Spekulatius

-

Posts

15,151 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

I sold $CATY for a quick flip. Sad to let here go, but bought other banks stocks from the proceeds. ($PNC, $TFC, more $USB). I think the super regionals and perhaps BAC is the way to invest, or gamble in stuff like $WAL

-

5% unemployment and 2% inflation is better than 5% inflation and 2% unemployment. There I said it.

-

New position in $LUV (starting out small). Edit - bought starters in regional bank stocks $PNC and $TFC

-

The same could be said for any other bank. CATY clients are chinese individuals and small business. They have established relationships with most customers. I don’t even think that 1.86% criticized assets is all that high given their focus on small business operating in urban centers. Most of their loans are floating rate, so further interest rate rises should not hurt so much even if they have to raise deposit interest rates (which they started doing). I do think that their deposit Beta moved closer to one, so further rises interest rates won’t do them much good.

-

I am sure the new CEO has a great time on his first day on the job.

-

The Fed may have asked JPM nicely. I think JPM will end up owning them.

-

SBNY wasn’t technically insolvent. They had losses from treasuries of about ~$2.5B, if I see this correctly, with $6.4B in equity. They had issues with liquidity (mostly large business accounts that are uninsured) and a taint from their crypto involvement that lead to a bank run. They have a liquidity problem, not a solvency problem. There are a lot of banks that can fail as well now, after SBNY fails. What we are seeing here are large scale viral nature bank runs. Game stop time for banks.

-

The failure of Signature Bank ($SBNY ) is scarier from a bank investors perspective than SVIB’s. SBNY had issues, but they weren’t insolvent even accounting for losses in their security portfolio. it was simply the liquidity shortfall from bank run that did them in. The bank run was caused by reputational damage from crypto and liquidity strain because crypto deposits were leaving, then came the know können on effect from SIVB. This wasn’t a bad bank per say, it neither was SIVB.

-

I think the bailout for depositors was done to prevent sudden deposit flight like the one who did SIVB in. There were likely many request from depositors the last few days to move fund away from banks that looked like they are having issues. With financials, perceived issues can very quickly become real issues due to reflexivity. Things can become much viral much faster than even 14 years ago during the GFC and it’s also a bit easier to move funds out. These frictionless systems can move very quickly in a herd like fashion even with many small participants as the GME short squeeze and similar events have shown.

-

I am a bit surprised that Signature bank is shut down. They clearly were on the ropes, but that was awfully quick. Maybe we should tax crypto to pay for this mess.

-

This is not Joe Sixpacks bank. Joe is protected anyways up to $250k and not many average people have more than that in a single bank account. These are corporation and VC firms who have CFO’s who made decisions. It was also Peter Thiel who literally cried fire and instigated a bank run here. are is well known as a libertarian. So, I am not sure sob stories “we couldn’t have known better “ are appropriate here. Feels a bit like trying to buy insurance after you had a car crash. In any case, the depositors will probably lose 20% or thereabouts above 250k. Everything below 250k is insured and can be paid out, so it’s not like Mondays payroll for a small form is in jeopardy here. Since liquid assets (even after haircuts ) are a bit more than 50% of the balance sheet, about 50% of deposits should be available very quickly (next week) with probably the other 30ish percent being paid out in weeks or so, all without rescue package. It’s not quite as catastrophic as it’s made out to be. The FDIC is government sponsernd but works like a Mutual insurance cos that banks need to pay in. If coverage is increased, then the contributions need to increase too, there is no free lunch.

-

I don’t think Berkshire is going to touch SIVB (too messy, he needs to replace management etc) but I think he might get some phone calls from other bank CEO’s that want to raise capital quickly. I am sure he is open to preferred deals with equity kickers with the right bank. SCHW might be a good bet. Berkshire not just get money quickly without fuzz, but also the seal of approval from Omaha, which is equally valuable.

-

Why would companies tap their revolvers? They only do this if they themselves are in a liquidity crunch. The bigger risk is deposit runs, Imo. I think those are unlikely, but there are few banks with strained liquidity and narrow focus like PACW that may have to do something.

-

This gal wasn’t the head of risk management. Looks like she was head of risk management for the UK sub which had little to do with the blowup. Head of risk management was Laura Izurieta, which came from Capital One and apparently had a carrier in banking.

-

Long list of filing on 3/10/2023 regarding SIVB. companies that held cash are RBLX, RKLB, ROKU, SGMO https://www.sec.gov/edgar/search/#/q=Silicon%20Valley%20Bank&dateRange=custom&startdt=2023-03-09&enddt=2023-03-11 Also, crypto of course involved with a stable coin failure: https://www.wsj.com/articles/crypto-investors-cash-out-2-billion-in-usd-coin-after-bank-collapse-1338a80f?mod=hp_lead_pos1

-

LOL, how many people actually read 10-K’s? I bet less than 1% of the people investing or even less than 10% of the people claiming to do a lot of reading when investing. To be fair to the banks, you need to look at both the asset as well as the liability side to get the full picture.

