thepupil

-

Posts

5,001 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

also consider splurging on a night nurse the first 2-3 weeks. Even every other night for 1-2 weeks is a huge blessing, particularly if the pregnancy was hard on the mom from a physical standpoint, though it is expensive. maybe less important though if you're not working. I took my leave later and was working a few days after born so having night nurse for a little was hugely helpful in letting me get a full night's sleep every other day.

-

if you have a ton of money and don't care about your career progression, i think you should take 15 months of paid leave regardless. that is an insane benefit. babies are a ton of work the first few months but one or both of you will eventually have a fair bit of free time with both of you at home, they sleep a lot. I took 3 weeks and my wife took 12 weeks (unpaid). I assume you're not in the U.S? I know plenty of dads who took none. two jobs offering 12-15 months of paid leave is wild!

-

this is also that if your bros friends are in peak wedding season they may have 5-6 or more weddings a year 2-3 bachelor parties and it becomes incredibly expensive so it may be they can’t get off work, it “can’t get off work” is also “I can afford to go to 2 weddings and 1 bachelor party this year” or “I technically could take off but it’ll put me behind and stress me out” i think one year we spent like $15k going to other people’s weddings. I spent $2-3k on a friends bachelor party (someone for whom money is not an object plans the events, sends bill to everyone at end). Through genetic lottery and high earnings was able to do that stuff, but it consumes a ton of money and time. Happy to be done with that now that all but a few stragglers are married. I don’t see how “normal” people afford the wedding and bachelor parties tha tha e become standard these days. Part of our wondrous societal excess.

-

so when you do this by community, what the most valuable community and what's it worth in your view to sh today?

-

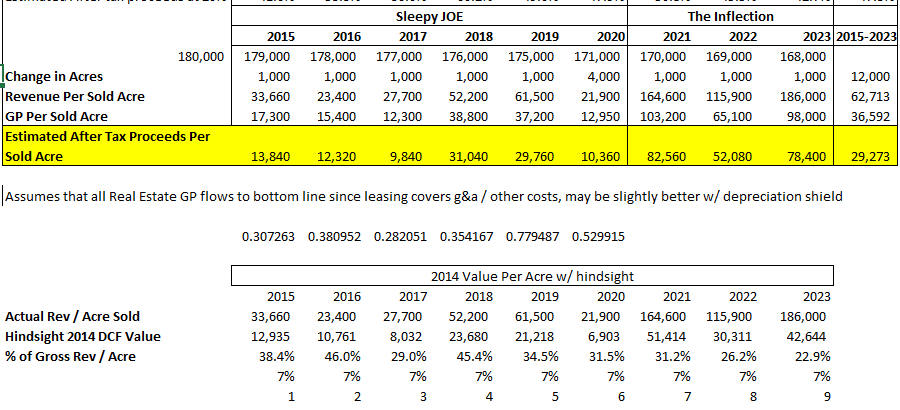

okay so for Camp Creek, you are doing 57 * ($1 million? $1.3 million?) and saying camp creek is worth 57*1.3*0.75 = $55 million to shareholders? I'm using lot sales in last 6 months on zillow and the pricing sheet here https://www.joe.com/community/watersound-camp-creek/available-homesites and for number I'm using the 57 in the table in most recent 10Q and same website says 200/263 already done which foots w/ the table in the Q The Watersound Camp Creek community will be home to 263 lots at full buildout. More than half of the community is sold out with 200 lots sold to date.

-

maybe to try to tackle this another way, when you value an individual community, as you have, what is the value of that community relative to the total sellout of that community?

-

I mean 2021 saw revenue double from 2020 which was almost double that of 2019 on increasing margin / price per lot etc. if that's not an awesome environment, I'm not sure what is. 2021 was objectively a smoking resi market everywhere. not sure how that's controversial. if the margins are reflected in later years and 2021 wasn't truly an awesome market...then whered they get pushed to? 2022? (which was lower) 2023 (lower), 2024 (same as 2022/3). 2015 2016 2017 2018 2019 2020 2021 2022 2023 Average Resi GM 48.6% 67.2% 42.1% 50.3% 51.3% 59.9% 60.7% 52.5% 50.0% 53.6% I have made no forecast. I don't think saying resi RE dev margins will probably be b/w 40-70% is even a forecast. it's too wide to be meaningful. like saying the stock market will return b/ -40% to +40. probably true, but doesn't really tell you anything. I'm simply pushing back on what i regard to be an outlandish statement "that you can get the value of the company in a few years pipeline" or whatever. that just seems wrong and out of line with any kind of reality and does not acknowledge costs, taxes, and time. i agree that valuing multiple decades of land sales is indeed too hard for someone of my analytical capabilities and free time. I think i could study JOE full time and not come up with an accurate measure of IV. i think it's unpredictable but positively skewed at this price. but we'll have to put it to rest as this is well beyond the point of productivity.

