Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@cubsfan , as I said, I agree that the US has legitimate grievances with the rest of the world. There are many ways to settle those grievances… All I am trying to do is: 1.) understand/process what Trump is doing, and 2.) the consequences that his actions will have on the US/global economy and stocks over time. I am not the sharpest knife in the drawer. And as of today, I have no idea what Trump’s end game really is and what the impacts to the US/global economy will be. It literally keeps changing every day. Crazy times. Anyways, I apologize for taking this thread into the realm of politics (yes, I am Canadian). So I will stop

-

@John Hjorth , the issue with the US is much more than just tariffs. Tump has decided the best approach to international relations is to run the US like a mafia/cosa nostra organization. He is dealing with long time allies like 1940 and 1950’s Chicago when it was run by the mafia. Think about running a business back then. Or growing up in that neighbourhood. I am not sure fear/intimidation/shakedowns/absolute loyalty/fealty/eliminate opponents is a great way to run the most powerful country in the world. But it is what it is. And the mafia did do some good things for some people back then. So hey, maybe a return to the good old days will be a good thing in the end. ————— Trump definitely has territorial aspirations. Canada. Greenland. Panama Canal. Who knows. But you would have to be an idiot to not take Trump seriously.

-

I don’t think most American’s understand the damage that Trump and his crew are doing to the American brand outside of the US. And Trump is just getting started. It will be punch after punch after punch… People in the rest of the world will respond - they will learn to despise America/Americans as they never have before. Needless to say, that will not be good for US companies doing business in the rest of the world. Something like +30% of revenue from S&P500 companies come from outside of the US. That will likely be moving lower in the coming years. All countries will be looking to decouple from the US wherever they can and as fast as they can (well, if they are smart they will). Because extortionists don’t stop… they keep coming back for more. My guess is fewer foreigners will be vacationing in the US. (My wife - who is not overly political - informed me recently that we will not be taking out annual vacation is the US this year.). And Americans vacationing abroad are likely to get a pretty chilly reception by some local residents. US dollar as the reserve currency? Countries will not have a choice - they will need to find a replacement (over the next decade). Tesla is one small example of what is coming for US companies that do business abroad. Who will be the winners of the ‘dump the US’ movement? Probably lots of European companies. And it’s not a cost thing - when it comes to maintaining/protecting your economy/way of life you do what you have to do. The rest of the world, ex US, is slowly waking up to the new reality. It will take many years for the adjustments to happen (in both the US and the rest of the world). Bottom line, I agree. What is going on with Tesla is different (much more severe and longer lasting) than what happened with Disney and Bud Light. ————— Listen, I am not saying the US does not have legitimate gripes with the rest of the world. But make no mistake, how Trump is doing what he is doing is going to have significant consequences for the America’s (citizens and businesses) standing in the world. If it continues, which I suspect it will (absent a big economic slowdown in the US, which I am not expecting).

-

@bluedevil , a pivotal time for both Markel and Fairfax was 2016 and the Allied World acquisition. I think Markel was interested but the deal did not happen due to ‘culture compatibility concerns’. I wonder if this has something to do with centralization/decentralization organization structures. Fairfax is very decentralized - insurance and investments. My guess is Allied World wanted a parent where AW would be allowed to be run as a stand alone company. Fairfax was the perfect fit. Markel? Do they have a more centralized structure - ie the Markel Way - with head office wanting a say in how things are run? I’m not sure. Prems annual letter this year did a great job of explaining Fairfax’s decentralized structure and its importance to the company. Insurance alone has 250 profit centers - essentially 250 companys being run by entrepreneurs. For this to work, you need someone like Andy at the top. But if you can pull it off, it is very powerful over time. Fairfax’s insurance business is not one company. It is many companies (250): - large and small - located all over the world - exploiting local/different insurance markets It has taken Fairfax decades to build this model. That is why they view it as part of their moat. Makes sense. ————— I worked at Kraft Canada for years - a great example of a highly centralized / top down organization. Very bad at innovation/growing organically so cost cutting/restructuring was constant (very disruptive). Focus at the end of every quarter was hitting the numbers so Wall Street would be happy with senior management/the company. Tail wagging the dog. Good place to work - terrible investment.

-

My view has been that the US - with Trump as president - is engaging in a big science experiment. Not as substantial as Argentina; but there are parallels. The first couple of months has been the Disney phase - lots of talk/actions (and bravado). In recent weeks we are getting to the consequences phase (likely just the start). We are taught that financial markets do not like uncertainty/volatility. Actually it’s worse than that - they HATE uncertainty/volatility. And today, with a pyromaniac in charge, we are now starting to get see some of the fireworks (and they are ‘big’ and ‘beautiful’.) Trump is now trying to shift the narrative - ‘no pain, no gain.’ What do US consumers think? Sentiment surveys are not moving higher - in fact it is quite the opposite. Like the stock market today, my guess is US consumers are not thrilled about losing their job because President Trump thinks its a good idea. If US consumers pull back, the US economy will be in deep shit. Slowing business spending at the same time consumers are pulling back? Not good for the US economy. Actions have consequences. Parents try to teach their kids this universal truth - so they don’t have to learn things the hard way. So I continue to watch Trump with great interest. Americans want someone who will burn things down. Well, Wall Street is burning today. I look forward to capitalizing on the consequences of Trump and his words/actions (groceries are getting put on sale).

-

I think that is the best letter that Prem has ever written. It is full of super valuable information. And it has multiple layers of really good information (for people like me who like to get into the weeds). Great discussion of: The culture/people of Fairfax. The importance of their decentralized operating structure. The insurance business - and its quality. The various equity holdings - including their level of profitability Prem also answered a number of questions that had been circulating on CofBF (how to think about diluted shares etc). And he clearly laid out where Fairfax is today (its fundamentals/prospects) and why it is a great investment. Now compare Prem’s letter to Tom Gaynor’s letter. In terms of giving shareholders useful information to help them understand the company/their investment. There is no comparison - one is like watching a high school basketball game and the other is like watching an NBA game. Prem’s letter this year is one of the best that you will find from a CEO - in any industry. It really demonstrates just how well the team at Fairfax (insurance and investments) is executing today (truth be told - for the last 5 years). Anyways, I just wanted to post a short/incomplete summary while I have time. I am helping a close family member prep their house for sale… I am going to be busy for about a week - my posting will be minimal (like it has been for a couple of days).

