John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

You obviously don't understand, that I'm not inclined in any way to swing at any of your provocations, nor do you even try to understand why it is so.

-

Awesome, and much better, @Pelagic! Thank you!

-

What has that to do with my critisism of your uncritical reposting of posts from X from a socalled Assistant News Director employed at Florida's Voice, a ticket seller, who looks like he's desparately trying to grow a beard, coming out of puberty like a bat out of hell?

-

In such case, that would likely be the most influential event for the future of the planet in our lifetime, @Spekulatius, It's really an unpleasant intellectual exercise to think about such a scenario.

-

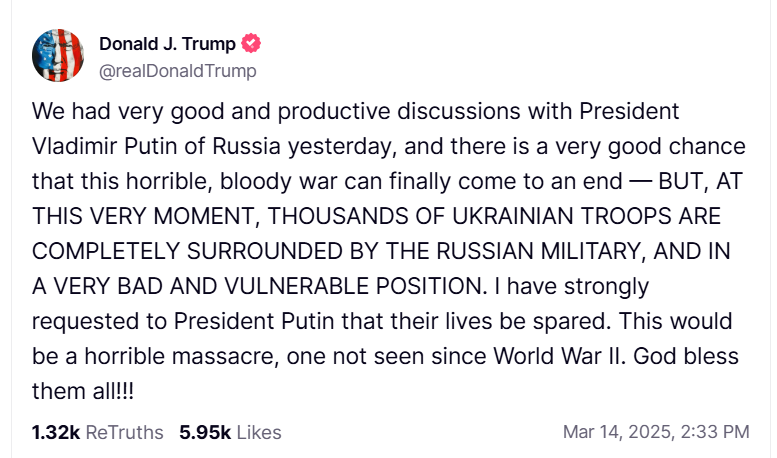

Today, I tried to find a visual status on the war by a map. It was quite hard and took some time, the whole main stream media surface here in Denmark is pretty much smeared in Western geopolitics. I found this, by now two days old : BBC - News - World/Europe - the Visual Journalism Team [March 13th 2025] : Ukraine in maps: Tracking the war with Russia. So, at least Thursday, the Ukrainian troops in the Kursk area do look surrounded by Russian troops, if one looks carefully at that particular map covering that area.

-

Just the usual biased *BS* and crap - unverified, second hand or worse - from X you drag in here on CofB&F, James [ @james22 ], Here is the whole truth about it, without anything left out : AP News - World News [March 14th 2025] : Greenland political parties join together against Trump comments about annexing the island. - - - o 0 o - - - Politiken [March 14th 2025] : The big winner of the election: "Trump's statements from the US are inappropriate". Subtitle : Rejection of Trump must be strengthened, believes Greenland's acting head of government, Múte B. Egede, who will unite parties after the US president answered in the affirmative to the question of a possible annexation. - - - o 0 o - - - Politiken [March 12th 2025] : Greenland's new political leader is young and liberal and has come down hard on Donald Trump. Subtitle : The winner of the Greenlandic election, Jens-Frederik Nielsen, is in favor of an independent Greenland. But it must be done peacefully. First of all, he himself is surprised that he won the election by such a large margin. - - - o 0 o - - - - DR.dk - The question of Greenland's future [March 15th 2025] : Demonstration against Trump's desire to take over Greenland: 'We are sending a message that they should leave us alone' Subtitle : At 1 p.m., demonstrations against the American president will begin in Greenland's two largest cities. - - - o 0 o - - - I'm as worried as can be about what all this brings.

-

Sanjeev [ @Parsad ], You certainly above sensed the overall Danish national and local picture, sentiment here, correctly. Bird flu sucks, and is such a downer for everyone hit! So, naturally, Denmark will send eggs to USA, to raise new American chickens. - Just wait and see. [Right now I'm in intense thoughts and doubts if this involves Danish chickens getting hit hard by language barriers in the US [<- j/k]].

-

The United States of America, - the World Wide Insurance company, financed by 100 years zero percent float, making everybody feel dry, warm, safe and secure [promises to the left] :

-

Mike [ @cubsfan ], @Ulti is here not the only one, who thinks you need to pay more attention to your modus operandi of discussion. If you're already carried away while posting, you've lost it in advance.

-

Please take it easy, @Sweet, From reading CofB&F I understand that you're British, and I'm Danish. We really don't need to play along with this sale of hot air on bottles from a fridge, if we don't want to. Eventually, if executed, it may end up doing very well, untill it doesen't. Absolutely reckless fiscal policy deferring debt problems 3 or 4 four generations into the future, to those you'll never know, because you've passed away long before they were born, so screw them!

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Page 2, paragraph 1 : - I've never in my life seen this combination of age and ownership requirements for director qualification. -

