Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

To partially close the loop, I exited 1/2 of my flex trade in Fairfax today (described above). The flex part of my position was up about 6% (on average). I started buying (more) Fairfax in mid October (yes, I was early) and continued to add to my position pretty much all the way to its recent the bottom. I did get a little more aggressive than usual with the size of my flex position - and that was because the stock kept selling off (at the same time fundamentals/the story continued to improve). Yes, Mr Market (volatility) can be an investors best friend. Of interest, the stock bottomed out the day earnings were announced (at around $1,550). Today, Fairfax traded as high as $1,740, which is an increase of $190 or 12% in less than 3 weeks. The key with my flex position is to not be too piggish. It is meant to be a short term trade. So sell it when it hits my return target (which in this case was about 6% or more). That is what I did today (well 1/2 of it). Bottom line, this trade has been a great way to squeeze a little more juice out of my understanding and investment in Fairfax while also being thoughtful about position size.

-

@Parsad, I agree that simplicity is super important to being able to analyze an investment properly. But a deep understanding of the investment is required first - this is what allows the simplicity to happen. Having a deep understanding also allows for conviction. And conviction does two things. It allows an investor to: Manage through and exploit volatility - not panic when it sells off. Get the right position size - how much to concentrate. My view is to be successful over the long term with concentrated positions an investor needs to be able to toggle between the two: simple and deep understanding.

-

It appears relations between Canada and India are improving. Nice to see. When things fell off the rails a year or two ago, there were concerns if it would impact Fairfax/Fairfax India’s business interests in India. Canada's Foreign Minister says Ottawa is working fast to advance India trade deal https://www.thehindu.com/news/national/canadas-top-diplomat-says-ottawa-is-working-fast-to-advance-india-trade-deal/article70320053.ece Both countries expect to be able to double bilateral trade by 2030, and noted that Canada is India's seventh largest trade partner for goods and services

-

@gfp, great point. Definitely something to include when thinking about Fairfax India was an investment. We kind of had a nice period there for a couple of years where the currency was somewhat stable.

-

Time to get reacquainted with Fairfax India. Why? The shares are trading at $16.00. BVPS is $20.72. So shares are trading at a discount to BV of $4.72/share, or 23%. Is 23% enough of a discount to get excited about? No, it's not. OK, so why am I so interested in Fairfax India at $16.00/share? I think book value of Fairfax India is materially understated. As a result, the discount the stock is currently trading at is far in excess of 23% to its economic/intrinsic value. I also think Fairfax India is exceptionally well managed. What is the problem at Fairfax India? One investment the company initiated in 2016 (it closed in 2017) - the purchase of part of Bangalore International Airport Limited (BIAL), the third largest airport in India. It performed spectacularly well for Fairfax India the first 3 years (in terms of growth in BV). But since 2019, its performance has been terrible - literally a dog with fleas. To make matters worse, management at Fairfax India has been aggressively buying much more of it over the years. Today it has an economic ownership stake in BIAL of 74%. What a bunch of dummies! BIAL now represents 53% of Fairfax India's total investments. How can management at Fairfax India be both 'exceptional' and 'dumb'? Of course, they can't be both. So, let's try and figure out which it is. What is the problem at BIAL? The 'value' of the company has not really changed in 6 years. At December 31 2019, 100% of BIAL was valued at $2.65 billion (using Fairfax's FV). At September 30 2025, 100% of BIAL was valued at $2.67 billion. How is this impacting Fairfax India? BIAL is Fairfax India's largest holdings. Over the past 6 years, BIAL increased from 23% of total investments to 53% today. BIAL is such a large holding, its 'poor performance' has submarined Fairfax India's performance. As a result, common shareholders' equity at Fairfax India has changed only modestly over the past 6 years. At December 31 2019, it was $2.58 billion. At September 30 2025 it was $2.83 billion. But here is where the Fairfax India story gets interesting. Do you really think the value of BIAL is the same today as it was 6 years ago? Of course, those of us who have followed BIAL over the past 6 years KNOW it's worth much more today than it was worth at the end of 2019. And guess what… the management team at Fairfax India knows it too. That is why they have been buying all of BIAL they can get their mitts on. To answer the question we posed earlier, the management team at Fairfax India is smart like a fox (they are NOT dumb). BIAL is exceptionally well managed (and has been since Hari Marar was installed as Managing Director and CEO in July 2017, after Fairfax India got a control position in BIAL). It is a completely different airport today than it was 6 years ago. It added a second runway which began operating December 2019. And a second terminal, which doubled capacity from 25 million to 51.5 million passengers, which began operating early 2023. An expansion plan for T2 will increase capacity further to 80 million passengers by the end of the decade. Passenger growth at BIAL is taking flight - with a long runway still ahead of it. The plans to develop the property adjacent to the airport are also progressing nicely (an initiative called 'Airport City') - creating a third earnings stream for BIAL with strong growth prospects over the next decade. How much is BIAL worth? Fairfax India is planning to IPO part of BIAL to the public in India (as part of Anchorage). When this happens, we will get an updated market value for BIAL. My guess is it will be significantly more than Fairfax India's current fair value. And given the size of BIAL within Fairfax India, this has the potential to significantly increase the BV of Fairfax India. Which should increase the share price of Fairfax India. When will the IPO of Anchorage/BIAL happen? That is the rub. We don't know. But given the economic/intrinsic value of BIAL is growing nicely every year, a delay in the IPO is actually a good thing for a long term investor. Of course, there is much more to the Fairfax India story. And the BIAL story. So please do your own due diligence before making an investment decision. For a more in-depth review of Fairfax India: James Emanuel: https://youtu.be/Ksctkf4Frkw?si=D-xfhumWl8wlcesX