-

Volatility is a GREAT THING for Fairfax. We all should be praying for crazy volatility to happen. That is when Fairfax (and all value investors) get their best opportunities. The difference today is Fairfax is all cashed up. Investors in Fairfax should be praying for a shitstorm. Especially given how Fairfax is situated today. Fairfax’s best moves over the past 5 years (the needle movers) all were made when the shit was hitting the fan. Bring it on I say If we get extreme volatility my return expectations for Fairfax will go up. And the stock will likely sell off. A great combo. Yes, it matters what they do. But their recent track record is very good.

-

This was an very good move for IIFL when they split into 4 companies: - Finance - Wealth - Securities - 5paisa Each company has prospered. The separation allowed each of the companies to get much more focussed/entrepreneurial. The value creation in the subsequent years for Fairfax and Fairfax India was material. Quess is a massive company. It houses many large, unrelated businesses. I love this move and my guess is it will be a very good move from both a business and financial (return) perspective for Quess shareholders. Quess’ stock is already up big time over the past year as investors anticipate/get positioned for what is to come (over the next 2 or 3 years). These are two great examples of the benefits of partnering with Fairfax: - patient partner - loyal partner (there in tough times) Great strategic advisor: - step 1 - grow through acquisition - step 2 - incubate - step 3 - spin off The goal is to build value over the long term for shareholders. Not simply grow for growths sake - and become a lumbering, poorly performing conglomerate. We are getting closer to the ‘get paid’ stage - that should happen in the coming years (like we saw with IIFL as Fairfax and Fairfax India opportunistically exited big chunks of their IIFL positions).

-

@dartmonkey , here is my guess. ‘His (Brett’s/Morningstar’s) basic idea is’ ignore Fairfax’s insurance business today. Ignore Fairfax’s investment management business today. Ignore the decisions the senior management team have made over the past 5 years. So, ignore the fundamentals and earnings prospects for Fairfax as they exist today. Instead, focus on Fairfax as it existed 10 years ago - its insurance business then. It’s investment management business then. And the decisions the senior management team were making then (equity hedges, Blackberry etc). Based solely on what we saw from Fairfax 10 years ago (fundamentals and prospects), Brett/Morningstar thinks the fair value for the stock today is C$1,290. I think I understand HOW he got his fair value estimate. But is that really the best way to value ANY COMPANY? I’ll let you answer that question on your own (that is called a 1 foot hurdle by Mr. Buffett).

-

Fairfax today is in unchartered territory when it comes to the earnings it is generating: 1.) Size - massive. 2.) Diversified - they have 5 different income streams. - earnings aren’t tied to the insurance cycle or to the economic cycle. 3.) High quality income streams - that have exploded in size and now dominate investment gains (which continue to be very good). 4.) Sustainable - that ‘high quality’ thing. This will give the company a great suit of options to pick from when the next shitstorm happens. It really is an interesting set up. ————— Buffett talks about how not all earnings are created equal. You want to find situations where the majority of the earnings are not needed by the business - the situation with Fairfax today (as the hard market slows). Along with other things, this capital can be used to grow/create new income streams. Capital was used from 2020-2023/2024 to enable the insurance subs to capitalize on the hard market.

-

@Junior R Good point. Fairfax’s stock really outperformed big time in the 2022 bear market in stocks (+40% compared to S&P500). Today Fairfax is flush with cash and they think their stock is cheap at current levels. And they are walking the talk (they reduced effective shares outstanding by 5.7% in 2024). So if the stock sells off meaningfully (i.e. 10% or more) I would expect Fairfax to get aggressive with buybacks again. Great set up for shareholders in the current environment (volatility appears to be picking up). Long term shareholders really should be hoping for a big decline in Fairfax’s share price. At least that is what Buffett has said repeatedly… It would be great if Fairfax was able to take out a significant number of shares in 2025 at a slight premium to book value.

