thepupil

-

Posts

5,000 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

but if one can't time markets, why would one ever have any cash?

-

How much are you down since the inauguration?

thepupil replied to Sweet's topic in General Discussion

My top 3 longs (BKUTK, NEN, TFG) were down (now they hadn’t gone down yet until today and one traded 2 shares and TFG will open up tommorow hopefully) . And had a couple hundred bps of - hedge pnl. To be fair, I only focus on my IBKR accounts. if I include fidelity, I’m flat. If I include 401k that’s indices, up a smidge and I have a small trust (1/3 ish of total portfolio) outside control that’s all indices that went up I’m sure (all of which is taken into account in terms of how much hedges) I think in actuality I probably made a fair bit of money today but I tend to focus on one account where all my activity is for short term stuff and the. Tend to focus on stuff I control for LT performance. -

I admire your confidence and equanimity while disagreeing with pretty much every word, but that’s why you’re richer than I am.

-

How much are you down since the inauguration?

thepupil replied to Sweet's topic in General Discussion

am down today and lost about 900 bps of YTD outperformance in a few hours...at least i can market my returns as uncorrelated -

I think it's quite early to conclude anything about a few days of volatility in the treasury market. This could simply be levered basis traders / other FI players unwinding and a "capital markets" event. maybe we'll get an LTCM or something and a fund or three or in a very bad scenario a bank will blow up. that certainly won't be good but is a problem the fed knows how to deal with and has dealt with in the past. if a fixed income rel val fund loses all its LP's money, it doesn't really matter from an economic standpoint.

-

I guess I'll put myself in the idiot camp. I believe this almost has to lead to a significant increase in the cost of many goods. That seems like inflation to me. Retailers must either raise prices or go out of business. they will praise prices. It can of course lead to deflation as the resulting excess in capacity from a seizing of global trade drastically slows down economic activity (too many goods chasing too few buyers)...this increases the burden of debt on levered producers and is what causes a deflationary depression. so on a 0 -12 month basis, I'd say its inflationary. as business default, people lose jobs, people default, I'd say it's likely to be deflationary. that would be my naive way of viewing this policy and likley potential ramifications outside of significant (and very hopefully) changes to the current policy. what are your hypotheses and why do you think mine are "staggeringly" dumb?

-

perhaps, but thus far, as is the case with every other risk event on record, spreads are increasing and corporates are selling off AAPL's long bonds have widened from 55 bps to 85 bps, CDX IG (credit deriv of 125 IG issuers at 5 yr tenor) has gone from 50 bps to 80 bps, high yield has gone from 300 to 475 bps. thus far, the sell-off has been like every other one...despite increasing liquidity issues in tsy market, tsy's are more liquid, receive better capital treatment, have full fath and credit, have the printer on their side the idea that the US has some sort of credit event and people would flee to USD denominations of corps remains very strange to me. as much as I enjoy @Gregmalhaving gone from #neverbond to a bond enjooooyer, i have to disagree. If the USD / government defaults (which despite everything i'd peg at an extremely low probability event given that the government, FED, and private US folks own 75% of our debt and we're still, despite all efforts to the contrary the reserve currency), then I would think ALL USD denominated obligations (tsy's, MBS, corps, etc) decline significantly relative to gold and other currency terms.

-

this is a fun, albeit unrealistic, chart.

-

this is just a proxy for "things that have high dollar value"...we are already a net exporter in a few of those categories based on below...and the net amounts are far less when taking into account how much we export w/i same category...it's not like we import 100% of our "machinery including computer" or "vehicles" or "plastics" (you didn't imply that), but we can't just look at the top 10 and conclude much from it without looking at the other side, right?

-

i guess we agree since ultimately I'm long ahave little cash...i haven't emigrated just yet....i think my job's immune and assets are relatively well positioned / have a margin of safety...I'll survive....butit could be my TDS, but I view the fuss as we have a president who uses flawed inputs in chatGPT as an opening volley in trade negotiations...the geopolitical equivalent of "hey let's make a deal, my nukes are aimed at you, please aim your nukes at me, let's go..i have more nukes"...the most bullish interpretation is nothing can be taken at face value/ it's all bluster but it has consequences (like the redditors complaining about their input costs already spiking)...i mean what corporation wants to risk capital, make long term investments in various geographies with this shit going on... i can't imagine how it feels to be a levered business with a chinese oriented supply chain....which I'm sure is MANY. Or how it feels to be say...Hawaii, where 85% of food is imported, mcuh of which from asia. as a beneficiary of winning the incredible genetic lottery and being blessed with exorbitantly privileged USD earnings and assets it's just strange to see the (potentially disingenuous fleeting) attack on global prosperity occurring from the US, once a beacon of capitalism, by some intern who put the whole thing together the night before using chatGPT...it's like watching a dark comedy, but it's on the news. is that emotional enough for ya? the most bullish stuff coming out of Bessent trying to tame it and the heretofore loyal billionaire class universally denouncing everything as idiotic...feels more like china centered than before (which still strikes me as quite negative bt not entirely unexpected)

