nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

The butterfly flapped it’s wings… $100 bn and counting Adani Crisis Deepens as Stock Rout Hits $107 Billion, Bonds Sink Gautam Adani’s businesses have lost $107 billion in a week, one of the biggest wipeouts in India’s history, after an explosive report by short-seller Hindenburg Research forced him to pull a stock sale at the 11th hour and led some lenders to reject his securities as collateral for client trades. https://www.bloomberg.com/news/articles/2023-02-02/adani-stock-rout-deepens-after-flagship-firm-pulls-share-sale

-

Go Charlie All this wild and wooly capitalism is much like that described in a remark often attributed to Mark Twain, who was thought to have said that “a mine is a hole in the ground with a liar on top.” Such wretched excess has gone on because there is a gap in regulation. A cryptocurrency is not a currency, not a commodity, and not a security. Instead, it’s a gambling contract with a nearly 100% edge for the house, entered into in a country where gambling contracts are traditionally regulated only by states that compete in laxity. Obviously the U.S. should now enact a new federal law that prevents this from happening. Why America Should Ban Crypto - WSJ

-

Thanks for correcting this, I should have gross error checked from first principles. I Fat-fingered and edited the currency conversion on your spreadsheet mistaking it for the share price. The good thing is the share price is rapidly moving away from the FX rate

-

Two steps forward one step back. With the allegations against Adani doing the rounds, perhaps we can read something positive into the knockbacks from SEBI. India's Digit Insurance to revamp $440 mln IPO again after regulator concerns | Reuters

-

For the moment . Eurobank is on a tear, +17% for the month or looking at it another way, +$400m to FFH. Fitch recently upgraded them saying "The upgrades reflect the structural improvements to Eurobank's profitability as a result of its successful de-risking and restructuring, supported by rising interest rates and economic growth in Greece. Buffers over regulatory capital requirement have strengthened and we expect internal capital generation to continue supporting metrics. The upgrade also reflects that Eurobank's funding stability and diversification have improved following consistent deposit growth and recent wholesale debt issuances. The expected resilience of the Greek economy in 2023, even in light of prevailing uncertainty, further underpin the upgrade." Fitch Upgrades Eurobank to 'BB-'; Outlook Stable (fitchratings.com)

-

The context is very helpful. Thanks for the link

-

Enough to strike terror into the heart of any investor with more than one cycle under their belts

-

@Xerxes correct me if I'm wrong but to paraphrase, short covering rallies can steal the bid from value stocks. Voting machine vs longer term weighing machine. Also to pipe in on the above discussion, I assume Fairfax is a 10-11% compounder over the longer term that also spits out 2% (based on its recent lows) and should be valued at a minimum 1.1 to 1.2 x's and that includes a margin of safety. If their Indian bets pay off then 1.4-1.5 is fair. Personally, I love the exposure to India but I also have my largest holding (by a smaller margin than 6 months ago) in Berkshire that cast's a wary eye on that mix of demographic opportunity and potential corruption to the core.

-

Adani Group: How The World’s 3rd Richest Man Is Pulling The Largest Con In Corporate History https://hindenburgresearch.com/adani/ Still playing catch up after the holidays but I believe Adani was one of the parties who submitted an EOI for IDBI Bank

-

Awesome, your massive alpha this year is well deserved.

-

Down 2% exc Divs. Biggest losers AAPL, KMX, 0669.HK. Offset by ATCO, Fairfax, and to a lesser extent MKL and BRK.A