-

Comparing Berkshire Hathaway to Fairfax Yes, Fairfax and Berkshire Hathaway are similar in many important ways. However, both companies also have important differences. We review both their similarities and differences in this post. How Berkshire Hathaway and Fairfax are similar: 1.) Ownership/Control: Founder is the controlling shareholder - allows business to be run with a long term focus. Insurance - Critical to being able to optimize the management of the insurance cycle. Investments - Expands opportunity set to higher return opportunities, like equities. Founders have modest pay packages. The vast majority of their net worth is held in the company. The result is strong alignment of their interests with those of shareholders. 2.) Business structure: Small head office – handles capital allocation and succession planning. Decentralized operating structure: Insurance businesses are run by their presidents/CEO’s. Investments / equity holdings are run by their CEO’s. 3.) Growth engine: P/C insurance business - generating low cost and growing amounts of float. 4.) Investing framework Value investors at their core – Ben Graham was the foundational teacher. 5.) strong culture - carefully crafted and shaped over decades; championed/role modelled by the founder/CEO. 6.) Communication with shareholders: Informs and teaches shareholders about the business. Long letters in each annual report. Presentation / Q&A at the AGM. 7.) Shareholder focus: Focus is on building per share value for shareholders over the long term. 8.) Exceptional long-term track record: Built an enormous amount of wealth for shareholders over decades: Berkshire Hathaway = 19.9% per year for 59 years Fairfax = 19% per year for 39 years (US$ including dividends) How Berkshire Hathaway and Fairfax are different: 1.) Size of company Berkshire Hathaway is a giant-sized company. Fairfax is a much smaller company. Today, this makes it much easier for Fairfax: To grow its insurance business (and float). When making investments. Fairfax has a much larger opportunity set (in both public and private markets). And a good decision will more easily move the performance needle at Fairfax. 2.) Importance of P/C insurance Berkshire Hathaway has morphed into a huge conglomerate over the past 2 decades; today, P/C insurance is one of a couple of large business units. Fairfax is still primarily a P/C insurance company; as a result its business is much more leveraged to the benefits of float. 3.) Capital allocation Berkshire Hathaway and Fairfax are very different animals when it comes to how they do capital allocation (what tools they use and how they use them). Berkshire Hathaway is much more constrained in its approach. Fairfax is open to using all tools in the capital allocation toolbox (like Henry Singleton was when he ran Teledyne). Fairfax can also be very creative with how it uses the tools. Below we highlight some of the differences in their approach. Sources of capital 4.) Use of equity Berkshire Hathaway is loathe to issue new BRK shares and, until recent years, was not a fan of buying back its stock. Fairfax has always been very active with its equity, issuing FFH shares when its stock was trading at a premium (using the proceeds to buy P/C insurers who were trading at a discount) and then - years later - aggressively buying back FFH shares when its stock was trading at a discount. 5.) Use of debt Berkshire Hathaway uses a very modest amount of debt (usually at the subsidiary level). Fairfax is much more comfortable using debt as an another form of leverage (in addition to float) to boost earnings and returns for shareholders. 6.) Use of minority partners Berkshire Hathaway does not use minority partners as a source of cash. Minority partners have been a significant source of short term capital for Fairfax over the years. Capital is sourced when opportunities arise (two recent examples: Allied World acquisition in 2017 and buyback of 2 million Fairfax shares in 2021). Minority partners are bought out when Fairfax is flush with cash (like we have been seeing in recent years). 7.) Holding period When it comes to investments, Berkshire Hathaway’s style can be described as ‘buy and hold forever.’ Fairfax is much more opportunistic when it comes to holding period. Selling is an important source of cash and it has delivered significant value to Fairfax and its shareholders over the years. Insurance: Taking advantage of the mania in cats and dogs, In 2022, Fairfax sold its pet insurance business and realized a $1 billion gain after tax. Most people did not even know that Fairfax owned this business (it was very small). Investments: In 2022, Fairfax sold Resolute Forest Products at the peak of the lumber cycle at a premium price. In 2024, Stelco was sold at a premium price to Cleveland-Cliffs. Investing 8.) Kind of value investor: After Ben Graham, the big influences on Buffett and Watsa’s/Fairfax’s investing styles have been quite different. Warren Buffett was influenced by Charlie Munger and Phil Fisher - This pushed Buffett to ‘quality at a fair price.’ Prem Watsa/Fairfax was influenced by John Templeton and Peter Cundill (others?) - Watsa/Fairfax has remained more of a traditional value investor (buy low and sell high). It does appear in recent years as though Fairfax has been moving towards ‘quality at a fair price’ (putting more of a premium on management, balance sheet strength and earnings profile). 9.) Geography Berkshire Hathaway has been focussed primarily on the US with its P/C insurance business and its investment businesses. Fairfax has been aggressively growing out its international P/C insurance footprint. And it has significant investments outside of the US (Canada, India, Greece). When Digit (P/C insurance start-up in India) was looking for a partner in 2016-17 they went to Berkshire Hathaway first – who said no. They then went to Fairfax , who said yes. And Berkshire’s loss has become Fairfax’s gain. Fairfax’s $154 million investment in Digit is now worth more than $2 billion. More importantly, today Fairfax owns a control position in a large, fast growing P/C insurance companies in India - who is expected to have the fastest growing economy in the world over the next decade. 10.) Resource industries/commodities Fairfax appears more comfortable investing in these sectors than Berkshire Hathaway - Fairfax will invest where they find value. More than 10% of Fairfax’s equity portfolio today is invested in a diverse group of resource/commodity plays – oil and gas, gold, copper, royalties. Other items 11.) Dividend Berkshire has never paid a dividend. Fairfax currently pays a small dividend of US$15/share. 12.) Stage of Life Cycle: At Berkshire Hathaway, today Buffett appears focused primarily on preservation of capital – listening to him talk about his responsibilities to long term shareholders, he sometimes sounds like he is managing a trust. Fairfax still appears to be primarily focused on driving per share returns for shareholders over the long term. Summary From a structural perspective, Berkshire Hathaway and Fairfax have many similarities. However, when it comes to execution, they both have many meaningful differences. Both companies have outstanding long term track records - they are both very good at what they do. Both companies should be celebrated for their differences (not derided). Importantly for today, Fairfax is a much younger and smaller company than Berkshire Hathaway. Fairfax looks like an athlete who has just entered their prime. Over the past 5 years, Fairfax’s performance (appreciation of share price) has been best-in-class among P/C insurance companies - and it hasn’t been close. It appears Berkshire Hathaway has handed off the outperformance baton to Fairfax who is now running with it - most investors just haven’t recognized it yet. ————- Pet peeve Does this mean we should start calling Prem Watsa the Warren Buffett of the north (again)? No. This was a stupid thing to say 20 or 30 years ago. It is even more stupid today. IMHO, it is a lazy and inaccurate comparison to try to make (although it will probably get lots of clicks). Buffett is the GOAT. Trying to compare anyone to the GOAT is never going to go well. To do so does a great disservice to Watsa. Both men are great in their own right - and each should be celebrated for what each has delivered/accomplished over many decades for small/retail investors (like me and many others on this wonderful board). ————— What about Markel? Markel is a fine company. It appears Markel has decided they are going to try and clone Warren Buffett. As I have said above, I don’t think that is possible. In recent years, Markel appears to be having its challenges executing that strategy/model - it’s business has been experiencing some issues and as a result its share price has badly lagged P/C insurance peers over the past 5 years. Recently, they have called in ‘external consultants and advisors’ to help them figure things out - hardly the sign of a well run company. Comparing Markel to Fairfax today, I think Fairfax is better positioned in both its core P/C insurance and its investment management businesses. But most importantly, over the past 5 years, Fairfax’s senior management team has been executing much better than the senior team at Markel (capital allocation, succession planning, P/C insurance, investments). As a result, my guess is Fairfax’s business results and share price will continue to outperform those of Markel in the coming years.

