nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Apple Car Play and L3 merc is pretty compelling. I know it was kind of laughed at WWDC this year as a bit of non-stat but I am definitely one of the 79% that would only consider Carplay. I understand Tesla wanting to own their own stack but I could never consider one of their vehicles because I am so entrenched in Apple. Merc all the way for us, kind of like a much lower version of Buffett's "indefensible" but it gives us joy every time we drive. Yep, if European regulator's want to blow up Tesla's autopilolt, the easiest way to do it is to require redundancy in the form of Lidar. I wouldn't argue with that view. The Tesla strawman argument saying that as humans we don't navigate by shooting lasers out of our eyes is plain silly. I dare say we may just be doing that via AR glasses in the next 10 years. Digital evolution. -

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Yep first to L3, might be a bit of European favouritism. Mercedes opens sales of Level 3 self-driving system on S-Class, EQS | Automotive News Europe (autonews.com) Thanks for the link btw. I have been toying with buying some shares at this level, a great brand. Very much the Apple of the auto universe which is why I have held off . It wouldn't happen but a JV with those two brands would be super compelling. Never seen the numbers but I would posit the vast majority of Mercedes owners would also be iphone owners. -

The 260’s are a good entry point. Kelly optimise if the opportunity presents. The probability of permanent capital loss over a 3-5 year period is very low IMHO.

-

BRK.B

-

Agree, especially the observation re talking book on Twitter. Still I find the longer form interviews one Blockworks Macro are illuminating. There are lots of dislocations in the energy market at the moment that will be resolved in the usual way in that the high price of oil solves the issue of the high price of oil one way or the other. Short term though, given the oil price feeding into most things, I am left wondering how interest rate increases will resolve the inflation issue. Short term it would appear that the price of oil, prior to a more complete energy transition, is a better proxy of hurdle rate while the fed catches up.

-

Interesting interview with Josh Young - Covers his Sandridge position in detail - Lays out his thinking in terms of oil price rising to $130-140/bbl which finally leads to demand destruction, oil drops 30% to 90-100> Stimulus then leads to all time inflation adjusted high for oil -TOTAL and Shell competing to blow up the most shareholder capital - renewables/powegen not their core competency - Interesting commentary on OXY. Much better values to be found in smaller names. Cultural issues at the company according to his contacts. 1:08:14

-

That’s a big call. i think starting from a 20-25% discount to stated book value has a lot to do with the it. I will take the outperformance but won’t be taking any victory laps too soon. Personally i think the current situation actually favours Berkshire more than Fairfax. At some point inflation, running at these levels, is going to kick the crap out of insurance companies even with a hard market. Buffett has been preparing Berkshire for that moment, I hope Prem has too. A couple of decent Cat 5’s or an earthquake or two would be just the way to round out 2022. I hope not, just sayin’.

-

Paste the link and I will see what I can do

-

@Viking Great video. My favourite moment, when George looks into the camera and referring to Cathy Wood says, "This market will not bottom until she loses all her assets" cheers nwoodman

-

Good to hear a date, October 2022, for T2

-

A very impressive set of results for Digit. They have now crossed the RS 5000 crore (USD650M) in GWP "Digit insurance said that in terms of written premiums in a year, the growth was seen at 62 per cent in FY21-22 whereas the industry on an average grew by 10.9 per cent. In FY21-22, across all products, Digit sold over 77.6 lakh policies, an increase of 40 per cent compared to the previous financial year. Further, the company’s health portfolio saw a growth of 132 per cent over FY20-21, led by group business." Digit Insurance crosses Rs 5,000 crore yearly revenue milestone - BusinessToday Digit Insurance rakes in over INR50bn in GWP | Insurance Business Asia (insurancebusinessmag.com)

-

Now posted https://s1.q4cdn.com/579586326/files/doc_presentations/2022/Fairfax-2022-AGM.pdf

-

At first pass, it looks fantastic. CR 93.1%. A hit to the bond portfolio but that was expected, but they faired better than most . BV 626. Given the absolute macro craziness of the first quarter, I say well played Fairfax!

-

KMX, OXY

-

New CEO at Digit https://www.livemint.com/insurance/news/digit-insurance-appoints-jasleen-kohli-as-new-md-and-ceo/amp-11650348439787.html The 42-year-old Jasleen Kohli will be one of the youngest CEOs in the insurance industry, as per the company release With 19 years worth of experience in the life and general insurance industry, Kohli last served as the director at Allianz Technology before joining Digit as the CDO in 2017

-

+1, greatly appreciated @gfp

-

An inconsequential position in KMX

-

Trimmed BRK.B, FRFHF, USAP, ATCO, AAPL. Exited DIS, BAM, BABA. all very small positions. Mainly tax matching and reducing the risk of sleep walking into a potential margin call if this really gets a head of steam up. We shall see. I can’t think of a better inflation pass thru entity than Berkshire but the market is thinking the same and has bid it accordingly, as much as I hate to say it I don’t want to get caught out on a mortality trade. The 50-60% drawdown test is all too real.

