Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

I am trying to quantify the value to long term shareholders of share buybacks. I am trying to come up with an actual number. I find the concept of the value of share buybacks is pretty easy to understand. Attaching a specific value is much more difficult. Is one way to simply treat the buyback like it was an investment in another company? We know what the average price paid was for the buybacks. And we know at what price the stock is trading at today. Does that give us one way to place an actual value on the buybacks? Yes it is very crude. But we are not looking to be precise. We are trying to understand magnitude: Is it a big number? If so, about how big? We also have a wrinkle... The Fairfax total return swap position. This is looking like it might be a stealth buyback (we will see if Fairfax continues to buy the shares from the counterparties and cancel them as it exits the position like it did in Q4, 2024). It is very easy to value the FFH-TRS position (before carrying costs). Let me know what you think. Is there another way to do this that is better? Bottom line, between buybacks and the FFH-TRS, what Fairfax has accomplished over the past 5 years has been epic in terms of the size of the benefit it has delivered to shareholders. Using my logic above, the 'value creation' for long term shareholders from these two 'investments' has been more than $8 billion. And growing every year (as the stock motors higher). Basically, Fairfax has been able to take out 25.8% of its effective shares outstanding at an average price of $589/share. At the same time (over the past 5 years) total earnings at Fairfax have exploded higher. Of course, this means per share numbers are up much more. Here is a little more detail on share buybacks.

-

@Hamburg Investor, thank you for clarifying your thoughts for me. Today I don't have a strong opinion on inflation and the impact on the results of the 'Berkalites.' Past, present or future. Where inflation goes over the next 5 years is one of the big macro questions out there today. It will be interesting to see what happens moving forward. Sorry, I don't have much to add. It's just a topic I haven't thought much about.

-

@Hamburg Investor, there is lots to chew on with you post. I haven’t thought deeply about how higher than expected inflation (like 3 to 5% per year for an extended period) might affect Fairfax. There are lots of puts and takes to consider. Here are a few: - Fixed income - tailwind to earnings - should sustain/lead to higher interest income. Average duration of fixed income portfolio is 3.3 years so earn through would be slower (than when average duration was at 1.2 years). - Insurance liabilities (long tail casualty lines) - headwind to earnings - likely see higher than modelled losses due to elevated costs/social inflation. - Equities - neutral? - equities are viewed as being an inflation hedge. But we could see the market multiple come down. But commodities might rip higher. In terms of Fairfax’s underperformance from 2010 to 2020, the big problem was the equity hedge/shorts. It cost them an average of $494 million per year for 11 years. Another problem was a bunch of their equity holdings were terrible (EXCO Resources, Fairfax Africa, APR Energy, Farmers Edge etc). And a number of other equity holdings were dead money for many years (Eurobank, Resolute Forest Products, AGT Food Ingredients etc). And yes, crazy low interest rates was also a problem. But my view is most of Fairfax’s issues when they were underperforming were self inflicted. I don't think this is a consensus view. There were two viscous bear markets in the early 1970’s. From mid-1975 to 2000 you had one of the greatest bull markets in history. The S&P500 went from 90 in 1975 to 1,500 in 1999, a 25-year CAGR of 11.9%. That was an incredible tailwind for equities. Its not surprising that Buffett’s best two 10-year stretches were 1975-1985 and 1985 to 1995. I do think experience matters when it comes to investment management. And Fiarfax has lots of people in their investment committee who were cutting their teeth in the late 1970’s/early 1980’s. This is a big advantage for them in today’s environment. Anyways, just some random thoughts.

-

@Xerxes , I do not have any special insight. My understanding is Hamas and Hezbollah work in close coordination with Iran. If that is not the case then that is new news to me. i will read up on the Abraham Accord - thanks for the insight.

-

Are Egypt and Jordan not instructive examples in terms of what Israel wants? Both countries normalized relations with Israel long ago. All three countries now peacefully coexist - and they have for decades. What happened? Egypt and Jordan recognized Israel's right to exist. They also decided they no longer wanted to kill Israeli's. Saudi Arabia was poised to normalize relations with Israel - and Iran and their proxies (Hamas, Hezbollah, Houthis) decided that couldn't happen and Hamas attacked Israel. We have two very different models/approaches to getting to peace in the Middle East. I think Egypt/Jordan's model is the better path to peace in the Middle East than Iran's. I think Israel wants the Egypt/Jordan path. But I am by no means an expert of what is going on there. So I will try and remain open minded to understanding the situation.

-

Hamas, Hezbollah and Iran have one - and only one - aim... to wipe Israel off the map. Israel has one primary aim - to survive. And to peacefully live with others in the region. Is the Middle East better off with Hamas, Hezbollah and now Iran defanged? I think so. Is the world better off with a non-nuclear Iran? Of course. I am not a fan of Trump. But I do think he is a much better fit than Biden/Democrats for what needs to be done in the Middle East today. It will always be a messy, messy situation. And there are lots of ways this situation could yet play out. Let's hope the developments of the past 24 months will result in a more peaceful Middle East in the coming decades - where more countries continue to normal relations with Israel. and the focus shifts to improving the lives of people (as opposed to trying to kill them).

-

Both BDT and ShawKwei are private equity firms. BDT specializes in investments in family-owned and founder-led businesses. Another important input is how the value of each of the funds is calculated at quarter and year end (that Fairfax uses in its reporting). And how representative is that mark to the actual intrinsic value of the holdings in the fund (which is what Fairfax really cares about). Clearly, Fairfax is very happy with how its investment in BDT is performing (given length of time and size). Part of valuing private equity holdings like BDT and ShawKwei is 'do you trust management.' By management I mean Fairfax. I do trust the management team at Fairfax. My level of trust has been increasing each of the past 4 years - based on how they have been executing and how they are communicating (IMHO, it has been very good).

-

@Marco Van Basten, I think the relationship with BDT is valuable because Fairfax thinks it is. Today BDT is one of Fairfax’s largest investments. The small amount of research I have done on Byron Trott suggests he is a quality individual. You state you think returns have not been very good. This sounds important to you - otherwise why ask your question. Why don’t you spend a few minutes and try and get an answer? And share your findings. That way we can all learn something. That is what I do. I generate a thesis. Do my research. And post what I find. And everyone on the board benefits. I am not wedded to any of my thoughts about Fairfax. As new facts emerge I will update my thinking on the company.