-

Warren Buffett and Berkshire Hathaway Warren Buffett just released his annual letter to shareholders. So it is timely to do a post on the artist himself and his masterpiece called Berkshire Hathaway. Warren Buffett is the GOAT. Over the past 59 years (1965-2024), the per-share market value of Berkshire Hathaway’s stock has increased at a CAGR of 19.9%. Over the same time frame, the S&P500 with dividends has increased at a CAGR of 10.4%. The CAGR of 19.9% is impressive. But what is even more impressive is how long it has been sustained - 59 years. Yes, that performance makes Buffett the GOAT. But there is more to the Buffett story than just the return he has delivered. He is very shareholder friendly. This gets glossed over at times (because he does so many things exceptionally well). But it is one of the things that separates Buffett from many other great capital allocators. He is also an educator with top-notch communication skills. Buffett’s annual letters have become must reads for investors. And tens of thousands make the pilgrimage to Omaha each year to hear Warren Buffett speak at Berkshire Hathaway’s annual meeting. He wanted small/retail investors to succeed. Many small/retail investors have made vast fortunes from their investment in Berkshire Hathaway over the past 6 decades. They did not have to pay nose-bleed high private equity fees (like a 2% annual management fee + 20% performance fee) to invest alongside Buffett. As a result, Buffett is both adored and worshipped by Berkshire Hathaway shareholders. And rightly so. This is very rare for someone who made their fortune running a business and investing in financial markets. Warren Buffett is also a unicorn - he is one of a kind. Buffett is one of a kind - his intellectual/psychological makeup. But that was not enough. He was also in the right place at right time. Born in the US. Born a male. Taught early in life (before his habits were formed) directly by the master himself, Ben Graham. Discovered his lifelong business partner, Charlie Munger, in 1959 - who taught him other important lessons, like the importance of buying quality. Buffett is a unicorn. What Buffett has accomplished for small/retail investors will never be repeated: What he did - CAGR of 19.9% for 59 years. How he did it - via Berkshire Hathaway - a publicly traded company (which allowed small/retail investors to participate and fully benefit from his amazing skills). Warren Buffett the god? Yes, Warren Buffett has assumed god-like status. His writings are considered sacred texts. His methods are now taken as gospel. This can be problematic (we will come back to this later). Where are we at today? Warren Buffett is 94 years old. And Berkshire Hathaway has morphed over the past 2 decades into a massive conglomerate. Its core growth engine, P/C insurance, is now just one of many big businesses that the company has. Berkshire Hathaway’s massive size and Buffett’s advanced age has important ramifications for Berkshire Hathaway shareholders - future returns will be lower than past returns. Buffett has been warning about this for decades. If we look at Berkshire Hathaway’s returns from the past 59 years and separate them into decades we can see the slowdown. Three periods become apparent: First 29 years (1965 to 1994) CAGR = 29.2% Next 10 years (1994 to 2004) CAGR = 15.7% Last 20 years (2004 to 2024) CAGR = 10.8% Bottom line, as an investment, Berkshire Hathaway’s best years are behind it. Moving forward, Berkshire Hathaway’s stock will likely generate returns that are similar to those of the S&P500 with dividends. This is not a bad outcome - most professional money managers underperform the S&P500 (when their returns are measured over a 10 year time horizon). This naturally leads to the following question: Who is the next Warren Buffett? Ok, you probably felt your pulse quicken when you read that question. This is, of course, the proverbial million dollar question. We are all on the lookout for the next ‘Warren Buffett.’ For investors, it is a bit like the endless search for the mythical holy grail. That person just HAS to be out there. But there is a problem. As we already pointed out, Buffett is a unicorn. What does this mean? It means it’s not possible to find another Warren Buffett. There I said it. Sorry if that felt a little like showering in cold water. But it is what it is. And an investor needs to live in the real world. OK. So does that mean investors should give up with their search? No. What should we do when we hit a wall? One solution is to reframe the question. Maybe investors are looking for the wrong thing. Instead of looking for the next Warren Buffett (impossible), why don’t we look for something that is possible… What is that? Which company could be the next Berkshire Hathaway? To answer this question, let’s review what Berkshire Hathaway’s secret sauce is/was: Run by founder - skilled at attracting and retaining top talent. Family/founder controlled - allowed for long term focus in running the business. Core engine is P/C insurance - benefited from growing, low cost float that could be invested. Decentralized operations - attracts entrepreneurs. Centralized capital allocation - among other things, invests in equities. Strong company culture - built over decades and championed by founder. Company is run for benefit of shareholders - focus is on growing per share value for shareholders over the long run. Good communicator - primarily via letter in annual report; Q&A at annual meeting. What about return expectations? We are going to keep this reasonable. We are looking for a company that might be able to deliver a return to shareholders of 15% per year over the next 10 years. Does a company like this exist? Before we can answer that question we need to discuss with one more issue. The curse of Warren Buffett. When investors look for the next Berkshire Hathaway, they usually do so through the lens of Warren Buffett. So, when they evaluate other companies - and the decisions made by their management teams - they usually ask the following question: “Is that what Warren Buffett would have done?” Do you see the problem with this approach? Yes, they are really looking for a clone of Warren Buffett. And as we discussed earlier, that does not exist. And I get it - investors can’t help themselves. They love and worship Warren Buffett so much they can’t let go - they don’t want to let go. In this regard, Buffett has become a curse for many investors. It is stopping them from being rational and dispassionate when they look at other companies. Is it possible to find another Warren Buffett? No. Is it possible to find another Berkshire Hathaway? Yes. Perhaps the key is the P/C insurance model. The P/C insurance model Buffett has said repeatedly that the core engine that propelled the growth of Berkshire Hathaway over the decades was its P/C insurance business. The really interesting thing is other investors/companies have done something similar. Other investors/companies have built great fortunes over many decades exploiting the P/C insurance model: Shelby Davis - CAGR of 23% over 47 years Henry Singleton/Teledyne - CAGR of 20.4% over 27 years. Larry Tisch/Loews Warren Buffett/Berkshire Hathaway - CAGR of 19.9% over 59 years. But here is the really interesting thing: they all did it in completely different ways. So investors don’t need to find the next Warren Buffett. Instead, they need to find the next investor/company who is poised to exploit the P/C insurance model to drive above average returns for shareholders in the coming years. This approach offers investors their best chance of finding the next ‘Berkshire Hathaway type of investment.’ ———— Which company looks poised to best exploit the P/C insurance model in the coming years? I think it might be Fairfax Financial. Truth be told, Fairfax has been successfully exploiting the P/C insurance model for decades. Over the past 39 years its share price (plus dividends) has delivered a CAGR of 19% in US$ terms (it was 18.3% at the end of 2023 - from Fairfax’s 2024 AGM presentation). That is exceptional long term performance. But more relevant to our post today, Fairfax is still a small company. It has been aggressively expanding its P/C insurance business over the past decade (growing that core engine). And it is still run by its founder. Over the past 5 years Fairfax has dramatically outperformed its P/C insurance peers. Fairfax has delivered a total return to shareholders of 25.2% for each of the past 5 years. And even after that performance, it is trading today at the lowest valuation (compared to peers). Most importantly, Fairfax’s P/C insurance business has never been better positioned. Its investment management business has never been better positioned. Over the past 5 years, the execution from its senior management team has been best-in-class. As a result, the company has never been better positioned in its history than it is today. Today, Fairfax is providing investors with the next iteration of how to successfully exploit the P/C insurance model - and drive enormous per share value for shareholders over the long term. Lots of investors just don’t see it… yet. Likely because they are looking for the wrong thing. Part 2 is contained in the next post in this thread.

