Spekulatius

-

Posts

19,032 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

The world is coming to an end - no more pad Thais for $30 or 2” fingernails for who knows how much. https://www.wsj.com/economy/consumers/women-spending-recession-economy-e492cc1e?mod=economy_feat3_consumers_pos1

-

The rare earth mineral ban was in place for a couple of days now. The market has ignored it so far, imo wrongly so. In a few month, we are going to have major shortages in many high tech goods, if this export controls are not reversed.

-

If you yourself in the shoes of a businessman l you would think the world has gone nuts. There is no way to predict anything due to the haphazard way of the administration doing things. So the best option is to hunker down and if this is what is collectively is occurring we are looking at a severe recession. Take the recent U- turn roe semiconductor or electronics imports from China. While this fine for Dell and Apple for the time being, if you are an US business that actually assembles components and produces computers, you are absolutely getting screwed here . Why - because your components gets tariff taxed, while the finished goods from Dell or Apple get zero tariffs. No way you can stay in business like that.. This is just a microcosm what it happening all over the place. About 40% of the exports from China are components that got used for finished goods. These components gets tariff taxed tariff taxes by 145% now. Some of those compete with competitors from other countries which may get lower tariffs. Even if not, exporting these out from the US now is pretty much impossible if the bill of material contains significant amount of good from China. I think it’s preset clear that the Trump administration went into this tariff & trade war without much thinking and preparation and now just makes up more stuff partly to reduce the damage from prior decisions. Seems like “Art of the deal” versus “Art of War”. I have read both and I have a strong opinion which one is better. I think it’s possible that Xi Jinping baited Trump into raising the tariffs so high with counter tariffs that the outcome is ridiculous and very damaging. The next few month will be very interesting. Put your life jacket on, or get a parachute if flying and make sure you get through the bumpy ride with little damage or even benefit from the U-turns and foibles that I think going to unfold. Perhaps we get a de- escalation and Xi Jinping and Trump become best buddies. I don’t think that’s too likely though because a decoupling that we have seen is very hard to reverse. Same with Europe in terms of security.

-

I would trust neither right now as an independent country. The long term depends on if the USA remains a Republic. The chance that the USA is not a Republic any more a decade from now is higher than it has been since the civil war. Right now, I think there is a risk that we go down an Imperialistic path which seems to be the MAGA vision. China is already imperialist country with a thin veil. No good choices. Welcome to the multipolar world. US hegemony for sure has ended regardless what is happening next.

-

If Monday rips, it will be a great opportunity to raise some cash and reduce risk in your portfolio, imo.

-

@TwoCitiesCapital well said.

-

Seem like you are ight. Thanks for the data. Anecdotally, prices at the pump have gone up here in the East coast since the trade war started despite crude oil going lower.

-

The Canadian oil right now has no other outlet though and reducing output it only feasible to a certain degree, so most of the 10% tariffs will be eaten by the Canadian producer in the short and medium term.

-

I think ~40% of Canada’s exports to the USA are still in the 25% bracket. auto, auto parts, Aluminum, steel, Lumber (lumber tariffs are even higher than 25% - 34%). I do wonder if negotiating with Trump makes sense at all . There is no decent deal to be had with Trump‘s maximalist demands. Trump also tends to rip up agreements anyways, even those he negotiated himself. The only thing that makes sense is stalling tactics . These 90 day will be interesting. I expect a lot of noise and very little tangible results, but we will see.

-

The EU still hadn’t a lot of trade with both China and the US. I don’t think they interested in any trade war. Same for literally any other nation. I still think the existing Tarifs are a grenade that has been thrown in a room that has not gone off yet. A lot of Chinese exports are components that go into existing products build in the US and elsewhere. Then there is the rare earth export control ( a de facto ban) that is going to have an impact in a few month when exiting stock is depleted. This will affect high tech manufacturing, RV production and many other things that are going to be hard to predict. My guess is that a severe recession ow is inevitable, at least for the manufacturing sector. I think the base case is that this trade conflict is toned down in the next few months but I think the US- China trade relationship will never be the same again.Both countries will decouple each other , sort of what Zeihan has predicted. Also note that this decoupling increases the risk of a military conflict down the road.

