thepupil

-

Posts

5,000 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

As a nocoiner, I personally like I understand its value as digital gold. I find these arguments convincing. Not for me but I get it. I do not understand its value as a medium of exchange. Like the above grocery store example. I firmly fall into the “don’t get it” camp here.

-

interesting..this says a large % of "medicaid adults" are working. I don't believe that 25% of the country is disabled. I do believe 25% of the country might be poor enough to get health insurance via medicaid. the below says about 13% of enrollees are because of disability. so do I beleive that 13% of 20-25% of the country is disabled? 2-3% seems about right??? https://www.kff.org/medicaid/issue-brief/10-things-to-know-about-medicaid/ https://www.kff.org/medicaid/issue-brief/understanding-the-intersection-of-medicaid-and-work-an-update/#:~:text=Among adults under age 65,working full or part-time your first example sound like they're underreporting their income and probably don't quality in reality / are committing fraud (in the same way that like 70% of nannies who take cash are...which is just pretty common/i've never really seen as some great societal ill) your 2nd two seems to be following law / simply choosing to not work, right?

-

fair enough, was assuming a single earner and the numbers are a little off. But I see no reason why 44% can't go to 50% via increased payroll taxes for high income folks. or even for...dividends/interest/capital gains etc. all income. if we want a welfare state that guarantees old folks not be destitute, we have to pay for it. flip side is cut benefits at the top. social security is just a transfer from those that earn to those that don't / old people. it's not like the income isn't there to redistribute as the electorate s desire. we'll increase taxes and decrease bennies when the math tells us too. the whole medicaid fraud thing seems to be particularly important to you. i don't have a strong view there and don't think there's some huge underemployed population choosing not to work. just never really seen that....i just don't really ever understand what you're talking about on this to be frank.

-

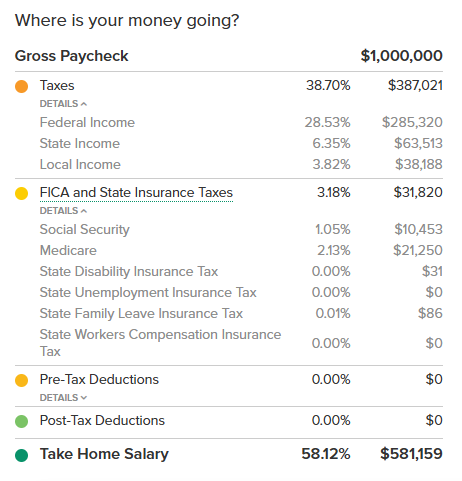

an NYC couple that makes $1mm with no deductions pays 3% of income (the employer also pays another 3%) in social security and medicare taxes and an effective overall tax rate of 42%. It can be higher. I would certainly not like it if it was, partcularly if I'm going to get $2K / month in toda's dolalrs instead of $5K/month from social security when that day comes. But it's simply what it will take. it's pretty straightforward in my view. cut bennies, increase taxes.

-

I'm a bit of a pollyanna regarding the US fiscal situation. for starters, ~20% is intragovernmental then 2/3 of the remaining 80% is domestically held. So about 73% is held by the government or by domestic institutions. we're not entirely "self funded", but moreso than headlines might suggest. Social Security is a relatively easy fix when the math dictates that we have to do so, which will be soon. Just increase taxes and reduce benefits. i don't really think it's reasonable my wealthy parents get $100K/yr adjusted for inflation..regardless of what they paid in...it should be a poverty insurance program...reduce bennies for the top 20-30%, increase payroll tax ceiling.. https://www.crfb.org/socialsecurityreformer/ you can try it here. taxing all wages and means testing for highest earners closes 80% of 75 year funding fap. it's already incredibly progressive. high earner get a very bad "return" on it. making it even worse is the answer IMO. I'm long term optimistic, we'll find some way to make healthcare incrementally cheaper. everything else is just details.

