thepupil

-

Posts

5,000 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

he got fired, but for whatever it's worth... https://www.npr.org/2025/06/02/nx-s1-5417994/former-doge-engineer-shares-his-experience-working-for-the-cost-cutting-unit

-

I don’t disagree with anything you said, but I still like to own some LT bonds. If I own $100/$200/$300k of 30 years, I’m still net duration/ “bonds” via my mortgage (which off top of my head is $700k notional and like $500k PV). You just want to be more net short than I do. i don’t really see the types of rates you’re talking as likely because we are far more indebted. When rates went to the teens we had like 30% debt to GDP. If we did that today at our debt load, it’s full on turkey/VZ time. Could happen but I’m more worried about civil unrest than my single digit bond allocation that will effectively be worthless. I worry more about japanification/eventual deflation as that would hurt many of the assets I own (hence why I own some bonds…but not enough to really protect me)

-

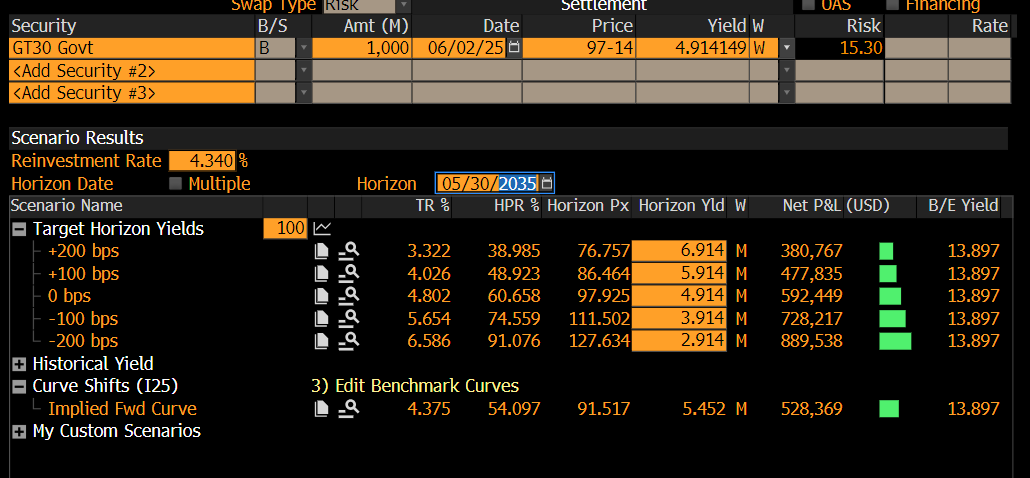

I don't really think the 30 yr = only 80 bps > t-bills is the right way to think about it. the 30 yr will have a VERY different return than t-bills on a 1,5,10 year time horizon and that approaches 4.8%/yr as you stretch the horizon to 30 yrs. at +-200 bps ending yield assuming reinvestment at 4.3% 30 yr will return b/w: -21% and 40%/yr on a 1 yr basis 0.7%/yr and 10%/yr on a 5 yr basis 3.3%/yr and 6.6%/yr on a 10 yr basis I think it's helpful to think of long term fixed income on a total return basis at different horizons than the maturity. 1 yr 5 yr 10 yr

-

I for one, don't think "the market" (or most people here) actually took the tarriffs at face value. If you didn't sell ALL your risk assets on April 3rd, you didn't have certainty on the tariffs being implemented as proposed. If one actually thought they would be, the clear (IMO) step to take would be to sell everything and buy protection at ATH high prices for said protection because this would have been "the big one". thus far, it does not appear to be "the big one" which was surely most people's base case....

-

I think you are the first person I've heard of who used to work in (finance?) and has made money investing in a restaurant rather than lost it as a kind of hobby/"tax strategy". Congrats!!!

-

as long as you leave employers occasionally, just roll to fidelity where you can invest as you wish. I no longer contribute to HSA because not best health plan for family, but have accumulated $60K or so from $20K or so of contributions some years back. I don't really do the whole save receipts thing and am just think of it as a traditional IRA/healthcare emergency fund (that I'd never use).