-

@djokovic1, Iike you, I also get good value from looking back at Fairfax's history - it clearly shows how much the company has changed. And why the future will not resemble the past. The Fairfax supertanker is going in an entirely new direction.

-

I love reading about Fairfax's history. It is really interesting. But is it informational for an investor today? I think it is a potential minefield for many investors. My view is the best way to think about Fairfax's history over the past 40 years is through the lens of 5 completely different companies - each one had a very different business model (what was actually driving earnings at the time). And, of course, earnings is the key. Looking at past versions of the company (and valuations like P/BV) and then using that as a core input to understand and value the company today is really problematic (IMHO). And that is because too many important things have changed at the company. This exact issue has been tripping up many smart investors for the past 5 years - Fairfax's colourful history is messing them up. It is stopping them from being able to look at the company with fresh eyes - to understand and value it for what it is today (unencumbered by its past). Charlie Munger was the master at understanding psychological biases - and how they constantly trip up investors. Fairfax is a real life example of this - it is tripping up people on this board. Is it any wonder the rest of the investing community is having such a hard time 'getting it' when it comes to understanding and valuing Fairfax? This is such a fascinating topic! Example: Druckenmiller talked about how he got his big break in his mid-20's. His boss at the time promoted him ahead of older and much more experienced traders. Why? He was young, smart, fresh and - most importantly - unencumbered by his past (he was a newbie). The older much more experienced traders had just been through some viscous bear markets - on the other side, Druckenmiller's boss knew they would be way too cautious. Lots of investors still have this exact same problem with Fairfax today - they continued to be haunted by its past. Remember this when you read Fairfax's history - there is a good change it is going to mess you up. Fairfax is like a kid who has been trying to figure out what they want to be when they grow up. Over the decades they kept trying different things. Learning what works and what doesn't. Over the past 5 years it appears Fairfax has finally figured it out - what they want to be. They have grown up right in front of our eyes. More mature. More responsible. Enjoying success. (Does it really help to know about their partying years?)

-

@djokovic1, great analysis. Looking at its evolution over the past 40 years, it looks to me like Fairfax keeps morphing. 1985-2000: Start-up? Build out P/C insurance business via aggressive acquisitions. Investment management business performing well. 2000-2006: turnaround. Massive losses in P/C insurance business (under-reserved) almost sink the company. Investment management business continues to perform well. 2007-2010: Hedge fund? Reap massive gains from CDS/equity hedges. 2011-2020: investment management lost is way (equity hedges/shorts and poor equity investments) masking a slowly improving insurance business. 2021-2025: After a decade of work, high quality insurance business emerges. Investment management fixes its investment framework. And deals with poorly performing equity holdings. Result is high quality investment management business. It is like Fairfax has been on a journey as a company - to find the ‘right’ business model. It has continuously tried different things. Importantly, it has kept learning from its mistakes (first with insurance and later with investment management). The company that exists today has never existed before. Comparing it to past versions (and multiples) makes no sense to me. I think that is the point you are making - and I whole heartedly agree. It’s like Fairfax has been on a 40 years journey - trying to create a great company (able to exploit the P/C insurance business model). I think they just (finally) figured it out/cracked the code. Mr. Market just doesn’t see it yet. That is a great set-up for a long term investor (getting a compounding machine but not having to pay for it). Another way to look at Fairfax is through the lens of a person. And their evolution and growth over time. Today, Fairfax is a talented, experienced and mature company - it is just entering its prime.

