 million installments, with the first installment paid upon closing of the Option Agreement and the remaining four installments payable every two months thereafter. Upon the exercise of the Option, Stelco would pay a net exercise price of US$500 million.” Transaction Highlights: Secures long-term future of Stelco's steel production and solidifies Stelco's low-cost advantage Provides supply of high-quality iron ore pellets from a well-understood and consistent source for the next eight years, or longer if the Option is exercised Increases annual pellet supply to level required for Stelco's higher production capacity following this year's blast furnace upgrade project Supports Stelco's tactical flexibility model to deliver highest margin outcomes based on prevailing market conditions Creates a secure pathway for Stelco to become a vertically integrated player in the future through ownership in a low-cost iron ore source which is the largest producing iron ore mine in the Mesabi iron range Structured in stages that will preserve Stelco's strong balance sheet and financial flexibility https://investors.stelco.com/news/news-details/2020/Stelco-Announces-Option-to-Acquire-25-Interest-in-Minntac-the-Largest-Iron-Ore-Mine-in-the-United-States-and-Entry-into-Long-Term-Extension-of-Pellet-Supply-Agreement-with-U.S.-Steel-04-20-2020/default.aspx

-

Fairfax is on track to earn a record amount of operating earnings in 2023 of around $4.3 billion. My guess is it increases further in 2024 and 2025 to more than $4.5 billion each year. At the same time, it appears the hard market is slowing. Of all P/C insurers, Fairfax appears to be the most disciplined today, with premium growth slowing to 5%. When the hard market ends what is Fairfax going to do with its $4.5 billion in operating earnings? If its share price falls $200 Fairfax will be buying Fairfax shares hand over fist. The gushing cash flow we are seeing today and in 2024 and 2025 are a perfect complement to the TRS-FFH position. Especially with the hard market in its late innings. Yes, there are risks to holding the TRS position. All investments have risks. I continue to think Fairfax shares are crazy cheap. 6 x normalized earnings? 1 x BV for a 15%ROE? The TRS position could easily gain +30% over the next year and +50% over the next 2 years. Ramping share buybacks higher are the ace in the hole.

-

@Thrifty3000 I could buy that if other P/C insurers were being valued the same way. Other P/C insurers have been significantly underperforming Fairfax for the past 4 years. The multiples RBC is using for companies is largely the same as it was 4 years ago (with some minor modifications). Please note, i am not complaining. How can i complain about a stock being up 200% in 3 years - that is still wicked cheap. Fairfax is climbing the wall of worry right now.