-

oh that table. that's what I used to calculate how many of camp creek lots they sold (using the changes from year end to 9/30). i don't really follow what @Gregmalis saying regarding those columns if that's what he's referring to. to me that stuff is all of incredibly varying duration, value, time to monetize, etc.

-

whether their GM is 70% or 50% or 40%, the point stands. they closed on 17 of those super high margin Camp Creek lots 9m 2023 (i believe, right?) and their blended margin was still 50% on RE sales. this is where the "super in the weeds, know everything about the company, forward looking projecting approach" doesn't exactly square with the rolled up company level reported financials. like we know a lot of those lots went off at glorious prices...but JOE's aggregate margins for resi RE 2024 are lower in part because of a lot of low margin stuff. we can choose to be incredibly detail oriented about it, or we can slap "50-60%" and cover most of the outcomes. we know what a year where they have huge sclae 500K acre sale looks like: 2014 = 87% GM we know what a gangbusters RE market looks like: 2021 = 63%. we know the lowest number was 44% in 2017. we know they have higher margin and lower margin projects. and we know they've averaged 58% over 8 years since the timber sale in total. you can counter with any individual deal or community on how it will be higher in the future. i again believe you and trust you have done your work. but won't there always be a mix? somethings ramping, something harvesting, such that the aggregate company reported levels of the past (the dummy financial statements preferred by lazy simpletons like me) are actually more reflective of reality than any individual project level economics/margins. like if you just look at the financials, can you see Camp Creek? do you notice it? I don't. now they got 57 more to go so maybe it will be more noticeable wen they sell more or maybe it won't because it will just blend in with a bunch of $100K lots in tally nasty. by the way, can you direct me to this "column" stuff you are referring to. you've referenced it a few times, but honestly can't find it. is it a spreadsheet you posted somewhere?

-

I think we're just talking past each other. I am making no other point than costs, taxes, and time value exist and will continue to exist. I cede any argument regarding actual detail and on the ground work to you. I have no desire to put in the degree of work to valuing JOE and I believe that an appraisal for any one piece of land (as discussed above) can vary a shit ton so there's obviously huge margin of error both ways in doing that 1000 times and the future is uncertain. I have little reason to believe JOE's margins, tax rate, or discount rates will be significantly/wildly different than the past, so would conclude that the multiple of gross RE revenue (whatever that revenue may be) justified by those things will not be radically different than in the past. if their gross margin goes from 50-70% because of whatever reason you know to be true, then it'd be $100 rev, $70 GP, $52 after tax and whatever PV for time; it's still 40% of gross revenue or whatever depending on how many years into the future that revenue may be. I'm not making any kind of statement about what lot sales or price per lot will be. I'm making an observation about the nature of a lot developer with low basis land wrapped in a C corp structure where developments take multiple years. to me those things will always be true and are informed by the financials across market environments, across different types of developments (in terms of price point) etc. to me, I'm making a statement that is so obviously true that it lacks any kind of analytical value add. It's like saying the grass is green and the sky is blue. $100 of revenue does not equal $100 of net income or cash extractable from the business. But I'm happy to hear an argument as to why the grass is red and the sky is purple and why what i said is not true.

-

I guess I misinterpreted what you were saying, paraphrasing, I believe you said "you have $2.2 -$2.5 billion in value from pipeline". I assume that's a gross number. the value is lower than the gross revenue. we can debate whether value to shareholders is $30 or $40 or $80, but it can't be $100. you used the phrase "$63 a share" which is $3.6B. I asusme this is pipeline gross revenue + income producing estate. I think that's flawed and the reason is costs, taxes, and time. If the $63 a share is via some other method, I'm all ears. I think the past IS representative of the future. the margin fairy will not bestow 100% gross margins on JOE or a 0% tax rate. the past may not appropriately predict the price at which an acre or a home trades (as you can see from the above spreadsheet, basing values on 2015-2019 transactions would completely fail to capture the massive positive inflection in fundamentals, but RE gross margins in 2015-2020 averaged 60% and averaged 57% 2021-2023. they were not wildly different. in the year where they sold huge plots of raw land to mormons (2014) they were 87%. So we can say margins on RE sales, based on ~10 years of data are likely to come in at 50-85% depending on the land type, corporate and state taxes will likely continue to exist, the time value of money will likely continue to exist. perhaps its overly semantic or even just stating the obvious, but $100 of revenue is less thanb $100 of value to shareholders...and I think the number is closer to $30 than $70. I own JOE and have been buying but I think EV / Acre is bullshit. I can only hope that it comes to be the valuation metric on which JOE is valued and I will happily sell my shares to more bullish people than I.