-

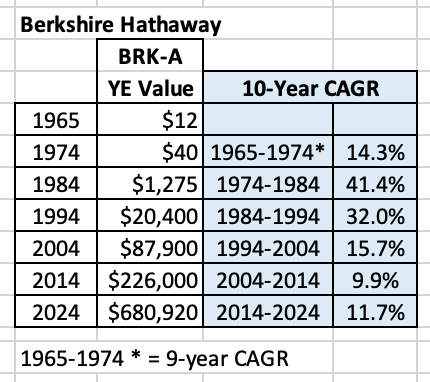

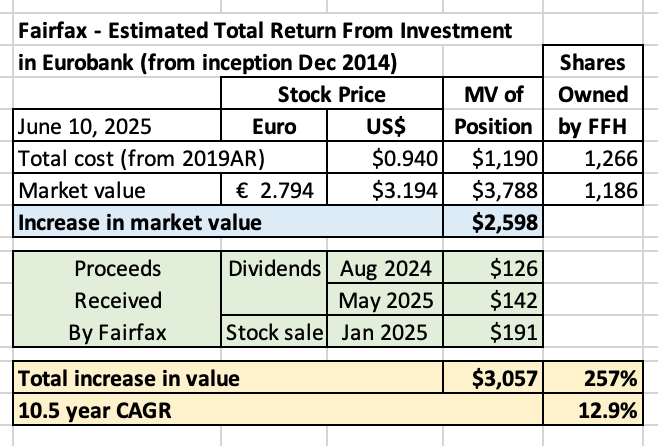

This is the fourth in a series of posts we are doing on leverage at Fairfax. Links to the first three posts are provided below: The first post introduced the topic and reviewed debt (holding company) and float. https://thecobf.com/forum/topic/21117-fairfax-2025/page/38/#findComment-622326 The second post reviewed 3 tactical ways that Fairfax uses leverage. https://thecobf.com/forum/topic/21117-fairfax-2025/page/39/#findComment-622725 The third post reviewed debt at non-insurance consolidated companies. https://thecobf.com/forum/topic/21117-fairfax-2025/page/39/#findComment-623255 With our post today we are going to look at leverage in a different way. Up to now we have looked only at types of financial leverage. But there are also types of non-financial leverage. Our focus is going to shift from looking at financial capital to looking at human capital. As a reminder, we have a very broad definition of leverage: Using other people and/or their money to boost returns and/or improve the quality of the company. ---------- Leverage - 7 - Non-financial leverage - human capital Human capital and the investment portfolio P/C insurance companies have two basic options when it comes to how they invest their investment portfolio: they can buy bonds or they can buy stocks, or some combination of the two. What do most P/C insurance companies do? Most insurance companies invest primarily in bonds (about 90% of their total investment portfolio). The remainder is invested in a variety of holdings, including stocks (about 10% of the total). Why do P/C insurance companies overwhelmingly prefer bonds? Bonds are considered a much safer investment than equities. Bonds are also less volatile. And bonds are easy (to purchase, and hold to maturity). Stocks, on the other hand, are considered to be a much more risky investment than bonds. Stocks are much more volatile. And stocks are difficult (stock picking). As a result, regulators and ratings agencies love bonds. So why doesn’t everyone (not just P/C insurance companies) own only bonds? Sounds like bonds is a no brainer. Why bother with stocks? Rate of return. The return on bonds is capped at the interest rate paid (let’s assume the bonds are owned to maturity, which most P/C insurance companies tend to do). Conversely, the return on stocks is unlimited. At least that is the theory. What can history teach us about returns? Comparing average historical returns: stocks and bonds What asset class tends to perform the best over the long term? Since 1928, stocks (CAGR = 9.94%) have outperformed bonds (CAGR = 6.62%) by a wide margin. Chart source: https://barbarafriedbergpersonalfinance.com/historical-stock-and-bond-returns/ Why do stocks outperform bonds by such a wide margin? Thanks for hanging in there with this post. We are getting to the good stuff… Stocks outperform bonds because they allow you to fully reap the rewards of human capital. That is the advantage of being the owner of a business. Being a lender does not allow you to benefit from human capital. And guess what the limits to human capital are? There are none. That is why owning stocks can be so good - and why you have unlimited upside. When you own stocks you are leveraging human capital. The genius of Warren Buffett Warren Buffett is using leverage at Berkshire Hathaway in two ways: Financial capital: Float from the P/C insurance business Human capital: Investing heavily in stocks. Yes, Buffett loves leverage. And he has been exploiting it brilliantly for 55 years. The genius of Charlie Munger Charlie Munger took Buffett’s model and made it even better. Stocks are good. But high quality stocks are even better. Why? Because the upside for high quality stocks is much, much higher than the upside for average stocks. Average stocks give you leverage to human capital. High quality stocks give you even more upside leverage to human capital. Buffett’s pivot to Munger’s way of thinking was monumental for Berkshire Hathaway shareholders. The pivot started in 1972 with the purchase of See’s Candy. From 1974 to 1984 Berkshire Hathaway posted a 10-year CAGR of 41.4%, its best performance. From 1984 to 1994 it posted a 10-year CAGR of 32%. That 20-year span was a magical time for Berkshire Hathaway shareholders. The company was still small. And in mid-1970 it was just beginning its shift to high quality equities. As Buffett telegraphed repeatedly, the law of large numbers eventually caught up to Berkshire Hathaway. And returns have come down to earth. There are three key learnings here: The P/C insurance model works - float. Investing in high quality equities works - leverage human capital. Size (eventually) negates the power of the first two (in terms of being able to generate outsized returns). This is not to suggest that Berkshire Hathaway is not a wonderful company today. It is. But it is now an aging elephant. It is no longer the predator that was back in 1975 - just entering its prime - and roaming a savannah that was teeming with game. What does all of this have to do with Fairfax? Like Berkshire Hathaway, Fairfax is using leverage in the same two ways: Financial capital: Float from the P/C insurance business. Human capital: Investing heavily in stocks. The pivot to quality at Fairfax And like Berkshire Hathaway, it looks like Fairfax has made the pivot to quality. It looks like the pivot happened around 2018 (I am guessing). Since then 2 very important things have been happening: Since 2018, new equity purchases have been very good. Holdings in their legacy equity portfolio (holdings purchased before 2018) have been fixed. It has been an 8 year journey for the company. And today, Fairfax now has a high quality equity portfolio. And we are seeing it in the results that Fairfax has been posting in recent years. The contributions from the equity portfolio have been very good. Importantly, an enormous amount of value has been created (economic results) that has not yet been reported in accounting results. This will be a tailwind to earnings in the coming years. But more important is the future. Fairfax is still a small company. And with its equity portfolio, it is just at the beginning of its ‘quality’ journey. ————— Of interest, Fairfax made a similar shift to quality in its P/C insurance portfolio in 2011 when it appointed Andy Barnard to president and chief operating officer of Fairfax Insurance Group. Under Andy, it has been a 14 year journey. And today Fairfax now has a top-tier P/C insurance business. ————— Reaping the rewards of human capital - founders/entrepreneurs/CEO’s Leveraging human capital is a powerful way for Fairfax to improve returns. But this time, instead of leveraging other people’s money, they tap into/exploit/leverage other people’s time, talent and experience. Fairfax’s shift to quality has been a little different than Berkshire Hathaway’s. That shouldn’t be a surprise… they are very different companies and external environment had changed a great deal from 1975. One of the tweaks that Fairfax made to their investing framework in 2018 was to put an emphasis on partnering with outstanding founders/entrepreneurs/CEO’s/capital allocators. Eight years later we can see the results of their efforts. The list of people that Fairfax is partnered with today with their equity holdings is impressive. Fokion Karavalis - Eurobank David Sokol/Bing Chen - Poseidon/Atlas/Seaspan Hari Marar - Bangalore International Airport (BIAL) Kamesh Goyal - Digit Insurance Pierre Lassonde/John Graham/Jason Simpson - Orla Mining (gold) Pierre Lassonde/Dan Myerson - Foran Mining (copper) Adam Waterous - Waterous Funds/Strathcona (oil) Harold Hickey - EXCO Reources (US natural gas) Byron Trott - BDT Capital Partners (private equity) Kyle Shaw - Shaw Kwei (private equity) Bill McMorrow - Kennedy Wilson (real estate) Evangelos Mytilineos - Metlen Energy and Metals Madhaven Menon/Mahesh Iyer - Thomas Cook India Frank Hennessy - Recipe Unlimited Christine Magee/Stewart Schaefer - Sleep Country Ed Kinnaly - Peak Achievement George Chryssikos - Grivalia Hospitality Raj Tugnait - Meadow Foods Krishan Balendra - John Keells Murad Al-Katib - AGT Food Ingredients Ajit Isaac - Quess companies Nirmal Jain - IIFL companies Outstanding people provide 2 benefits: Downside protection: They find a way to deal with adversity/view it