-

Excellent news. Thanks for the link

-

Sure is. I think it is going to catch a lot of investors by surprise, in a good way. https://indianexpress.com/article/cities/bangalore/international-departures-increase-25-each-day-bengaluru-airport-7846332/

-

Was trying to triangulate it with other sources too, but first read about it here https://www.zerohedge.com/energy/gazprom-halts-gas-shipments-europe-critical-pipeline

-

Spot on. I think the price/IV has only closed marginally. I was always a little gun shy about some of their marks, what is becoming apparent to me is that there are plenty of unrecognised gems too. As Munger said “Sit on your ass. You’re paying less to brokers, you’re listening to less nonsense, and if it works, the tax system gives you an extra one, two, or three percentage points per annum.” I don’t think it is falling in love with companies per se it is more I hate paying tax. I will be more than happy if this closes the IV gap over 3-5 years and then performs at inflation + 7% over rolling 5 year periods. Happy with lumpy as long as they are not blowing up capital as per the past 10 years. This then makes it margin-able and as an investment it’s utility improves greatly for my purposes. Everything that I am seeing at the moment seems to suggest this will prove to be the case. A small amount of margin and large unrealised tax liabilities seems to work out OK over the long run as long as the underlying investments keep on keeping on.

-

The following article suggests India’s position may be improved by the current crisis but they can’t overplay their hand. India’s value as a democracy and capacity as the only other military power able to push back against Chinese aggression in Asia is not lost on the Quad. But a lot will depend on how well India — more nimble under Modi — articulates its position on Ukraine. “India is today in an enviable position because of years of careful diplomacy, and fortuitous geo-politics,” Aparna Pande, a South Asia expert at the Hudson Institute, a Washington DC think tank, told CNBC. “The US and its partners — in Europe and Asia — need India on their side in the long-term peer competition with China. They are, therefore, more understanding of India’s predicament.” But Pande cautioned that India’s reluctance, as a democracy and as a key member of the Indo-Pacific to support the liberal international order will be remembered. India faces a stark choice, said Bruce Bennett from the Rand Corporation, a think tank headquartered in Santa Monica, California. “The key question is whether India will want to be known as a principled country or a nationalistic country. A principled country stands up against any violation of national boundaries, whether it is Russia invading the Ukraine or China invading parts of India,” he said. “If India decides to ‘sit on the fence’ to maximize its national leverage and influence, I think many people around the world will lose sympathy for India’s concerns about its own territorial integrity.” https://www.cnbc.com/2022/03/24/india-is-in-a-sweet-spot-courted-by-the-quad-china-and-russia.html

-

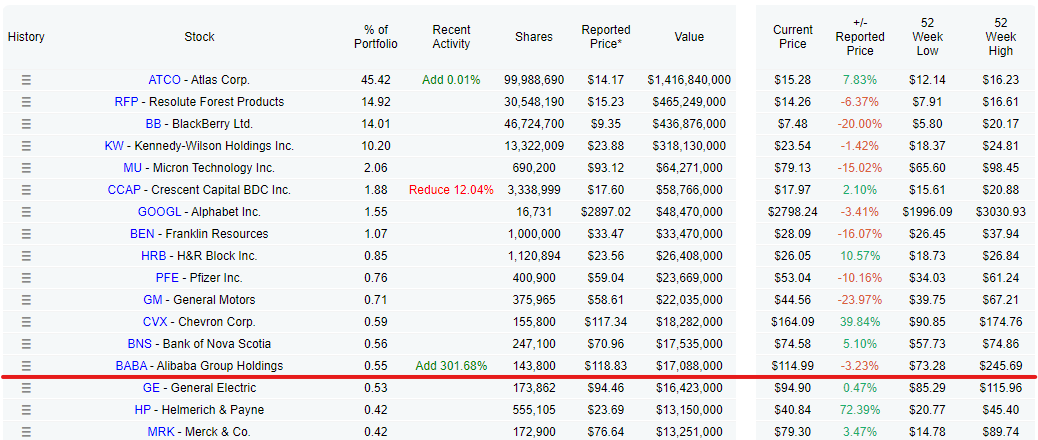

It won't be material but it will be interesting to see if they increased their stake in BABA significantly during the recent sell off

-

Morningstar’s Greg Warren on the Alleghany deal “We expect to increase our fair value estimate for Berkshire Hathaway (BRK.B) by 3%-5% following news that the wide-moat firm has agreed to acquire the outstanding equity of Alleghany, a property/casualty insurer with reinsurance and specialty insurance lines, for $11.6 billion. While the deal seems pricey at first glance, with Berkshire offering $848.02 per share in cash for Alleghany--a 29% premium to Alleghany's average stock price over the last 30 days (and a 16% premium to the firm's 52-week high closing price)-the acquisition price works out to a multiple of 1.26 times Alleghany's book value per share at the end of 2021. Berkshire has been buying back its own common stock for an average of 1.37 times prior quarter book value per share the past year, so a premium that lifts the deal price for Alleghany up to 1.26 times book seems reasonable to us from a price perspective. That said, we'll have to see how much value Berkshire can extract from Alleghany's insurance operations, noting that insurance deals can be tricky as the acquirer is assuming potential future claims established by the acquired firm's past underwriting. While Alleghany's inability to generate excess returns on a consistent basis could be a sign of underwriting weakness, we'd note that the firm's reinsurance arm (which can be hit with large catastrophe losses at any given time) have had a greater influence on overall results the past decade. We'll also have to see how Berkshire handles the investment portfolio at Alleghany, which has been dedicated more to bonds (80%-85% of holdings the past two years) than equities (15%-20%), the complete opposite of Berkshire's insurance operations (which has had 80%-85% invested in equities). Should Berkshire avoid unforeseen underwriting issues and reallocate the acquired investment portfolio to more lucrative options, this could end up being a good deal (something Berkshire has struggled to find for much of the past decade).”