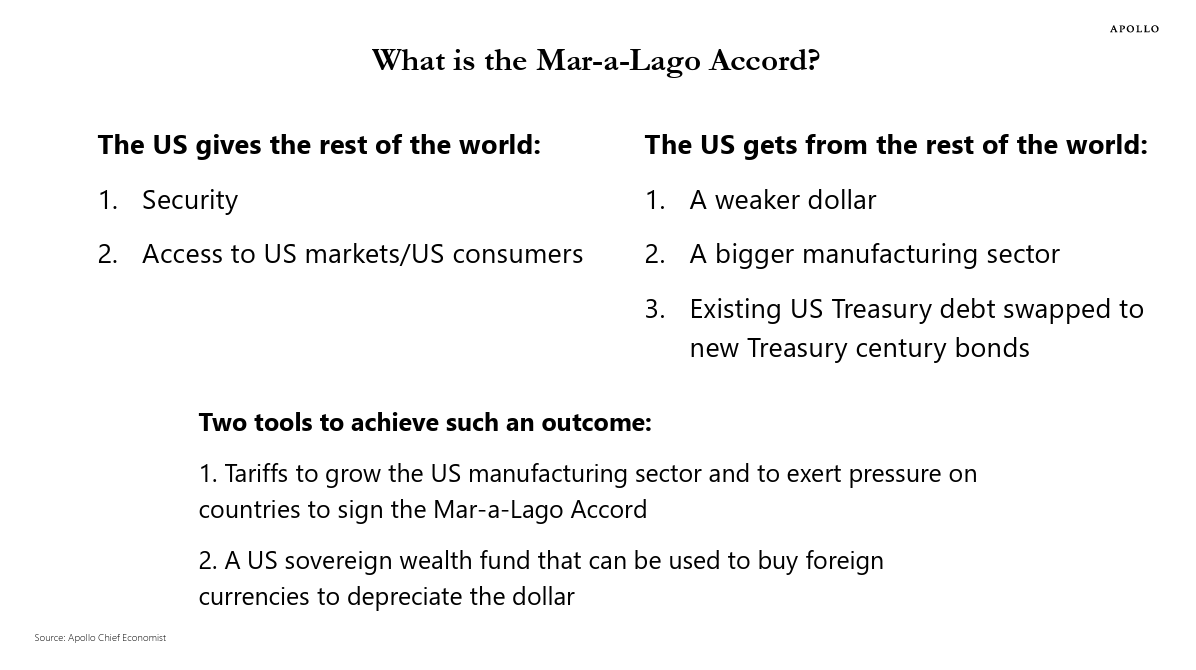

From Apollo Academy : What is the Mar A Lago Accord? Link

-

No sweat, @Xerxes, Danes do not behave so. The fun was limited to things like placing digital mobile phones in drawers in the crew accomodation section of the AOPS ship in the 3-D drawings in SmartPlant, as Friday fun, before entering weekend. I have no information about what Irving Shipyard actually did with those drawings. Danes are just such troublemakers!

-

Yahoo!Finance [March 14th 2025] : Americans sour on economy as inflation expectations hit highest level since 1991.

-

This. Absolutely awesome post, that I have been chewing on the whole day today. If I had a 'bookmark' button here on CofB&F, I would for sure push it here. Do you remember in POTUS' first presidential period, when he eventually ran - more or less - out of steam, and was asked critical questions about why there was registered 'executive time' - over and over again - in his public calendar, just to keep him clear of anything and everything, to rest, answering the question with something like : '... I have a tough job!'? - - - o 0 o - - - And the other guy is already way in over his head, and he doesen't even have clue about what has started to happen to him by now.

-

@Xerxes, Lol!, yes that was a tough and long lasting war! And based on Canadas experience with the tough Danes during that war, Canada decided to ramp on surveillance in the Artic waters around Canada, ordering first six, later expanding the order to eight Arctic Offshore Patrol Ships, which are built [six produced and completed so far] at Irwing Shipyard, Halifax, Nova Scotia, Canada. And who won the design contract? - A Danish ship design engineering company! - - - o 0 o - - - Edit : https://truthsocial.com/@realDonaldTrump/posts/114161039436456514

-

More on the Tesla-Musk paradox : Reuters - Business - Autos, transportation [March 14th 2025] : Tesla warns it could face retaliatory tariffs. Summary : Tesla warns of retaliatory tariffs in wake of Trump's trade policies Tesla emphasizes difficulty in sourcing parts domestically Autos Drive America trade group warns tariffs could disrupt U.S. production Tesla letter mentioned in acticle attached. USTR-2025-0001-00111195-CAT-5983-Public Document.pdf

-

Putin is likely stalling his response by now, likely because of Russian war progress by now in Kursk region. I personally speculate, that he does not really have any idea of how to answer, because he fears the american reaction, if he just replies with with a 'no'.

-

The meeting between NATO secretary general Mark Rutte and POTUS derailed shortly into a Greenland talk [again], wich has caused some lively communication in Denmark and other places, i.e. here between Danish MP Rasmus Jarlov and Roger Stone : - - - o 0 o - - - Meanwhile, USA has asked Denmark for help with ... eggs [ ] : FødevareWatch [English : Food Watch] - Porduction [March 14 2025] : The US has asked Denmark for extra eggs Subtitle : American authorities have contacted the Danish Eggs trade association. Eggs have become a hot political issue in the United States due to rapidly rising prices and shortages in supermarkets. -So much for bird flu in USA. - - - o 0 o - - - Nobody can complain about lack of entertainment value here.

-

@Cod Liver Oil, 30 days after 18th February, ref. :

-

@Spekulatius, Yes, he looks like something dragged into the house by the cat. Likely stressed, likely because of the pressure he feels from various head winds in his sphere, perhaps he is sleep deprived, too.

-

It seems to be working satisfactorily, over time. The key so far has been patience of the holder.

-

I'm pretty sure the first time I bought Berkshire was a thursday. No matter the weekday, you may have done well, if you've been holding on, @longlake95!

-

Mike [ @cubsfan ], About the NATO members' defence spending budgets, you are right. Spain [holding its head low, pretty much saying nothing all the time], Italy [sending this white dressed, high heeled, talking, lady [Meloni] every time there is a meeting, giving interviews over and over again], committing nothing to the cause, and then our our foot-dragging friends up in Canada, who now suddenly have their hands full! [Trump-wise]

-

Roger [ @rogermunibond ], 'Lost him'? - He has never had him anyway!