-

I see the 30 year bond as ~98 / 4.73% YTM / 4.71% current yield The 46 year 2071 UNP bonds are 67.25 / 5.86% YTM / 5.65% current yield So on a YTM basis you get ~113 bps more for the credit/liquidity/16 year difference in tenor etc. A bond nerd nuance here: the Z spread is actually 216 bps. https://en.wikipedia.org/wiki/Z-spread the two bonds have roughly similar duration, though the discounted UNP bond has slightly more convexity than the treasury bond since the treasury becomes a premium bond w/ additional appreciation so pull to par becomes your enemy instead of your friend. a 1% decrease in YTM yields 20% appreciation for the UNP bond and 18% for treasury. A zero gives you about 31%. so if you reframe the UNP bond as having more cash yield, more convexity, and 120-200 bps more than the nearest tenor treasury / treasury curve, assuming no tax, I can certianly see why one would want some of the UNP bond over 30 yr treasury... for me it's a toss up. I do like long low coupon corps (universities/railroads/things like that) once they get to certain yields. the biggest issue is so do other buyers of duration and these are illiquid as tar because they're locked up in people's hands. the ability to monetize when one wants to is more uncertain than treasuries. I own some 2100+ bonds for my parents that I can't relaly buy or sell though this has more to do with fidelity sucking than anything.

-

Not offended at all. i disagree that there is “no real upside”. long term bonds offer significant upside and downside. The 30 year zero trades for 24 cents. Long term rates go to 3% I a dire economic scenario, that’s worth 40, +66%. Not the expectation but an illustration . If 20 yr rates are 3.5% in ten years, a 30 yr zero bought today makes 7%/yr for 10 years. Not terrible. There were plenty of safe corporate bonds that returned 15,20 30+% if purchased in ‘22 sell off since spreads and rates blew out. also beyond the pure upside is the potential for low or negative correlation with ones other investments, potentially beneficial for decreasing drawdowns and having something to sell in a pinch. Also, while it’s a minority of my spending, I’ m short a 25 year amortizing 2 7/8% “bond” (my mortgage) to the tune of about $40k/yr so the price of nominal long term cash flows is of interest to me. Of course I can try to offset that with equities instead of bonds, but good to have bonds as a potential tool.

-

Why not? Stocks are discounted cash flows, so are bonds.

-

@Dinar do you not have any tax advantaged vehicles? You regularly and accurately point out the terrible tax efficiency of various things but I’d assume you’d have some % in IRA, no?

-

median IG company is 2.7x https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/12/total-debt-for-rated-us-companies-reaches-new-high-86683893 as an imperfect swag: we know that the S&P 500 is mostly IG. We know that a large swathe of the S&P 500 has net cash, particularly at the top. We know that IG companies have 2.7 turns of debt and pay a 4.1% coupon. we know that wgt avg maturity is 10.5 years. so for those with debt that are IG if you just slap 6% instead of 4% on to 2.7 turns than you go from paying 11% of EBITDA in interest to 16% (2.7x & 4% = 11% 2.7x * 6% = 16%). So over a period of 10 ish years, ceteris paribus, you'll see a low single digit % of EBITDA go to bonds instead of equity. and that's before any offsetting factors (debt buybacks just as one example, nominal inflation decreasing real value of long term debt, etc) again...who cares? it's a complete nothingburger unless you think EBITDA/EBIT/NI is going to massively contract in nominal terms.