-

"potentially a good deal...if you've got a long term perspective" March 2009 LOL.

-

yea...in today's world that'd be bid to 15%-18% gross highly levered IRR by PE firms. @73 Reds I like that they showed discipline and sold huge slugs of AAPL after it significantly re-rated. completely resonates with me and hard to do given the giant tax bill involved. I just wish Berkshire's own stock didn't follow suit. After a decade+ or so of being somewhere between moderately and significantly cheap, it just gets much less comfortable to be paying "fair to expensive" when 2/3 of assets / all of equity is in "easy to value"* cash / stocks. We've all read buffett's thoughts on cash as an option on everything else, but if we're paying a 10-20-30-40%** premium to that cash, and that cash is $350 billion, and we lack evidence of successful LARGE scale capital deployment outside of share repo's at Berkshire for a while...it just becomes tough for me... anyways, I'll be the black sheep at the family reunion once my parents see their tax bill... *I say this with some humility of course. AAPL was "easy to value" before it went up a shit ton. If there's anything in the public portfolio with similar upside, I certainly don't see it. **we're paying a 70% premium to book, but Berkshire worth more than book, so the premium paid to cash is lower.

-

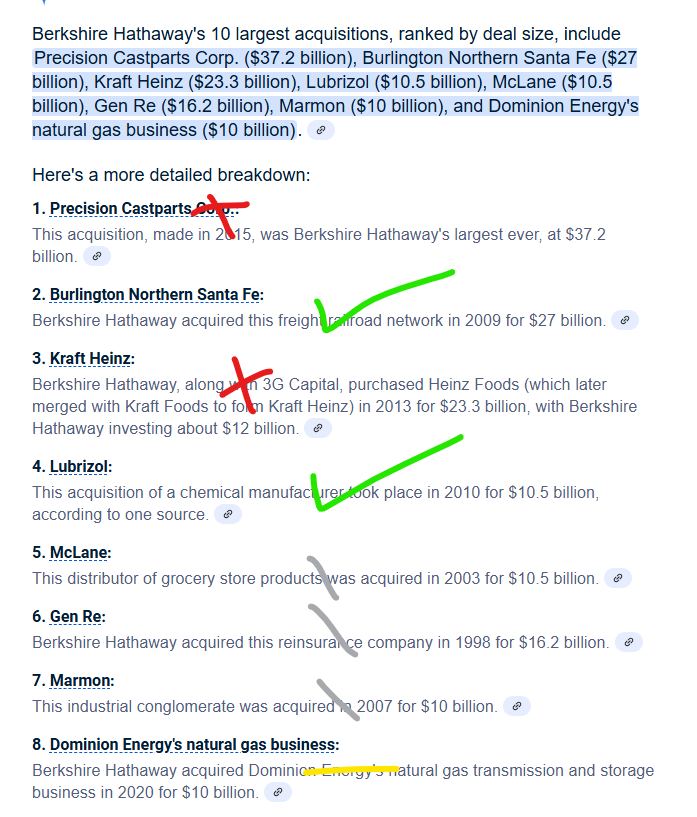

Yea that’s what I get for using the AI…I wasn’t going to systematically pore through 15+ years of filings to show what I know to be true as a shareholder of 13-14 years…if I’m forgetting some big deal, please correct me. at least for me, it’s hard not to be pretty down on Berkshire at current price, cash&stock mix..