-

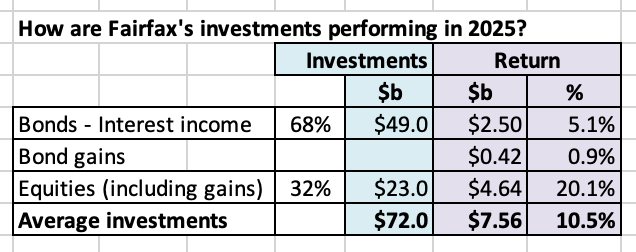

Why does Fairfax invest in equities? To earn a higher return (compared to if it just invested in bonds). Does it? Yes. In our previous post we provided the proof (the historical numbers). 2025 is shaping up to be a fantastic year for Fairfax with investments. How good? Fairfax is tracking to earn $7.56 billion on its investment portfolio. This is a rate of return of about 10.5% (on an average portfolio of about $72 billion). We can break the return down further: Fixed income (including gains from bonds) = 6.0% Equities/investment gains (excluding bonds) = 20.1% Fairfax's stellar return on its equity portfolio in 2025 is not a one hit wonder. Returns have been strong for each of the past 5 years. More importantly, Fairfax has been slowly upgrading the quality of its equity portfolio over the past 6 or 7 years. Their hard work is showing up in (better) reported results. Importantly, having a higher quality portfolio suggests future results will continue to be strong. Welcome to new Fairfax. At some point Mr. Market will figure it out. The return on the equity portfolio makes sense Fairfax's largest equity holdings are having stellar years in 2025, lead by Eurobank, FFH-TRS and Orla Mining. But many other smaller holdings are also having great years (CIB, Altius, Dexterra etc). But the story is even better My numbers below do not capture all the value creation that is happening at Fairfax these days. My numbers do capture excess of FV over CV for associate and consolidated holdings. But they do not capture all the value creating that is happening at some of the private holdings (like BIAL and Poseidon). And Fairfax has been aggressively building out the size of its private holdings in recent years. Another interesting angle: Leverage (thank you insurance float) Leverage of investments to common shareholders' equity is about 2.9x.