-

Buffett/Berkshire - general news

Spekulatius replied to fareastwarriors's topic in Berkshire Hathaway

I imaging this to be Warren Buffett raising cash: -

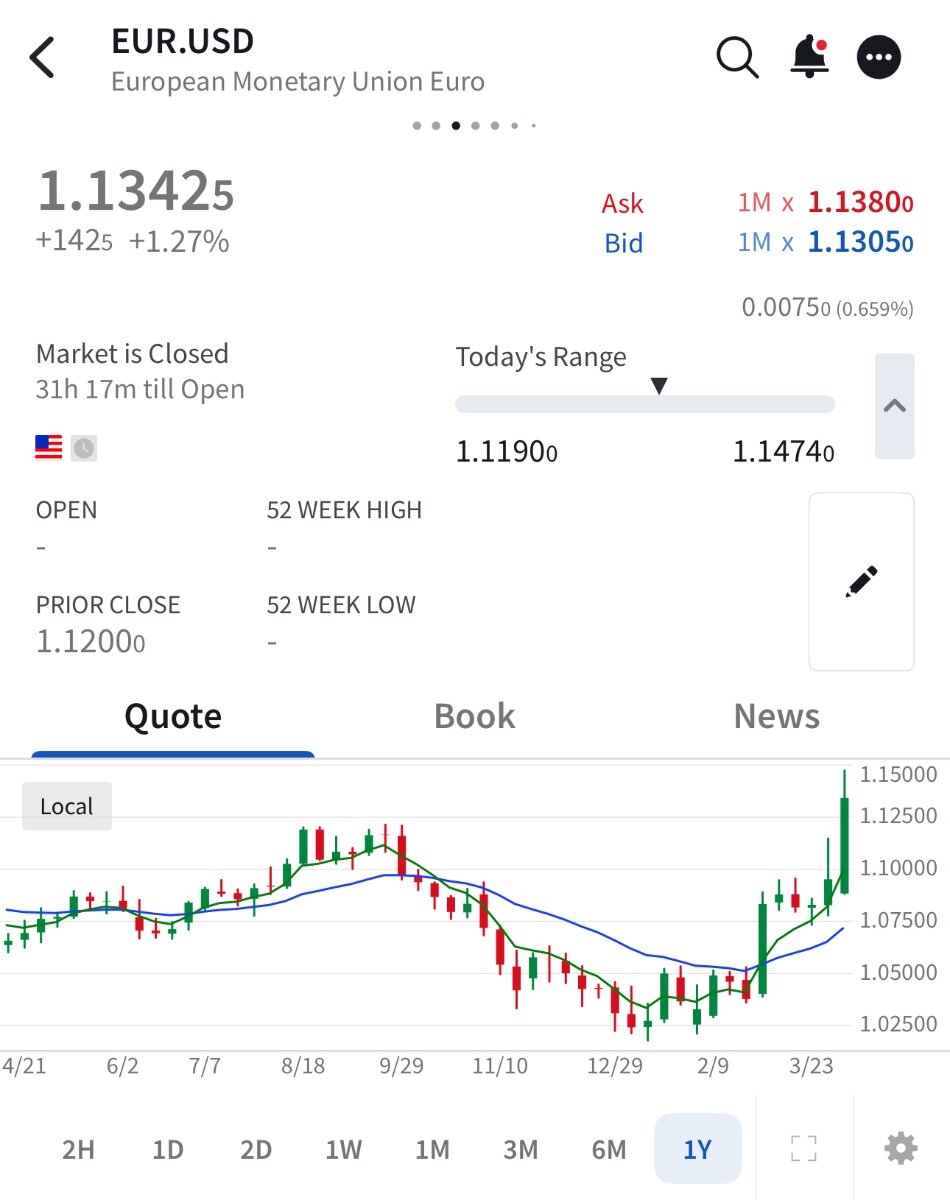

I think the bond trade breaks down in a stagflation scenario too and with spectaculary bad outcome. on another note and regarding the exchange rate - the Euro is having a spectacular run. You could say that part of the Mar de Largo accord plan (if this is the plan?) is working.