-

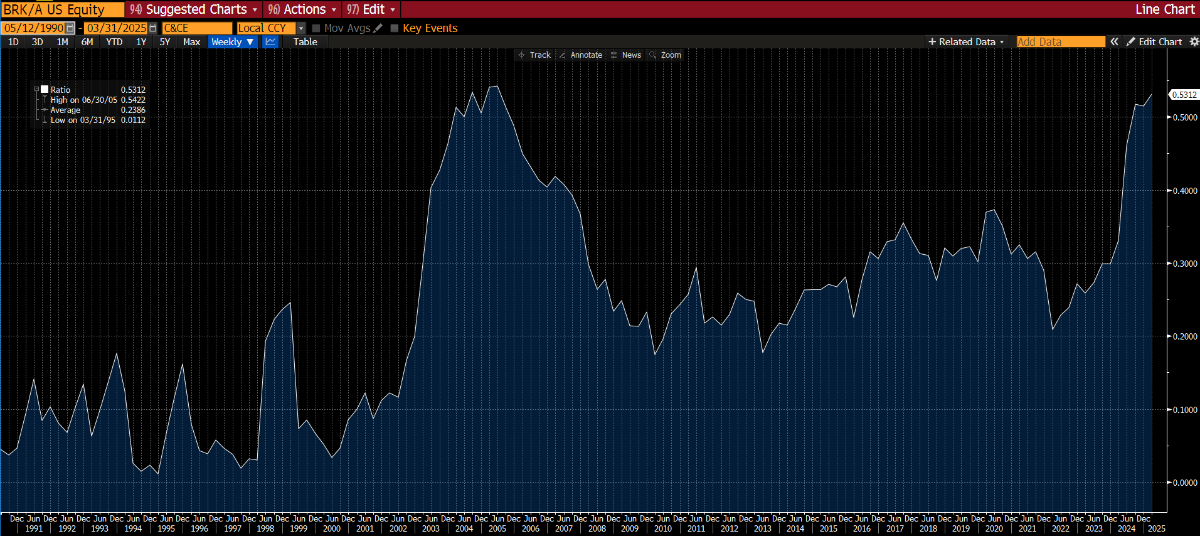

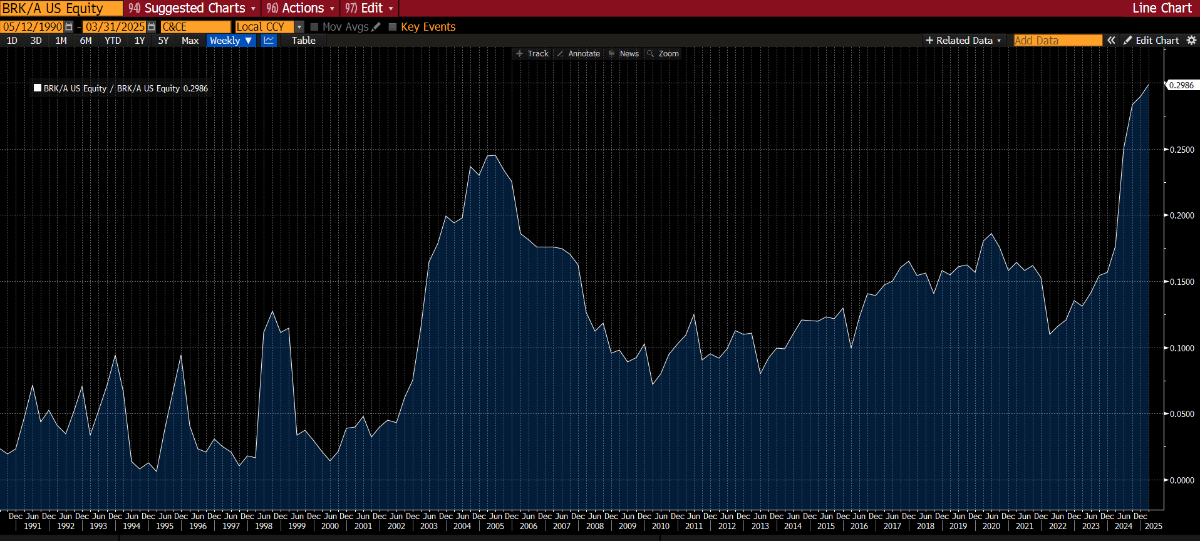

i'm sure some noise/imperfection in this, but it's pretty stark. cash as a % of equity and assets.