-

I don't really know or care what any of that means, but from a simplistic reported financials spreadsheet standpoint, JOE real estate gross profit margins are around 50%-60%. JOE is a taxable C Corp. So $100 of land value = $50-$60 of GP, you actually have 4.5% state income tax, 21% federal, so multiply $50 -$60 by 0.75 = $37.5 - $45 and if something is in one or two years multiply by 0.9 or 0.8 = $30 - $40. The math to me is pretty simple. If you think JOE's going to sell $100 of gross value of finishded lots in a 3 years, it's worth $30-$40 today. If they're going to sell $100 of a 40 acre section in the sticks that they haven't touched / put any cost into, then it's probably worth $60 (75% for taxes then a couple years of discounting). What you can't do, in my opinion, is take the gross value of a pipeline and divide by shares and say they have X / share in pipeline value. empirically there are costs.

-

I assume this is a gross number. I haven't updated this for 2024 and its pretty rough, but as a sanity check, I try to see "in hindsight what should one have paid for all the acres sold 2015 - present in 2014. Your multiple of gross is like 20-40% because of costs, taxes, discounting, etc. So if JOE has $2.2-$2.5B of gross sales from the pipeline, I'd argue that pipeline is worth $400-$800 million of PV to shareholders, unless for some reason that pipeline is particularly high margin or will be monetized more quickly than others or some other factor.

-

Stock up 8% today on 14x normal daily volume, though it's illiquid so only $2mm traded today on $1.4B cap. Stock is up to $15.40 vs the $11.26-$12.75 I paid in October (and cost of very long held position around $10). I've started to trim a little bit given we haven't heard confirmatory news regarding Equitix. It remains my 1st or 2nd largest position and I see substantial upside, I just hate when stocks go up a fair bit on no news. downside risk increasing if they dont sell Equitix and we go back to "this will never work" land, but still probably good for another 40-80% if they do sell. ($40 NAV re-rate to 0.7x w/ large capital return = $28, or $37 NAV re-rate to 0.6x = $22.2).

-

it's done for every president https://www.marketplace.org/2018/12/05/stock-market-close-day-mourning-president-bush-history/

-

ha yes, when value guys had it easy!

-

Overall made about 15%. Since tracking a consolidated number (2017) of all accounts, I've made +14.9%/yr while the S&P 500 has made 14.7% / year with greater tax efficiency and lower effort for SPY. Since May 2013, my consolidated IBKR accounts which are the bulk of my investments have made 14.4%/yr on a time weighted basis and 15.7% IRR, vs 13.5% for the S&P 500 (again with better tax efficiency and no effort favoring the index Since August 2016, my fidelity accounts have made 11.3%/yr on a time weighted basis vs the market's 14.4%. for the time frame that this account underperformed it was small so money weighted would be a lot better but don't have that data. Regarding 2024, I'd repeat 2023 and say that I deserved to underperform this year. I haven't owned the market's best performing businesses (fundamentally) and haven't found high conviction in a lot of stuff. Have been running overly diversified and low-ish risk and shouldn't expect to keep up in a year like last. I expect to continue to underperform should the environment remain similar. I'm 12 or so years into this and it's unclear that I've added any value, but on an absolute basis, I'm satisfied. I've done a little better than the index owning very little tech, but no points for difficulty. my investment accounts are about 50% of my net worth, with 32% or so being in a trust which i don't control but receive distributions (primarily invested in indices), and the remainder in home equity. 2024: +15% 2023: +18% 2022: +4.5% 2021: +55% 2020: +2% 2019: +20% 2018: -2% 2017: +15%

-

https://www.bankofutica.com/about/tv-commercials/ethnic-restaurants.php 13%-er at average of $440 (started at $372 ended at $500+) yea, I'm a crazy person

-

1) it’s a PFIC. 2) thesis is that it’s largest asset (equitix) is rumored to be for sale at a significant premium to NAV; if rumor and price prove true, will generate about 100% of market cap in cash and NAV will increase and be significantly de-risked. Has traded up from 28% ish of NAV to 40% of NAV. I significantly increased my long held position. The company confirmed they are exploring alternatives for the Equitix and also changed their methodology of how they value it.

-

unless one's thesis was hinged upon the CEO (which technically this wasn't the CEO of the whole group), I would regard this as immaterial to the earnings power of the company / a non-event from a stock perspective. if a CEO/CFO killed himself, I'd be more concerned about fraud, but murder wouldn't concern me as a shareholder.