-

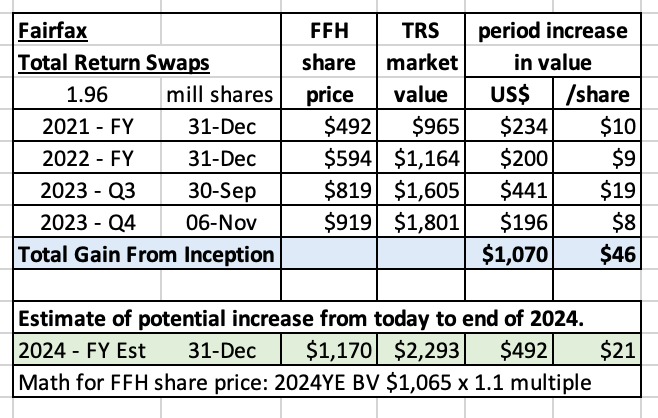

Below is an update to a previous post I did on the TRS-FFH position. In the last couple of days, the position passed the $1 billion mark in gains. I still have a hard time wrapping my head around this investment. It is a mind bender. And a fantastic investment. Could its best days still be ahead? ---------- Fairfax Total Return Swaps – 1.96 million shares The table is set for total return swap (TRS-FFH) to become one of Fairfax’s best investments ever. As of today, the investment has a total value of $1.8 billion and it now shows a gain of $1.07 billion since inception (over the last 34 months). Already in Q4 the position is up another $196 million or $8/Fairfax share. Wow! What about moving forward? I think it could deliver another $500 million in gains ($21/share) from today to the end of 2024. What are my assumptions? Fairfax earnings of about $160/share in 2024. And the company trades at a 1.1 x multiple to book value - which I estimate at $1,065/share at Dec 31, 2024. These look like pretty reasonable assumptions to me. “We think this will be a great investment for Fairfax, perhaps our best yet!” This is what Prem said in his letter in the 2020 annual report when first describing this investment. Clearly, Fairfax was thinking big when they made this investment. The genius of this single investment is still lost on most investors/analysts. Probably because the TRS is a non-traditional type of investment. So, it is largely ignored by investors/analysts in their analysis of the company and its potential impact on future earnings. Well let’s do a deep dive on this investment to better understand just what I am talking about. What is the TRS-FFH investment? In late 2020 and early 2021, Fairfax purchased total return swaps giving it exposure to 1.96 million Fairfax shares with an average notional amount (cost) of US$373/share. At the time, Fairfax had about 26.2 million effective shares outstanding, so this investment represented 7.5% of the company’s shares. Effective shares outstanding at the end of Q3, 2023 dropped to 23.1 million so this investment now represents 8.5% of the company’s shares. Fairfax’s equity portfolio is about $16.5 billion in size. The TRS-FFH position currently has a market value of $1.8 billion = 11% of the total equity portfolio. This is Fairfax’s third largest equity position, slightly smaller than Poseidon and Eurobank. It is a very large investment for Fairfax. Why did Fairfax make this investment? Fairfax's stock was trading at a crazy cheap valuation in late 2020. It was, by far, the best investment opportunity available to Fairfax at the time. To state the obvious, it was an investment they understood very well. So, it was a very low risk and very high return opportunity. Comments from Prem about the total return swap purchase from the 2020AR. “Throughout much of last year (2020) following the pandemic-induced market plunge, I made public statements to the effect that our belief was that Fairfax shares were trading in the market at a ridiculously cheap price. In the summer I backed that up by personally purchasing close to $150 million of shares. Additionally, following our value investing philosophy, since the latter part of 2020 Fairfax has purchased total return swaps with respect to 1.4 million subordinate voting shares of Fairfax with a total market value at the time of those agreements of $484.9 million ($344.45 per share). We think this will be a great investment for Fairfax, perhaps our best yet!” P.Watsa FFH 2020AR Prem’s answer to question from Mark Dwelle (RBC) on the Q4 conference call in Feb 2021. Mark Dwelle: “My second question relates to executing the total return swap with respect to Fairfax shares. I guess, I was just curious why you pursue that structure, rather than just buying back the stock, if you felt like that was the good opportunity? I mean, is this a capital constraint that you couldn't really buy back that much?” Prem Watsa: “We have to be careful, right? So not so much -- yes, we have to be very careful in terms of how much we can buy back. When we looked at Fairfax as a stock price and looked at everything else that we could buy, which is not over return swap on Fairfax. Right now, we paid US$344 per shares, our book value is $478. I mean, if you want the math, just on our