as opportunity. Unlimited upside: They are constantly delivering surprises - upside surprises, the good kind. Of course, not every investment is going to work out. But by continually upgrading their portfolio of holdings/partnerships over time they keep increasing the probabilities that good outcomes will happen. ————— Let’s pivot in our analysis from theory to practice Theory is good and interesting. But we live in the real world. Let’s review three examples of what has actually been happening at Fairfax’s equity holdings in recent years. New equity purchase - Stelco. Legacy equity purchase - Eurobank Deal flow - Kennedy Wilson - getting an investment idea from a partner. Case study 1: Stelco (a Canadian steelmaker) In November 2018, Fairfax paid $193 million for 14.7% of Stelco (13 million shares at C$20.50/share). On July 15, 2024, Stelco announced that the company had been sold to Cleveland-Cliffs for about C$70/share (consisting of C$60.00 in cash and 0.454 of a share of Cliffs common stock). Over its 6-year holding period, Fairfax earned a total return of about US$544 million (+282%) on its $193 million investment in Stelco. The 6-year CAGR was 25%. That is an outstanding return. Bottom line, the team at Fairfax/Hamblin Watsa absolutely crushed their investment in Stelco. What made Stelco such a good investment for Fairfax? It was the CEO of Stelco, Alan Kestenbaum. Since buying Stelco out of bankruptcy in 2017 (via Bedrock Industries) Kestenbaum's capital allocation decisions were exceptional: Invested smartly in the business. Minntac iron ore supply agreement struck with US Steel in 2020 (during Covid) was brilliant. Sold non-core assets at a premium price (Stelco lands in Hamilton). Bought back 38% of the company’s stock and did not overpay. And the final act? Selling the entire company for C$70.00 in July 2024. This investment provides a wonderful real world example of the incredible returns that can be generated by partnering with outstanding entrepreneurs/CEO’s. This was a new investment for Fairfax. What about the legacy holdings? Those bought pre-2018 and still owned by Fairfax. ————— Case study 2: Eurobank (financial services - with operations in Greece, Cypress and Bulgaria) When Fairfax was culling its legacy equity holdings (those purchased before 2018), it made the call to keep Eurobank. This was a great decision. Fairfax first invested in Eurobank in December 2014. Over a couple of years they invested a total of $1.19 billion. To June 10, 2025, the investment has delivered a total return of about $3.06 billion. What happened? Four things: 1.) Exceptional management. Over the past 7 years, the management team at Eurobank has been putting on a clinic. Their most recent great decision was the purchase of Hellenic Bank (and paying 4 x earnings). 2.) Strong economic performance. The depression in Greece ended. For two elections in a row, Greece has elected a pro-business government. Animal spirits have been unleased. And Greece has had one of Europe’s best performing economies. 3.) Increase in interest rates Central banks around the world ended their disastrous zero interest rate policies. Higher interest rates has spiked earnings for banks. 4.) Patient controlling shareholder. Eurobank was given time to work through their issues. This also allowed them to think strategically and manage the business for the long-term. 2 lessons: When adversity hits, outstanding people will usually figure out a way to get through it. And then when they get to the other side, they will thrive. Example 3: Kennedy Wilson and Pac West Deal flow is a very important driver of investment returns. That is what we will review with this example. Financial markets were in turmoil during the US regional banking crisis in spring of 2023. Kennedy Wilson and Fairfax were opportunistic. Their initial investment in PacWest loans has performed very well. More importantly they used the crisis to build a new business/income stream - making both companies stronger in the process. In June of 2023, Kennedy Wilson and Fairfax purchased a $4.5 billion construction loan portfolio from PacWest. PacWest was caught in the regional bank crisis and they were forced to sell their best assets at a discount. At Fairfax's AGM in April 2025, Bill McMorrow from Kennedy Wilson provided an update. How has the investment performed? Was it a good decision? There are two angles to this transaction: 1.) Initial transaction - purchase of the $4.5 billion construction loan portfolio. 27 of those 65 loans have been paid off at par (they were bought at a discount). Since inception, the loans have generated almost $500 million of interest income. The current portfolio is generating roughly $350 million a year in interest income. 2.) Building the business One of the conditions of the original deal with PacWest was the 40 people who were running the loan portfolio would also move over the Kennedy Wilson. At the same time, the regional banks backed away from the multifamily and student housing market. Over the past 18 months, the new team at Kennedy Wilson has generated about $5.5 billion of new loan originations. As a result, interest income of $350 million is expected to grow significantly in the coming years. “It was another one of these success stories that really turned out well for both our companies." Bill McMorrow, Kennedy Wilson The idea to buy the PacWest construction loan portfolio came from Bill McMorrow at Kennedy Wilson (he also gave Fairfax the idea to invest in Bank of Ireland in 2011 - an investment that delivered +$1 billion realized gain to Fairfax and its shareholders when it was exited in 2017). There are a couple of really important lessons that come from this investment: Relationships matter. Fairfax has built an extensive network of external relationships/partnerships across industries and geographies. This capability leads to deal flow. Fairfax's phone is ringing. This is a great example of how extreme volatility in financial markets has been a good thing for Fairfax and its shareholders. Something to keep in mind in the current environment. What did we learn from our three examples? Exceptional people can make a huge difference. Alan Kestenbaum - Stelco Fokion Karavalis - Eurobank Bill McMorrow - Kennedy Wilson Earlier in this post I provided a list of more than 20 people/companies that Fairfax is partnered with. Here is the crazy thing. I could have provided many more examples (like the three above) of the outstanding work they are all doing for Fairfax. They are generating enormous economic value for Fairfax and its shareholders. We are seeing the power of human capital getting fully unleashed at Fairfax’s $24 billion equity portfolio. ————— Conclusion Human capital is more powerful than financial capital. Fairfax has gotten much better at leveraging human capital within its equity portfolio. The benefits of this pivot to high quality equities are just starting to show up in reported results. Fairfax has been reporting exceptional total results in recent years and one of the drivers has been large gains from its equity portfolio. Interestingly, Fairfax’s stock is still cheap (yes, even after its big run). Investors do not understand/appreciate the amount of leverage that Fairfax has embedded within its equity portfolio (human and financial). And the significant impact that leverage is going to have on business results (including earnings) moving forward. The benefits of this transition to high quality equity holdings are just emerging. Fairfax is a small company. And it is just getting started on this part of its journey. Fairfax is a like a lion that is just entering its prime and the savannah is once again teeming with game (volatility). Float + equities + quality = exceptional returns Add time + compounding = enormous value creation for long term shareholders = magic

-

Viking Vancouver @VikingVan100

-

@Liberty, you are welcome. Since I posted the update Friday night, there have been about 365 downloads of the PDF (290 of the current and 75 of version I posted Friday night) and 115 downloads of the Excel workbook. I think the Barron's article this weekend on 'BRK Wanebees' might have drummed up some new interest in Fairfax. My Twitter/X handle has also picked up well over 100 new followers over the past 4 days (it is up to over 2,600, which is pretty crazy given I only Tweet about Fairfax).