-

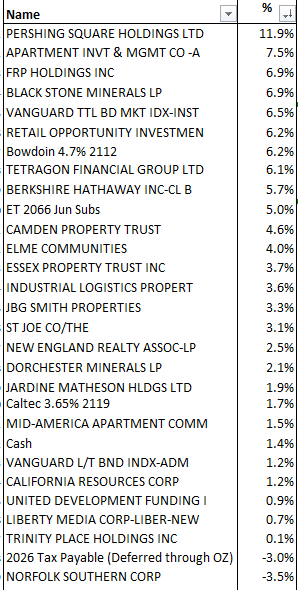

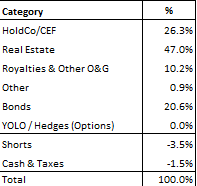

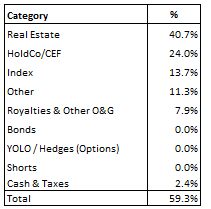

zzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzzz this inspired me to look at my portfolio / update my spreadsheet....I kind of hate it at the moment. bunch of stale things and mediocre ideas at immaterial sizing. been buying a fair bit of #1 and #4, but 4's pretty illiquid / don't want to pump it given I've already moved price up a fair bit.

-

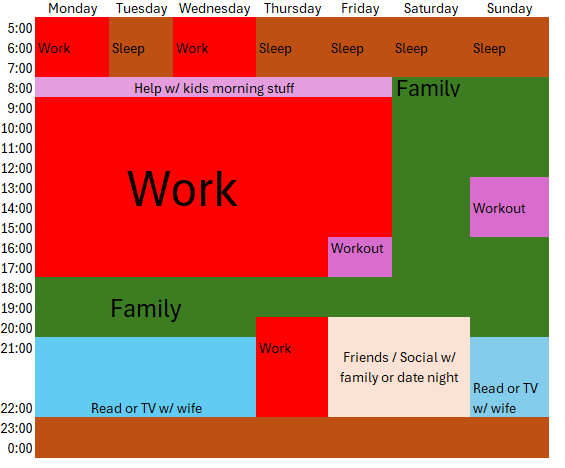

i do travel ~3-4 weeks/year in total and do have to work more occasionally. I hold 7-8AM, 5-8PM as sacred for my young kid. If I need to get more done, I wake up at 4:30 or get it done at night in lieu of the reading. also have calls late at night but generally able to schedule b/w 8-10PM. but yea, I'm lucky. many have to travel more / work more hours. also helpful, I've optimized for a short commute and work home 1-2 days/wk.

-

something like this probably should work out more....

-

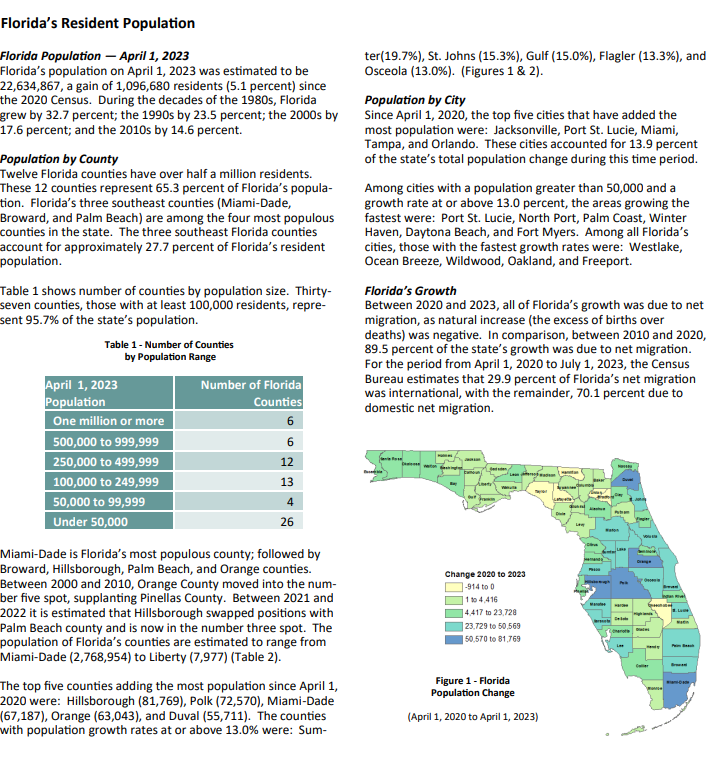

sorry if I'm not following; on which region/s of florida do you have a positive/negative view?

-

my family all lives inf south Florida, know lots of realtors / homeowners etc. I've not heard a peep about decreasing demand. some other family on west coast got hit pretty hard by irma, including one in property management / RE who had to repair a bunch of stuff across 50+ properties. rebuilt and back to record rental rates/values. interesting disconnect between your anecdata and mine. the data is quite clear regarding net migration of people and even more clear regarding migration of income / assets. are you saying you expect this to reverse based on what people in your circle are saying? what is clear is that old condo's are facing huge assessments / pockets of distress because they're old and need a lot of capital investment, but not clear to me how that clouds/changes the overall story.