-

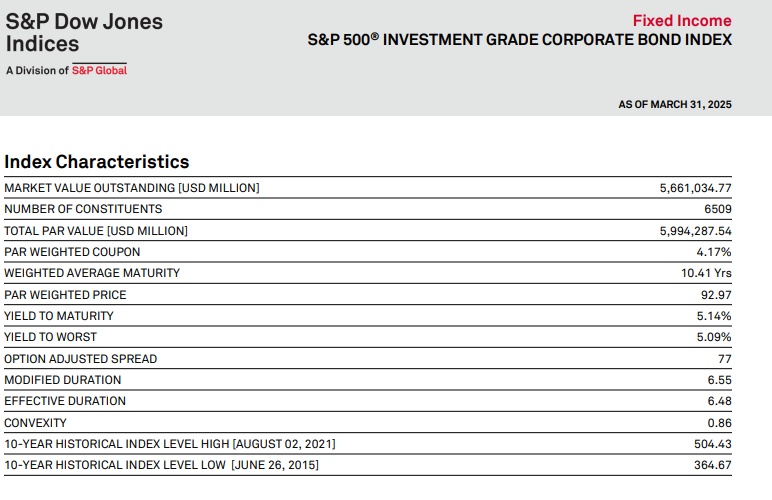

you can google around for statistics on the IG bond market. Again, 33% of the S&P 500 is 10 companies (summarized above). Google AI tells us 4% of the S&P 500's market cap is junk rated. So if you know that 4% looks like HY issuers (and probably on the higher quality end of those, you know what 33% that's the top 10 looks like and for the other 60% just assume they look like the IG market. you will likely conclude that the S&P 500 is not overly levered. I have bloomberg so I can just download every company and look at each one's ND/EBITDA, which i did a while back and came to a similar and slightly more robust/comprehensive conclusion. another way would be to consider the S&P 500 bond inde has $6.4 trillion outstanding bonds. this is relative to $44T of market cap. So if the S&P 500 were a house it'd be like one that trades for $50T with a mortgage of $6.5T....13% LTV. that probably understates it because banks are far more levered, but i regard US banks to generally be in good health (you are free to form/articulate an opposing view). there's simply lots of data whether it be aggregate / market level or just looking at the large companies that points to very strong capitalization and high credit health.

-

the US corporate bond market is 11 trillion, so assuming data issue or bank liabilities are interfering that. of course there are other liabilities, but usually those are things like working capital (offset by current assets), or things like pension (corporate pensions very well funded). again, I'd encourage you to go bottom up. just go down the list of S&P 500 companies. I've done 1-10 for you. keep going and tell me when you find some overlevered companies, tell me what % of the stock market those are, and why i should care. or take a look at the IG market stats as a proxy.

-

yea that was clearer upon a second read. some people say basis unwind, others say foreign selling. i don't know how to weight all that but would if i had to pick one it'd be basis traders unwinding into a choppy market

-

what do you mean? the leadership of the U.S. threatened its populace with the largest tax increase ever and threatened the world with significant trade barriers that would significantly impact the global and domestic economy and potentially have an acute impact on a lot of companies. then there was some indication that all that could revers and stocks ripped. it's not like nothing happened. we can debate what eventually happens, but think significant volatility should be expected and it's hardly fabricated. there are numerous threats to various companies' fundamentals and overall economic sentiment and activity presented by the policies. with regards to bond market, have seen some stuff about volatility blowing out some basis trades, have seen some stuff re canada coordinating sell-off of bonds by Japan and them as retaliation for trade stuff, but i don't know how to weight that stuff. we have seen at least one headline on a fund haveing a -10% on basis trade blow out...(name doesn't come to mind, was in the journal).

-

this is precisely my point. it will take 7-10+ years to roll over even when it does, current market rates are ~1.5-2% ish higher than the weighted average coupon. you could bearishly phrase this as a 50% increase in coupon, but leverage is very low it barely matters. AAPL has $140 billion of cash and $97 billion of debt. MSFT has $70 billion cash and $100 billion of debt. They are expected to make $98 billion NVDA has $43 billion of cash and $10 billion of debt AMZN has $100 billin of cash and $147 Billion of debt. $87 billion of net income for 2025, ~$50B of FCF META $30B of net cash ($77B cash $50B debt) Berkshire Hathaway a truck load of cash Google $70B of net cash Broadcom has $10B of cash and $66B of debt (this is the first one that could be scary given AI boom and actually levered, but on current financials it's 1.5x ND/EBITDA) LLY has $30B of net debt and is supposed to make $20B this year. so that's like 30% of the S&P 500...and maybe 25% of the US stock market. some net cash, most with like 1 years of net income in debt... okay what about the other 70%? well you can use the index stats for that and they tell a similarly low leverage story (not to same degree) I did this exercise with @RuleNumberOne back in 2019...i basically said "there are no overlevered companies in the S&P500...and if they are they're small or REITs"..covid happened...then rates spike...and guess what...barely any defaults... the leverage is in private equity and shadow banking. it's not in large cap stocks. I challenge you to find 10 companies in the S&P 500 with what you'd regard to be an unhealthy balance sheet whose debt repricing would be a problem.