book value basis, we'd have about $200 million gain. And Fairfax stock price for book value is worth another 200 million. We just think it's a terrific investment and our total return swap structure was a very good way for us to do it. And so we did it.” Why buy the TRS-FFH versus simply buying back stock? Fairfax did not have the cash at the time to buy back a significant amount of Fairfax stock directly. Again, from the Q4 2021 conference call. Mark Dwelle: “I don't disagree with you that it was a good a good strike price, I guess it was really -- the form of the transaction rather than just actually buying the shares, using a derivative instead is just -- it's a little bit unusual. I haven't usually seen that with most of the companies that I've followed. So that was really my main question.” Prem Watsa: “Yes, so, Mark, our point is just that we wanted to keep up -- we could -- where you have more than $1 billion in cash and the only company once -- or almost have down $375 million, we just wanted to be financially sound, and in all ways, as opposed to use that cash at this point in time.” This investment demonstrates Fairfax’s management team at their best: Rational: best available opportunity Opportunistic: buy when the stock was crazy cheap Creative: didn’t have the cash to do a buyback. Hello TRS. Conviction: wanted to buy a significant stake. Hello TRS (leverage). Simply a brilliant investment - especially given the circumstances. What is the outlook and for this investment? The outlook for this investment is very good. Despite the run up over the past 34 months, Fairfax’s stock price still looks cheap. This means the value of the TRS-FFH could be understated today. Having a low starting point matters greatly when calculating future returns for an investment. Three possible catalysts: Record consistent cash flow: It looks promising for the next three years. Lower share count: Average decline of around 2% per year looks like a good estimate. Growing multiple to book value: Over time, Mr. Market will likely come to understand and appreciate the Fairfax story. All three happening together could drive Fairfax’s stock price higher - which of course means the value of the TRS-FFH investment would also be driven higher. This investment is poised to continue to generate solid returns for Fairfax in the coming years. What are sell-side analysts saying? This group doesn’t know how to model Fairfax’s equity holdings. The FFH-TRS position is a head scratcher for this group. So, they ignore it. I am serious. Most sell-side analysts estimate Fairfax will earn $140 to $150/share next year. That translates to a $300 million gain in the FFH-TRS position. Most sell-side analysts estimate investment gains of about $500 to $600 million for Fairfax in 2024. That is for their total investment portfolio of $56.5 billion. Bonds and stocks. And FFH-TRS. If my estimate is accurate and the FFH-TRS delivers $500 million in gains next year it means analyst estimates are likely way, way low. What is the lesson here for investors? Sell-side analysts are like a limb on the body of Mr. Market. What does Ben Graham teach us about Mr. Market? He (she) is there to serve you – not to inform or advise you. Mr. Market often gets things wrong. You job as an investor is to profit from Mr. Markets mistakes. A note on share buybacks Capital allocation is one of the most important decisions for a management team. Fairfax has said they believe their stock is very undervalued. They have also said that as the hard market in insurance slows, they will look to use excess capital to buy back their stock more aggressively. Fairfax is likely motivated to drive the share price higher. Every $100 increase in the share price equals a $200 million before-tax investment gain. The TRS-FFH investment makes share buybacks an even more compelling capital allocation decision for Fairfax. Is the TRS-FFH investment like a buyback? The TRS-FFH is the next best thing to doing a big buyback. Buybacks are powerful because they improve per-share financial metrics: EPS & BVPS. Buybacks lower the denominator (per share). If the buyback is large and sustained – and pushes up the share price over time - the TRS position could gain significantly in value. At the same time, the TRS- FFH investment increases the numerator (earnings and BV). Investors