-

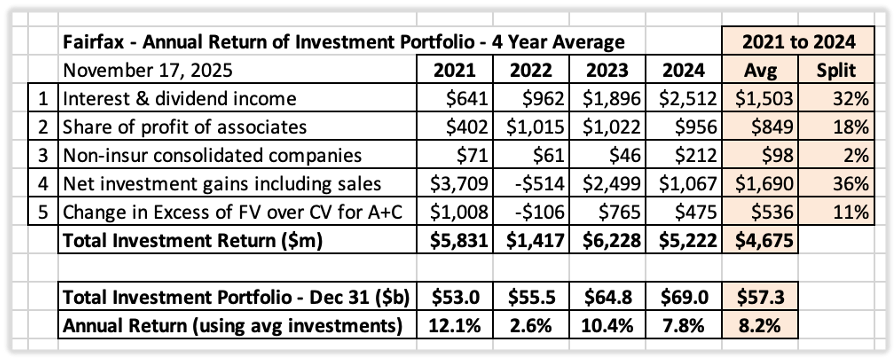

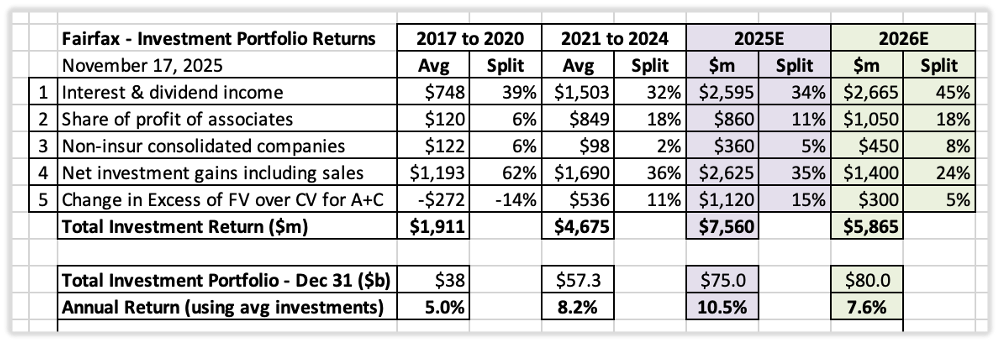

What is the Total Return Fairfax is Generating on its Investment Portfolio? Past, Present and Future. In this post we explore the returns Fairfax has generated on its investment portfolio. What we learn will help us evaluate the management team and to value the company. Our analysis breaks down into seven parts: Part 1: Introduction Part 2: How Fairfax Invests Part 3: Methodology for Measuring Returns Part 4: Past Performance Review (2017-2024) Part 5: Future Estimates (2025-2026) Part 6: Normalized Rate of Return Part 7: Conclusion ———— Part 1: Introduction Fairfax has built an exceptional business model This is no exaggeration. Over the past 39 years, Fairfax’s per share market value (in US$) has grown at a compound annual growth rate (CAGR) of 19.2%. Among roughly 6,000 publicly listed companies since 1985, Fairfax ranks as the 8th best performer – an extraordinary achievement. (Source: Fairfax AGM, April 2025) Two questions arise: How has Fairfax delivered such outstanding long-term returns? How is the company positioned today? Fairfax tends to be underfollowed by investors. As a result, many struggle to answer either question. The key to Fairfax’s success lies in its two business engines and their impact on earnings: Property & Casualty (P/C) Insurance: Generates an underwriting profit, measured by the combined ratio. This is pretty straight forward. Investment management: Generates a total return on its portfolio, measured by the rate of return. This is more complex. This post focuses on Fairfax’s total return on its investment portfolio – both in absolute dollars and as a percentage return – starting with historical data and ending with future estimates. ———— Part 2: How Fairfax Invests Let’s get the big picture. Portfolio Size: As of December 31, 2024, Fairfax managed an investment portfolio valued at approximately $69 billion. Investment Allocation: Fixed Income: $47 billion (68%) Equities (broadly defined): $22 billion (32%) How does this compare with peers? Most P/C insurers heavily favour fixed income, typically allocating about 95% to bonds and 5% elsewhere. Fairfax’s 32% allocation to equities is notably different, more akin to a much younger Berkshire Hathaway. How Fairfax invests is unique among peers. Why a big equity allocation? Because equities deliver higher long-term returns than bonds - historically proven. With a sizeable equity stake, Fairfax aims to generate better portfolio returns, driving stronger earnings and ultimately a higher stock price to benefit long-term shareholders. Why don’t peers follow suit? Likely due to their lower tolerance for short-term volatility. Fairfax embraces this volatility for the greater return payoff. To summarize, Fairfax’s unique portfolio mix and large equity exposure should, in theory, lead to superior investment returns compared to typical P/C insurers. Do the numbers back this up? ———— Part 3: What Methodology Should We Use to Measure Returns? Before diving into the numbers, we need to clarify our approach by answering three questions: Economic or Accounting Return? Most focus on accounting returns—they’re simpler and safer. But Warren Buffett advocates for economic return, as it better captures real shareholder value creation over time. We agree and will focus on economic returns here. What Inputs Will We Use? We calculate Fairfax’s total economic return using five key quarterly-reported inputs: Interest and Dividend Income: From fixed income and dividend-paying market to market equities. Share of Profit of Associates: Fairfax’s share of pre-tax earnings from stakes in companies it partially owns including Eurobank, Poseidon, EXCO Resources, Fairfax India (their associate holdings). Non-Insurance Consolidated Companies: Pre-tax earnings from companies Fairfax owns including Recipe, Sleep Country, Peak Achievement, Grivalia Hospitality, TC India, Meadow Foods, AGT Food Ingredients and Dexterra. Net Gains (Losses) on Investments: Both realized and unrealized gains on stocks and bonds, including insurance-related gains. Annual Change in Excess of Fair Value over Carrying Value: For non-insurance associate and consolidated holdings. Economic value being created that is not captured in reported earnings. What Time Frame? For investors - unlike speculators - a longer-term horizon matters. Warren Buffett recommends five years; we extend that to eight years (2017-2024) plus two future years (2025-2026) for a full decade view. This helps smooth out short-term volatility. ———— Part 4: Fairfax’s Investment Returns, 2017 to 2024 We analyze two four year periods: 2017 to 2020: Average annual return from investments: $1.91 billion or ~5.0% This was a challenging period for the company. Key headwinds included: Ultra-low interest rates globally depressed fixed income yields and interest income. Equity portfolio underperformed, due to short positions and too many struggling holdings. (The last short position was removed in late 2020.) Despite the significant headwinds, Fairfax was still able to achieve a respectable return of 5.0%. Net gains on investment (at 62%) were the biggest driver. 2021 to 2024: Average annual return from investments: $4.68 billion or ~8.2% Tailwinds replaced headwinds: Rising interest rates lifted bond yields and interest income, with Fairfax’s short-duration fixed income portfolio well positioned. Legacy underperforming equity holdings were fixed. New equity investments performed well. Fairfax achieved a much better return of 8.2%. The company also diversified its investment returns, reducing reliance on investment gains. ———— Part 5: Future Estimates (2025 and 2026) 2025: Estimated total return from investments $7.56 billion or ~10.5% Reasons: Strong first 9 months, fixed income yields around 5.1%, and high-quality equity portfolio driving outsized gains. 2026: Estimated total return $5.87 billion or ~7.6% (likely conservative) In 2025, at $2.6 billion, investment gains are elevated; 2026’s forecast of $1.4 billion for investment gains is likely understated (and we already know Fairfax will book a gain of about $250 million when the sale of Eurolife’s life insurance business closes in Q1, 2026). Fairfax is generating very good returns on its investment portfolio. The sources of the returns are diversified – and becoming more so. ———— Part 6: A Normalized Rate of Return? What is a reasonable normalized return to expect going forward? We estimate Fairfax can sustainably generate about 8% per year on its investment portfolio (economic return basis). Why 8%? Because Fairfax’s management has demonstrated best-in-class capital allocation over the past five years, positioning them well for future success. Comparing to peers: Typical P/C insurance peers earn about 5.5% annually on their portfolios—mostly fixed income. Fairfax’s 8% return therefore represents a meaningful advantage of approximately 2.5% per year. ———— Part 7: Conclusion Fairfax manages a substantial $69 billion portfolio, uniquely invested with a significant equity component (32%). This strategic difference drives superior returns: 5.0% average return during the tough 2017-2020 period 8.2% average return more recently (2021-2024) Estimated 10.5% return in 2025 A normalized expectation of 8% economic return going forward is reasonable and represents a clear advantage over peers. Fairfax is very well positioned. This investment performance explains part of Fairfax’s 19.2% CAGR in per-share market value over 39 years. The advantage comes from how they invest, coupled with skillful capital allocation and leverage (2.9x investments to common shareholders’ equity).