-

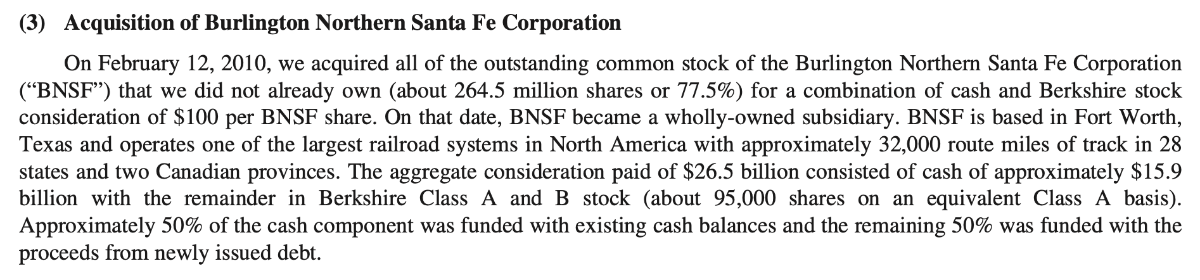

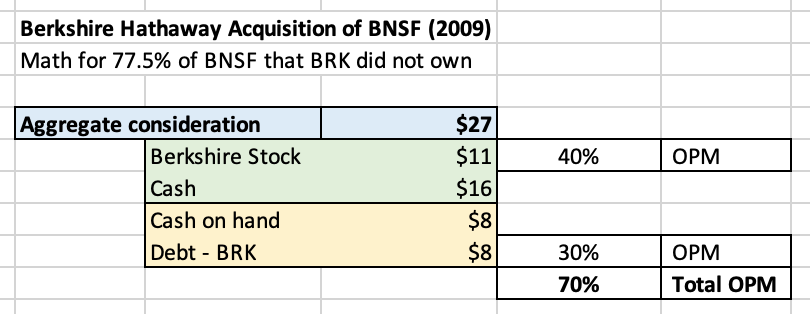

@gfp , I appreciate you post for 2 reasons: 1.) Confirmation on the specifics of the deal. 2.) Help clarifying my thinking around stock issuance. That is (obviously) a pretty clear example of using 'other people's money.' I need to refine my thinking about stock issuance and leverage. Here is a summary of how BRK paid for BNSF. A total of 70% of the total purchase price came from other people. Actual cash contribution from BRK was 30%. Super interesting. From BRK's 2009AR

-

I have a question for those posters on the board who follow Berkshire Hathaway closely... When Buffett took BNSF private in 2009 was part of the take-out price funded by an increase in borrowings at BNSF? Has Buffett also been using the 'LBO light' model I reference in my previous post?

