nwoodman

-

Posts

1,390 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Haven’t fully crunched the numbers but this growth in lending seems somewhat higher than GDP growth. Eyeballing it seems around 12-13% CAGR over the 9 years from the graph. Something to keep an eye on and a good test for the RBI. https://asia.nikkei.com/Business/Business-Spotlight/Indian-consumer-borrowing-surges-raising-fears-of-defaults “The central bank's change of risk weightings could prod lenders to increase rates, thereby discouraging consumers from reckless borrowing, analysts say. If banks choose to absorb the cost, their margins will shrink, making unsecured loans a less attractive segment. Financial services company Paytm said in a statement that it would reduce the disbursal of small loans "on the back of recent macro development and regulatory guidance." "That nudge from RBI to be cautious on unsecured retail lending can push lenders to slow growth in this segment, which can also impact overall bank credit growth by up to 100 basis points," research company Jefferies wrote in a note.”

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Now that’s my kind of funeral. RIP Shane McGowan Full Service https://www.youtube.com/live/tO8rWUq1U_A?si=_JmDkmBHp6CEmj8h -

Great post, but are you seeing something across the entire entity less stat requirements that can’t be solved “in a stroke of a pen” or is it more a sub risk. Along the lines of we had liquidity but it was good until reached for but has now ceased to exist. I.e multi cats.

-

-

I will leave it to more intelligent participants to answer your question directly. However, I did enjoy the body of your post especially the examples. My feeling it was a conscious decision by Charlie in terms of the problems he enjoyed thinking about and solving. I doubt going from $20m to $2bn for Charlie made that much of a difference in terms of lifestyle anyway. From what I can gather though he thoroughly loved giving it away and getting to use both sides of his brain. What an amazing man.

-

Am I wrong in seeing this as simply debt recycling and not really news? I don’t see it as necessarily improving medium term liquidity in itself at the HoldCo, but I question whether this is a real problem anyway. It is silly for me to even remotely make a comparison to my own situation but I see the cash balance in a sub as transferrable in minutes, so the aggregate cash is my primary concern. I realise that there are tighter regulatory controls for insurance Co’s. I think all being equal, their ability to generate profits that I thought were 5 years off, fixes this issue nicely.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I agree, it's almost a little over produced. Definitely a band that delivers live though. I had the good fortune to see another Australian export, Parkway Drive at Knottfest earlier this year. They blew me and the crowd away. Got home and listened to a few of their albums and it was the same deal, something seemed to be missing. As you say, some bands/ music styles are just better live. -

Thanks @SafetyinNumbers. That multiple is mighty impressive. “That is a near-30 per cent premium to Heathrow's regulated asset base. It is also about 13 times next year's ebitda, projected to fall given the cut in regulated landing fees. Listed competitors travel at around 10 times. Vinci, which bought 50.1 per cent of Gatwick in 2018, paid more, but that was for a pre-pandemic majority purchase. Ardian and PIF might end up stuck at 25 percent.”

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I am amazed he lasted this long! Great band, Fairy Tale of New York and A Pair of Brown Eyes are my faves. -

Cheers, paywalled for me. Any additional metrics or info? Thanks @netcash1 for flagging this

-

Such a formative figure and at the top of his game to the very last. “We all are learning, modifying, or destroying ideas all the time. Rapid destruction of your ideas when the time is right is one of the most valuable qualities you can acquire. You must force yourself to consider arguments on the other side” In terms of his framework invert to solve, the courage to blow up your best idea and arguing both sides of an argument were a game changer for me. Still haven’t mastered it, but at least he made me aware.

-

Me too, Fairfax look like they have kicked a real nugget here. I note that Foran recently bought options on up to 100% of Denare West, an adjacent property from Purepoint. The recent drilling program looks good too, with further evidence that Tesla and MB are linked. https://purepoint.ca/news/purepoint-uranium-enters-into-option-agreement-with-foran-mining-corporation-for-the-denare-west-project/

-

I guess more mouths to feed at Recipe restaurants is a good thing. These mass immigration policies are typically hell bent on nominal GDP growth rather than the thing that matters to the current population, GDP/capita growth. If there is stagnant or even declining living standards then there inevitably will be push back. These immigrants get old too, so is a bit of a Ponzi scheme in that respect. This is not to say immigration per se is bad, just that it needs to be measured and not a means of plastering over other poor economic choices.