get a double benefit. ————— Comments from Prem about the total return swap position from the 2022AR. “During 2022 the company entered into $217.4 notional amount of long equity total return swaps for investment purposes. At December 31, 2022 the company held long equity total return swaps on individual equities for investment purposes with an original notional amount of $1,012.6 (December 31, 2021 – $866.2), which included an aggregate of 1,964,155 Fairfax subordinate voting shares with an original notional amount of $732.5 (Cdn$935.0) or approximately $372.96 (Cdn$476.03) per share at December 31, 2022 and 2021. During 2022 the long equity total return swaps on Fairfax subordinate voting shares produced net gains of $255.4 (2021 – $222.7). Long equity total return swaps provide a return which is directly correlated to changes in the fair values of the underlying individual equities.” Prem Watsa – Fairfax 2022AR Comments from Prem about the total return swap position from the 2021AR. “For our stock price to match our book value’s compound rate of 18.2%, our stock price in Canadian dollars should be $1,335. And our intrinsic value exceeds book value, a principal reason being that our insurance companies generate huge amounts of float at no cost. This is the reason we continue to hold total return swaps with respect to 1.96 million subordinate voting shares of Fairfax with a total market value of $968 million at year-end.” Prem Watsa – Fairfax 2021AR Comments from Prem about the total return swap position from the 2020AR. “Throughout much of last year following the pandemic-induced market plunge, I made public statements to the effect that our belief was that Fairfax shares were trading in the market at a ridiculously cheap price. In the summer I backed that up by personally purchasing close to $150 million of shares. Additionally, following our value investing philosophy, since the latter part of 2020 Fairfax has purchased total return swaps with respect to 1.4 million subordinate voting shares of Fairfax with a total market value at the time of those agreements of $484.9 million ($344.45 per share). We think this will be a great investment for Fairfax, perhaps our best yet!” “Investment returns are very sensitive to end date values, so with a stock price of only $341 per share at the end of December 2020, our five and ten year and longer returns have been affected. We expect this to change as Fairfax begins to reflect intrinsic values again. Nothing that a $1,000 share price won’t solve!” Prem Watsa Fairfax 2020AR Total Return Swap: Some Additional Details The other major benefit of a total return swap is that it enables the TRS receiver to make a leveraged investment, thus making maximum use of its investment capital. Unlike in a repurchase agreement where there is a transfer of asset ownership, there is no ownership transfer in a TRS contract. This means that the total return receiver does not have to lay out substantial capital to purchase the asset. Instead, a TRS allows the receiver to benefit from the underlying asset without actually owning it, making it the most preferred form of financing for hedge funds and Special Purpose Vehicles. There are several types of risk that parties in a TRS contract are subjected to. One of these is counterparty risk. When a hedge fund enters into multiple TRS contracts on similar underlying assets, any decline in the value of these assets will result in reduced returns as the fund continues to make regular payments to the TRS payer/owner. If the decline in the value of assets continues over an extended period and the hedge fund is not adequately capitalized, the payer will be at risk of the fund’s default. The risk may be heightened by the high secrecy of hedge funds and the treatment of such assets as off-balance sheet items. Both parties in a TRS contract are affected by interest rate risk. The payments made by the total return receiver are equal to LIBOR +/- an agreed-upon spread. An increase in LIBOR during the agreement increases payments due to the payer, while a decrease in LIBOR decreases the payments to the payer. Interest rate risk is higher on the receiver’s side, and they may hedge the risk through interest rate derivatives such as futures. https://corporatefinanceinstitute.com/resources/derivatives/total-return-swap-trs/