-

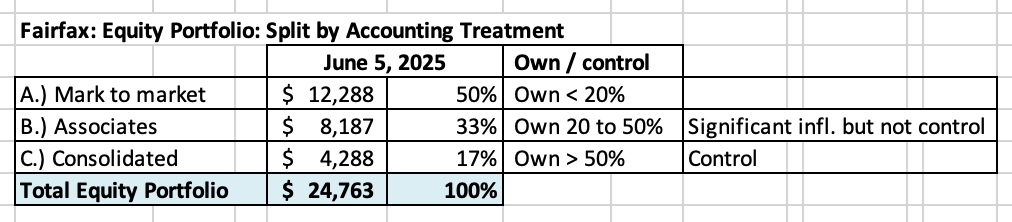

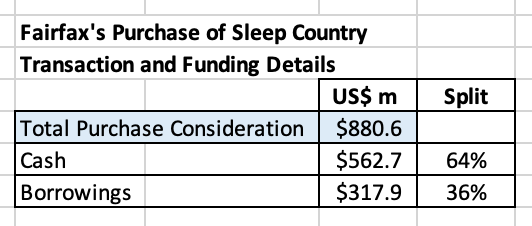

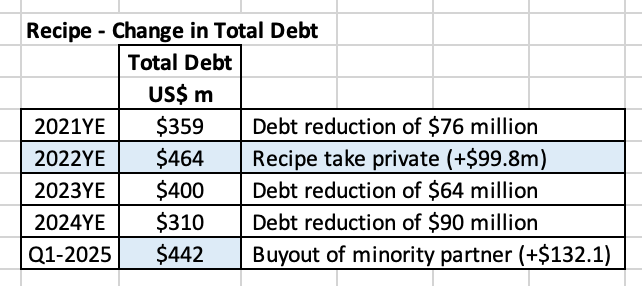

This is the third in a series of posts we are doing on leverage at Fairfax. Links to the first two posts are provided below: The first post introduced the topic and reviewed debt (holding company) and float. https://thecobf.com/forum/topic/21117-fairfax-2025/page/38/#findComment-622326 The second post reviewed 3 tactical ways that Fairfax uses leverage. https://thecobf.com/forum/topic/21117-fairfax-2025/page/39/#findComment-622725 In our post today we will review another way that Fairfax uses debt - in a way that provides embedded leverage. 6.) Debt - At the non-insurance consolidated company level Fairfax’s equity portfolio had a value of about $24.8 billion at June 5, 2025. The equity holdings that are captured in the ‘consolidated’ bucket had a total value of about $4.3 billion, or 17% of Fairfax’s total equity portfolio. These are holdings where Fairfax owns more than 50% and/or exerts control over the business. Fairfax has been aggressively growing the holdings in the ‘consolidated’ bucket of holdings. Over the past three years, Fairfax has made 5 different investments for total purchase consideration of $2 billion. Where did the cash come from? This is where the story gets interesting. Fairfax did not spend $2 billion in cash. It was much less than that. Fairfax used other people’s money to finance a large part of the total purchase price. Usually debt. Equity in one case (Recipe’s minority partner). This is a form of embedded leverage. What is Fairfax doing? With many of its recent large consolidated equity purchases, Fairfax is using a strategy that is similar to one used by private equity funds: Leveraged buyout (LBO) merger and acquisition (M&A) model The LBO M&A model used by private equity can be summarized as follows: Buy another company (using a lot of leverage). Improve its operations. Use the cash flow from the business to reduce leverage. Sell the company for a big profit five or more years later. A small up-front equity investment can deliver an exceptional rate of return over time. The financial assets of the acquired company are used as collateral to obtain the debt financing. The debt is non-recourse to the financial sponsor. The free cash flow of the acquired company is used to: Pay the interest costs. Pay down debt. Grow the business. Funding most of the purchase price with debt applies a significant amount of leverage to the deal for the financial sponsor. As the debt is paid down, the value of the equity increases. Because a small amount of equity was used to make the initial purchase, over time the return on equity for the financial sponsor can be quite large. For this model to work the company being acquired needs to have: A strong management team. Strong free cash flow generation - consistent and resilient (not highly cyclical). Let’s apply what we learned to Fairfax’s many take-private deals from the past 3 years. Fairfax’s ‘LBO light’ M&A model “If it If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.” Fairfax is not a private equity shop. It is a P/C insurance company. As a result, it is going to ‘tweak’ the LBO M&A model described above to fit its business model. Fairfax made two important ‘tweaks’ to the traditional LBO M&A model with its consolidated equity purchases of the past few years: They go easy on the total amount of leverage they use (which lowers the risk). And they sometimes use both debt and equity as sources of leverage (which lowers the risk even more). Because of how they execute the model, I call it ‘LBO light.’ Fairfax has a stated return target of 15% when making equity investments. Using a modest amount of leverage helps Fairfax achieve this target. Let’s look at one example of what they did. Sleep Country In July 2024, Fairfax purchased publicly traded Sleep Country for total purchase consideration of $880 million. Fairfax paid $562.7 million in cash. The remaining $317.9 million came from borrowings. Fairfax supply 64% and ‘other people’ provided 36% of the total amount required to take Sleep Country private. Importantly, the borrowings reside on Sleep Country’s balance sheet and are non-recourse to Fairfax. The free cash flow from Sleep Country will be used to pay the interest costs, grow the business and pay down debt. What does Fairfax like about Sleep Country? My guess is Fairfax likes: The senior management team. The size and stability of the earnings stream that Sleep Country is generating. The long-term prospects of the business. Fairfax bought a quality business for a fair price. Exactly the sort of thing that many investors have been hoping Fairfax would do more of. Welcome to ‘new Fairfax.’ Let’s start to wrap this post up. Why does Fairfax use debt with its non-insurance consolidated holdings? 1.) To achieve the long-term strategic goals of the company. To be opportunistic - strike when the opportunity presents itself. To make larger acquisitions. To make private/control acquisitions. 2.) To maximize value creation for shareholders. To improve the return profile of the acquisition. Is Fairfax being responsible with its use of debt? IMHO, it looks to me like Fairfax is being thoughtful and responsible with the amount of debt that it is using is at the non-insurance consolidated company level. ————— The big picture of what Fairfax is doing Let’s close off by reviewing what Fairfax is doing with its non-insurance consolidated companies bucket of holdings and how it fits in to the bigger picture for the company. Fairfax has 5 income streams that drives its earnings. The first 4 are: Underwriting profit Interest and dividend income Share of profit of associates Investment gains The 5th income stream is ‘non-insurance consolidated companies.’ This is the smallest income stream. But as we learned above, over the past three years, Fairfax has been aggressively building out this collection of holdings. From a run rate today of about $150 million annually, earnings from this collection of holdings could increase to over $300 million annually as soon as 2025 or 2026. This income stream is poised to be Fairfax’s fastest growing income stream in the coming years. This 5th income stream also provides Fairfax with many structural and strategic benefits: Earnings diversification: The earnings from this income stream are not correlated with the P/C insurance cycle. Liquidity: These holdings provide Fairfax with an important source of liquidity - holdings could be sold (in whole or in part) if Fairfax needed cash. Capital allocation benefits: Retained earnings/free cash flow from the various holdings can be re-invested into the best available opportunity within the Fairfax organization. ————— Comments from Wade Burton on Fairfax’s Q3-2024 earnings conference call: “For the $20 billion in equities, not much changed. Our core holdings and investments continued to perform well, all making good income against invested capital. Our experienced investment team is constantly searching for new opportunities, but as managers of insurance float, we have the very great benefit of taking a long term approach to investing. It means we can wait for prices to come to us, and we won’t invest unless we see a margin of safety. “We did make one significant announcement in the quarter. We bought out our main partners in Peak Achievement, an athletic wear and equipment company focused on hockey and lacrosse. It is an outstanding business operating in a highly consolidated industry, well run by Ed Kinnaly and his team, incredible track record, and we paid a fair price. We think we will make a very good return over the long run for our shareholders, and importantly, Ed runs the company very much in tune with the Fairfax culture. “Looking back over the last two years, we’ve made three significant long term equity investments, one in Meadow Dairy, a dominant milk ingredients company in the U.K. that is doing very well; another in Sleep Country, a dominant mattress distributor and retailer in Canada; and now a third, Peak, a dominant sporting goods company focused on hockey and lacrosse. All immediately are or will contribute to our earnings, and we believe all will continue to contribute more and more as their businesses progress.” Jen Allen’s comments on Fairfax’s Q3-2024 conference call “As Wade noted, with our recently announced Sleep Country and Peak Achievement transactions, we expect the operating income from our non- insurance companies reporting segment will grow in the future periods, reflecting the operating income diversity these investments will add to the segment.” ————— Do total debt levels really come down over time? To answer this question, let’s look at two legacy consolidated holdings: Recipe and AGT Food Ingredients. Recipe Unlimited At the time of the take private in 2022, total borrowings at Recipe increased to $464 million. Total borrowings at Recipe were reduced by $154 million in 2023 and 2024, finishing the year at $310 million. In Q1 2025, Fairfax bought out its 16% minority equity partner in Recipe (CARA Operations and the founding Phelan family). The purchase was paid from an increase in borrowings at Recipe of $132.1 million. Fairfax now owns 100% of Recipe (and its significant free cash flow) and did not have to inject any new capital to make it happen. AGT Food Ingredients In Q1, 2025, AGT Food Ingredients sold its non-core rail and infrastructure assets for $132 million and the proceeds were used to pay down debt. AGT had total borrowings of $465 million at December 31, 2024. This drops total borrowing to $333 million, a significant reduction. In both of our examples, yes, total debt levels are coming down over time. ---------- We will continue to go down the leverage rabbit hole... our next post should be out in the next week. In it we will explore human capital. Leveraging human capital was Warren Buffett's real genius (with the help of Munger).

-

@Gregmal and @73 Reds , to think that Berkshire Hathaway might be better off (in terms of growth of intrinsic value) without Buffett - that is a real mind bender idea. I like it. Its not as crazy as it might sound at first.

-

What is the specific problem(s) you are trying to solve for? Is the issue psychology - how you are wired? Or is the issue your investment framework - how to invest? I am a recovering concentration investor. My issue was 95% psychology. My ‘new’ investment framework is being designed to fit better with how I am wired. I started rolling it out 18 months ago. It is going well. It is a work in progress. I have also had to do some internal re-wiring… see my comment below. My investment framework ‘solution’ was to put a big chunk of my portfolio into broad based index funds (XEQT and VOO). I also usually have a fairly big cash position (part of which will cover living expenses for 2 years). I still actively manage a big chunk of my portfolio. I do play with the weightings in the three buckets. ————— It might also be useful to look in the mirror and have a honest discussion with the person you see about why you concentrate. For lots of people it is greed - they want more. And more. The need never stops (no matter how big the pile of dough gets). I think that might be at the root of my concentration problem. If you are serious about changing how you invest you might need to slay some internal demons first.