-

As long as BIAL is increasing in value each year I am a happy camper. My view is that asset is special. An Anchorage IPO will simply be the cherry on top.

-

+1. And I think the management team is stellar.

-

When it comes to the fees Fairfax earns from Fairfax India i think one of Buffett’s core principles might help the discussion: ‘Price is what you pay. Value is what you get.’ Lots of focus on ‘price paid’. (Fees) It is the easy part. Very little focus on ‘value received.’ This is the difficult part. Book value tells part of the story. But there is much more to it: What is economic/intrinsic value of Fairfax India today? How much hidden value has been created? How good is management? What is the ‘earnings power’ of Fairfax India (i.e. its potential, the value of decisions yet to be made)? On top of this, Fairfax India shares are trading at US$15.85. Looks like a Black Friday sale to me.

-

Owning Fairfax India in recent years (as a long term investor) has felt a little like those investors holding the CDS position in the Big Short after the housing market had clearly started imploding - and their position was not getting marked properly. My guess is a big payday is coming for investors in Fairfax India... but it will require conviction and patience. @Crip1, if you are measuring your return solely on market price then, yes, your return has been poor compared to alternatives, like a broad based index fund. A question: Does economic/intrinsic value matter? My view is Fairfax India's market value (share price) does a good job of reflecting the value of the assets that are publicly traded and the assets that have been monetized over the years. And it does a terrible job of reflecting the economic/intrinsic value of the private assets, especially BIAL. And the disparity is growing every year. In many ways, Fairfax India is like a coiled spring. Over time, it keeps selling other smaller assets and buying more and more BIAL. Each purchase coils the spring tighter and tighter. Over time, Fairfax India is becoming more and more a levered play on BIAL. And I love it. Because I like the asset so much.

-

The important thing to me is what is going on under the hood at Fairfax India. I think BIAL is a jewel of an asset. My guess is it is increasing in value nicely every year. That is the primary the reason why I own Fairfax India today. You can get a high quality asset like BIAL at a significant discount to its economic/intrinsic value. I also love Hari Mahar and the management team. It is such a no brainer at $16 (risk/reward). With Fairfax India, I think lots of people on this board are focussed on the price of the stock (i.e. trying to figure out/time exactly when it will re-rate etc)... and/or the fee structure. For me, both of those are non-issues. The big question for me is do I make Fairfax India a meaningful permanent position or continue to trade it. I have done very well trading in and out of it over the years. However, almost every year, Fairfax India keeps buying more and more of BIAL. As a result, they have an economic interest now in BIAL of 74%. I love this asset. Therefore, I likely should keep a core position moving forward - it is only a matter of time until this asset gets re-valued higher. And as others have pointed out, it could be a meaningful amount. In other words, patience might be the best strategy for me for Fairfax India moving forward. Yes, I do get some exposure to BIAL with Fairfax. But it is very small compared to what I get from owning Fairfax India directly.

-

Mr Market is a wonderful and very accommodating fellow. Fairfax India has sold off aggressively the past month or so and is down to $16.00/share. Why? No idea. What to do? Today, I am very happy to re-establish a position in the company about $16.00/share. Book value at Sept 30, 2025 was $20.72/share. Of course, this materially undervalues BIAL (and other private assets). What is the catalyst? At some point we will get an Anchorage IPO. And this will likely spike the BV of Fairfax India. When will this happen? No idea. And it doesn’t matter (the when) - the economic/intrinsic value of BIAL is compounding nicely each year. Time is definitely the friend of this business. Could Fairfax India go lower from here? Yes, of course it could. If fact if the market averages continue to sell off, it is likely that Fairfax India will extend its current sell off. After all, stocks are volatile.