-

@MMM20 , in the past I emailed Mark Dwelle at RBC. He got back to me... and said he was impressed that someone was actually reading his reports on P/C insurance. Cracked me up at the time. I think he retired a couple of months ago. I really enjoyed reading Mark's stuff... he educated readers, was thorough and had a wicked sense of humour. I am wondering if Scott is perhaps US based and just doesn't follow Fairfax.

-

RBC sent out their research report on Fairfax last night. It was pretty positive on the company - with earnings estimates increased. Price target was increased by US$40 to US$1,020. But there was one head scratcher for me... they feel Fairfax should be valued at 1 x BV. Really? After what we have seen Fairfax deliver over the past 3 years? And how they are poised moving forward? So late last night I decided to ask RBC (Scott) what he is seeing that I am missing. I'll let you know if/how he responds. ---------- RBC increased price target for Fairfax to US$1,020 (based on 1 x 2024YE book value). They forecast EPS of $151 in 2023 (up from $135), $140 in 2024 (up from $130) and $150 for 2025 (new).

-

@steph , I agree. Over the past 2 years, have we just witnessed the one of the greatest investments in the recent history of the P/C insurance industry? When he retires (hopefully not any time soon), my guess is Brian Bradstreet will be a unanimous selection for entry into the fixed income Hall of Fame for P/C insurers. Yes, that sounds like hyperbole. But outside of Berkshire Hathaway, can anyone provide me with a better example? 1.) aggressive move to 1.2 years average duration late 2021. Selling all corporates (locking in realized gains) and moving into treasuries. This protected Fairfax’s balance sheet. 2.) aggressive move to 3.1 years average duration in Oct 2023 with the long end of the curve around 5%. This locks in record/high interest income for the next 3 years. The team at Fairfax just successfully navigated Fairfax (and Fairfax shareholders) through the greatest fixed income bear market in history. The bond market was in a bubble of epic proportions - and it popped in late 2021 and 2022. It will take years for the carnage to fully play out (it is still mostly hidden on balance sheets). How many billions did this freaking crazy set of decisions make Fairfax shareholders over the past 2 years? Does anyone have an estimate of what the financial benefit to Fairfax shareholders has actually been? - The avoidance of losses? - The ability to quickly pivot into higher yielding fixed income instruments? - And now the extension of duration locking in higher yields (likely in the 5% range)? This string of decisions was done with a portfolio close to $40 billion in size. WTF? And the table is now set for Fairfax to earn in the range of $2 billion in interest and dividend income in each of the next 4 years. Add underwriting profit and share of profit of associates and you are over $4 billion per year. My guess is some people on this board do not yet grasp the significance of what Prem opened the Q3 conference call with - so is it surprising Mr Market doesn’t get it yet? Q3 Conference Call - Prem: “As I've said for the last number of quarters, the most important point I can make for you is to repeat what I have said in the past. For the first time in our 37-year history, almost 38 years now, I can say to you we expect, of course no guarantees, our operating income to be more than $3 billion annually for the next three years.” (Edit: this number is now comically low…). “Operating income consisting of $1.5 billion-plus from interest and dividend income we earned $1.4 billion year-to-date, $1 billion from underwriting profit, we made $943 million year-to-date, and $500 million from associates and management companies versus $1 billion year-to-date. This works out to be over $100 per share after interest expenses overhead and taxes.” (Edit: Fairfax has exceeded their annual guidance in 9 months…) “We continue to exceed our expectations for the year with the year-to-date operating income already at $3.1 billion, excluding the effects of discounting and risk margin. Fluctuations in stock and bond prices will be on top of that. And this only really matters, as I've said many times, over the long-term.” (Edit: this is the really important part) “Recently, in October, during spike in treasury yields, we have extended our duration to 3.1 years with an average maturity of approximately 4 years, and yield of 4.9%.” (Edit: and the table is set for the next possible move) “In the next four years, we are likely to have a recession in the United States, resulting in corporate spreads widening, allowing us to extend our maturities further.” ————— Fairfax detractors say “yes, earnings are great in 2023 but they are not sustainable.” Well, we have just learned earnings ARE sustainable. $150/share is the new baseline for earnings. This number should grow nicely over time (as capital allocation and compounding work their magic). What is an appropriate PE? 8X is low. That would be a share price of US$1,200. What is an appropriate P/BV? 1.3 is low (given a +20% ROE in 2023 and high teems ROE likely continuing for the next few years). That would be a share price of about $1,200 (assuming BV comes in around $920 at year end). So US$1,200/share looks like a cheapish reasonable valuation for today. Add in E$160/share in earnings in 2024 and that would bump the share price to $1,360 as a reasonable target looking out 12 months. Shares closed Friday at $897. That suggests significant return potential over the next 12 months. Despite the stellar run up over the past 3 years, Fairfax's shares still look significantly undervalued to me. The gift that keeps on giving...