-

I am trying to understand what is going on with Musk and Trump. And how it impacts Tesla. I think it is safe to say that most Western countries (ex US) hate Musk. As a result, buying a Tesla is not going to happen. Probably the same with Democrats in the US. And now Republicans? Yes, I am exaggerating a little to make my point... but what a crazy set up. Welcome to the new reality of running a business in the US today. Yes, Musk/Tesla is an extreme example. But probably not as much as many think.

-

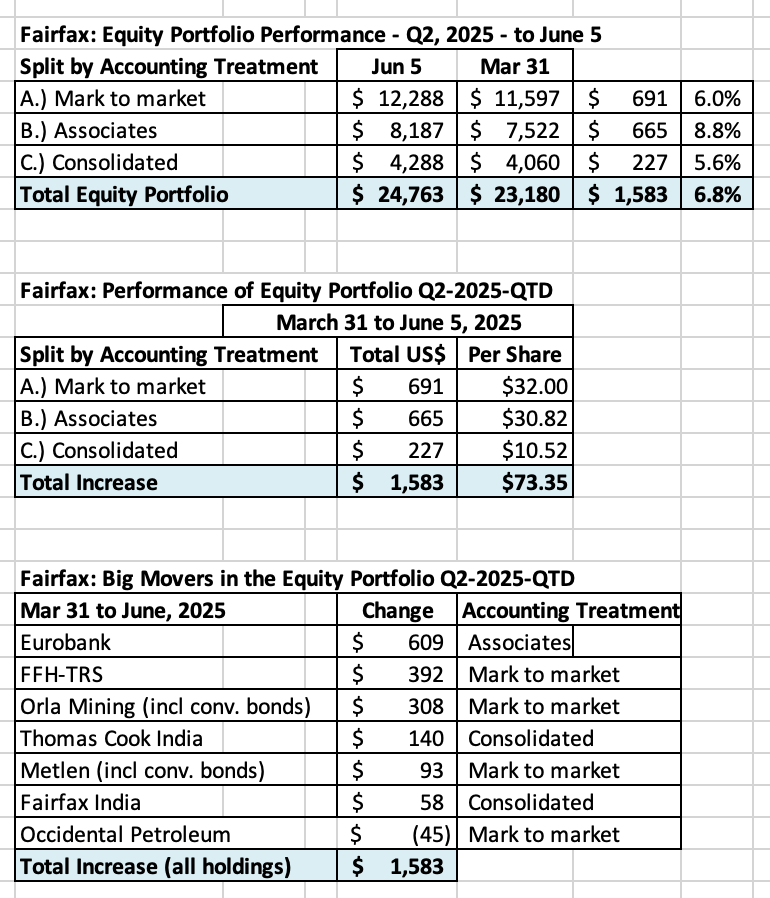

Fairfax's equity portfolio continues to perform very well in QTD-Q2. The equities I track are up $1.6 billion or $73 per Fairfax share (pre-tax). The mark-to-market increase is about $700m or $32 per Fairfax share. This doesn't include mark-to-market gains from Digit (perhaps another $150 million?). Currency is a tailwind.

-

@Redskin212 , great post. You highlight another super important advantage to going the private versus the public route - speed in executing the deal. This is important for how Fairfax typically uses this source of funds (opportunistically to take advantage of short term dislocations). You also highlight the importance of having a long term relationship and a high level of trust - with your private partner.

-

@Maverick47 , BINGO! Of course, what Fairfax is doing with minority partners - using equity - isn't new for them. It's just the latest iteration (tapping private markets versus public markets). As you say, the previous model involved taking part of the insurance company public. And yes, public markets are a big pain in the ass (compared to private markets) - especially later when you are flush with cash and want to buy out the minority partners. And you have to pay a big premium - and even then lots of people are not happy. Thanks for providing some additional colour based on experiences from your previous life. It is very instructive!

-

@73 Reds , I agree. Options can be a hugely asymmetric bet = at a low cost, can provide a great deal of upside leverage to a transaction/investment. I think we are all still learning (do not fully appreciate) all the different things Fairfax has been doing with its business model over the past 7 or 8 years. Of course, over time (the past 3 or 4 years) the picture is coming more into focus - as what they have done flows though into earnings (FFH-TRS is one of many good examples of this). But there is a lag. And lots of what they have been putting in place has not yet hit reported results (it is coming). The optionality/leverage is being embedded all over the place. I am especially interested/excited with what they have been doing with their equity holdings. Investing in equities (unlimited upside) is a form of leverage compared to investing in bonds (where you get a fixed return - your upside is capped). But Fairfax is taking it one step further - with their equity holdings they are now partnering with outstanding founders/entrepreneurs/capital allocators. It has been a 7 or 8 year journey (from old Fairfax to new Fairfax). The result? It is a shift to high quality investing with their equity portfolio (public and private). But quality in a different way (i.e. it is not like buying Coke back in the 1980's) - they are doing it in a way that fits with Fairfax and the current economic/market environment. Partnering with outstanding founders/entrepreneurs/CEO with their equity holdings is giving the equity portfolio at Fairfax an enormous amount of upside leverage moving forward. (Buying/holding shitty equities gives you some leverage to the upside... buying/holding quality equities gives you much, much more leverage to the upside.) Stelco is a great example of the power of the model (and the types of returns that are possible) that Fairfax is currently executing with their equity holdings. --------- Here is another way of looking at/understanding the sea-change that has happened over the past 7 or 8 years with how Fairfax manages its equity portfolio. With 'old Fairfax', when volatility hit financial markets hard it usually hit Fairfax's low quality equity portfolio especially hard. This resulted in big mark to market (unrealized) losses for Fairfax. And this usually caused Fairfax's share price to plummet. As a result, high downside volatility usually caused long term Fairfax shareholders to curl up in a fetal position and hug their blanket tightly. With 'new Fairfax', when volatility hits financial markets the founders/entrepreneurs/CEO's managing Fairfax's equity holdings will (in general) view it as opportunity - something to be exploited (which is the same approach Fairfax will have). Exceptional/smart people tend to find a way to make lemonade out of lemons. Yes, there will be some short term volatility in price - but the majority of the holdings are not mark to market (they are associate or consolidated). It is a brave new world for long term Fairfax shareholders.