-

agreed. the reality is there just aren't many needle moving things out there. Berkshire hasn't had a home run successful large operating company acquisition in 15 years. the below is google AI, and I think misses Alleghany (which was $12B), but I'm going to define large as >5% of Berkshire equity. Today that'd be $30B+, so buying $14B of trading houses is cool and all but doesn't really move things. I would add to the google below, the two most important "acquisitions" of the last decade: ~$40 billion of apple stock....an absolute home run success ~$78 billion of Berkshire stock...very good investment w/ great timing. That $120 billion are the last ten years greatest hits...but it's hard for me to say "hey warren is 94 and has an investible universe of ~100-200 stocks that will make a difference, I'm pumped for him to buy $50 billion of _______ on my behalf at 1.7x book). if the stock went down 20-25%, I'd feel a bit differently as that opens a very straightforward "acquisition opportunity"... I think indexing, large scale tender, or breakup is the long term destiny....happy to change mind/be proven wrong. to be clear, I 1000% agree with Berkshire's decision to blow out of AAPL at the prices they did and create the "reinvestment problem" that exists right now. RED = Bad Green=Good Grey= Ancient Yellow=TBD / no view

-

this is actually very common. it's why for example, non-profits invest in the offshore versions of hedge funds (the cayman blocker corp shields the LP from UBTI).

-

can you point me to this "threshold". this would be (very bad) news to me. https://www.irs.gov/instructions/i8621

-

I don't think the fact that you're dependent on someone wlese to sell to is a good argument against owning any BTC or Gold or Porsche 911's or Old Masters paintings or sports teams for that matter as stores of value. It is true that for those to make a return, you need to sell to another (well i guess you could rent out the Porsche or painting but let's ignore that). You can make money on things that you sell to others and it doesn't entirely discount them as worthwhile. But it is a valid distinction. If my whole portfolio went private tomorrow and I couldn't sell, I'd still derive tremendous benefit from the dividends and distributions. investment assets throw off cash which is not dependent on the sale of the asset to realize the economic return therefrom. But part of gold/BTC's appeal as a store of value is that they don't do that, because if they did, they'd be dependent on some form of economic activity which may or may not endure for decades or centuries. Things that offer no "intrinsic value" as represented by a DCF but have "intrinsic appeal" such as gold**/diamonds**/bitcoin/etc have value independent of some business value which is a positive attribute that makes them different "stores of value" than investments meant to generate cash. If i lived in the congo and owned 10 houses that I rented out, they'd have a greater DCF value than gold or BTC, but that doesn't mean I'd prefer to store my wealth in congolese real estate. mobile value has benefit. I'd want the gold/BTC/diamonds/physical cash etc. So I'm trying to perhaps pointlessly thread a needle here of 1) it is absolutely not true that "every other investment" requires sale to realize economic return. 2) it is true of gold/bitcoin / non cash generating assets 3) both types of assets can offer value to a portfolio but one should be clear minded about the distinction. **that of course doesnt' make these risk free. you can have huge discoveries of gold (many times in history) increase supply, you can have lab grown diamonds destroy the value of your diamonds, you can have something that breaks BTC in 10,20,50 years...who knows. all investments have different types of risks.

-

I don’t regard the tactics as similar. I pointed out that we have imperfect information as a caveat to my argument, not as evidence that the tactics are dissimilar. I’m uncomfortable in definitively concluding that Trump was a terrible real estate investor without full information. I don’t have a comprehensive IRR /MOIC of all his deals. How much money was granted to him and how many times was he bailed out by his dad versus how many times he actually brought something of value to the table or made a shrewd decision. generally my hypothesis is he was a bad investor, he engaged in many unethical tactics (most notably just not paying people) and he repeatedly was bailed out by his (slumlord and many times investigated but actually very successful) father. he is undoubtedly a successful media personality and potentially the worlds most powerful and successful grifter. He reportedly and e$400mm from apprentice and his net worth is growing non linearly now that he’s in office and engaging in unabashed corruption. FWIW I have spoken to enough sharp elbowed distressed debt* guys who engage in all out courtroom war / zero sum games and who hold trump in such low regard relative to the their fellow vultures that I don’t think that my view is entirely outlandish. These are old timers with direct dealings with him.He’s a different breed of scum.