-

@UK , thanks for attaching the screen shot from Fairfax’s Q3 report. Yes, it would be good to get your question answered: “Somebody should just ask on the earnings call plain and simple, if this damned thing will reverse as quickly as it grew, if interest rates will go substantially lower in the future.” But with Fairfax extending duration of their fixed income portfolio, if interest rates decline they will get a large unrealized gain. Perhaps the two (average duration of insurance liabilities and fixed income portfolio) largely offset each other now. I am not concerned - but i need to keep learning. The important things for me are: 1.) underwriting - CR 2.) yield/duration of fixed income portfolio 3.) quality/performance of equity holdings 4.) shares outstanding 5.) capital allocation decisions Quarterly movements in the value of the fixed income or equity portfolio or now insurance liabilities (IFRS 17) is largely just noise. Every quarter there are puts and takes with each - so i would like to understand them.

-

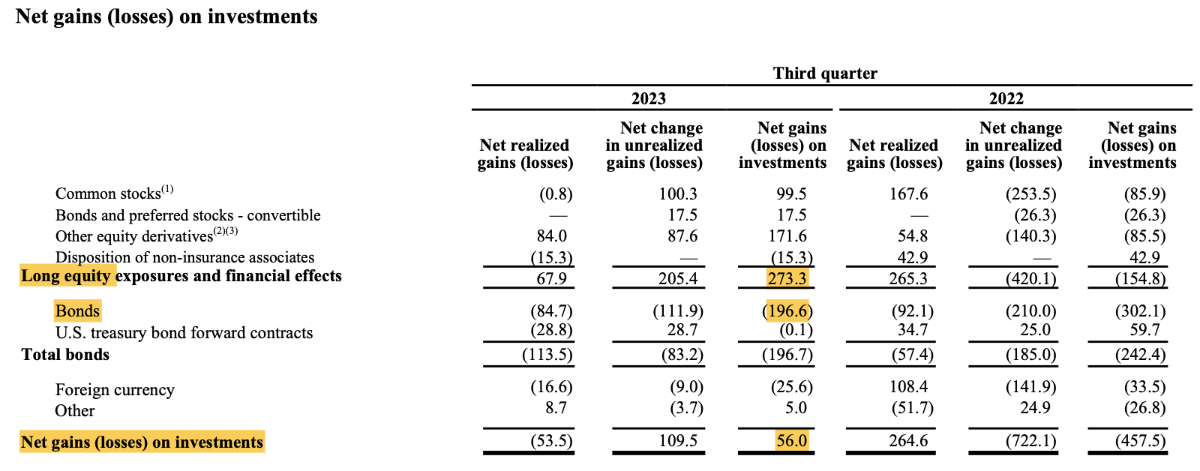

Great quarter. I am travelling so my comments will be short. Below are some answers to the questions I asked a couple of days ago. The conference call in the morning will provide some more answers. The big news is the extension of duration of the bond portfolio. 1.) Topline growth? Slowing from 8% to 5%. This is lower growth than peers. Positive if this means Fairfax is exercising discipline when it comes to underwriting. 2.) underwriting profit/CR? Very strong 95% CR was 100.3% in Q3 2022 CR was 93.9% in 1H 2023 Is Fairfax moving up the quality chain (of insurers) when it comes to underwriting? After Q3 results, can you still say Markel is a better underwriter than Fairfax? 3.) Interest and dividend income for Q3? $512.7 = +100% to prior year. Right around what I had modelled. Q1 = $382.3 million Q2 = $464.6 Q3 2022 = $256.5 4.) Average duration of bond portfolio? We should learn this on the conference call. At Q2, it was 2.4 years What Fairfax has done here is likely the most significant development of the quarter. 5.) Share of profit of associates? $291.5 = much stronger than expected. 6.) Investment gains (losses): $56 (see chart) Equities = +$273 million Bonds = - $196.6 7.) IFRS 17 offset (effects of discounting and risk adjustment): looks to me like it was a big tailwind about $450 million? Big number, if my estimate is accurate. 8.) Share buybacks during quarter? At September 30, 2023 there were 23,115,838 common shares effectively outstanding. 9.) Book value? $876.55 Q2 = $834/share 10.) GIG update - still expected to close in 2023? Yes.