-

it could be because I lost like 3-5 years of wealth accumulation in a few weeks during March 2020 and this time around i lost 30 days (so far...maybe things change), but I didn't get the sense that this feels at ALL like covid. covid was panic, saw liquidations of levered vehicles, margin calls, etc. this felt pretty rational / orderly with the exception of sunday night and yesterday (which featured a fake headline that drove a short lived massive rally). this felt like a rational (partial?) repricing of significantly increased economic tail risk and the most poignant reminder yet of the chaotic/incompetent nature of our country's executive branch. I also don't really understand why we should think of risk as confined to paying a little extra for Nike's. Is not the risk massive business failure as business models of importing from China (and others) are greatly disrupted/ margins decrease for many businesses, levered businesses get really hurt, defaults of all kinds spike. some prices potentially increase and strain lower end consumers. rich people feel a little less rich and don't spend as much...oh by the way a month or two after we the country's larges employer fired ~10% of workforce. so for me it felt (and feels) like the market's not down much and the risk is massively up. i dicked around with some index trades just because I have to preclear stocks and it's just something to do while waiting for the rest of the portfolio / prospective ideas to decline in value, but that urge to run into the burning building and buy something at the epicenter down just like 30% or to buy some "unaffected" (if there is such a thing) business down 10-15% just isn't there. the fact that DJT may be neutered by mid terms doesn't really provide solace to any US businesses seeing a massive spike in cost of materials/goods from China / elsewhere that will potentially be out of biz before then. my feeling may also be influenced by the fact that my largest position has traded $2,000 (not shares) since April 4th

-

I don't really disagree here. Visa is a great company. It's at 25x 2026E, which is "more reasonable". But when volatility heats up like this, I expect to have lost years of profits and for stuff to be a little more "slap you in the face". maybe that's a dumb way to view the world, but my parents' Visa purchased in July 2024 has made 19%. I expect real downturns to make prior purchases look really dumb, to feel more pain. this could be the wrong way of viewing it though, particularly in higher nominal inflation world.

-

topix future. cant resist a down 8% day. Probably won’t hold long. Edit: made a meaningless half million yen before bedtime (but it’s fun speaking in yen)…some people do sports gambling…I apparently day trade topix during the reGFC

-

How much are you down since the inauguration?

thepupil replied to Sweet's topic in General Discussion

thought you were an IBKR guy? Did you get Fido to match their margin rates? -

DMLP has no debt which is one of the reasons it does not generate UBTI. Not tax advice and DYODD but I believe you can own in an IRA w/o problem.

-

I don’t think they’re attractively priced now (despite optically high yields), but would put a plug in for my permahold positions in BSM and DMLP as potential alternatives, particularly DMLP which has a very simple formula: no debt, no UBTI, all royalties go to unit holders, heavy inside ownership, issuance to increase the base. because of how clean story is and because they’ve (in my opinion) done a nice job with accretive issuance over time, I’d be inclined to buy more DMLP On any kind of real pullback. At current prices they’re more of a hedge/bet on rising prices as opposed to assymetric across wide range of scenarios as they were in 2020/21 they, particularly BSM are more gassy though.

-

I have felt zero compulsion to buy much of anything. most stuff has lost 3 months to 1 year of gains. The fundamental picture and degree of certainty seems far worse. Illiquid stuff I own isn’t down. RE isn’t down. and high quality stuff is down a teensy bit. Maybe GOOG is a little tempting, but I’m a little sheepish on the AI front there. Sentiment feels bad in terms of violence but not in terms of absolute valuations. i could just be scarred from covid where I was dumb and loaded up on the wrong stuff early and got bailed out by everything else selling off which allowed for healthy rotation/doversification. But alternative histories exist where I’d have blown myself up and impaired my capital because I was overly cavalier regarding the degree to which the world had potentially changed. what I’ve also discovered in the last two days is I also suck at being hedged. Made an immaterial $$$ and got out of those index shorts in hurry. Being short 100% of my taxable account I. Indices for all of two days massively increased degree to which I watched the screens. It mitigated losses while somehow increasing my stress. Not for me. So long way of saying, I’m doing jack until something slaps me in the face as obvious.