-

Here is a plug I posted on Twitter for David’s new book. Fairfax was founded in 1985. A $1,000 investment with Prem and team back then would now be worth more than $1 million. Yes, an amazing return = CAGR of 19% over 40 yrs. How did they it do it? In his book called ‘The Fairfax Way’, author David Thomas provides many of the answers. The narrative for Fairfax is upside down Fairfax is well known for a few of the big mistakes made that it has made. What is not well know are the many important things that the company got right. And given its outstanding performance over the past 40 years, it got way more right than it got wrong. What did it get right? The answers go way beyond the numbers. It includes the people, structure and culture - and a moat that has been slowly increasing in size around the company over the past 40 years: Prem Watsa (founder and CEO) - Driven, optimistic, risk taker, unconventional, ‘right’ temperament, able to attract and retain talent, nice and more… High quality management - Fairfax is stacked with quality people in all parts of the organization. We get to hear from many of them (past and present). A proven organizational structure. Decentralized operations - Run by entrepreneurs. Centralized capital allocation - Run by a best-in-class team. Long term focus. A strong culture - Its employee retention has been amazing. David’s book explores all of these topics and more. It is a treasure trove of information on the company. It is a great resource for investors. I really enjoyed and got great value from reading the book (I learned a lot). David, well done and thank you! ————— The 19% return over 40 years is in US$ and assumes all dividends were reinvested.

-

@valueinvesting101, the historical numbers for each of the 5 items in my model come directly from Fairfax’s consolidated income statement. There is no double counting (that I am aware of). Dividends from associate holdings are considered return of investment not return on investment. They do not show up in ‘interest and dividend income’ or ‘share of profit of associates’. Summary of accounting treatment of dividends received by Fairfax from associate holdings (accountants please feel free to chime in): Does not show up in the income statement. Shows up as a reduction in the carrying value of the holding on the balance sheet Shows up in the cash flow statement (operating activities) I also have a model that calculates the return that Fairfax earns on its investment portfolio. That includes excess of FV over CV for non-insurance associate and consolidated holdings (and excludes underwriting profit). I should have an update out in the next week or so.

-

@wondering, yes, it is important to think about what the risks are to Fairfax. But I separate them into the ‘unusual’ risks and the ‘usual’ risks. When it comes to ‘unusual’ risks, these are the ones that could take the company down (or severely cripple it). These are the unknowable things. Something bigger than a 1-in-100 year massive insurance event - bigger than a big earthquake on the West Coast of the US or a cat 5 hurricane hitting the north East Coast of the US (in highly populated centres). That would be bad. But I am thinking of something worse. Something we have never seen before that isn’t built into the models. This risk is the #1 reason I keep my Fairfax core position size to a reasonable level for me (max 35%). I think this is kind of why Buffett has always been so cautious with how he has structured Berkshire Hathaway. He KNOWS a big , bad one is coming… he just doesn't know when. You are discussing the ‘usual’ risks. I prefer to talk about the usual ‘risks’ and the resultant ‘opportunities’ at the same time. Part of this also has to do with time frame - what often appears to be a big ‘risk’ in the short term can also be an even bigger ‘opportunity’ in the medium term. To only talk about one and not equally the other doesn't make sense to me (i.e. is not balanced). In general, I think Fairfax is a much safer investment today than it has ever been in its history. I think this is reflected in the two rounds of upgrades the company has received from ratings agencies in recent years. Higher quality P/C insurance = higher underwriting profit. Higher quality equities/normalized interest rates = higher investment returns. I think the build out of the private non-insurance consolidated companies buckets is important in this regard - it gives the company even more financial flexibility. The company looks much more resilient today than it has ever before. And each year it looks to me like they are building in even more financial resilience.