-

@dartmonkey , great point. Thanks for pointing out my mistake. Much appreciated (as that is how I learn).

-

Interesting take. Makes sense. Past is prologue. Time to brush up on past Imperialist times to get a glimpse of what might be coming...

-

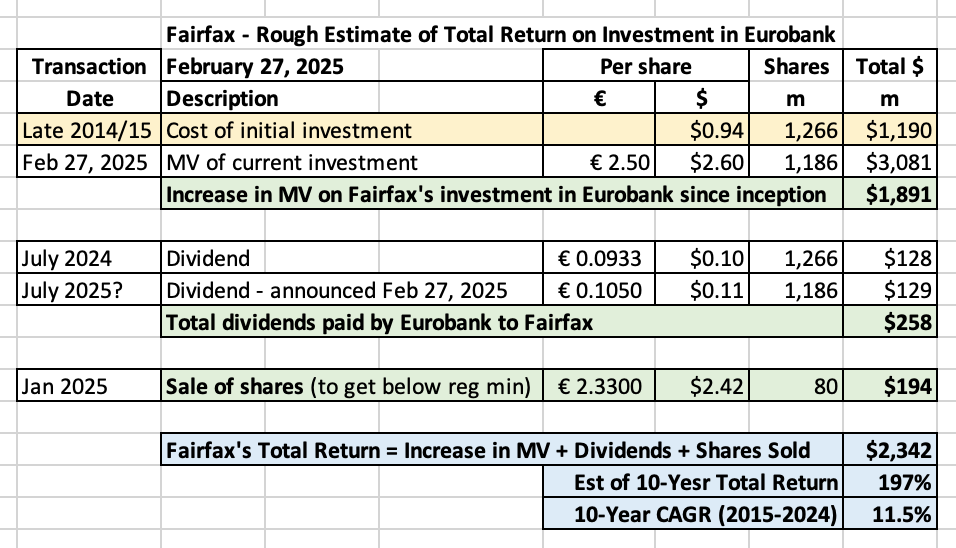

Eurobank is turning into a very good investment for Fairfax. It has increased in value by about $2.3b over the past 10 years (with all of the return coming in the last 4 years). More importantly, Eurobank is poised to grow TBV at +15% in the coming years. It has a stellar management team. Yes, my total return estimate is calculated at a very high level (like counting the 2025 dividend payment which hasn't happened yet). Given all the moving parts, I am simply trying to find a way to evaluate how the investment has performed. Eurobank is a great example of the pivot of Fairfax's equity holdings from 'old Fairfax' to 'new Fairfax.' Eurobank always had a good management team. They needed (and got) external help: Greece elected a pro business government - to 2 terms. Global central banks ended zero interest rate experiment. The result has been magic for Fairfax shareholders over the past 4 years. Eurobank is Fairfax's largest equity holding, with a MV of $3 billion. If it performs strongly that bodes well for the return will generate on its total equity portfolio in the coming years.

-

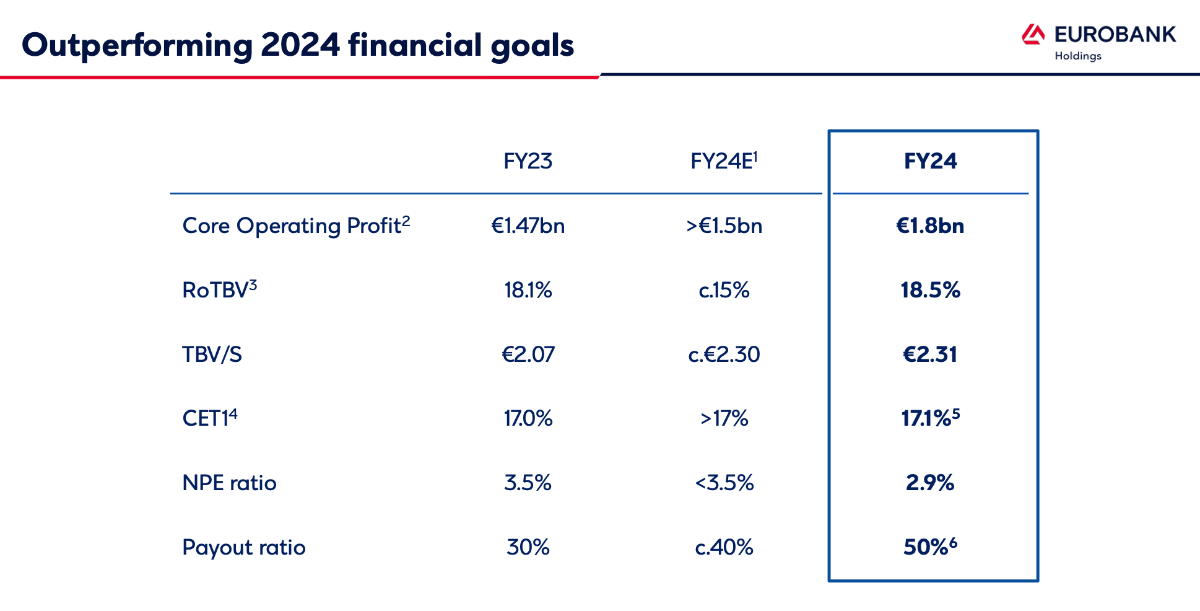

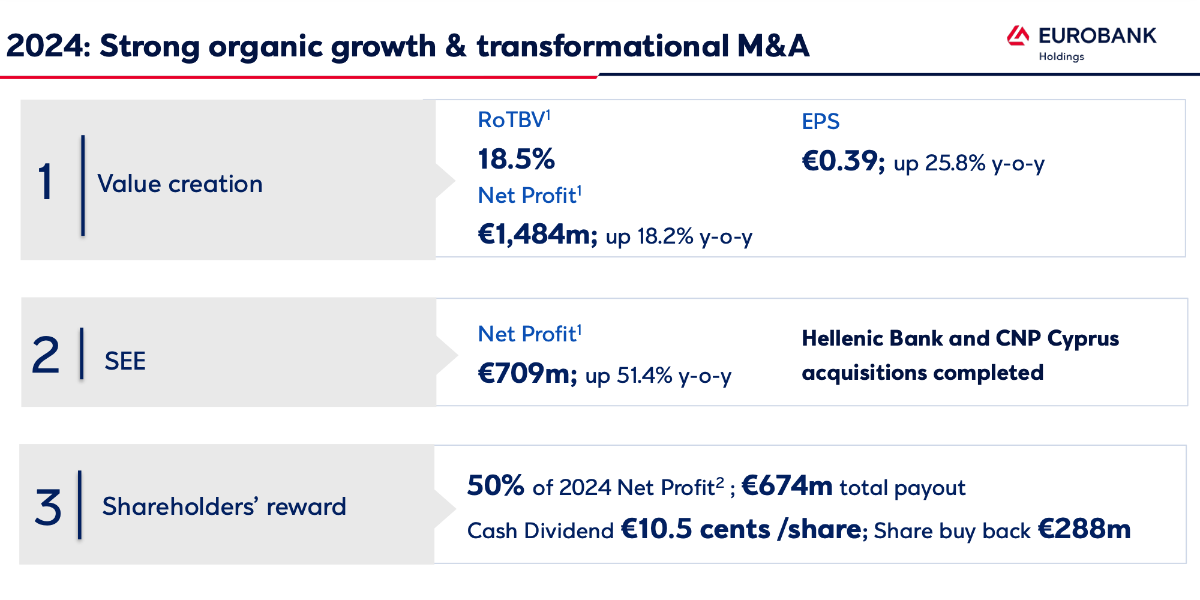

@nwoodman , I agree... what an exceptional year. Its interesting... over a 12 month period (July 2024 to July 2025), Eurobank will have 'provided' Fairfax with about $450 million in proceeds ($250 million in dividends and $200 million from sale of shares - rough math). Fairfax's equity investments are increasingly becoming significant sources of cash for Fairfax. That is an important development. The Eurobank management team is best-in-class. One of the things I really like is they underpromise and over-deliver. Below is the slide for 2024. The middle column is what they promised at the start of the year. The column to the right is what they delivered. https://www.eurobankholdings.gr/-/media/holding/omilos/enimerosi-ependuton/enimerosi-metoxon-eurobank/oikonomika-apotelesmata-part-01/2025/fy-2024/4q2024-results-presentation.pdf

-

@73 Reds , I appreciated reading your post... as a Canadian, it is helping me understand the American perspective. I view what Trump is doing as kind of like a big science experiment - with the ultimate outcome unknowable. I try to be as rational/logical as I can when looking at businesses/the economy/politics. The problem I have today when I look at much of what Trump is doing is I can't actually make any sense of it - in a logical/rational way. It looks to me like the US has devolved into 'the law of the jungle' method when it comes to so many important issues. Might is right. Nothing else matters. With that mind set, smaller countries like Canada are bugs to be crushed. It is all surreal - but I do understand it. Now American's on the board might think I am exaggerating / overreacting. We will see how things play out over the next 4 years. My brain (logic/rational) can't actually process what Trump is doing... so my emotions take over, which is never a good thing. So my approach is to just turn it off. It's like a bunch of kids in a playground. And the big kid is thumping the weakest kid. The other kids are watching mesmerized. Some kids are cheering on the big kid. Others kids are watching and their stomach is turning over. Like I said, what is going on today just seems so surreal (to me).

-

Gang, I love all the detailed analysis on Ki. My takeaway is Ki is another (significantly?) undervalued asset sitting on Fairfax’s balance sheet today. Importantly, it is poised to compound at a high rate in the coming years. We now have a number of different examples of significant value that is being created at Fairfax that is not showing up in accounting results (EPS and BVPS): Excess of fair value over carrying value for associate and non-insurance consolidated companies ($1.48 billion = $68/share pre-tax). BIAL - my guess is its current intrinsic value is much higher than its carrying value. Ki - the latest example, as discussed in the most recent posts in this thread. My guess is there are more examples. Fairfax’s carrying value for Poseidon has not changed much in recent years - at the same time the size of the company has increased dramatically. Grivalia Hospitality is another interesting investment. AGT Food Ingredients is a phantom holding. Bottom line, Fairfax had largely cleaned up its equity portfolio. And that higher quality portfolio has been compounding in value for years now. Some holdings, like Eurobank, we can see. There are lots of holdings at Fairfax where we dan’t see the value that has been building - it is like a spring that is quietly being coiled tighter and tighter… The value that has been created (and will be created in the coming years) will show up over time in accounting results (EPS and BVPS) - via ‘surprise’ investment gains.

-

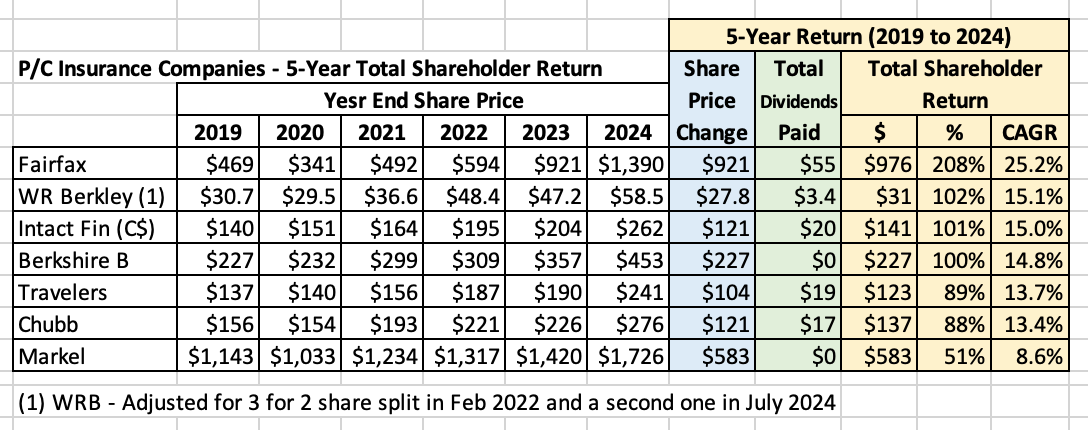

How Does Fairfax’s Valuation Compare to Other P/C Insurance Co’s There are lots of methods an investor can use to value a company and its share price. In this post, we are going to use a method called ‘relative valuation.’ We are going to compare Fairfax to other P/C insurance peers to see what we can learn. How have they performed? How are they being valued today? When compared to some of the best P/C insurance companies in North America. Which companies are we going to include? Below is the list of the seven P/C insurers we will compare (listed in alphabetical order): Berkshire Hathaway: historically, the gold standard; now more of a conglomerate than P/C insurer. We include it for fun. Chubb: Large, traditional insurer; international in scope. Fairfax Financial: An up-and-comer; about 30% of investments are in equities; international in scope. Intact Financial: Largest P/C insurer in Canada; expanding globally. Markel: ‘Baby Berk’; US focus Travelers: Large, traditional insurer; US focus. Part of DJIA. WR Berkley: Traditional insurer; US focus To state the obvious, all P/C insurance companies have unique business models. As a result, we will keep our analysis very high level. Buffett suggests 5 years is a good time frame to use to measure/evaluate the performance of a company - so that is what we will use. The post has been updated to include 2024 actuals for Berkshire Hathaway. ————— “In other words, the percentage change in book value in any given year is likely to be reasonably close to that year’s change in intrinsic value.” Warren Buffett The most important metric used by investors and analysts to assess the performance of a P/C insurance company is change in book value. Yes, it has its flaws. However, it is a good place to start. 5-Year Change in Book Value We are going to look at the change in book value from December 31, 2019 to December 31, 2024. We have sorted the results in the table below from the best to the worst performers. So, which company has increased BVPS the most? Fairfax Financial. Fairfax has grown book value by 118% over the past 5 years, a CAGR of 16.8%. Wow! The second surprise is the size of Fairfax’s outperformance - it is much higher than #2 Berkshire Hathaway and way, way higher (+10% per year) than #6 Chubb and #7 Travelers. I think it is safe to say that Fairfax’s performance has trounced that of its peer group. That is pretty impressive. There are a lot of many quality P/C insurance companies on this list. Were you expecting that? I bet you weren’t expecting that. Looking at accounting results is only the start An added wrinkle The investment portfolio of most P/C insurance companies contain mostly bonds. These are easy to value. As result the value of the investment portfolio captured in book value for most P/C insurance companies is pretty accurate. Fairfax owns lots of equities (about 30% of the total investment portfolio). And over the past 5 years, the ‘excess of fair value over carrying value’ for associate and consolidated companies has increased and sits at $1.48 billion pre-tax ($68/share) at December 31, 2024. This is economic business value that has been created by Fairfax over the past 5 years that has not been captured in its accounting (book) value. When we include this additional value creation, Fairfax’s outperformance versus peers is even better than what we see looking only at the change in BVPS. In recent years Buffett has soured on using book value to measure the performance of Berkshire Hathaway (it is now a conglomerate). His new preferred measure for Berkshire Hathaway? The change in the stock price over time. So let’s now compare the performance of the same group of insurance companies using this measure. Some of our companies pay a dividend. So to be fair, we are going to look at total shareholder return (total increase in share price + dividend paid). 5-Year Total Shareholder Return We are going to look at the total shareholder return for the 5-year period from December 31, 2019 to December 31, 2024. Once again, we have sorted the results in the table below from the best to the worst performers. So, which company has seen the biggest increase in their share price? Fairfax Financial. It has delivered a total return of 208% = CAGR of 25.2% That is an outstanding level of performance - especially over a 5 year time frame. A second surprise is the size of Fairfax’s outperformance compared to peers… it has been much better - more than 10% more per year than the #2 WR Berkley and more than 15% higher than #7 Markel. Wow! Markel has been the clear laggard of the group, with a CAGR of 8.6%. The remaining 5 companies all have a very respectable CAGR in the mid to low teens, which is good. The P/C insurance sector has been a pretty good place to invest over the past 5 years. Let’s move from measures of past performance. Let’s now look at some measures of valuation and how our 7 companies compare. Let’s start by comparing the stock price with the all important measure of book value. Price to Book Value (P/BV) We are going to use the share price for each company today (Feb 19, 2025). And their book value at December 31, 2024. This will give us a trailing P/BV multiple. We have sorted the results in the table below from the company with the highest multiple (most expensive) to the lowest (cheapest). Does anything in the chart below jump out? Fairfax’s valuation is the cheapest. And compared to the most expensive companies (Intact Financial and WR Berkley), Fairfax’s valuation is much, much cheaper. Fairfax’s valuation is even cheaper than it looks - when we include ‘excess of FV over CV for associate and consolidated holdings’ (we discussed that earlier in this post so we won’t repeat it here). Let’s look at another valuation measure and see what it tells us. Yes, P/E is frowned upon as an measure to use when analyzing P/C insurance companies. But it can be useful as a tool to compare companies in the same industry. And that is what we are doing here. Price to Earnings Ratio (PE) We are going to use the share price for each company today (Feb 19, 2025). And their reported earnings per share for 2024. This will give us a trailing P/E ratio. We have sorted the results in the table below from the company with the highest ratio (most expensive) to the lowest (cheapest). Does anything in the chart below jump out? Fairfax’s valuation is the cheapest. Again. And compared to the most expensive companies (Intact Financial and WR Berkley), Fairfax’s valuation is much, much cheaper. Conclusion 5-Year Performance When looking at a large group of high quality P/C insurance companies, Fairfax has delivered the best performance over the past 5 years - both in terms of increase in BVPS and total shareholder return (share price + dividends). The second key take-away is Fairfax’s outperformance of peers - across both measures - has been significant. It has been much, much better. What this demonstrates is the outstanding job that Fairfax has done of building per share value for shareholders over the past 5 years. It has a high quality P/C insurance business. Its investment management business is once again performing at a very high level. And the execution from its senior management team has been best-in-class. Current Valuation When looking at the same large group of high quality P/C insurance companies, Fairfax’s share price today is trading at the cheapest valuation across both P/BV multiple and PE ratio measures. The second key take-away is how much more cheaper Fairfax than many peers - the gap is very large. What does this mean? An investor today is able to buy the top performing P/C insurance company - with among the best future prospects - at the cheapest valuation. Does that make any sense? No, of course not. "The way of the successful investor is normally to do nothing -- not until you see money lying there, somewhere over in the corner, and all that is left for you to do is go over and pick it up." Jim Rogers ————— What is really going on with Fairfax today? Investors have apparently forgotten the incredible power of the P/C insurance (float) model. Buffett leveraged the P/C insurance (float) model to deliver staggeringly high returns for Berkshire Hathaway shareholders. But even more impressive was how long he was able to sustain that performance - it went on for decades. Yes, Fairfax has had 5 very good years. But they are still a small company. It looks to me like they are just getting started. (Hint: There are many ways to use the P/C insurance (float) model to drive incredible returns for shareholders over the long term. Shelby Davis. Henry Singleton/Teledyne. Larry Tisch/Loews. And yes, Warren Buffett/Berkshire Hathaway. The really important point is they all did it in very different ways. Today Fairfax is providing us with the next iteration of how to capitalize on this very powerful model to drive enormous value for shareholders over the long term. Lots of investors just don’t see it yet. And that succinctly explains how the top performer can trade at the cheapest valuation.) Still not sure what to do? If so, you might want to read my last long-form post (it is the sister post to the one above): Is Fairfax ‘the big fish that got away?’ Musings on mistakes that investors keep making. https://thecobf.com/forum/topic/21117-fairfax-2025/page/16/#findComment-601681

-

@glider3834 I appreciate the heads up. Board members, please let me know if you see any other items that can be updated. Your input helps me greatly in keeping the summary accurate/up to date.

-

@Munger_Disciple, as of today, I am comfortable having Fairfax as a core position of about 35% of my total portfolio. I will flex this position up (and then back down) to take advantage of short term price volatility (like I do with all the stocks I own). I think this is what I have been constantly saying for about a year now. Disclaimer: I may change my mind tomorrow. So you are warned! Position size is a complicated topic. It is very situational. And my views on the subject are not fixed - they are continually evolving. Factors for me: - Age / life stage / health situation - Size of total portfolio - Percent of total net worth in financial assets - Estate planning - My spouse (quite risk averse) - Opportunity set - Account types (most of my financial assets are in registered accounts - so it is very easy for me to flex my position) Note, none of the above includes a discussion of the company and its intrinsic value - which is also important

-

We have just had 2 very strong years - equity markets are up +50%. Valuations are probably getting stretched. I like that Fairfax is being very disciplined. But this will change - we will get another bear market. And next time, Fairfax will be flush with cash….

-

Since 2018, Fairfax’s track record with new equity purchases has been very good. The perception is they invest in value traps. That was true pre-2018. That has not been the case since then. Further, they have dealt with almost of all of the former value traps that they owned from pre-2018 (what is remaining is very small it terms of the total equity portfolio). A great example is Stelco. Bought in late 2018. People hated it at the time (including me). At the time it probably checked all the boxes of being a classic value trap. And then it then delivered a CAGR of 25% per year for the next 6 years. Simply outstanding.

-

The equity hedges were taken of at the end of 2016. That was more than 8 years ago. The Blackberry purchase was years before that. My view is Fairfax has learned important lessons from mistakes made in the past. I think it actually makes them a stronger company today. The analogue is when Fairfax messed up on the insurance side of its business in the early 2000's. The lesson's learned then have resulted in the strong insurance business model they have today. They learned from their mistake and it has made them a stronger company. Yes, the view is not what the current narrative is today regarding Fairfax. But that is where my reading of the facts/analysis takes me. I could be wrong. We will see in the coming years.