-

Do we know what the average duration of Fairfax’s insurance liabilities are? As an investor, a risk to Fairfax is if short term interest rates crater. How? Bad recession in 2024. Or something breaking in financial system causing central banks to aggressively ease. Not a base case. This would likely cause interest income to decline. It makes sense to me to get average duration on fixed income closer to average duration of liabilities. Because, with the move up in yields further out on the curve, you are (finally) getting paid for duration today. (And you were not for much of the past decade.) As an investor i like certainty - so i am hopeful they extend duration. 2.6 years? 2.8 years? WR Berkely, who is also at 2.4 years average duration telegraphed on their call that they may begin to extend duration of their fixed income portfolio. Having said that, Fairfax has many factors to consider when deciding on average duration of their fixed income portfolio. What i might want as an investor is not on their list of factors (and it shouldn’t be). They have a very good fixed income team. They will have good reasons for whatever average duration they report with Q3 results.

-

@StubbleJumper , i am with you. Interest and dividends is the number i am looking forward to seeing the most. Duration? Composition (any shift into corporates)? The problem with a quarterly forecast is Fairfax is probably pretty active each quarter and we don’t know what amount is actually maturing each quarter. So we will see… Joseph Wang (the Fed Guy) has nailed the move higher in interest rates over the past year. He thinks interest rates might be in the peaking at current levels (for now). Might be a good time to lock in some duration. Pretty much everyone is in the higher for longer camp today… and a year ago everyone thought a recession was imminent (they were completely wrong). Locking in duration looks like such fat pitch right now.

-

With Fairfax set to report Q3 results after markets close on Thursday here are a few of the things i will be looking for: 1.) Topline growth? Over or under recent trend of 8%? What is outlook for remainder of 2023 and outlook for hard market for 2024? 2.) underwriting profit/CR? CR was 100.3% in Q3 2022 CR was 93.9% in 1H 2023 3.) Interest and dividend income for Q3? Q1 = $382.3 million Q2 = $464.6 Q3E = $521? Q3 2022 = $256.5 4.) Average duration of bond portfolio? At Q2, it was 2.4 years 5.) Share of profit of associates? What is build: Eurobank, Poseidon, Exco, other? 6.) Investment gains (losses): Equities: tailwind Fixed income: headwind IFRS 17 offset: small tailwind 7.) Share buybacks during quarter? Is there any commentary about future buybacks on conference call? 8.) Book value? Q2 = $834/share 9.) GIG update - still expected to close in 2023?

-

Or the board has decided that it/Blackberry needs to move on from John. I don’t follow Blackberry (to much personal baggage for me).

-

@Spekulatius , i agree interest rates have been a big factor. But Fairfax’s performance has also been driven by many other very good decisions my management: 1.) buying total return swaps giving the company exposure to 1.96 million Fairfax shares at a cost of $373; this has delivered about $900 million so far. 2.) buying back 2 million shares at $500/share. The creativity to execute these two deals was exceptional. 3.) selling pet insurance for $1.4 billion ($992 million after tax gain) was exceptional. There have been many more smaller ‘decisions’ made over the past three years that have worked out very well for Fairfax shareholders. In short, ‘active management’ has also worked out exceptionally well in the current whipsaw financial/economic environment.

-

Of the three companies, BAM was (is) the company i understand the least. Back in Nov 2020, i voted largely based on Flatt’s public reputation/track record over previous decade. @dealraker ‘s posts on BAM have got me thinking a little more critically about Flatt and BAM/BN today. What is interesting is the turnaround in the business results of Fairfax. And the reputation of the company and Prem. Far exceeded what anyone thought possible three years ago. Reinforces the importance of doing the work, trusting the analysis, acting on the findings, monitoring the situation. It really has been a crazy three year period.