-

yes but it's soooo much easier to supplement a small young portfolio with savings. if your portfolio is 2x your annual savings you can have a -50% investment return and still be flat in $$ at end of year. if you have 10x your annual savings then you lose 5 years in a 50% decline.

-

I admittedly don't know how to read this given the various abbreviations. Care to spell it out.

-

because prior to any resulting retaliation from yesterday, they did not exist?

-

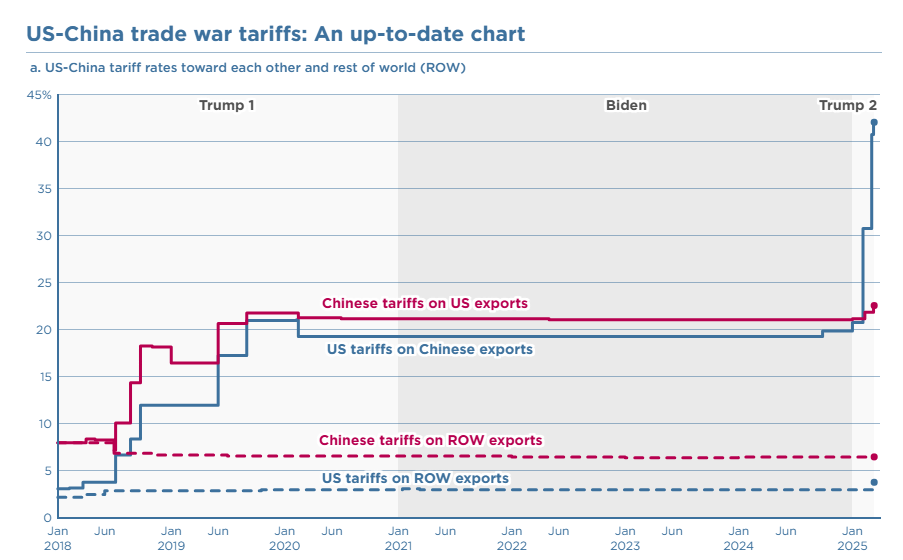

I'm a little confused by the 60% number you cite. I do not have a source for it anywhere. there is the trump chart from last night with a dubiously calculated 67% number, which is the subject of ridicule. Is this what you are referring to? From my understanding, the Trump admin and China began a trade war/raising of tariffs against each other in Trump's first term. Biden / China kept those stable, then Trump just did this. A chart of the tariff rates between the two countries is below. Prior to Trump initiating the trade war it appears China had a tariff on US exports b/w 5-10% on fewer than 2% of US exports. The tarriffs on US exports were in line with those charged by China relative to the rest of the world and on an immaterial portion of trade. https://www.piie.com/research/piie-charts/2019/us-china-trade-war-tariffs-date-chart my assumption that China became manufacturer to the world because of, initially, cheap labor, and thereafter, scale, innovation, and a healthy dose of systematic IP "exchange" facilitated by compliant multinationals who lusted for access to the chinese market. I don't belief tariffs played a material role.

-

How much are you down since the inauguration?

thepupil replied to Sweet's topic in General Discussion

I'm up a little bit. REITs / RE have outperformed, mean reversion after significant underperformance year last year, illiquids are not going down (fake outperformance). I should probably be rotating into high quality companies going down in price, but I've activated full pansy mode and am not.

-

I kind of hate myself for this, but seeing SPX only down 3%, I sold enough e-mini’s to bring my taxable account to mkt neutral / which will bring me overall to 75% net (100% long 25% short). I’ll probably reverse/regret it, but this just seems insane and the market is still “fully” valued. Maybe trump will walk it back and my face will get ripped off , but this seems far worse than feared.

-

as the most liberal of my friends from back home/family and most conservative of my friends in my limousine liberal adopted home, I understand what you are referring to.

-

anyone having this discussion probably has long term gains, which are at most 23.8% at federal level. I guess a wealthy californian could get to 37%.