thepupil

-

Posts

5,000 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

what is luxury voting? are you referring to "luxury beliefs"...as in non-traditional social mores held by the upper class who is often immune from the consequences of the resulting policies or contradicted by the actions of the upper class such as 1. not believing in traditional family structure while getting married, having kids, in a traditional family structure 2. being "soft on crime" while living in crime-less sheltered expensive enclaves or something else?

-

i agree with you there as it relates to actual dollars deployed. If I followed my emotions regarding TSLA, I’d have gone bankrupt a long time ago. Bjt I do have, to use ackman’s term “psychological shorts”, companies and people who I do not wish to succeed…and those I do. We all have our biases/veliefs/values. TSLA is a consequential company, economically and from a capital markets perspective. I don’t think one must be long/short to follow what’s happening with it.

-

I think it matters in that TSLA is 1% of the global stock market, a little more of US and 3% of QQQ and much more heavily represented in select portfolios. i pay attention to TSLA as a bellwether of speculative companies and to a lesser extent Large cap tech/Mag7 (though it is dwarved by others in that basket and hopefully will be further dwarved). and I pay attention because I’ve hated Musk since like 2014. So there’s also a pure spectator element of it for me which wishes misfortune upon the company, slightly offset/contradicted by patriotism/ wanting American companies/investors to do well. In the case of TSLA though, the former far outweighs the latter.

-

yes, by about 2%/yr over 12 years and 5%/yr over last 10, 8%/yr last 5 (thought that's bottom ticking my RE heavy portfolio in march 2020) but I took far greater risk and did so with worse tax efficiency. I don't have great data for 2011-2013, but from memory, yes...caveated that memories of one's own deeds can be..selective. on a risk adjusted/tax adjusted basis, I'd say Berkshire did better...though taxes not relevant for significant portion of my money since I owned Berkshire throughout this time, much of which as my largest position, it technically dragged down my returns (since my portfolio's done > berkshire, the portfolio ex berkshire did better than the berkshire), but that is only w/ benefit of hindsight. I thought Berkshire was a great r/r for much of the past decade and a half. I think it's as worse as it has been but still a potentially reasonable way to grow/preserve one's capital. i can promise you WEB would outperform me even at his age if he were working with my balance sheet rather than the $500-$1T of regulated assets over this time frame.

-

we don't really have evidence of successful large scale m&a at Berkshire since BNSF, which was a great purchase, but that was in 2010. 2016's PCP was decent size ($30B) but financially bad. Pilot was small and involved litigation with the seller. Of course there are bolt-ons here and there, but no evidence of ability to do anything needle moving for a $1.1T company. the investment runway in utilities feels less exciting than in the past after california. What we do have is Berkshire executed one of the best and most impactful stock trades of all time with the purchase and sale of AAPL, which salvaged an otherwise poor stock picking track record over my ownership (2010--->present). That's wonderful and I'm happy to have benefitted from it as a Berkshire holder. But I don't want to pay 1.75x for that (or whatever one is paying after making various adjustemnts for the premium to book the other biz's are worth). the ability to add value on a $300B stock portfolio with a very defined universe of companies at 94 years old is not really something I want to pay a premium for. again WEB is WEB but the stock's recent positive re-rating is undeserved IMO (though insurance is doing very well)

-

I think Berkshire's at its worst absolute valuation in a very long time. relative can be debated but have found other places to invest the proceeds. I just sold 1/3 of my parents BRK and stuck them w/ a big ass tax bill. I was already personally 100% out as of last year. 1.75x book. Large portion of assets/equity in cash/stocks that are marked to market and only worth book. of course the insurance franchise is worth more, BHE/BNSF/MSR worth >book, but these are all finite upward adjustments. the old man is closer to death each year. UNP>BNSF, PGR>GEICO, SHW>Benj Moore, lots of examples of companies' w/i berkshire umbrella doing worse than direct comparables. my biggest nagging question over the years is "is it at all advantageous to be owned by berkshire? do good companies want to be owned by berkshire anymore, particularly when Buffett dies?" overall my view of berkshire's operating businesses relative performance and prospects is probably closer to the bottom than the top over last 15 years, the valuation is the highest its been, the % cash is highest and theres been a very strong NT run w/ rotation out of Mag7 / index down Berkshire up a fair bit. with all that said, it's still my parents' biggest position, namely because buffett's the GOAT and i don't want to sell it all at once for tax reasons. sell decisions are to be taken seriously when taxes are 13-15% of proceeds...were it held in a tax free account, I'd be all out. I may get options approved for their account to buy protective puts on it. curious as to opposing views. anyone buying berkshire of late?