-

I Need a Laugh. Tell me a Joke. Keep em PC.

Spekulatius replied to doughishere's topic in General Discussion

Asshole, Asshole, Snob/pompous ass, Idiot. What do you say? -

I Need a Laugh. Tell me a Joke. Keep em PC.

Spekulatius replied to doughishere's topic in General Discussion

My grandma had an Ara bird who she kept on the balcony in summer. He would hurled insults at passerby’s, all of them in Berliner Slang. She had no clue for along time, her boyfriend thought those words to him, not herself. Stuff alike Arschloch, Arschloch, Fatzke, Dummkopf…If a passerby replied to him he would yell: Watt denn, Watt denn ? -

I Need a Laugh. Tell me a Joke. Keep em PC.

Spekulatius replied to doughishere's topic in General Discussion

-

However printing money means a rising deficit which is the opposite of what seems to be the goal hege. The Fed does not print money, the Treasury does. FWIW, I do think that despite all the austere talk, the deficit this year will be larger than last year, the recession we are looking at alone will make sure of that.

-

I think we are looking at a severe recession with no place to hide. The two largest economies basically have stopped trading with each other. If this continued a lot of supply chains and industries will melt down (retail, automobile, aerospace (aluminum tariffs , rare earth export controls ), consumer goods (Apple) and I expect semi and other tech sectors to be hard hit controls). Perhaps even industrial sectors in general will have issues ad many small components come from China like small elector motors for example which also often contain rare earth. The US government has a stockpiles (for strategic industries like defense) and companies have safety stock of material components but that will only last a few month and after that I expect shortages. I hope there will be some deal and currently the market is implicitly pricing it in , otherwise we would be much lower.

-

I think the smart thing is to buy when he says so and sell a little later for a quick flip and hopefully a nice gain. The stock market has become a Trump and Tariff Meme market basically.

-

I think ist more likely that institutions want to reduce interest rate and currency risks. Note that the Yen and the Euro are moving higher. I think it’s an indication of financial stress in the system. It would surprise me to see some hedge funds or maybe even bank blowing up somewhere.

-

He has done it before. It als happened with Russian stocks.

-

Some shuffling ahead of Project Greenland:

-

Only 15% of treasuries see held abroad though. I do think it’s a possibility as the trade war makes other sanctions more likely.

-

I continue mostly to add to existing positions (GOOGL, PAX, CX, REGN, ADM, NVO, ARE, 4368.T ,etc) on large down days. A new one I bought a couple of days is a new IPO in Australia - CCL (Cuscal). It does payment processing in Australia and has a high market share there. Their first report looked pretty good, imo. It’s sort of a busted IPO and looks pretty cheap on many metrics. I don’t know much about it, but the cheapness and the low Australian dollar make it an attractive bet.

-

It appears that there is now a delisting threat to Chinese equities due to deteriorating relationships with China. This happened before in late 2020 when some Chinese companies were delisted and you could not buy them any more on US exchanges: https://www.scmp.com/business/markets/article/3306203/delisting-us-listed-chinese-firms-boost-hong-kongs-status-fundraising-hub?module=top_story&pgtype=section I think the chances are better than 50% that this is going to happen.

-

WSJ article how Trump decided to defer some tariffs for a while: https://www.wsj.com/politics/policy/why-trump-blinked-on-tariffs-b588aea8?mod=WSJ_home_supertoppermiddle_pos_3