-

When Brookfield sends in jingle mail, they’re not violating their contractual agreements. The lender (usually CMBS) understands that was a risk. OTOH the trail of legal actions throughout his career would suggest otherwise for Trump.

-

I regard this to be a false equivalence. Trump’s investments failed so many times, he was blacklisted by the banks (except DB, who apparently waited til Jan 6th). Brookfield, despite all its flaws and mistakes actually has a consolidated track record of people giving them money and those same people having more of it at the end. There are people for whom Brookfield has created value. I am not aware of a long list of skimped contractors and unpaid bills at Brookfield. Obviously Brookfield sends plenty of jingle mail, but I think their rate of not paying g contractors would be orders of magnitude lower than trumps. again all this is with imperfect info, we don’t have the audited financials of the trump organization. trump has had a lot of success as a media personality and builder of a brand. if America actually wanted a successful investor/businessman, we’d have elected Romney. Early Bain funds’ IRR’s were incredible. We could have a moral debate regarding the methods but the result was crystal clear.

-

my point is, I assume we're looking at mostly the same "facts" (his business record/how that was built) and come to a vastly different conclusion. but the "facts" themselves are quite murky an to be disputed by either side. I don't think if we had "full information" a systematic factual record of all his dealings from birth to present, we'd agree on the interpretation. so to a degree it's all kind of pointless..but we knew that

-

it is statements like this that remind me no one will ever change their minds on these threads.

-

what are you referring to? increased spending by non US members?

-

i mean...i guess...that's a "plan"... I'm a #nevertrumper who despises him so I'll admit to bias potentially clouding my view, but i fail to see any rationality or benefit to the united states in this plan. if there was 10 year plan to bolster/domesticize significant components of our industrial supply chain (defense/healthcare) at the expense of "pure free markets" I could get on board with that...but alienating the entirety of the world, including our heretofore closest allies does not seem like the easiest path to "small victories" it is honestly difficult for me to envision positives which result from the "plan" as enacted and that's why I'd conclude there is "no plan". perhaps the brilliance of it all will become clearer with time

-

what is the best articulation of the plan that you've seen?

-

factually conveying recently enacted taxes is..."a hostile and political act". I guess the $40 million tribute to the king wasn't enough.

-

as for the actual thing being discussed here...I'm just some dude on the internet and by no means "credible" but given that we're at 2-3% real rates right now (2% = TIPS, 3% = truflation), the far easier path seems like what we've always done: financial repression and inflation.

-

One way to think about this is I think most of you all are person 4. and some of the more sanguine regarding risks to bonds are person 3. I'm basically person 3.5 or 3.75. Why is this relevant? Well we're talking about massive haircuts to "the bond market" which I htink of is agg. agg is about 45% treasuries, 25% MBS and the balance IG bonds. are the mortaged people of america going to get arbitrary extensions too? what about IG? most people, particularly right now are short a long term fixed stream of USD payments. until you have a lot more in bonds than your mortgage, you aren't really taking huge risk by owning some bonds. you may have some opp costs relative to equities/bills/etc if duration does poorly, but there are of course scenarios where that goes well. even if you're debt free, have $10mm and just want to stay rich, isn't it worthwhile to have some deflation insurance / protection against "the big one"*. Person 1: Owns $1mm home w/ no mortgage Person 2: Owns $1mm home w/ a $500K mortgage. Has $500K cash in the bank. Person 3: Owns $1mm home w/ $500K of mortgage, $350K stocks $150K of bonds roughly matching the mortgage's duration Person 4: Owns $1mm home w/ $500K mortgage. $500K of stocks just used round numbers here... *"the big one" = a big drawdown where the traditional stock/bond negative correlation holds. it's not the only kind of big one. the big one could be a different one like where the banking system collapses because the government extends the debt arbitraily. guns/gold/canned food, maybe even some bitcoin might be better for that.