-

this is amazing.

-

I'll delete later. but because of significant portfolio change in last 6 mo's...here it is. I continue to enjoy the diversified pansy stage of life. Name % TETRAGON FINANCIAL GROUP LTD 12.1% NEW ENGLAND REALTY ASSOC-LP 11.9% BANK UTICA N Y 11.0% 401K: VANGUARD EM MKT STK IND-INST 10.1% ARMADA HOFFLER PROPERTIES IN 7.2% BLACK STONE MINERALS LP 5.0% PERSHING SQUARE HOLDINGS LTD 5.0% APARTMENT INVT & MGMT CO -A 4.0% ALEXANDER'S INC 3.8% ESSEX PROPERTY TRUST INC 3.4% HAW PAR CORP LTD 3.0% CK HUTCHISON HOLDINGS LTD 2.6% FARMERS & MERCHANTS BANK/CA 2.6% ALEXANDER & BALDWIN INC 2.3% INDUSTRIAL LOGISTICS PROPERT 2.0% Wife 401K: AMER FND 2065 TRGT RTRM-A 1.9% ST JOE CO/THE 1.8% FRP HOLDINGS INC 1.8% FAIRHOLME FUND 1.8% 401K: VANGUARD TTL BD MKT IDX-INST 1.6% DORCHESTER MINERALS LP 1.5% JARDINE MATHESON HLDGS LTD 1.5% READY CAPITAL CORP 1.0% TUSIMPLE HOLDINGS INC - A 0.9% BRUNSWICK CORP BONDS 0.7% FOXBY CORP 0.5% CALIFORNIA RESOURCES CORP 0.5% MID-AMERICA APARTMENT COMM 0.4% TRINITY PLACE HOLDINGS INC 0.0% 2026 Tax Payable (Deferred through OZ) -2.2%

-

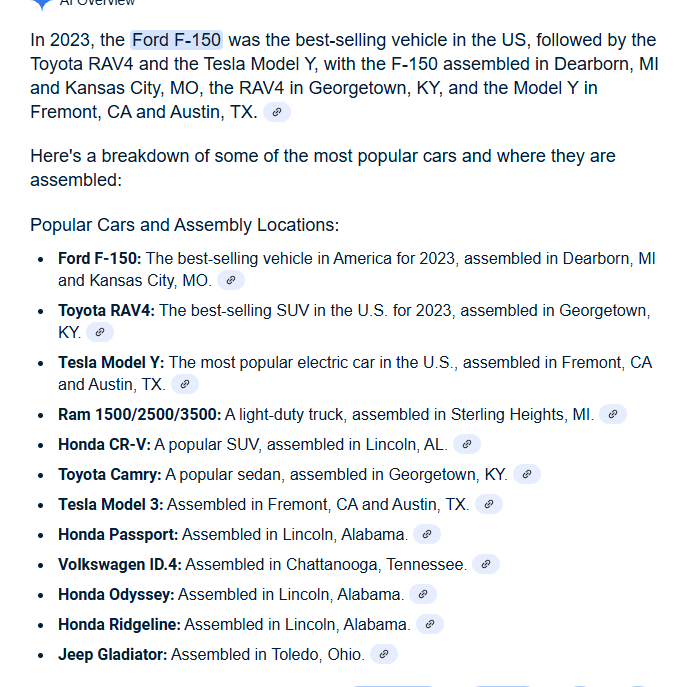

American companies that will benefit from tariffs?

thepupil replied to flesh's topic in General Discussion

interesting that Toyota is just as American as GM and Subaru and Honda are moreso than Stellantis or GM -

American companies that will benefit from tariffs?

thepupil replied to flesh's topic in General Discussion

while i do not agree with the policy, it's interesting to note that every google result for most popular cars in US is assembled in the US already

-

So total return is what matters in investing. At the end of the day, the total realized proceeds of an investment relative to dollars put out should be everyone's north star. it shouldn't matter whther that comes from divvies or capital appreciation and divvies are not tax efficient so US taxable folks shoould prefer the old "buy / borrow / die" without divvies. with that said, over time the yield on my portfolio has increased from something like 2% to 4% before special dividends and higher with specials. I think that's a combination of a number of things such as a) cash/bonds now yield something b) selling non yielding securities (such as berkshire) to buy various yielding securities c) 3 of my top 10 have declared big specials in the last few months. I feel like companies have gotten comfortable with new rate environment and ones with b/s are sharing their cash...I kind of hate it all from a tax inefficiency standpoint, but I also love it. this has no point other than to just bounce off others...anyone else feeling awash in dividends...I'm trying to put all the divvy payers in the IRA's, but I've run out of them and practically everything i own is sending me cash....

-

Fair enough. You are free to take that view. I think you have a real gift in turning someone’s opposing view into a very weird kind of straw man. I often find myself not really wanting to argue with your views so much as your portrayal of my own. But it’s Saturday night…enjoy that sweet sweet additional 50 bps of pre tax carry.

-

being the basic bitch that I am, I will continue to be bewildered at liking corporate credit at these spread levels. And will continue to expect spreads to widen into any meaningful risk event in markets.

-

33% unlevered? For your dream home? money is the slave, not the master. I’m on team “buy it” given the information provided. Only you can decide / have enough information to make this decision.

-

I sold 100% of my ELME, realizing a 36% return since 10/2023, slight underperformance to SPY (+42%). I sold 25% of my FRPH , realizing positive return but significant underperformance to relevant benchmarks (my position doesn't have a single buy/sell date so not really clear of exact return) I also sold some ZROZ which were up 10% in a few weeks while market was down 2%. I put all the proceeds of this into ST tips (IRA) and t-bills (taxable), degrossing to a degree that is almost uncomfortable for me (close to 15% cash). I am taking the DOGE threat to the DC area (and broader) economy seriously. My home equity which is a significant component of my net worth is exposed to this as well. I had about 10% of my portfolio in stocks with this exposure and now have 4% (FRPH), not counting AIV's exposure. I don't expect ELME to get more than $19-$20 in a sale so upside of 15% or so + divvies from here just didn't seem quite enough reward to own mediocre apartments where 10-20% of tenants are feds or contractors.

-

normally I explain ST BRK/B moves w/ XLF, but this runup after earnings is above and beyond XLFs performance. your explanations seem plausible.

-

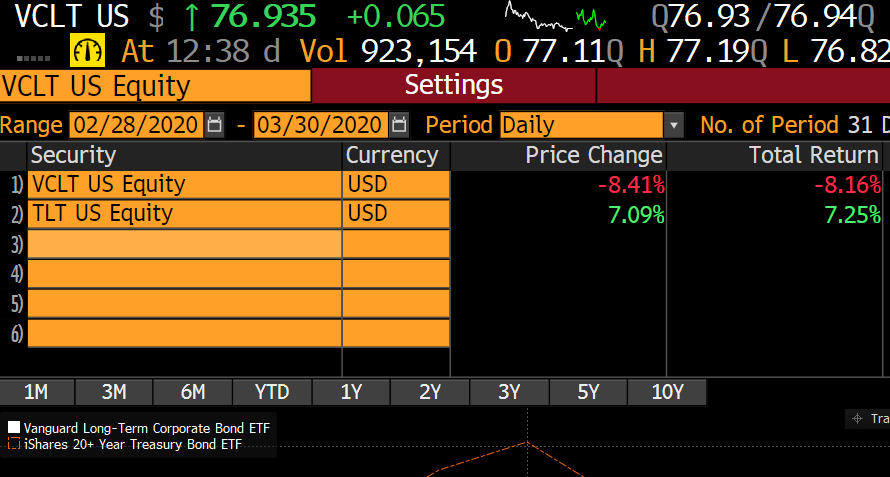

for example, you can sell the ATM TLT put for for what looks like a slight credit. this would leave you with no capital outlay, a little long of duration short the spreads. you have to do it in huge size to matter and are playhing for a pretty specific thing though

-

i completely agree. But without a clear catalyst it's a tough bet to make. Ackman's bet worked so well because he got short so much notional and monetized in a month. if he had to keep it for a year, he'd have been out hundreds of millions in premium rather than 10's. for a while there were ETF's to short CDX (WYDE) but it never gained traction...you could build your own by going long a tsy/tsy ETF and short IG ETF of course. VCLT /LQD puts funded with TLT / BND put sales or something

-

@Gregmal feast your eyes!

-

I’ve avoided commenting but I’ll just say that I think what’s happening and the pace at which it is happening appears counterproductive and chaotic and without regards to any kind of logic. i harbored no antipathy to the civil service and most government workers I know (in my DC burb bubble) are highly educated hard working people who work for the feds because they want to a) serve the country b) not work nights/weekends so they can raise families and c) because they often have family money and can afford to make the low salaries of federal workers. Obviously that’s a type specific to my neighborhood. my other exposure to this is my wife is in the medical field and trained at federal government hospital where they are perpetually understaffed in her field. She works in private practice. 2 of her former colleagues are looking to join her which will gut the VA hospital’s ability to perform care…why work for the feds under this admin? that’s just anecdata. For actual data regarding the cost of the civil service,where the growth and bloat is I would point to this paper from Brookings The federal government employees has been flat for decades while the economy and population grew significantly. Most of the growth in spending is with contractors, 60% of which are defense related. gutting the national park service or (pick your agency) to save dollars seems wholly ineffective. Back to anecdata and biased opinions. as a trump hating conservatively inclined person, I think this will swing the country HARD to the left. https://www.brookings.edu/articles/is-government-too-big-reflections-on-the-size-and-composition-of-todays-federal-government/

-

agreed, duration will likely be the main driver of your position. I’d be inclined to short corporate spreads here / rather than be long them. i can use the same line of argument of “anything can happen” to argue that Meta should trade 1000 over, but that would go against empirical observation and the historical default rate of IG paper which is like <0.1%. The spread on MSFT/META/AAPL bondcan be thought of as a minuscule default credit spread and a less minuscule but still small liquidity spread. I see no reason for either of those to go away. One reason for a liquidity spread is there are simply so many corporate cusips whereas treasure notes and bonds only have a few per year. Buyers sellers are spread across tons of issuers and then tons of bonds of that issuer. another reason for greater liquidity in treasuries is capital treatment by regulated entities. now of course one can conceive how for a day or two some heretofore unbroken relationship can break down, but I still don’t understand any of your logic here beyond “it can happen”. I mean technically I can win the lottery tomorrow. But does that matter. rates will go down because of (insert macro reason for rates going down) but at the same time spreads will “collapse”. Because people are losing faith in the US government credit quality (those same folks bidding up long term obligations of the government) so in the margin they’ll bid up corporates even more furiously? I am just befuddled by the reasoning here. I’ll give you credit for the independent thinking but am reminded of Benny G “You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right” Contrarianism for its own sake feels just as if not more fraught than blind following of the consensus. in the end, though, duration will drive the trade and none of this will matter

-

Ha, was working late last night. Early flight this AM…I do love how there’s time zone/schedule diversity on COBF so it’s never “off”. Like Bitcoin trading.

-

Agreed. Spread tightening into a risk event is nonsensical, particularly at the long end. Goes against empirical precedent / lived experience and logic / first principles. Makes no sense to me, but “that’s what makes a market”

-

Of course perpetual real assets can trade at lower going in yields than nominal obligations, but negative corporate spreads is a whole nother ball game the corporates don’t have a printer.

-

In such a scenario where “full faith and credit” becomes questioned (outside of the usual debt. Ceiling hullabaloo) I don’t want to own any USD denominated nominal obligations. If you think the US gov’s willingness to pay creditors is decreasing, I’d say other currencies / gold / BTC / guns / canned food the better trade. Duration is for just your normal recession/slowdown. it seems like a real stretch to think we see corps trade through tsy’s…think we’re just on a different page here