-

This is our second in three posts on leverage and Fairfax. In our first post we introduced the topic and looked at 2 structural ways that Fairfax uses leverage - debt and float. In this post we will review 3 tactical ways that Fairfax has used leverage - to grow their P/C insurance by acquisition and to buy back stock (total return swaps and dutch auction). To read our first post ‘Leverage - Part 1’ click the link below: https://thecobf.com/forum/topic/21117-fairfax-2025/page/38/#findComment-622326 Definition of leverage: “Using other people and/or their money to boost returns and/or improve the quality of the company.” Leverage - Part 2 When people think about leverage they tend to only think about debt. But it can also be attained using equity. How? That is what we will review next. 3.) Equity - Minority partners Growth by acquisition From 2015 to 2017, Fairfax executed an aggressive acquisition strategy to build out its global P/C insurance footprint. At the time PC insurance was in a soft market so top-line growth was stagnant and underwriting margins were under pressure. The investment side of the business was also struggling - bond yields were very low. As a result, the stocks of P/C insurance companies were cheap. This was the perfect time to grow by acquisition. From 2015 to 2017, Fairfax made 11 different purchases of P/C insurance companies. The total cost was $7.6 billion. To provide context, at the end of 2014, common shareholders’s equity at Fairfax was $8.4 billion. Fairfax saw a big opportunity and they acted with conviction and backed up the truck. How did Fairfax pay for the acquisitions? To pay Fairfax used the traditional sources: equity (it issued Fairfax shares) and debt. But Fairfax used one more novel source of capital - it brought on minority equity partners. Of the total cost of $7.6 billion, Fairfax supplied $5.3 billion (70%) and minority partners supplied $2.3 billion (30%). Fairfax's contribution was $3.3 equity (new share issuance) and about $2 billion in a combination of new borrowings (debt) and retained earnings. 'Other people’s money' - debt + minority partners - funded a significant portion of the total purchase price of $7.6 billion. Why did Fairfax use minority partners? As we explained earlier, P/C insurance stocks were on sale. At the same time, Fairfax’s investment management business was underperforming. As a result, Fairfax’s shares were also on sale - trading only at a slight premium to book value. This was not a good time to issue equity. So Fairfax wanted to limit the amount of equity it used (shares it issued). At the same time, Fairfax also needed to be careful with the amount of debt it used. It needed to keep the ratings agencies and insurance regulators happy. What was the solution? Classic Fairfax. Get creative. Do something no one else was doing/thought of - bring on minority equity partners. The benefit By bringing on minority equity partners Fairfax was able to do more acquisitions - it allowed them to buy more with less up front capital (supplied by Fairfax). Most importantly, Fairfax had complete control of all P/C insurance acquisitions - its partners were passive partners. Exit strategy Using minority partners is a temporary funding arrangement for Fairfax. By temporary I mean a 5-year or so arrangement. Yes, that is 'short term' for Fairfax. Down the road, when Fairfax had the cash, they would take out their minority partners. And this is what has happened over the past 3 years. Fairfax is flush with cash these days. Today, Fairfax owns 100% of Brit and 80% of Eurolife (minority partner OMERS was taken out completely). At Allied World, the minority stake has been reduced from 32.5% to 16.6%. And it looks likely increase their ownership of Allie world to 100% in the next couple of years. Call option feature When the deal is put in place with the minority partner it includes a call option feature. The call option gives Fairfax the right - but not the obligation - to buy out their minority partner at a specified price and by a specified date. Fairfax profits if the underlying asset increases in price. What was the cost to Fairfax? Allied World paid dividends to its minority partners in 2019, 2020 and 2021 of $126 million. This provided minority partners with an 8.0% return (using $1,560 million as the cost base). If accurate, this is a solid return for the minority partners (remember, this was a time when interest rates were very low). This has been a great deal for Fairfax. Why? Let’s discuss this next. What are the benefits to Fairfax from bringing on minority partners? Using minority partners allowed Fairfax to be opportunistic and maximize the size of its P/C insurance purchases from 2015 to 2017 (secure control). While at the same time keeping total debt and new share issuance (Fairfax shares) at a reasonable level. With these transactions, Fairfax used two different kinds of leverage: debt and equity (minority partners). Strategic: From 2015 to 2017, Fairfax was able to build out its global platform and significantly increase the size of the company’s P/C insurance business. This was a significant accomplishment that mades Fairfax today a much stronger company. It diversifies their insurance business. It also provides them with significant growth opportunities. Financial: Fairfax made their acquisitions at the perfect time. P/C insurance companies were out of favour. This means they did not overpay. They made the purchases a couple of years before the onset of the hard market in 2019. This gave Fairfax a couple of years to integrate the new companies. And then to fully capitalize on the historic hard market that has played out over the past 6 years. Fairfax has been able to double the size of its insurance business (net premiums written) in the current hard market. Organic growth is the best kind of growth for a P/C insurance company. With the call option feature, Fairfax is able to take out the minority partners at an attractive price (given how much the businesses have increased in value over the holding period). This was only possible with the use of minority partners and the $2.3 billion of capital that they supplied to Fairfax. This is a great example of Fairfax using other people’s money to capitalize on a temporary and significant opportunity that existed (P/C insurance companies were on sale). With these transactions, Fairfax did both - boosted returns and improved the quality of the company. This is yet another example of exceptional capital allocation from the management team at Fairfax. ———— Running the business with a long term focus I described this use of leverage by Fairfax as being ‘temporary.’ Is that correct? Yes. Fairfax runs its business for the long term. Decisions, like the ones described above that play out over 5 or 10-year spans of time are ‘short term’ for them. Managing the business with a long term focus is a competitive advantage for Fairfax. It allows them to think and manage the business differently than other P/C insurance peers - and as a result deliver higher returns for shareholders. ———— Minority partners (equity) - Capital allocation Fairfax added a new tool to their capital allocation toolbox - minority partners (equity). Yes, this is a non-traditional tool. As we described above, it is very effective when used properly. This gives them an important source of future cash. Temporary - usually paid back after 5 or so years. Acceptable cost. Not debt (keeps the ratings agencies and regulators happy). Equity. Most importantly, it gives them another tool that allows them to be opportunistic and capitalize on significant short term opportunities. ———— The team at Fairfax was not resting on their laurels. In late 2020, Fairfax added a brand new tool to their capital allocation toolbox. Is volatility in financial markets a good or a bad thing for Fairfax? The next two examples of leverage will be instructive. 4.) Total Return Swaps (late 2020/early 2021) - Getting exposure to 1.96 million shares at $373/share “Opportunities come infrequently. When it rains gold, put out the bucket, not the thimble” Warren Buffett A wonderful opportunity presents itself In 2020, financial markets experienced some wicked volatility. But what happened in the broader market was nothing like what happened to Fairfax. For most of 2020 Fairfax's stock was trading at a historically low valuation. Fairfax communicated this loudly to investors: in June 2020, Prem Watsa bought $149 million in Fairfax stock ($311/share). (For context, when Jamie Dimon made his famous and much lauded 'vote of confidence' purchase of JP Morgan shares in 2016 he spend $25 million). Circle of competence In late 2020, Fairfax understood how undervalued their stock was. As a result, buying back stock was a high certainty / low risk investment for Fairfax. Position size What should an investor do when they find a great investment that they understand better than anybody else and it is trading at a historically cheap valuation? They should ‘back up the truck.’ They should make the investment a concentrated position. The investment In late 2020/early 2021, Fairfax purchased credit default swaps giving it exposure to 1.96 million Fairfax shares at an average cost of $373/share. The total notional value of the investment was $731 million. Yes, a total return swap is a non-traditional tool for P/C insurance companies to use in their investment management business. At the time, Fairfax had 26.2 million effective share outstanding. This investment gave them exposure to 7.5% of shares outstanding. This was a very large investment. Where did they get the cash? The FFH-TRS position had a notional value of $731 million. That is what it would have cost Fairfax to buy 1.96 million shares. Back in late 2020/early 2021, Fairfax did not have a lot of extra cash. The hard market in P/C insurance was taking off. Hard markets happen only about once every 20 years - when they happen they need to be the priority for excess capital. Fairfax also closed out its last short position in December 2020 and this resulted in a $529 million investment loss. Debt levels at Fairfax were ok. But taking on more debt to fund a buyback was not an option. What else could they do? Fairfax got creative. They pulled a play from the hedge fund playbook. They didn’t buy the shares directly. They did the next best thing… they purchased total return swaps. This kept their capital outlay to a minimum. And they got exposure to 1.96 million shares of Fairfax (without actually owning the stock). What has been the gross return from this investment? Since being put on, the FFH-TRS position has delivered to Fairfax a total return of about $2.54 billion. This is before carrying costs. That is an exceptional return over a 4.5-year period. The FFH-TRS has become one of their best investments ever. What is the cost of this investment? The cost to carry this investment is a component of two things: LIBOR/SOFR plus a fixed rate (2%?) = 4.32% + 2% = @ 6.5%? While holding the TRS, Fairfax collects the dividend paid on its shares. The dividend was $10/share in 2021, 2022 and 2023. And $15/share in 2024 and 2025. Total dividends paid since the position was established = $60/share. Fairfax has received more than $100 million in dividends since the position was put on. Does this look roughly correct? I look forward to hearing what other board members think. How has the investment worked out? Bottom line, the return to Fairfax from this investment has been significant. This is a great example of how the team at Fairfax has used other people’s money to boost earnings. To be opportunistic and take advantage of a short term market dislocation - this time the historically low price of Fairfax’s shares. Exit strategy The FFH-TRS is an investment for Fairfax. It is not a permanent holding. Fairfax began exiting the position in Q4, 2024 when they reduced their exposure by 203,800 shares. At March 31, 2025, Fairfax continued to have exposure to 1.76 million shares. Of interest, Fairfax purchased the shares from the counterparty and retired them. The FFH-TRS investment was like a stealth buyback (at $373/share). ————— You are going to experience deja vu with this next example. What is better than making one great investment? Making two great investments. 5.) Dutch Auction (December 2021) - Buy back 2 million shares "Too much of a good thing can be wonderful!" Mae West Another wonderful opportunity presents itself In 2021, Fairfax’s shares continued to trade at a very cheap valuation. Circle of competence In December 2021, Fairfax understood how undervalued their stock was. As a result, buy back stock was a high certainty / low risk investment for Fairfax. Position size What should an investor do when they find a great investment that they understand better than anybody else and it is trading at a historically cheap valuation? They should ‘back up the truck.’ They should make the investment a concentrated position. The investment On November 17, 2021, Fairfax announced a Substantial Issuer Bid. They repurchased 2 million shares at $500/share. The total cost to Fairfax was $1 billion. At the time, Fairfax had about 26 million effective share outstanding. Buying back 2 million reduced effective shares outstanding by 7.7%. This was a very large share repurchase. Where did they get the cash? Fairfax did not have $1 billion lying around at the time. What capital they did have was being used to allow the P/C insurance companies to drive growth/capitalize on the hard market. Debt levels at Fairfax were ok. But taking on more debt to fund a buyback was not an option. What else could they do? Pull out the 'minority shareholder' tool from their capital allocation toolbox and use equity. To fund the big buyback Fairfax sold 9.99% of Odyssey to OMERS. They tapped the private equity market. This raised $900 million for Fairfax. Fairfax issued equity in Odyssey at 1.7x book value. And bought back Fairfax shares at 0.9x book value (from Fairfax's Q4 conference call in February 2022). What has been the gross return from this investment? To calculate the return from this investment, let’s keep things really simple. Let’s pretend that instead of buying back shares, Fairfax had simply bought shares in another company. This makes the return calculation simple. Looking at it this way, the gross return Fairfax has earned over the past 3.5 years from buying back 2 million shares in December 2021 has been $2.35 billion. This is what Fairfax has earned before costs. What is the cost of this investment? OMERS invested $900 million. Let’s assume OMERS is earnings 8% = $72 million per year (Fairfax paid OMERS a dividend of $65 million in 2022). This puts the total cost over the past 3.5 years at about $252 million ($72 x 3.5 years). Fairfax no longer has to pay a dividend on 2 million shares. The total savings from this over the past 3.5 years has been $100 million (4 payments of $10+$10+$15+$15=$50 x 2 million = $100). If my numbers are roughly accurate, the net cost to Fairfax to execute this investment over the past 3.5 years has been about $142 million. How has the investment worked out? The ‘net’ return from this investment has been about $2.2 billion. This is yet another example of how the team at Fairfax has used other people’s money to boost its returns. Yes. I know my return calculation is not technically the right way to look at this. But the benefits of stock buybacks can be really hard to conceptualize. The important message here is Fairfax’s dutch auction in 2021 has delivered an amazing return for the company and for shareholders. Exit strategy Fairfax uses minority partners as a source of capital to take advantage of a significant short term opportunity that has materialized. It is used as a short term source of funds (not intended to be permanent). Now that Fairfax is flush with cash it can take OMERS out and return its ownership position in Odyssey to 100%. My guess is this is what Fairfax will do in the next couple of years. Using leverage (other people’s money) to capitalize on a temporary significant short term opportunity was a brilliant move on the part of the management team at Fairfax. ————— Fairfax was very opportunistic in late 2020 and 2021. They were able to buy back/get exposure to 4 million Fairfax shares at an average cost of $437/share. This was 15% of shares outstanding. How much of their own capital did they have to use? Very little. The ‘return’ over the past 4.5 years from these two investment has been over $4 billion. How did they do it? They used other people’s money. Freaking brilliant. ————— We have one more post coming in our 3-post review of how Fairfax uses leverage. We have much more to cover on this interesting and important topic. Among other things, our next post will dig into how Fairfax is leveraging 'human capital' in new ways that are not yet recognized or fully understood (in terms of its impact on future results).