-

agreed. this is one area where I'm basically an absolute permabull. for large cap investment grade corporate america, borrowing cost barely matter at all...some had net interest expense DECLINE with rate hikes as they were making yield on their cash while paying same on their fied rate long term borrowings. . we are 3 years into rate hikes and S&P 500 issuers that are IG still have 10.5 year wgt average maturity at 4.1% tax deductible interest rate. even if rates really really really spike, this will take a LONG time to matter. Not to mention large cap IG corporate america has low levels of gross debt and could always shift from stock repo's to debt repo's if rates really went up and you'd get some nice gains from buying back debt at a discount. anyone who's actually looked at the company data would be hard pressed to find an overly indebted company of consequence / market cap. of course higher financing costs impact borrowers that are private, housheholds, etc. but those aren't the big companies with a lot of market cap. that could be a concern for overall economy/banks. but the top ~20% of America looks a lot like the large corporations. cash rich with long term fixed rate leverage. so rates going up actually increases their income too. many people talk about how yellen failed to extend the term of the U.S. borrowings....i'll withold an opinion on that, but i thought part of the whole QE thing of 2010-2022 was to extend private borrowings and that's been gloriously effective. corporate issuers and households have lots of long term fixed rate debt and cash.

-

I don't know man...I just like to use my Amex Blue Cash Preferred and get 6% cash back when i go to the grocery store. Can I ask what you see as the benefit of purchasing food via "private channels"?...I mean i can certainly understand the benefit of purchasing illegal things or if one needs to flee a jurisdiction...but in what world is my grocery bill a matter of personal privacy?* *outside of implementation of a social credit regime...but I think my purchase of a bunch of overpriced organic stuff would get me points in this regard.

-

yes, the two bonds are different. the on the run 20 year has duration of 12.8 / current yield of 4.87% and is "yieldier", whereas the seasoned off the run 2.5% of 2045 has duration of 14.6, less yieldy (3.65% current) and more convex. The corresponding zero coupon bond has no current yield, yields 5.1% and has duration of 19.3 and is even more convex. Said differently the off the run has a greater portion of its cash flows at the 20 year maturity than the new one with more coupons. Discount rates are highest at the 20 yr part of curve so it should yield more because its closer to being a 0 coupon bond.

-

That sentence is doing a lot of work given the middle 40% of India makes $2K-$3K/yr and air trips per capita is 1/5 of China and 1/30th of the US. I don't think anyone denies that aerospace is growing at > GDP, but on what time horizon would one expect Indians to travel as much as americans/europeans. 30 years? 50 years? 75 years? never? https://www.bain.com/insights/air-travel-forecast-interactive/ the big brains at Bain predict global air travel in 2030 will be 136% of 2019 volume, for whatever that is worth. that's 3.1%/yr