-

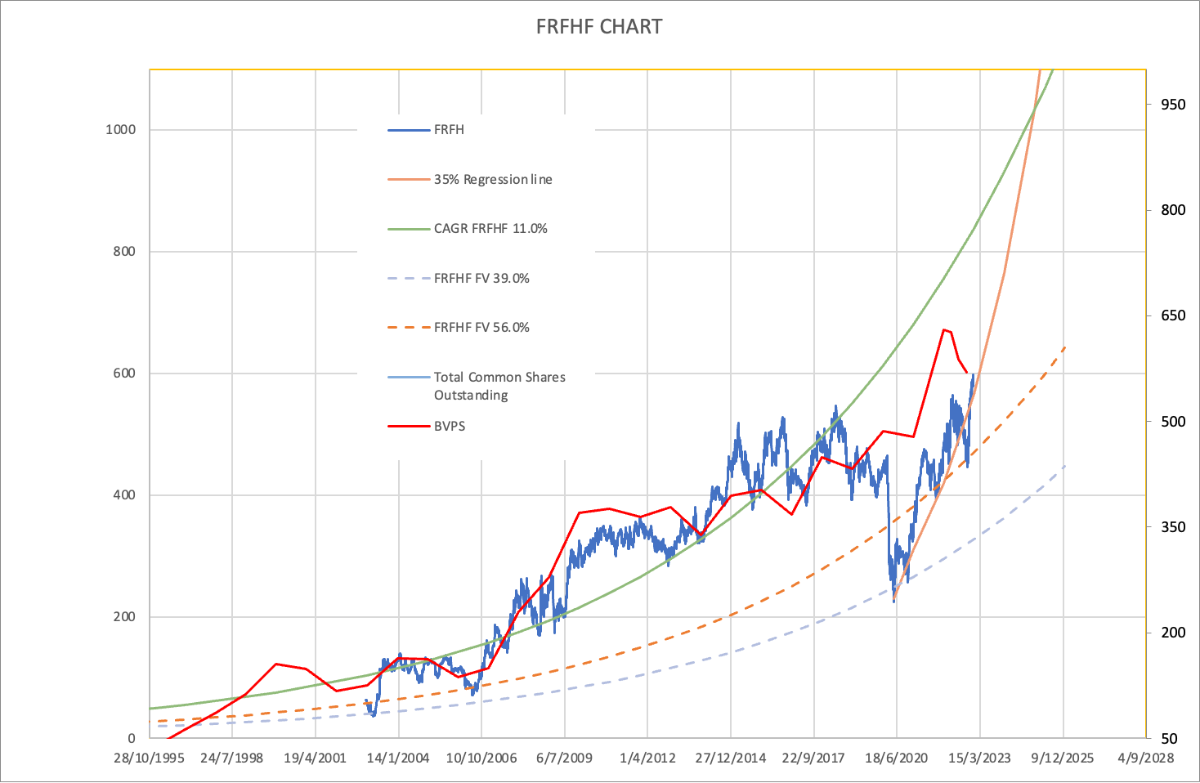

Personally I think Fairfax have passed their biggest test and that was the bond portfolio. Not reaching for yield and flipping from an deflationary bias to an inflationary bias should set them up for peer outperformance for the foreseeable future. If you take the view that that their bond prowess goes a long way to offsetting some of the investment clunkers then it is not hard to form a conservative view that they are worth of at least a 11% CAGR over the longer term. Their regression to this mean of 35%CAGR from the COVID lows is still intact, more an observation than a prediction. I won't be relying on $US1000 by YE 24 but it wouldn't surprise me either. It's also be done to death, but the decision to become members of "shorters anonymous" should make returns more predictable. However, I often wonder a little bit if their shorts may have been in the black overall but I would take what is a slightly more humble Fairfax compared to the company I sold out of completely in 2019.

-

Merry Christmas all. Thanks to everyone for such fascinating food for thought. Sanjeev thanks for all your hard work again this year to facilitate such a great site

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Good one. Interesting to see Apple has signed up for second season of Bad Sisters. https://bgr.com/entertainment/apple-tv-plus-just-renewed-bad-sisters-one-of-its-best-reviewed-shows/ -

As far as I can tell that is all they need. However, I am somewhat surprised that Fairfax hasn’t issued a press release. I think it is a development worthy of a one-pager. This leads me to think that there might be more to it.

-

Thanks for the heads up. A couple of points grabbed my attention ‘We continue to believe Berkshire is best positioned to get the most value out of Alleghany—something we don't feel the market fully appreciates” Allegheny is mentioned a couple of times and reflects the thesis that it’s investments under Berkshire will be redeployed at higher rates of return “We view Berkshire's decentralized business model, broad business diversification, high cash-generation capabilities, and unmatched balance sheet strength as true differentiators for the firm. While these advantages have been overshadowed during much of the past decade by the company's ever expanding cash balances—which have earned next to nothing in near-zero short-term interest rate environments—we believe the company has finally hit a nexus where it is focused on reducing its cash hoard through a mixture of stock investments and share repurchases. Over the past 12 calendar quarters, the company has repurchased $41 billion worth of its common stock, equivalent to $3.4 billion per quarter on average, which has eliminated close to 10% of the company's total shares outstanding. The company has also pursued higher dividend yielding securities when purchasing equity securities the past several quarters.” I have been thinking that this is shaping up to be quite the decade for Berkshire thanks to Buffett’s incredible patience. “We've increased our fair value estimate for Berkshire Hathaway to $370 per Class B share (from $357) after updating our forecasts for the company's operating businesses and insurance investment portfolio. Our new fair value estimate is equivalent to 1.69, 1.45, and 1.33 times our estimates for Berkshire's book value per share at the end of 2022, 2023, and 2024, respectively. For some perspective, during the past five (10) years, the shares have traded at an average of 1.40 (1.39) times trailing calendar quarter-end book value per share. We use a 9.0% cost of equity in our valuation and assume that Berkshire pays a minimum of 15% corporate alternative minimum tax on adjusted financial statement income for taxable years beginning in 2023.” 1.69 x’s book is pretty optimistic IMHO, but is perhaps reflective of the shares repurchased to date. brk.b - berkshire hathaway analysis & rating - nyse morningstar.pdf

-

NTDOY

-

Awesome, @Hoodlum you made my day and no doubt many others

-

Interesting thought. Personally, I was more relieved by a high profile Charlie Munger style “public hanging”. Hence Sokol’s comments struck me as very odd and added to my feelings of unease about the guy.