-

If you look at past actions, I think SJ is suggesting that you need to be a little wary. In no way is he suggesting running for the hills, it is just something to keep in mind. Probabilistically if you are a passive minority shareholder in a sub that Fairfax controls, the chances of getting screwed are reasonable; as a direct investor in Fairfax, it is low but not zero etc. That's why, for me, Farmers Edge isn't about the money. It is the effect on their reputation. However Fairfax has been flipping assets on and off the markets for as long as I have been following them, they seem to get away with it despite what I think. This ain't Berkshire and that's fine with me because I have plenty invested already in that name.

-

In general, Deal flow is super important, as well as the ability to say no. Buffet's Hang, Your Life's work in the Berkshire gallery, hasn't worked well but hasn't held them back in terms of decent returns. Fairfax seems to create a lot of optionality. This used to be levered, but these days, it seems to be cleverer and more Berkshire-like in terms of optionality that doesn't bet the farm. i.e heads, I win tails I don't lose to much. Not sure I see any massive moat, but the balance sheet has improved significantly, and for decent capital allocators, being the strong hand is good enough for me. Keenly waiting to see if Atlas/Poseidon is an albatross around the neck or not. So far, it seems to be a non-contributor rather than a cash sucker which is pretty good for an early Fairfax investment.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I have meant to post the musical discovery epiphany that is radio station KEXP, out of Seattle, Washington. They have been putting together live shows on YouTube for years now. Some key finds for me : Pigsx7 (UK) - Stoner Metal at its finest. Seeing them live in December, can't wait Aurora (NOR) - reminds me a little of Bjork, maybe Sugar Cubes but different. Definitely Scandinavian eclectic SLIFT (FR) - Guitar at its finest. They do a set (SLIFT-Levitation Sessions) at the CEMES laboratory which is even better Amyl and The Sniffers (AU) - punks not dead baby! Saw them supporting Smashing Pumpkins a while back and Amy is a force to be reckoned with The list of artists that have recorded live with them is pretty impressive, and worth a peruse if you are feeling a little rusted on. -

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

+1. We grew up on very similar musical diets. It's interesting, although they were my faves of the day on a road trip now we are more likely to favour grunge such as Alice in Chains, Pearl Jam and even that Canadian gift The Tea Party....one of the seminal gigs of my life. -

I don’t see this as a positive at all. It provides further validity to the market’s view that Fairfax IPO’s are not to be touched with a 10’ pole. Perhaps a bit negative but I just wish they wouldn’t stuff around with these crappy positions.

-

Minor upgrade to Eurobank from Nida Iqbal at Morgan Stanley on the back of stronger forward guidance. PT €2.01 A strong balance sheet means that Eurobank is one of the the most resilient Greek banks in our coverage. We expect performing loans to grow at a ~5% CAGR in 2023-25. We forecast NIMs to decline ~10bps in 2024 followed by a 18bps contraction in 2025, as we expect the rate-cutting cycle to begin in 2Q24, thus driving asset yields lower. 3Q23 NPE ratio stood at 5.0%; we forecast it to reach 3.9% by 2025. However, we remain Equal-weight on the shares as we see a more defensive deposit beta in NBG in the coming quarters.

-

Just got through the KW CC. Interesting to see they picked up so many of the Pacwest team. “For example, in June, we sourced and acquired off market a $4.1 billion construction loan portfolio from a regional bank at a discount, representing the largest single transaction in our company’s history. This transaction was possible given our reputation in the banking industry and our ability to move with speed and certainty to get a transaction of this size closed inside of 30 days.” “During Q3, we welcomed 40 new employees from the regional bank I mentioned, who have integrated perfectly into our existing operations and considerably strengthened our lending capabilities. We are currently one of the few active construction lenders in the U.S. market, and our team has a strong pipeline of new loans, of which a significant amount will close here in the fourth quarter.”

-

Certainly is interesting at these levels. Flies in the face of my resolution to never to invest in a FFH holding but I do have respect for Bill.

-

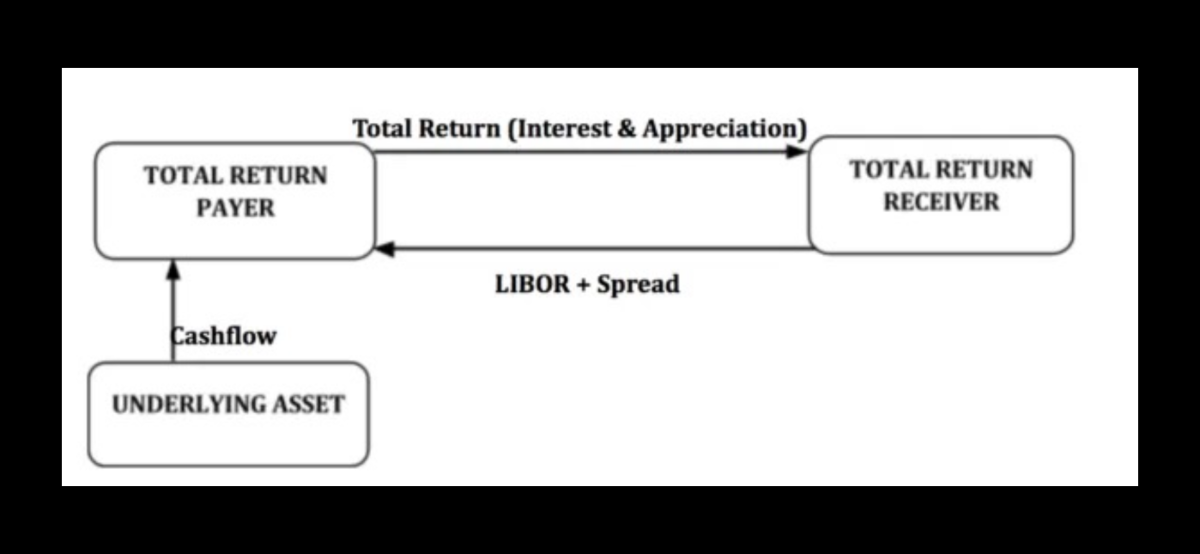

+1 Reposting the link to TRS below because it is important to understand this is a well considered directional bet that @StubbleJumper points out could unwind in a heart beat with a big market sell off, not to mention the cost to finance is now material. It's worked out great but the risk reward has now narrowed considerably. My expectation is they ditch this around 1.1-1.2x’s book, Prem’s $1000 per share. I won’t be disappointed to see this levered play disappear this financial year or early next year at the latest.. https://corporatefinanceinstitute.com/resources/derivatives/total-return-swap-trs/#

-

Why would they? Fairfax is renting their balance sheet. Fairfax is the one placing a directional bet not the counterparty. They are Fairfax “agnostic”.