-

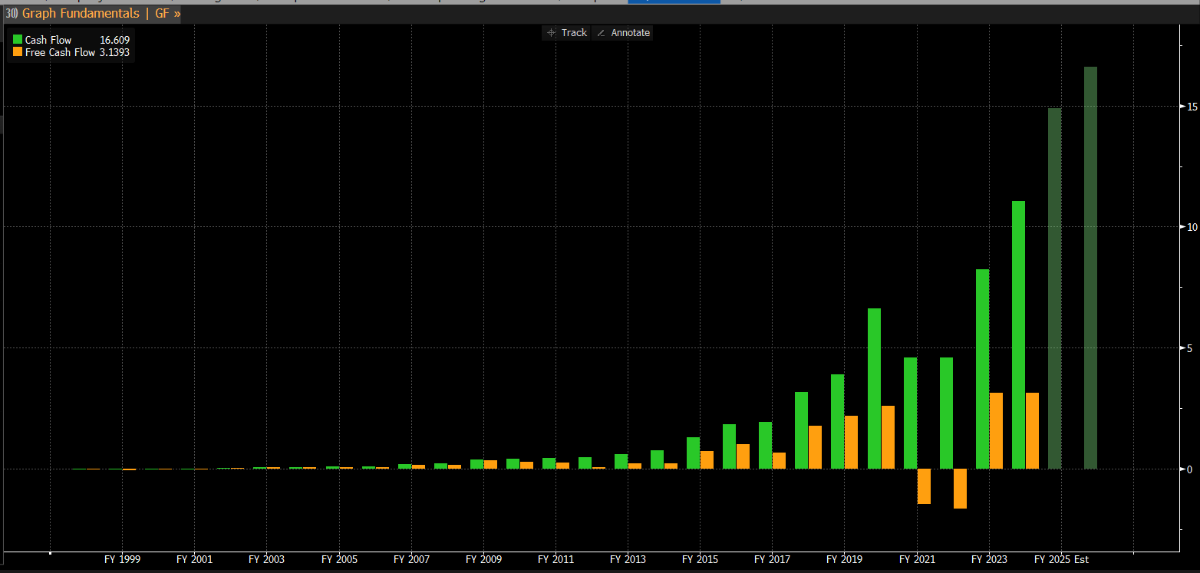

i don't really wish to participate in this debate, but AMZN has had positive operating cash flow since 2002 and positive free cash flow most years since then except for the '20-'21 capex binge. it has not consistently had net income, for a number of reasons (stock based comp, growth effectively financed by suppliers via growing negative working capital, substantial depreciation, etc). AMZN has not been consistently net income generative, but it has been consistently cash generative (as has most of big tech, the others are generally NI and cash generative). again, don't wish to really engage in the bitcoin debate. below is AMZN's OCF and FCF per share. whether or not the price paid relative to observable and predictable inputs at some given point of time made the investment "speculative", I leave to those smarter than I to determine.

-

Honestly my biggest issue with TLT is that because it has decent coupons now there’s not enough duration. Might have to Go Options on 30yr futures or zeroes. Zeroes have bad tax treatment on the accrual but the return will mostly be gain / loss from duration anyway. like let’s say you put 10 points in 30 yr zero on margin. That will cost you 50-60 bps/yr in interest and another 18 bps in taxes on the accrual. So it negatively carries, call it 70 bps. i think that 70 bps a year buys you a fair amount of punch as a deflation / depression hedge. Rates fall a couple % and you’re gaining 6 points to your portfolio. In an extreme japanification your getting 20 pts

-

I bought TLT synthetic call on Friday, Jan 27 $70 puts are $2.5 or whatever. I’m sure that’s historically expensive. But cutting off the tail is implrtant to me given recent events. I think the duration sell off is mostly levered folks unwinding and it will reverse and there will potentially be a nice bid for duration in a likely economic downturns. over very long term, I think damage is done and th dollar/US’s status is diminished. but at least I’m short a mortgage in greater size… But think a little early to conclude we’re spiraling into currency crisis/stagflation/etc.

-

bonds do well in a low growth/low inflation/recessionary environment. we could be going into one. of course, there is increased tail risk of losing reserve status / other bad shit happening, too that would be bad for bonds. i don't think it's more complicated than that. the effectiveness of TLT will depend if we re-enter a period where the stock/bond correlation is negative...let's say the USD doesn't collapse but there is a recession, earnings fall, inflation is low, and rates go from 4.8% today to 3.0% a year from now (not my base case but hear me out). The OTR 30 yr in that case is 37% higher and you made 4.8% in coupon, so you've made 40% and stocks are down say...20%...so your 30 yr treasury outperforms stocks by 60% and you can sell it and go buy some cheap stuff...that's a stylized example of the theory at least

-

I actually think trump has united the country in the last week. You’ve got Paul (R) and Wyden (D) co sponsoring bills to take away the presidents emergency power to enact tariffs. You’ve got leftists (ie Rachel Maddow)and billionaire bankers and random Twitter bros railing against the idiocy of it all. It’s kind of beautiful (if there weren’t real time human costs to the haphazard nature of it all ).

-

Apologies if this has already been quoted. I find the below fascinating...like is Bessent leaking to the WSJ, "guys he doesn't want a depression, we're good". https://www.wsj.com/politics/policy/why-trump-blinked-on-tariffs-b588aea8