-

The book is short, at about 340 pages. That likely limited the author quite a bit in terms of what to talk about out. It appears one of the core objectives was to communicate extensively on Fairfax’s culture, primarily through the lens of the build out of the P/C insurance business. The investment management side of the business is discussed, but more at a very high level. To do this part of Fairfax’s business justice, it likely would have needed another +200 pages. That would have made the book too long. And taken it off topic (away from the culture theme). What is amazing to me is what the company was able to accomplish over the past 39 years when different arms were tied behind their back: 1985 to 2011 - insurance was generally underperforming, some years massively. In some respects, for the first 15 years, this was kind of by design (what do you expect when you are buying a lot of clunkers from highly motivated sellers)? 2011 to 2020 - investment management was underperforming massively. This was not by design. And the underperformance was caused by three different problems: Equity hedges - removed in late 2016 Significant short positions - last one was removed in late 2020 Too many terrible equity investments, made largely from 2014-2017 - last one, Boat Rocker, was finally ‘fixed’ in 2025. The interesting thing to me is this - despite the issues I outline above, Fairfax was still able to compound at 19.2% for 39 years. What happened that allowed the company to do this? In some respects, that to me is the real story of Fairfax. Because today Fairfax no longer has any hands tied behind their back. The version of Fairfax that exists today has never existed before. If they can compound at 19.2% when facing big headwinds for much of the time, what can they compound at today? Yes, we need to exclude some of the massive growth in the very early years, so that would take down the 19.2% CAGR. But regardless, there is some magic in the Fairfax business model that we still do not fully understand today (I sure don’t). And that is one of the reasons I am confident the company can compound ROE at a mid to high teens rate over the next 5 years, and perhaps longer. What is the ‘something that happened’ at Fairfax that allowed them to compound at 19.2% for 39 years despite the big set-backs? Decentralized structure? Long term focus? Culture? These are important parts of the answer. But I think there is more. One example is how good they are at incubating start-ups on the insurance side of the business (First Capital, ICICI Lombard, pet insurance, Digit) and then monetizing them for big gains (each of these delivered an investment gain of about $1 billion or more). Perhaps I am looking to quantify things too much.

-

Fairfax has 5 income streams that flow through to reported earnings. What are they? How big are they? What are we forecasting for 2025 and 2026? How have they changed over the past 4 years? What are some of the key take-aways? These are the questions we will answer below. What are they? Underwriting profit Interest and dividend income Share of profit of associates Non-insurance consolidated companies Net gains (losses) on investments How big are they? Below is a chart which provides a summary of the size of each of Fairfax’s 5 income streams. Included is: For context, the average for the six years from 2016 to 2021. Actuals for the past 4 years: 2021 to 2024. My current forecast for 2025 and 2026. Forecast for 2025 and 2026 I am forecasting that Fairfax’s 5 income streams will come in at about $8.1 billion in 2025 ($387/share), which would be a big increase from $6.5 billion in 2024 ($301/share). How have the income streams changed in recent years? There are a couple of things that immediately jump out: 1.) The total growth of the 5 income streams over the past 4 years has been significant. From $2.5 billion (average from 2016-2021) to $8.1 billion (estimate for 2025), an increase of $5.6 billion or 224%. This is a 4-year CAGR of 34.1%. 2.) The per share growth of the 5 income streams over the past 4 years has been much better than the total growth. From $96/share (average from 2016-2021) to $387/share (estimate for 2025), an increase of $291/share or 303%. This is a 4-year CAGR of 41.7%. Fairfax has been very aggressive with share buybacks in recent years and this is delivering significant value to long term shareholders. 3.) Most of the significant growth seen in recent years has been in the four buckets that comprise operating income (underwriting profit, interest and dividend income, share of profit of associates and non-insurance consolidated companies). This is important because operating income is considered to be the highest quality sources of income for a P/C insurance company. They are considered to be high quality because they tend to be predictable and durable. The growth in operating income at Fairfax over the past 4 years has been exceptionally large. From $1.25 billion (average from 2016-2021) to $5.50 billion (estimate for 2025). From $49/share (average from 2016-2021) to $262/share, an increase of 435%. This is a 4-year CAGR of 52.0% Operating earnings now represents about 81% of total income streams at Fairfax, up from 51% (average from 2016-2020). The income streams of Fairfax have been transformed over the past 4 years – they are much larger and of much higher quality. This is really important. Let's explore this further. Operating income Underwriting income has increased in importance from 12% of total income streams (average from 2016-2021) to 24% (2026E). Fairfax's P/C insurance business has exploded in size. And its underwriting has improved. This is further confirmation that the quality of this business has improved. Interest and dividend income has increased in importance from 28% of total income streams (average from 2016-2021) to 37% (2026E). Yes, Fairfax has been a big beneficiary of higher interest rates. We can sum the two remaining parts of operating income: share of profit of associates and non-insurance operating companies. I think Fairfax views them as one bucket. David Thomas in his book 'The Fairfax Way' refers to Fairfax creating a third economic engine and I think this bucket might be what he is referring to. This 'bucket' has increased in importance from 10% of total income streams (average from 2016-2021) to 20% (2026E). This was one of the buckets that propelled Berkshire Hathaway's growth over the decades. It appears it is just starting to have the same impact at Fairfax. Importantly, this 'bucket' is not tied to the P/C insurance cycle - it should see even more growth in the coming years as the hard market slows (and Fairfax allocates more capital to investments). 4.) Underwriting income represents about 24% of total income streams. For most P/C insurance companies, underwriting income is closer to 45% of their total income streams. From an earnings perspective, Fairfax is MUCH LESS exposed to the P/C insurance cycle (i.e. a soft market) than other P/C insurance companies. For two important and very different reasons: Underwriting income is a much smaller income stream (as a percent of the total) for Fairfax compared to traditional P/C insurance companies. At Fairfax, capital can be easily shifted from P/C insurance to its investment management business. This will allow Fairfax to continue to compound capital at high rates even as the hard market slows. Most other P/C insurance companies do not have this capability. This is important to keep in mind in the coming years as the hard market comes to an end.