-

This thread is awesome. It is always a little humbling to read what you posted a year ago… even more so 2 years ago. A key learning? Be inquisitive. Be open minded. And when the facts change… update your thesis/views. The changes in the macro environment has been crazy the past 3 years. The lingering effects of Covid (from goods to services). Inflation spiking to double digit high levels. Historic swing in interest rates. Bear markets in stocks and bonds. Emergence of of authoritarian China. De-globalization. War in Ukraine - accelerating the decline of Russia. War in the middle east. So much going on that significantly impacts intrinsic value of all companies.

-

@treasurehunt and @UK , it is important to note that Evan Greenberg (and Rob Berkley) do a good job of talking their own book on conference calls. So i do take what they say with a grain of salt… I think the point that Evan is trying to make is, at least on the casualty side, the risk of future inflation is likely higher than what most insurers have modelled. So they need rate today to get prepared for what might happen in the coming years. It also sounds like some European reinsurers have said current levels of social inflation (legal costs) for casualty are higher than they expected/modelled. Both WRB and Chubb laughed at this (the being surprised part). The other aspect, as @vinod1 points out, is duration of fixed income portfolio matters. Chubb has an average duration of about 4.6 years so the benefit of higher interest rates will take a couple of years to play out. However, for short duration fixed income portfolios like Fairfax and WRB - who are at 2.4 years, they will see the benefit of higher interest income much more quickly. But i think Fairfax and WRB are outliers (in P/C insurance) with such short duration in their fixed income portfolios. And both are focussed on profitability - not market share. Bottom line, for most insurers, the risk of inflation/rising costs is offsetting a chunk of the slow increase they are seeing in interest income. So they need to be very careful until they know what is happening with inflation and its impact on loss costs. ————— Personal lines/auto insurance looks like it has been a hot mess that past couple of years. This line is not out of the woods yet. My guess is insurers where auto is a big part of their business are needing to keep their margins high in non-auto lines to keep their overall profitability and return targets in line. ————— The renewed increase in interest rates in Q2 and Q3 is causing another round of large unrealized losses in fixed income portfolios for P/ insurers - leading to stagnant to declining book values. This likely is keeping P/C insurers rational on the growth/pricing front. With book values declining significantly at lots of P/C insurers over the past 18 months my guess is ratings agencies / regulators today will not be happy with insurers who get stupid with pricing in an attempt to aggressively grow market share. The last thing a management team at a P/C insurer wants right now is to be put on a ratings watch/downgrade. ————— Please note, i am not an insurance expert. My comments above could be way off base.

-

Many sceptics who follow P/C insurance companies are waiting with baited breath for the hard market to end. High interest rates HAVE TO cause the end of the hard market. Right? Well, maybe not. Why? Chubb provided some context on the casualty side of the insurance business. It looks to me like 2024 could see similar top line growth as 2023 of 8 to 10%. Similarly, company combined ratios could also come in similar to 2023. Excellent news for P/C insurance companies if that is what happens. From the Chubb Q3 conference call: Brian Meredith …Evan, a little bigger picture here, just thinking about just generally, the casualty lines here. As you kind of pointed out, really attractive combined ratios that you're printing and in the industry in general. And now we're also looking at long-term interest rates that are, gosh, decade high, right? Are we seeing any weakness at all from a pricing perspective? Do you anticipate that's going to start happening here in the next 12 months, just given the return profile of the business and how attractive it is? Evan Greenberg I haven't seen it really, because higher interest rates are also a proxy for loss cost inflation. So, you've got an industry that I think is trying to stay on top of loss cost or has that impetus behind them to stay on top of loss cost in casualty. And other than in workers' comp, it hasn't been totally benign as you well know, and it's been around for a while. So, I think that higher yields are ameliorating. And by the way, if you do the math and you translate the higher yields to what it means to earn the same return, what combined ratio affect you would get to achieve the same return, it's modest in combined ratio relatively, 1 point here, 1 point there. It’s not like, wow, I can raise my combined ratio by 5 points to achieve the same 15%, as an example, risk-adjusted return. No, you can't, and we run the math.