-

@Haryana, we are of the same mind. +1

-

@Maverick47 , your comment really hits the nail on the head. My goal with the poll was to highlight just how many significant exceptional capital allocation decisions the management team at Fairfax has made over the past 10 years. To your point, many were synergistic with others. It is telling that my list was missing a couple of big items - this was pointed out by other posters. Thanks to everyone on the board for voting and especially for taking the time to comment. There is lots of wisdom in the comments. But here is where things get a little crazy… Fairfax accomplished all of this when they were capital constrained. What can this company deliver/accomplish when they are all cashed up? With record operating earnings locked and loaded for the next 4 years? Their insurance business has never been better positioned. Their investment management business has never been better positioned. The quality of their portfolio of equity holdings has never been better (in terms of management, cash flow, prospects). Their capabilities as capital allocators (and as a company) appear ideally suited for the current economic environment (lots of volatility). As fun (and profitable) as the past 4.5 years have been, I can’t wait to see what they do the next 5 years. ‘Time is the friend of the wonderful company.’ ----------- Below is a summary of the results with 73 people having voted.

-

My vote was ‘Other.’ The choice to maximize the growth of the P/C insurance business in the hard market since 2019. As a result Fairfax has been able to almost double the size of their insurance business over the past 5 years. This has significantly increased float and the size of the investment portfolio. At the same time, the quality of the insurance business has also improved (measured in terms of underwriting). This will be the gift that keeps on giving.

.png.c1c3251350bfd4a9d744b47e6cf54787.png)