-

Totally agree, not sure how this one will work for Fairfax shareholders of which I am one. It beggars belief that Sokol even needs to wade into this.

-

MS blue paper on India attached. Thanks @Vikingfor the friendly reminder. Key takeaways: India’s GDP is likely to surpass US$7.5trn by 2031, more than double current levels, making it the third-largest economy and adding about US$500bn per annum on an incremental basis over the decade. India's market capitalization will likely grow by over 11% annually, to US$10trn, in the coming decade. We estimate that manufacturing's share of GDP will rise to 21% by 2031, implying an incremental U$1trn manufacturing opportunity. We expect India’s global export market share to more than double to 4.5% by 2031, providing an incremental US$1.2trn export opportunity. India’s services exports will almost treble to US$527bn (from US$178bn in 2021) over the next decade. Credit to GDP rises from 57% to 100%, implying compound annual growth in credit of 17% over 10 years. India's per capita income rises from US$2,278 now to US$5,242 in 2031, setting the stage for a discretionary spending boom. The number of households earning in excess of US$35,000/year is likely to rise fivefold in the coming decade, to over 25mn. US$1.1trn incremental retail opportunity in ten years. E-commerce penetration to nearly double from 6.5% to 12.3% by 2031. Internet users in India to increase from 650mn to 960mn while online shoppers will grow from 250mn to 700mn over the next 10 years. 25% of incremental global carsales over 2021-2030 will be from India, and we expect 30% of 2030 PV sales to be EVs. India should hit a major inflection point for the next residential property boom in 2030 – aconfluence of high per-capita income, a mid-30s median age, and higher urbanization. India’s work force in the technology services sector to more than double from 5.1mn in 2021 to 12.2mn in 2031, leading to an increase in office absorption from 32-35msf pa to a run-rate of 45-50msf over the next 5-10 years. Healthcare penetration in India can rise from 30-40% now to 60-70%; implying 400mn new entrants to the formal healthcare system. The defense budget (US$18bn)is growing steadily(10%CAGR)–traditionally there has been large import dependence (about 60%) but there is now a strong thrust towards local manufacturing. US$700bn+in energy investments over the next decade as India accelerates its energy transition. thenew_20221031_0000.pdf

-

-

Fascinating purchase by Berkshire. A couple of thoughts. 1. Is this a cheap way to ride the Apple juggernaut? 2. Is this more Munger than Buffett? Charlie being interviewed tomorrow on CNBC - coincidence? 3. TSMC were down another 10% from the end of Q3 so perhaps this position is closer to $5-6bn (taken into account the bounce and Buffett pop). 4. Would the recent discussions of 3nm manufacture in the USA figure at all i.e. more USA exposure less China risk.

-

Decent bump in the MU position https://www.dataroma.com/m/holdings.php?m=FFH

-

Interesting. This link was paywalled for me but this one seems like a reprint https://newsboring.com/adani-eyes-stake-at-bengaluru-airport-news-boring/ So it sounds like rumours were kind of right, it sounds like Adani has been in talks with Fairfax, perhaps a joint bid, for the forthcoming 13% Airports Authority of India (AAI) stake. Easy to see why they have been raising cash, Prem thinks there are some fat pitches coming his way. MS was out recently with a breathless piece on why this will be India’s decade. I will post it in the macro thread. Some excerpts: “We believe India is set to become the world’s third-largest economy and stock market by the end of this decade. As a consequence, India is gaining power in the world economy, and in our opinion these idiosyncratic changes imply a once-in-a-generation shift and an opportunity for investors and companies.” “If India is already the 'office to the world', it is increasingly becoming its factory as well. We anticipate a wave of manufacturing capex owing to government policies aimed at lifting corporate profits' share of GDP via tax cuts and hard dollars for investing in specific sectors, and we note that performance-linked incentive (PLI) schemes now total US$33bn across 14 sectors. Multinationals are more optimistic than ever about investing in India, as the alltime high on our MNC Sentiment Index shows ( Exhibit 37 ), and the government is encouraging investment by both building infrastructure and supplying land for factories. The trends outlined in Morgan Stanley’s multipolar world thesis and cheap labor add to the mix. We estimate that manufacturing's share of GDP will rise from 15.6% currently to 21% by 2031, which implies nominal output jumping from US$447bn to about US$1.49trn” I think there is value in India but there is a material sovereign risk too. However, if it does come to pass, assets like the BIAL are going to look very cheap in hindsight and potentially insanely cheap in USD terms. FFH remains my preferred way to gain EM exposure.