-

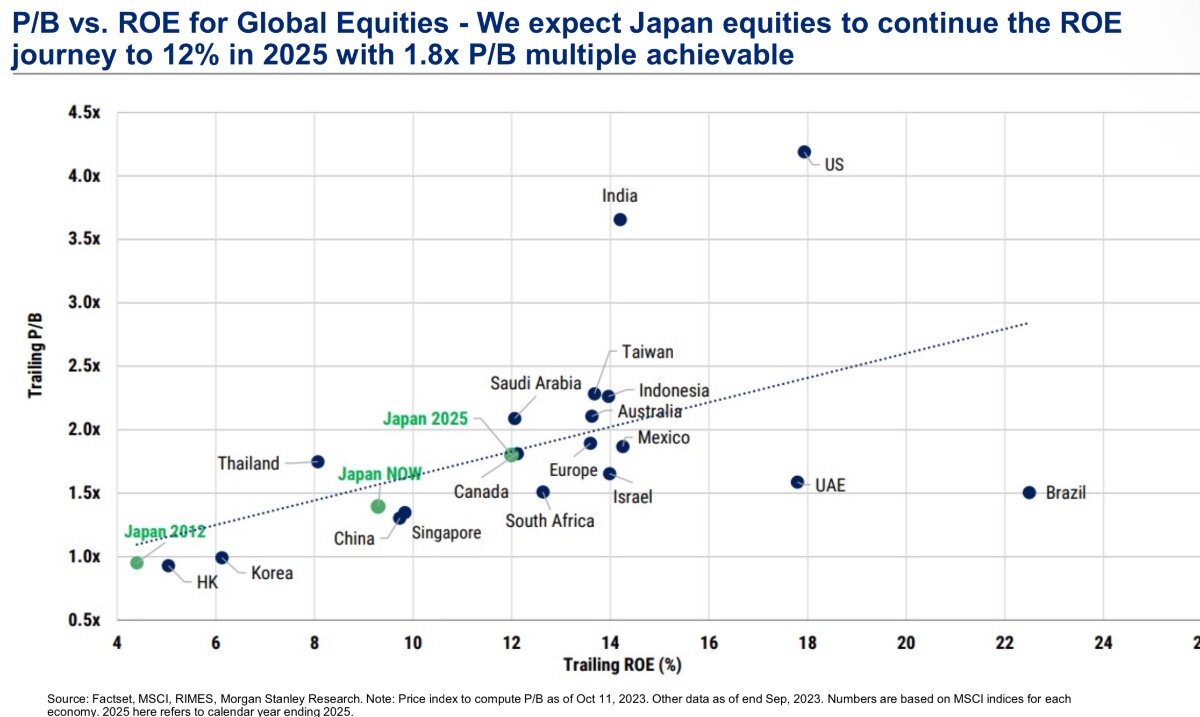

MS put out a note on Japanese prospects (attached) which may be of interest to some here. They offer the following: “Sustained reflation and rising productivity at the macro level - working in combination with improved corporate governance at the micro level - will likely drive further improvement in corporate profitability in Japan. We raise our forecast for MSCI Japan Return on Equity to 12% (from 11%) by year-end 2025. This would be almost 2.5x the level when Abenomics was launched in late 2012. In turn, that will likely drive further valuation re-rating from 14x P/B to 1.8x and market outperformance versus global equity peers.” japan_20231017_2000.pdf

-

Some speculation on how the current Canadian/India frostiness may affect the sale process for IDBI bank https://www.thehindubusinessline.com/money-and-banking/idbi-bank-divestment-indo-canadian-spat-may-dim-fairfaxs-chance/article67427015.ece "Fairfax India Holdings, the investment arm of Indian-origin Canadian billionaire Prem Watsa, seen as one of the top contenders for IDBI Bank, could now be in the back seat — thanks to the ongoing geopolitical spat between India and Canada. Highly placed sources say with the political tension not easing anytime soon, Fairfax’s is unlikely to be at an advantageous position to secure IDBI Bank in the ongoing divestment process. “If the tension between the two countries escalates or doesn’t end soon, Fairfax may lose its edge in the process,” the source said." Also an update on the timing "Amidst talks of delay in the divestment of IDBI Bank, people close to the development say the process is very much intact and the sale may conclude before March 31, 2024. While the bidding timelines for appointment of asset valuers has been extended from October 9-10 to October 30-31, it is gathered that the delay is more due to change in clauses pertaining to the bidding process based on suggestions received from potential bidders." From what I can gather, the bid is being put forward via Fairfax India and CSB https://bfsi.economictimes.indiatimes.com/news/banking/idbi-bank-sale-rbi-set-to-complete-vetting-of-buyers-bids-likely-early-next-year/104452746 IDBI Current Market Cap INR750 Bn =>$US9.02bn Stake to be sold off 60.7% x $9bn >=> $5.5bn As stated previously, this would be a massive purchase, so I have been wondering, given Eurobank's aspirations for India, whether they might participate in a book build. It's probably too messy, but you never know. OMERS?