-

Ok. Just finished the book. What is my key take-away? I think ‘we’ have a very good handle on Fairfax. By ‘we’, I mean the members of this board. Does this mean I learned nothing from reading the book? Of course not. I learned plenty. But it is good to know that we are generally on the right track today with our analysis/understanding of Fairfax and our assessment of where the company is likely headed in the coming years. The book spends a fair bit of time chronicling the evolution over the past 40 years of the P/C insurance business at Fairfax. What a crazy ride the first 25 to 30 years were. We get to hear directly from all of the top executives in the P/C insurance part of the business. I really liked the case studies at the end (for the many insights they provided). My guess is this focus was by design - P/C insurance has transformed over the past 10 years into a high quality business and has become today the engine at the core of Fairfax’s business model. I don’t think you could make this claim for the first 25 years of the company’s existence. This, of course, has important implications for Fairfax’s fundamentals today, its future and how the company should be valued. I don’t think this is the current/consensus view with investors and analysts. What is something I learned? All parts of Fairfax are stuffed with exceptional people. I kind of understood this already - one of the big benefits of attending Fairfax’s AGM each year is the opportunity to hear directly from the various executives at the different events. The book introduces us to a wider range of key players at Fairfax (past and present). One of these was Rick Salzburg (he passed away last year). Rick plays a prominent role in the book - so readers get an introduction and hear directly from one of the individuals who was critically important to Fairfax’s evolution into the powerhouse company that it is today. It is super helpful/informative to hear firsthand from many of the first class people at Fairfax, like Rick. Anyways, I don’t intend this post to be a complete review of the book. I will have more to say about the book, which I really enjoyed reading (David, well done!). What are some of the key take-aways from board members?

-

Fairfax's equity portfolio is having a stellar year in 2025. It is not just the big boys like Eurobank and Orla Mining. Many of the smaller positions are also performing exceptionally well. Altius Minerals is a smaller equity holding for Fairfax (it is a top 25 based on MV). The stock has increased in price by 64% in 2025. The market value of Fairfax's position has grown from US$127 million at the start of the year to $208 million at Nov 13, 2025, an increase of $81 million. Altius also pays a small dividend. What is the total return Fairfax has generated on this investment since inception? Fairfax made an initial investment in Altius of C$100 million (US$78 million) in April 2017. Over the past 8.5 years, Fairfax has generated a total return on this investment of about US$153 million, or 197%. This is a CAGR of about 13.6%. Total return = increase in market value + interest + dividends Summary Altius is yet another example of the team at Fairfax's investment management business allocating capital exceptionally well. Who is Altius Minerals? Altius is a diversified , long-Life, natural resource royalties company. https://altiusminerals.com/_resources/presentations/corporate-presentation.pdf?v=0.336

-

And to frame it another way, if investors/analysts really do understand #2 (reinvestment) and #3 (compounding) how is it possible Fairfax can trade today at US$1,600/share?

-

No, I don’t think they are the same. But they are complementary/synergistic. But I might not have explained it well. 2.) Reinvestment is key for a company like Fairfax today. They are generating an enormous amount of excess capital. They can reinvest in a way that delivers below average, average or above average rates of return (in aggregate). My guess is most investors are not thinking deeply about reinvestment at Fairfax. Let alone how good Fairfax is at it. Reinvestment at Fairfax deserves its own long post. Suffice to say, Fairfax has many good options, they are skilled and they are generating above average returns (in aggregate). 3.) So what? This is where compounding comes in to play. My view is people can define compounding but they don’t really get it. Human brains can think linearly but not exponentially. This is probably what leads them to sell compounding machines when they own them - they simply underestimate the power of compounding and time. So some investors who understand #2 (the importance of reinvestment at above average rates of return) will still not invest (or sell a position prematurely) because they don’t really understand #3 (compounding). Smart people have said Buffett’s greatest strength is his patience. He understands compounding/exponential growth. Patience ensures you do not interrupt exponential growth. Getting both #2 and #3 right is really hard. This is perhaps part of the reason why Philip Fisher said you NEVER sell a compounding machine when they when you have found one - regardless of what the valuation is.