-

During the last financial crisis, E*Trade got into trouble, because they also started a banking sub and made it easy to get home equity loans. They had some toxic looking assets on the balance sheet that they could work out over time, but it does not take much for the customers to get running, especially since brokerage is very commoditized product with low switching costs. I guess these things repeat. Schwab is probably fine here, but what I don’t get is why even take a chance? Why not just create a short treasury ladder instead of going for long duration bonds for an extra 1% or so yield.

-

Nope. Banks can get liquidity by various sources, but for example overnite FHLB advances cost ~4.5% interest rates right now. That hurts if a large part of your balance sheet is parked in underwater MBS with a now 10 yearn+ duration and 2.2% interest rates (was probably 1.8% when they bought them) https://www.fhlbdm.com/products-services/advances/

-

BAC and a lot of other banks did:

-

What bank is most likely acquirer of SIVB?

Spekulatius replied to ratiman's topic in General Discussion

SIVB is a $200B bank. Only a major National bank can swallow this one whole. Think JPM, WFC, BAC. It’s too large for a bank like USB, especially since they are currently involved in the Union bank acquisition and have some rebuilding on the capital ratios to do. -

I am fairly sure the yield curve inversion will at some point revert whether we get a recession or not. Even if we don’t get a recession over time, the higher interest rates will reduce inflation and that will likely revert the yield curve into a more normal shape. The current shape is the result of the Fed tightening very quickly. I also think that current event in banking will reduce lending, simply because banks are going to be more concerned about the liquidity buffer. When you look at bank balance sheet, the liquidity has been drained because deposits have been mostly flat and lending has continued to increase at healthy rate, probably caused by inflation. As we know , the current holdings of under water MBS and treasury also has sterilized part of the banks balance sheet, as selling them would cause losses denting regulatory capital and banks don’t want that.

-

iPhone 11 Updated to iOS 16 and Now Refuses to Charge

Spekulatius replied to DooDiligence's topic in General Discussion

Charging has nothing to do with the operating system update. Since you swapped the cable, it’s probably an issue with your phone plug having problems to make the electrical contact. I would bring it to the Apple Store. I have an iPhone XR on iOS 16 and my son has an 8+ that still works as well. -

Yes, I recall I looked at them when you mentioned the stock a while ago. having lived near the Bay area, I was somewhat familiar with them and I think my inlaws have an account with them. They have pretty good metrics profitability (mid thirties efficiency ratio) due to having somewhat of a moat with Chinese people preferring to bank with them. it was simply something that I knew and have checked for pitfalls when the hell broke loose. Same thing with USB where I added to my position. Given more time, i would possibly pick up some spicier stuff like $ZION but I simply did not have enough time to double check the FFIEC filings, 10-K's transcript to get confidence here. I'd rather play it safe then getting into some gotcha's because I venture into something that I haven't fully checked out.

-

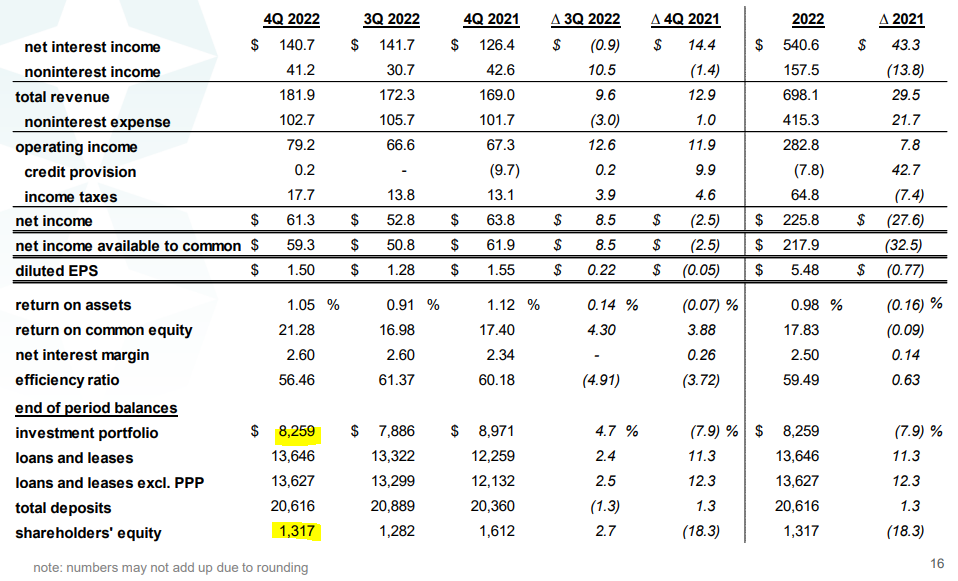

To me BOH looks pretty safe. They do have a large security portfolio as well - ~$8.3B with ~$1.3B in equity. this looks scary, but BOH has a very stable deposit base because there is very limited competition in Hawaii. I think they will be fine. They have traded at premium valuation because the lack of competition has enabled above average ROE with very low risk lending.

-

My ad of the day. It's getting ugly out (or in) there: